Mitigating Fraud. June 22, Sept. 21, 2014

|

|

|

- Allyson Perry

- 5 years ago

- Views:

Transcription

1 Mitigating Fraud June 22, 2016 Sept. 21, 2014

2 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

3 Association of Certified Fraud Examiners 2016 Report to the Nations

4 Executive Summary Based on information provided by certified fraud examiners from 114 countries 2,410 fraud cases investigated between January 2014 and October 2015 The CFEs who participated in our survey estimated that the typical organization loses 5% of revenues in a given year as a result of fraud.

5 Fraud Losses

6 Types of Fraud Asset misappropriation was by far the most common form of occupational fraud, occurring in more than 83% of cases, but causing the smallest median loss of $125,000. Financial statement fraud was on the other end of the spectrum, occurring in less than 10% of cases but causing a median loss of $975,000. Corruption cases fell in the middle, with 35.4% of cases and a median loss of $200,000.

7 Most Common Occupational Fraud

8 Interesting Stats More occupational frauds originated in the accounting department (16.6%) than in any other business unit. In 94.5% of the cases in our study, the perpetrator took some efforts to conceal the fraud. The most common concealment methods were creating and altering physical documents.

9 Length of Time

10 Asset Misappropration Asset Misappropriation is a more frequent type of fraud, however, it is also the least costly type of fraud. Schemes include: Skimming Refunds Write offs Lapping Larceny Theft of equipment Fraudulent disbursements Billing Schemes

11 Asset Misappropriation Schemes

12 Corruption Corruption includes: Bid rigging Bribery Collusion (price setting) Kickbacks Conflicts of interest Illegal gratuities Fraud Indicators for Corruption: Circumventing established procurement procedures Vendor complaints

13 Most Common Concealment Methods

14 Initial Detection

15 Reporting Mechanisms

16 Source of Tips

17 Case Study #1 Housing Authority Fraud High level agency official worked with a bank president friend to falsify loan documents for nonexistent borrowers Over 3 years, 27 loans and received $1M in loan proceeds. Sentenced to 12 years plus restitution.

18 Victim Organizations

19 Anti-Fraud Controls

20 Reporting Mechanism

21 Fraud Perpetrators

22 Perpetrator s Criminal Background

23 Action Taken Against Perpetrator

24 Fraud Triangle Opportunity is the only element that an organization can control

25 Behavioral Red Flags In effort to limit loss due to fraud, it is important for employers to be aware of certain behavioral red flags that employees display when they are engaged in fraudulent activity.

26 Living Beyond One s Means Red Flag #1 Living Large

27 Red Flag #2 Financial Difficulty Warning signs of financial difficulties Known legal or financial issues Excessive phone calls from debt collectors Sick family member Affairs or divorce Child custody battle Borrowing money from co-workers

28 Red Flag #3 Refusing to Take Time Off For fear of detection, employees committing fraud often refuse to take time off Refusing to delegate Refusing help when an employee is clearly overloaded Refuse a promotion When an employee is out, it is important that another employee performs their functions

29 Internal Controls Preventative vs. Detective Preventative Control - A key control that prevents misstatements from occurring, whether due to fraud or error. Detective Control A mitigating control, in the absence of a key control, that will detect a misstatement, whether due to fraud or error.

30 Construction Triangle Schedule Quality Cost Remember the tendency to focus too heavily on only two of these three areas will cause the third to suffer.

31 Fraud Risks Capital Projects Construction Projects Areas of risk Billing for equipment or labor at higher rates than agreed upon Billing for costs not associated with the project Intentional mathematical errors on pay application Material substitution Failure to credit for unused materials Overpricing change orders

32 Case Study #2 Construction Fraud University of Texas San Antonio (August 2013) Three contractors and a former project manager indicted on charges they committed more than $1 million in fraud through bid rigging scheme 17 count federal indictment Rigged and inflated bids Kept contracts under $25,000 threshold for formal sealed bid Same three companies would respond Only one company was real Reported by an anonymous caller to fraud hotline at UTSA

33 Lessons Learned Primary internal control weaknesses of victim organizations with greater than 100 employees: Lack of internal controls Override of existing internal controls Lack of management review Poor tone at the top Lack of competent personnel in oversight roles Lack of independent checks/audit Lack of clear lines of authority Lack of employee fraud education Lack of reporting mechanism

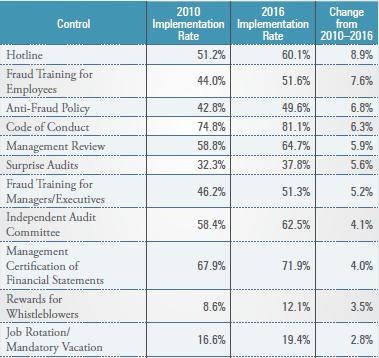

34 Recommended Mitigation Tools External Audit of Financial Statements Management Certification of Financial Statements Code of Conduct Anti-Fraud Policy Fraud Training Internal Audit Department Independent Audit Committee Hotline Management Review Employee Support Program Surprise Audit Data Monitoring/Analysis Job Rotation/Mandatory Vacation Fraud Department/Function Formal Fraud Risk Assessment

35 Lone Star College Ethics Hotline Home Page

36 Lone Star College Ethics Hotline Categories Academic Affairs Accounting and Financial Human Resources Information Technology Research Risk and Safety Matters Other

37 Why implement a Hotline? Chancellor initiative Good business practice Demonstrates fiscal responsibility Serves as a deterrent to fraud, waste, and abuse Inspires confidence with stakeholders Creates a culture that values ethical behavior Ability to deal with problems internally Leverages small internal audit department

38 Third Party Hotline Provider NavexGlobal EthicsPoint Hotline available 24/7/365 Web and phone based Multilingual Ability to follow-up and communicate anonymously Case management and reporting capability Advanced analytics module

39 Lone Star College Ethics Hotline Hotline launched 9/1/2015 Managed by Chief of Staff Less than 30 cases received to date Most have been complaints related to Human Resources

40 Closing Questions? Special Thanks to Whitley Penn, LLP

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

Figure 1: Occupational Frauds by Category Frequency

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

Figure 1: Breakdown of Cases by Country

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

Fraud in Government. Mike Nolan, CPA, CFE, CGMA. CCACC & CCA&RMC Conference Monterey, CA September 2014

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

Have you dealt with fraud in the past?

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

November 2017 ICPAK FORENSIC AUDIT SEMINAR

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

Sunera Canada ULC. Effective Fraud Risk Assessment Annual Fraud Program. October 21, 2016

Sunera Canada ULC Effective Fraud Risk Assessment 2016 Annual Fraud Program October 21, 2016 Sunera LLC Snapshot Professional consultancy with core competency in Governance, SOx, NI 52-109, Internal Audit,

Sunera Canada ULC Effective Fraud Risk Assessment 2016 Annual Fraud Program October 21, 2016 Sunera LLC Snapshot Professional consultancy with core competency in Governance, SOx, NI 52-109, Internal Audit,

Fraud Prevention for Nonprofits

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Fraud prevention for credit unions

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Is Your Construction Project a Victim of Fraud?

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE GLObAL FrAUD STUDy

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

Chapter 2 Skimming. 2. To a fraudster, the principle advantage of skimming is the difficulty with which the scheme is detected. a. True b.

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

AGA Risk and Fraud Webinar

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

A c f e. Report to. the Nation. on Occupational Fraud & Abuse

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE FOREWORD Bruce Dorris, J.D., CFE, CPA President and CEO, Association of Certified Fraud Examiners With the publication of the 2018

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE FOREWORD Bruce Dorris, J.D., CFE, CPA President and CEO, Association of Certified Fraud Examiners With the publication of the 2018

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

Analyzing a Potpourri of Fraud in Higher Education. Calvin Wendelboe, CPA, CIA, CFE

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

IIA Fraud Conference. Case studies from recent investigations. 8 April 2015

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

Everything You Didn t Want To Know About Employee Crime

Everything You Didn t Want To Know About Employee Crime It's something employers don't want to have to think about: employee crime. Finding out that trusted, long-term employees have been stealing from

Everything You Didn t Want To Know About Employee Crime It's something employers don't want to have to think about: employee crime. Finding out that trusted, long-term employees have been stealing from

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Chapter 2 Skimming 1

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY Letter from the President In 1996, Dr. Joseph T. Wells, CFE, CPA, founder and Chairman of the ACFE, directed the publication

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY Letter from the President In 1996, Dr. Joseph T. Wells, CFE, CPA, founder and Chairman of the ACFE, directed the publication

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

Figure 1: Geographical Location of Victim Organizations

Figure 1: Geographical Location of Victim Organizations Region Number of Cases Percent of Cases Median Loss (in U.S. dollars) United States 646 48.0% $100,000 Sub-Saharan Africa 173 12.8% $120,000 Asia-Pacific

Figure 1: Geographical Location of Victim Organizations Region Number of Cases Percent of Cases Median Loss (in U.S. dollars) United States 646 48.0% $100,000 Sub-Saharan Africa 173 12.8% $120,000 Asia-Pacific

1/24/14. Fraud Detec/on and Preven/on. Agenda. Fraud Cases in Minnesota - Schools

February 7, 2014 Fraud Detec/on and Preven/on Presented by: Steve Wischmann, CPA, CFE, CFF, CCFE, MAFF Agenda 1. Actual Minnesota School Cases in the News 2. Definition of Fraud 3. Fraud Statistics-ACFE

February 7, 2014 Fraud Detec/on and Preven/on Presented by: Steve Wischmann, CPA, CFE, CFF, CCFE, MAFF Agenda 1. Actual Minnesota School Cases in the News 2. Definition of Fraud 3. Fraud Statistics-ACFE

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen:

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Last Updated: 1 February 2018 To be reviewed: Annually

CARE International Policy on Fraud and Corruption Awareness, Prevention, Reporting and Response Sponsor: Secretary General/CEO Policy Owner: Deputy Secretary General, CARE International Effective Date:

CARE International Policy on Fraud and Corruption Awareness, Prevention, Reporting and Response Sponsor: Secretary General/CEO Policy Owner: Deputy Secretary General, CARE International Effective Date:

Fraud Prevention and Detection. Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar

Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar") Fraud Prevention and Detection Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar Opening Remarks Fraud - what is it? Fraud Risk Management Fraud

Fraud Prevention and Detection Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar Opening Remarks Fraud - what is it? Fraud Risk Management Fraud

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Whistle-Blowing Policy

2017 Ithmaar Bank Human Resources Department Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 3.0- Actions Constituting Fraud 3.1- Criminal / Unethical Conduct 3.2-

2017 Ithmaar Bank Human Resources Department Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 3.0- Actions Constituting Fraud 3.1- Criminal / Unethical Conduct 3.2-

Fraud in the Government Realm. Introduction. What is Fraud? My career began with a local government fraud in 1993

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud Examination. Prevention, Detection, and Investigation. Steven M. Bragg

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud risk management. Oil and gas sector

Fraud risk management Oil and gas sector Fraud risk management oil and gas sector Contents Why should you be concerned about fraud risks? 1 Key risks in the oil and gas sector 2 Five key factors your business

Fraud risk management Oil and gas sector Fraud risk management oil and gas sector Contents Why should you be concerned about fraud risks? 1 Key risks in the oil and gas sector 2 Five key factors your business

The Procurement Fraud Equation. Tom Caulfield

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

Approval version. G l o b a l P o l i c y : F r a u d R e s p o n s e a n d W h i s t l e b l o w i n g P o l i c y. Board of Directors.

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

OCCUPATIONAL FRAUD 9/20/2018

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

Catch Me If You Can. Fraud in Local Government. CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Community College Audit and Fiscal Compliance Workshop. VAVRINEK, TRINE, DAY & CO., LLP May 23, 2017

Community College Audit and Fiscal Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP May 23, 2017 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Community College Audit and Fiscal Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP May 23, 2017 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Lecture Notes for How to Steal $500 Million

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

T H E A S S O C I A T I O N

A B O U T T H E A S S O C I A T I O N Since 1988 there has been only one organization whose main focus is to train anti-fraud professionals in their fight against economic crime: the Association of Certified

A B O U T T H E A S S O C I A T I O N Since 1988 there has been only one organization whose main focus is to train anti-fraud professionals in their fight against economic crime: the Association of Certified

OAPT June 9, Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

CSMFO CONFERENCE 2018

CSMFO CONFERENCE 2018 Fraud: A Story of Embezzlement, Response, and Resilience February 22, 2018 Presented by: Damien Arrula City of Placentia Kenneth H. Pun The Pun Group, LLP 1 Objectives Hear a real

CSMFO CONFERENCE 2018 Fraud: A Story of Embezzlement, Response, and Resilience February 22, 2018 Presented by: Damien Arrula City of Placentia Kenneth H. Pun The Pun Group, LLP 1 Objectives Hear a real

U.S. DEPARTMENT OF JUSTICE ANTITRUST DIVISION. National Tax Liens Association

Presentation By The U.S. DEPARTMENT OF JUSTICE ANTITRUST DIVISION To National Tax Liens Association February 26, 2015 DISCLAIMER: The views expressed in this presentation are not purported to reflect those

Presentation By The U.S. DEPARTMENT OF JUSTICE ANTITRUST DIVISION To National Tax Liens Association February 26, 2015 DISCLAIMER: The views expressed in this presentation are not purported to reflect those

Internal Bank Fraud Schemes & Scams in an Economic Downturn. Fictitious Loans. Bank Fraud Investigations. Tracking spreadsheet Affidavit 1 Affidavit 2

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

Fraud: How to Get Your District Free Publicity

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

Mortgage Bankers Association of Puerto Rico Mortgage Fraud Prevention Seminar

Mortgage Bankers Association of Puerto Rico 2018 Mortgage Fraud Prevention Seminar Agenda The Federal Housing Finance Agency (FHFA) and the financial crisis The FHFA Office of Inspector General (FHFA-OIG)

Mortgage Bankers Association of Puerto Rico 2018 Mortgage Fraud Prevention Seminar Agenda The Federal Housing Finance Agency (FHFA) and the financial crisis The FHFA Office of Inspector General (FHFA-OIG)

Whistle-Blowing Policy

2011 Ithmaar Bank Risk Management & Compliance Division 21-Oct-11 Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 4 3.0- Actions Constituting Fraud 4 3.1- Criminal

2011 Ithmaar Bank Risk Management & Compliance Division 21-Oct-11 Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 4 3.0- Actions Constituting Fraud 4 3.1- Criminal

SCOPE This policy applies to all members of the University Board of Trustee and all employees and volunteers of the University.

Section Number: Effective Date: June 12, 2006 Section Header: Financial Integrity Policy Revision Date: December 8, 2008 Responsible Office: Finance and Administration Responsible Officer: Vice President

Section Number: Effective Date: June 12, 2006 Section Header: Financial Integrity Policy Revision Date: December 8, 2008 Responsible Office: Finance and Administration Responsible Officer: Vice President

POLICY: FRAUD PREVENTION. October 2017

POLICY: October 2017 CONTENTS 1. PURPOSE P3 2. SCOPE P3 3. LEGISLATION AND CORPORATE GOVERNANCE REQUIREMENTS REFERENCE 4. POLICY STATEMENT AND INTERNAL STANDARDS P3 P4 4.1 Background P4 4.2 Actions constituting

POLICY: October 2017 CONTENTS 1. PURPOSE P3 2. SCOPE P3 3. LEGISLATION AND CORPORATE GOVERNANCE REQUIREMENTS REFERENCE 4. POLICY STATEMENT AND INTERNAL STANDARDS P3 P4 4.1 Background P4 4.2 Actions constituting

TEXAS WORKFORCE COMMISSION LETTER. ID/No: Regulatory Integrity Date: August 17, 2009

TEXAS WORKFORCE COMMISSION LETTER ID/No: Regulatory Integrity 04-09 Date: August 17, 2009 TO: FROM: Executive Director Deputy Executive Director Commission Executive Staff Department Heads LWDB Executive

TEXAS WORKFORCE COMMISSION LETTER ID/No: Regulatory Integrity 04-09 Date: August 17, 2009 TO: FROM: Executive Director Deputy Executive Director Commission Executive Staff Department Heads LWDB Executive

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

Whistleblower Protection

Whistleblower Protection Scope: CITYWIDE Policy Contact Howard Chan, Assistant City Manager, (916) 808-7488, hchan@cityofsacramento.org Jorge Oseguera, City Auditor, (916) 808-7270, joseguera@cityofsacramento.org

Whistleblower Protection Scope: CITYWIDE Policy Contact Howard Chan, Assistant City Manager, (916) 808-7488, hchan@cityofsacramento.org Jorge Oseguera, City Auditor, (916) 808-7270, joseguera@cityofsacramento.org

Fraud Awareness & Prevention for Higher Education. Neil Cohen Deputy Director Audit, Oversight & Investigations

Fraud Awareness & Prevention for Higher Education Neil Cohen Deputy Director Audit, Oversight & Investigations Goals Raise your fraud awareness and introduce you to fraud prevention methods. 2 Disclaimers

Fraud Awareness & Prevention for Higher Education Neil Cohen Deputy Director Audit, Oversight & Investigations Goals Raise your fraud awareness and introduce you to fraud prevention methods. 2 Disclaimers

Spotting Financial Distortions: A Primer for Attorneys

Spotting Financial Distortions: A Primer for Attorneys The Web Conference Series For Corporate Counsel January 17, 2007 To ask a question using the question pane Enter your question into the text area

Spotting Financial Distortions: A Primer for Attorneys The Web Conference Series For Corporate Counsel January 17, 2007 To ask a question using the question pane Enter your question into the text area

ACFE CFEX. Certified Fraud Examiner (CFEX)

") ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

MIS 520 Data Analytics for IT Auditors

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

SOMERVILLE HOUSING AUTHORITY ANTI- FRAUD POLICY. April 3, 2013

SOMERVILLE HOUSING AUTHORITY ANTI- FRAUD POLICY April 3, 2013 Introduction The Board of Commissioners of the Somerville Housing Authority has established an anti-fraud policy to enforce controls and to

SOMERVILLE HOUSING AUTHORITY ANTI- FRAUD POLICY April 3, 2013 Introduction The Board of Commissioners of the Somerville Housing Authority has established an anti-fraud policy to enforce controls and to

An Overview of Fraud Risk. Presented by: Rick Potocek CPA MBA CFE

An Overview of Fraud Risk Presented by: Rick Potocek CPA MBA CFE To raise awareness of: Who commits fraud and why Red flags to consider Simple steps to take to immediately reduce the risk of fraud According

An Overview of Fraud Risk Presented by: Rick Potocek CPA MBA CFE To raise awareness of: Who commits fraud and why Red flags to consider Simple steps to take to immediately reduce the risk of fraud According

Lecture notes for: Corporate Cons

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Capital Improvement Programs: Where is the Fraud, Waste and Abuse

1 Capital Improvement Programs: Where is the Fraud, Waste and Abuse 1 Agenda: Definition and Statistics Internal Fraud Construction Risks Types of Contracts and Red Flags Take-Aways 2 Definition The use

1 Capital Improvement Programs: Where is the Fraud, Waste and Abuse 1 Agenda: Definition and Statistics Internal Fraud Construction Risks Types of Contracts and Red Flags Take-Aways 2 Definition The use

The State of the Art of Fraud. Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

VOLUME 3 NUMBER 3 MARCH HEADNOTE: HOW TO DEAL WITH WHISTLEBLOWERS PROVISIONS Steven A. Meyerowitz 193

Financial Fraud Law Report VOLUME 3 NUMBER 3 MARCH 2011 HEADNOTE: HOW TO DEAL WITH WHISTLEBLOWERS PROVISIONS Steven A. Meyerowitz 193 STRATEGIC RESPONSES TO THE WHISTLEBLOWER PROVISIONS OF THE DODD-FRANK

Financial Fraud Law Report VOLUME 3 NUMBER 3 MARCH 2011 HEADNOTE: HOW TO DEAL WITH WHISTLEBLOWERS PROVISIONS Steven A. Meyerowitz 193 STRATEGIC RESPONSES TO THE WHISTLEBLOWER PROVISIONS OF THE DODD-FRANK

NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations

NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations Allan Bachman, CFE Retired Education Manager ACFE Agenda The ACFE & Mission ACFE 2016 Report to

NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations Allan Bachman, CFE Retired Education Manager ACFE Agenda The ACFE & Mission ACFE 2016 Report to

Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags

Forensic Services Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags 2 What % of revenues are lost to fraud? 5% Source: 2016 ACFE Report to the Nations 3 Has your

Forensic Services Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags 2 What % of revenues are lost to fraud? 5% Source: 2016 ACFE Report to the Nations 3 Has your

ANTI-FRAUD POLICY. Reference No: ANTIFP-251. Policy Type: Governance. Directorate Area: All Directorates. Policy Author / Champion: Maurice Atkinson

ANTI-FRAUD POLICY Reference No: ANTIFP-251 Policy Type: Directorate Area: Policy Author / Champion: Governance All Directorates Maurice Atkinson Date(s) Equality Screened: 21 July 2017 Date(s) Approved

ANTI-FRAUD POLICY Reference No: ANTIFP-251 Policy Type: Directorate Area: Policy Author / Champion: Governance All Directorates Maurice Atkinson Date(s) Equality Screened: 21 July 2017 Date(s) Approved

Global Policy on Anti-Bribery and Anti-Corruption

1 Global Policy on Anti-Bribery and Anti-Corruption OUR GLOBAL POLICY ON ANTI-BRIBERY AND ANTI-CORRUPTION Did You know?? PolyOne is committed to the prevention, deterrence and detection of fraud, bribery

1 Global Policy on Anti-Bribery and Anti-Corruption OUR GLOBAL POLICY ON ANTI-BRIBERY AND ANTI-CORRUPTION Did You know?? PolyOne is committed to the prevention, deterrence and detection of fraud, bribery

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

Anti-fraud and Corruption Policy

Anti-fraud and Corruption Policy Responsible Division: Finances Validated by: Board (Executive Committee) Date of approval: 17/05/2017 Date of next review: May 2019 Language versions available: English

Anti-fraud and Corruption Policy Responsible Division: Finances Validated by: Board (Executive Committee) Date of approval: 17/05/2017 Date of next review: May 2019 Language versions available: English

C-SUITE S DIRTY LITTLE FRAUD SECRET

Fraud committed by CEOs, CFOs, and others in the C-suite is a dirty little secret. It is rarely discussed, but it happens with disturbing regularity. It is one of those once in a lifetime events that seems

Fraud committed by CEOs, CFOs, and others in the C-suite is a dirty little secret. It is rarely discussed, but it happens with disturbing regularity. It is one of those once in a lifetime events that seems

Procurement Fraud s Anatomy. By Tom Caulfield CFE/CIG/CIGI

Procurement Fraud s Anatomy By Tom Caulfield CFE/CIG/CIGI LEARNING OBJECTIVES 1. Identify statutes, regulations, and key personnel associated with the contracting process. 2. Identify the primary acquisition

Procurement Fraud s Anatomy By Tom Caulfield CFE/CIG/CIGI LEARNING OBJECTIVES 1. Identify statutes, regulations, and key personnel associated with the contracting process. 2. Identify the primary acquisition

FRAUD EXAMINERS MANUAL

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

Fraud Detection and Prevention for Governmental Organizations. Michael A. Swafford, CIA, CFE

Fraud Detection and Prevention for Governmental Organizations Michael A. Swafford, CIA, CFE Presenter Michael A. Swafford, CIA, CFE Mike is a Consulting Manager in our Forensic Valuation Services Practice

Fraud Detection and Prevention for Governmental Organizations Michael A. Swafford, CIA, CFE Presenter Michael A. Swafford, CIA, CFE Mike is a Consulting Manager in our Forensic Valuation Services Practice

Capital Area SBO. Accounting/Auditing Update. May 24, Kevin B. Stouffer, CPA. Audit Manager

Capital Area SBO Accounting/Auditing Update May 24, 2017 Kevin B. Stouffer, CPA Audit Manager Information and training provided by Smith Elliott Kearns & Company, LLC is intended for reference only. As

Capital Area SBO Accounting/Auditing Update May 24, 2017 Kevin B. Stouffer, CPA Audit Manager Information and training provided by Smith Elliott Kearns & Company, LLC is intended for reference only. As

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT MODERATOR: LAURIE DE ARMOND TIM MOHR, MIKE SORRELLS AND RANDAL SIMONETTI DECEMBER 9, 2013 BDO USA, LLP, a Delaware limited liability partnership,

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT MODERATOR: LAURIE DE ARMOND TIM MOHR, MIKE SORRELLS AND RANDAL SIMONETTI DECEMBER 9, 2013 BDO USA, LLP, a Delaware limited liability partnership,

Looking for Fraud Through Rose-Colored Glasses

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Grant Fraud. Leslie Les Hollie Assistant Inspector General For Investigations

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Delivering Financial Oversight: Strengthening Your Policies and Procedures

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut