Great Internal Controls and Then IT Happens Fraud!

|

|

|

- Allison McCoy

- 5 years ago

- Views:

Transcription

1 Then IT Happens Fraud! Pamela Mantone, CPA, CFE, CFF, CITP, CGMA, FCPA, MAFF Pamela S. Mantone CPA, CFF, CFE, MAFF, CITP, CGMA, FCPA Director April 21, 2016

2 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation is for informational purposes and does not contain or convey specific advice. It should not be used or relied upon in regard to any particular situation or circumstances without first consulting the appropriate advisor. No part of the presentation may be circulated, quoted, or reproduced for distribution without prior written approval from Elliott Davis Decosimo.

3 Even the best internal control structure is not guaranteed to prevent fraud. Inherent limitations Judgment Breakdowns Management override Materiality Point-in-time evaluation Cost/benefit considerations Cannot rely on regulatory exams, internal audit or external audits to find fraud. It is a game of chance for those not sufficiently trained to perform forensic accounting.

4 The greatest internal fraud preventive technique is monitoring allows the perception of detection Authorizations Approvals Reviews Reviews And review some more Opportunity can be controlled by an organization while motive and rationalization cannot be controlled (The Fraud Triangle)

5 Are banks subject to legal issues when acting as a 3 rd Party in transactions related to fraudulent activity? PATCO vs. Ocean Bank 1 st Circuit of Appeals, July 3, 2012 Facts: PATCO, a small construction company in Maine and a longtime customer of the bank sustained 6 unauthorized ACH transfers from their payroll account ($588,851.26) Court found in favor of PATCO, despite bank s security system was provided through a reputable, well-known vendor Court referred to FFEIC standards as relevant to standard of care

6 Choice (Choice)Escrow and Title vs BancorpSouth Bank(BSB) 8 th Circuit of Appeals, June 11, 2014 Facts: Choice sued BSB for $440,000 that internet fraudsters stole from their account Court found in favor of BSB since Choice chose to decline BSB s fourth security measure of dual control and signed a waiver acknowledging that dual control was declined and understood the risks associated with using a single-control security system Dual control created a pending payment order for approval by a second party Really a win? Court firmly held that when a customer insists on using a higher-risk procedure because it is more convenient or cheaper, the account holder has voluntarily assumed the risk and cannot shift responsibility to the bank.

7 South State Bank (formerly The Savannah Bank) Lawsuits involving funds put into bank and held in trust (fiduciary funds) stolen by Probate Court Clerk- on-going with multiple lawsuits from victims in Chatham County State Court Last motion heard March 24, 2016, last proceeding dated April 1, 2016 Over $800,000 taken from various accounts South State Bank improperly monitored the account under the control of Birge, Probate Court Clerk Multiple checks written to cash with no endorsement on back Many of these checks were $2,900 or less Many of these transactions occurred two at a time on the same day within minutes of each other Notations from bank clerks stamps well-known customer Generally used the same tellers at the different branches SARS??

8 Fraud risks associated with financial institutions Technology threats Embezzlement Loan Fraud Real estate fraud Mortgage fraud New Accounts Money transfer (wire) fraud ATM Fraud Money Laundering and the list goes on

9 Loan Fraud Loans to non-existent borrowers Sham loans with kickbacks and diversion Double-pledging collateral Daisy chains Linked financing False applications with false credit information and/or credit data blocking Single-family housing loan fraud Construction loans lots of opportunities Loan collateral sold out of trust

10 Red Flags for Loan Fraud Non performing loans Fraudulent appraisals False statements Equity skimming Construction over budget items Land flips Disguised transactions High turnover in developer s personnel (construction lending) High turnover in tenant mix Abnormal change orders (construction lending) Missing documentation in the loan file Loan increases or extensions, replacement loans, evergreen loans Change in ownership makeup Cash flow deficiencies (commercial lending) Disguised transactions

11 An unusual twist for loan fraud allowing embezzlement of funds Over $176,000 taken in about 18 months New accounts set up using fictitious names and addresses, with name changes on the accounts occurring at various times. 19 accounts used to funnel money from institution. Hint: Geo-coding is an excellent way to check out addresses, also Google Maps Paying off loans of actual customers accounts and issuing new loans with a cash withdrawal generally occurring at the same time Cash tickets destroyed Missing support documentation for loans Multiple file maintenance changes performed to various members documentation, including extensions of next payment due and last payment date to prevent loan being shown as past due Access to user ids and ability to change passwords

12 An unusual twist for loan fraud allowing embezzlement of funds - continued Security access set up by 3 rd party vendor and not reviewed Background checks not performed for future employees. Credit reports do not provide sufficient information for the hiring process Lack of proper safe-keeping of documents Lack of adequate review from the loan committee Passive performance from the audit committee Slow process in hiring new CEO, there was no CEO during the time the embezzlement occurred Lack of proper reviews and monitoring at all levels Case presented to district attorney and state regulatory agency

13 Loan fraud found accidently by regulatory agency requiring examination by a forensic investigation Over $500,000 taken from institution through the use of fictitious loans and ACH transactions Loan officer had a degree in information technology and very capable of manipulating computerized records Set up fictitious loan accounts combining information from existing customers Loans set up under lending limits CD s and other property used as collateral were CD s from customers UCC filings contained falsified VIN numbers and other information Part of loan proceeds were used to set up separate checking accounts Credit cards set up for these accounts Statements sent to two different P. O. box numbers

14 Loan fraud found accidently by regulatory agency requiring examination by a forensic investigation - continued Over $500,000 taken from institution through the use of fictitious loans and ACH transactions Loan payments made from other fictitious accounts and other new fictitious loans Loan payments washed through multiple times and then applied to fictitious accounts Personal favorite was check made to a T. Swindle Deleted transactions from computerized records Worked after hours without authorization Changed 65 transactions night before start of regulatory exam Part of loan proceeds were used to set up separate checking accounts Personal property taxes paid out of loan proceeds Personal items purchased on credit cards

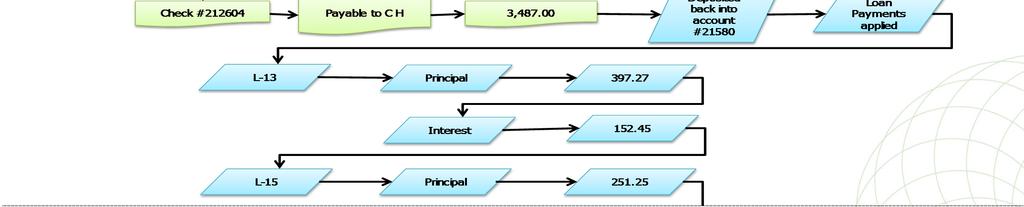

15 The chain for one check issued!

16

17 A lot of work for $1,000 in cash but remember, fraudulent loans must be paid as well!

18 Loan fraud found accidently by regulatory agency requiring examination by a forensic investigation Excellent example of an internal control breakdown Employee did not follow policies and procedures Maintained information in such a manner that it appeared that loans were valid loans and payments made monthly Followed lending limits to prevent detection Pled guilty in federal court, sentenced on December, 2014 Ordered to pay restitution and sentenced to 27 months in a minimum security federal prison and four years of supervised release

19 Wire Fraud Contact within the target company and aggressive in carrying out theft Dishonest bank employees Misrepresentation of identity System password security compromised Forged authorizations Unauthorized entry and interception

20 A wire fraud case where the insurance company required a forensic investigation before paying for the loss Shareholder s computer compromised and identity information stolen, including social security number, bank information and account numbers and retirement accounts Shareholder to bank requesting funds wired to another bank Bank requested phone call but shareholder was in a meeting and could not call then, but gave a phone number to call later More shareholder s gently persuading transfer of funds Additional requests for wire transfers Funds wired to various banks, all under $25,000 until balance in account was very minimal

21 A wire fraud case where the insurance company required a forensic investigation before paying for the loss - continued Funds bounced from various accounts at various branches of a nationally large bank and funds were off-shore within 24 hours - Recipients Russian mafia - Use of mules - Persuasive passive aggressive techniques used to promote compliance Shareholder notified financial institution that identity was stolen too late for the transfers though Over $250,000 transferred within a three-day period No employees from the financial institution were found to be involved with the wire transfer fraud and losses were paid by insurer

22 Ways to Prevent and Detect Wire Fraud Review all wire transfer transactions at the end of each day Provide fraud awareness training including social engineering techniques, especially passive aggressive techniques and phishing Don t execute wire transfers solely from faxed or instructions Require all personnel who handle wire transfers to go on vacation (minimum of one week) Provide customers with unique codes that are required to authorize or order wire transfers Re-assign wire transfer employees who have given notice to another department for the time left

23 Fraud risks associated with financial institutions Embezzlement False accounting entries Suspense accounts False or unauthorized transfers Unauthorized withdrawals Unauthorized disbursements of funds to outsiders Paying personal expenses from bank funds Theft of physical property Dormant or inactive accounts Unauthorized cash payments Unauthorized use of collateral Skimming

24 Red Flags for embezzlement Missing source documents Unusual amount of out-of-sequence check numbers Payees on checks do not match entries in general ledger Receipts or invoices lack professional quality Duplicate payment documents Payee identification information matches an employee s information or that of his relatives Apparent signs of alteration to source documents Lack of original source documents (photo copies only) Excessive voids or credits Abnormal increase in reconciling items Cashier s checks made payable to Cash

25 Dimensional testing for Employee Networks as Vendors - Employee Emergency contact and other dependents - Address - Business address - Company phone number - Company or personal fax number

26 Conflicts of Interest Board Member Interrelationships

27 An embezzlement cover-up with an unusual twist CEO embezzled more than $1.5M from financial institution through loans concerning his farming operations Used second individual at another financial institution to kite checks and float deposits for sale of cattle to hide the embezzled funds Kiting the process of recording the deposit of an interbank transfer before recording the disbursement Floating Current holder of funds has been given credit for the funds before the check clears the financial institution upon which it is drawn Floating makes check kiting possible Both more difficult with shorter floating period Kite continued over one year before the house of cards fell

28 An embezzlement cover-up with an unusual twist SARS?? Nothing good comes from fraudulent activity well sometimes Financial institution failed Shareholders of the financial institution lost their investments CEO destroyed all records and committed suicide But the second party of the kite received over $600,000 in funds from the last float and, under oath, stated that there was no overage of funds in his personal account. So these funds were used for personal expenses. Ultimately, these funds became part of the recovery costs for the shareholders of the financial institution

29 The expected never happens; it is the unexpected always. John Maynard Keynes Corruption, embezzlement, fraud, these are all characteristics which exist everywhere. It is regrettably the way human nature functions, whether we like it or not. What successful economies do is keep it to a minimum. No one has ever eliminated any of that stuff. - Alan Greenspan

30 Providing Additional Resources to Meet Your Needs

31 Pam Mantone Phone: Website: Elliott Davis Decosimo ranks among the top 30 CPA firms in the U.S. With sixteen offices across six states, the firm provides clients across a wide range of industries with smart, customized solutions. Elliott Davis Decosimo is an independent firm associated with Moore Stephens International Limited, one of the world's largest CPA firm associations with resources in every major market around the globe. For more information, please visit elliottdavis.com.

32 Analytical Tools and Techniques

Financial Transactions and Fraud Schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Fraud Examination. Prevention, Detection, and Investigation. Steven M. Bragg

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Prevention for Nonprofits

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

COVERAGE FRAUD IN EMPLOYEE BENEFIT PLANS 5/15/2014. Where employee benefit fraud is likely. Internal controls that help prevent fraud

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Chapter 2 Skimming. 2. To a fraudster, the principle advantage of skimming is the difficulty with which the scheme is detected. a. True b.

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Good From The Inside Out. Saturday, April 8, 2017

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Grant Fraud. Leslie Les Hollie Assistant Inspector General For Investigations

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Insights Into Accounting Schemes and Scams

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

The Auditor s Responsibilities. Audit of Financial Statements

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

Retirement Plan Compliance and Controls

Retirement Plan Compliance and Controls Cindy Lusk, CPA, RPA Manager, Employee Benefit Plan Practice May 12, 2015 Elliott Davis Decosimo, LLC Elliott Davis Decosimo, PLLC 1 Retirement Plan Compliance and

Retirement Plan Compliance and Controls Cindy Lusk, CPA, RPA Manager, Employee Benefit Plan Practice May 12, 2015 Elliott Davis Decosimo, LLC Elliott Davis Decosimo, PLLC 1 Retirement Plan Compliance and

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

International Standard on Auditing (Ireland) 240

240") International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

Looking for Fraud Through Rose-Colored Glasses

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Red Flag Rule Procedures Under Princeton University s Identity Theft Prevention Program Effective: December 31, 2010

Red Flag Rule Procedures Under Princeton University s Identity Theft Prevention Program Effective: December 31, 2010 Princeton University employees are responsible for detecting Red Flags consistent with

Red Flag Rule Procedures Under Princeton University s Identity Theft Prevention Program Effective: December 31, 2010 Princeton University employees are responsible for detecting Red Flags consistent with

Recognizing Credit Card Fraud

1 Recognizing Credit Card Fraud Credit card fraud happens when consumers give their credit card number to unfamiliar individuals, when cards are lost or stolen, when mail is diverted from the intended

1 Recognizing Credit Card Fraud Credit card fraud happens when consumers give their credit card number to unfamiliar individuals, when cards are lost or stolen, when mail is diverted from the intended

Employee Dishonesty Lessons Learned: Internal Controls

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

Securing Your Balance Sheet Fidelity/Crime Insurance. Presenter: Mary da Costa, Manager, Corporate Insurance

Securing Your Balance Sheet Fidelity/Crime Insurance Presenter: Mary da Costa, Manager, Corporate Insurance DISCLAIMER The following presentation is for general information. In all cases the terms of the

Securing Your Balance Sheet Fidelity/Crime Insurance Presenter: Mary da Costa, Manager, Corporate Insurance DISCLAIMER The following presentation is for general information. In all cases the terms of the

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

FRAUD TRENDS TO WATCH FOR IN Presented by: Daniel J. Mahalak

FRAUD TRENDS TO WATCH FOR IN 2018 Presented by: Daniel J. Mahalak Session Overview In recent years, fraud has seemingly been increasing in credit unions. Some of this fraud is related to the technology

FRAUD TRENDS TO WATCH FOR IN 2018 Presented by: Daniel J. Mahalak Session Overview In recent years, fraud has seemingly been increasing in credit unions. Some of this fraud is related to the technology

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

International Standard on Auditing (UK) 240 (Revised June 2016)

240 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Bank Secrecy Act OFAC FinCEN

Bank Secrecy Act OFAC FinCEN 2017 CREDIT UNION EMPLOYEE TRAINING Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer Identification Program Customer Due Diligence

Bank Secrecy Act OFAC FinCEN 2017 CREDIT UNION EMPLOYEE TRAINING Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer Identification Program Customer Due Diligence

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

Lecture Notes for How to Steal $500 Million

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

ORGANIZATIONAL MANUAL

I. PURPOSE ORGANIZATIONAL MANUAL IDENTITY THEFT PROTECTION A. To establish an Identity Theft Prevention Program designed to detect, prevent and mitigate Identity Theft in connection with the opening of

I. PURPOSE ORGANIZATIONAL MANUAL IDENTITY THEFT PROTECTION A. To establish an Identity Theft Prevention Program designed to detect, prevent and mitigate Identity Theft in connection with the opening of

Deposit Account Agreement Privacy Notice How to Contact Us

Deposit Account Agreement Privacy Notice How to Contact Us Important legal information, disclosures and terms you should know Issue Date: NOV 2017 Table of Contents DEPOSIT ACCOUNT AGREEMENT... 2 General

Deposit Account Agreement Privacy Notice How to Contact Us Important legal information, disclosures and terms you should know Issue Date: NOV 2017 Table of Contents DEPOSIT ACCOUNT AGREEMENT... 2 General

Employee Benefit Plans DOL Criminal Enforcement Cases April 2009 November 2011

Employee Benefit Plans DOL Criminal Enforcement Cases April 2009 November 2011 The AICPA Employee Benefit Plan Audit Quality Center has developed this summary analysis of the U.S. Department of Labor (DOL)

Employee Benefit Plans DOL Criminal Enforcement Cases April 2009 November 2011 The AICPA Employee Benefit Plan Audit Quality Center has developed this summary analysis of the U.S. Department of Labor (DOL)

A Review of Actual Fraud Cases in 2017 FRAUD REVIEW

A Review of Actual Fraud Cases in 2017 FRAUD REVIEW Contents Introduction 3 Fraud Snapshot 4 Case Studies Credit Card Fraud 5 Business Email Compromise Fraud 6 Payroll Fraud 7 Supplier Fraud 8 Outlook

A Review of Actual Fraud Cases in 2017 FRAUD REVIEW Contents Introduction 3 Fraud Snapshot 4 Case Studies Credit Card Fraud 5 Business Email Compromise Fraud 6 Payroll Fraud 7 Supplier Fraud 8 Outlook

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

Protecting against check fraud perspectives and best practices

Protecting against check fraud perspectives and best practices Presenter Name Corp Title, Functional Title Date of presentation 2016 Wells Fargo Bank, N.A. All rights reserved. For public use. Agenda Check

Protecting against check fraud perspectives and best practices Presenter Name Corp Title, Functional Title Date of presentation 2016 Wells Fargo Bank, N.A. All rights reserved. For public use. Agenda Check

Lecture notes for: Corporate Cons

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

The State of the Art of Fraud. Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

Identity Theft Prevention Program. Approved by the Board of Trustees on February 20, 2009

Identity Theft Prevention Program Approved by the Board of Trustees on February 20, 2009 I. Purpose & Scope This Program was developed pursuant to the Federal Trade Commission s ( FTC ) Red Flag Rules

Identity Theft Prevention Program Approved by the Board of Trustees on February 20, 2009 I. Purpose & Scope This Program was developed pursuant to the Federal Trade Commission s ( FTC ) Red Flag Rules

INTERNAL FRAUD PREVENTION:

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

FINN BY CHASE SM DEPOSIT ACCOUNT AGREEMENT

FINN BY CHASE SM DEPOSIT ACCOUNT AGREEMENT FINN CHECKING AND SAVINGS PRODUCT INFORMATION WELCOME TO FINN Thank you for opening your Finn Checking and Savings accounts during our pilot. This Finn Checking

FINN BY CHASE SM DEPOSIT ACCOUNT AGREEMENT FINN CHECKING AND SAVINGS PRODUCT INFORMATION WELCOME TO FINN Thank you for opening your Finn Checking and Savings accounts during our pilot. This Finn Checking

Employee Benefit Plan Fraud Examples

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

Controls over Bank Accounts

Subsection: Control of Bank Accounts Page: 1 of 16 Controls over Bank Accounts Objective Authority The objective is to ensure proper internal controls are in place where bank accounts are used. The Financial

Subsection: Control of Bank Accounts Page: 1 of 16 Controls over Bank Accounts Objective Authority The objective is to ensure proper internal controls are in place where bank accounts are used. The Financial

Uniform Guidance. Jeremy Dunn. Senior Manager November 4, Elliott Davis Decosimo, LLC Elliott Davis Decosimo, PLLC

Uniform Guidance Jeremy Dunn Senior Manager November 4, 2015 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation

Uniform Guidance Jeremy Dunn Senior Manager November 4, 2015 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation

Chapter 2 Skimming 1

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

1/18/2018. Fraud Prevention and Detection: Special Investigations, Information and Examples. Office of the State Auditor Role and Responsibility

Fraud Prevention and Detection: Special Investigations, Information and Examples 2018 MACO Annual Winter Conference Thursday, February 15, 2018 10:15-12:00 Mark Kerr, JD, CFE Special Investigations Director

Fraud Prevention and Detection: Special Investigations, Information and Examples 2018 MACO Annual Winter Conference Thursday, February 15, 2018 10:15-12:00 Mark Kerr, JD, CFE Special Investigations Director

Personal Deposit Account Agreement

Personal Deposit Account Agreement Personal Deposit Account Agreement TABLE OF CONTENTS WELCOME 4 A. GENERAL ACCOUNT TERMS 5 1. DEFINITIONS 5 2. OPENING A PERSONAL DEPOSIT ACCOUNT 5 3. USING YOUR ACCOUNT

Personal Deposit Account Agreement Personal Deposit Account Agreement TABLE OF CONTENTS WELCOME 4 A. GENERAL ACCOUNT TERMS 5 1. DEFINITIONS 5 2. OPENING A PERSONAL DEPOSIT ACCOUNT 5 3. USING YOUR ACCOUNT

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

Fraud prevention for credit unions

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Subject: Identity Theft, G-113 Department: All & Branches References: Part 717, NCUA Rules and Regs, FACT Act, Companion SOP s G-30 (Opening New

Subject: Identity Theft, G-113 Department: All & Branches References: Part 717, NCUA Rules and Regs, FACT Act, Companion SOP s G-30 (Opening New Accounts), G-38 (E-Commerce), G-40 (Issuance of Visa Cards),

Subject: Identity Theft, G-113 Department: All & Branches References: Part 717, NCUA Rules and Regs, FACT Act, Companion SOP s G-30 (Opening New Accounts), G-38 (E-Commerce), G-40 (Issuance of Visa Cards),

EVEREST NATIONAL INSURANCE COMPANY FINANCIAL INSTITUTION APPLICATION

EVEREST NATIONAL INSURANCE COMPANY DIRECTORS & OFFICERS / COMPANY LIABILITY FINANCIAL INSTITUTION BOND/CSD FINANCIAL INSTITUTION APPLICATION FDIC No. EMPLOYMENT PRACTICES LIABILITY THE LIABILITY POLICIES

EVEREST NATIONAL INSURANCE COMPANY DIRECTORS & OFFICERS / COMPANY LIABILITY FINANCIAL INSTITUTION BOND/CSD FINANCIAL INSTITUTION APPLICATION FDIC No. EMPLOYMENT PRACTICES LIABILITY THE LIABILITY POLICIES

Delivering Financial Oversight: Strengthening Your Policies and Procedures

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

IN THE SUPREME COURT OF FLORIDA (Before a Referee) REPORT OF REFEREE

REPORT OF REFEREE") IN THE SUPREME COURT OF FLORIDA (Before a Referee) THE FLORIDA BAR, Complainant, v. CASE NO.: SC10-1824 TFB NOS.: 2009-10,429(12C) 2009-11,531(12C) GERI LYNN HALLERMAN WAKSLER, Respondent. / REPORT OF

IN THE SUPREME COURT OF FLORIDA (Before a Referee) THE FLORIDA BAR, Complainant, v. CASE NO.: SC10-1824 TFB NOS.: 2009-10,429(12C) 2009-11,531(12C) GERI LYNN HALLERMAN WAKSLER, Respondent. / REPORT OF

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

I WOULD NOT DO THAT! Adam Lippe Chief, Economic Crime Unit Baltimore County State s Attorney s Office

I WOULD NOT DO THAT! Adam Lippe Chief, Economic Crime Unit Baltimore County State s Attorney s Office BUT SOMEONE ELSE WOULD A former South Texas juvenile justice department employee has been arrested

I WOULD NOT DO THAT! Adam Lippe Chief, Economic Crime Unit Baltimore County State s Attorney s Office BUT SOMEONE ELSE WOULD A former South Texas juvenile justice department employee has been arrested

Watching the Vault: Employee Dishonesty

Watching the Vault: Employee Dishonesty Managing your most pressing risks NCOFCU 2016 Conference CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group,

Watching the Vault: Employee Dishonesty Managing your most pressing risks NCOFCU 2016 Conference CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group,

Solutions. I. Auditing Cash and Cash Equivalents. A. Learning Question Answers

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

PRODUCT OVERVIEW DEPOSIT ACCOUNT AGREEMENT PRIVACY NOTICE HOW TO CONTACT US

PLEASE REVIEW THIS BOOKLET FOR IMPORTANT ACCOUNT INFORMATION PRODUCT OVERVIEW DEPOSIT ACCOUNT AGREEMENT PRIVACY NOTICE HOW TO CONTACT US Welcome to Chase Thank you for opening your new account with Chase;

PLEASE REVIEW THIS BOOKLET FOR IMPORTANT ACCOUNT INFORMATION PRODUCT OVERVIEW DEPOSIT ACCOUNT AGREEMENT PRIVACY NOTICE HOW TO CONTACT US Welcome to Chase Thank you for opening your new account with Chase;

Defending Against the Latest Fraud Trends

Defending Against the Latest Fraud Trends Joni Lovingood, CRM, CFE Corporate Property & Casualty Sales Specialist CUNA Mutual Group joni.lovingood@cunamutual.com CUNA Mutual Group Proprietary Reproduction,

Defending Against the Latest Fraud Trends Joni Lovingood, CRM, CFE Corporate Property & Casualty Sales Specialist CUNA Mutual Group joni.lovingood@cunamutual.com CUNA Mutual Group Proprietary Reproduction,

BANKING PROCEDURE AND CONTROL OF CASH

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

Thursday, November 29, Mortgage Fraud Investigations

Thursday, November 29, 2007 Mortgage Fraud Investigations 1 DUE DILIGENCE & MORTGAGE FRAUD Jim Vaules, CEO NFC Global LLC November 29, 2007 2 In God We Trust, Everyone Else Bring Data!!!! 3 Due Diligence,

Thursday, November 29, 2007 Mortgage Fraud Investigations 1 DUE DILIGENCE & MORTGAGE FRAUD Jim Vaules, CEO NFC Global LLC November 29, 2007 2 In God We Trust, Everyone Else Bring Data!!!! 3 Due Diligence,

POLICY: Identity Theft Red Flag Prevention

POLICY SUBJECT: POLICY: Identity Theft Red Flag Prevention It shall be the policy of the Cooperative to take all reasonable steps to identify, detect, and prevent the theft of its members personal information

POLICY SUBJECT: POLICY: Identity Theft Red Flag Prevention It shall be the policy of the Cooperative to take all reasonable steps to identify, detect, and prevent the theft of its members personal information

IRS Criminal Investigation SPECIAL AGENT FELICIA MCCAIN PUBLIC INFORMATION OFFICER (619)

") IRS Criminal Investigation SPECIAL AGENT FELICIA MCCAIN PUBLIC INFORMATION OFFICER (619) 770-9317 FELICIA.MCCAIN@CI.IRS.GOV Areas of Emphasis for CI Abusive Return Preparers International Fraud Refund

IRS Criminal Investigation SPECIAL AGENT FELICIA MCCAIN PUBLIC INFORMATION OFFICER (619) 770-9317 FELICIA.MCCAIN@CI.IRS.GOV Areas of Emphasis for CI Abusive Return Preparers International Fraud Refund

Fraud Risk Assessment Awareness in Employee Benefit Plans

Fraud Risk Assessment Awareness in Employee Benefit Plans Tyler Geiman, CPA, CFE, CFF Novak Francella, LLC Phone: (443) 832-4009 Fax: (443) 393-0323 Web: www.novakfrancella.com Fraud is any intentional

Fraud Risk Assessment Awareness in Employee Benefit Plans Tyler Geiman, CPA, CFE, CFF Novak Francella, LLC Phone: (443) 832-4009 Fax: (443) 393-0323 Web: www.novakfrancella.com Fraud is any intentional

Fraud Risk Assessment

Fraud Risk AHIA Southeast Regional Seminar Houston Texas Friday, November 12, 2010 Today s Discussion Agenda What is fraud? Industry fraud statistics Common fraud scenarios Fraud risk assessment (FRA)

Fraud Risk AHIA Southeast Regional Seminar Houston Texas Friday, November 12, 2010 Today s Discussion Agenda What is fraud? Industry fraud statistics Common fraud scenarios Fraud risk assessment (FRA)

Membership and Account Agreement Riverside Federal Credit Union

Membership and Account Agreement Riverside Federal Credit Union THIS MEMBERSHIP AND ACCOUNT AGREEMENT DISCLOSURE COVERS THE RIGHTS AND RESPONSIBILITIES CONCERNING ACCOUNTS RIVERSIDE FEDERAL CREDIT UNION

Membership and Account Agreement Riverside Federal Credit Union THIS MEMBERSHIP AND ACCOUNT AGREEMENT DISCLOSURE COVERS THE RIGHTS AND RESPONSIBILITIES CONCERNING ACCOUNTS RIVERSIDE FEDERAL CREDIT UNION

Bank Secrecy Act OFAC FinCEN

Bank Secrecy Act OFAC FinCEN SOUTHEAST DIRECTORS AND SUPERVISORY COMMITTEE CONFERENCE SEPTEMBER 18, 2017 Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer

Bank Secrecy Act OFAC FinCEN SOUTHEAST DIRECTORS AND SUPERVISORY COMMITTEE CONFERENCE SEPTEMBER 18, 2017 Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer

Fraud in Government. Mike Nolan, CPA, CFE, CGMA. CCACC & CCA&RMC Conference Monterey, CA September 2014

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Delivering Confidence PAGE 1

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

CUSTOMERS BANK FEE SCHEDULE

CUSTOMERS BANK FEE SCHEDULE Bill Pay FREE Voice Response (800-849-4809) FREE NET URL (www.customersbank.com) FREE ATM/Debit Card FREE Returned Check Charge $10.00 Non Sufficient Funds (NSF) Charge * $40.00

CUSTOMERS BANK FEE SCHEDULE Bill Pay FREE Voice Response (800-849-4809) FREE NET URL (www.customersbank.com) FREE ATM/Debit Card FREE Returned Check Charge $10.00 Non Sufficient Funds (NSF) Charge * $40.00

LOSS PREVENTION AND INTERNAL CONTROLS SUPPLEMENTAL APPLICATION FOR FINANCIAL INSTITUTIONS

Name of Insurance Company to which application is made LOSS PREVENTION AND INTERNAL CONTROLS SUPPLEMENTAL APPLICATION FOR FINANCIAL INSTITUTIONS NAME OF INSURED: ADDRESS: A. GENERAL INFORMATION 1. During

Name of Insurance Company to which application is made LOSS PREVENTION AND INTERNAL CONTROLS SUPPLEMENTAL APPLICATION FOR FINANCIAL INSTITUTIONS NAME OF INSURED: ADDRESS: A. GENERAL INFORMATION 1. During

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

Registration Disclosure

Registration Disclosure ONLINE BANKING ACCOUNT ACCESS AGREEMENT AND DISCLOSURE STATEMENT Vibrant Credit Union This Agreement establishes the rules that cover your electronic access to your account(s) at

Registration Disclosure ONLINE BANKING ACCOUNT ACCESS AGREEMENT AND DISCLOSURE STATEMENT Vibrant Credit Union This Agreement establishes the rules that cover your electronic access to your account(s) at

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

CAFR Reporting Ryan D. Miller, CPA May 2, 2016

CAFR Reporting Ryan D. Miller, CPA May 2, 2016 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation is for informational

CAFR Reporting Ryan D. Miller, CPA May 2, 2016 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation is for informational

Fraud: How to Get Your District Free Publicity

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

Shell Companies, Corrupt Practices, and How to Uncover Them. Lisa Duke, CFE, CPA, MAFF Supervisor Forensic Accountant FBI

Shell Companies, Corrupt Practices, and How to Uncover Them Lisa Duke, CFE, CPA, MAFF Supervisor Forensic Accountant FBI Shell Companies, Corrupt Practices and How to Uncover Them Lisa S. Duke, CFE, CPA,

Shell Companies, Corrupt Practices, and How to Uncover Them Lisa Duke, CFE, CPA, MAFF Supervisor Forensic Accountant FBI Shell Companies, Corrupt Practices and How to Uncover Them Lisa S. Duke, CFE, CPA,

Forensic Data Mining Finding Needles in the Haystack. Bank Fraud Investigations

acumen insight ideas Forensic Data Mining Finding Needles in the Haystack Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant BKD, LLP attention reach expertise depth agility

acumen insight ideas Forensic Data Mining Finding Needles in the Haystack Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant BKD, LLP attention reach expertise depth agility

Common 403b Audit Deficiencies & What s New This Year

Common 403b Audit Deficiencies & What s New This Year Mallory Sinclair, CPA Howie Houston, CPA May 22, 2014 This material was used by Elliott Davis during an oral presentation; it is not a complete record

Common 403b Audit Deficiencies & What s New This Year Mallory Sinclair, CPA Howie Houston, CPA May 22, 2014 This material was used by Elliott Davis during an oral presentation; it is not a complete record

University of Cincinnati FACTA Red Flag Identity Theft Prevention Program

FACTA Red Flag Identity Theft Prevention Program FACTA Red Flag Policy Program, page 1 of 6 Contents Overview 3 Definition of Terms 3 Covered Accounts..3 List of Red Flags 3 Suspicious Documents...4 Suspicious

FACTA Red Flag Identity Theft Prevention Program FACTA Red Flag Policy Program, page 1 of 6 Contents Overview 3 Definition of Terms 3 Covered Accounts..3 List of Red Flags 3 Suspicious Documents...4 Suspicious

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

Cash and Internal Control C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Internal Bank Fraud Schemes & Scams in an Economic Downturn. Fictitious Loans. Bank Fraud Investigations. Tracking spreadsheet Affidavit 1 Affidavit 2

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

ACFE CFEX. Certified Fraud Examiner (CFEX)

") ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

Financial Institution Bond Application

Financial Institution Bond Application *To be able to save this form after the fields are filled in, you will need to have Adobe Reader 9 or later. If you do not have version 9 or later, please download

Financial Institution Bond Application *To be able to save this form after the fields are filled in, you will need to have Adobe Reader 9 or later. If you do not have version 9 or later, please download

Financial Institution Bond Application

FDIC #: DATE: *To be able to save this form after the fields are filled in, you will need to have Adobe Reader 9 or later. If you do not have version 9 or later, please download the free tool at: http://get.adobe.com/reader/.

FDIC #: DATE: *To be able to save this form after the fields are filled in, you will need to have Adobe Reader 9 or later. If you do not have version 9 or later, please download the free tool at: http://get.adobe.com/reader/.

CASH HANDLING POLICIES

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

Is Your Construction Project a Victim of Fraud?

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction