One-Close Construction

|

|

|

- Esther Shepherd

- 5 years ago

- Views:

Transcription

1 RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction transactions without having completed the course. PRIMARY RESIDENCE CONFORMING CONSTRUCTION/CONSTRUCTION-PERM Property Type 1-Unit PUD Site Condo Modular Maximum LTV 1 Maximum CLTV Minimum Credit Score 1 90% Subordinate 720 Financing Not 70% Allowed 700 Underwriting Engine & AUS Response DU Approve/Eligible 1. Loans with a loan to value of 70.01% and greater OR a credit score of less than 700 must be requalified at completion of construction. See below. PROGRAM SUMMARY Conforming one-time close six, nine or 12 month construction term program allowing for payment of interestonly during construction. Note to be modified upon completion of improvements to a fully amortized principal and interest payment. Soft costs (architectural, engineering and permit fees) may be financed, closing costs may not. Full third party builder contracts only. All loans close in the name of Flagstar Bank. PRODUCTS OFFERED Product Name Term Construction/Interest- Loan Term for Only Period Registration 30-Yr Conforming (12-mo Const) 30 years 12 months Yr Conforming (9-mo Const) 30 years 9 months Yr Conforming (6-mo Const) 30 years 6 months Yr Conforming (12-mo Const) 15 years 12 months Yr Conforming (9-mo Const) 15 years 9 months Yr Conforming (6-mo Const) 15 years 6 months 186 LOAN REGISTRATION Purpose type Two loan purpose types are available for use under specific circumstances based on the borrower s ownership status of the lot at the time of application. o Construction purpose type is used if the borrower is not the owner of record at the time of loan application o Construction Perm purpose type is used if the borrower is the owner of record, regardless of length of time owned or how title was acquired. Loan term selection per table above. Prior to selecting interest rate the Construction Worksheet must be completed. The worksheet can be accessed by clicking on Add Loan Purpose Info within the loan registration module. Year built should be entered as the year when construction is expected to be completed based on anticipated closing and loan term. Select Proposed in the building status field. All Loan Estimates will be prepared by Flagstar Disclosure Management. V. Product Descriptions 1 of 10 Document #5717

2 CONSTRUCTION TO PERM Construction to Perm loans are treated as a Rate & Term refinance. Complete construction worksheet (Add Loan Purpose Info) Go to the Real Estate Owned section. o Using drop down for indicator select SUBJECT OF LOAN o Using drop down for Disposition select RETAINED-WILL BECOME PRIMARY OR ADDITIONAL RESIDENCE o Enter the Estimated as completed Value in the Present Market value field. Note: the Amt of Mtgs Liens field currently shows the value of the land. This will be updated once the Liabilities Section has been completed. In the Liabilities screen o Enter the Builder s Price to Build plus Unpaid Balance of Lot from the Construction Worksheet in the Balance field. The Amt of Mtgs liens field will update on the REO screen. o Be sure the paid by close box is selected. Check Details of Transaction screen to verify that line d reflects the cost of construction + outstanding lot lien balance Select Complete Registration to go to the products screen. See EXHIBIT A for further detail. MAXIMUM LOAN AMOUNT Maximum: $424,100. Minimum: $50,000. ELIGIBLE PROPERTY TYPES 1-unit site-built homes. Planned unit development (PUD). Modular home (constructed in sections off-site, but when installed at the site takes on the characteristics of a site-built home). Site condominium (detached). Must be fee simple interest for land and dwelling. Rural Properties. INELIGIBLE PROPERTY TYPES Manufactured homes. 2-4 unit properties. Properties where construction has already begun. Lots in excess of 10 acres. Log homes. INELIGIBLE BORROWERS: Non-occupant co-borrowers. V. Product Descriptions 2 of 10 Document #5717

3 TEMPORARY BUYDOWNS Not allowed. MINIMUM CREDIT SCORES: Refer to eligibility grid above. QUALIFYING RATE: Note rate, fully amortizing over 30 or 15 years. QUALIFYING RATIOS Per DU. TAX AND INSURANCE ESCROW Escrows will be collected at time of closing for taxes and insurance. The underwriter may (or must in some circumstances) project the real estate taxes as follows: For Properties in California, property taxes may be calculated using 1.25% of the purchase price or the current tax rate as obtained from the local tax assessor s office. All other states the taxes may be calculated based on the current tax rate as obtained from the local tax assessor s office or the underwriter will use 1.5% of the purchase price. During construction, the borrower will make interest-only payments on the funds disbursed along with taxes and insurance. When the house is complete, the borrower s payment will be modified to principal, interest, taxes and insurance. Mortgage insurance will be activated and the premium included in the modified monthly payment. This process will not affect those loans for which an escrow waiver is obtained. Borrower must carry a builder s risk policy until the property is eligible for standard homeowner insurance policy. PRICING Refer to the Construction Price Indication Sheet for details. FEES CONSTRUCTION INTEREST RATE Add 0.75% to permanent interest rate CONSTRUCTION DRAW FEE Flagstar Bank works with Granite Loan Management, LLC for the purpose of managing builder/project review and the draw process for construction lending. All loans require a builder and project review/approval by Granite. The number of draws and the fees charged by Granite for their services will vary as follows: Loan Amount Flat Fee Number of Draws Included in Flat Fee Cost of Additional Draws Up to $200,000 $1,250 3 $230 $200,001 - $424,100 $1,600 5 $240 V. Product Descriptions 3 of 10 Document #5717

