Fraud Prevention for Nonprofits

|

|

|

- Melinda Hines

- 6 years ago

- Views:

Transcription

1 Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary is our longest tenure employee and would never commit fraud. We don t have enough staff to have financial controls. Our audit will catch any fraud. How many of you know of a nonprofit organization that has been a victim of fraud? 1

2016 Report to the Nations, it is estimated that the typical organization loses 5% of revenue in a given year as a result of fraud.")

2 Is fraud really that big of a deal? According to the Association of Certified Fraud Examiners (ACFE) 2016 Report to the Nations, it is estimated that the typical organization loses 5% of revenue in a given year as a result of fraud. ACFE 2016 Report Findings Median loss suffered by small organizations (fewer than 100 employees) was the same as that incurred by the largest organizations (more than 10,000 employees). However, this type of loss is likely to have a much greater impact on smaller organizations. Organizations of different sizes tend to have different fraud risks. Corruption was more prevalent in larger organizations, while check tampering, skimming, payroll and cash larceny schemes were twice as common in small organizations as in larger organizations. ACFE 2016 Report Findings Most prominent organizational weakness that contributed to the frauds in the study was lack of internal controls, which was cited in 29.3% of cases, followed by an override of existing internal controls, which contributed to just over 20% of cases. In 40.7% of cases, the victim organizations decided not to refer their fraud cases to law enforcement, with the fear of bad publicity being the most cited reason. 2

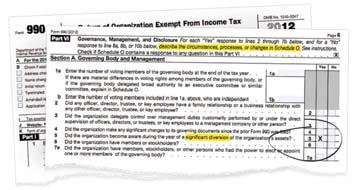

3 Characteristics of a Fraudster Washington Post Study IRS Form 990, revised in

4 Washington Post Study October 2013 study Form 990 filings from More than 1,000 nonprofits checked the box 10 of the largest disclosures had losses totaling more than a half billion dollars Fraud Triangle Pressure/Incentive Pressure may be actual or perceived Provides a motivation to commit fraud 4

5 Examples of Pressures/Incentives A nonprofit s executive director may be told by the board to achieve a certain level of fund raising by the end of the fiscal year (real pressure). The executive director also may believe that if she does not meet the board s expectations, her employment will be terminated (perceived pressure). In an effort to obtain additional grant funds or contributions, nonprofits may have an incentive to overstate revenues or results. Conversely, nonprofits may have an incentive to understate expenses in an effort to appear more efficient or effective to potential grantors or donors. Examples of Pressures/Incentives For some higher level management, annual compensation may be based, in part, on the organization s financial, service or overall performance. Organizations operate in a competitive environment for contributions. Potential donors can readily compare an organization s Form 990 to other organizations with a similar mission. An organization feels pressure to maximize the reported program expenses and minimize the reported fund raising and management and general expenses to attract donors. Examples of Pressures/Incentives An organization incurs some significant fund raising expenses that the organization believes will result in contributions in future years. Management is concerned the reporting these fund raising expenses in the current year will appear to make the development staff appear ineffective as the contributions will not be generated until future years. An organization has had several years of healthy increases in unrestricted net assets. The Executive Director is concerned that potential donors may be less inclined to donate to the organization if they believe the organization does not need assistance. 5

6 Examples of Pressures/Incentives An organization received a conditional promise to give of one dollar for every two dollars raised from other donors prior to year end. Going into the final month of the year, the organization is far behind its matching funds for the grant. An organization is facing a likely deficit in unrestricted net assets. Over the years, the organization has received a number of temporarily restricted contributions. The organization does not foresee itself taking on such projects in the near future and the original donors do not ask about the status of the projects. Examples of Pressures/Incentives An organization receives a grant that is renewed annually. One of the terms of the grant is that any unused funds at the end of the grant year must be returned to the grantor. The current year has had less activity than normal. The organization is concerned about having to refund a portion of the grant funds and that future grants may be reduced. Opportunity A lack of personnel, or sufficiently qualified personnel Absences of controls Ineffective controls Ability of management to override controls 6

