Broker and Correspondent Training

|

|

|

- Lionel Knight

- 5 years ago

- Views:

Transcription

1 Broker and Correspondent Training

2 Flanagan State Bank headquarters is located in Flanagan, IL. The bank was founded in 1913 and has been family owned/operated since the 1930 s by the Schwerin family. FSB is a bank that believes in providing the best possible customer service. We do not believe in going just half way and will commit to taking care of our customers 100% Our TPO Division continues to cultivate new investors and agencies to provide the best possible programs and rates that we can.

3 Programs FHA USDA VA Conventional Services Appraisal Department Scenario Review Income Analysis Q & A Quick Underwriting Forms & Docs Loan Officer Marketing Materials Contact Information Helpful Links Program Information

4 Correspondent Closes loans in their company name Funds their own loans that are closing in their name using a warehouse line, funding line or own funds Does not disclose YSP/SRP FSB will purchase the loan from them after delivery of the closing package Broker Loan closes in Flanagan s name FSB funds are used to fund the loan Disclosure of LPC required Loan is funded at time of closing if a purchase or recission if a refi. For most of our customers, a combination of both Corr and Broker is used due to FHA

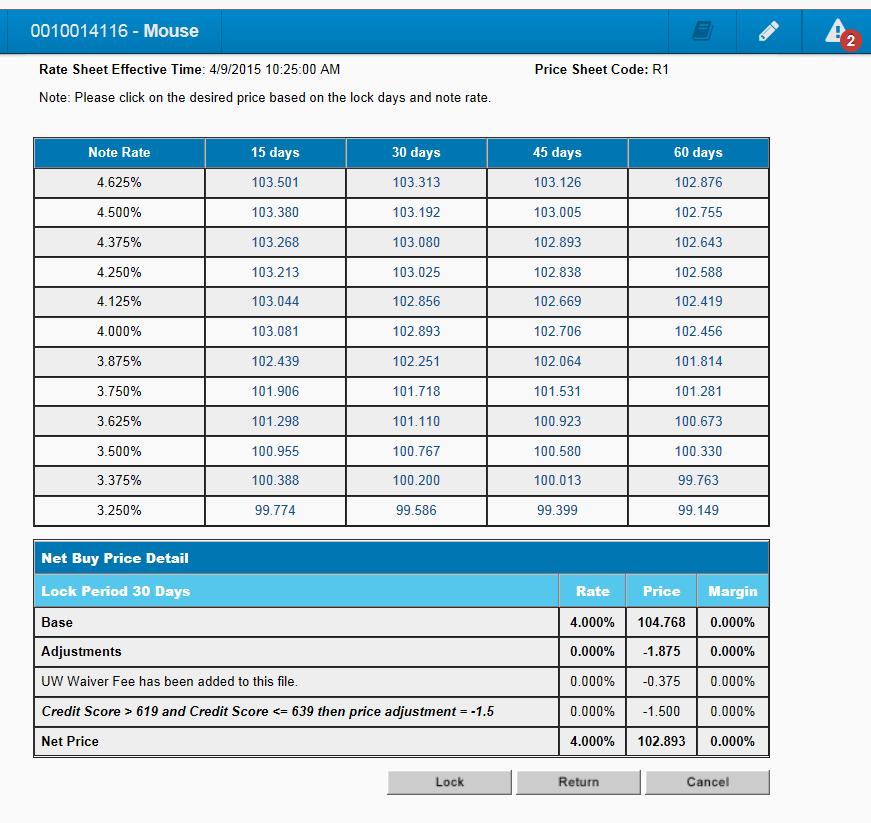

5 Rate sheets are distributed via every morning and then as rates change throughout the day Available on our website at Off sheet pricing available for Jumbo loans, high balance FHA & VA loans

6 USDA Loan Scenario - $85, loan amount, 649 credit score, IL property, waiving underwriting Work your way backwards to the profit your company identifies as needed from each transaction. IF your company designates your profit should be 2.75 Lender Paid, start adding your adjustments up first. For this scenario that would equal: Loan Size N/A Credit Score State Location N/A Waiving Underwriting Fee Total Adjustments = Now add your anticipated compensation to the total adjustments = 4.50 Your rate must cover at a minimum or it will result in a discount being paid by the borrower. Looking at the rate sheet in your hand outs, this would put the rate offered at: 4.375% paying (30 day lock) subtract your adjustments/comp needed and you are left with.248 credit to the borrower towards closing costs or rate extensions.

7 FSB does not set any limits on Borrower Paid Compensation. However, the loan must pass the final Points & Fees Test or fees will be reduced at closing. Pricing will work similar to the screen before, but compensation will not be reduced from the yield on the rate. The remaining yield left on the rate will be provided to the borrower as a credit, but the credit CANNOT be used towards the Borrower Paid Origination Fee showing on the GFE. It can be used for all other closing costs except the origination fee.

8 Please note: FSB s lowest loan amount is: $30,000 on USDA $35,000 on FHA/VA $40,000 on Conventional

9 The Correspondent customers do not have Lender Paid Compensation. They do not have to disclose the yield earned on the rate on the GFE/TIL They are limited only by max pricing on the program/rate sheets for each program. Please note USDA is limited to FHA/VA is limited to Conventional is limited to The max pricing is after adjustments! Corr files may charge Upfront fee and earn yield on rate

10 All locks are completed online within the file you are locking Once locked within the file, an confirmation will be sent to confirm pricing Off sheet pricing for Jumbo and High Balance VA/FHA loans is available Pricing is subject to change as the market changes, always confirm pricing either using online pricing/scenario Pricer or have the most recent rate sheet

11 LO or Processor begins file in Mortgagebot Upload of FNMA 3.2 or manual entry file Registration of File is completed Loan can be locked at this time, if desired Submission Package is uploaded for review Loan is finaled to notify Underwriting Department loan is ready for review File is received in Underwriting Jr Underwriters pick up file in order of receipt and sort/label documents for UW to review. All reports are ordered Jr Underwriters complete compliance review of file and condition accordingly Loan is sent to UW for credit underwriting Underwriters review and condition for PTC and PTF items needed File is sent back to Jr UW s to deliver Conditional Approval to LO/Processor File is received for resubmission Conditions are sorted and labeled by the Jr. Underwriter. Compliance Conditions are reviewed by the Jr UW and signed off if provided Jr UW sends loan to UW for condition review UW clears conditions and sends updated approval to Jr UW Jr UW delivers update Conditional Approval to LO/Processor Resubmission of conditions (consecutive attempt) Same pattern as above If loan is USDA: all conditions are met, file is sent to USDA office for CC If all conditions are met, UW will FINAL loan clearing all conditions Loan is sent back to Jr UW to confirm all Compliance conditions are cleared. If all are cleared CTC can be issued. is sent to LO/Processor confirming CTC or requesting items needed for CTC Clear to Close LO/Processor to send Closing Request Form to Closing Department via Closer will confirm receipt of document and closing date Closing Instructions are sent out at least 24 hours prior to closing or per closing request HUD to be approved on all brokered loans prior to closing package sent to Title Company Wire for broker funded loans is sent 24 hours prior to closing Post Closing (Correspondent) If a loan is a Corr that is closing, the closing package is to be uploaded in the Mortgagebot file The original Allonge, Note and Bailey Letter is to be sent to the TPO Division Headquarters The LO/Processor will the Correspondent and notify them the package is ready for review The Jr UW will review and advise if all is in file for Purchase The file and originals must be delivered prior to the lock expiring

12 Tips and Tricks to getting your file through our underwriting review quickly

13 One of the most common things we see in underwriting is the 1003 having missing information or inaccurate information. It is very important that the application contain ALL the boxes filled in, not just some of them The next few slides will provide insight into the most common errors that show up on a 1003 and these errors will add conditions to your approval that tie up your time and could be avoided

14 The highlighted section should be accurate and match the GFE/TIL. If a Joint account, the top section should be signed by both applicants. The refinance section should only be completed IF a refinance and all sections should be completed.

15 It is important to list their current address and any addresses the borrower/co-borrower may have had over the past 2 years. If the address does not match the Driver s License that is submitted, the underwriter will require an LOX. If RENT is marked in the residence history, a VOR will be requested. If Own is marked in the residence history, the REO section should contain coordinating information. IF the applicant does not rent or own, neither should be marked and an LOX from the borrower should be included noting the circumstances of the housing for the borrower. All forms that show a section for initials or signatures must be fully executed to meet compliance requirements.

16 The employment history section must be completed in detail. Any missing information will result in conditions from the underwriter to complete the section. Phone number should be accurate and not a number that will reach the borrower. This number will be used to complete the Verbal Verification of Employment that will be completed within 48 hours of closing. If a borrower has multiple W-2 s for the most recent 2 years, all W-2 employment must be listed on the Dates must be correct and a verification may be requested at the discretion of the underwriter.

17 Monthly Income and Housing Expense Accurate income is always crucial in a mortgage loan. Income should be broken down according to its correct classification and not lumped together if containing OT, Bonus or Commission. SSI can be grossed up according to the tax bracket chart and will be listed under Other Income. Self employment income will also be referenced in this section. If rent/own are checked in the residence history, then Present Housing Expense must be completed. This section allows the underwriter to verify how much payment shock the borrower will experience. Proposed housing should include the full PITI payment that the loan will generate.

18 Assets: If assets are listed in the application, then 2 months bank statements MUST be provided. Bank statements will also be required regardless if on application or not when verifying fixed income, down payment funds (to verify borrower used own funds for Earnest Money Deposit if cancelled check not provided) or cash to close is noted in details of transaction. If bank statements note NSF, overdrafts or other negative activity on accounts, UW guides do note that this is financial mismanagement and will not approve the borrower for a loan. It is important that the Loan Officer/Processor review statements prior to submission to underwriting. If the circumstance was a one time occurrence, an exception may be made based on the reason for the NSF. Liabilities: Must all be included that are on the credit report and any that might not report on the report, but should be a part of the DTI. Paystubs should be reviewed for child support garnishments prior to underwriting submission.

19 Under Assets Section, many LO s will list household goods and Automobiles in this section. For the purposes of mortgage loans, this information is not required. Liquid assets are more important to an application than non liquid assets. Alimony, Child Support, Maintenance will required documentation to support. A divorce decree and verification of children s ages are basic documents needed. Job related expenses: Listed here will be union dues, unreimbursed expenses taken from tax returns and other misc amounts that are the borrower s responsibility based on their employment. These are recurring expenses. Unreimbursed expenses are typically a surprise to the LO and 8 out of 10 times a deal killer. FSB strongly suggests requesting the tax returns from the borrower to verify there are not any surprises before it is underwritten.

20 REO Section Full disclosure of properties owned is required. This should include lots, land, commercial property, residential property, etc. USDA is very specific about a borrower only retaining a single residential property in addition to purchase the new one. They must qualify with BOTH PITI payments. Properties that are pending sale or recently sold should be referenced in this section, too. Free & Clear properties must be documented so the underwriter can see that the property truly is Free & Clear PITI must be proven on all properties either through tax returns (Schedule E or mortgage statements, tax statements and proof of HOI)

21 Details of transaction: a) Purchase price should match the contract b) If escrow is being held for repairs to property, include this amount here. c) N/A only for construction lending d) If a refi debts to be paid off should transfer to this section from marked to be paid liabilities e) Prepaid items as showing on GFE f) Closing costs as showing on GFE g) Government Loan Fee as applicable h) Discount points if applicable i) Total costs of transaction j) DPA/Grant will show in this box k) Closing costs paid by seller per contract l) Other Credits such as property tax credit, broker credit, etc will reflect here m) Base loan amount n) Government Loan fee(should match g) o) Total Loan amount p) Cash from/to borrower. If cash from borrower, assets to cover this amount need to show in Assets section of No cash back allowed to borrower except for reimbursement of fees paid in advance

22 All questions must be marked correctly. The borrower does sign acknowledging that all information contained in the applications is true and accurate. The questions we see that are normally marked inaccurately are: B C G Double check the answers with the borrower to insure accuracy and eliminate surprises later in the loan process.

23 Borrowers signatures will be matched to driver s license signatures to confirm identity and verify matching. Date of application should match date of GFE/TIL and other initial application disclosures. Date of 1003 may be after credit report date on a purchase. Typically the receipt of the purchase contract is a simple reference date for determining when the 3 day rules begins for disclosures. On a refinance it should be dated within 3 days of the credit report per compliance rules.

24 Ethnicity, Race and Sex should be checked based on information from the LO. Originator to indicate how application was taken. LO s information and signature required. Should be dated within the 3 days required per RESPA for initial disclosure.

25 Credit Reports are valid for 90 days from the date pulled All non traditional tradelines must be added to the reports as a supplement All government loans will require letter of explanation for the derogatory credit that shows on the report. The LOX must show what happened, how the borrower overcame the problem and how the problem will not happen again. All inquiries must be listed on the Undisclosed Debt Form and note if new credit was opened or not. FSB does pull a soft pull credit report that will show any new credit, updated balances and new inquires at the end of the underwriting process.

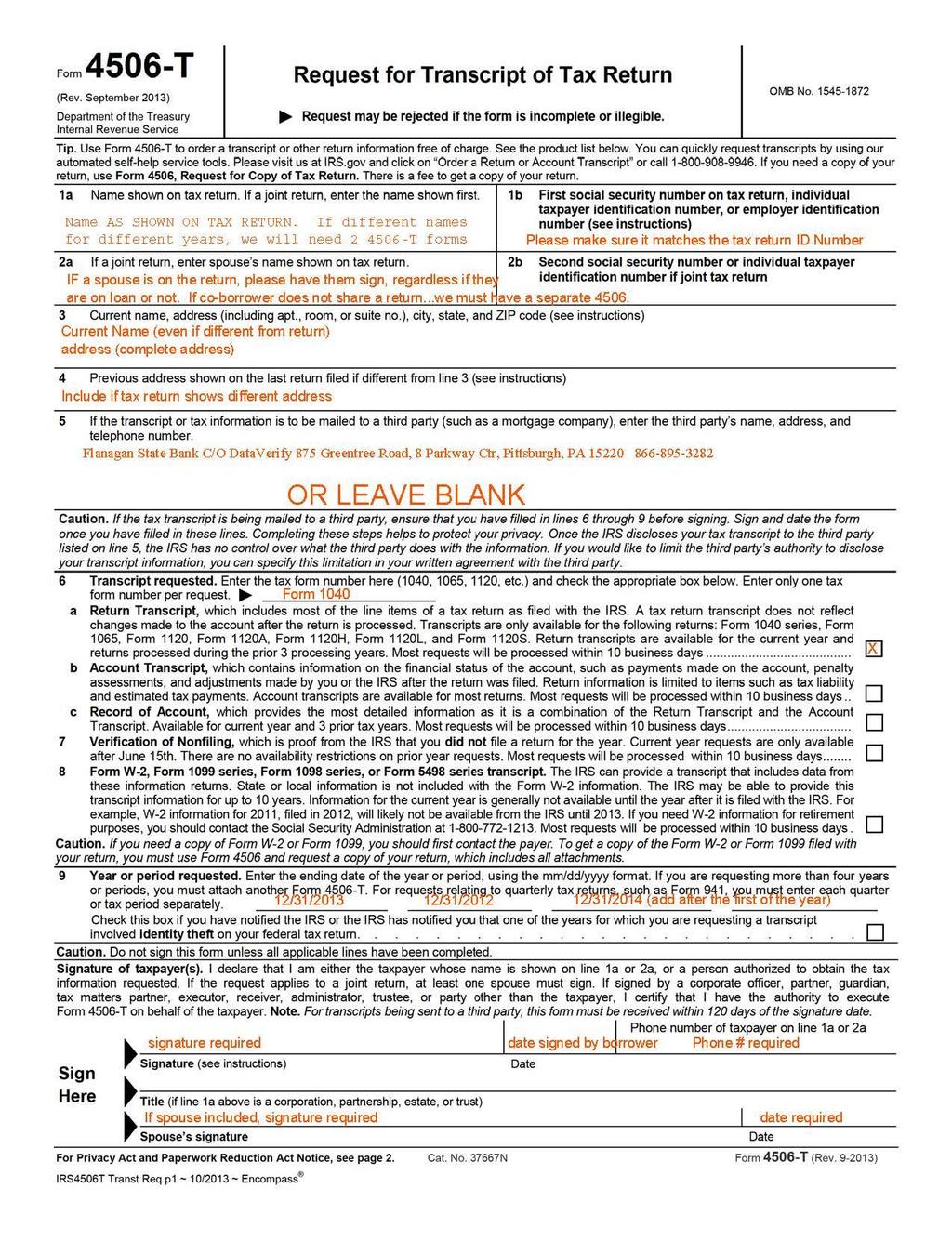

26 The minimum documentation required for submitting a file to underwriting is: All required application disclosures GFE & TIL years W-2 s most recent 30 days most recent paystubs Written VOE if using OT, Bonus, Commission or job time is under 2 years Verbal VOE if straight wage earner income and job time over 2 years Credit Report Purchase contract, if purchase transaction Payoff, if refinance transaction 2 months bank statements or assets statements if other type of asset Letters of explanation for derogatory credit Letter of explanation for rent free as applicable Verification of mortgage/rent added to credit if not showing on the credit Copy of Driver s License must be valid and not expired 4506T fully executed If self employed 2 most recent years of tax returns (personal & business returns with all schedules)