4 Loan Amount $424,101 High Cost Area Loan Limits Flat Fee Number of Draws Included in Flat Fee Cost of Additional Draws $2,500 7 $275 Total fees collected at closing are paid to Granite after close and any unused draw fees are not refundable. FINAL INSPECTION FEE The final construction inspection fee (usually by appraiser) should be disclosed as $ This fee will be held in escrow by Flagstar to cover the final inspection cost at the end of the construction phase. If the actual charge incurred by Flagstar is less than the amount collected, the difference will be refunded to the borrower within 30 days of conversion to the permanent phase. FINAL TITLE UPDATE FEE See Title Insurance section for discussion of title insurance requirements and obtaining a title fee quote. A final title update fee of $ will be held in escrow by Flagstar to cover the final title update cost at the end of the construction phase. If the actual charge incurred by Flagstar is less than the amount collected, the difference will be refunded to the borrower within 30 days of conversion to the permanent phase. CONSTRUCTION SURVEY FEE A construction survey fee will be required to be held in escrow by Flagstar to cover the cost of the survey. The recommended amount to collect is $750 and the fee will default to that amount. When the subject property is located in one of the following states the following fee must be collected: California $8,500 Minnesota $1,025 New Jersey $1,900 New York $1,900 Oregon $5,200 Texas $1,375 LOT SURVEY FEE A lot survey may also be required by the title company in certain states, which would require a separate fee not held by Flagstar (use the standard survey fee line for the lot survey and not the construction survey fee line). If a lot survey is required, the originator must ensure the lot survey fee is properly disclosed on the Loan Estimate using the standard Survey fee line. ADDITIONAL FEES FOR TEXAS LOANS Loans in Texas should take additional attorney fees into consideration when issuing initial disclosures and may include a doc prep fee and fee for the preparation of mechanics lien note. V. Product Descriptions 4 of 10 Document #5717

5 CONSTRUCTION GUIDES It is the responsibility of the loan officer to provide the borrower with the Construction Loan Guide within 3 days of application per TILA RESPA requirements. Executed borrower acknowledgement must be in the loan file at time of submission to underwriting. The construction guide and supporting documentation can be found under Construction Forms in the 3000 series of the Seller s Guide. Borrower and contractor must also be supplied with the appropriate State Statutory Form package and State Draw Requirement Letter. These can be found under Construction Forms in the 3000 series of the Seller s Guide. FILE SUBMISSION BUILDER/PROJECT PACKAGE Builder/project packages must be submitted to: Granite Loan Management, LLC Briarwood Ave., Suite 280 Centennial, CO Phone: (866) Fax: (800) projects@graniteloan.com CREDIT PACKAGE: Credit packages must be submitted to Underwriting through paperless loan submission and must include the executed Construction Guide Acknowledgement. APPRAISAL All appraisals must be ordered through Flagstar Loantrac from an approved Appraisal Management Company even if the customer has AIR Compliant status. All appraisals must be reviewed by the Flagstar Appraisal Review department, please allow extra time for this process. UNDERWRITING All loans must meet Fannie Mae underwriting criteria as set out in Flagstar Bank s current Residential Underwriting Guidelines if not addressed within this document. ALL loans must be underwritten by Flagstar. Project/builder will be reviewed by Granite Loan Management, LLC. Cost to construct must be documented by fully executed arms length third-party builder contract (or up to two contracts for modular). No manufactured homes. Fourth-party transactions are not eligible. No alternate credit history. Construction cannot have already started. The LTV ratio will be calculated as follows: o Construction purpose type (borrower not owner of record of lot): Divide loan amount by the lesser of the total acquisition cost (sum of the cost of construction plus the purchase price of the lot) or the as completed appraised value of the property (lot and improvements). V. Product Descriptions 5 of 10 Document #5717

6 o Construction to Perm purpose type (borrower is owner of record): Divide loan amount by the as completed appraised value of the property (lot and improvements). o All payments made by the borrower directly to builder, or purchases of materials outside of the builders contract, will not be considered in the total acquisition cost calculation. If the lot was acquired within 120 days of loan application, acquisition funds must be documented. Sweat equity will not be accepted. $2,000 or 2% cash back to borrower is not eligible on this program. Escrows will be collected at time of closing for taxes and insurance. The amount collected will be based on the current assessed value of the vacant land and the current tax rate. During construction, the borrower will make interest-only payments on the funds disbursed along with taxes and insurance. When the house is complete, the borrower s payment will be modified to principal, interest, taxes and insurance. This process will not affect those loans for which an escrow waiver is obtained. Interest Reserve Accounts to pay interest during the Construction Period are not eligible. Borrower must make an interest-only payment during the construction period. Credit documents must be dated within 120 days of the closing date. Appraisal must be dated within 120 days of the closing date. DU FINDINGS/RISK ELIGIBILITY: FOR CONSTRUCTION TO PERM DU response must reflect Approve Eligible. Approve/Ineligible findings are acceptable only if the reason for ineligibility is for detached condominium as a property type. See Exhibit A for REO entries. Findings must reflect o This loan casefile has been underwritten as a limited cash-out refinance. o For single-closing construction-to-permanent financing, special feature code 151 must be provided at delivery. SPECIAL FEATURE CODES Loan must include Special Feature Code 151. If the borrower purchased the property prior to the closing of the construction loan transaction, Special Feature Code 007 must be added by the underwriter. Properties secured by a site condo must include SFC 917. Loans with an LTV of 70.01% must be requalified at completion of construction. RESERVES The following tables provide minimum reserve requirements. Reserves (PITIA) in Months Borrower does not own an owner occupied property or current residence will not be retained at the time of the loan closing. Per DU plus 6 months PITIA on the subject property Current residence will be retained at the time of closing. Per DU plus 6 months PITIA on the subject property and V. Product Descriptions 6 of 10 Document #5717

7 Reserves (PITIA) in Months Current residence will be retained at the time of closing. If 30% equity or more on the previous principal residence: 2 months PITIA on the subject property, and 2 months PITIA on previous primary: or If less than 30% equity on previous principal residence: 6 months on subject property, and 6 months on previous principal residence MORTGAGE INSURANCE Mortgage insurance commitment must be issued prior to closing of loan and be for a minimum of 12 months. Mortgage insurance providers may have additional restrictions not listed within the document. Due to rapid changes within the industry, please refer to each mortgage insurance company s website for complete details. Refer to MI Company Parameter Matrix to assist you with keeping up with these changes. However, this document is to be used as a reference only. STANDARD MORTGAGE INSURANCE GUIDELINES All loans above 80% LTV require mortgage insurance coverage according to the following guidelines. LTV 30-Year 15-Year % 25% 12% % 12% 6% Mortgage insurance is eligible to be obtained from MGIC or Genworth and must be activated at completion of construction and prior to shipping. Mortgage insurance effective date must be entered to match the expected end of the construction term to ensure proper disclosures and servicing boarding. NEW YORK PROPERTIES See Conventional Underwriting Guidelines. TITLE INSURANCE Long-form title insurance must be obtained for all construction loans; short-form title policies are not acceptable. Title updates are required at the time of each draw. Ensure when you request your title quote that the title company understands the quote is for a construction loan. Long-form title is required, and the title quote must include the cost of endorsements required with each draw. For properties located in Illinois, all title commitments, updates and final policies must be provided by: First American Title Fidelity National Title Chicago Title Attorneys Title Guaranty V. Product Descriptions 7 of 10 Document #5717

8 For a smoother draw process with your construction loans you may wish to use one of these companies in all eligible states. EXTENSIONS OF CONSTRUCTION PERIOD Extensions may be granted, pursuant to a change order, if Lender reasonably believes work will not be done by the scheduled completion date. Maximum extension period is six whole months (extensions will not be granted for partial months). Flagstar Bank will charge a Construction Extension Fee of $700 that allows for an extension of up to two months if the construction is not completed by the pre-determined completion date. STATE ELIGIBILITY State/Territory Alaska Hawaii Virgin Islands Restriction Not eligible Not eligible Not eligible Originators may only submit loans in the state within which they reside. No out-of-state originations. An exception will be made for loans located in bordering states if the originator is located near the state border. CLOSING DOCUMENTATION Closing Disclosures and closing documents will be prepared by Closing Services. Interim interest is not collected at closing. Loans closing within the first 7 days of the month cannot be closed with an interest credit. Maximum draw request from builder at closing is capped at 10% or $50,000 of the total cost to build, whichever is less. No further draws can occur until closing package has been received and post-closed by Flagstar Bank (usually 10 business days). V. Product Descriptions 8 of 10 Document #5717

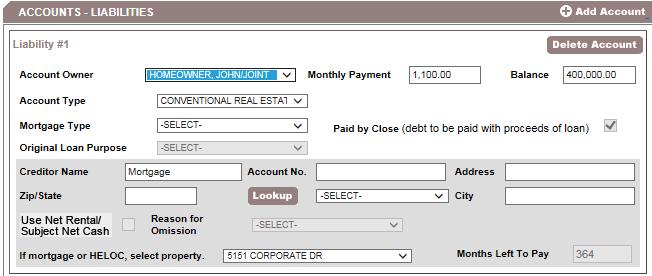

9 EXHIBIT A When registering a Construction to Perm loan, after completing the Loan Purpose screen, some of the information must be manually entered into the REO and LIABILITIES screens. The Estimated As completed Appraisal is the present market value on the REO screen. The Unpaid Balance of Lot plus Builder s Price to Build from the Construction worksheet is entered in the Liabilities balance field and marked as Paid by Close. V. Product Descriptions 9 of 10 Document #5717

10 V. Product Descriptions 10 of 10 Document #5717

ONE TIME CLOSE RENOVATION TO PERM OPTION III

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

VERY IMPORTANT THE LOAN WILL BE RUN THROUGH DU PRIOR TO START OF CONSTRUCTION AND MUST REFLECT APPROVE ELIGIBLE.

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE. Reserves

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Property Type Max. LTV Max. CLTV

Click here for PDF version Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Loan Credit Score 3 Program 1- to 2-unit 95% 1 n/a $300,000 28/36 2 months 660 Standard

Click here for PDF version Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Loan Credit Score 3 Program 1- to 2-unit 95% 1 n/a $300,000 28/36 2 months 660 Standard

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT Conventional Conforming fixed rate mortgage with High- Balance loan limits DU Version 10.2 Servicing retained 10 to 30 year

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT Conventional Conforming fixed rate mortgage with High- Balance loan limits DU Version 10.2 Servicing retained 10 to 30 year

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

Fannie Mae has specific requirements for multiple financed properties:

Fannie Mae has specific requirements for multiple financed properties: If subject loan is owner occupied, Fannie Mae has no limit on number of properties financed If subject is second home or investment

Fannie Mae has specific requirements for multiple financed properties: If subject loan is owner occupied, Fannie Mae has no limit on number of properties financed If subject is second home or investment

ditech BUSINESS LENDING CONFORMING DITECH-PAID LPMI PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate with lender paid mortgage insurance DU Version 10.2 Servicing retained 10 to 30-year term in annual increments Manufactured Homes -30 year term

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate with lender paid mortgage insurance DU Version 10.2 Servicing retained 10 to 30-year term in annual increments Manufactured Homes -30 year term

ditech BUSINESS LENDING CONFORMING TEXAS HOME EQUITY PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments

Section Agency Loan Programs

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

CONFORMING UNDERWRTING GUIDELINES DUREFIPLUS PROGRAM - WHOLESALE

Table of Contents APPRAISAL & PROPERTY INFORMATION.... 2 Appraisal Requirements... 2 LTVs > 95%..... 3 Property Inspection Waiver (Property Field work Waiver Requirements).... 3 ELIGIBLE PROPERTIES...

Table of Contents APPRAISAL & PROPERTY INFORMATION.... 2 Appraisal Requirements... 2 LTVs > 95%..... 3 Property Inspection Waiver (Property Field work Waiver Requirements).... 3 ELIGIBLE PROPERTIES...

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

DU Refi Plus. Eligibility Matrix Loan Amount & LTV Limitations

This matrix is intended as an aid to assist in determining if a property/loan qualifies for the DU Refi Plus program. It is not intended as a replacement for the full DU Refi Plus guidelines. Users are

This matrix is intended as an aid to assist in determining if a property/loan qualifies for the DU Refi Plus program. It is not intended as a replacement for the full DU Refi Plus guidelines. Users are

Conforming Balance Primary Residence

Texas Cash-Out Program Conforming Balance Summary Product Types 30yr & 15yr Fixed Only For Conforming Loan Amounts, view State/County limits: https://www.fanniemae.com/singlefamily/loan-limits Conforming

Texas Cash-Out Program Conforming Balance Summary Product Types 30yr & 15yr Fixed Only For Conforming Loan Amounts, view State/County limits: https://www.fanniemae.com/singlefamily/loan-limits Conforming

Du Refi Plus Guidelines

Du Refi Plus Guidelines Units Contiguous States, DC Alaska, Hawaii Max Loan Amount Conforming 1 Unit 2 Unit 3 Unit 4 Unit $417,000 $533,850 $645,300 $801,950 $625,500 $800,775 $967,950 $1,202,925 Units

Du Refi Plus Guidelines Units Contiguous States, DC Alaska, Hawaii Max Loan Amount Conforming 1 Unit 2 Unit 3 Unit 4 Unit $417,000 $533,850 $645,300 $801,950 $625,500 $800,775 $967,950 $1,202,925 Units

HIGH BALANCE CONFORMING (DU) See last page for 7-10 Financed Properties OK on DU 100, 300, 500, & 800 Series

See last page for 7-10 Financed Properties OK on DU 100, 300, 500, & 800 Series") HIGH BALANCE CONFORMING (DU) See last page for 7-10 Financed Properties OK on DU 100, 300, 500, & 800 Series 100 Series does not allow s Product Description Conventional Conforming Fixed and High Balance

HIGH BALANCE CONFORMING (DU) See last page for 7-10 Financed Properties OK on DU 100, 300, 500, & 800 Series 100 Series does not allow s Product Description Conventional Conforming Fixed and High Balance

High-Cost Area (High Balance) Loan Amounts

Loan Amounts") Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

FNMA Conforming Mortgage

Topic Program Description Products AUS method Eligible States Maximum Loan Amounts Agency Conforming Loan Limits Product Guideline This is base Fannie Mae mortgage parameters for primary, second and investor

Topic Program Description Products AUS method Eligible States Maximum Loan Amounts Agency Conforming Loan Limits Product Guideline This is base Fannie Mae mortgage parameters for primary, second and investor

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Max LTV/CLTV FICO 1 Unit 95/95% /90% 620 Purchase 85/85% 620 Refi 75/75% 2 Units Purchase & Refi- 85/85% 620 N/A N/A 75/75% 620

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Stockton Mortgage Funding HomeReady Fixed Rate Mortgage Product

1. PRODUCT DESCRIPTION Conventional C onforming fixed rate m ortgage DU Version 9.3 10, 15, 20, or 30 year terms for product 30 year term only for product Fully amortizing Qualified Mortgage (QM) Safe

1. PRODUCT DESCRIPTION Conventional C onforming fixed rate m ortgage DU Version 9.3 10, 15, 20, or 30 year terms for product 30 year term only for product Fully amortizing Qualified Mortgage (QM) Safe

Conforming Loans as of October 24, 2007

Conforming Loans Fixed Rate, Fixed Period ARMs, and Standard ARMs (Full/Alt Documentation) (Standard Amortization) Cash Out Refinances Occupancy 1 1 1 1 1 1 1-Unit Properties 95/95% 95/95% 85/85% 2-Unit

Conforming Loans Fixed Rate, Fixed Period ARMs, and Standard ARMs (Full/Alt Documentation) (Standard Amortization) Cash Out Refinances Occupancy 1 1 1 1 1 1 1-Unit Properties 95/95% 95/95% 85/85% 2-Unit

Correspondent Lending FHA Fixed Rate & ARM Product Profile

Government Occupancy Correspondent Lending ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM High Balance 15 & 30 YR Fixed Rates Primary Residence Purchase Property

Government Occupancy Correspondent Lending ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM High Balance 15 & 30 YR Fixed Rates Primary Residence Purchase Property

Correspondent Lending FHA Fixed Rate

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Wholesale Lending DU Refi Plus 12/27/2013

Program Code Loan Description Program Type Loan_Type Program Code DU30-105 DU REFI 30 YR FIXED LTV 0-105 FIXED CONV DU20-105 DU REFI 20 YR FIXED LTV 0-105 FIXED CONV DU15-105 DU REFI 15 YR FIXED LTV 0-105

Program Code Loan Description Program Type Loan_Type Program Code DU30-105 DU REFI 30 YR FIXED LTV 0-105 FIXED CONV DU20-105 DU REFI 20 YR FIXED LTV 0-105 FIXED CONV DU15-105 DU REFI 15 YR FIXED LTV 0-105

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

Fannie Mae DU Refi Plus ; Conforming High Balance Changes and New Appraisal Pricing

MSI Mortgage Services III, LLC Wholesale Partner Announcement At MSI Your Interest Is Our Priority! A Subsidiary of First State Bank Member FDIC Issue Date 5/07/09 Effective Date As Noted WPA 2009-020

MSI Mortgage Services III, LLC Wholesale Partner Announcement At MSI Your Interest Is Our Priority! A Subsidiary of First State Bank Member FDIC Issue Date 5/07/09 Effective Date As Noted WPA 2009-020

HUNTINGTON PORTFOLIO Fixed and Adjustable Rate Conforming and Non-Conforming Products INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs

PRODUCTS: 15 yr Fixed Rate INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs CODE: Conforming & Non-Conforming 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 10/01/2016 PRODUCT CRITERIA 1) PRODUCT

PRODUCTS: 15 yr Fixed Rate INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs CODE: Conforming & Non-Conforming 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 10/01/2016 PRODUCT CRITERIA 1) PRODUCT

TABLE OF CONTENTS. PRODUCT DESCRIPTION Page # Product Description 3

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Property Types: Eligible & Ineligible 3 imum Loan Amounts 3 Assumability 3 Buydowns 3 Prepayment Penalty 3 Cash

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Property Types: Eligible & Ineligible 3 imum Loan Amounts 3 Assumability 3 Buydowns 3 Prepayment Penalty 3 Cash

Multiple Financed Properties Program Fannie Mae/Freddie Mac. Table of Contents

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

PennyMac Correspondent Group DU Refi Plus The loan must have an application date on or before December 31, 2018

PennyMac Correspondent Group DU Refi Plus 01.18.18 The loan must have an application date on or before December 31, 2018 Overlays to Fannie Mae are underlined Mortgage Product FNMA DU Refi Plus HARP 2.0

PennyMac Correspondent Group DU Refi Plus 01.18.18 The loan must have an application date on or before December 31, 2018 Overlays to Fannie Mae are underlined Mortgage Product FNMA DU Refi Plus HARP 2.0

ditech BUSINESS LENDING HOMEREADY LPMI FIXED RATE MORTGAGE PRODUCT

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING HOMEREADY LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10, 15, 20, or 30 year terms Manufactured

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING HOMEREADY LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10, 15, 20, or 30 year terms Manufactured

Texas Cash-out Program Guide Fixed Rate

Texas Cash-out Program Guide Fixed Rate Wholesale Lending July 20, 2015 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay and Qualified Mortgage... 2 Program Parameters...

Texas Cash-out Program Guide Fixed Rate Wholesale Lending July 20, 2015 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay and Qualified Mortgage... 2 Program Parameters...

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE DITECH-PAID LPMI FIXED RATE AND ARM PRODUCT

1. PRODUCT DESCRIPTI ON Conventional Conforming fixed rate w ith lender paid mortgage insurance Servicing retained 10 to 30-year term in annual increments Manufactured Homes -30 year term only Fully amortizing

1. PRODUCT DESCRIPTI ON Conventional Conforming fixed rate w ith lender paid mortgage insurance Servicing retained 10 to 30-year term in annual increments Manufactured Homes -30 year term only Fully amortizing

V40 15 Yr Fannie/Freddie High-Balance Fixed X49 20 Yr Super Conforming Freddie Mac Eligible

1. Loan Term Fixed Rate: 10 to 30-year terms in annual increments ARM: 30-year term 2. Fixed Rate Product Codes 3. ARM Product Codes W90 10 Yr Fannie/Freddie Fixed W91 10 Yr Freddie Mac Eligible Fixed

1. Loan Term Fixed Rate: 10 to 30-year terms in annual increments ARM: 30-year term 2. Fixed Rate Product Codes 3. ARM Product Codes W90 10 Yr Fannie/Freddie Fixed W91 10 Yr Freddie Mac Eligible Fixed

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

Fannie Mae High Balance Matrix

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

PRODUCT GUIDELINES USBHM CONVENTIONAL NON-CONFORMING FIXED 30 YEAR YEAR YEAR 3777 Core Portfolio Revised 01/02/18

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

WHOLESALE Non-Agency Jumbo Fixed and ARM Fixed: T Year fixed rate, T Year fixed rate ARM: A500-5/1 ARM. A522-7/1 ARM and A527-10/1 ARM

Transaction Type Units Min-Maximum Loan Amt. Non-Agency Fixed and ARM Jumbo Matrix 1 WHOLESALE BUSINESS CHANNEL ONLY Maximum Min. LTV 3 FICO Min.# Mos. Verified PITIA Maximum DTI Maximum Cash Out 4 1 Primary

Transaction Type Units Min-Maximum Loan Amt. Non-Agency Fixed and ARM Jumbo Matrix 1 WHOLESALE BUSINESS CHANNEL ONLY Maximum Min. LTV 3 FICO Min.# Mos. Verified PITIA Maximum DTI Maximum Cash Out 4 1 Primary

Section Jumbo Solution Second Mortgage

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

Fixed-rate, fully amortizing with level payments for life of loan. This program is for conventional conforming loan amounts.

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

PRODUCT MATRICES. For Information on any of our products, please contact:

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

SONYMA Conventional Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Correspondent Guidelines. Loan Program: 7/1 LIBOR ARM 5/2/5 Dollar Bank (1700) LTV Limits:

LTV Limits:") Loan Program: 7/1 LIBOR ARM 5/2/5 Dollar Bank (1700) LTV Limits: Occupancy Primary Residence Investment & Non-Owner PURCHASE AND LIMITED CASH-OUT REFINANCE MORTGAGES Property Type 1 Unit Max LTV Max TLTV

Loan Program: 7/1 LIBOR ARM 5/2/5 Dollar Bank (1700) LTV Limits: Occupancy Primary Residence Investment & Non-Owner PURCHASE AND LIMITED CASH-OUT REFINANCE MORTGAGES Property Type 1 Unit Max LTV Max TLTV

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions Fixed Rate

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions Fixed Rate

ELIGIBILITY MATRIX Table of Contents

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive loan-to-value (LTV) ratios, combined LTV ratios (CLTV), and home equity CLTV ratios (HCLTV) and minimum credit scores (if applicable)

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive loan-to-value (LTV) ratios, combined LTV ratios (CLTV), and home equity CLTV ratios (HCLTV) and minimum credit scores (if applicable)

Wholesale Overlay Matrix

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

CONFORMING FIXED LENDER PAID MORTGAGE INSURANCE PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A conforming conventional loan with a fixed interest rate for the term of the loan. Loan Term Program Category 30-year Conf Fixed 30 15-year Conf Fixed 15 Transaction

Program Summary Loan Term & Program Category A conforming conventional loan with a fixed interest rate for the term of the loan. Loan Term Program Category 30-year Conf Fixed 30 15-year Conf Fixed 15 Transaction

Conforming and High Balance Guideline Fannie Mae

Revision: December 18, 2017 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied Second

Revision: December 18, 2017 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied Second

ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. PRODUCT CODES ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. PRODUCT CODES ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1

CONFORMING LIBOR ARMS PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

APMC DU REFI PLUS MATRIX

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. FINAL FUNDING DATE Conventional Conforming Fixed Rate DU Version 9.1 LTV

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. FINAL FUNDING DATE Conventional Conforming Fixed Rate DU Version 9.1 LTV

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile Overlays to Fannie Mae are underlined

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

FREDDIE MAC FANNIE MAE. 1. Loan Term Fixed Rate: 10 to 30-year terms in annual increments ARM: 30-year term 2. Fixed Rate Product Codes

1. Loan Term Fixed Rate: 10 to 30-year terms in annual increments : 30-year term 2. Fixed Rate Product Codes 3. Product Codes FREDDIE MAC X35 10 Yr Fannie/Freddie Fixed Texas Home FF4 10 Yr Freddie Mac

1. Loan Term Fixed Rate: 10 to 30-year terms in annual increments : 30-year term 2. Fixed Rate Product Codes 3. Product Codes FREDDIE MAC X35 10 Yr Fannie/Freddie Fixed Texas Home FF4 10 Yr Freddie Mac

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE SUPER CONFORMING FIXED RATE AND ARM PRODUCT

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE SUPER CONFORMING FIXED RATE AND ARM PRODUCT Conventional Conforming fixed rate mortgage w ith Super Conforming/High- Balance loan limits

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE SUPER CONFORMING FIXED RATE AND ARM PRODUCT Conventional Conforming fixed rate mortgage w ith Super Conforming/High- Balance loan limits

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Guidelines Correspondent

Loan Program: 30-Year Fixed Fannie Mae (630) 20-Year Fixed Fannie Mae (620) 15-Year Fixed Fannie Mae (615) LTV Limits: ❶ ❷ ❸ Occupancy Investment & Non-Owner Type❷ 1 Unit PURCHASE MORTGAGES Max LTV Max

Loan Program: 30-Year Fixed Fannie Mae (630) 20-Year Fixed Fannie Mae (620) 15-Year Fixed Fannie Mae (615) LTV Limits: ❶ ❷ ❸ Occupancy Investment & Non-Owner Type❷ 1 Unit PURCHASE MORTGAGES Max LTV Max

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

FNMA Jumbo Conforming Fixed & ARM (HIGH BALANCE LOANS) T300J 30 Year Fixed & T301J 15 Year Fixed A341J 5/1 ARM & A342J 7/1 ARM 30 Year Adjustable

T300J 30 Year Fixed & T301J 15 Year Fixed A341J 5/1 ARM & A342J 7/1 ARM 30 Year Adjustable") High Balance loan limits (including 2013) are posted on E Fannie Mae website. Link: https://www.efanniemae.com/sf/refmaterials/loanlimits/xls/loanlimref.xls The following link can also be used for specific

High Balance loan limits (including 2013) are posted on E Fannie Mae website. Link: https://www.efanniemae.com/sf/refmaterials/loanlimits/xls/loanlimref.xls The following link can also be used for specific

Section DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

HOMESTYLE ENERGY MORTGAGES & PROPERTY ASSESSED CLEAN ENERGY LOANS (FANNIE MAE ONLY)

") OVERVIEW HOMESTYLE ENERGY MORTGAGES There are a number of HomeStyle Energy financing options available to a borrower who wishes to improve the energy and/or water efficiency of an existing property and

OVERVIEW HOMESTYLE ENERGY MORTGAGES There are a number of HomeStyle Energy financing options available to a borrower who wishes to improve the energy and/or water efficiency of an existing property and

FRESH START. Max 85% LTV with no MI No seasoning on derogatory events No mortgage/rental payment history required Low Minimum FICO

Program Highlights FRESH START Max 85% LTV with no MI No seasoning on derogatory events No mortgage/rental payment history required Low Minimum FICO Fresh Start ARM and Fixed PURCHASE AND RATE TERM REFINANCE

Program Highlights FRESH START Max 85% LTV with no MI No seasoning on derogatory events No mortgage/rental payment history required Low Minimum FICO Fresh Start ARM and Fixed PURCHASE AND RATE TERM REFINANCE

ditech BUSINESS LENDING FHA PURCHASE PRODUCT

1. PRODUCT DESCRIPTION FHA Fixed Rate Mortgage for Purchase Transactions FHA three year adjustable rate mortgage for Purchase Transactions 5 to 30 year term in annual increments 30 year term Fully amortizing

1. PRODUCT DESCRIPTION FHA Fixed Rate Mortgage for Purchase Transactions FHA three year adjustable rate mortgage for Purchase Transactions 5 to 30 year term in annual increments 30 year term Fully amortizing

Maximum LTV/CLTV 3 /HCLTV. Number of Units. Minimum Credit Score 4. Transaction Type 1,2. Principal Residence

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive loan-to-value (LTV) ratios, combined LTV ratios (CLTV), and home equity CLTV ratios (HCLTV) and minimum credit scores (if applicable)

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive loan-to-value (LTV) ratios, combined LTV ratios (CLTV), and home equity CLTV ratios (HCLTV) and minimum credit scores (if applicable)

Jumbo Non-Conforming Products (Series-49)

") Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Fixed Rate = Note Rate 5/1 ARM = start rate plus 2% 7/1 and 10/1 ARM = The greater of the start rate or the fully indexed rate Debt Ratio

Product Description (LP) Conventional Conforming Fixed and ARM High Balance (LP) Program Numbers 30 = 15 yr fixed 31 = 30 yr fixed ARMs are not available for all Series Numbers 32 = 5/1 ARM 33 = 7/1 ARM

Product Description (LP) Conventional Conforming Fixed and ARM High Balance (LP) Program Numbers 30 = 15 yr fixed 31 = 30 yr fixed ARMs are not available for all Series Numbers 32 = 5/1 ARM 33 = 7/1 ARM

Core Seconds S Year Fixed S Year Fixed

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Underwriting Methods 3 Documentation Requirements 3 Transaction Types 3 Eligible Property Types, Ineligible Property

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Underwriting Methods 3 Documentation Requirements 3 Transaction Types 3 Eligible Property Types, Ineligible Property

Conventional Loan Program - Quick Reference Guide

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

JUMBO A PROGRAM GUIDE

TABLE OF CONTENTS 1 OVERVIEW... 3 2 UNDERWRITING CRITERIA... 3 3 PRODUCT ELIGIBILITY... 4 3.1 AVAILABLE PRODUCTS... 4 3.2 ADJUSTABLE RATE CRITERIA... 4 4 PRODUCT MATRIX... 5 4.1 GEOGRAPHY... 5 4.2 MINIMUM

TABLE OF CONTENTS 1 OVERVIEW... 3 2 UNDERWRITING CRITERIA... 3 3 PRODUCT ELIGIBILITY... 4 3.1 AVAILABLE PRODUCTS... 4 3.2 ADJUSTABLE RATE CRITERIA... 4 4 PRODUCT MATRIX... 5 4.1 GEOGRAPHY... 5 4.2 MINIMUM

Announcement 09-08R June 8, Temporary High-Cost Area Loan Limits and Revised Eligibility Requirements for High-Balance Mortgage Loans

Announcement 09-08R June 8, 2009 Amends these Guides: Selling Temporary High-Cost Area Loan Limits and Revised Eligibility Requirements for High-Balance Mortgage Loans Introduction This Announcement (09-08R)

Announcement 09-08R June 8, 2009 Amends these Guides: Selling Temporary High-Cost Area Loan Limits and Revised Eligibility Requirements for High-Balance Mortgage Loans Introduction This Announcement (09-08R)

SUPER JUMBO PRIMARY RESIDENCE. Min FICO. SFR, Condo* Townhouse PUD, 2 Units. Min FICO. SFR, Condo, Townhouse, PUD, 2 Units SECOND HOMES.

SJ Series SUPER JUMBO PRIMARY RESIDENCE Occupancy Loan Purpose Property Type Min FICO LTV/CLTV Max Loan Amt Primary Residence Purchase & Rate/Term Refinance SFR, Condo* PUD, 2 Units 720 80/80 $2,000,000

SJ Series SUPER JUMBO PRIMARY RESIDENCE Occupancy Loan Purpose Property Type Min FICO LTV/CLTV Max Loan Amt Primary Residence Purchase & Rate/Term Refinance SFR, Condo* PUD, 2 Units 720 80/80 $2,000,000

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

CONFORMING PRODUCTS: Eligible on Mammoth, Acadia, Cascades and Yosemite. ARM Rate ( Purchase & Rate/Term Refinances)-Fannie Mae DU

-Fannie Mae DU") CONFORMING PRODUCTS: Eligible on Mammoth, Acadia, Cascades and Yosemite Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Occupancy Owner Occupied Second Home Investment Property Property Type

CONFORMING PRODUCTS: Eligible on Mammoth, Acadia, Cascades and Yosemite Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Occupancy Owner Occupied Second Home Investment Property Property Type

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

ditech BUSINESS LENDING FREDDIE MAC HOME POSSIBLE LPMI FIXED RATE MORTGAGE PRODUCT

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING FREDDIE MAC HOME POSSIBLE LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage Servicing retained 10-30 year term in annual increments

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING FREDDIE MAC HOME POSSIBLE LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage Servicing retained 10-30 year term in annual increments

ditech BUSINESS LENDING VA REFINANCE PRODUCTS

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in annual increments Fully amortizing Servicing retained Qualified Mortgage (QM) Safe

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in annual increments Fully amortizing Servicing retained Qualified Mortgage (QM) Safe

HomeReady Conforming Fixed Program Summary

HomeReady Conforming Fixed Program Summary HomeReady Matrix with Mortgage Insurance Guideline Overlays: PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO/Score LTV/CLTV/HCLTV Primary Residence 1 620

HomeReady Conforming Fixed Program Summary HomeReady Matrix with Mortgage Insurance Guideline Overlays: PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO/Score LTV/CLTV/HCLTV Primary Residence 1 620

ditech BUSINESS LENDING VA REFINANCE PRODUCTS

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in annual increments Fully amortizing Servicing retained Qualified Mortgage (QM) Safe

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in annual increments Fully amortizing Servicing retained Qualified Mortgage (QM) Safe

REO; Matrices; Multiple Properties and Fannie Mae PIW

REO; Matrices; Multiple Properties and Fannie Mae PIW Purpose This announcement includes the following topics: REO- Exceptions for Fannie/Freddie held properties. Updated Matrices HomePath and Conforming

REO; Matrices; Multiple Properties and Fannie Mae PIW Purpose This announcement includes the following topics: REO- Exceptions for Fannie/Freddie held properties. Updated Matrices HomePath and Conforming

ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s Products 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s DU Approve/Eligible

Agency ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s Products 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s DU Approve/Eligible

ELIGIBILITY MATRIX. Table of Contents. Standard Eligibility Requirements - Desktop Underwriter Page 2

The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix also includes credit

The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix also includes credit

PREMIER JUMBO PROGRAM GUIDE

\ PREMIER JUMBO PROGRAM GUIDE This document is provided for approved loan sellers only and may not be copied, distributed or disclosed to any other party. All terms herein are subject to change by FundLoans

\ PREMIER JUMBO PROGRAM GUIDE This document is provided for approved loan sellers only and may not be copied, distributed or disclosed to any other party. All terms herein are subject to change by FundLoans

Mortgage Insurance Help

Mortgage Insurance Help Address Line 1 Address Line 2 All Other Monthly Payments Amortization Term Amortization Type Application Number Appraisal Value Borrower's First Name Borrower's Last Name Borrower's

Mortgage Insurance Help Address Line 1 Address Line 2 All Other Monthly Payments Amortization Term Amortization Type Application Number Appraisal Value Borrower's First Name Borrower's Last Name Borrower's

FHLMC PROGRAM LINEUP`

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

FAQs June 20, Product. Submission. Financed MI (Single Premium) SplitEdge. ExpressTrack SM. Refer with Caution, Caution

SplitEdge. ExpressTrack SM. Refer with Caution, Caution") s June 20, 2016 The answers contained within are specific to loan files reviewed for eligibility under Radian s standard published guidelines. A separate is available for loan files which qualify under

s June 20, 2016 The answers contained within are specific to loan files reviewed for eligibility under Radian s standard published guidelines. A separate is available for loan files which qualify under

M&T National Correspondent Product Matrix

M&T National Correspondent Product Matrix Look to M&T Bank for your Correspondent Services. Renovation Lending Specialists and much more. Ask us today! Renovation Programs Renovation Programs FHA 203(k)

M&T National Correspondent Product Matrix Look to M&T Bank for your Correspondent Services. Renovation Lending Specialists and much more. Ask us today! Renovation Programs Renovation Programs FHA 203(k)

Core Seconds S Year Fixed S Due-in 15 Fixed

Last Revised: September 1, 2005 Core Seconds S070 15 Year Fixed S071 30-Due-in 15 Fixed CORE SECONDS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Documentation Requirements

Last Revised: September 1, 2005 Core Seconds S070 15 Year Fixed S071 30-Due-in 15 Fixed CORE SECONDS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Documentation Requirements

***UPDATED 9/5/18*** TPO Fannie Mae HomeStyle Renovation Product

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

LPA HOME POSSIBLE. Home Possible

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

") ; LOAN AMOUNTS

; LOAN AMOUNTS Home Equity Line of Credit

Home Equity Line of Credit PRIMARY RESIDENCE 1 PURCHASE, RATE/TERM REFINANCE & CASH-OUT REFINANCE Property Type 1 to 2-Unit Warrantable Condo PUD Maximum CLTV Maximum Line Amount Minimum Credit Score Total

Home Equity Line of Credit PRIMARY RESIDENCE 1 PURCHASE, RATE/TERM REFINANCE & CASH-OUT REFINANCE Property Type 1 to 2-Unit Warrantable Condo PUD Maximum CLTV Maximum Line Amount Minimum Credit Score Total

85/85/85 No Co-ops 620 if 75% 1 Unit Co-op 85%/NA/NA 620 if 75% 3-4 Units 75/75/75% 680 Second Home. 1 Unit Co-op LCOR: 75%/NA/NA

ELIGIBILITY MATRIX Standard Eligibility Criteria Maximum Allowable LTV Ratios and Minimum Credit Scores for Manual Underwriting (Excludes MyCommunityMortgage, HomeStyle Renovation, Streamlined Refinance

ELIGIBILITY MATRIX Standard Eligibility Criteria Maximum Allowable LTV Ratios and Minimum Credit Scores for Manual Underwriting (Excludes MyCommunityMortgage, HomeStyle Renovation, Streamlined Refinance