Renovation Lending Suite

|

|

|

- Shon McDowell

- 5 years ago

- Views:

Transcription

1 Renovation Lending Suite M A R C H, /10/2019 1

2 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why Renovation Loans? Program Highlights Program Highlights Renovation Consultant Loan Estimate/Fees & Submission Requirements MMWs Renovation Stats Eligibility & Loan Terms Eligibility & Loan Terms Construction Requirements Renovation Specialist & Process Flow Job Aids and Best Practices Why loandepot Wholesale? Maximum Mortgage Calculations Maximum Mortgage Calculations Contractor & Bid Requirements Appraisals, Final Approval, & Post-Close White Label Flyers 4/10/2019 2

3 Renovation Loans Defined Renovation programs are designed for individuals that want to rehabilitate, repair, or update a new or currently owned property Includes funds needed to purchase or refinance funds needed for repairs and related expenses all in one loan Low down payment requirements put renovation projects within reach for borrowers who otherwise could not afford them Purchase Price or Existing Lien Renovation Costs Renovation Loan 4/10/2019 3

4 Why a renovation loan? Renovation loans open up more choices to homebuyers by expanding search parameters Not every home is move-in ready and many buyers don t have the extra funds to upgrade or renovate Home improvements can be personalized - for homebuyers and existing owners Increases property value and builds equity Eliminates need for a construction loan, second mortgage, or use of high interest rate credit cards to fund renovations 4/10/2019 4

5 Renovation Statistics > $350 Billion 2019 Estimated Homeowner Improvements/Repairs U.S. Homes Built Prior to 1989 > 50% > 7.63 Million Average Number of Fixer-Upper Show Viewers from Sources: /10/2019 5

6 Why loandepot Wholesale? With our Renovation Lending Suite we can accommodate the entire renovation spectrum; projects large and small A Renovation Specialist is assigned to each Renovation file and plays an integral role in all Renovation aspects of the loan We provide Marketing Materials, Job Aids, Best Practice documents, easy to use Maximum Mortgage Worksheets, and Training Videos You will have no post-funding responsibilities with our Renovation loans; get paid at closing and you are done with the transaction Your Account Executive has the expertise, tools, and support to help you structure, market, and originate Renovation Loans 4/10/2019 6

7 FHA 203(k)

8 FHA 203(k) Programs The limited program is designed for non-structural repairs up to a maximum of $35,000 in total renovation costs this includes the contingency reserve and any additional fees The standard program is for all projects > $35,000 or homes requiring major renovations, such as structural changes, room additions, or renovations that make the home uninhabitable during construction 4/10/2019 8

9 Program Eligibility Purchase or No Cash-Out Refinance Owner-Occupied only Minimum 620 credit score Conforming and High Balance up to FHA loan limits 4/10/ and 30 Year Fixed Rate terms 5/1 CMT ARM 1/1/5 Caps 1.75% Margin 9

10 FHA 203(k) Limited

11 Limited 203(k) Highlights $5,000-$35,000 repair amount including all other associated costs The property must be occupied within 15 days of close and be habitable throughout the entire construction project Self-help (DIY) not allowed, with the exception of painting and appliance purchases Maximum of 2 draws, initial and final initial draw is the lesser of ½ the bid or full materials cost 4/10/

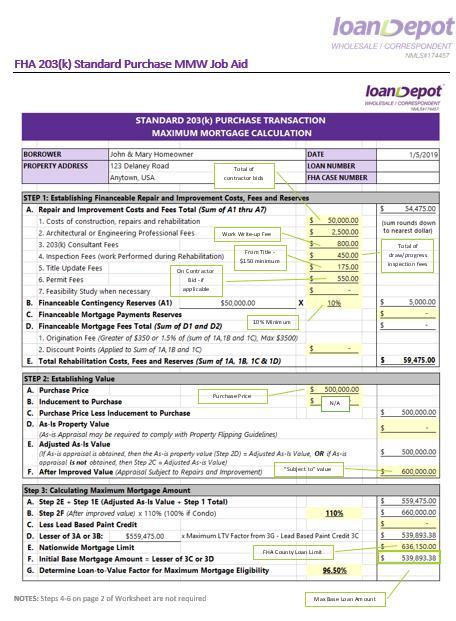

12 Limited: Maximum Mortgage Calculation Step 1: Establishing Financeable Repair and Improvement Costs, Fees, & Reserves Purchase and Refinance total of contractor bids title update fee from title company inspection fee estimated at $150 10% default city permit fees from contractor bid 4/10/

13 Limited: Maximum Mortgage Calculation Step 2: Establishing Value Purchase Subject To Appraisal with an After Improved Value 4/10/

14 Limited: Maximum Mortgage Calculation Step 3: Calculating Maximum Mortgage Amount Purchase Enter FHA county mortgage limit Maximum Mortgage Amount 4/10/

15 Limited: Maximum Mortgage Calculation Step 2: Establishing Value Refinance 2 appraisals required: a subject to and an as is 4/10/

16 Limited: Maximum Mortgage Calculation Step 3: Calculating Maximum Mortgage Amount Refinance Enter FHA county mortgage limit Maximum Mortgage Amount 4/10/

17 FHA 203(k) Standard

18 Standard 203(k) Highlights $5,000 minimum - no maximum repair amount up to FHA County limits Requires a licensed HUD Consultant that manages the entire project; working directly with the borrower and contractor(s) Up to 5 draws as determined by HUD consultant - no initial draw is allowed Up to 6 months PITI can be included in the loan amount if the property is uninhabitable during renovations also determined by the HUD Consultant 4/10/

19 Standard: Maximum Mortgage Calculation Step 1: Establishing Financeable Repair and Improvement Costs, Fees, & Reserves Purchase and Refinance Total of contractor bids Refer to HUD fee schedule title update fee from title company HUD Consultant s fee per inspection/draw Determined by consultant or appraisal can be as high as 20% city permit fees from contractor bid 4/10/

20 Standard: Maximum Mortgage Calculation Step 2: Establishing Value Purchase Subject To Appraisal with an After Improved Value 4/10/

21 Standard: Maximum Mortgage Calculation Step 3: Calculating Maximum Mortgage Amount Purchase Enter FHA county mortgage limit Maximum Mortgage Amount 4/10/

22 Standard: Maximum Mortgage Calculation Step 2: Establishing Value Refinance Discount points, prepaids, and closing costs 2 appraisals required: a subject to and an as is 4/10/

23 Standard: Maximum Mortgage Calculation Step 3: Calculating Maximum Mortgage Amount Refinance Enter FHA county mortgage limit Maximum Mortgage Amount 4/10/

24 FNMA HomeStyle

25 HomeStyle Programs There are two types of HomeStyle transactions available: Up to $50,000 in total renovation costs including contingency reserve and any additional fees Designed for non-structural repairs and allows for two draws Projects > $50,000 in total renovation cost including contingency reserve and any additional fees Homes requiring major renovations, such as structural changes/room additions and allows up to five draws 4/10/

26 Program Eligibility 4/10/

27 Eligible Loan Terms Conforming and High Balance up to FNMA loan limits 15, 20, 25, and 30 Year Fixed Rate terms 5/1, 7/1, & 10/1 ARM Amortization: 30 Years Index: LIBOR 5/1 ARM Caps: 2/2/5 Qual Rate: Higher of note rate + 2% or fully indexed rate 7/1 & 10/1 ARM: Caps: 5/2/5 Qual Rate: Higher of note rate or fully indexed rate 4/10/

28 Mortgage Insurance Mortgage Insurance is required > 80% LTV MI loans are subject to MI Company guidelines LPMI is not available 4/10/

29 New Home Eligibility HomeStyle Renovation may be used to complete the final work on a new built home, when the home is at least 90% complete The remaining improvements must be related to the completion of nonstructural items the original builder was unable to finish Such as installation of buyer-selected items: flooring, cabinetry, kitchen appliances, fixtures, and trim 4/10/

30 Purchase: Maximum Mortgage Amount 1. Identify the lesser of figure:* Purchase Price + Renovation Costs OR After- Improved Value 2. Multiply lesser figure by the LTV to determine loan amount Lesser Figure X LTV = Loan Amount * Maximum allowable repairs cannot exceed 75% of the lesser figure 4/10/

31 Refinance: Maximum Mortgage Amount After- Improved Value* X LTV = Loan Amount * Maximum allowable repairs cannot exceed 75% of the after-improved value 4/10/

32 Maximum Mortgage Worksheet enter LTV & choose loan purpose choose occupancy type enter purchase price or existing loan balance and will receive a FAIL estimated as message when completed value 4/10/2019 renovations exceed 75% 32

33 Maximum Mortgage Worksheet Defaults to 10% if Consultant is required title update fee from title company actual costs for city permits total of contractor bids architectural and engineering fees if applicable estimated at $150 for each draw; approximately 3-5 Maximum Mortgage Amount 4/10/

34 Renovation Need to Knows

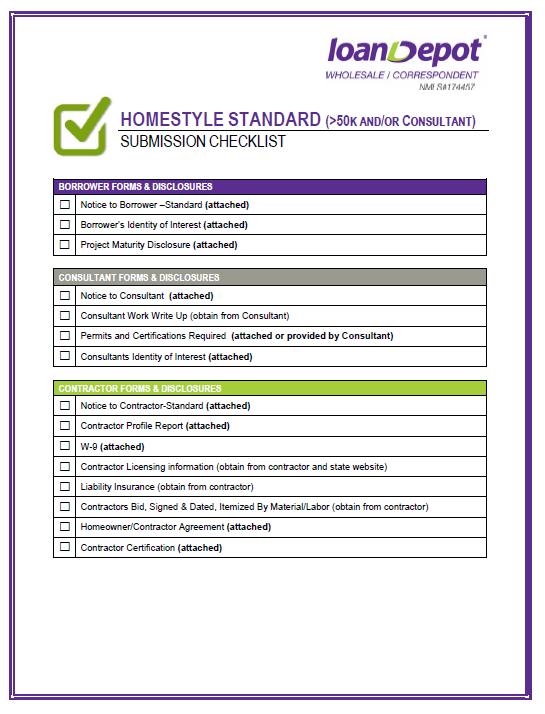

35 Renovation/HUD Consultant Role A licensed Renovation/HUD Consultant is required for: HomeStyle > $50,000 and/or any structural repairs FHA 203(k) Standard Program The Renovation/HUD Consultant: Meets with borrowers and inspects property for required repairs Completes a Work Write Up/Project Review report Works with Contractors to remain within budget and establish draw parameters Performs draw Inspections, authorizing disbursement of funds, throughout renovation HUD maintains a list of Licensed Consultants to choose from 4/10/

36 Purchase Contract/Realtor Tips Purchase contracts must make mention of renovation financing; acceptable on purchase contract or as an addendum Ensure accessibility to property for contractors, HUD consultants, inspectors, architects/engineers, and appraisers Ensure utilities power and water are on at time of appraisal inspection to avoid additional contingency reserves 4/10/

37 Construction Requirements Allowable Construction Period 203(k): repairs must start within 30 days of closing and be completed within 6 months HomeStyle: renovations must be completed within 12 months of closing Minimum renovation amount HomeStyle: no minimum 203(k): $5,000 in repairs minimum Appliance Purchases 203(k): can be the entire project as long as purchases are > $5,000 HomeStyle: must be part of a larger overall project 4/10/

38 Construction Requirements EPA or State Certified painter/contractor required for dwellings built before 1978 Avoid Big Box Contractors Stores like Home Depot, Lowes, and Sears are great for getting appliances but they will not sign any of our required agreements. Not A DIY Loan: the borrower may complete work on HomeStyle and the 203(k) Standard program IF they themselves are licensed and have experience in that scope of repairs. Not intended for the complete tear-down and reconstruction of a dwelling Up to 3 licensed specialized contractors allowed, without a General Contractor 4/10/

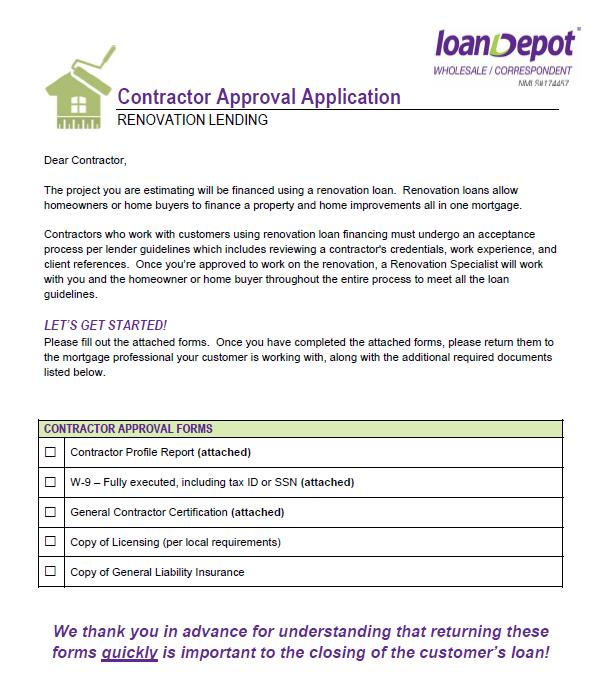

39 Contractor Requirements Contractor Approval Package: PTD Condition Contractor Profile Contractor Certification W-9 Licensing required by state and local jurisdictions Liability Insurance Identity of Interest: the contractor cannot be related to anyone involved in the transaction Licensing/Insurance: the contractor must be appropriate licensed and insured in compliance with state and local jurisdiction - through the date of funding 4/10/

40 Contractor Bid Requirements Contractor Bids can be a pain point in Renovation Lending. Following these best practices, will make for a smoother process flow: Must be typed on company letterhead cannot be handwritten Include Borrowers name and property address Improvements must be detailed and broken out by material, labor, and sales tax Include permit fees - if applicable All health and safety issues are addressed; FHA s minimum property requirements Signed by all parties at time of submission to expedite appraisal ordering 4/10/

41 Processing Renovation Loans

42 Loan Estimate/Fees Portal Product/Pricing Screen Renovation/Holdback maps to Section H of LE Consultant fee (if applicable) maps to Section C of LE Appraised Value Purchase: purchase price + renovation/holdback Refinance: as completed appraised value Loan Estimate Appraisal Fees from LDW posted Appraisal Fee Schedule Section B 203(k) Refinance only: 2 appraisal fees +$200 Misc. fee Title Update Fee Section C Other Inspection Fee Section H 4/10/

43 Sample Loan Estimate 203(k) Refi 2 appraisal fees from LDW Appraisal Fee Schedule + $200 misc. fee From Consultant/Inspector Rehab/Holdback will auto-populate from Portal pricing screen 4/10/

44 Sample Loan Estimate Renovation Consultant Fee will auto-populate from Portal pricing Screen From Title Quote 4/10/

45 Minimum Submission Documents In addition to all standard FHA or FNMA submission documents, the following documents are need to accept a Renovation application and issue initial disclosures: Required at Submission Form Prepared By Notes Maximum Mortgage Worksheet (MMW) Contractor Bids and Consultant s Work Write Up/Cost Estimate - if applicable Broker Contractor or Consultant Used to calculate loan amount for submission and initial disclosures Contractor and Consultant must inspect property prior to completion 4/10/

46 Renovation Specialist A designated Renovation Specialist is assigned when the file is sent to Underwriting The Renovation Specialist is there to answer any Renovation questions you may have at any time prior to submission through post-close. Serves as your liaison, not only with our internal Operations staff, such as the Underwriter and Account Manager, but also communicates directly with Contractors, Consultants, Architects, Inspectors, etc. If desired they can work directly with the Borrower to obtain required forms and clarify construction requirements. We will do as much or as little communicating with others involved in the transaction as you prefer. 4/10/

47 Loan Workflow Submit to LDW Loan Set-Up: App Accepted Renovation Desk: Initial Review Initial Underwrite: CLA Submit Conditions to LDW Renovation Desk: Renovation Conditions & Appraisal Underwriting: Final Approval Account Manager: Closing Prep Closing Coordinator: Doc Prep Funding & Closing

48 Appraisal Orders Appraisals are ordered after the file has been sent to Underwriting and the Renovation Specialist has reviewed the Contractor Bids and all other relevant renovation documentation To ensure the appraisal is ordered in a timely manner, make sure the Contractor Bids and/or Consultant Work Write-up are signed by all parties at time of submission Who orders the appraisal(s)? Wholesale appraisals are ordered by the LDW Renovation Desk NDC appraisals can be ordered by LDW or the Lender 203(k) Refinances require 2 appraisals one with a subject to value and one with an as is value Appraisal Fees should be obtain from LDW Appraisal Fee Schedule 4/10/

49 Renovation Final Approval Upon receipt of all renovation conditions and the appraisal, a Renovation Final Approval will be requested. Please allow 24 hours for this review Once the Renovation Final Approval is issued, the file is ready to move to closing as soon as the Underwriter issues the Credit Final Approval 4/10/

50 Post-Close Process days after loan closing, a Draw Coordinator will be assigned and will act as the liaison between loandepot and the Borrower throughout the renovation process. The Draw Coordinator will reach out to the Borrowers directly via a Welcome , advising them of the process moving forward and confirm the mailing address for draw/disbursement checks. Draws are processed upon receipt of a Draw Process Form from the Borrower or Consultant, if applicable All draw checks are issued as dual party to both the Borrower and Contractor The Draw Coordinator will follow up with the Borrower or Consultant every 30 days until project completion A final inspection of the property is ordered by loandepot upon project completion and required for the final disbursement 4/10/

51 White Label Flyers 4/10/

52 Max Mortgage Worksheets 4/10/

53 Forms Packages 4/10/

54 Best Practices Docs 4/10/

55 Disclaimer loandepot Wholesale loandepot Wholesale is a division of loandepot.com, LLC NMLS # / 2600 Michelson Drive, Ste 1400, Irvine, CA Information contained herein is provided to assist real estate professionals and is not an advertisement to extend consumer credit as defined by section of Regulation Z. loandepot Wholesale, a division of loandepot.com, LLC at 2600 Michelson Drive, Ste 1400, Irvine, CA NMLS ID NMLS Consumer Access IN NO EVENT SHALL LDWholesale BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES OF ANY KIND WHATSOEVER WITH RESPECT TO THE TRAINING AND THE MATERIALS.

56 Questions

FNMA Homestyle Steps to Success

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

203(k) Program Full and Streamline

Program Full and Streamline") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

HomeStyle Renovation Product Offering 8/29/14

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

One loan to renovate. Your homebuyer guide to renovation

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

FHA 203(k) () streamline mortgage Program. make improvements all with a single loan

() streamline mortgage Program. make improvements all with a single loan") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

FHA 203(K) PROGRAM. General Description. Overlays. Available Options

PROGRAM. General Description. Overlays. Available Options") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

Benefits to Borrower - Why Renovation?

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

CONSTRUCTION-TO-PERMANENT GUIDELINES BROKER LOANS

AKA USALLIANCE FEDERAL CREDIT UNION CONSTRUCTION-TO-PERMANENT GUIDELINES BROKER LOANS Available Conforming and Jumbo FIXED: 10 Year, 15 Year, 20 Year and *30 Year Programs: ARMS: 5/1, 5/5 and 7/1 (*30

AKA USALLIANCE FEDERAL CREDIT UNION CONSTRUCTION-TO-PERMANENT GUIDELINES BROKER LOANS Available Conforming and Jumbo FIXED: 10 Year, 15 Year, 20 Year and *30 Year Programs: ARMS: 5/1, 5/5 and 7/1 (*30

Low down payment option; qualify with as little as 3.5% down

Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the

Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the

FHA 203(k) () streamline mortgage Program

() streamline mortgage Program") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

203K Steps to Success

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

***UPDATED 9/5/18*** TPO Fannie Mae HomeStyle Renovation Product

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

HomeStyle Renovation & Energy Mortgages. Finance renovation or energy efficient costs into a single-close home purchase or refinance loan

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

Renovate your Real Estate Business

Renovate your Real Estate Business Shawn Barsness NMLS ID #67292 Renovation Lending This class is to help real estate agents better serve their clients by understanding how renovation loans work to solve

Renovate your Real Estate Business Shawn Barsness NMLS ID #67292 Renovation Lending This class is to help real estate agents better serve their clients by understanding how renovation loans work to solve

Under Construction. Construction and Rehab Loan Programs

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

Renovating and Rebuilding America - One Home at a Time. FHA 203(K) Renovation Lending Product Information

Renovation Lending Product Information") FHA 203(K) Product Information 1 Program Summary The FHA 203(k) The FHA 203(k) loan allows a borrower to purchase or refinance and repair or renovate a property all in one loan. The borrower closes with

FHA 203(K) Product Information 1 Program Summary The FHA 203(k) The FHA 203(k) loan allows a borrower to purchase or refinance and repair or renovate a property all in one loan. The borrower closes with

Revised 4/6/18. FHA 203K Renovation

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

FHA Renovation Loan Program, or 203K

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

Buy a home, plus make improvements, with just one loan

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

FHA 203(k) Standard Product Guide

Standard Product Guide") FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

One-Close Construction

RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction

RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction

Limited FHA 203K. Village Mortgage NMLS Intended for Mortgage Professionals Only 1

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

Products. Loan Amount

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET At AmeriFirst we are committed to providing you with all the information you need regarding your construction loan. This guide will walk you through

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET At AmeriFirst we are committed to providing you with all the information you need regarding your construction loan. This guide will walk you through

Your Home Should Be YOUR WAY. That s the FAIR WAY! A Renovation Guide Made Simple

Your Home Should Be YOUR WAY That s the FAIR WAY! A Renovation Guide Made Simple Table of Contents The Renovation Loan: A Solution to a Problem... 3 Options for Renovation... 4 10 FHA 203k Standard FHA

Your Home Should Be YOUR WAY That s the FAIR WAY! A Renovation Guide Made Simple Table of Contents The Renovation Loan: A Solution to a Problem... 3 Options for Renovation... 4 10 FHA 203k Standard FHA

PRODUCT MATRICES. For Information on any of our products, please contact:

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Revised 04/30/18. FHA Standard 203K

Revised 04/30/18 FHA Standard 203K FHA Standard 203K Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official

Revised 04/30/18 FHA Standard 203K FHA Standard 203K Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official

Plaza s VA Renovation

Click here to add a longer headline about the slide Plaza s VA Renovation July 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial

Click here to add a longer headline about the slide Plaza s VA Renovation July 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial

USDA REPAIR ESCROW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/5/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/5/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

FHA 203K MATRIX. Second Appraisal Requirements

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

Home Possible and Home Possible Advantage

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Sponsored by: Mortgage 101

Sponsored by: Mortgage 101 Who is Equity Resources, Inc? Direct mortgage banker - Fannie Mae and Ginnie Mae Seller Servicer FHA/VA/Conventional/RD loans Underwrite in our main office Company began in 1993

Sponsored by: Mortgage 101 Who is Equity Resources, Inc? Direct mortgage banker - Fannie Mae and Ginnie Mae Seller Servicer FHA/VA/Conventional/RD loans Underwrite in our main office Company began in 1993

FULL DOC. PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO. Owner Occupied (O/O) 1 unit 80% 80% unit (see MI section below) 95% 95% 700

1 unit 80% 80% unit (see MI section below) 95% 95% 700") FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

M&T National Correspondent Product Matrix

M&T National Correspondent Product Matrix Look to M&T Bank for your Correspondent Services. Renovation Lending Specialists and much more. Ask us today! Renovation Programs Renovation Programs FHA 203(k)

M&T National Correspondent Product Matrix Look to M&T Bank for your Correspondent Services. Renovation Lending Specialists and much more. Ask us today! Renovation Programs Renovation Programs FHA 203(k)

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

FNMA s HomeReady Program

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

FHA 203(k) Rehabilitation Mortgage REMN Wholesale Product Description

Rehabilitation Mortgage REMN Wholesale Product Description") PROGRAM OVERVIEW STANDARD... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 LIMITED... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 Footnotes...

PROGRAM OVERVIEW STANDARD... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 LIMITED... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 Footnotes...

Wholesale Overlay Matrix

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

FHA FIXED & ADJUSTABLE RATE Series 300, 500, 700, & 800

FHA FIXED & ADJUSTABLE RATE Series 300, 500, 700, & 800 Product Description FHA Conforming Fixed Rate & ARM FHA15 = 15 year fixed FHA30 = 30 year fixed Program Numbers FHA5/1 = 5/1 ARM FHASTREAM15 = 15

FHA FIXED & ADJUSTABLE RATE Series 300, 500, 700, & 800 Product Description FHA Conforming Fixed Rate & ARM FHA15 = 15 year fixed FHA30 = 30 year fixed Program Numbers FHA5/1 = 5/1 ARM FHASTREAM15 = 15

Rehab Financing The FHA Streamline 203(k) Program

Program") The FHA Streamline 203(k) Program A Guide to Financing Your Home Improvement Project The Program: This is a new 1 st mortgage program sponsored by the FHA and designed to provide homeowners with low-cost

The FHA Streamline 203(k) Program A Guide to Financing Your Home Improvement Project The Program: This is a new 1 st mortgage program sponsored by the FHA and designed to provide homeowners with low-cost

Financing Residential Real Estate. FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, graduated payment mortgages, FHA insurance premiums, sales concessions such

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, graduated payment mortgages, FHA insurance premiums, sales concessions such

This saves borrowers thousands of dollars out of pocket.

A 203(k) loan is a loan that allows the borrower to purchase or refinance a home and include in the loan the costs to do repairs, upgrades and remodeling of the home. This saves borrowers thousands of

A 203(k) loan is a loan that allows the borrower to purchase or refinance a home and include in the loan the costs to do repairs, upgrades and remodeling of the home. This saves borrowers thousands of

Assistance Program: Miami Dade County PHCD Affordable Housing First Time Homebuyer Program Code: DFLMIAMCY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

ONE TIME CLOSE RENOVATION TO PERM OPTION III

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

All-in-One Custom Construction

Wholesale Lending All-in-One Custom Construction This is a true one-time-close loan program designed to finance the construction or major remodel of a primary residence or second home. This loan includes

Wholesale Lending All-in-One Custom Construction This is a true one-time-close loan program designed to finance the construction or major remodel of a primary residence or second home. This loan includes

YOUR GUIDE. To Home Ownership

YOUR GUIDE To Home Ownership FIRST TIME HOMEBUYER? There are many advantages of home ownership Home ownership is one of life s major events, and it provides some unique personal and financial rewards.

YOUR GUIDE To Home Ownership FIRST TIME HOMEBUYER? There are many advantages of home ownership Home ownership is one of life s major events, and it provides some unique personal and financial rewards.

Good for 120 days. Minimum Required Investment Little to NO reserves ARMS allowed Manual Underwriting is Allowed

FHA PURCHASE Credit Score 620+ Score required ----------- 580-619 -with 2 month PITI reserves -NO gift funds -Max base loan $417,000 Max LTV 1/1/5 3/1/5 5/2/6 ARMs Appraisal 96.5% Allowed Yes Good for

FHA PURCHASE Credit Score 620+ Score required ----------- 580-619 -with 2 month PITI reserves -NO gift funds -Max base loan $417,000 Max LTV 1/1/5 3/1/5 5/2/6 ARMs Appraisal 96.5% Allowed Yes Good for

PRODUCT MATRICES. For Information on any of our products, please contact your USBHM Account Executive

Wholesale Lending PRODUCT MATRICES March 2017 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Wholesale Lending PRODUCT MATRICES March 2017 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

PRODUCT MATRIX 3/15/07

PRODUCT MATRIX 3/15/07 For More information on any of our products please contact: Underwriting Help Desk 866-807-6049 (for product questions or scenarios) Help Desk Bloomington 800-200-5881(for Pricing

PRODUCT MATRIX 3/15/07 For More information on any of our products please contact: Underwriting Help Desk 866-807-6049 (for product questions or scenarios) Help Desk Bloomington 800-200-5881(for Pricing

NEIGHBORHOOD STABILIZATION PROGRAM HOME SALES PROGRAM GUIDANCE

NEIGHBORHOOD STABILIZATION PROGRAM HOME SALES PROGRAM GUIDANCE PROGRAM DETAILS... NSP SUMMARY... ELIGIBILITY CRITERIA... WAITING LIST... APPLICANT INTAKE... HOMEBUYER COUNSELING... CLOSING COST ASSISTANCE...

NEIGHBORHOOD STABILIZATION PROGRAM HOME SALES PROGRAM GUIDANCE PROGRAM DETAILS... NSP SUMMARY... ELIGIBILITY CRITERIA... WAITING LIST... APPLICANT INTAKE... HOMEBUYER COUNSELING... CLOSING COST ASSISTANCE...

FHA 203(k) Product Offering 8/12/14

Product Offering 8/12/14") FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

Fannie Mae Conforming and High Balance

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

LOCK SUBMISSION DEADLINE

9815 S 240 W (Monroe Street), Ste 203, Sandy, UT 84070 Office Phone: (801) 262-6033 or 1-888-891-5440 IMPORTANT ANNOUNCEMENTS All 30 & 45 day locks must submit loan files within 7 days of lock date to

9815 S 240 W (Monroe Street), Ste 203, Sandy, UT 84070 Office Phone: (801) 262-6033 or 1-888-891-5440 IMPORTANT ANNOUNCEMENTS All 30 & 45 day locks must submit loan files within 7 days of lock date to

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Opportunity Down Payment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Opportunity Down Payment Assistance Program can

to Renovation Financing

YOUR GUIDE to Renovation Financing IT S MORE THAN A MORTGAGE It Can Be Your Custom Home If you re shopping for a home, you likely have a wish list and with each house you enter, you re wondering if you

YOUR GUIDE to Renovation Financing IT S MORE THAN A MORTGAGE It Can Be Your Custom Home If you re shopping for a home, you likely have a wish list and with each house you enter, you re wondering if you

YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES. Funding Source. Program Code. Eligible States Minimum Loan Amount.

Revised 6/8/2015 YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income

Revised 6/8/2015 YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income

REVERSE MORTGAGE GUIDE

REVERSE MORTGAGE GUIDE Reap The Rewards Of A Lifetime Investment In Homeownership INVICTA MORTGAGE GROUP Better programs. Better service. Better financing. Licensed by PA Dept of Banking. NMLS# 111947

REVERSE MORTGAGE GUIDE Reap The Rewards Of A Lifetime Investment In Homeownership INVICTA MORTGAGE GROUP Better programs. Better service. Better financing. Licensed by PA Dept of Banking. NMLS# 111947

203k Quick Reference Guide

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

FNMA HomeStyle Steps to Success

WHOLESALE EDITION - Nov 2013 FNMA HomeStyle Steps to Success Step One- Program Education Register for classes at M&T University Review Program Product Pages and M&T Agency Underwriting and Eligibility

WHOLESALE EDITION - Nov 2013 FNMA HomeStyle Steps to Success Step One- Program Education Register for classes at M&T University Review Program Product Pages and M&T Agency Underwriting and Eligibility

Construction and Rehabilitation Construction Financing

Construction and Rehabilitation Construction Financing YOUR INSTRUCTORS Dave Konrad District Manager First Horizon Home Loans Mary Robenalt Porter General Counsel NorthStar Title Services, LLC Course Intro

Construction and Rehabilitation Construction Financing YOUR INSTRUCTORS Dave Konrad District Manager First Horizon Home Loans Mary Robenalt Porter General Counsel NorthStar Title Services, LLC Course Intro

DETROIT HOME MORTGAGE RENOVATION EDUCATION

DETROIT HOME MORTGAGE RENOVATION EDUCATION COURSE OUTLINE Ways to Renovate Using Detroit Home Mortgage Things to Consider Before You Begin Renovating Roles and Responsibilities Renovation-Related Documents

DETROIT HOME MORTGAGE RENOVATION EDUCATION COURSE OUTLINE Ways to Renovate Using Detroit Home Mortgage Things to Consider Before You Begin Renovating Roles and Responsibilities Renovation-Related Documents

BUILD BUY RENOVATE. Your guide to understanding and financing your new home

BUILD BUY RENOVATE Your guide to understanding and financing your new home TURNERR@FNB-CORP.COM Table of Contents Your Dreams become reality 3 Overview 3 Why Construction / Renovation Permanent 4 Financing

BUILD BUY RENOVATE Your guide to understanding and financing your new home TURNERR@FNB-CORP.COM Table of Contents Your Dreams become reality 3 Overview 3 Why Construction / Renovation Permanent 4 Financing

FHA Product Overview. Product and Underwriting Guidelines. U.S. Bank Home Mortgage Wholesale Division CAT CR U.S.

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

REG Z PORTFOLIO ARMS - Primary Residence. REG Z PORTFOLIO ARMS - Non-Owner Occupied (Cash out or Delayed Finance, Not Business Entity) A+ CREDIT

A+ CREDIT") California Luther Burbank Savings ~ Wholesale Rate Sheet 5/23/2016 8:00 AM PST Lock Desk: 7:30 AM - 4:00 PM PST, Monday - Friday Index: Website www.lutherburbanksavingswholesale.com 1 Yr LIBOR 1.2990%

California Luther Burbank Savings ~ Wholesale Rate Sheet 5/23/2016 8:00 AM PST Lock Desk: 7:30 AM - 4:00 PM PST, Monday - Friday Index: Website www.lutherburbanksavingswholesale.com 1 Yr LIBOR 1.2990%

UNDERSTANDING THE DOWN PAYMENT ASSISTANCE QUALIFYING PROCESS THROUGH THE STATE HOUSING INITIATIVES PARTNERSHIP PROGRAM (SHIP) FOR HERNANDO COUNTY

FOR HERNANDO COUNTY") UNDERSTANDING THE DOWN PAYMENT ASSISTANCE QUALIFYING PROCESS THROUGH THE STATE HOUSING INITIATIVES PARTNERSHIP PROGRAM (SHIP) FOR HERNANDO COUNTY 1661 Blaise Drive Brooksville, FL 34601 Phone: (352) 754-4160

UNDERSTANDING THE DOWN PAYMENT ASSISTANCE QUALIFYING PROCESS THROUGH THE STATE HOUSING INITIATIVES PARTNERSHIP PROGRAM (SHIP) FOR HERNANDO COUNTY 1661 Blaise Drive Brooksville, FL 34601 Phone: (352) 754-4160

YORK HOMEBUYER ASSISTANCE PROGRAM

Revised 12/16/2010 YORK HOMEBUYER ASSISTANCE PROGRAM Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income households in

Revised 12/16/2010 YORK HOMEBUYER ASSISTANCE PROGRAM Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income households in

Assistance Program: City of Los Angeles Low Income Purchase Assistance Program (LIPA) Zero Interest Code: DCALIPADP

Zero Interest Code: DCALIPADP") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Section Agency Loan Programs

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

CHOOSING THE RIGHT MORTGAGE PARTNER

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Know Your Products. Marc Kaplan, Sr. VP Retail Sales

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

Detroit Home Mortgage. Request for Qualifications: Detroit Home Mortgage Project Manager

Detroit Home Mortgage Request for Qualifications: Detroit Home Mortgage Project Manager INTRODUCTION A. Overview This Request for Qualifications ( RFQ ) is being issued by Detroit Home Mortgage ( DHM ),

Detroit Home Mortgage Request for Qualifications: Detroit Home Mortgage Project Manager INTRODUCTION A. Overview This Request for Qualifications ( RFQ ) is being issued by Detroit Home Mortgage ( DHM ),

YOUR NEW HOME. Member FDIC

7EASY STEPS TO YOUR NEW HOME Member FDIC 1The First Step Getting prequalified or preapproved by your bank is essential before you start looking at houses. A Frandsen lender can help you determine how much

7EASY STEPS TO YOUR NEW HOME Member FDIC 1The First Step Getting prequalified or preapproved by your bank is essential before you start looking at houses. A Frandsen lender can help you determine how much

Annoucement Correspondent Lending

Superior Performance Our Commit ment New VP Correspondent Lending Turn Times New Correspondent Team Members Update Guidelines Annoucement 2011 10-25 Correspondent Lending IN THIS ANNCOUNCEMENT 203Ks Updated

Superior Performance Our Commit ment New VP Correspondent Lending Turn Times New Correspondent Team Members Update Guidelines Annoucement 2011 10-25 Correspondent Lending IN THIS ANNCOUNCEMENT 203Ks Updated

BUYING YOUR FIRST HOME

BUYING YOUR FIRST HOME Finding the home of your dreams is the tough part, the mortgage process shouldn t be. That s why we ve created a guide to make your first-time home buying experience easier. This

BUYING YOUR FIRST HOME Finding the home of your dreams is the tough part, the mortgage process shouldn t be. That s why we ve created a guide to make your first-time home buying experience easier. This

NEW HOME BUYER Guide

NEW HOME BUYER Guide???? 1. INITIAL CONSULTATION 8. CLEAR TO CLOSE 9. NUMBERS REVIEW 2. PRE-APPROVAL 7. CLOSING PACKAGE 10. CLOSING DAY! 3. FINDING YOUR HOME 6. UNDERWRITING APPROVAL 4. APPRAISAL 5. PROCESSING

NEW HOME BUYER Guide???? 1. INITIAL CONSULTATION 8. CLEAR TO CLOSE 9. NUMBERS REVIEW 2. PRE-APPROVAL 7. CLOSING PACKAGE 10. CLOSING DAY! 3. FINDING YOUR HOME 6. UNDERWRITING APPROVAL 4. APPRAISAL 5. PROCESSING

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME 4 REASONS WHY YOU SHOULD CHOOSE PPG UPFRONT UNDERWRITING And pre-approvals! This reduces your stress when buying a home. EASY MOBILE APPLICATION We keep

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME 4 REASONS WHY YOU SHOULD CHOOSE PPG UPFRONT UNDERWRITING And pre-approvals! This reduces your stress when buying a home. EASY MOBILE APPLICATION We keep

WELCOME TO YOUR HOMEBUYER JOURNAL

WELCOME TO YOUR HOMEBUYER JOURNAL THIS JOURNAL BELONGS TO: Congratulations, you ve taken the first step and decided to buy a home! Use this journal to keep track of your home buying search. There is a

WELCOME TO YOUR HOMEBUYER JOURNAL THIS JOURNAL BELONGS TO: Congratulations, you ve taken the first step and decided to buy a home! Use this journal to keep track of your home buying search. There is a

EverBank Wholesale Lending

EverBank Wholesale Lending LOAN PROGRAM CODE PRODUCT OVERVIEW LOAN TYPE LOAN TERMS ELIGIBLE PROPERTY TYPES INELIGIBLE PROPERTY TYPES OCCUPANCY 30 Year - 30FNMC 15 Year - 15FNMC The FNMA MyCommunity products

EverBank Wholesale Lending LOAN PROGRAM CODE PRODUCT OVERVIEW LOAN TYPE LOAN TERMS ELIGIBLE PROPERTY TYPES INELIGIBLE PROPERTY TYPES OCCUPANCY 30 Year - 30FNMC 15 Year - 15FNMC The FNMA MyCommunity products

HomeStyle Renovation Submission Checklist

HomeStyle Renovation Submission Checklist Borrower Name: Loan #: Homestyle Calculation Worksheet (LoanBuilder) * HomeStyle Renovation Consumer Tips (Form 1204) signed by borrower Appraisal with all improvements

HomeStyle Renovation Submission Checklist Borrower Name: Loan #: Homestyle Calculation Worksheet (LoanBuilder) * HomeStyle Renovation Consumer Tips (Form 1204) signed by borrower Appraisal with all improvements

Fannie Mae Conforming and High Balance

Primary Purchase or 620 620 Second Home 1 Fixed 97% 1,2 / ARM 90% 2 Fixed 85% / ARM 75% 3-4 Fixed 75% / ARM 65% 1 Fixed 80% / ARM 75% 2-4 Fixed 75% / ARM 65% Purchase or 620 1 Fixed 90% / ARM 80% 620 1

Primary Purchase or 620 620 Second Home 1 Fixed 97% 1,2 / ARM 90% 2 Fixed 85% / ARM 75% 3-4 Fixed 75% / ARM 65% 1 Fixed 80% / ARM 75% 2-4 Fixed 75% / ARM 65% Purchase or 620 1 Fixed 90% / ARM 80% 620 1

#1 KY RHS Lender. #1 MCC Tax Credit Lender. #3 KHC Delegated Lender by Volume. Fannie Mae Direct Lender Seller/Servicer. FHA Approved DE Lender

#1 KY RHS Lender #1 MCC Tax Credit Lender #3 KHC Delegated Lender by Volume 2nd Largest Independent Mortgage Banker in KY Fannie Mae Direct Lender Seller/Servicer FHA Approved DE Lender VA Automatic/LAPP

#1 KY RHS Lender #1 MCC Tax Credit Lender #3 KHC Delegated Lender by Volume 2nd Largest Independent Mortgage Banker in KY Fannie Mae Direct Lender Seller/Servicer FHA Approved DE Lender VA Automatic/LAPP

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage 0% Downpayment Assistance Program

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage 0% Downpayment Assistance Program

I. Creating a one-time close construction to permanent loan or a one-time close renovation to permanent loan.

Construction to Permanent FNMA One Time Close DU Data Entry MOTION Important: Items must be completed in the following order Create or Import a construction to permanent loan Select construction product

Construction to Permanent FNMA One Time Close DU Data Entry MOTION Important: Items must be completed in the following order Create or Import a construction to permanent loan Select construction product

Tips for First-Time Homebuyers

Tips for First-Time Homebuyers If you re just beginning the process of financing your first home, you might be unsure of all the costs or the decisions you ll have to make eventually. Months before applying

Tips for First-Time Homebuyers If you re just beginning the process of financing your first home, you might be unsure of all the costs or the decisions you ll have to make eventually. Months before applying

Your Reverse Mortgage Guide. Reaping The Rewards Of A Lifetime Investment In Homeownership

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Mortgage Insurance Help

Mortgage Insurance Help Address Line 1 Address Line 2 All Other Monthly Payments Amortization Term Amortization Type Application Number Appraisal Value Borrower's First Name Borrower's Last Name Borrower's

Mortgage Insurance Help Address Line 1 Address Line 2 All Other Monthly Payments Amortization Term Amortization Type Application Number Appraisal Value Borrower's First Name Borrower's Last Name Borrower's

LPA HOME POSSIBLE. Home Possible

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

HOMEBUYER S GUIDE WE RE ALL ABOUT THAT NEW HOME SMELL

FIRST-TIME HOMEBUYER S GUIDE WE RE ALL ABOUT THAT NEW HOME SMELL THE SCENT OF FRESH PAINT WITH A HINT OF EQUITY & A DASH OF ACCOMPLISHMENT Anthony Rael REALTOR RE/MAX ALLIANCE 303.520.3179 Tiffany L Swisher

FIRST-TIME HOMEBUYER S GUIDE WE RE ALL ABOUT THAT NEW HOME SMELL THE SCENT OF FRESH PAINT WITH A HINT OF EQUITY & A DASH OF ACCOMPLISHMENT Anthony Rael REALTOR RE/MAX ALLIANCE 303.520.3179 Tiffany L Swisher

WCDA LOAN PRODUCT MATRIX

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

VERY IMPORTANT THE LOAN WILL BE RUN THROUGH DU PRIOR TO START OF CONSTRUCTION AND MUST REFLECT APPROVE ELIGIBLE.

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

California Wholesale Rate Sheet

Effective Fri 01/25/2019 9:44 AM EST California Wholesale Rate Sheet Jumbo Series H is Here! - See page 15 for details. Rate Fall-Out Specials on SmartEdge, SmartCondo & Dream Big! Smart Funds - See page

Effective Fri 01/25/2019 9:44 AM EST California Wholesale Rate Sheet Jumbo Series H is Here! - See page 15 for details. Rate Fall-Out Specials on SmartEdge, SmartCondo & Dream Big! Smart Funds - See page

FHA 203(h) For Disaster Victims COPYRIGHT 2018 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

For Disaster Victims COPYRIGHT 2018 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") 10/26/2018 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

10/26/2018 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

Dream Big Jumbo Is Now Available

Effective Tue 04/10/2018 9:54 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Tue 04/10/2018 9:54 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up