27 HOI Quote or binder VA Certificate of eligibility Notes to underwriter providing details for the file Property info if Condo or PUD condo/pud questionnaire, HOA bylaws, master policies, etc Tax returns for all borrowers of all income types Title commitment with tax info included

28 It is important to note that compliance requires all docs to be included in the loan as required by Federal and State Laws. The list of documents on the next page incorporates all regulations mortgage lenders and brokers currently have to meet to remain compliant. If you ever disagree with our requirements, we just ask that you supply proof that the document in question is not required in your state. To do this, we must have it in writing from your State Regulator.

29 Submission Cover Sheet State Disclosure as applicable for your state Initial 1003 GFE Itemization of Fees/Fees Worksheet to match GFE Intent to Proceed TIL HUD Counseling Disclosure Acknowledgment Servicing Disclosure Notice of Right to Receive Copy of Appraisal Equal Credit Opportunity Act Disclosure Service Provider Form, if State required or if items listed in Section 6 on GFE Notice to Home Loan Applicant Credit Score Info Disclosure (usually final pages of credit report) Risk Based Pricing/Your Credit Score and the Price You Pay For Credit Disclosures notices Undisclosed Debt Acknowledgment Form Copy of Driver s License 4506T form fully completed Mortgage Fraud FBI Form Mortgage Broker Disclosure if applicable Privacy Act Disclosure Flood Disaster Protection Act of 1973 Borrower s Certification & Authorization Fair Credit Reporting Act Patriot Act Disclosure Anti-Steering Disclosure if LPC and must have 3 options completed! Proof of Delivery of HUD Settlement Book Program Specific Disclosures All disclosures are available at or from your Account Executive Team

30 4506T being sent in with form correctly completed FSB will order transcripts immediately upon receipt of file. If the form is not completed correctly it will be rejected by the IRS and cause delays Proper submission of file to underwriting the inclusion of the needed docs for Federal and State are the responsibility of the submitting LO to obtain and insure all dates, figures and amounts match and are correct Telling the Underwriter the story of the file. Please do not leave the underwriter to guess at what needs to be know on the file. Supply a Note To Underwriter outlining what you are trying to accomplish, how you are doing it, what items you are missing, etc. The more information you supply the better your conditions will be. Numerous conditions come from an underwriter trying to piece the file together with limited information. Providing as complete a file as possible for initial underwriting if you need a quick turn around for a closing deadline then we need as full of a file as possible. We can close fast, as long as we have everything we need to do our part. When re-submitting conditions, do not upload one or two and then resub. We want as many conditions as possible to review at one time. Our goal is to touch a file 2 3 times and then be ready for closing. Touching a file more than this slows our process up and will result in delays on our turn times.

31

32 The Corr files will have less compliance conditions on the front end of the underwriting process. The compliance conditions will be noted, but will be required with the closing package Corr files will be responsible for providing: Flood Cert and tax transcripts HOI and Title will be in the name of the Correspondent Funding the loan Reviewing the Purchase Advice Preparing the Allonge and Bailey Letter for closing The Corr will be responsible for delivering the closing package after the closing. The delivery will occur in this manner: The closing package and any outstanding PTF conditions and Compliance Conditions will be uploaded to the file in Mortgagebot to Closing Package. The original Note, Allonge and Bailey Letter will be overnighted or mailed to FSB The closing package (all items) must be received by FSB before we can purchase the loan The rate must be valid through the purchasing of the file.

33 Do Insure that all your dates on your initial disclosures are uniform Make sure the LO signs the 1003 before submission and dates the form correctly Application Dates are: Purchase date property address was obtained. Usually determined by purchase contract. Refinance date should be on or within 3 days of credit report date GFE Prepared Date within 3 days of 1003 blank dates are not allowed LO to sign TIL, 92900A and any other documents that have a signature space for them. Blanks are not acceptable Don t Send in docs with dates that are not within 3 days from application Have multiple dates throughout the forms. Send in a GFE that does not match the fees worksheet and the Details of Transaction on the 1003 Send in a GFE with blanks all must be completed properly Send in a TIL with the recording fee a different amount than what is disclosed on the GFE

34 When reviewing your submitted GFE, we are looking for this information in the Important Dates Section:

35 Insert System Training here!! If you have already had our LOS training, please proceed to the next slide

36 The next few screens will outline how to utilize our Pricing Engine and lock the files.

37 To locate the Scenario Pricing Engine, open Forms & Docs and midway down the menu click on Scenario Pricer. All sections in RED must have information entered to price correctly.

38 Originator Compensation must be entered. Choose one of the following options: Lender Paid Borrower Paid Origination fee: Must be completed to reflect the amount being charged for either LPC or BPC as chosen above The lock information does not carry over to the GFE at this time. If using our system to prepare Initial Docs, please note you will still have to complete the GFE in full. On Correspondent Loans, it is not necessary to choose compensation type.

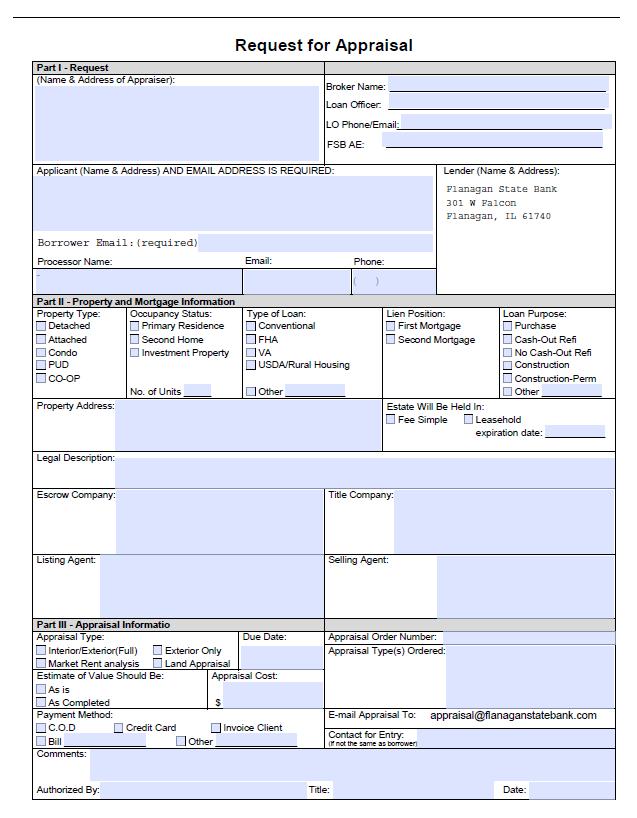

39 Make sure to complete the Credit Information section for accurate pricing! In the same section you will be able to tell us to waive the underwriting/commitment fee. Under credit grade choose UW WAIVER.

40 Once the form is completed appropriately, click on PRODUCT SELECTION at the bottom of the screen. Your pricing options will be shown and you may choose which rate/pricing is best for your loan. All adjustments will show at the bottom. You may choose any of the options from the buttons below the pricing. Please note that you will not be able to choose a rate until you choose the lock button at the bottom.

41 Located two spots down from the Scenario Pricer, this screen is used for when the LO is ready to complete the lock and does not need to price out the loan. Screens are similar to Scenario Pricer All information must be entered to accurately price the loan. Any information needed but not entered will result in pricing not being shown. To waive UW fee, use drop down under Credit Information Credit Grade

42

43 Confirmation will be sent via

44 If your rate expires, you will be charged an extension fee PLUS worst case scenario for the difference, as applicable It is best to not let rates expire and simply extend so as not to have any additional adjustments If your loan will not be closing for whatever reason and it is locked, please cancel your locks with the lock desk A new lock cannot be completed until the current one has expired for 61 days

the FHA case number will be returned to you To request a TRANSFER from another lender to FSB")

45 FHA Case Numbers To request a NEW case number complete the form and to govrequests@flanaganstatebank.com Within a few hours (or less) the FHA case number will be returned to you To request a TRANSFER from another lender to FSB of a case number, you must contact the Lender that holds the case number and provide them with our FHA ID. They will then transfer it to us. To have FSB Transfer a case number to another Lender, complete the Transfer Section of the form and send to govrequests@flanaganstatebank.com The appraisal CANNOT be ordered until the case number is received per FHA guides VA Case Numbers These must be requested through the VA Portal by the submitting company When you request the case number the appraisal is automatically ordered

46 FSB does not maintain any AMC relationships We accept any AMC appraisal, but will not order through the AMC on behalf of our accounts We will maintain a roster for each company and each companies branch allowing them to use local appraisers. There must be a minimum of 3 appraisers on the roster to begin ordering through FSB We do not collect any fees and all appraisal fees are to be paid at closing To order an appraisal, complete the Appraisal Order form located on our website at Leave the Name/Address of the Appraiser BLANK FSB will complete If a purchase order, include purchase contract with the order form and send to appraisal@flanaganstatebank.com If a refi, only the order is needed The appraisal department will confirm receipt of order and acceptance of order by the appraiser. Notes will be maintained in the file on status of appraisal and due date

47

48 Mortgagee Clause for title: Flanagan State Bank ISAOA 333 Chicago Road, PO Box 302 Paw Paw, IL Loan # EPA & COMP endorsements needed 24 month chain of title. Must include the verbiage a 24 month chain of title has been completed CPL Wire Instructions if FSB is funding the loan Property taxes must be noted on title or a tax certificate provided Lender s coverage must match the loan amount Clear title must be provided before closing will occur

49 Currently 24 hour underwriting turn times on all products A conditional approval does not mean that additional conditions will not apply. Although FSB does not wish to consistently add conditions to a loan, it may be necessary as new information is presented in the file for review. It is strongly suggested to present the best possible file at submission to avoid additional conditions as the file progresses. Goal: to touch files no more than 2 3 times before closing the file AE Team will be able to answer majority of your underwriting questions, but you may contact the underwriter via or phone with questions, as well. Please try to keep these to a minimum to allow them to maintain underwriting turn times The duties for underwriting are split up between the Jr Underwriting and Underwriter. The Jr Underwriter reviews all compliance items and provides the compliance conditions The Underwriter completes the Prior to Closing (PTC) and Prior to Funding (PTF) conditions. Questions should be directed to each accordingly

50 Broker Loans The underwriter will provide Final Approval, but the Jr Underwriter actually gives the CTC on the file once all compliance conditions are met The CTC will be sent to the LO or Processor (or both) with a notice to send the completed Closing Request Form to the Closing Department to schedule with them The Closing Department, upon receipt of the Closing Request Form will confirm the closing and date of closing with the sender Closing Instructions are sent out first with instructions for the preparation of the HUD The HUD will be sent back to the assigned closer for review and upon HUD approval, the closing docs will be sent to the title company The wire for the closing is sent 24 hours in advance, or as soon as possible on a closing that is a rush Correspondent Loans Follow above, but wire will be sent by Correspondent If docs are prepared by Corr, they will be responsible for HUD approval

51 Upload closing package to file within 48 hours and advise them the package is uploaded and ready for review. Overnight/Mail original Allonge, Bailey Letter and Note to: Flanagan State Bank 333 Chicago Road, PO Box 302 Paw Paw, IL Att: Correspondent Department Lock must be valid through receipt of the original documents. It is the Correspondent companies responsibility to extend accordingly Review Purchase Advice when sent by Flanagan and confirm accuracy The loan is not considered delivered to FSB until the Note and Allonge are in our possession

52 For both Brokered Loans and Correspondent Loans If our investors request a document that you may have in your file or requires contact with the borrower, we will come back to you for assistance in meeting such a request In all our closing packages, a First Payment Letter is prepared. This contains information needed by the borrower to mail their first payment to us by the due date shown. Often times, this notice is not pointed out by the closers. Please bring this to your borrower s attention so they can make their payment on time and mailed to the correct place. Your borrower will get notification of the transfer of their loan. If you would like to confirm they were notified by the correct company, please contact your Account Executive for this information.

53 Thank you for viewing our training. If you have questions after this training you may or contact your Account Executive Team

USDA Rural Development Mortgage Training

USDA Rural Development Mortgage Training Why use a USDA Loan? 100% Financing of purchase price Can cover closing costs up to appraised value IF property appraises over purchase price Low rates Low Monthly

USDA Rural Development Mortgage Training Why use a USDA Loan? 100% Financing of purchase price Can cover closing costs up to appraised value IF property appraises over purchase price Low rates Low Monthly

Flanagan State Banks Guide to FHA Disclosures

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

GFE/TIL AND COC WORKFLOW

Table of Contents Page 1 of the GFE... 2 Tolerance Levels... 5 Page 2 of the GFE... 7 Box 6 of the GFE... 12 How to Calculate Transfer Tax... 13 Page 3 of the GFE... 14 Events Triggering Re-disclosure...

Table of Contents Page 1 of the GFE... 2 Tolerance Levels... 5 Page 2 of the GFE... 7 Box 6 of the GFE... 12 How to Calculate Transfer Tax... 13 Page 3 of the GFE... 14 Events Triggering Re-disclosure...

***PROVIDE PRELIM HUD FROM TITLE SHOWING THEIR FEE BREAKDOWN***

CCI DOC ORDER FORM INVESTOR: LOAN #: CIRCLE ONE: CONV / FHA / VA / 2ND INVESTOR PROGRAM CODE: CLOSING DATE & TIME: DISBURSEMENT DATE: FIRST PYMT DUE DATE: BASE LOAN AMOUNT: TOTAL LOAN AMT: INTEREST RATE:

CCI DOC ORDER FORM INVESTOR: LOAN #: CIRCLE ONE: CONV / FHA / VA / 2ND INVESTOR PROGRAM CODE: CLOSING DATE & TIME: DISBURSEMENT DATE: FIRST PYMT DUE DATE: BASE LOAN AMOUNT: TOTAL LOAN AMT: INTEREST RATE:

How to do business with MMC under TRID

How to do business with MMC under TRID Rev. 10/27/15 Presented by J.J. Sawicki, CMP AVP of TPO/Merrimack Mortgage Co, LLC Correspondent Lending with Merrimack Mortgage Rev. 9/1/2016 Website - www.mmcitpo.com

How to do business with MMC under TRID Rev. 10/27/15 Presented by J.J. Sawicki, CMP AVP of TPO/Merrimack Mortgage Co, LLC Correspondent Lending with Merrimack Mortgage Rev. 9/1/2016 Website - www.mmcitpo.com

NEW LOAN REGISTRATION PROCESS

1 I N T R O D U C T I O N TO M I C H I G AN M U T U AL S NEW LOAN REGISTRATION PROCESS MIMUTUAL PORTAL PORTAL FEATURES Loan Status s Pipeline Icon Functionality Document Upload Loan Change Requests Appraisal

1 I N T R O D U C T I O N TO M I C H I G AN M U T U AL S NEW LOAN REGISTRATION PROCESS MIMUTUAL PORTAL PORTAL FEATURES Loan Status s Pipeline Icon Functionality Document Upload Loan Change Requests Appraisal

WHOLESALE Good Faith Estimate Compliance Manual

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

TRID (TILA-RESPA ITNEGRATED DISCLOSURE RULE) FAQ

FAQ") TRID (TILA-RESPA ITNEGRATED DISCLOSURE RULE) FAQ This frequently asked questions in this document have been categorized into the following three sections: Loan Estimate Closing Disclosure Miscellaneous

TRID (TILA-RESPA ITNEGRATED DISCLOSURE RULE) FAQ This frequently asked questions in this document have been categorized into the following three sections: Loan Estimate Closing Disclosure Miscellaneous

Processing Checklist:

Processing Checklist: Loan#: Borrower: Processor: AUS Run thru DT Note - Verify Terms Rate/term refi verify P&I pymnt on Note and mtg. statement match to evidence loan not modified. Refer to guidelines

Processing Checklist: Loan#: Borrower: Processor: AUS Run thru DT Note - Verify Terms Rate/term refi verify P&I pymnt on Note and mtg. statement match to evidence loan not modified. Refer to guidelines

Correspondent Lending Client Job Aid

Correspondent Lending Client Job Aid 2 Table of Contents Purpose... 3 Procedures... 3 1. Login... 3 2. Automated Importing of Loan Data... 4 3. Manually Input Loan... 6 4. Product Selection, Submitting

Correspondent Lending Client Job Aid 2 Table of Contents Purpose... 3 Procedures... 3 1. Login... 3 2. Automated Importing of Loan Data... 4 3. Manually Input Loan... 6 4. Product Selection, Submitting

California Homebuyer Fund CHF

California Homebuyer Fund CHF Purchase Primary Residence Loan Type Property Type Max. LTV/CLTV (1) Min. FICO Max DTI FHA VA USDA 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 96.5%

California Homebuyer Fund CHF Purchase Primary Residence Loan Type Property Type Max. LTV/CLTV (1) Min. FICO Max DTI FHA VA USDA 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 96.5%

Loan Originator Workflow. General Overview

Loan Originator Workflow General Overview Responsibilities Obtaining a complete and accurate loan application. Completing all required fields within Point including but not limited to Company or Personal

Loan Originator Workflow General Overview Responsibilities Obtaining a complete and accurate loan application. Completing all required fields within Point including but not limited to Company or Personal

All Credit Reports - All Pages Including Disclosure Credit Inquries Letter and Credit LOE(s) Deposit Explanation Letter(s) Mortgage Statement(s)

Deposit Explanation Letter(s) Mortgage Statement(s)") Borrower(s): Loan Officer: Processor: Investor: Interest Rate: Loan Amount: Broker / Correspondent Conventional / FHA / VA / Jumbo / Reverse Other: Purchase / Refinance Fixed - 30yr, 20yr, 15yr, 10yr Arm

Borrower(s): Loan Officer: Processor: Investor: Interest Rate: Loan Amount: Broker / Correspondent Conventional / FHA / VA / Jumbo / Reverse Other: Purchase / Refinance Fixed - 30yr, 20yr, 15yr, 10yr Arm

USDA STREAMLINE ASSIST

USDA STREAMLINE ASSIST (MUST CURRENTLY BE A USDA LOAN-CANNOT BE DIRECT) Minimum Credit Score Max Loan Amount Balance Appraisal Seasoning Current Mortgage Credit Can GUS be used Net Tangible Benefit Annual

USDA STREAMLINE ASSIST (MUST CURRENTLY BE A USDA LOAN-CANNOT BE DIRECT) Minimum Credit Score Max Loan Amount Balance Appraisal Seasoning Current Mortgage Credit Can GUS be used Net Tangible Benefit Annual

RESPA REFORM TRAINING Effective January 1, FOR MORTGAGE PROFESSIONALS ONLY Rev 1, 12/29/09

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

Accenture Mortgage Cadence. Loan Fulfillment Center. Forms Job Aid

Accenture Mortgage Cadence Loan Fulfillment Center f Table of Contents FORM FORMATS...8 1003 UNIFORM RESIDENTIAL LOAN APPLICATION...9 1008 UNIFORM UNDERWRITING AND TRANSMITTAL SUMMARY... 10 1008 Uniform

Accenture Mortgage Cadence Loan Fulfillment Center f Table of Contents FORM FORMATS...8 1003 UNIFORM RESIDENTIAL LOAN APPLICATION...9 1008 UNIFORM UNDERWRITING AND TRANSMITTAL SUMMARY... 10 1008 Uniform

Correspondent Procedures. rev. 8/3/16

Correspondent Procedures rev. 8/3/16 1 Website www.mmcitpo.com AUS Run Requests Definition of an application Fees Registration/Rate Lock The Loan Estimate Submission Checklists TBDs LE/CD Revision Requests

Correspondent Procedures rev. 8/3/16 1 Website www.mmcitpo.com AUS Run Requests Definition of an application Fees Registration/Rate Lock The Loan Estimate Submission Checklists TBDs LE/CD Revision Requests

Merchants Bank, National Association

Merchants Bank, National Association Encompass TPO WebCenter User Guide Full Document Processing Table of Contents Third Party Origination Website User Guide Getting Started Section 1 Gaining Initial Access

Merchants Bank, National Association Encompass TPO WebCenter User Guide Full Document Processing Table of Contents Third Party Origination Website User Guide Getting Started Section 1 Gaining Initial Access

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

Change in Circumstance. CIC Instructions and Request Form

Change in Circumstance CIC Instructions and Request Form The following pages show in detail how to complete a CIC with First Community Mortgage. These scenarios are for educational use only. This is not

Change in Circumstance CIC Instructions and Request Form The following pages show in detail how to complete a CIC with First Community Mortgage. These scenarios are for educational use only. This is not

Good Faith Estimate Training 2/3/14

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

From: Fowler Williams, CMB President, Crescent Mortgage Company To: Our National Network of Community Lending Partners RE: TRID Policy Update CD 2.

Closing Process Motion TILA RESPA Integrated Disclosure Closing Disclosure 2.0 From: Fowler Williams, CMB President, To: Our National Network of Community Lending Partners RE: TRID Policy Update CD 2.0

Closing Process Motion TILA RESPA Integrated Disclosure Closing Disclosure 2.0 From: Fowler Williams, CMB President, To: Our National Network of Community Lending Partners RE: TRID Policy Update CD 2.0

Origination Submission Guidance

Introduction: In this training material, we explore working with retail loan submissions. We will step by step walk you through the general processes and required procedures. The information contained

Introduction: In this training material, we explore working with retail loan submissions. We will step by step walk you through the general processes and required procedures. The information contained

National Homebuyers Fund With Second Mortgage Investor 38 Retail Only

National Homebuyers Fund With Second Mortgage Investor 38 Retail Only This program is temporarily suspended. New lock requests will not be accepted effective 6/22/15. Revisions Date Revisions 3/11/15 Updated

National Homebuyers Fund With Second Mortgage Investor 38 Retail Only This program is temporarily suspended. New lock requests will not be accepted effective 6/22/15. Revisions Date Revisions 3/11/15 Updated

All Credit Reports - All Pages Including Disclosure Credit Inquries Letter and Credit LOE(s) Deposit Explanation Letter(s) Mortgage Statement(s)

Deposit Explanation Letter(s) Mortgage Statement(s)") Borrower(s): Loan Officer: Processor: Investor: Interest Rate: Loan Amount: Broker / Correspondent Conventional / FHA / VA / Jumbo / Reverse Other: Purchase / Refinance Fixed - 30yr, 20yr, 15yr, 10yr Arm

Borrower(s): Loan Officer: Processor: Investor: Interest Rate: Loan Amount: Broker / Correspondent Conventional / FHA / VA / Jumbo / Reverse Other: Purchase / Refinance Fixed - 30yr, 20yr, 15yr, 10yr Arm

Home Equity Line of Credit

Home Equity Line of Credit PRIMARY RESIDENCE 1 PURCHASE, RATE/TERM REFINANCE & CASH-OUT REFINANCE Property Type 1 to 2-Unit Warrantable Condo PUD Maximum CLTV Maximum Line Amount Minimum Credit Score Total

Home Equity Line of Credit PRIMARY RESIDENCE 1 PURCHASE, RATE/TERM REFINANCE & CASH-OUT REFINANCE Property Type 1 to 2-Unit Warrantable Condo PUD Maximum CLTV Maximum Line Amount Minimum Credit Score Total

Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents

![Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents](/thumbs/94/118687243.jpg "Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents") Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING...

Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING...

A1 Mortgage Processing Services, Inc., Contract Processing Agreement

A1 Mortgage Processing Services, Inc., Contract Processing Agreement This agreement is made and entered into this day of,, by and between (Broker name), hereinafter referred to as "the Broker", and A1

A1 Mortgage Processing Services, Inc., Contract Processing Agreement This agreement is made and entered into this day of,, by and between (Broker name), hereinafter referred to as "the Broker", and A1

Alert / Messages Matrix

Alert HPML Needs Impounds This is an HPML Loan and requires impounds. Either reduce the APR below the HPML threshold or add impounds. This is an HPML Loan and requires impounds. Either reduce the APR below

Alert HPML Needs Impounds This is an HPML Loan and requires impounds. Either reduce the APR below the HPML threshold or add impounds. This is an HPML Loan and requires impounds. Either reduce the APR below

APMC DU REFI PLUS MATRIX

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. FINAL FUNDING DATE Conventional Conforming Fixed Rate DU Version 9.1 LTV

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. FINAL FUNDING DATE Conventional Conforming Fixed Rate DU Version 9.1 LTV

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program BORROWER NAME(S): HMFA Loan # Smart Start Loan # Address: City State Zip Code Lender Name:

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program BORROWER NAME(S): HMFA Loan # Smart Start Loan # Address: City State Zip Code Lender Name:

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name: Required Items

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name: Required Items

Section 1 Pricing Policies and Procedures

Section 1 Pricing Policies and Procedures For quicker navigation, click on Bookmarks Tab on the top left of the PDF. Pricing Policies and Procedures Loans with borrower FICO Scores below 680 will not be

Section 1 Pricing Policies and Procedures For quicker navigation, click on Bookmarks Tab on the top left of the PDF. Pricing Policies and Procedures Loans with borrower FICO Scores below 680 will not be

AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist

Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist") Applicant Information AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist Loan Request: $ Loan Purpose: Purchase - Sales Price: $ Refinance

Applicant Information AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist Loan Request: $ Loan Purpose: Purchase - Sales Price: $ Refinance

HOW TO SUBMIT A USDA, RD GUARANTEED ORIGINATION PURCHASE OR REFINANCE FILE TO GEORGIA

GA SFH Guaranteed Loan Program From the Georgia State Office Single Family Housing Guaranteed Loan Program September 21, 2012 HOW TO SUBMIT A USDA, RD GUARANTEED ORIGINATION PURCHASE OR REFINANCE FILE

GA SFH Guaranteed Loan Program From the Georgia State Office Single Family Housing Guaranteed Loan Program September 21, 2012 HOW TO SUBMIT A USDA, RD GUARANTEED ORIGINATION PURCHASE OR REFINANCE FILE

Processing Overview I

2/14/2017 Introduction: In this training material and supplemental training exercises, we explore the items necessary to open a loan. We will step by step walk you through the general processes and required

2/14/2017 Introduction: In this training material and supplemental training exercises, we explore the items necessary to open a loan. We will step by step walk you through the general processes and required

Single Family Housing Guaranteed Loan Program Quick Reference

Single Family Housing Guaranteed Loan Program Quick Reference Topic 7 CFR 3555 HB-1-3555 7 CFR Part 3555 Appendix 1 A Abandoned or Vacant Property 3555.302 19.2 A Account Acceleration 3555.306 18.6 Acceptable

Single Family Housing Guaranteed Loan Program Quick Reference Topic 7 CFR 3555 HB-1-3555 7 CFR Part 3555 Appendix 1 A Abandoned or Vacant Property 3555.302 19.2 A Account Acceleration 3555.306 18.6 Acceptable

CREATE FILE IN BLITZDOCS

1. Log-into BlitzDocs CREATE FILE IN BLITZDOCS All loan submissions must be submitted through BlitzDocs. In order to obtain a user name and password, a BlitzDocs Audit Checklist form must be completed

1. Log-into BlitzDocs CREATE FILE IN BLITZDOCS All loan submissions must be submitted through BlitzDocs. In order to obtain a user name and password, a BlitzDocs Audit Checklist form must be completed

ACHIEVE YOUR AMERICAN DREAM WITH AMERICAN LENDING!

Green - Doctors Program Guidelines Property Type 1-Unit Warrantable Condo PUD PRIMARY RESIDENCE - PURCHASE & RATE.TERM REFINANCE Minimum LTV 80.01% 80.01% 80.01% Maximum LTV/CLTV/HCLTV 97% 95% 90% Minimum

Green - Doctors Program Guidelines Property Type 1-Unit Warrantable Condo PUD PRIMARY RESIDENCE - PURCHASE & RATE.TERM REFINANCE Minimum LTV 80.01% 80.01% 80.01% Maximum LTV/CLTV/HCLTV 97% 95% 90% Minimum

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE CASH-OUT REFINANCE SECOND HOME PURCHASE AND RATE/TERM REFINANCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T ***Wholesale Use Only*** Proof of 4506 Tax Audit Ordered (highly recommend fully processed

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T ***Wholesale Use Only*** Proof of 4506 Tax Audit Ordered (highly recommend fully processed

Streamline Assist Refinance Product

Streamline Assist Refinance Product Credit Policy 09/06/2016 DISCLAIMER USDA has provided VERY LITTLE information as to their exact documentation requirements on this new product. Therefore, we ve done

Streamline Assist Refinance Product Credit Policy 09/06/2016 DISCLAIMER USDA has provided VERY LITTLE information as to their exact documentation requirements on this new product. Therefore, we ve done

March 12, 2018 Closing and Quality Review - MRB

March 12, 2018 Closing and Quality Review - MRB Investing in quality housing solutions. KHC Program Guide MRB Closing and Quality Review March 12, 2018 Down payment Assistance Programs (DAPs) Effective

March 12, 2018 Closing and Quality Review - MRB Investing in quality housing solutions. KHC Program Guide MRB Closing and Quality Review March 12, 2018 Down payment Assistance Programs (DAPs) Effective

Program Qualifications

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328

1. TITLE POLICY DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328 [ ] Short form title policies with proper ALTA

1. TITLE POLICY DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328 [ ] Short form title policies with proper ALTA

ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. PRODUCT CODES ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. PRODUCT CODES ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1

Section 5 UNDERWRITING REQUIREMENTS 5.1 GENERAL

Section 5 UNDERWRITING REQUIREMENTS 5.1 GENERAL Huntington underwrites Broker transactions prior to closing/loan purchase. We provide the Broker with a loan approval, which lists any conditions of our

Section 5 UNDERWRITING REQUIREMENTS 5.1 GENERAL Huntington underwrites Broker transactions prior to closing/loan purchase. We provide the Broker with a loan approval, which lists any conditions of our

APMC DU REFI PLUS MATRIX

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. FINAL FUNDING DATE Conventional Conforming Fixed Rate DU Version 9.3 LTV

1. PRODUCT DESCRIPTION 2. EXISTING FIRST MORTGAGE ELIGIBILITY 3. FINAL FUNDING DATE Conventional Conforming Fixed Rate DU Version 9.3 LTV

September 6, 2017 Closing and Quality Review - Secondary Market Programs

September 6, 2017 Closing and Quality Review - Secondary Market Programs Investing in quality housing solutions. KHC Program Guide Secondary Market Closing and Quality Review September 6, 2017 Changes/Additions

September 6, 2017 Closing and Quality Review - Secondary Market Programs Investing in quality housing solutions. KHC Program Guide Secondary Market Closing and Quality Review September 6, 2017 Changes/Additions

Prior to Closing Wholesale

Closing Section 5 Prior to Closing Wholesale ------------------------------------------------------------ 5.2 Closing the Loan Wholesale ---------------------------------------------------------- 5.2 Title

Closing Section 5 Prior to Closing Wholesale ------------------------------------------------------------ 5.2 Closing the Loan Wholesale ---------------------------------------------------------- 5.2 Title

FHA Changes Effective for Case Numbers on or after 9/14/15

FHA Changes Effective for Case Numbers on or after 9/14/15 Topic Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Earnest Money Assets Not clear about requiring donor s bank statement

FHA Changes Effective for Case Numbers on or after 9/14/15 Topic Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Earnest Money Assets Not clear about requiring donor s bank statement

FHA Processing Checklist

FHA Processing Checklist DU/LP Findings PLEASE NOTE: AT THIS TIME, FHA ARMS ARE NOT AVAILABLE DUE TO RECENT FHA MI CHANGES. FHA ARM s ARE NOW CLASSIFIED AS HPMLS. Read DU Findings thoroughly and document

FHA Processing Checklist DU/LP Findings PLEASE NOTE: AT THIS TIME, FHA ARMS ARE NOT AVAILABLE DUE TO RECENT FHA MI CHANGES. FHA ARM s ARE NOW CLASSIFIED AS HPMLS. Read DU Findings thoroughly and document

SECTION 8 DOWNPAYMENT ASSISTANCE PROGRAM

SECTION 8 DOWNPAYMENT ASSISTANCE PROGRAM 8.1 Qualification of Participating Lenders 8.2 Funds Availability 8.3 Eligibility 8.4 Computation of DAP Loan Amounts 8.5 Application Processing 8.6 Loan Preparation

SECTION 8 DOWNPAYMENT ASSISTANCE PROGRAM 8.1 Qualification of Participating Lenders 8.2 Funds Availability 8.3 Eligibility 8.4 Computation of DAP Loan Amounts 8.5 Application Processing 8.6 Loan Preparation

Processing FHA TOTAL Mortgages

Introduction This reference contains information to help you process Federal Housing Administration (FHA) mortgages using Freddie Mac Loan Product Advisor SM, including information on data entry requirements,

Introduction This reference contains information to help you process Federal Housing Administration (FHA) mortgages using Freddie Mac Loan Product Advisor SM, including information on data entry requirements,

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix The information in this matrix is provided as a tool to help you document Federal Housing Administration (FHA) mortgages. The matrix

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix The information in this matrix is provided as a tool to help you document Federal Housing Administration (FHA) mortgages. The matrix

ORIGINATING AGENTS GUIDE REVISION 105. October 05, 2015

Ralph M. Perrey, Executive Director ORIGINATING AGENTS GUIDE REVISION 105 October 05, 2015 Remove and discard: Replace with enclosed: Page iii (Revised 09/22/15)... Page iii (Revised 10/05/15) Page 24

Ralph M. Perrey, Executive Director ORIGINATING AGENTS GUIDE REVISION 105 October 05, 2015 Remove and discard: Replace with enclosed: Page iii (Revised 09/22/15)... Page iii (Revised 10/05/15) Page 24

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS. Mortgage Planner Marketing

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS Mortgage Planner Marketing Qualified & Formal Approval Becoming qualified is the first step. This means having your debt ratios and credit report

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS Mortgage Planner Marketing Qualified & Formal Approval Becoming qualified is the first step. This means having your debt ratios and credit report

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

10/23/17. Chenoa Fund Program

10/23/17 Chenoa Fund Program Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official statements of PRMG

10/23/17 Chenoa Fund Program Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official statements of PRMG

5/1 ARM 1 ; 7/1 or 10/1 ARM 2 Must exceed Conforming Standard and High Balance Limit for State/County %/40% 80%* 80%* $2,000,000 1

Conventional Jumbo Loan Program The Conventional Jumbo Loan program can be used to provide financing options for Primary Residences with jumbo loan amounts in excess of Conventional High-Balance limits.

Conventional Jumbo Loan Program The Conventional Jumbo Loan program can be used to provide financing options for Primary Residences with jumbo loan amounts in excess of Conventional High-Balance limits.

Idaho Housing and Finance Association Reference Guide

Reference Guide Servicing CHFA Loan Types: FHA, VA and USDA Service Released Lenders only HFA Preferred TM - All Lenders / HFA Advantage - Eligible Lenders Conventional loans that are uninsured All Lenders

Reference Guide Servicing CHFA Loan Types: FHA, VA and USDA Service Released Lenders only HFA Preferred TM - All Lenders / HFA Advantage - Eligible Lenders Conventional loans that are uninsured All Lenders

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

# Required? Form ID: Doc Name: Copy? Special Instructions: In Sub? 1 ALL HMFA 100 ALL Purchase Submission Cover Sheet.

HMFA Seller s Guide can be found on our website at www.njhousing.gov In Sub? # Required? Form ID: Doc Name:? Special Instructions: 1 ALL HMFA 100 ALL Purchase Submission Cover Sheet HMFA -100 2 ALL Note

HMFA Seller s Guide can be found on our website at www.njhousing.gov In Sub? # Required? Form ID: Doc Name:? Special Instructions: 1 ALL HMFA 100 ALL Purchase Submission Cover Sheet HMFA -100 2 ALL Note

Completing the 4506-T For Ordering of Tax Transcripts using Partners (formerly Old Republic)

") The turn-around times by the IRS can vary for a variety of reasons that include time of year and their operating budget. Ordering transcripts before you submit the borrower s credit package to Flanagan

The turn-around times by the IRS can vary for a variety of reasons that include time of year and their operating budget. Ordering transcripts before you submit the borrower s credit package to Flanagan

HUNTINGTON PORTFOLIO Fixed and Adjustable Rate Conforming and Non-Conforming Products INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs

PRODUCTS: 15 yr Fixed Rate INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs CODE: Conforming & Non-Conforming 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 10/01/2016 PRODUCT CRITERIA 1) PRODUCT

PRODUCTS: 15 yr Fixed Rate INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs CODE: Conforming & Non-Conforming 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 10/01/2016 PRODUCT CRITERIA 1) PRODUCT

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist Homeward Bound Borrower Name(s):

:") New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist Homeward Bound Borrower Name(s): HMFA Homeward Bound Loan Number: SS / Homeseeker # Delivery packages are to be sent

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist Homeward Bound Borrower Name(s): HMFA Homeward Bound Loan Number: SS / Homeseeker # Delivery packages are to be sent

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Utah Fee Agreement (Only required on properties located in Utah) Utah Servicing Disclosure (Only required

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Utah Fee Agreement (Only required on properties located in Utah) Utah Servicing Disclosure (Only required

Non-Conforming Initial Loan Submission Checklist Exhibit 6 1/9/2018

Wells Fargo Funding Loan information Wells Fargo Funding Loan number (required): Borrower name: Subject property address: Contact information for file Company name: Contact for this file: Phone number:

Wells Fargo Funding Loan information Wells Fargo Funding Loan number (required): Borrower name: Subject property address: Contact information for file Company name: Contact for this file: Phone number:

AFR JUMBO OVERVIEW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

National Correspondent Division Lender Guide

FREQUENTLY ASKED QUESTIONS Q) What is the minimum net worth requirement for becoming a NewRez Lender? A) The minimum net worth requirement for NewRez is $500,000 for Non-Delegated and $1,500,000 for Delegated

FREQUENTLY ASKED QUESTIONS Q) What is the minimum net worth requirement for becoming a NewRez Lender? A) The minimum net worth requirement for NewRez is $500,000 for Non-Delegated and $1,500,000 for Delegated

Borrower Signature Authorization

Borrower Signature Authorization Privacy Act Notice: This information is to be used by the agency collecting it or its assignees in determining whether you qualify as a prospective mortgagor under its

Borrower Signature Authorization Privacy Act Notice: This information is to be used by the agency collecting it or its assignees in determining whether you qualify as a prospective mortgagor under its

MINIMUM MORTGAGE: None

LOAN PROGRAM DESCRIPTION:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 3 AGE OF DOCUMENTS:... 3 APPLICATION REQUIREMENTS:...

LOAN PROGRAM DESCRIPTION:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 3 AGE OF DOCUMENTS:... 3 APPLICATION REQUIREMENTS:...

BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 11/10/2017

PRODUCTS: 15yr Fixed Rate, 1/1, 3/1, 5/1, 7/1, 10/1 & 15/1 ARMs INVESTOR CODE: 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 11/10/2017 PRODUCT CRITERIA 1) PRODUCT BENEFITS: Available to medical

PRODUCTS: 15yr Fixed Rate, 1/1, 3/1, 5/1, 7/1, 10/1 & 15/1 ARMs INVESTOR CODE: 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 11/10/2017 PRODUCT CRITERIA 1) PRODUCT BENEFITS: Available to medical

Wholesale Quick Start Guide. Import Loan. Validate Agents & Loan Information

Wholesale Quick Start Guide 2510 Red Hill Ave. Santa Ana, CA 92705 949-390-2688 l www.jmaclending.com Import Loan Validate Agents & Loan Information 1. Click Create New Loan 2. Click Import loan file 3.

Wholesale Quick Start Guide 2510 Red Hill Ave. Santa Ana, CA 92705 949-390-2688 l www.jmaclending.com Import Loan Validate Agents & Loan Information 1. Click Create New Loan 2. Click Import loan file 3.

RESP RE A SP A & & Good Good Fa F ith ith Estima tima e R quir quir d e d Disclosure Disclosur s Corresponden Corr esponden t Lending July 22, 2013

RESPA & Good Faith Estimate Required Disclosures Correspondent Lending July 22, 2013 What s Different and When is it Effective? January 1, 2010 (1003 dated on or after) New GFE form: does not indicate

RESPA & Good Faith Estimate Required Disclosures Correspondent Lending July 22, 2013 What s Different and When is it Effective? January 1, 2010 (1003 dated on or after) New GFE form: does not indicate

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage 0% Downpayment Assistance Program

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage 0% Downpayment Assistance Program

Instructions for Completing the Uniform Residential Loan Application Fannie Mae 1003 / Freddie Mac 65

Instructions for Completing the Uniform Residential Loan Application Fannie Mae 1003 / Freddie Mac 65 Completed Applications should be returned to: First Federal 118 NE Third Street PO Box 239 McMinnville,

Instructions for Completing the Uniform Residential Loan Application Fannie Mae 1003 / Freddie Mac 65 Completed Applications should be returned to: First Federal 118 NE Third Street PO Box 239 McMinnville,

FHA Product Overview. Product and Underwriting Guidelines. U.S. Bank Home Mortgage Wholesale Division CAT CR U.S.

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

Lender Letter LL

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

MORTGAGE QUICK START GUIDE

MORTGAGE QUICK START GUIDE Contents Our Solutions page 2 Tips and Terms to Know page 3-4 The Mortgage Process: Step by Step page 5 How to Submit Your Mortgage Application page 6 Pre-Qualification Application

MORTGAGE QUICK START GUIDE Contents Our Solutions page 2 Tips and Terms to Know page 3-4 The Mortgage Process: Step by Step page 5 How to Submit Your Mortgage Application page 6 Pre-Qualification Application

Oklahoma County Home Finance Authority Turnkey Mortgage Origination Program

Oklahoma County Home Finance Authority Turnkey Mortgage Origination Program Administrator Guideline Published - January 4, 2013 Revised 10-12-13 Revisions are shown on Page 3 OCHFA Turnkey Mortgage Origination

Oklahoma County Home Finance Authority Turnkey Mortgage Origination Program Administrator Guideline Published - January 4, 2013 Revised 10-12-13 Revisions are shown on Page 3 OCHFA Turnkey Mortgage Origination

Dream Big Jumbo Is Now Available The Smart Series is live! Check page 2 for more info. Check out our enhaned conventional LPMI pricing.

Effective Fri 02/23/2018 10:20 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Fri 02/23/2018 10:20 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Dream Big Jumbo Is Now Available

Effective Tue 04/10/2018 9:54 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Tue 04/10/2018 9:54 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

HOW THE CALDWELL QC PLAN MEETS HUD REQUIREMENTS

Q-5 How the Caldwell QC Plan Meets HUD Requirements HOW THE CALDWELL QC PLAN MEETS HUD REQUIREMENTS Every FHA-approved mortgage lender, including loan correspondents, must implement a written quality control

Q-5 How the Caldwell QC Plan Meets HUD Requirements HOW THE CALDWELL QC PLAN MEETS HUD REQUIREMENTS Every FHA-approved mortgage lender, including loan correspondents, must implement a written quality control

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME 4 REASONS WHY YOU SHOULD CHOOSE PPG UPFRONT UNDERWRITING And pre-approvals! This reduces your stress when buying a home. EASY MOBILE APPLICATION We keep

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME 4 REASONS WHY YOU SHOULD CHOOSE PPG UPFRONT UNDERWRITING And pre-approvals! This reduces your stress when buying a home. EASY MOBILE APPLICATION We keep

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Opportunity Down Payment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Opportunity Down Payment Assistance Program can

CRA PORTFOLIO NON-CONFORMING PROGRAM

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

USDA Guaranteed Rural Housing Product Profile

USDA Guaranteed Rural Housing Product Profile PROGRAM CODES: 30RH Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 620 100%* 620 *exclusive

USDA Guaranteed Rural Housing Product Profile PROGRAM CODES: 30RH Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 620 100%* 620 *exclusive

FHA Underwriting Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015 September 14, 2015

September 14, 2015 Assets Gift Funds Documenting Transfer Earnest Money Not clear about requiring donor s bank statement in all instances. Document source of funds if amount exceeds 2% of sales price or

September 14, 2015 Assets Gift Funds Documenting Transfer Earnest Money Not clear about requiring donor s bank statement in all instances. Document source of funds if amount exceeds 2% of sales price or

Delaware State Housing Authority. Homeownership Loan Programs Lender Training

Delaware State Housing Authority Homeownership Loan Programs Lender Training DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

Delaware State Housing Authority Homeownership Loan Programs Lender Training DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

USDA Guaranteed Rural Housing Product Profile

Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 640 100%* 640 *exclusive of financed guarantee fee A full appraisal (e.g. form 1004 or

Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 640 100%* 640 *exclusive of financed guarantee fee A full appraisal (e.g. form 1004 or

FHA Underwriting Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015

Topic Assets Interested Party Credits / Costs Paid Outside Closing / Minimum Required Investment (MRI) Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Not clear about requiring

Topic Assets Interested Party Credits / Costs Paid Outside Closing / Minimum Required Investment (MRI) Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Not clear about requiring

"MCC HANDBOOK" A Summary and Quick Reference Guide For MCC Processors

"MCC HANDBOOK" A Summary and Quick Reference Guide For MCC Processors PART 1 BASIC PROGRAM INFORMATION... 3 1. Eligibility Guidelines...3 Targeted Census Tracts...3 First Time Home Buyer...3 Citizenship...4

"MCC HANDBOOK" A Summary and Quick Reference Guide For MCC Processors PART 1 BASIC PROGRAM INFORMATION... 3 1. Eligibility Guidelines...3 Targeted Census Tracts...3 First Time Home Buyer...3 Citizenship...4

OPEN MORTGAGE. October 22, 2015

OPEN MORTGAGE October 22, 2015 Borrower Eligibility All occupying Borrowers 18 years or older and Non- Purchasing Spouse must be a first-time homebuyer Household income is within NIFA s Income limit Purchase

OPEN MORTGAGE October 22, 2015 Borrower Eligibility All occupying Borrowers 18 years or older and Non- Purchasing Spouse must be a first-time homebuyer Household income is within NIFA s Income limit Purchase

TCF HELOCs. Combined 1 CLTV

TCF HELOCs MiMutual works directly with TCF to be able to offer simultaneous secondary financing in the form of a HELOC. These are not permitted to be submitted through the correspondent channel they must

TCF HELOCs MiMutual works directly with TCF to be able to offer simultaneous secondary financing in the form of a HELOC. These are not permitted to be submitted through the correspondent channel they must

Idaho Housing and Finance Association Reference Guide

Reference Guide Servicing CHFA Loan Types: FHA, VA and USDA Service Released Lenders only HFA Preferred TM - All Lenders / HFA Advantage - Eligible Lenders Conventional loans that are uninsured All Lenders

Reference Guide Servicing CHFA Loan Types: FHA, VA and USDA Service Released Lenders only HFA Preferred TM - All Lenders / HFA Advantage - Eligible Lenders Conventional loans that are uninsured All Lenders

Non Delegated Correspondent Seller Guide Section 1 Seller Eligibility & Warehouse Bank Policy

Table of Contents Seller Guide Section 1 Purpose and Scope... 2 Seller Approval Requirements... 2 Non Delegated Underwriting Authority... 3 Documentation Requirements... 4 Correspondent Due Diligence...

Table of Contents Seller Guide Section 1 Purpose and Scope... 2 Seller Approval Requirements... 2 Non Delegated Underwriting Authority... 3 Documentation Requirements... 4 Correspondent Due Diligence...

FIXED RATE (30 & 15)

") Page 1 of 19 FIXED RATE (30 & 15) PRIMARY RESIDENCE Purchase & Rate/Term Refinance PROPERTY TYPE LTVCLTV/HCLTV LOAN AMOUNT 1 FICO 2 MAX DTI UNDW OPTIONS 3 1 unit (SFR,Condos,PUDs) Cash/Out Refinance 4

Page 1 of 19 FIXED RATE (30 & 15) PRIMARY RESIDENCE Purchase & Rate/Term Refinance PROPERTY TYPE LTVCLTV/HCLTV LOAN AMOUNT 1 FICO 2 MAX DTI UNDW OPTIONS 3 1 unit (SFR,Condos,PUDs) Cash/Out Refinance 4

FNMA HomePath Product Guidelines

April 15, 2013 FNMA HomePath Product Guidelines Standard Conforming Occupancy Primary Residence Max LTV Max TLTV Max CLTV 1 Unit 97 97 97 2 Unit 80 80 80 3-4 Unit 75 75 75 Second Home 1 Unit 90 90 90 Investment

April 15, 2013 FNMA HomePath Product Guidelines Standard Conforming Occupancy Primary Residence Max LTV Max TLTV Max CLTV 1 Unit 97 97 97 2 Unit 80 80 80 3-4 Unit 75 75 75 Second Home 1 Unit 90 90 90 Investment