Forensic Data Mining Finding Needles in the Haystack. Bank Fraud Investigations

|

|

|

- Wilfrid Austin

- 5 years ago

- Views:

Transcription

1 acumen insight ideas Forensic Data Mining Finding Needles in the Haystack Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant BKD, LLP attention reach expertise depth agility talent Bank Fraud Investigations Kickbacks on loans Data center manager online entries to move money to personal accounts CFO walking transactions to proof moving money to personal account Fictitious loans recorded by bank presidents & chief lending officers Fictitious financial statements submitted by business customers SBA loan fraud

Trust officers misusing")

2 Bank Fraud Investigations Undisclosed ownership interests in loan customers & conflicts of interest Host of schemes to manipulate past due loans &/or payment dates or roll loans over & over Variety of purchasing schemes generally amounting to paying personal expenses Schemes by bank customers to abscond with various types of loan collateral (often in bankruptcies) Trust officers misusing customer funds Straw Loans & Reg O Violations acumen insight ideas attention reach expertise depth agility talent 2008 by the Association of Certified Fraud Examiners, Inc.

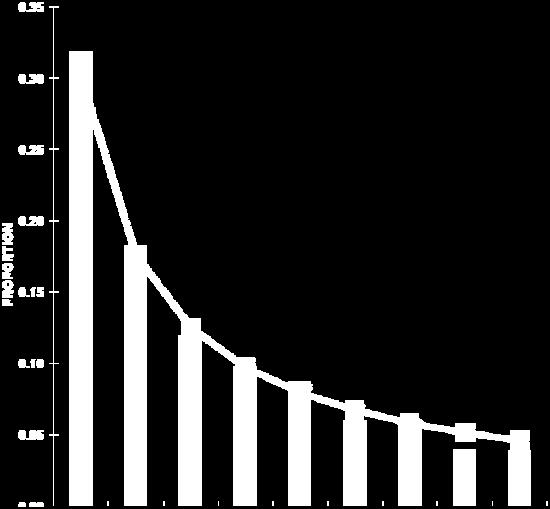

3 Cost of Fraud & Abuse $994 billion annually 7% of revenues 42% recover nothing after fraud is discovered Victim Organizations 2008 by the Association of Certified Fraud Examiners, Inc. 6

4 Victim Organizations Occupational Fraud Schemes in Banking & Financial Services Industry (132 cases) The sum of percentages in this chart exceeds 100 percent because several cases involved multiple schemes from more than one category by the Association of Certified Fraud Examiners, Inc. Profile of Fraud Perpetrator Male or female No prior criminal history (<8%) Well liked by co-workers Likes to give gifts/compulsive shopper Gambling problems not unusual Long-term employee Rationalizes: Starts small or borrows Lifestyle clues

5 Bank Specific Characteristics Credit problems NSF in personal accounts Unusual transactions in personal accounts Management override of internal controls Less experienced employees unknowingly aid Second person signs off on transaction based on trust Why Forensic Data Mining? 30% of all frauds are found by analysis vs. tips, accidental discovery & disclosure (David Coderre, Fraud Detection: A Revealing Look at Fraud ) More efficient & effective than traditional sampling Can help find needle in a haystack 100% analysis is the most effective way to analyze for fraud (Dr. Conan Albrecht, BYU)

6 Data Cleansing , (417) , , Missoura, MO, Mis, Miss, MZ, MS, Miz, Mizz , , PO Box 34, P.O. Box 34, Box 34, Bx 34, P.O Box 34 Mallery, Malery, Mallrey, Mallory, Malory Common Data Mining Areas Employees & Payroll Vendors & Accounts Payable Expense Reimbursement Loans (for financial institutions only) Sales Inventory

7 Vendor Trending Analysis Time Series Analysis: Acceleration Vendor: JLM Plumbing Authorized: Janice L. McPhearson Acceleration as confidence builds Getting Greedy Test phase Name Mining Anagrams

8 Name Mining Anagrams Address Mining Maildrops Fictitious Vendor with UPS Store Address

9 Name & Address Mining Name & ID analysis Direct matching Phonetic matching (Double Metaphone Hybrid) Compare to known name dictionaries Anagram search Duplicate Employee ID / SSN, Invalid SSNs Address analysis Direct matching No address, invalid address, PO/RR address Proximity by latitude/longitude lookup Address is known mailbox service (FedEx Kinkos, UPS Store, etc.) Visual Map Analysis Address Matching Address match example

10 Employee Vendor Proximity Benford s Law Analysis

11 Benford s Law Payroll Normal Pattern Benford s Law Payroll Abnormal Pattern?

12 Benford s Law A/P Benford s Law A/P

via time series analysis Duplicate invoices")

13 Check Sequence Analysis Accounts Payable Mining AP: Fictitious vendors, duplicate payments, etc. Benford s analysis Acronym search on employee name Acceleration (systematic spending increases) via time series analysis Duplicate invoices Duplicate payments Identify invoices in excess of n% of vendor average Compare PO/invoice amount to check amount Identify transactions ending in 5 or 0 Baseline vendor activity against overall activity Classify transactions by clerk/approver Compare multiple vendor master files over 3 years Identify statistical outliers (Z-score method)

14 Payroll Mining Payroll detail Employees with no deductions PR activity subsequent to termination Employee vs department baselines ($ & hrs) Department vs company baselines ($ & hrs) Benford's analysis of gross / net payroll Time series analysis Employee with no sick/vacation/time off Computed pay rate vs. Employee master rate Compare actual pay rates to rate schedule Other analysis Duplicate phone number(s) Duplicate direct deposit accounts Short duration of hire/termination Loan Master & Maintenance Fictitious loans Straw loans Unknown relationships Subprime lending Multiple renewals Slow or no amortization Manipulation of past due loans Manipulation of due dates

15 Loan Maintenance File Interest rate manipulations Past due manipulations Maintenance by user Be Alert To PO boxes Unusual items being passed at teller line Suspense accounts do not reconcile Trust activity w/o proper authorization TIN used on accounts with different names No phone Business account w/ no business phone

16 Be Alert To Transactions brought directly to proof Loans to employees not meeting requirements Insiders loaning personal funds to customers or borrowing from customers Insiders appear to give or receive favors to (from) customers Insiders involved in business that borrows from bank Be Alert To Insider with heavy debt that appears to require most or all of salary Financing of insider sale of personal assets to third party Insider relationship with shady characters or high rollers Insider keeps unusual number of customer files at their desk

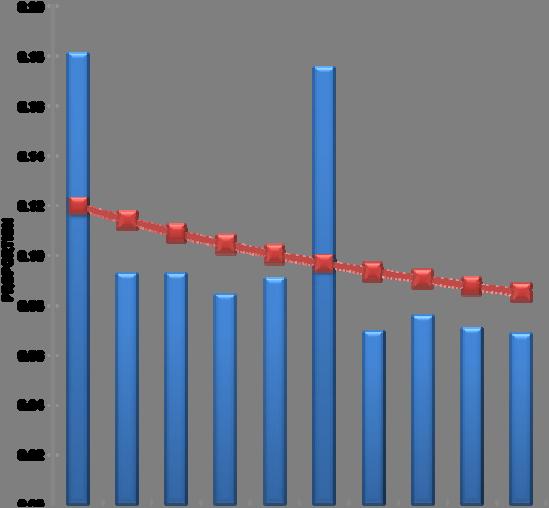

17 Be Alert To Insider making payments on another borrower s loans Insider frequently takes documents outside bank for customer signature Insider processes transactions in absence of customer as special favors Changes to loan master file due dates Detection of Fraud Schemes Initial Detection of Occupational Frauds 4 4 The sum of percentages in this chart exceeds 100 percent because in some cases respondents identified more than one detection method by the Association of Certified Fraud Examiners, Inc.

18 Five Things to Remember 1. Review personal accounts of employees & officers 2. Perform data mining of loan master & maintenance files 3. Train tellers not to accept unusual transactions from insiders 4. Encourage questioning & reporting unusual transactions have confidential hotline 5. Be aware of relationships between insiders & loan customers Questions?

19 Contact Information Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant BKD, LLP 901 E. St. Louis Street Springfield, MO Phone: Fax:

Internal Bank Fraud Schemes & Scams in an Economic Downturn. Fictitious Loans. Bank Fraud Investigations. Tracking spreadsheet Affidavit 1 Affidavit 2

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

7/21/2015. July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT. Lessons from the Trenches. Angela Morelock Partner

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

1/3/2012. Cooking the Books: Financial Statement Fraud Issues & Examples. Financial Statement Fraud

Cooking the Books: Financial Statement Fraud Issues & Examples Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant Financial Statement Fraud Def. Deliberate fraud committed

Cooking the Books: Financial Statement Fraud Issues & Examples Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant Financial Statement Fraud Def. Deliberate fraud committed

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Insights Into Accounting Schemes and Scams

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Is Your Construction Project a Victim of Fraud?

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

INCREASING INVESTIGATOR EFFICIENCY USING NETWORK ANALYTICS

INCREASING INVESTIGATOR EFFICIENCY USING NETWORK ANALYTICS ACFE ANNUAL CONFERENCE ORLANDO, FL JUNE 20, 2012 DAN BARTA CPA, CFE DAVID STEWART CAMS Fraud & Financial Crimes Practice TOPICS INCREASING INVESTIGATOR

INCREASING INVESTIGATOR EFFICIENCY USING NETWORK ANALYTICS ACFE ANNUAL CONFERENCE ORLANDO, FL JUNE 20, 2012 DAN BARTA CPA, CFE DAVID STEWART CAMS Fraud & Financial Crimes Practice TOPICS INCREASING INVESTIGATOR

Employee Dishonesty Lessons Learned: Internal Controls

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Figure 1: Occupational Frauds by Category Frequency

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

INTERNAL FRAUD PREVENTION:

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

Palomar Community College District Procedure AP 5900 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS

1 STUDENT SERVICES 2 3 AP 5900 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 References: Fair

1 STUDENT SERVICES 2 3 AP 5900 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 References: Fair

Number: Identity Theft Program Procedures and Protocol Responsible Office: Business and Finance

POLICY USF System USF USFSP USFSM Number: 0-109 Title: Identity Theft Program Procedures and Protocol Responsible Office: Business and Finance Date of Origin: 1-11-11 Date Last Amended: Date Last Reviewed:

POLICY USF System USF USFSP USFSM Number: 0-109 Title: Identity Theft Program Procedures and Protocol Responsible Office: Business and Finance Date of Origin: 1-11-11 Date Last Amended: Date Last Reviewed:

Demystifying Forensic Accounting

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com Adrian Sierra, CPA, CFE, CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com Adrian Sierra, CPA, CFE, CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining

Riverside Community College District Policy No Student Services PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS

Riverside Community College District Policy No. 5900 Student Services BP 5900 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS Reference: Fair and Accurate Credit Transactions Act, (15 U.S.C.

Riverside Community College District Policy No. 5900 Student Services BP 5900 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS Reference: Fair and Accurate Credit Transactions Act, (15 U.S.C.

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

Fraud Examination. Prevention, Detection, and Investigation. Steven M. Bragg

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Looking for Fraud Through Rose-Colored Glasses

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Crime Coverage Section Application (Large Public Company > $1B revenues)

") Crime Coverage Section Application (Large Public Company > $1B revenues) BY COMPLETING THIS CRIME APPLICATION THE APPLICANT IS APPLYING FOR COVERAGE WITH CHUBB INSURANCE COMPANY OF CANADA (THE COMPANY

Crime Coverage Section Application (Large Public Company > $1B revenues) BY COMPLETING THIS CRIME APPLICATION THE APPLICANT IS APPLYING FOR COVERAGE WITH CHUBB INSURANCE COMPANY OF CANADA (THE COMPANY

SXU Financial Statement Fraud

SXU Financial Statement Fraud Quiz Three INSTRUCTIONS: There are a total of 61 questions on this quiz. Each question has a value of four points. You may choose any 25 questions to answer. If you answer

SXU Financial Statement Fraud Quiz Three INSTRUCTIONS: There are a total of 61 questions on this quiz. Each question has a value of four points. You may choose any 25 questions to answer. If you answer

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

To Receive CPE Credit

May 14, 2014 I Purchased a Company... But What Did I Buy??? Rand Gambrell, CPA, ABV, CFE, CFF, CVA Director Forensics & Valuation Services rgambrell@bkd.com experience expertise // Elevate your understanding

May 14, 2014 I Purchased a Company... But What Did I Buy??? Rand Gambrell, CPA, ABV, CFE, CFF, CVA Director Forensics & Valuation Services rgambrell@bkd.com experience expertise // Elevate your understanding

An Overview of Fraud Risk. Presented by: Rick Potocek CPA MBA CFE

An Overview of Fraud Risk Presented by: Rick Potocek CPA MBA CFE To raise awareness of: Who commits fraud and why Red flags to consider Simple steps to take to immediately reduce the risk of fraud According

An Overview of Fraud Risk Presented by: Rick Potocek CPA MBA CFE To raise awareness of: Who commits fraud and why Red flags to consider Simple steps to take to immediately reduce the risk of fraud According

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

TOOLS FOR FRAUD DETERRENCE AND DETECTION BUILDING A HOUSE OF CARDS: USING THE REVERSE ENTRY TO HIDE FRAUD

TOOLS FOR FRAUD DETERRENCE AND DETECTION BUILDING A HOUSE OF CARDS: USING THE REVERSE ENTRY TO HIDE FRAUD Financial statement accounts can, when used together in a specific way, perpetrate fraud and even

TOOLS FOR FRAUD DETERRENCE AND DETECTION BUILDING A HOUSE OF CARDS: USING THE REVERSE ENTRY TO HIDE FRAUD Financial statement accounts can, when used together in a specific way, perpetrate fraud and even

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Great Internal Controls and Then IT Happens Fraud!

Then IT Happens Fraud! Pamela Mantone, CPA, CFE, CFF, CITP, CGMA, FCPA, MAFF Pamela S. Mantone CPA, CFF, CFE, MAFF, CITP, CGMA, FCPA Director April 21, 2016 This material was used by Elliott Davis Decosimo

Then IT Happens Fraud! Pamela Mantone, CPA, CFE, CFF, CITP, CGMA, FCPA, MAFF Pamela S. Mantone CPA, CFF, CFE, MAFF, CITP, CGMA, FCPA Director April 21, 2016 This material was used by Elliott Davis Decosimo

5/15/2015. Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace

Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace by Donna M. Ingram, CPA, CFE, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Luca Pacioli, the "Father of Accounting",

Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace by Donna M. Ingram, CPA, CFE, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Luca Pacioli, the "Father of Accounting",

How to Bulletproof Your Expert: Surviving Daubert Challenges to Accounting Expert Opinions & Damage Calculations

How to Bulletproof Your Expert: Surviving Daubert Challenges to Accounting Expert Opinions & Damage Calculations James Snyder, JD, CFE Managing Partner Angela Morelock, CPA, CFE, CFF, ABV, CrFA Partner

How to Bulletproof Your Expert: Surviving Daubert Challenges to Accounting Expert Opinions & Damage Calculations James Snyder, JD, CFE Managing Partner Angela Morelock, CPA, CFE, CFF, ABV, CrFA Partner

PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS

Reference: 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA)) I. The Purpose of the Identity Theft Prevention Program The purpose of this Identity Theft Prevention

Reference: 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA)) I. The Purpose of the Identity Theft Prevention Program The purpose of this Identity Theft Prevention

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

Figure 1: Breakdown of Cases by Country

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS

Last Reviewed May 24, 2016 AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS Reference: 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA))

Last Reviewed May 24, 2016 AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS Reference: 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA))

IIA Fraud Conference. Case studies from recent investigations. 8 April 2015

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Prevention of Identity Theft in Student Financial Transactions

AP 5800 Reference: Prevention of Identity Theft in Student Financial Transactions 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA)) Date Issued: November 5,

AP 5800 Reference: Prevention of Identity Theft in Student Financial Transactions 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA)) Date Issued: November 5,

PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS

AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS References: 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA)) I. The Purpose of the Identity

AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS References: 15 U.S. Code Section 1681m(e) (Fair and Accurate Credit Transactions Act (FACT ACT or FACTA)) I. The Purpose of the Identity

Chapter 9. #17 is a bad question if it is changed as follows the answer is d

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Watching the Vault: Employee Dishonesty

Watching the Vault: Employee Dishonesty Managing your most pressing risks NCOFCU 2016 Conference CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group,

Watching the Vault: Employee Dishonesty Managing your most pressing risks NCOFCU 2016 Conference CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group,

Good From The Inside Out. Saturday, April 8, 2017

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Grant Fraud. Leslie Les Hollie Assistant Inspector General For Investigations

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Chapter Five: Student Services and Operations AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS

AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS I. Purpose of the Identity Theft Prevention Program The purpose of this Identity Theft Prevention Program (ITPP) is to control reasonably

AP 5800 PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS I. Purpose of the Identity Theft Prevention Program The purpose of this Identity Theft Prevention Program (ITPP) is to control reasonably

A c f e. Report to. the Nation. on Occupational Fraud & Abuse

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

The role of data analytics in present and future claims cost containment

Image: loveguli / Getty Images The role of data analytics in present and future claims cost containment Dr. Andreas Bayerstadler Senior Consultant Business Analytics Dubai, 12 th September 2018 Wearables

Image: loveguli / Getty Images The role of data analytics in present and future claims cost containment Dr. Andreas Bayerstadler Senior Consultant Business Analytics Dubai, 12 th September 2018 Wearables

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Red Flags of Fraud. What we will cover. Solutions Conference. Sarah L. Jennings, CPA, CFE Principal Maner Costerisan. The Problem Defined

Red Flags of Fraud Solutions Conference Sarah L. Jennings, CPA, CFE Principal Maner Costerisan What we will cover The Problem Defined What Fraud Looks Like How to Identify Red Flags Now What 1 What is

Red Flags of Fraud Solutions Conference Sarah L. Jennings, CPA, CFE Principal Maner Costerisan What we will cover The Problem Defined What Fraud Looks Like How to Identify Red Flags Now What 1 What is

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

Demystifying Forensic Accounting

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com AdrianSierra,CPA,CFE,CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining and

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com AdrianSierra,CPA,CFE,CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining and

Fraud Detection and Prevention for Governmental Organizations. Michael A. Swafford, CIA, CFE

Fraud Detection and Prevention for Governmental Organizations Michael A. Swafford, CIA, CFE Presenter Michael A. Swafford, CIA, CFE Mike is a Consulting Manager in our Forensic Valuation Services Practice

Fraud Detection and Prevention for Governmental Organizations Michael A. Swafford, CIA, CFE Presenter Michael A. Swafford, CIA, CFE Mike is a Consulting Manager in our Forensic Valuation Services Practice

Mortgage Bankers Association of Puerto Rico Mortgage Fraud Prevention Seminar

Mortgage Bankers Association of Puerto Rico 2018 Mortgage Fraud Prevention Seminar Agenda The Federal Housing Finance Agency (FHFA) and the financial crisis The FHFA Office of Inspector General (FHFA-OIG)

Mortgage Bankers Association of Puerto Rico 2018 Mortgage Fraud Prevention Seminar Agenda The Federal Housing Finance Agency (FHFA) and the financial crisis The FHFA Office of Inspector General (FHFA-OIG)

Financial Transaction

Administrative Procedure 5800 Prevention of Identity Theft in Student Financial Transaction I. The Purpose of the Identity Theft Prevention Program The purpose of this Identity Theft Prevention Program

Administrative Procedure 5800 Prevention of Identity Theft in Student Financial Transaction I. The Purpose of the Identity Theft Prevention Program The purpose of this Identity Theft Prevention Program

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

Internal Controls over Expenditures

Internal Controls over Expenditures Trainer: Anthony Gerharz, CPA 1 Materials/Disclaimer Please note that these materials are incomplete without the accompanying oral comments by the trainer(s). These

Internal Controls over Expenditures Trainer: Anthony Gerharz, CPA 1 Materials/Disclaimer Please note that these materials are incomplete without the accompanying oral comments by the trainer(s). These

Surviving The Market NECA National Convention. Seattle, Washington September 2009

Surviving The Market NECA National Convention Seattle, Washington September 2009 1 INTRODUCTION Weber O Brien Ltd. Toledo, Ohio Certified Public Accountants 5580 Monroe Street Sylvania, OH 43560 Telephone:

Surviving The Market NECA National Convention Seattle, Washington September 2009 1 INTRODUCTION Weber O Brien Ltd. Toledo, Ohio Certified Public Accountants 5580 Monroe Street Sylvania, OH 43560 Telephone:

Delivering Financial Oversight: Strengthening Your Policies and Procedures

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Red Flag Rule Procedures Under Princeton University s Identity Theft Prevention Program Effective: December 31, 2010

Red Flag Rule Procedures Under Princeton University s Identity Theft Prevention Program Effective: December 31, 2010 Princeton University employees are responsible for detecting Red Flags consistent with

Red Flag Rule Procedures Under Princeton University s Identity Theft Prevention Program Effective: December 31, 2010 Princeton University employees are responsible for detecting Red Flags consistent with

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Office of Investigations. GEOFFREY CHERRINGTON, DEPUTY ASSISTANT INSPECTOR GENERAL FOR INVESTIGATIONS

Introduction to the GSA OIG Office of Investigations GEOFFREY CHERRINGTON, DEPUTY ASSISTANT INSPECTOR GENERAL FOR INVESTIGATIONS Geoffrey.cherrington@gsa.gov History of the Inspector General The Inspector

Introduction to the GSA OIG Office of Investigations GEOFFREY CHERRINGTON, DEPUTY ASSISTANT INSPECTOR GENERAL FOR INVESTIGATIONS Geoffrey.cherrington@gsa.gov History of the Inspector General The Inspector

Introduction: Section 2: Management of Purchase Cards

Introduction: The Office of Charge Card Management (OCCM) has developed a point by point analysis of S.300, otherwise known as the Charge Card Abuse Prevention Act, in order to illustrate the overlap between

Introduction: The Office of Charge Card Management (OCCM) has developed a point by point analysis of S.300, otherwise known as the Charge Card Abuse Prevention Act, in order to illustrate the overlap between

November 2017 ICPAK FORENSIC AUDIT SEMINAR

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

Subject: Identity Theft, G-113 Department: All & Branches References: Part 717, NCUA Rules and Regs, FACT Act, Companion SOP s G-30 (Opening New

Subject: Identity Theft, G-113 Department: All & Branches References: Part 717, NCUA Rules and Regs, FACT Act, Companion SOP s G-30 (Opening New Accounts), G-38 (E-Commerce), G-40 (Issuance of Visa Cards),

Subject: Identity Theft, G-113 Department: All & Branches References: Part 717, NCUA Rules and Regs, FACT Act, Companion SOP s G-30 (Opening New Accounts), G-38 (E-Commerce), G-40 (Issuance of Visa Cards),

Fraud in the Government Realm. Introduction. What is Fraud? My career began with a local government fraud in 1993

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

Clarion University Identity Theft Prevention Program

Clarion University Identity Theft Prevention Program A) Purpose The purpose of the Identity Theft Prevention Program (Program) is to detect, prevent and mitigate identity theft in connection with any covered

Clarion University Identity Theft Prevention Program A) Purpose The purpose of the Identity Theft Prevention Program (Program) is to detect, prevent and mitigate identity theft in connection with any covered

The Procurement Fraud Equation. Tom Caulfield

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

OAPT June 9, Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

Identity theft detection, prevention and mitigation policy. (a) : policies and procedure for student records;

: policies and procedure for student records;") 3359-11-10.8 Identity theft detection, prevention and mitigation policy. (A) Introduction. (1) The university of Akron is committed to the detection, prevention and mitigation of identity theft associated

3359-11-10.8 Identity theft detection, prevention and mitigation policy. (A) Introduction. (1) The university of Akron is committed to the detection, prevention and mitigation of identity theft associated

The State of the Art of Fraud. Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

CoreLogic Credco First American Way Poway, CA (800)

") Red Flag Regulation WHAT IT IS The Red Flag Regulation implements Sections 114 and 315 of the FACT Act. It finalizes three distinct requirements two of which are relevant to automotive, RV and marine dealers,

Red Flag Regulation WHAT IT IS The Red Flag Regulation implements Sections 114 and 315 of the FACT Act. It finalizes three distinct requirements two of which are relevant to automotive, RV and marine dealers,

Solutions. I. Auditing Cash and Cash Equivalents. A. Learning Question Answers

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

ADMINISTRATIVE PROCEDURE 5800 DESERT COMMUNITY COLLEGE DISTRICT

ADMINISTRATIVE PROCEDURE 5800 DESERT COMMUNITY COLLEGE DISTRICT PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS The purpose of this Identity Theft Prevention Program (ITPP) is to control

ADMINISTRATIVE PROCEDURE 5800 DESERT COMMUNITY COLLEGE DISTRICT PREVENTION OF IDENTITY THEFT IN STUDENT FINANCIAL TRANSACTIONS The purpose of this Identity Theft Prevention Program (ITPP) is to control

Cash and Internal Control C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags

Forensic Services Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags 2 What % of revenues are lost to fraud? 5% Source: 2016 ACFE Report to the Nations 3 Has your

Forensic Services Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags 2 What % of revenues are lost to fraud? 5% Source: 2016 ACFE Report to the Nations 3 Has your

Fraud prevention for credit unions

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

FRAUD EXAMINERS MANUAL (INTERNATIONAL EDITION)

") TABLE OF CONTENTS SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES OCCUPATIONAL FRAUDS ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 FINANCIAL STATEMENT FRAUD What Is Financial

TABLE OF CONTENTS SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES OCCUPATIONAL FRAUDS ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 FINANCIAL STATEMENT FRAUD What Is Financial

POLICY: Identity Theft Red Flag Prevention

POLICY SUBJECT: POLICY: Identity Theft Red Flag Prevention It shall be the policy of the Cooperative to take all reasonable steps to identify, detect, and prevent the theft of its members personal information

POLICY SUBJECT: POLICY: Identity Theft Red Flag Prevention It shall be the policy of the Cooperative to take all reasonable steps to identify, detect, and prevent the theft of its members personal information

The following Red Flags have been listed here as a guide to assist in the processing, underwriting, quality control and loss mitigation review of loan files. These Red Flags do not necessarily mean that

The following Red Flags have been listed here as a guide to assist in the processing, underwriting, quality control and loss mitigation review of loan files. These Red Flags do not necessarily mean that

Mitigating Fraud. June 22, Sept. 21, 2014

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

WILLIAM I. ESKIN, CPA. Presentation to : Southeastern Accounting Show FINANCIAL STATEMENT ANALYSIS/FRAUD. August 18, 2011.

WILLIAM I. ESKIN, CPA Presentation to : Southeastern Accounting Show FINANCIAL STATEMENT ANALYSIS/FRAUD August 18, 2011 Introduction What is Fraud? SAS No. 99 defines fraud as: an intentional act that

WILLIAM I. ESKIN, CPA Presentation to : Southeastern Accounting Show FINANCIAL STATEMENT ANALYSIS/FRAUD August 18, 2011 Introduction What is Fraud? SAS No. 99 defines fraud as: an intentional act that

COVERAGE FRAUD IN EMPLOYEE BENEFIT PLANS 5/15/2014. Where employee benefit fraud is likely. Internal controls that help prevent fraud

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

Debt & Equity-Financing The Deal: Considerations & Trends. National Business Institute Seminar May 11, 2015

Debt & Equity-Financing The Deal: Considerations & Trends National Business Institute Seminar May 11, 2015 IronHorse is a K.C. based special situation professional services firm with practice specialties

Debt & Equity-Financing The Deal: Considerations & Trends National Business Institute Seminar May 11, 2015 IronHorse is a K.C. based special situation professional services firm with practice specialties

Posting Date: Page 1 of 11 FIN & INFO Procurement Card Policies & Procedures

Posting Date: 2010-09-01 Page 1 of 11 Section # Table of Contents 1.0 Purpose 2.0 Overview 3.0 Cardholder Eligibility 4.0 Establishment of Credit Limits 5.0 Methodology 6.0 Responsibilities 7.0 Application

Posting Date: 2010-09-01 Page 1 of 11 Section # Table of Contents 1.0 Purpose 2.0 Overview 3.0 Cardholder Eligibility 4.0 Establishment of Credit Limits 5.0 Methodology 6.0 Responsibilities 7.0 Application

Catch Me If You Can. Fraud in Local Government. CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Delivering Confidence PAGE 1

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

In the Wake of Catastrophe: Navigating Business Income Losses

In the Wake of Catastrophe: Navigating Business Income Losses Todd Burchett, CPA/ABV, ASA, CFF, CFE Partner tburchett@bkd.com Keith Seiffert, CPA, CFE Managing Consultant kseiffert@bkd.com October 11,

In the Wake of Catastrophe: Navigating Business Income Losses Todd Burchett, CPA/ABV, ASA, CFF, CFE Partner tburchett@bkd.com Keith Seiffert, CPA, CFE Managing Consultant kseiffert@bkd.com October 11,