Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility

|

|

|

- Percival Walsh

- 5 years ago

- Views:

Transcription

1

2 Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips for calculating a USDA loan amount Tips for preparing a USDA GFE Provide USDA helpful resources

3 USDA Rural Development s Single Family Housing Guaranteed Loan Program is intended to assist low to moderate income, rural homebuyers 100% financing for a home purchase, or refinancing, for properties located in a USDA designated rural area Applicant s may have up to 115% of the median income for the area Guaranteed by the US Department of Agriculture (USDA)

4 Key program highlights include: Maximum loan amount up to appraised value plus a one time Guarantee Fee of 2% on purchases No Mortgage Insurance required No cash contribution (down payment) or cash reserve requirement Primary residences only Not limited to first time homebuyers Low to moderate income buyers

5 Appraisal required? Loans eligible for refinancing Purchase/Non-Streamlined Refinance Streamlined Refinance Pilot Program Yes -Full appraisal (Completed by FHA roster appraiser on purchase) Section 502 Direct or Guaranteed Loan (no conventional, FHA, VA) No Guaranteed Loan only (no USDA 502 Direct, conventional, FHA, VA) Yes exterior only Section 502 Direct or Guaranteed Loan (no conventional, FHA, VA) Do income limits apply? Yes Yes Yes Is property required to be in rural area? Does property have to be a primary residence Eligible states Purchase Yes Refinance No. If property was eligible at origination it is eligible for refinance even if no longer in rural area as defined by USDA No - If property was eligible at origination it is eligible for refinance even if no longer in rural area as defined by USDA No- If property was eligible at origination it is eligible for refinance even if no longer in rural area as defined by USDA Yes Yes Yes All Except Massachusetts All Except Massachusetts Limited to: AK, AL, AR, AZ, CA, CO, FL, GA, ID, IL, IN, KS, KY, MI, MO, MS, MT, NC, ND, NJ, NM, NV, OH, OK, OR, RI, SC, SD, TN, TX, UT, WA, WI, WV Credit report required? Yes - Full Yes - Full Yes - Mortgage only on subject property Mortgage History/ Seasoning Interest rate and loan term DTI Purchase - > 680 credit score, not required month housing history required Refinance 0x30 in previous 12 months Minimum of 6 months payment history on current mortgage for the subject property Fixed rate - 30 years Maximum 45% regardless of GUS findings 0x30 in previous 12 months - Minimum of 6 months payment history on the current mortgage for the subject property. Fixed rate - 30 years 29%/41% On an exception basis max 32%/44% subject to: Rural Development approval. Additionally, all borrowers must have 680 credit score and meet compensating factor requirement* 0x30 in previous 12 months - 12 months of payments on the current mortgage secured by the subject property required Fixed rate: Must be a minimum of 1% below the borrower s current interest rate; 30 year loan term Not applicable debt ratios not calculated

6 Purchase/Non-Streamlined Refinance Streamlined Refinance Pilot Program What may be included in new loan amount? Closing costs and lender fees Cash-out allowed? (Principal reduction required if cash back > borrower out of pocket money) Principal balance plus guarantee fee, accrued interest (refis), eligible closing costs, and lender fees may be included if including if including does not exceed 100% LTV (if financing guarantee fee 102% LTV allowed) Normal and customary allowed Principal balance plus guarantee fee only No accrued interests, closing costs, etc. may be included in the new loan amount Normal and customary allowed Principal balance plus accrued interest, eligible closing costs, lender fees, guarantee fee, plus origination fee not to exceed the lesser of 2% of the loan amount or $3,000 Normal and customary allowed but may not exceed the cost paid by the lender or charged to the lender by the service provider No No No Manual Underwriting No Yes Yes Is adding/deleting borrowers allowed? Refinance Yes New borrowers may be added and existing borrowers may be deleted however one existing borrower must remain on the loan and title. Yes New borrowers may ne added and existing borrowers may be deleted however one existing borrower must remain on the loan and title. Yes New Borrowers may be added however existing borrowers may not be removed unless they are deceased. Termite/Septic/Well required Purchase Well always required. Termite/septic if appraiser indicates issue Refinance - No No No Reserves Not required Not required Not required

7 Non-Streamlined Refinance Benefits Streamlined Refinance Benefits Pilot Program Benefits Direct 502 and Guaranteed loans may be refinanced New loan amount may include accrued interest, guarantee fee and closing costs if including does not exceed appraised value. New borrowers may be removed (as long as one original borrower remains on the loan/title). Eligible in all states except Massachusetts Guaranteed loans may be refinanced No appraisal required New borrowers may be added and existing borrowers may be removed (as long as one original borrower remains on the loan/title) Eligible in all states except Massachusetts Direct 502 and Guaranteed loans may be refinanced 2055 exterior-only appraisal Mortgage-only credit report Debt ratios not calculated New loan amount may include principal balance plus guarantee fee, accrued interest, eligible closing costs, and lender fees. Additionally, an origination fee, not to exceed 1% of the loan amount may also be charged. NOTE: Pilot Refinances do not have a DTI calculation but do require income documentation be provided to determine income eligibility

8 Rural Development has a maximum rate that can be charged The maximum rate is based on the 90 day Fannie Mae 30 year A/A Yield basis points and rounded up to the next ¼% Example: Fannie Mae 90 day 30 year fixed rate A/A = 4.72% Add 60 basis points Total 5.72% Rounded up to next ¼% 5.75% Maximum rate = 5.75% Fannie Mae rates can be found at:

9 The first step in qualifying a potential USDA applicant is determining Borrower, Property and Income eligibility: Subject property not a part of or associated with an urban area Area population is generally less than 20,000 Income cannot exceed 115% of the HUD median income limit for the area Income based on number of people occupying the property as their primary residence Income includes total gross income of applicant, co-applicant and other household adults

10 To qualify for USDA, the borrower must: Earn adequate and dependable income Provide proof of residency as a U.S. Citizen, Legal Permanent Resident or Non-Permanent Resident Alien Meet income eligibility requirements Live in a USDA eligible area Have a valid social security number; TIN not acceptable Not require a co-signer or non-occupant co-borrower

11 Borrower may retain only ONE dwelling in addition to the new property financed Property to be retained must be: Deemed unsafe or unsound or requires significant retrofitting to accommodate the disability/limited mobility of a household member No longer adequate size for family

12 Property eligibility for purchase transactions: Use the Single Family Housing property eligibility search on the USDA website Properties must be located in a rural area as defined by USDA to be eligible for this program. Enter the property address and confirm the property is located in an eligible area: Note on Refinances: If property was eligible at origination, it is eligible for refinance if even if it is no longer in a USDA rural area.

13 Eligible Property Types: 1- unit single family reside 1-unit PUD Project review not required Condo Must meet Fannie Mae, HUD or VA guidelines and be common to area Purchases in non-approved projects will require a full review Planet Home Lending will require supporting documents to ensure project meets Fannie Mae requirements and the Planet Home Lending Condo/PUD Warranty Form is required Modular New Construction

14 Ineligible Property Types: Income producing properties or working farms 2-4 units Properties with buildings or equipment for specific income producing purposes or large farm service buildings Properties with windmills, wind turbines, or cell phone towers Manufactured Second/vacation homes

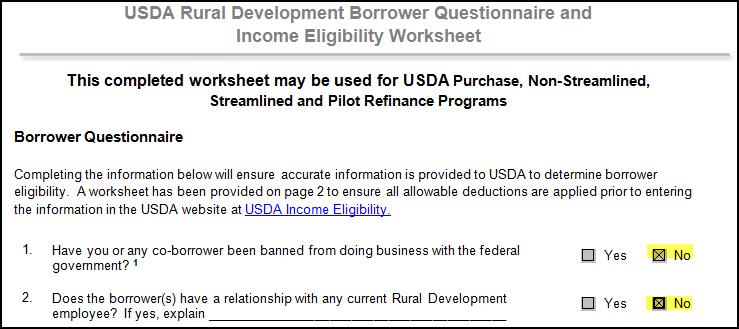

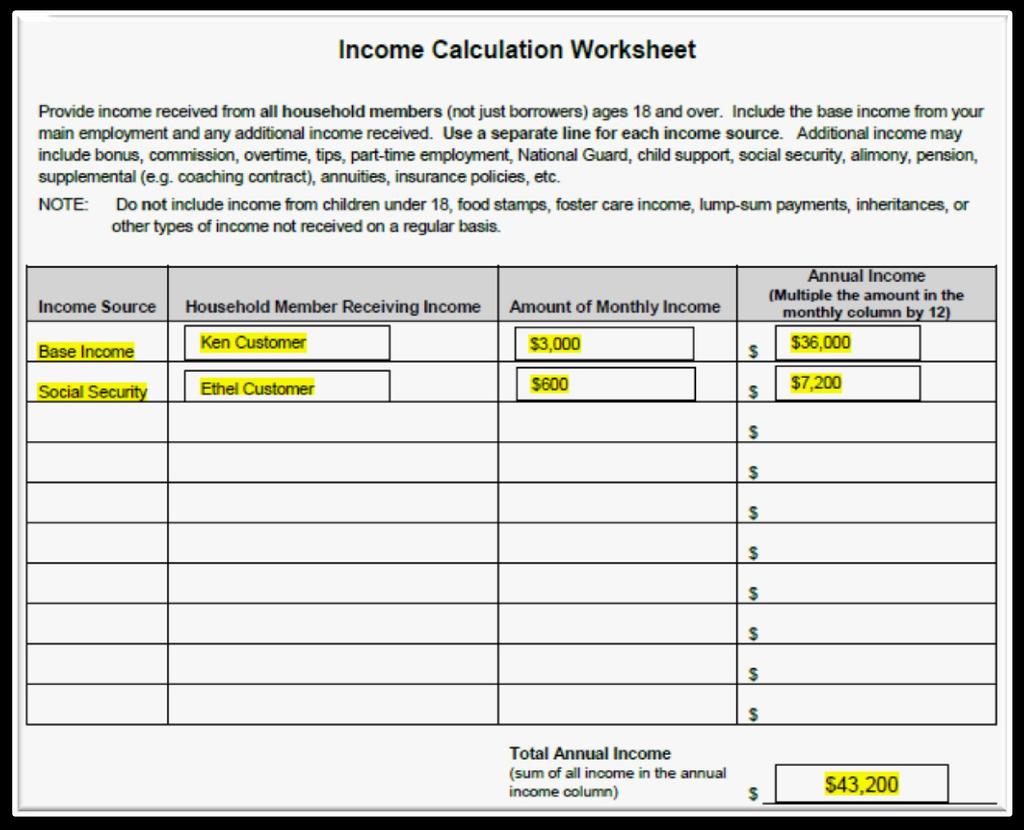

15 There are 3 distinct income calculations that must be considered for income eligibility: 1. Annual Income (Household Income): All income received by adult household members that will reside in our subject property 2. Adjusted Annual Income: Annual Income minus eligible household deductions, determines whether the household is eligible 3. Repayment Income (Qualifying Income): The stable and dependable income utilized to calculate housing and total debt ratios. Only the applicants that will be a party to the note are considered. A sample Questionnaire and Income Eligibility Worksheet can be found at:

16 To calculate Annual Income add the gross income amount of all adult household members (18 years old and up) and projected income from all sources for the next 12 months: Example Income Types Include: Gross income from taxable sources Interest/Dividend income Rental Income Social Security/Unemployment/Disability Alimony/Child Support Income on any net family assets in excess of $5,000 after closing Note: This calculation projects the income that the adult household will potentially earn in the next 12 months

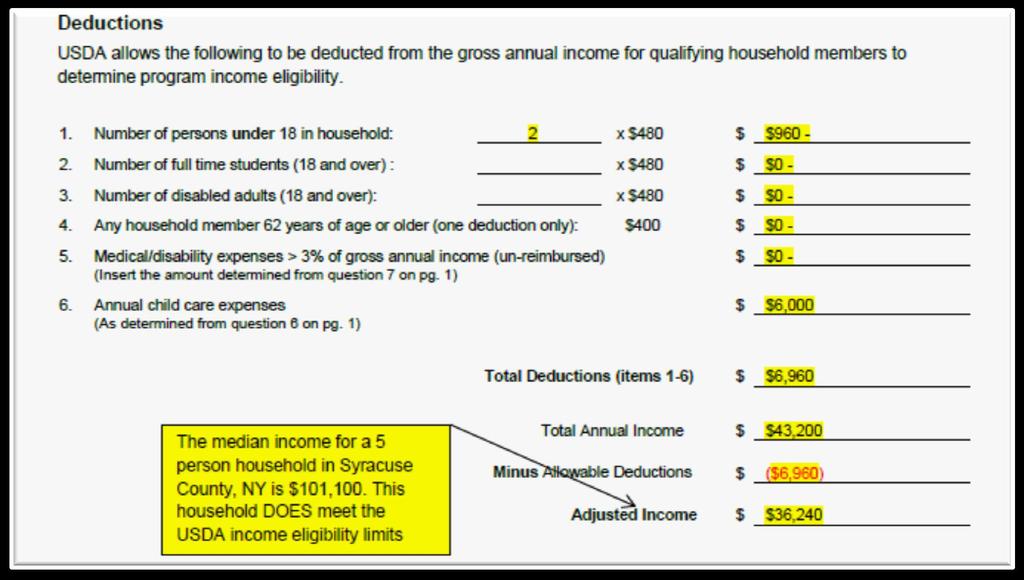

17 To calculate Adjusted Income deduct the following from the Annual Income amount: Deduct $480 for each person who is: Under 18 Disabled and is 18 or over A full-time student who is 18 or older Deduct a flat $400 for an applicant, 62 years or older, and is: Head-of-Household Spouse Sole household member NOTE: One time deduction; not per person

18 If the applicant is eligible for the flat $400 deduction, described in the previous slide, the family is classified an Elderly Family Family - See USDA HB for additional options in classifying Elderly/Disabled Family Deduct Medical and Disability expenses in excess of 3% of gross annual income for an Elderly or Disabled Family: Projected medical expenses for ensuing 12 months Costs not covered by insurance Reasonable attendant care Equipment to enable handicapped household member Deduct child care expenses for minors 12 years and under: Enables the applicant to be employed or educated (i.e. child care) Cannot exceed the amount of income received from applicant's employment Payments (i.e., childcare) cannot be made to any dependent of applicant

19 Cannot exceed the limit set by Rural Development for the state/county where the property is located The final adjusted income must be < 115% of the area median Deductions assist the applicant s ability to qualify Non-applicant household member s most recent paystub showing current YTD will be used for Annual Income Calculation For non-wage earners, alternative documentation may be required

20

21

22 Page 1 footnotes regarding eligibility

23

24

25 To calculate Repayment Income (Qualifying Income), include the gross amounts of income that is stable and dependable for all applicants: Document a history of receipt and assurance of continuance Wage Earner: Current paystubs for previous 30 days with YTD income + Previous 2 Years W-2s Self Employed: 2 years tax returns + YTD P & L + Balance Sheet + YTD Income & Expense Statement Repayment income is used to calculate DTI ratios Income documentation must be < 120 day from the Note date Note on Pilot Program: Reduced income documentation is required for eligibility but DTI is NOT calculated

26 Once the three income types have been calculated, income eligibility can be determined. Income Eligibility: Use the Income Eligibility search on the USDA website: Choose the state and county that the subject property is located in:

")

27 Complete Household Member(s) Information:

28 Complete all fields that apply for Deductions and Income: Tip: Click the question mark symbol for field definitions

29 Confirm income is Eligible for the 502 Guaranteed Rural Housing Loan:

30 Credit reports must be < 120 days from the Note date Minimum 640 FICO required on all USDA programs

31 Any of the following are indicators of an unacceptable credit history per Rural Development: More than one 30 day late within the past 12 months (refinance transactions require 0x30 on mortgage) Bankruptcy or foreclosure that occurred within the past 3 years Outstanding tax liens or delinquent government debt Outstanding judgments within the past 12 months Any account converted to a collection in past 12 months Outstanding collections accounts with no satisfactory payment arrangements Any account written or charged off in past 3 years Applicants with a foreclosure on a previous RD loan are ineligible Note: Pilot Refinance will consider mortgage history on subject only

32 Installment debt with10 months or less omitted from DTI Revolving debts with no payment listed on credit Use greater of $10.00 or 5% of balance reported on credit used Child Support/Alimony/Garnishments are included in DTI 401K loans not included in DTI Deferred student loans must be included in DTI regardless of deferment period. Refer to USDA Program guides for requirements Note: Pilot Refinance is exempt from these requirements as a mortgage only history is analyzed on subject property

33 All federal debts and judgments must be paid in full or otherwise resolved with supportive documentation CAIVRS identifies any delinquent federal debts CAIVRS claims must have official documentation that the delinquency has been paid in full or otherwise resolved

34 USDA HPML Loans will be restricted to 43% DTI on all products Debt of non-purchasing spouse included in DTI when applicant lives in a community property state or property is located in a community property state Maximum DTI: Purchase/Non-Streamlined Refi: 45% regardless of GUS Findings Streamlined Refi: 29%/41%. Exceptions may be granted to 32%/44% (refer to guidelines for requirements for exceptions) Pilot Program: DTI not calculated

35 Purchases: Always required regardless of down payment Used to qualify conventional finance testing Refinances: Required when funds are needed to close Documentation: 2 months bank statements dated within 45 days of application date Checking/Savings Sale proceeds from an owned property 401k/Retirement accounts at 60% of vested account balance Stocks and Bond Asset documentation must be < 120 days from the Note date

36 Gift funds allowed for closing costs or may be applied to Guarantee Fee or towards voluntary down payment on purchases May not be used towards cash reserves as a compensating factor May not come from a household member Transfer of gift funds and donor s ability must be documented

37 The Conventional Finance Test: Borrowers must lack the ability to qualify for conventional purchase financing to be eligible for USDA financing If an applicant meets all six criteria below, they are considered eligible for conventional financing: 20% down in available liquid assets, excluding retirement Additional funds after down payment are available to pay for closing costs and fees Applicant is not required to obtain private mortgage insurance DTI does not exceed 28/36 with a loan amount at 20% down No adverse credit, prohibiting conventional financing Acceptable credit history length and tradelines

38 First Time Homebuyer Education Rural Development may require the applicant to complete homebuyer education counseling as part of the conditional commitment Planet Home Lending will only require this when required by Rural Development Requirement is based on local practice for individual USDA offices Seller Contributions Allowed up to 6% Eligible for closing costs, down payment, or repairs

39 Payment Shock Payment shock is considered a risk layer when: DTI > 29% and New PITI is > 100% of applicant s current housing payment or The applicant does not have a housing payment history To calculate payment shock: Proposed PITI current housing 1 x 100 = Payment Shock Percent Loans where payment shock is a risk layer are acceptable if there are no additional risk layers and strong, documented compensating factors are evident (cash reserves, credit score > 680, potential for increased earnings, etc.)

40 Appraisal report type varies by product: Purchase/Non-Streamlined Refi: Full appraisal required Streamlined Refi: No appraisal required Pilot Refinance: 2055 Exterior-only Appraisal must be 120 days old at loan closing and must include a Market Condition Addendum (Fannie Mae Form 1004MC) A 30 day extension of the appraisal is allowed per USDA guidelines. The appraisal with an extension must be 150 days from the effective date of the appraisal at loan closing (120 days + 30 day extension) Purchases/Non-Streamlined Refinances only: Appraisal transfers are allowed

41 Termite inspections: Only required when purchase contract requires one or there is evidence of infestation Well inspections: Required on purchase transactions Septic inspections: Only required if defects noted by appraiser Escrow Holdbacks are not permitted Value of the lot cannot exceed 30% of appraised value

42 There is a non-refundable up front Guarantee Fee on USDA loans The Guarantee Fee can be: Paid in cash Paid by seller, lender credit or gift funds Financed in to the loan amount Partially financed into the loan amount The Guarantee Fee is 2% of the total loan amount for: Refinances Purchases

43 Purchase & Non-Streamlined Refinance New loan amount can include: - Upfront Guarantee Fee - Eligible closings costs* - Lender fees* - Accrued interest (refis)* *Not to exceed 100% of the appraised value Streamlined Refinance New loan amount can include: - Principal balance on existing loan - Upfront Guarantee Fee Maximum loan amount cannot exceed existing balance on loan being refinanced Pilot Program Refinance New loan amount can include: - Principal balance on existing loan - Accrued interest - Upfront Guarantee Fee - Eligible closing costs - Lender fees - Origination fee of the < 2% of total loan amount or $3,000 (Borrower & Lender paid) Note: Maximum LTV is 102% when financing the 2% Guarantee Fee

44 Example #1: Purchase Financing USDA s Guarantee Fee Purchase Price $250,000 Appraised Value $258,000 Applicant wants to finance $8,000 in closing costs in the loan since appraised value is higher than the purchase price Base Loan Amount $258, Total Loan Amount $263, Subtract Base Loan Amount ($258,000) Guarantee Fee $5, LTV is 102% after up front Guarantee Fee is included

45 Example #2: Non-Streamlined Refinance Financing USDA s Guarantee Fee Appraised Value $175,000 Principal balance on existing loan $172,000 Applicant wants to finance $3,000 in closing costs and accrued interest since appraised value is higher than the principal balance Base Loan Amount $175, Total Loan Amount = $178, Subtract Base Loan Amount ($175,000) Guarantee Fee = $3, LTV is 102% after up front Guarantee Fee is included

46 Example #3: Streamlined Refinance Financing USDA s Guarantee Fee Appraised Value is $300,000 Principal of existing loan $255,000 This product does not allow for financing closing costs or accrued interest Base Loan Amount $255, Total Loan Amount $260, Subtract Base Loan Amount ($255,000) Guarantee Fee $5, LTV is 87% after up front Guarantee Fee is included

47 Example #4: Pilot Program Refinance, Borrower Paid Compensation Financing USDA s Guarantee Fee Appraised Value is $185,000 Principal of existing loan $174,000 Applicant wants to finance up to $7,000 in closing costs and accrued interest in addition to the principal balance Closing costs and accrued interest, including a 1% origination are $4,000 Base Loan Amount $178, Total Loan Amount $181,633 Subtract Base Loan Amount ($178,000) Guarantee Fee $3, LTV is 98% after up front Guarantee Fee is included

48 There is an annual fee that is collected on all USDA loans Collected in the borrowers monthly payment Similar to how monthly mortgage insurance is collected Required for the life of the loan Purchase and Refinances = 0.50% The annual fee is based upon the unpaid principal balance The fee is re-calculated every year Example: Loan Amount = $175,000 Loan Amount X.004 = $ annually $ months = $58.33 monthly fee

49 Guaranteed Underwriting System (GUS) GUS recommendation Accept/Eligible or Refer/Eligible on Purchase, and Non-Streamlined Refinances NOTE: Refer/Eligible requires a manual underwrite and compensating factors; refer to guidelines Calculates adjusted income Checks property eligibility Rates credit and debt profile Calculates base and maximum loan amounts Runs CAIVRS check Seller runs at time of initial underwrite when applicable Findings are no cost to borrower

50 Borrower cannot receive any cash back at closing Out of pocket money with supporting documentation allowed Examples: Earnest deposit, appraisal fee Principal reductions are required to avoid cash back at closing Maximum Principal Reduction amount is 1% of loan amount Escrows are required Insurance: Required coverage is on loan amount only for loans where appraisal not required, or 2055/2075 when cost new section is not completed (i.e. Streamlined and Pilot Refis) POAs are eligible on an exception basis for closing docs only All applicants must sign initial disclosures and application Verbal verification of employment within 10 days of Note date

51 The most current information for USDA (guides and forms) can be found at: Property eligibility: Income eligibility: The Planet Home Lending USDA guidelines have active links to USDA property/income eligibility and guideline pages

52

USDA Guaranteed Rural Housing Product Profile

USDA Guaranteed Rural Housing Product Profile PROGRAM CODES: 30RH Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 620 100%* 620 *exclusive

USDA Guaranteed Rural Housing Product Profile PROGRAM CODES: 30RH Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 620 100%* 620 *exclusive

USDA Guaranteed Rural Housing Product Profile

Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 640 100%* 640 *exclusive of financed guarantee fee A full appraisal (e.g. form 1004 or

Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 640 100%* 640 *exclusive of financed guarantee fee A full appraisal (e.g. form 1004 or

PRODUCT GUIDELINES USDA PROGRAM PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE. Revised 10/1/ % / 100% Excluding USDA

PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE Maximum LTV/CLTV* Max Loan Amount Min FICO Max Ratios 100% / 100% Excluding USDA 620 Per GUS** Determined by qualifying ratios and county maximum income

PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE Maximum LTV/CLTV* Max Loan Amount Min FICO Max Ratios 100% / 100% Excluding USDA 620 Per GUS** Determined by qualifying ratios and county maximum income

Product Guidelines USDA STREAMLINED ASSIST REFINANCE

REFINANCE Maximum LTV Max Loan Amount Min FICO Max Ratios Mortgage/Rental History Based on Loan Amount - No LTV Restriction Determined by county maximum limits and payoff amount No Minimum NA 0 x 30 last

REFINANCE Maximum LTV Max Loan Amount Min FICO Max Ratios Mortgage/Rental History Based on Loan Amount - No LTV Restriction Determined by county maximum limits and payoff amount No Minimum NA 0 x 30 last

USDA Guidelines GUSDA30

USDA Guidelines GUSDA30 BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all inclusive of different situations that may arise

USDA Guidelines GUSDA30 BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all inclusive of different situations that may arise

LOANS MUST BE RUN THROUGH GUS*

AmeriSave USDA USDA 30 Rural Housing 30 year Fixed Only *ALL LOANS MUST BE RUN THROUGH GUS* Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $453,100 US Citizens n-occupant

AmeriSave USDA USDA 30 Rural Housing 30 year Fixed Only *ALL LOANS MUST BE RUN THROUGH GUS* Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $453,100 US Citizens n-occupant

AmeriSave Wholesale USDA Effective Date: February 2017 USDA 30 Rural Housing 30 Year Fixed Only

AmeriSave Wholesale USDA Effective Date: February 2017 Product Term: USDA 30 Rural Housing 30 Year Fixed Only Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $424,100

AmeriSave Wholesale USDA Effective Date: February 2017 Product Term: USDA 30 Rural Housing 30 Year Fixed Only Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $424,100

Program Qualifications

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

Rural Housing Refinances

Rural Housing Refinances Rev. 11/16/2016 Presented by J.J. Sawicki, CMP/ AVP of Training and Development at Merrimack Mortgage Rural Housing Refinance Programs If you have originated an RD loan in the

Rural Housing Refinances Rev. 11/16/2016 Presented by J.J. Sawicki, CMP/ AVP of Training and Development at Merrimack Mortgage Rural Housing Refinance Programs If you have originated an RD loan in the

FULL DOC. PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO. Owner Occupied (O/O) 1 unit 80% 80% unit (see MI section below) 95% 95% 700

1 unit 80% 80% unit (see MI section below) 95% 95% 700") FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

Product Guidelines USDA Matrix (Guidelines Based on Updated USDA Handbook Effective 12/01/14) PROGRAM CODES: U30F, UH30F Version 4.

PROGRAM CODES: U30F, UH30F Version 4.") PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE Maximum LTV/CLTV* Max Loan Amount Min FICO Max Ratios Mortgage/Rental History 100% / 100% Excluding USDA Guarantee Fee Determined by qualifying ratios and

PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE Maximum LTV/CLTV* Max Loan Amount Min FICO Max Ratios Mortgage/Rental History 100% / 100% Excluding USDA Guarantee Fee Determined by qualifying ratios and

PREMIUM: JUMBO TIER 2 PROGRAM

PREMIUM: JUMBO TIER 2 PROGRAM Introduction: This program is intended for borrowers with good credit and higher documented liabilities, when the Debt to Income ratio (DTI) can be allowed up to 50%. Program

PREMIUM: JUMBO TIER 2 PROGRAM Introduction: This program is intended for borrowers with good credit and higher documented liabilities, when the Debt to Income ratio (DTI) can be allowed up to 50%. Program

Guaranteed Rural Housing Program Guide

Guaranteed Rural Housing Program Guide Please refer to www.swmc.com/swmc/disclaimer.php and www.nmlsconsumeraccess.org/entitydetails.aspx/company/3277 to see where Sun West Mortgage Company, Inc. (NMLS

Guaranteed Rural Housing Program Guide Please refer to www.swmc.com/swmc/disclaimer.php and www.nmlsconsumeraccess.org/entitydetails.aspx/company/3277 to see where Sun West Mortgage Company, Inc. (NMLS

5/1 ARM 1 ; 7/1 or 10/1 ARM 2 Must exceed Conforming Standard and High Balance Limit for State/County %/40% 80%* 80%* $2,000,000 1

Conventional Jumbo Loan Program The Conventional Jumbo Loan program can be used to provide financing options for Primary Residences with jumbo loan amounts in excess of Conventional High-Balance limits.

Conventional Jumbo Loan Program The Conventional Jumbo Loan program can be used to provide financing options for Primary Residences with jumbo loan amounts in excess of Conventional High-Balance limits.

USDA Rural Development Single Family Guaranteed Rural Housing Program Purchase and Non-Streamlined Refinance

USDA Rural Development Single Family Guaranteed Rural Housing Program Purchase and Non-Streamlined Refinance Fixed Rate Primary Residence Full Documentation Transaction Type Units LTV Credit Score Purchase

USDA Rural Development Single Family Guaranteed Rural Housing Program Purchase and Non-Streamlined Refinance Fixed Rate Primary Residence Full Documentation Transaction Type Units LTV Credit Score Purchase

The Chase Guaranteed Rural Housing Purchase Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

USDA Standard Product Guidelines

Min Max DTI Max Loan Occupancy Credit Ratio Amount CONFORMING & HIGH BALANCE Transaction Type Max LTV Max CLTV Mortgage Rating Purchase 100%** 100% 0x30 for 12 mos prior to application date*** Based on

Min Max DTI Max Loan Occupancy Credit Ratio Amount CONFORMING & HIGH BALANCE Transaction Type Max LTV Max CLTV Mortgage Rating Purchase 100%** 100% 0x30 for 12 mos prior to application date*** Based on

USDA STREAMLINE ASSIST

USDA STREAMLINE ASSIST (MUST CURRENTLY BE A USDA LOAN-CANNOT BE DIRECT) Minimum Credit Score Max Loan Amount Balance Appraisal Seasoning Current Mortgage Credit Can GUS be used Net Tangible Benefit Annual

USDA STREAMLINE ASSIST (MUST CURRENTLY BE A USDA LOAN-CANNOT BE DIRECT) Minimum Credit Score Max Loan Amount Balance Appraisal Seasoning Current Mortgage Credit Can GUS be used Net Tangible Benefit Annual

Premium Jumbo Fixed & 10/1 ARM

Last Update 11/29/2017 Primary (Purchase & Rate/Term NO MI OPTION) Primary (Purchase) Primary (Rate/Term Ref.) Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV

Last Update 11/29/2017 Primary (Purchase & Rate/Term NO MI OPTION) Primary (Purchase) Primary (Rate/Term Ref.) Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV

Mortgage Services III, L.L.C.

(Bank & Credit Union Partners Only) Market conditions are generally: (compared to previous price sheet) Slightly Worse! December 8, 2017 Rate Sheet Updated as of: CONFORMING -- FIXED RATE PROGRAMS #300000-30

(Bank & Credit Union Partners Only) Market conditions are generally: (compared to previous price sheet) Slightly Worse! December 8, 2017 Rate Sheet Updated as of: CONFORMING -- FIXED RATE PROGRAMS #300000-30

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Mortgage Services III, L.L.C.

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

The 2017 Economic Outlook Summit

The 2017 Economic Outlook Summit Southeast Fairfax Development Corporation Mount Vernon-Lee Chamber of Commerce Frank Nothaft, CoreLogic SVP & Chief Economist April 6, 2017 2017 Market: Less Affordability

The 2017 Economic Outlook Summit Southeast Fairfax Development Corporation Mount Vernon-Lee Chamber of Commerce Frank Nothaft, CoreLogic SVP & Chief Economist April 6, 2017 2017 Market: Less Affordability

Mortgage Services III, L.L.C.

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

First Time Homebuyers

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

PennyMac USDA Guaranteed Rural Housing Product Profile

PennyMac USDA Guaranteed Rural Housing Product Profile 01.18.18 Clients must be specifically approved by PennyMac to deliver Rural Housing Mortgages. Contact your Account Manager for Rural Housing approval

PennyMac USDA Guaranteed Rural Housing Product Profile 01.18.18 Clients must be specifically approved by PennyMac to deliver Rural Housing Mortgages. Contact your Account Manager for Rural Housing approval

Premium Jumbo 7/1 & 5/1 ARM

Premium Jumbo 7/1 & 5/1 ARM Program Codes: PJ 7/1 & PJ 5/1 ARM Purchase and Rate/Term Refinance Primary (Purchase) Primary (Rate/Term Ref.) Max Loan Amt Max LTV/CLTV Min Fico DTI Reserves Max Loan Amt

Premium Jumbo 7/1 & 5/1 ARM Program Codes: PJ 7/1 & PJ 5/1 ARM Purchase and Rate/Term Refinance Primary (Purchase) Primary (Rate/Term Ref.) Max Loan Amt Max LTV/CLTV Min Fico DTI Reserves Max Loan Amt

Mortgage Services III, L.L.C.

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz Bloomington Office Ph. #: 888-664-9108

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz Bloomington Office Ph. #: 888-664-9108

FHLMC Only Conforming and Maximum DTI is the more restrictive of Loan Product Advisor or 50%.

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

Correspondent Lending FHA Fixed Rate

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Fannie Mae 2012 Second-Quarter Credit Supplement. August 8, 2012

Fannie Mae 2012 Second-Quarter Credit Supplement August 8, 2012 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

Fannie Mae 2012 Second-Quarter Credit Supplement August 8, 2012 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

USDA HB REVISIONS Effective March 9, 2016 Chapter 5: Origination and Underwriting Review

Chapter 5: Origination and Underwriting Review 5.2 Requesting a Guarantee A. Preliminary Determination of Applicant Eligibility 2. Credit 5.3 Utilizing the Guaranteed Underwriting System (GUS) E. Reserves

Chapter 5: Origination and Underwriting Review 5.2 Requesting a Guarantee A. Preliminary Determination of Applicant Eligibility 2. Credit 5.3 Utilizing the Guaranteed Underwriting System (GUS) E. Reserves

USDA30 PRODUCT MATRIX USDA GUIDELINES RURAL DEVELOPMENT HB HANDBOOK

USDA GUIDELINES RURAL DEVELOPMENT HB-1-3555 HANDBOOK Posted PROGRAM MISSION USDA RURAL HOUSING PBM-Manual -Quick Look Manual-Affordable Housing Programs -USDA Guidelines PROGRAM BENEFITS USDA Guaranteed

USDA GUIDELINES RURAL DEVELOPMENT HB-1-3555 HANDBOOK Posted PROGRAM MISSION USDA RURAL HOUSING PBM-Manual -Quick Look Manual-Affordable Housing Programs -USDA Guidelines PROGRAM BENEFITS USDA Guaranteed

Fannie Mae 2014 Second Quarter Credit Supplement. August 7, 2014

Fannie Mae Second Quarter Credit Supplement August 7, This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for the quarter

Fannie Mae Second Quarter Credit Supplement August 7, This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for the quarter

CROSS INDEX RD Builder's Warranty RD Plan Certification Guaranteed Rural Housing Lender Record Change form

1924-19 RD Builder's Warranty 177 1924-25 RD Plan Certification 179 1980-11 Guaranteed Rural Housing Lender Record Change form 78 1980-17 Loan Note Guarantee form 76 1980-19 Guaranteed Loan Closing Report

1924-19 RD Builder's Warranty 177 1924-25 RD Plan Certification 179 1980-11 Guaranteed Rural Housing Lender Record Change form 78 1980-17 Loan Note Guarantee form 76 1980-19 Guaranteed Loan Closing Report

TCF HELOCs. Combined 1 CLTV

TCF HELOCs MiMutual works directly with TCF to be able to offer simultaneous secondary financing in the form of a HELOC. These are not permitted to be submitted through the correspondent channel they must

TCF HELOCs MiMutual works directly with TCF to be able to offer simultaneous secondary financing in the form of a HELOC. These are not permitted to be submitted through the correspondent channel they must

Guideline Reference Applies to ALL Products

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

MAGNOLIA BANK CORRESPONDENT FUNDING RURAL DEVELOPMENT PRODUCT SUMMARY

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

Enhance Your Financial Security. With a Home Equity Conversion Mortgage

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

FNMA Home Affordable Refinance Program (HARP) Transaction Type Number of Units Fixed Rate Max LTV/CLTV

Transaction Type Number of Units Fixed Rate Max LTV/CLTV") FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families.

VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families. 100% financing on purchase and refinance transactions No down payment required on loan

VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families. 100% financing on purchase and refinance transactions No down payment required on loan

Purchase: Conventional, FHA, USDA, VA. Refinance: Conventional, FHA, USDA, VA. Emerging Banker

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

Underwriting Guideline Matrix

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 12/18/2017 Copyright 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 12/18/2017 Copyright 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage

Fannie Mae 2009 First Quarter Credit Supplement. May 8, 2009

Fannie Mae 2009 First Quarter Credit Supplement May 8, 2009 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2009 First Quarter Credit Supplement May 8, 2009 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

FHA Underwriting Changes. Effective for case numbers issued on and after September 14, 2015

FHA Underwriting Changes Effective for case numbers issued on and after September 14, 2015 Today s Presentation Overview of the most substantial changes to the FHA single family handbook. Not realistic

FHA Underwriting Changes Effective for case numbers issued on and after September 14, 2015 Today s Presentation Overview of the most substantial changes to the FHA single family handbook. Not realistic

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE CASH-OUT REFINANCE SECOND HOME PURCHASE AND RATE/TERM REFINANCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Conventional and Government Program Overlays

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

FHA FIXED PROGRAM HIGHLIGHTS

Product Summary These guidelines represent the companies underwriting requirements for FHA fixed rate and ARM mortgages, and are to be utilized in conjunction with the following FHA Handbooks: 4155.1 for

Product Summary These guidelines represent the companies underwriting requirements for FHA fixed rate and ARM mortgages, and are to be utilized in conjunction with the following FHA Handbooks: 4155.1 for

Core Seconds S Year Fixed S Year Fixed

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Underwriting Methods 3 Documentation Requirements 3 Transaction Types 3 Eligible Property Types, Ineligible Property

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Underwriting Methods 3 Documentation Requirements 3 Transaction Types 3 Eligible Property Types, Ineligible Property

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Purchase: Conventional, FHA, USDA, VA. Refinance: Conventional, FHA, USDA, VA. Emerging Banker

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

FHA Product Overview. Product and Underwriting Guidelines. U.S. Bank Home Mortgage Wholesale Division CAT CR U.S.

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

Fannie Mae (DU) Conventional Loan Matrix

Conventional Loan Matrix") PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

FIXED RATE (30 & 15)

") Page 1 of 19 FIXED RATE (30 & 15) PRIMARY RESIDENCE Purchase & Rate/Term Refinance PROPERTY TYPE LTVCLTV/HCLTV LOAN AMOUNT 1 FICO 2 MAX DTI UNDW OPTIONS 3 1 unit (SFR,Condos,PUDs) Cash/Out Refinance 4

Page 1 of 19 FIXED RATE (30 & 15) PRIMARY RESIDENCE Purchase & Rate/Term Refinance PROPERTY TYPE LTVCLTV/HCLTV LOAN AMOUNT 1 FICO 2 MAX DTI UNDW OPTIONS 3 1 unit (SFR,Condos,PUDs) Cash/Out Refinance 4

FHA CREDIT QUALIFYING STREAMLINE REFINANCE

Table of Contents 1. Eligible Mortgage Product-Existing Loan... 2 2. FICO... 2 3. Eligible Mortgage Product-New Loan... 2 4. Maximium Loan Amount... 2 5. Maximium LTV/CLTV... 2 6. MIP Requirements..2-4

Table of Contents 1. Eligible Mortgage Product-Existing Loan... 2 2. FICO... 2 3. Eligible Mortgage Product-New Loan... 2 4. Maximium Loan Amount... 2 5. Maximium LTV/CLTV... 2 6. MIP Requirements..2-4

Expanded Prime Matrix

Expanded Prime Matrix Program Max LTVs Primary and Second Homes Program Requirements Alternative Doc Enhanced Debt Ratio Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum

Expanded Prime Matrix Program Max LTVs Primary and Second Homes Program Requirements Alternative Doc Enhanced Debt Ratio Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum

USDA PROGRAMS PRODUCT MATRIX

OCCUPANCY LTV UNITS CLTV STANDARD PORTFOLIO FICO REQUIREMENTS Purchase O/O 100% 1 1 100% 1 620 Rate and Term O/O 100% 1 1 100% 1 620 Rural Streamlined-Assist O/O N/A 1 N/A 620 1 Exclusive of Guarantee

OCCUPANCY LTV UNITS CLTV STANDARD PORTFOLIO FICO REQUIREMENTS Purchase O/O 100% 1 1 100% 1 620 Rate and Term O/O 100% 1 1 100% 1 620 Rural Streamlined-Assist O/O N/A 1 N/A 620 1 Exclusive of Guarantee

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist

Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist") Applicant Information AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist Loan Request: $ Loan Purpose: Purchase - Sales Price: $ Refinance

Applicant Information AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist Loan Request: $ Loan Purpose: Purchase - Sales Price: $ Refinance

Rate Lock Hours: 7:30-4:00 PST Toll Free: (866) WHOLESALE RATESHEET Lock Desk: (866) FHA Loan Programs

WHOLESALE RATESHEET Lock Desk: (866) FHA Loan Programs") FHA Loan Programs FHA 30yr Fixed FHA 30yr Fixed High Balance FHA 15yr Fixed F30F H30F F15F 5.000 (6.000) (6.000) (6.000) (6.000) 4.625 (5.596) (5.471) (5.346) (5.221) 4.125 (4.870) (4.729) (4.566) (4.406)

FHA Loan Programs FHA 30yr Fixed FHA 30yr Fixed High Balance FHA 15yr Fixed F30F H30F F15F 5.000 (6.000) (6.000) (6.000) (6.000) 4.625 (5.596) (5.471) (5.346) (5.221) 4.125 (4.870) (4.729) (4.566) (4.406)

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

FHA Streamline (Full Credit and Non-Credit Qualifying)

") . This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

. This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

Wholesale Lending FHA Product Profile 03/23/2015 Overlays to HUD Guidelines are underlined

FHA CONFORMING Program Code GF30 GF15 GA05 GA07 Loan Description FHA CONFORMING 30 YEAR FIXED FHA CONFORMING 15 YEAR FIXED FHA CONFORMING 5/1 LIBOR ARM FHA CONFORMING 7/1 LIBOR ARM Program Code FHA HIGH

FHA CONFORMING Program Code GF30 GF15 GA05 GA07 Loan Description FHA CONFORMING 30 YEAR FIXED FHA CONFORMING 15 YEAR FIXED FHA CONFORMING 5/1 LIBOR ARM FHA CONFORMING 7/1 LIBOR ARM Program Code FHA HIGH

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs Red indicates changes from previous matrix Overlays to Investor guidelines are underlined and in italics Owner Occupied

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs Red indicates changes from previous matrix Overlays to Investor guidelines are underlined and in italics Owner Occupied

Caliber RESPA/TILA Fee Guide By Fee Name

203 (k) Architectural and Engineering Fee Section C. Can Shop No 203 (k) Contingency Reserve Section H. Other No 203 (k) Repairs Section H. Other No 203 (k) Title Update Fee Section C. Can Shop Yes 203K

203 (k) Architectural and Engineering Fee Section C. Can Shop No 203 (k) Contingency Reserve Section H. Other No 203 (k) Repairs Section H. Other No 203 (k) Title Update Fee Section C. Can Shop Yes 203K

JUMBO PRIME PROGRAM (FIXED & ARM)

") JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

AltQM TM Investor Program Underwriting Guidelines

Underwriting Philosophy Impac takes a common sense approach to underwriting a borrower s creditworthiness to determine the willingness and ability to repay the loan. Each applicant has a different situation

Underwriting Philosophy Impac takes a common sense approach to underwriting a borrower s creditworthiness to determine the willingness and ability to repay the loan. Each applicant has a different situation

LPA HOME POSSIBLE. Home Possible

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

California Homebuyer Fund CHF

California Homebuyer Fund CHF Purchase Primary Residence Loan Type Property Type Max. LTV/CLTV (1) Min. FICO Max DTI FHA VA USDA 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 96.5%

California Homebuyer Fund CHF Purchase Primary Residence Loan Type Property Type Max. LTV/CLTV (1) Min. FICO Max DTI FHA VA USDA 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 1 Unit SFR, Condo, PUD 96.5%

JUMBO PRIME PROGRAM JUMBO PRIME PROGRAM

JUMBO PRIME PROGRAM PRIMARY RESIDENCE Purchase & Rate/Term Refinance Units Max. Loan Amount (1) LTV CLTV Min. FICO Max. Cash-Out $2,000,000 80% 80% 740 $1,750,000 80% 80% 720 $2,000,000 75% 75% 720 $2,250,000

JUMBO PRIME PROGRAM PRIMARY RESIDENCE Purchase & Rate/Term Refinance Units Max. Loan Amount (1) LTV CLTV Min. FICO Max. Cash-Out $2,000,000 80% 80% 740 $1,750,000 80% 80% 720 $2,000,000 75% 75% 720 $2,250,000

ELIGIBILITY MATRIX & SUMMARY GUIDELINES 15 & 30 YR Fixed Rates

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

PennyMac Correspondent Group Overlays, February 25, 2019 X Indicates Overlay

PennyMac Correspondent Group Overlays, February 25, 2019 Indicates Overlay GOVERNMENT FHA Full doc FHA Streamline VA Full Doc VA IRRRL Rural Housing Topic Overlay/Modification 203(k) Specific PennyMac

PennyMac Correspondent Group Overlays, February 25, 2019 Indicates Overlay GOVERNMENT FHA Full doc FHA Streamline VA Full Doc VA IRRRL Rural Housing Topic Overlay/Modification 203(k) Specific PennyMac

CRA PORTFOLIO NON-CONFORMING PROGRAM

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

Federal Housing Administration (FHA) Product Matrix

Product Matrix") APPRAISAL All FHA appraisals are valid for 120 days including New Construction and HUD REO s. FHA approved lenders are prohibited from accepting appraisals prepared by appraisers who are selected, retained

APPRAISAL All FHA appraisals are valid for 120 days including New Construction and HUD REO s. FHA approved lenders are prohibited from accepting appraisals prepared by appraisers who are selected, retained

Single Family Housing Guaranteed Loan Program Quick Reference

Single Family Housing Guaranteed Loan Program Quick Reference Topic 7 CFR 3555 HB-1-3555 7 CFR Part 3555 Appendix 1 A Abandoned or Vacant Property 3555.302 19.2 A Account Acceleration 3555.306 18.6 Acceptable

Single Family Housing Guaranteed Loan Program Quick Reference Topic 7 CFR 3555 HB-1-3555 7 CFR Part 3555 Appendix 1 A Abandoned or Vacant Property 3555.302 19.2 A Account Acceleration 3555.306 18.6 Acceptable

Streamline Assist Refinance Product

Streamline Assist Refinance Product Credit Policy 09/06/2016 DISCLAIMER USDA has provided VERY LITTLE information as to their exact documentation requirements on this new product. Therefore, we ve done

Streamline Assist Refinance Product Credit Policy 09/06/2016 DISCLAIMER USDA has provided VERY LITTLE information as to their exact documentation requirements on this new product. Therefore, we ve done

SIERRA CLASSIC JUMBO Fixed and ARM Matrix ( 1)(10)(11) RETAIL BUSINESS CHANNEL ONLY

(10)(11) RETAIL BUSINESS CHANNEL ONLY") SIERRA CLASSIC JUMBO Fixed and ARM Matrix ( 1)(10)(11) RETAIL BUSINESS CHANNEL ONLY Loan Purpose Property Type Owner Occupied Properties Minimum Credit Score (1) LTV/CLTV (2)(3)(8) Maximum Loan Amount

SIERRA CLASSIC JUMBO Fixed and ARM Matrix ( 1)(10)(11) RETAIL BUSINESS CHANNEL ONLY Loan Purpose Property Type Owner Occupied Properties Minimum Credit Score (1) LTV/CLTV (2)(3)(8) Maximum Loan Amount

Refinance Report August 2012

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

PRODUCT MATRICES. For Information on any of our products, please contact:

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Fannie Mae Conforming and High Balance

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

FHA Standard Refinance (Cash Out)

") This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

Guide to the FHA Basics

Guide to the FHA Basics Navigating your way to FHA success!! Rev. 6/13/2016 FHA Basics FHA insures the loan for an insurance fee (referred to as UFMIP) which is collected at loan closing. UFMIP can be

Guide to the FHA Basics Navigating your way to FHA success!! Rev. 6/13/2016 FHA Basics FHA insures the loan for an insurance fee (referred to as UFMIP) which is collected at loan closing. UFMIP can be

Core Seconds S Year Fixed S Due-in 15 Fixed

Last Revised: September 1, 2005 Core Seconds S070 15 Year Fixed S071 30-Due-in 15 Fixed CORE SECONDS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Documentation Requirements

Last Revised: September 1, 2005 Core Seconds S070 15 Year Fixed S071 30-Due-in 15 Fixed CORE SECONDS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Documentation Requirements

Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of

Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of") Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of factors indicative of a consumer s credit capacity, including:

Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of factors indicative of a consumer s credit capacity, including:

FHLMC PROGRAM LINEUP`

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

PRIMARY RESIDENCE PURCHASE FIXED 5/1 & 7/1 ARM 10/1 ARM

PRIMARY RESIDENCE PURCHASE FIXED Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO $1,000,000 85% (1) N/A 760 $1,500,000 80% 80% 720 1 Unit $2,000,000 75% 75% 720 PUD, Condo $1,000,000 70%

PRIMARY RESIDENCE PURCHASE FIXED Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO $1,000,000 85% (1) N/A 760 $1,500,000 80% 80% 720 1 Unit $2,000,000 75% 75% 720 PUD, Condo $1,000,000 70%

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

Fannie Mae 2010 First Quarter Credit Supplement. May 10, 2010

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

FHA Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015 April 30, 2015

Assets Gift Funds Documenting Transfer Not clear about requiring donor s bank statement in all instances. Requires donor s bank statement showing withdrawal of funds. Earnest Money Document source of funds

Assets Gift Funds Documenting Transfer Not clear about requiring donor s bank statement in all instances. Requires donor s bank statement showing withdrawal of funds. Earnest Money Document source of funds

H Coordinator NACS DRAFT 6/13/05

H Coordinator NACS DRAFT 6/13/05 What I miss.. NACS DRAFT 6/13/05 What I don t miss. NACS DRAFT 6/13/05 USDA, Rural Development Guaranteed Rural Housing Benefits Direct Single Family Housing Applicant

H Coordinator NACS DRAFT 6/13/05 What I miss.. NACS DRAFT 6/13/05 What I don t miss. NACS DRAFT 6/13/05 USDA, Rural Development Guaranteed Rural Housing Benefits Direct Single Family Housing Applicant

HOUSING TRUST SILICON VALLEY LOAN GENERAL UNDERWRITING GUIDELINES

HOUSING TRUST SILICON VALLEY LOAN GENERAL UNDERWRITING GUIDELINES The Housing Trust reserves the right to revise and change guidelines at its discretion. APPLICATION PROCESS An applicant may apply through

HOUSING TRUST SILICON VALLEY LOAN GENERAL UNDERWRITING GUIDELINES The Housing Trust reserves the right to revise and change guidelines at its discretion. APPLICATION PROCESS An applicant may apply through