7 Examples of Opportunity A nonprofit may have a number of locations where cash is collected for payment of services. In addition, the cash may be collected by persons, such as volunteers, who lack knowledge of existing controls. A nonprofit s management may view anti fraud programs as unnecessary because they do not believe anyone would want to defraud their organization. This misperception could result from the believe that volunteers or employees are committed to the mission and would not be willing to harm the nonprofit. Examples of Opportunity An organization s Executive Director has a dynamic personality. As a result, the Executive Director has a great deal of power of the board of directors and staff. An organization s bookkeeper/office manager is responsible from everything from answering the phones to writing checks to making deposits. There is basically no oversight of the bookkeeper/office manager. Examples of Opportunity A church relies heavily on volunteers that are not subject to oversight in many financial areas (purchasing items, counting offerings, etc.). An organization receives contributions to assist those in need in the community. As part of its mission, it distributes food, clothing and gift cards to individuals to help them through difficult times. 7

8 Rationalization Being able to rationalize a fraudulent act as being consistent with their personal code of ethics. It s okay to commit fraud because or I am not really doing anything wrong because Examples of Rationalization Nonprofit employees are often paid less than their counterparts in the private sector. Some nonprofit employees rationalize the misappropriation of physical assets as compensation for their low salaries. Nonprofit employees may feel pressured to appear efficient and effective to attract donors or obtain grant funds. These circumstances, when combined with pressure to provide high levels of service, may create an environment in which employees are able to rationalize perpetrating fraud. Examples of Rationalization Lack of ownership attributes in nonprofits may result in an additional fraud risk. The existence of owners is sometimes a fraud deterrent. Employees are less prone to defraud an actual person. An organization s payroll supervisor has grown dissatisfied with her position due to lack of raises, rejections for the request of an assistant, and requests to reduce her hours due to budget constraints. 8

9 Fraud Basics No matter the size of the entity, the execution of the fraud is similar. Commits fraud receives benefits conceals fraud Internal frauds Fraudulent financial reporting Asset misappropriation Fraudulent Financial Reporting Intentional misstatements or omissions designed to deceive financial statement users Accomplished by Manipulation, falsification, or alteration of accounting records or supporting documents Misrepresentation in, or intentional omission from, the financial statements Intentional misapplication of accounting principles Fraudulent Financial Reporting Revenue Overstating revenue or delayed revenue to meet budgeted amounts Improper determination of when membership dues earnings process is complete Pressure to generate positive operating results may take an aggressive approach to recording grant revenue Failure to report receivables in the correct period Holding records open beyond the period end date to inflate revenues Misclassifying restricted donations 9

10 Fraudulent Financial Reporting Expenses Overstating expenses Understating expenses Failure to report accounts payable in the correct period Misclassifying expenses regarding the funds used for programs Improper allocation of expenses by function Improper allocation of fund raising expenses Fraudulent Financial Reporting Mgmt Override Ability to manipulate accounting records and prepare fraudulent financial statements by overriding controls that otherwise appear to operate effectively Journal entries Accounting estimates Allowances for uncollectible receivables Estimated useful lives of capital assets Estimates of accrued compensated absences Estimated contingent liabilities for litigation or claims Circumstances that May Indicate Fraudulent Financial Reporting Significant or unusual adjustments at year end Documentation relating to cash receipts that is missing or altered Cash flow from operating activities inconsistent with actual cash flow Unusual or unexplained fluctuations from year to year or budgeted to actual Significant related party transactions or failing to report related party transactions Transactions that have been pre or post dated from the actual transaction date 10

11 Misappropriation of Assets Actual theft of an entity s assets Accomplished by: Causing an organization to pay for goods and services not received Using an organization s assets for personal use or simply stealing the organization s assets Embezzling receipts Misappropriation of Assets Skimming Theft of donated merchandise Credit card abuse Fictitious vendor schemes Ghost employees Overstatement of hours worked Fictitious expenditures Outright theft of the organization s property Personal use of the organization s assets and other resources Circumstances that May Indicate Misappropriation of Assets Missing or out of sequence blank checks Significant bank reconciling items without reasonable explanation Second payee or unusual endorsement on checks Missing cancelled checks Unusual disbursement transactions or transactions lacking sufficient supporting documentation Complaints about amounts owed to the organization (for services rendered, contribution pledges, etc.) 11

12 Circumstances that May Indicate Misappropriation of Assets Missing, unusual looking or altered time an attendance records Time and attendance records signed by someone other than the usual supervisor Unusual vendor names and addresses Copies of invoices, purchase orders or receiving documents rather than the original Orders for material or supplies already on hand in sufficient quantities or that are not consistent with the organization s mission Actual Fraud Cases Organization A Who: Treasurer How much: More than $20,000 How: Used organization s funds for personal use. Most was taken through ATM withdrawals not authorized by the organization s members. Time period: June 2011 February 2014 Charged in Allen Superior Court Actual Fraud Cases Organization B Who: Finance Manager How much: More than $130,000 How: Created false invoices from an unnamed company, recorded payments for equipment the organization had not bought in its ledgers. Money was then routed to the Finance Manager s bank account in amounts ranging from $100 to $17,890. Time period: 3 year period beginning shortly after October 2009 Arrested by the FBI after a federal grand jury handed down a 20 count criminal indictment. 12

13 Actual Fraud Cases Organization C Who: Executive Director How much: Approximately $30,000 How: Paid herself in addition to her normal pay without board approval. Time period: August 2011 August 2012 Charged in Allen Superior Court with a felony count of corrupt business influence. Actual Fraud Cases Organization D Who: Executive Director How much: Approximately $1,500 How: Used a debit card issued to the organization for personal items and to pay personal bills. Time period: July 2009 September 2010 Pled guilty to 4 counts of theft, each a class D felony. Actual Fraud Cases Organization E Who: Bookkeeper How much: More than $364,000 How: Wrote checks to her business from the organization s checking account. The checks were then deposited into her business account and subsequently transferred into personal account. The checks were listed in the organization s records as payments to a local nonprofit. When the checks were returned from the bank, the Bookkeeper altered the payee from her business name to a vendor used by the organization. Time period: June 2004 April 2009 Indicted by U.S. District Court on 10 counts, ranging from wire fraud to tax evasion. 13

14 Actual Fraud Cases Organization F Who: Director of Finance How much: More than $276,000 How: Used electronic funds transfers from the organization s accounts to pay his personal credit cars and medical bills and to buy cars and motorcycles. Time period: June 2004 July 2008 Charged with 8 counts of theft and one count of fraud. Actual Fraud Cases Organization G Who: Administrative Assistant How much: $95,000 How: Used the organization s credit cards, transferred money and wrote checks to herself. More than 140 checks had forged signatures. Time period: Over 5 years (sentenced in 2006) Sentenced to 5 months in prison and 5 months home detention and ordered to repay the $95,000 she stole. Actual Fraud Cases Organization H Who: Treasurer How much: $8,570 How: Opened an unauthorized charge card at Sam s Club and used the organization s money for personal use. Time period: August 2006 August 2007 Faced theft and fraud charges. 14

15 Fraud Warning Signs Employees that refuse to take vacation High turnover Lifestyle or behavioral changes; employees living beyond their means Check requests for reimbursement that do not contain original receipts Unusual or unexplainable variances in financial statements Misreporting functional expense classification (little or no management and general or fund raising) Financial records are disorganized Bounced checks Fraud Warning Signs Old accounts receivable balances Large amount of journal entries Journal entries to cash or with round amounts Lack of thank you letters Budget cutbacks Anonymous tips How to Prevent and Detect Fraud Tone at the top Asses fraud risks Segregation of duties* Screen employees Reconcile regularly Provide training Encourage whistle blowing Restrict access 15

16 How to Prevent Fraud Purchase bonding insurance Institute job rotation and mandatory vacations Perform ratio analysis Provide board oversight Review journal entries Proper approval of voids and credit memos Use checks in sequential order Never allow checks to be pre signed How to Prevent Fraud Provide contribution receipts for donors Communicate with donors Request multiple quotes from different vendors Proper documentation for disbursements Require two signatures Conduct a fixed asset inventory Do not rely on your external audit Segregation of Duties Separate responsibilities of Authorizing Recording Maintaining transactions transactions custody of assets 16

17 Segregation of Duties Community Foundation internal controls documentation For those organizations that do not have multiple accounting staff, non accounting personnel such as an office manager can be trained to perform less technical duties. Also board members, such as the board treasurer, can be utilized to further segregate duties. Segregation of Duties 2 person staff Executive Director Receives and lists receipts Makes bank deposits Approves invoices Signs checks Mails checks Opens and reviews bank statements Reviews bank reconciliations Approves journal entries Accounting Staff Prepares bank deposits Enters receipts into the general ledger Writes/prints checks Reconciles bank statement Records journal entries Segregation of Duties 3 person staff Executive Director Prepares bank deposits Signs checks Reviews bank reconciliations Approves journal entries Accounting Staff #1 Enters receipts into the general ledger Writes/prints checks Reconciles bank statement Records journal entries Accounting Staff #2 Receives and lists receipts Makes deposits Approves invoices Mails checks Opens and reviews bank statements 17

18 Questions? Dulin, Ward & DeWald, Inc Dupont Circle Drive West, Suite 300 Fort Wayne, Indiana minded nonprofits Carrie Minnich, CPA, MAcct Jenny Lemmon, CPA, CFE 18

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Lecture notes for: Corporate Cons

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture Notes for How to Steal $500 Million

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

FRAUD TRENDS TO WATCH FOR IN Presented by: Daniel J. Mahalak

FRAUD TRENDS TO WATCH FOR IN 2018 Presented by: Daniel J. Mahalak Session Overview In recent years, fraud has seemingly been increasing in credit unions. Some of this fraud is related to the technology

FRAUD TRENDS TO WATCH FOR IN 2018 Presented by: Daniel J. Mahalak Session Overview In recent years, fraud has seemingly been increasing in credit unions. Some of this fraud is related to the technology

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Safeguarding the Financial Assets of Your Church. Indiana Conference of the United Methodist Church

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Mitigating Fraud. June 22, Sept. 21, 2014

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Grant Fraud. Leslie Les Hollie Assistant Inspector General For Investigations

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

OCCUPATIONAL FRAUD 9/20/2018

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

Delivering Financial Oversight: Strengthening Your Policies and Procedures

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Fraud in Government. Mike Nolan, CPA, CFE, CGMA. CCACC & CCA&RMC Conference Monterey, CA September 2014

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

OAPT June 9, Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

Fraud prevention for credit unions

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

International Standard on Auditing (Ireland) 240

240") International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

Looking for Fraud Through Rose-Colored Glasses

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Chapter 2 Skimming. 2. To a fraudster, the principle advantage of skimming is the difficulty with which the scheme is detected. a. True b.

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Delivering Confidence PAGE 1

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

The Auditor s Responsibilities. Audit of Financial Statements

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

A c f e. Report to. the Nation. on Occupational Fraud & Abuse

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

International Standard on Auditing (UK) 240 (Revised June 2016)

240 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

THE SCHOOL DISTRICT OF GREENVILLE COUNTY

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Fraud: How to Get Your District Free Publicity

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

Solutions. I. Auditing Cash and Cash Equivalents. A. Learning Question Answers

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

November 2017 ICPAK FORENSIC AUDIT SEMINAR

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

Fraud in Nonprofits: Real Stories. Presented by: Mike Hablewitz, CPA, Senior Manager

Fraud in Nonprofits: Real Stories Presented by: Mike Hablewitz, CPA, Senior Manager Fraud Triangle 3 factors are generally present in any fraud: Pressure Rationalization Fraud Triangle! Opportunity Case

Fraud in Nonprofits: Real Stories Presented by: Mike Hablewitz, CPA, Senior Manager Fraud Triangle 3 factors are generally present in any fraud: Pressure Rationalization Fraud Triangle! Opportunity Case

AGA Risk and Fraud Webinar

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

INTERNAL FRAUD PREVENTION:

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

CRIMEGUARD CHOICE SM Fidelity and Crime Insurance APPLICATION. Name of Applicant: Principal Address: Date Business Established: Annual Revenues:

GENERAL INFORMATION National Union Fire Insurance Company of Pittsburgh, Pa. (a capital stock company, herein called the Company ) Executive Offices: 175 Water Street New York, NY 10038 CRIMEGUARD CHOICE

GENERAL INFORMATION National Union Fire Insurance Company of Pittsburgh, Pa. (a capital stock company, herein called the Company ) Executive Offices: 175 Water Street New York, NY 10038 CRIMEGUARD CHOICE

Cash and Internal Control C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE GLObAL FrAUD STUDy

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

An Overview of Fraud Risk. Presented by: Rick Potocek CPA MBA CFE

An Overview of Fraud Risk Presented by: Rick Potocek CPA MBA CFE To raise awareness of: Who commits fraud and why Red flags to consider Simple steps to take to immediately reduce the risk of fraud According

An Overview of Fraud Risk Presented by: Rick Potocek CPA MBA CFE To raise awareness of: Who commits fraud and why Red flags to consider Simple steps to take to immediately reduce the risk of fraud According

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

Financial Transactions and Fraud Schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT MODERATOR: LAURIE DE ARMOND TIM MOHR, MIKE SORRELLS AND RANDAL SIMONETTI DECEMBER 9, 2013 BDO USA, LLP, a Delaware limited liability partnership,

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT MODERATOR: LAURIE DE ARMOND TIM MOHR, MIKE SORRELLS AND RANDAL SIMONETTI DECEMBER 9, 2013 BDO USA, LLP, a Delaware limited liability partnership,

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Financial Statements. Financial Statement Analysis and Budget Tracking. What is Financial Statement Analysis? 3/20/2013

Financial Statement Analysis and Budget Tracking by Donna M. Ingram, CPA, CFE, Cr.FA, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com What is Financial Statement Analysis? Financial statement analysis

Financial Statement Analysis and Budget Tracking by Donna M. Ingram, CPA, CFE, Cr.FA, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com What is Financial Statement Analysis? Financial statement analysis

Employee Benefit Plans DOL Criminal Enforcement Cases April 2009 November 2011

Employee Benefit Plans DOL Criminal Enforcement Cases April 2009 November 2011 The AICPA Employee Benefit Plan Audit Quality Center has developed this summary analysis of the U.S. Department of Labor (DOL)

Employee Benefit Plans DOL Criminal Enforcement Cases April 2009 November 2011 The AICPA Employee Benefit Plan Audit Quality Center has developed this summary analysis of the U.S. Department of Labor (DOL)

Finacial Statement Fraud. Peter N Munachewa, CFE Risk Management Consultant

Finacial Statement Fraud Peter N Munachewa, CFE Risk Management Consultant What is FSF Falsification, alteration, or manipulation of material financial records, supporting documents, or business transactions

Finacial Statement Fraud Peter N Munachewa, CFE Risk Management Consultant What is FSF Falsification, alteration, or manipulation of material financial records, supporting documents, or business transactions

Chapter 2 Skimming 1

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

LOCAL CHURCH AUDIT GUIDE

LOCAL CHURCH AUDIT GUIDE Rev. Aug 2017 This booklet is given to you as a service of the Committee on Audit and Review of the General Council on Finance and Administration of The United Methodist Church

LOCAL CHURCH AUDIT GUIDE Rev. Aug 2017 This booklet is given to you as a service of the Committee on Audit and Review of the General Council on Finance and Administration of The United Methodist Church

Campus Financial Sub-Certification - Explanation

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

Second Annual Nonprofit Executive Summit:

Second Annual Nonprofit Executive Summit: Bringing Nonprofit Leaders Together to Discuss Legal, Finance, Tax, and Operational Issues Impacting the Sector Thursday, October 2, 2014 Venable LLP Washington,

Second Annual Nonprofit Executive Summit: Bringing Nonprofit Leaders Together to Discuss Legal, Finance, Tax, and Operational Issues Impacting the Sector Thursday, October 2, 2014 Venable LLP Washington,

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

COVERAGE FRAUD IN EMPLOYEE BENEFIT PLANS 5/15/2014. Where employee benefit fraud is likely. Internal controls that help prevent fraud

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

ACFE CFEX. Certified Fraud Examiner (CFEX)

") ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

Insights Into Accounting Schemes and Scams

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

Fraud Risk Assessment

Fraud Risk AHIA Southeast Regional Seminar Houston Texas Friday, November 12, 2010 Today s Discussion Agenda What is fraud? Industry fraud statistics Common fraud scenarios Fraud risk assessment (FRA)

Fraud Risk AHIA Southeast Regional Seminar Houston Texas Friday, November 12, 2010 Today s Discussion Agenda What is fraud? Industry fraud statistics Common fraud scenarios Fraud risk assessment (FRA)

(No., Street) Present Crime Insurance Program: (Include primary AND excess, if applicable) If not applicable, please check here:

Present Crime Insurance Program: (Include primary AND excess, if applicable) If not applicable, please check here:") , a stock insurance company, herein called the Insurer THE HARTFORD CRIMESHIELD SM ADVANCED POLICY APPLICATION FOR NON-CUSTODIAL INVESTMENT ADVISERS (FIRST PARTY) Agency Name: Hartford Agency Code: Application

, a stock insurance company, herein called the Insurer THE HARTFORD CRIMESHIELD SM ADVANCED POLICY APPLICATION FOR NON-CUSTODIAL INVESTMENT ADVISERS (FIRST PARTY) Agency Name: Hartford Agency Code: Application

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

POLICY APPLICATION for COMMERCIAL and GOVERNMENTAL ENTITIES

, a stock insurance company, herein called the Insurer CrimeSHIELD SM POLICY APPLICATION for COMMERCIAL and GOVERNMENTAL ENTITIES Agency Name: Hartford Agency Code: Application is hereby made by: (First

, a stock insurance company, herein called the Insurer CrimeSHIELD SM POLICY APPLICATION for COMMERCIAL and GOVERNMENTAL ENTITIES Agency Name: Hartford Agency Code: Application is hereby made by: (First

5/15/2015. Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace

Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace by Donna M. Ingram, CPA, CFE, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Luca Pacioli, the "Father of Accounting",

Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace by Donna M. Ingram, CPA, CFE, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Luca Pacioli, the "Father of Accounting",

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Fraud in the Government Realm. Introduction. What is Fraud? My career began with a local government fraud in 1993

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

The 2015 Hiscox Embezzlement Watchlist: A Snapshot of Employee Theft in the US

The 2015 Hiscox Embezzlement Watchlist: A Snapshot of Employee Theft in the US CONTENTS Introduction...1 The At-Risk Organization...2 Common Themes, Common Schemes...3 Industries in Focus...4 The Employee,

The 2015 Hiscox Embezzlement Watchlist: A Snapshot of Employee Theft in the US CONTENTS Introduction...1 The At-Risk Organization...2 Common Themes, Common Schemes...3 Industries in Focus...4 The Employee,

Financial Institutions Bond Application Form 24 for Commercial Banks, Savings Banks and Savings and Loan Associations New Business Application

General Information 1. Name of Applicant: 2. Address of Applicant: Please attach a list of all subsidiaries including operations, percent of ownership and the date acquired or created. (te: The application

General Information 1. Name of Applicant: 2. Address of Applicant: Please attach a list of all subsidiaries including operations, percent of ownership and the date acquired or created. (te: The application

Fraud and Understanding Fraud Basics MACC Expo Charles A. Albert, CPA/CFE Curtis Blakely and Co, PC, CPAs

Fraud and Understanding Fraud Basics 2017 MACC Expo Charles A. Albert, CPA/CFE Curtis Blakely and Co, PC, CPAs o o o o Qualifications Curtis Blakely And Co, CPAs, PC has been serving the utility industry

Fraud and Understanding Fraud Basics 2017 MACC Expo Charles A. Albert, CPA/CFE Curtis Blakely and Co, PC, CPAs o o o o Qualifications Curtis Blakely And Co, CPAs, PC has been serving the utility industry

JACKSON PARISH HOSPITAL SERVICE DISTRICT NO. 1

JACKSON PARISH HOSPITAL SERVICE DISTRICT NO. 1 INVESTIGATIVE AUDIT APRIL 8, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE

JACKSON PARISH HOSPITAL SERVICE DISTRICT NO. 1 INVESTIGATIVE AUDIT APRIL 8, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE

Analyzing a Potpourri of Fraud in Higher Education. Calvin Wendelboe, CPA, CIA, CFE

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Additional Information on the Dirty Dozen

Additional Information on the Dirty Dozen 1. Identity Theft Topping this year s list Dirty Dozen list is identity theft. In response to growing identity theft concerns, the IRS has embarked on a comprehensive

Additional Information on the Dirty Dozen 1. Identity Theft Topping this year s list Dirty Dozen list is identity theft. In response to growing identity theft concerns, the IRS has embarked on a comprehensive

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Finance. Financial Accountability 02/09/2018. Financial Accountability for Nonprofits. Finance Sales Tax Best Practices Accountability Risk Management

Financial Accountability Important Stuff Nonprofit Boards MUST Know Presenter Miriam Robeson, Attorney February 9, 2018 Financial Accountability for Nonprofits Finance Sales Tax Best Practices Accountability

Financial Accountability Important Stuff Nonprofit Boards MUST Know Presenter Miriam Robeson, Attorney February 9, 2018 Financial Accountability for Nonprofits Finance Sales Tax Best Practices Accountability

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

COMMUNITY TRANSPORTATION NETWORK, INC.

COMMUNITY TRANSPORTATION NETWORK, INC. FINANCIAL STATEMENTS Year Ended June 30, 2018 With Summarized Information for the Year Ended June 30, 2017 TABLE OF CONTENTS PAGE NO. INDEPENDENT AUDITORS' REPORT...

COMMUNITY TRANSPORTATION NETWORK, INC. FINANCIAL STATEMENTS Year Ended June 30, 2018 With Summarized Information for the Year Ended June 30, 2017 TABLE OF CONTENTS PAGE NO. INDEPENDENT AUDITORS' REPORT...

The State of the Art of Fraud. Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

Have you dealt with fraud in the past?

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

Illustrate by way of some example how Fraudulent Financial Reporting and Misappropriation of Asset can be done?

SA240(R) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL What is a Fraud? Intentional mistakes to get unjust advantage are commonly known as fraud. Fraud as defined by SA 240

SA240(R) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL What is a Fraud? Intentional mistakes to get unjust advantage are commonly known as fraud. Fraud as defined by SA 240

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations