NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations

|

|

|

- Myron Townsend

- 5 years ago

- Views:

Transcription

1 NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations Allan Bachman, CFE Retired Education Manager ACFE

?")

2 Agenda The ACFE & Mission ACFE 2016 Report to the Nations Who are Certified Fraud Examiners (CFEs)? CFE Value Added Becoming a CFE Resources 2 of

3 About the ACFE ACFE - Association of Certified Fraud Examiners Largest global anti-fraud organization Founded in 1988 More than 80,000 members worldwide (160 countries) 3 of

4 About the ACFE Headquartered in Austin, Texas (over 180 local chapters worldwide) Premier provider of anti-fraud training worldwide Globally recognized professional designation: Certified Fraud Examiner (CFE) 4 of

5 ACFE Mission The mission of the Association of Certified Fraud Examiners is to reduce the incidence of fraud and white-collar crime and to assist the Membership in fraud detection and deterrence. 5 of

6 2016 Report to the Nations Organizations lose 5% of revenues to fraud each year. Median losses by a single case of occupational fraud $145,000. Median losses by scheme: Asset misappropriation: $130,000 Corruption: $200,000 Financial statement fraud: $1,000,000 6 of

7 2016 Report to the Nations Organizations with less than 100 employees realize 28% higher median fraud losses. When collusion occurs, median losses increase substantially: $80,000 one perpetrator $300,000 two or more perpetrators 7 of

8 Who Are CFEs? Certified Fraud Examiners (CFEs) posses expertise in all aspects of the antifraud profession and have the proven ability to detect, prevent, and investigate a wide range of fraud. 8 of

9 CFE Core Competencies Understand the ways in which fraud is committed and how these schemes can be prevented and detected Understand the underlying factors that motivate individuals to commit fraud Examine documents and records to detect and trace fraudulent transactions 9 of

10 CFE Core Competencies Interview suspects to obtain information and confessions. Write investigation reports, advise clients as to their findings, and testify at trial. Understand the law as it relates to fraud and fraud examinations. 10 of

11 Professional Fields for CFEs Accounting and Forensic Accounting Auditing (External and Internal) Law Enforcement Government Agencies (i.e OIG) Investigation Loss Prevention Computer Forensics Risk Management Corporate Compliance Law Firms Higher Education Consulting 11 of

12 Cynthia Cooper Certified Fraud Examiners Uncovered a $3.8 Billion accounting fraud at one of the world s largest telecomm companies, WorldCom. 12 of

13 Harry Markopolos Certified Fraud Examiners Identified that Bernie Madoff was running one of the largest frauds and Ponzi schemes in modern history. Reported his concerns to the SEC on numerous occasions but no one listened. 13 of

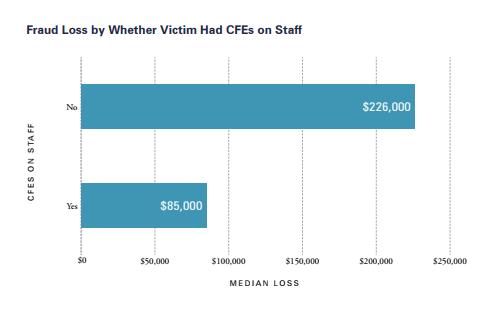

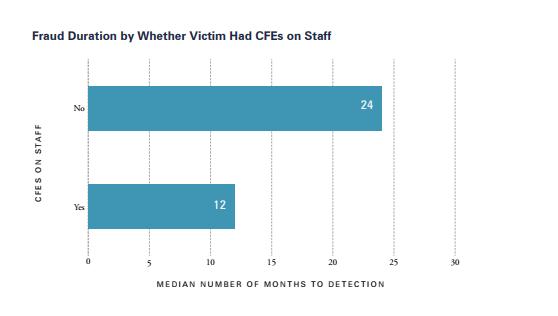

14 CFE Value Added CFEs possess expertise in preventing, detecting and investigating fraud, and this proactive approach reduces the duration and median loss of a fraud. ACFE research shows that organizations with CFEs on staff uncover frauds 50 percent sooner and suffer losses 62 percent lower than organizations without CFEs 14 of

15 15 of

16 16 of

17 Becoming Certified: The CFE Exam Exam contains 500 questions and consists of four parts: Fraud Prevention and Deterrence Financial Transactions and Fraud Schemes Investigation Law 17 of

18 Fraud Prevention and Deterrence Tests your understanding of why people commit fraud and ways to prevent it. Topics covered in this section include crime causation, white-collar crime, occupational fraud, fraud prevention, fraud risk assessment, and the ACFE Code of Professional Ethics. 18 of

19 Financial Transactions and Fraud Schemes Tests your comprehension of the types of fraudulent financial transactions incurred in accounting records. This section requires you to demonstrate knowledge of the following concepts: basic accounting and auditing theory, fraud schemes, internal controls to deter fraud and other auditing and accounting matters. 20 of

20 Investigation This section includes questions about interviewing, taking statements, obtaining information from public records, tracing illicit transactions, evaluating deception and report writing. 22 of

21 Law This section ensures your familiarity with the many legal ramifications of conducting fraud examinations, including criminal and civil law, rules of evidence, rights of the accused and accuser, and expert witness matters. 24 of

22 Compensation by Job Function 26 of

23 ACFE Educational Opportunities Seminars, webinars, self-studies, onsite-specialized training Conferences Chapter events Discussion forums Fraud Magazine ACFE Bookstore 27 of

24 ACFE.com Report to the Nations FraudConference.com Fraud Magazine Resources 28 of

25 Questions? Allan Bachman, CFE Education Manager [retired] ACFE

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

FRAUD EXAMINERS MANUAL (INTERNATIONAL EDITION)

") TABLE OF CONTENTS SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES OCCUPATIONAL FRAUDS ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 FINANCIAL STATEMENT FRAUD What Is Financial

TABLE OF CONTENTS SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES OCCUPATIONAL FRAUDS ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 FINANCIAL STATEMENT FRAUD What Is Financial

FRAUD EXAMINERS MANUAL

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

AGA Risk and Fraud Webinar

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

INVESTIGATING AND PROSECUTING MONEY LAUNDERING

INVESTIGATING AND PROSECUTING MONEY LAUNDERING This one-day course will discuss the criminal elements and case law for N.J.S.A criminal statue 2C:21-25, Financial Facilitation of Criminal Activity, also

INVESTIGATING AND PROSECUTING MONEY LAUNDERING This one-day course will discuss the criminal elements and case law for N.J.S.A criminal statue 2C:21-25, Financial Facilitation of Criminal Activity, also

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

HOW TO LOCATE ASSETS DURING A FINANCIAL CRIMES/NARCOTICS INVESTIGATION

HOW TO LOCATE ASSETS DURING A FINANCIAL CRIMES/NARCOTICS INVESTIGATION This one-day course will benefit any detective and/or prosecutor assigned to white collar crime/narcotics investigations. Preliminary

HOW TO LOCATE ASSETS DURING A FINANCIAL CRIMES/NARCOTICS INVESTIGATION This one-day course will benefit any detective and/or prosecutor assigned to white collar crime/narcotics investigations. Preliminary

COMPENSATION GUIDE FOR ANTI-FRAUD PROFESSIONALS

COMPENSATION GUIDE FOR ANTI-FRAUD PROFESSIONALS 2015/2016 GLOBAL SALARY STUDY ACCOUNTING Table of Contents Letter from the President and CEO... 3 Accounting... 4 Accounting Median Total Compensation...

COMPENSATION GUIDE FOR ANTI-FRAUD PROFESSIONALS 2015/2016 GLOBAL SALARY STUDY ACCOUNTING Table of Contents Letter from the President and CEO... 3 Accounting... 4 Accounting Median Total Compensation...

HOW TO LOCATE ASSETS DURING A FINANCIAL CRIMES/NARCOTICS INVESTIGATION

HOW TO LOCATE ASSETS DURING A FINANCIAL CRIMES/NARCOTICS INVESTIGATION This one-day course will benefit any detective and/or prosecutor assigned to white collar crime/narcotics investigations. Preliminary

HOW TO LOCATE ASSETS DURING A FINANCIAL CRIMES/NARCOTICS INVESTIGATION This one-day course will benefit any detective and/or prosecutor assigned to white collar crime/narcotics investigations. Preliminary

ABOUT THE PROGRAMME. The FCPA certification programme consists of 5 papers:

ABOUT THE PROGRAMME The Forensic Certified Public Accountant (FCPA) programme is a certification program developed by the FCPA Society of the United States of America. It is an internationally accepted

ABOUT THE PROGRAMME The Forensic Certified Public Accountant (FCPA) programme is a certification program developed by the FCPA Society of the United States of America. It is an internationally accepted

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

Crime Pays Recovering Employee-Dishonesty Claims.

Crime Pays Recovering Employee-Dishonesty Claims. September 23,2014 Today s Speakers CHRISTOPHER GIOVINO Global Practice Leader for forensic investigations, crime and fidelity claims and Cyber Evaluation

Crime Pays Recovering Employee-Dishonesty Claims. September 23,2014 Today s Speakers CHRISTOPHER GIOVINO Global Practice Leader for forensic investigations, crime and fidelity claims and Cyber Evaluation

FINANCIAL CRIMES LAW IN NEW JERSEY

FINANCIAL CRIMES LAW IN NEW JERSEY This one-day course will provide a detailed analysis of N.J.S.A Chapters 20 & 21 related to financial crimes investigations. Case studies will describe key elements for

FINANCIAL CRIMES LAW IN NEW JERSEY This one-day course will provide a detailed analysis of N.J.S.A Chapters 20 & 21 related to financial crimes investigations. Case studies will describe key elements for

Fraud in Government. Mike Nolan, CPA, CFE, CGMA. CCACC & CCA&RMC Conference Monterey, CA September 2014

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

METHODS OF LOCATING AND SEIZING HIDDEN ASSETS

METHODS OF LOCATING AND SEIZING HIDDEN ASSETS This one-day course will benefit any detective and/or prosecutor assigned to white collar crime/narcotics investigations. Preliminary discussion will center

METHODS OF LOCATING AND SEIZING HIDDEN ASSETS This one-day course will benefit any detective and/or prosecutor assigned to white collar crime/narcotics investigations. Preliminary discussion will center

INVESTIGATING AND PROSECUTING MONEY LAUNDERING

INVESTIGATING AND PROSECUTING MONEY LAUNDERING This one-day course will discuss the criminal elements and case law for N.J.S.A criminal statue 2C:21-25, Financial Facilitation of Criminal Activity, also

INVESTIGATING AND PROSECUTING MONEY LAUNDERING This one-day course will discuss the criminal elements and case law for N.J.S.A criminal statue 2C:21-25, Financial Facilitation of Criminal Activity, also

November 16 or 17 Las Vegas Accounts Conf, Trial Slide Set 7/26/2017. Financial Statement Types. Financial Statement Fraud

ACCOUNTEX Conference September 6, 2017 Concealing Fraud in Financial Statements Allan Bachman, CFE Education Manager [retired] Association of Certified Fraud Examiners Austin, Texas Agenda Overview and

ACCOUNTEX Conference September 6, 2017 Concealing Fraud in Financial Statements Allan Bachman, CFE Education Manager [retired] Association of Certified Fraud Examiners Austin, Texas Agenda Overview and

Annie Chan Managing Director Forensic & Investigation Services FCPA, LLB, LLM, MBA,CFE

Forensic Accounting and Fraud Risks for MNCs in China Presented by: Annie Chan Managing Director Forensic & Investigation Services FCPA, LLB, LLM, MBA,CFE What is Forensic Accounting A discipline that

Forensic Accounting and Fraud Risks for MNCs in China Presented by: Annie Chan Managing Director Forensic & Investigation Services FCPA, LLB, LLM, MBA,CFE What is Forensic Accounting A discipline that

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

MIS 520 Data Analytics for IT Auditors

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

C-SUITE S DIRTY LITTLE FRAUD SECRET

Fraud committed by CEOs, CFOs, and others in the C-suite is a dirty little secret. It is rarely discussed, but it happens with disturbing regularity. It is one of those once in a lifetime events that seems

Fraud committed by CEOs, CFOs, and others in the C-suite is a dirty little secret. It is rarely discussed, but it happens with disturbing regularity. It is one of those once in a lifetime events that seems

In-House Fraud Investigation Teams: 2017 Benchmarking Report

In-House Fraud Investigation Teams: 2017 Benchmarking Report Contents Key Findings 3 Introduction 4 Methodology...4 Respondent Demographics 5 Industry of Respondents Organizations...6 Region of Respondents

In-House Fraud Investigation Teams: 2017 Benchmarking Report Contents Key Findings 3 Introduction 4 Methodology...4 Respondent Demographics 5 Industry of Respondents Organizations...6 Region of Respondents

Figure 1: Occupational Frauds by Category Frequency

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

White Paper Conducting Fraud and Corruption Investigations

White Paper Conducting Fraud and Corruption Investigations August 2017 The Institute of Internal Auditors Australia Level 7, 133 Castlereagh Street Sydney NSW Australia 2000 Telephone: 02 9267 9155 International:

White Paper Conducting Fraud and Corruption Investigations August 2017 The Institute of Internal Auditors Australia Level 7, 133 Castlereagh Street Sydney NSW Australia 2000 Telephone: 02 9267 9155 International:

Mitigating Fraud. June 22, Sept. 21, 2014

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

The State of the Art of Fraud. Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

The State of the Art of Fraud Glenn L. Helms, Ph.D., CPA, CIA, CITP, CISA, CFF GlennHelmsCPA@aol.com Can You Identify Red Flags? City of Rutland, Vermont Fraud Fraud is good in good times. Fraud is good

INTRODUCTION TO FRAUD EXAMINATION

TABLE OF CONTENTS I. INTRODUCTION TO FRAUD EXAMINATION Introduction... 1 Axioms of Fraud Examination... 1 Fraud Is Hidden... 1 Reverse Proof... 1 Existence of Fraud... 2 Predication... 2 Fraud Theory Approach...

TABLE OF CONTENTS I. INTRODUCTION TO FRAUD EXAMINATION Introduction... 1 Axioms of Fraud Examination... 1 Fraud Is Hidden... 1 Reverse Proof... 1 Existence of Fraud... 2 Predication... 2 Fraud Theory Approach...

Conducting Fraud and Corruption Investigations

Connect Support Advance Whitepaper Conducting Fraud and Corruption Investigations AUGUST 2017 Level 7, 133 Castlereagh Street, Sydney NSW 2000 PO Box A2311, Sydney South NSW 1235 T +61 2 9267 9155 F +61

Connect Support Advance Whitepaper Conducting Fraud and Corruption Investigations AUGUST 2017 Level 7, 133 Castlereagh Street, Sydney NSW 2000 PO Box A2311, Sydney South NSW 1235 T +61 2 9267 9155 F +61

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Analyzing a Potpourri of Fraud in Higher Education. Calvin Wendelboe, CPA, CIA, CFE

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

FINANCIER. Corporate fraud & corruption ANNUAL REVIEW ONLINE CONTENT MAY 2017 R E P R I N T F I N A N C I E R W O R L D W I D E.

R E P R I N T F I N A N C I E R W O R L D W I D E. C O M ANNUAL REVIEW Corporate fraud & corruption REPRINTED FROM ONLINE CONTENT MAY 2017 2017 Financier Worldwide Limited Permission to use this reprint

R E P R I N T F I N A N C I E R W O R L D W I D E. C O M ANNUAL REVIEW Corporate fraud & corruption REPRINTED FROM ONLINE CONTENT MAY 2017 2017 Financier Worldwide Limited Permission to use this reprint

Experienced, Talented, Trusted.

Experienced, Talented, Trusted. Bates Group s internationally recognized AML, KYC, BSA and Financial Crimes Consultants & Experts Barry Koch Martin Feuer Susan Berger Ali Ansari Penny Borgerding Timothy

Experienced, Talented, Trusted. Bates Group s internationally recognized AML, KYC, BSA and Financial Crimes Consultants & Experts Barry Koch Martin Feuer Susan Berger Ali Ansari Penny Borgerding Timothy

TOOLS FOR FRAUD DETERRENCE AND DETECTION DIAGNOSING HEALTH CARE FRAUD

TOOLS FOR FRAUD DETERRENCE AND DETECTION DIAGNOSING HEALTH CARE FRAUD What is the true cost of health care fraud, and how does it differ from fraud in other industries? This session will introduce you

TOOLS FOR FRAUD DETERRENCE AND DETECTION DIAGNOSING HEALTH CARE FRAUD What is the true cost of health care fraud, and how does it differ from fraud in other industries? This session will introduce you

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

Demystifying Forensic Accounting

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com AdrianSierra,CPA,CFE,CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining and

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com AdrianSierra,CPA,CFE,CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining and

Demystifying Forensic Accounting

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com Adrian Sierra, CPA, CFE, CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com Adrian Sierra, CPA, CFE, CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

Presented by Duncan Will CPA/ABV/CFF, CFE

Texas Society of CPAs Title Austin - Heading Chapter Risk Management and the Emerging Profession: Risks and Rewards Presented by Duncan Will CPA/ABV/CFF, CFE Sound Familiar? The accompanying financial

Texas Society of CPAs Title Austin - Heading Chapter Risk Management and the Emerging Profession: Risks and Rewards Presented by Duncan Will CPA/ABV/CFF, CFE Sound Familiar? The accompanying financial

2007 global economic crime survey

Investigations and Forensic Services 2007 global economic crime survey Introduction We are pleased to present PricewaterhouseCoopers 2007 Global Economic Crime survey:. While the Global survey is based

Investigations and Forensic Services 2007 global economic crime survey Introduction We are pleased to present PricewaterhouseCoopers 2007 Global Economic Crime survey:. While the Global survey is based

Aletheia Financial Forensics, P.L.L.C.

Aletheia Financial Forensics, P.L.L.C. Forensic Accounting, Investigations & Expert Services CURRICULUM VITAE James H. Rumph Certified Public Accountant (CPA)/ Certified Fraud Examiner (CFE)/ Certified

Aletheia Financial Forensics, P.L.L.C. Forensic Accounting, Investigations & Expert Services CURRICULUM VITAE James H. Rumph Certified Public Accountant (CPA)/ Certified Fraud Examiner (CFE)/ Certified

California Department of Insurance. Steve Poizner. Insurance Commissioner. Dale Banda Deputy Commissioner, Enforcement Branch

California Department of Insurance Steve Poizner Insurance Commissioner 2007 Dale Banda Deputy Commissioner, Enforcement Branch Effective Anti-Fraud Program (California) Insurance is a $118 Billion Dollar

California Department of Insurance Steve Poizner Insurance Commissioner 2007 Dale Banda Deputy Commissioner, Enforcement Branch Effective Anti-Fraud Program (California) Insurance is a $118 Billion Dollar

POLICY: FRAUD PREVENTION. October 2017

POLICY: October 2017 CONTENTS 1. PURPOSE P3 2. SCOPE P3 3. LEGISLATION AND CORPORATE GOVERNANCE REQUIREMENTS REFERENCE 4. POLICY STATEMENT AND INTERNAL STANDARDS P3 P4 4.1 Background P4 4.2 Actions constituting

POLICY: October 2017 CONTENTS 1. PURPOSE P3 2. SCOPE P3 3. LEGISLATION AND CORPORATE GOVERNANCE REQUIREMENTS REFERENCE 4. POLICY STATEMENT AND INTERNAL STANDARDS P3 P4 4.1 Background P4 4.2 Actions constituting

Combatting fraud and corruption in EIB s operations

Combatting fraud and corruption in EIB s operations The European Investment Bank Group (EIB Group) has zero tolerance of fraud and corruption. The Fraud Investigations Division of the Inspectorate General

Combatting fraud and corruption in EIB s operations The European Investment Bank Group (EIB Group) has zero tolerance of fraud and corruption. The Fraud Investigations Division of the Inspectorate General

Figure 1: Breakdown of Cases by Country

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Anti-Fraud Policy. Version: 8.0 Approval Status: Approved. Document Owner: Graham Feek. Review Date: 07/12/2018

Anti-Fraud Policy Version: 8.0 Approval Status: Approved Document Owner: Graham Feek Classification: External Review Date: 07/12/2018 Last Reviewed: 09/12/2016 Table of Contents 1. Policy Statement...

Anti-Fraud Policy Version: 8.0 Approval Status: Approved Document Owner: Graham Feek Classification: External Review Date: 07/12/2018 Last Reviewed: 09/12/2016 Table of Contents 1. Policy Statement...

Forensic Accounting. Ms. Dhir. Forensic Accountant (FoA) #IMASLC17

#IMASLC17") Forensic Accounting Ms. Dhir Forensic Accountant (FoA) OUTLINE Introduction Definitions History Today (Industry, Public Accounting, Government (Crimes) ) Engagements Qualifications (Skills & Certifications,

Forensic Accounting Ms. Dhir Forensic Accountant (FoA) OUTLINE Introduction Definitions History Today (Industry, Public Accounting, Government (Crimes) ) Engagements Qualifications (Skills & Certifications,

Fraud & Financial Services

Fraud & Financial Services Understanding the 2017 Criminal Finances Bill This course can be presented in-house for you on a date of your choosing The Banking and Corporate Finance Training Specialist Course

Fraud & Financial Services Understanding the 2017 Criminal Finances Bill This course can be presented in-house for you on a date of your choosing The Banking and Corporate Finance Training Specialist Course

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

At any given moment, there is a certain percentage of the population that s up to no good. J. Edgar Hoover. Compliance & Ethics Institute

Compliance & Ethics Institute 604 Auditing for Corruption in Emerging Markets: Applying fraud detection skills to reduce corruption October 14, 2012 At any given moment, there is a certain percentage of

Compliance & Ethics Institute 604 Auditing for Corruption in Emerging Markets: Applying fraud detection skills to reduce corruption October 14, 2012 At any given moment, there is a certain percentage of

At any given moment, there is a certain percentage of the population that s up to no good. J. Edgar Hoover. Compliance & Ethics Institute

Compliance & Ethics Institute 604 Auditing for Corruption in Emerging Markets: Applying fraud detection skills to reduce corruption October 14, 2012 At any given moment, there is a certain percentage of

Compliance & Ethics Institute 604 Auditing for Corruption in Emerging Markets: Applying fraud detection skills to reduce corruption October 14, 2012 At any given moment, there is a certain percentage of

Presenter: Mr Harold Phillip BA, LLB (Hons) LEC, MBA Commissioner of Police (Ag) Trinidad and Tobago Police Service

LEC, MBA Commissioner of Police (Ag) Trinidad and Tobago Police Service") DEALING WITH WHITE COLLAR CRIME SUCCESSES & CHALLENGES Presenter: Mr Harold Phillip BA, LLB (Hons) LEC, MBA Commissioner of Police (Ag) Trinidad and Tobago Police Service VISION STATEMENT q To make every

DEALING WITH WHITE COLLAR CRIME SUCCESSES & CHALLENGES Presenter: Mr Harold Phillip BA, LLB (Hons) LEC, MBA Commissioner of Police (Ag) Trinidad and Tobago Police Service VISION STATEMENT q To make every

Digital Marketing Partner Organizer Knowledge Partner. May 26-27, 2017 New Delhi. June 9-10, 2017 Chennai.

Digital Marketing Partner Organizer Knowledge Partner May 26-27, 2017 New Delhi June 9-10, 2017 Chennai www.achromicpoint.com Introduction to the Program Corporate White Collar Crimes in India are spreading

Digital Marketing Partner Organizer Knowledge Partner May 26-27, 2017 New Delhi June 9-10, 2017 Chennai www.achromicpoint.com Introduction to the Program Corporate White Collar Crimes in India are spreading

ANTI-FRAUD POLICY. Reference No: ANTIFP-251. Policy Type: Governance. Directorate Area: All Directorates. Policy Author / Champion: Maurice Atkinson

ANTI-FRAUD POLICY Reference No: ANTIFP-251 Policy Type: Directorate Area: Policy Author / Champion: Governance All Directorates Maurice Atkinson Date(s) Equality Screened: 21 July 2017 Date(s) Approved

ANTI-FRAUD POLICY Reference No: ANTIFP-251 Policy Type: Directorate Area: Policy Author / Champion: Governance All Directorates Maurice Atkinson Date(s) Equality Screened: 21 July 2017 Date(s) Approved

ENFORCEMENT AND DISCLOSURES DIRECTORATE (EDD), CANADA REVENUE AGENCY (CRA)

, CANADA REVENUE AGENCY (CRA)") (EDD), CANADA REVENUE AGENCY (CRA) This presentation will explain that the mission of the Canada Revenue Agency s (CRA s) enforcement area is to deter, detect, and correct tax crimes. CRA s main goal is

(EDD), CANADA REVENUE AGENCY (CRA) This presentation will explain that the mission of the Canada Revenue Agency s (CRA s) enforcement area is to deter, detect, and correct tax crimes. CRA s main goal is

MANAGING THE RISK OF FRAUD IN A GLOBAL ENVIRONMENT

MANAGING THE RISK OF FRAUD IN A GLOBAL ENVIRONMENT PRESENTED BY DR. JOSHUA A. OKUMBE CHIEF EXECUTIVE OFFICER CENTRE FOR CORPORATE GOVERNANCE DURING ICPAK S 28 TH ANNUAL SEMINAR HELD AT THE PRIDE INN SAI

MANAGING THE RISK OF FRAUD IN A GLOBAL ENVIRONMENT PRESENTED BY DR. JOSHUA A. OKUMBE CHIEF EXECUTIVE OFFICER CENTRE FOR CORPORATE GOVERNANCE DURING ICPAK S 28 TH ANNUAL SEMINAR HELD AT THE PRIDE INN SAI

Fraud Prevention and Detection. Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar

Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar") Fraud Prevention and Detection Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar Opening Remarks Fraud - what is it? Fraud Risk Management Fraud

Fraud Prevention and Detection Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar Opening Remarks Fraud - what is it? Fraud Risk Management Fraud

The Risk of Economic Crime

The Risk of Economic Crime 0 ACFE European Fraud Conference London, March 7, 0 GROUP SECURITY HERE TO PROTECT OUR WORLD Torsten Wolf Group Head of Crime and Fraud Prevention Agenda Introduction Economic

The Risk of Economic Crime 0 ACFE European Fraud Conference London, March 7, 0 GROUP SECURITY HERE TO PROTECT OUR WORLD Torsten Wolf Group Head of Crime and Fraud Prevention Agenda Introduction Economic

Have you dealt with fraud in the past?

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

ANTI-FRAUD, BRIBERY AND CORRUPTION POLICY

ANTI-FRAUD, BRIBERY AND CORRUPTION POLICY Version: 6 Date issued: February 2018 Review date: February 2021 Applies to: All Trust staff, contractors and vendors This document is available in other formats,

ANTI-FRAUD, BRIBERY AND CORRUPTION POLICY Version: 6 Date issued: February 2018 Review date: February 2021 Applies to: All Trust staff, contractors and vendors This document is available in other formats,

Anti-fraud and Corruption Policy

Anti-fraud and Corruption Policy Responsible Division: Finances Validated by: Board (Executive Committee) Date of approval: 17/05/2017 Date of next review: May 2019 Language versions available: English

Anti-fraud and Corruption Policy Responsible Division: Finances Validated by: Board (Executive Committee) Date of approval: 17/05/2017 Date of next review: May 2019 Language versions available: English

Fraud prevention for credit unions

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

November 2017 ICPAK FORENSIC AUDIT SEMINAR

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

Forensic Accounting & Fraud Examination. Peter McLaren, CGA, CFE Partner McLaren Trefanenko Inc., CGA s

Forensic Accounting & Examination Peter McLaren, CGA, CFE Partner McLaren Trefanenko Inc., CGA s What is the ACFE? Global professional association providing anti-fraud information & education to help members

Forensic Accounting & Examination Peter McLaren, CGA, CFE Partner McLaren Trefanenko Inc., CGA s What is the ACFE? Global professional association providing anti-fraud information & education to help members

RICHARD B. HARER C.F.E., C.F.S. C.P.I., C.P.I.I., W.C.C.A.

9255 Corbin Ave. St. 200 Northridge, CA. 91324 (800) 714-FRAUD (3728) (818) 909-9607//(818) 782-3012, fax Internet: http://www.attyinfo.com E-mail: RichardH@specialpi.com RICHARD B. HARER C.F.E., C.F.S.

9255 Corbin Ave. St. 200 Northridge, CA. 91324 (800) 714-FRAUD (3728) (818) 909-9607//(818) 782-3012, fax Internet: http://www.attyinfo.com E-mail: RichardH@specialpi.com RICHARD B. HARER C.F.E., C.F.S.

ANTI FRAUD, BRIBERY AND CORRUPTION POLICY

ANTI FRAUD, BRIBERY AND CORRUPTION POLICY St Alban Catholic Academies Trust Anti-Fraud, Bribery and Corruption Policy 1. Introduction The Scheme of Delegation and/or the Financial Regulations Handbook

ANTI FRAUD, BRIBERY AND CORRUPTION POLICY St Alban Catholic Academies Trust Anti-Fraud, Bribery and Corruption Policy 1. Introduction The Scheme of Delegation and/or the Financial Regulations Handbook

Approval version. G l o b a l P o l i c y : F r a u d R e s p o n s e a n d W h i s t l e b l o w i n g P o l i c y. Board of Directors.

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

FINANCIAL STATEMENT FRAUD: IT S NOT JUST FOR BIG BUSINESS

Financial statement fraud is not limited to big business. It is more widespread than you may think. Explore the motivations behind and methods of manipulating reported financial results. From the landmark

Financial statement fraud is not limited to big business. It is more widespread than you may think. Explore the motivations behind and methods of manipulating reported financial results. From the landmark

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

A PRESENTATION AT THE 4 TH ANNUAL INSITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA (ICPAK) FINANCIAL CONFERNCE HILTON HOTEL, NAIROBI

FINANCIAL CONFERNCE HILTON HOTEL, NAIROBI") A PRESENTATION AT THE 4 TH ANNUAL INSITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA (ICPAK) FINANCIAL CONFERNCE HILTON HOTEL, NAIROBI BY CNTRAL BANK OF KENYA o Introduction? o Vulnerability of Accountants

A PRESENTATION AT THE 4 TH ANNUAL INSITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA (ICPAK) FINANCIAL CONFERNCE HILTON HOTEL, NAIROBI BY CNTRAL BANK OF KENYA o Introduction? o Vulnerability of Accountants

Whistle-Blowing Policy

2017 Ithmaar Bank Human Resources Department Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 3.0- Actions Constituting Fraud 3.1- Criminal / Unethical Conduct 3.2-

2017 Ithmaar Bank Human Resources Department Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 3.0- Actions Constituting Fraud 3.1- Criminal / Unethical Conduct 3.2-

IIA Fraud Conference. Case studies from recent investigations. 8 April 2015

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

Anti-Fraud Policy Date: Version: Review Date:

Anti-Fraud Policy Date: July 2017 Version: 4.0 Review Date: July 2019 Policy Title Anti-Fraud Policy Policy Number: POL 022 Version 4.0 Policy Sponsor Policy Owner Committee Chief Executive Director of

Anti-Fraud Policy Date: July 2017 Version: 4.0 Review Date: July 2019 Policy Title Anti-Fraud Policy Policy Number: POL 022 Version 4.0 Policy Sponsor Policy Owner Committee Chief Executive Director of

Revised: May Fraud Prevention Policy

Revised: May 2011 Fraud Prevention Policy Contents Page 1. Introduction 2 2. Basis of the Policy 3 3. Purpose and Definitions 3 4. Management and Staff Responsibilities 4 5. Adherence to University Regulations,

Revised: May 2011 Fraud Prevention Policy Contents Page 1. Introduction 2 2. Basis of the Policy 3 3. Purpose and Definitions 3 4. Management and Staff Responsibilities 4 5. Adherence to University Regulations,

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE GLObAL FrAUD STUDy

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

Theft, Fraud & Embezzlement

American Society of Health-System Pharmacists Theft, Fraud & Embezzlement ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] INTRODUCTION One of the main LEGAL responsibilities of

American Society of Health-System Pharmacists Theft, Fraud & Embezzlement ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] INTRODUCTION One of the main LEGAL responsibilities of

FRAUD POLICY. Fraud Policy-001

Effective Date: March 28, 2018 Owned by: Fraud Committee Review Cycle: Biennial Last Approved: March 28, 2018 Approved By: Executive Management Committee Revision History Revisions to Policy documents

Effective Date: March 28, 2018 Owned by: Fraud Committee Review Cycle: Biennial Last Approved: March 28, 2018 Approved By: Executive Management Committee Revision History Revisions to Policy documents

FOCUS ON FRAUD DETERRENCE

Audit Watch FOCUS ON FRAUD DETERRENCE With the recent sentencing of the former Dixon Comptroller, governmental fraud has become an all too familiar local news item. This month s edition of the Audit Watch

Audit Watch FOCUS ON FRAUD DETERRENCE With the recent sentencing of the former Dixon Comptroller, governmental fraud has become an all too familiar local news item. This month s edition of the Audit Watch

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

Rajeshri Rajani FCA AMAE BSC(Econ)

") Rajeshri Rajani FCA AMAE BSC(Econ) raj@rajaniandco.com 01933276327 PROFILE: Highly experienced forensic accountant and business advisor, remarkably versatile, having worked in a number of different industry

Rajeshri Rajani FCA AMAE BSC(Econ) raj@rajaniandco.com 01933276327 PROFILE: Highly experienced forensic accountant and business advisor, remarkably versatile, having worked in a number of different industry

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

University Fraud Policy

Section 1 University Fraud Policy 1. Introductory Statement The University is committed to the application of the Seven Principles of Public Life commended by the Committee for Standards in Public Life,

Section 1 University Fraud Policy 1. Introductory Statement The University is committed to the application of the Seven Principles of Public Life commended by the Committee for Standards in Public Life,

Fraud Awareness & Prevention for Higher Education. Neil Cohen Deputy Director Audit, Oversight & Investigations

Fraud Awareness & Prevention for Higher Education Neil Cohen Deputy Director Audit, Oversight & Investigations Goals Raise your fraud awareness and introduce you to fraud prevention methods. 2 Disclaimers

Fraud Awareness & Prevention for Higher Education Neil Cohen Deputy Director Audit, Oversight & Investigations Goals Raise your fraud awareness and introduce you to fraud prevention methods. 2 Disclaimers

Board Members. President: James Fellin, CPA, CFE

May 2009 Volume 9 Issue 11 The ACFE is the professional organization for fraud examiners. The mission of the ACFE is to reduce the incidence of fraud and whitecollar crime, and to assist the membership

May 2009 Volume 9 Issue 11 The ACFE is the professional organization for fraud examiners. The mission of the ACFE is to reduce the incidence of fraud and whitecollar crime, and to assist the membership

HFMU INVESTIGATOR TRAINING INDABA OPENING AND WELCOME

HFMU INVESTIGATOR TRAINING INDABA OPENING AND WELCOME Esteemed speakers, colleagues and guests it is with great pleasure that we welcome you to the 2013 HFMU investigator training indaba. We trust that

HFMU INVESTIGATOR TRAINING INDABA OPENING AND WELCOME Esteemed speakers, colleagues and guests it is with great pleasure that we welcome you to the 2013 HFMU investigator training indaba. We trust that

Chapter 1 THE NATURE OF FRAUD. Discussion Questions

Fraud Examination 5th Edition Solutions Manual by Albrecht Solutions Manual by W. Steve Albrecht, Chad O. Albrecht, Conan C. Albrecht, Mark F. Zimbelman. Download: https://testbankarea.com/download/fraud-examination-5th-editionsolutions-manual-albrecht/

Fraud Examination 5th Edition Solutions Manual by Albrecht Solutions Manual by W. Steve Albrecht, Chad O. Albrecht, Conan C. Albrecht, Mark F. Zimbelman. Download: https://testbankarea.com/download/fraud-examination-5th-editionsolutions-manual-albrecht/

global economic crime survey 2005

global economic crime survey 2005 Introduction Rodney Hay, Dispute Analysis and Investigations I am pleased to present the n results of the third biennial PricewaterhouseCoopers Economic Crime Survey.

global economic crime survey 2005 Introduction Rodney Hay, Dispute Analysis and Investigations I am pleased to present the n results of the third biennial PricewaterhouseCoopers Economic Crime Survey.

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

FRAUD POLICY. Mr Paul Nicholson, Assistant Director of Finance

Policy Code: TW/2/Fin (v5) 2016 Title: Author(s): Ownership: FRAUD POLICY Fraud Policy Mr Paul Nicholson, Assistant Director of Finance Finance and IT Directorate Date of SEMT Approval: April 2016 Date

Policy Code: TW/2/Fin (v5) 2016 Title: Author(s): Ownership: FRAUD POLICY Fraud Policy Mr Paul Nicholson, Assistant Director of Finance Finance and IT Directorate Date of SEMT Approval: April 2016 Date

2012 ACFE Canadian Fraud Conference. Fraud is a global problem. Be a part of the solution. KEYNOTE SPEAKERS. October 28-31, 2012 Ottawa

Fraud is a global problem. Be a part of the solution. 2012 ACFE Canadian Fraud Conference October 28-31, 2012 Ottawa KEYNOTE SPEAKERS Pamela Meyer, CFE Best-selling author of Liespotting: Proven Techniques

Fraud is a global problem. Be a part of the solution. 2012 ACFE Canadian Fraud Conference October 28-31, 2012 Ottawa KEYNOTE SPEAKERS Pamela Meyer, CFE Best-selling author of Liespotting: Proven Techniques

Course 4200: Detecting and Investigating Financial Statement Fraud (2 days)

") Course 4200: Detecting and Investigating Financial Statement Fraud (2 days) Course introduction This two-day immersion course provides an in-depth examination of financial statement fraud how it is defined,

Course 4200: Detecting and Investigating Financial Statement Fraud (2 days) Course introduction This two-day immersion course provides an in-depth examination of financial statement fraud how it is defined,

Report on cooperation challenges faced by the Court with respect to financial investigations. Workshop October 2015, The Hague, Netherlands

Report on cooperation challenges faced by the Court with respect to financial investigations Workshop 26-27 October 2015, The Hague, Netherlands Forward-looking conclusions Strengthening financial investigations

Report on cooperation challenges faced by the Court with respect to financial investigations Workshop 26-27 October 2015, The Hague, Netherlands Forward-looking conclusions Strengthening financial investigations

IESBA Agenda Paper 5-B February 2011 New Delhi, India

DRAFT WORDING Responding to Suspected Fraud or Illegal Acts 225.1 This section provides guidance to a professional accountant in public practice on how to respond when the accountant encounters a suspected

DRAFT WORDING Responding to Suspected Fraud or Illegal Acts 225.1 This section provides guidance to a professional accountant in public practice on how to respond when the accountant encounters a suspected

PROFILE. Key Qualifications. Certifications, License & Specialties

HARRY J. GARCIA, CFE, CPP, PRINCIPAL H. Garcia & Associates, Inc. 79 Vantis Drive, Aliso Viejo, CA 92656 California License No. PI 25405 714-334-2938 hgarcia@gar-max.com PROFILE Harry Garcia is the president

HARRY J. GARCIA, CFE, CPP, PRINCIPAL H. Garcia & Associates, Inc. 79 Vantis Drive, Aliso Viejo, CA 92656 California License No. PI 25405 714-334-2938 hgarcia@gar-max.com PROFILE Harry Garcia is the president

Called Contact Senior Clerk - John Pyne Telephone Fax

Called 2005 Email jamiesharma@187fleetstreet.com Contact Senior Clerk - John Pyne Telephone 0207 430 7423 Fax 0207 430 7431 Jamie Sharma Profile Jamie is a specialist lawyer in business crime and civil

Called 2005 Email jamiesharma@187fleetstreet.com Contact Senior Clerk - John Pyne Telephone 0207 430 7423 Fax 0207 430 7431 Jamie Sharma Profile Jamie is a specialist lawyer in business crime and civil

Conference of the States Parties to the United Nations Convention against Corruption

United Nations CAC/COSP/2013/L.11/Rev.1 Conference of the States Parties to the United Nations Convention against Corruption Distr.: Limited 28 November 2013 Original: English Fifth session Panama City,

United Nations CAC/COSP/2013/L.11/Rev.1 Conference of the States Parties to the United Nations Convention against Corruption Distr.: Limited 28 November 2013 Original: English Fifth session Panama City,

The Security Title Guarantee Corporation of Baltimore Anti Fraud Plan Update

The Security Title Guarantee Corporation of Baltimore Anti Fraud Plan 2013 Update Introduction The Security Title Guarantee Corporation of Baltimore (Company) recognizes that an insurance company must

The Security Title Guarantee Corporation of Baltimore Anti Fraud Plan 2013 Update Introduction The Security Title Guarantee Corporation of Baltimore (Company) recognizes that an insurance company must