Have you dealt with fraud in the past?

|

|

|

- Susan Harrell

- 5 years ago

- Views:

Transcription

1 Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham CPE Seminar 1

2 Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Bribery Illegal Gratuities Economic Extortion Financial Non-Financial Cash Non-Cash Larceny Skimming Fraudulent Disbursements Check Tampering Billing Schemes Payroll Schemes Expense Reimbursement Schemes Register Disbursements Misuse Larceny 3 Purpose of Internal Controls Ensures everything is done timely (order and efficiency) Ensures everything is done correctly (accuracy and completeness) Protects the assets of the organization (waste, fraud, and abuse) 4 DHG Birmingham CPE Seminar 2

3 The Human Element Internal controls in and of themselves do not ensure these purposes are met People within and organization following and enforcing internal controls do 5 The Human Element Controls Impeded Efficiency Inherent in every internal control is an additional layer of time and effort added to an individual s responsibilities Lack of Communication and Understanding Trust Trust is not an internal control 6 DHG Birmingham CPE Seminar 3

4 White Collar Crimes 7 Capital Crimes 8 DHG Birmingham CPE Seminar 4

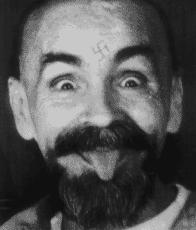

5 White Collar Criminals Don t Necessarily Look Like Criminals 9 Do good people commit fraud? 10 DHG Birmingham CPE Seminar 5

6 YES Business Partner Trusted Employee Friend Family Member Business Advisor Trustee 11 Good People Commit Fraud Understanding this fact is the key to establishing awareness and deterrence in this area to protect an organization and its employees Small Businesses vs. Big Businesses Big businesses are comprised of a lot of small businesses 12 DHG Birmingham CPE Seminar 6

7 Perpetrators * Association of Fraud Examiners 2014 Report to the Nations on Occupational Fraud and Abuse 13 Perpetrators * Association of Fraud Examiners 2014 Report to the Nations on Occupational Fraud and Abuse 14 DHG Birmingham CPE Seminar 7

8 Enabling Factors Donald Cressey s Fraud Triangle Perceived Opportunity Incentive / Pressure Rationalization **Personal integrity may be the most important factor in keeping a person from misappropriating assets.** 15 The Cycle Long term trusted employee Opportunity Runs into outside pressure or incentives Begins to rationalize Intends to repay I deserve it Makes the wrong decision Starts gradually Builds slowly over a period of time Hindsight is 20/20 It all makes sense in the end 16 DHG Birmingham CPE Seminar 8

9 Pressures and/or Incentives Mid-life Crisis Alcohol/Drugs Gambling Financial Difficulties Medical Costs due to illness Work Pressures To meet budgets To enhance bonuses 17 The 18 DHG Birmingham CPE Seminar 9

10 What do you do? Contact Counsel Labor Law Insurance Regulatory Identify and preserve sources of evidence Digital Public Records Social Media Records in Office Investigate Interview 19 Deterrence The most cost effective way to deal with occupational fraud is to deter it Deal with what we know Good people commit fraud Communication / awareness Controls protect organization and employees 20 DHG Birmingham CPE Seminar 10

11 Prevention Atmosphere of oversight Fraud Policy ( Because nobody asked. ) Fraud Risk Assessment Fraud Awareness Training 21 Prevention Afew key areas based on real fraud investigations Bank reconciliations; review cancelled checks Real segregation of duties Unpredictability in all compliance testing SURPRISE! SURPRISE! Unannounced Do not disclose sample selections Anonymous reporting mechanisms Job rotation/mandatory vacation 22 DHG Birmingham CPE Seminar 11

23 Analytical Results Benford s Law 24 DHG Birmingham CPE")

12 Prevention Afew key areas based on real fraud investigations Understand relationships In-house Customers Vendors Communicate importance of approval process Process of substance Utilize technology in testing (data analytics) 23 Analytical Results Benford s Law 24 DHG Birmingham CPE Seminar 12

13 Fraudulent Disbursements Example #1 25 Check Image 26 DHG Birmingham CPE Seminar 13

14 Bank Statement 27 Check Register 28 DHG Birmingham CPE Seminar 14

15 Fraudulent Disbursements Example #2 29 Check Image 30 DHG Birmingham CPE Seminar 15

16 Bank Statement 31 General Ledger 32 DHG Birmingham CPE Seminar 16

17 The Review of the Bank Reconciliation is a Process of Substance 33 Fraudulent Disbursements Example #3 34 DHG Birmingham CPE Seminar 17

18 Check Image 35 Check Image 36 DHG Birmingham CPE Seminar 18

19 Fraudulent Disbursements Example #4 37 Payable to Bank 38 DHG Birmingham CPE Seminar 19

20 Payable to Bank 39 Importance of Electronic Evidence 40 DHG Birmingham CPE Seminar 20

21 Text Messages Example #5 41 Theft of Vault Cash November 21, :53:59 PM EST They up my xxx with all of this. November 21, :54:46 PM EST Proving u took anythg is going to be the hard part because ur lifestyle never changed. But everyone is hurting right now. November 21, :55:15 PM EST I will call u in a bit. Just stick with ur story cause again they have to prove u took the funds. November 21, :55:36 PM EST I gotta cover my xxx cause I think they gonna try to come at me and xxxx cause I'm over operations. 42 DHG Birmingham CPE Seminar 21

22 Questions 43 Questions Roy Strickland, CPA/CFF, CFE, MAFF Charleston, SC DHG Birmingham CPE Seminar 22

Mitigating Fraud. June 22, Sept. 21, 2014

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

Figure 1: Occupational Frauds by Category Frequency

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Figure 1: Breakdown of Cases by Country

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Figure 1: Breakdown of Cases by Country Country Number of Cases Albania 1 Armenia 3 Bulgaria 5 Czech Republic 8 Hungary 2 Kazakhstan 5 Kosovo 1 Montenegro 2 Poland 8 Romania 11 Russia 21 Serbia 4 Slovakia

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

OAPT June 9, Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen:

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

AGA Risk and Fraud Webinar

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

AGA Risk and Fraud Webinar February 22, 2017 Let s Begin with the Basics 5% of revenues lost to fraud every year Median fraud duration from start to detection is 18 months Small organizations tend to suffer

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Analyzing a Potpourri of Fraud in Higher Education. Calvin Wendelboe, CPA, CIA, CFE

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

OCCUPATIONAL FRAUD 9/20/2018

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

Catch Me If You Can. Fraud in Local Government. CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Good From The Inside Out. Saturday, April 8, 2017

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Fraud Prevention for Nonprofits

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud in Government. Mike Nolan, CPA, CFE, CGMA. CCACC & CCA&RMC Conference Monterey, CA September 2014

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud Detection and Prevention for Governmental Organizations. Michael A. Swafford, CIA, CFE

Fraud Detection and Prevention for Governmental Organizations Michael A. Swafford, CIA, CFE Presenter Michael A. Swafford, CIA, CFE Mike is a Consulting Manager in our Forensic Valuation Services Practice

Fraud Detection and Prevention for Governmental Organizations Michael A. Swafford, CIA, CFE Presenter Michael A. Swafford, CIA, CFE Mike is a Consulting Manager in our Forensic Valuation Services Practice

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

FRAUD EXAMINERS MANUAL (INTERNATIONAL EDITION)

") TABLE OF CONTENTS SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES OCCUPATIONAL FRAUDS ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 FINANCIAL STATEMENT FRAUD What Is Financial

TABLE OF CONTENTS SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES OCCUPATIONAL FRAUDS ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 FINANCIAL STATEMENT FRAUD What Is Financial

Fraud in the Government Realm. Introduction. What is Fraud? My career began with a local government fraud in 1993

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

MIS 520 Data Analytics for IT Auditors

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

Sunera Canada ULC. Effective Fraud Risk Assessment Annual Fraud Program. October 21, 2016

Sunera Canada ULC Effective Fraud Risk Assessment 2016 Annual Fraud Program October 21, 2016 Sunera LLC Snapshot Professional consultancy with core competency in Governance, SOx, NI 52-109, Internal Audit,

Sunera Canada ULC Effective Fraud Risk Assessment 2016 Annual Fraud Program October 21, 2016 Sunera LLC Snapshot Professional consultancy with core competency in Governance, SOx, NI 52-109, Internal Audit,

A c f e. Report to. the Nation. on Occupational Fraud & Abuse

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Presented by Duncan Will CPA/ABV/CFF, CFE

Texas Society of CPAs Title Austin - Heading Chapter Risk Management and the Emerging Profession: Risks and Rewards Presented by Duncan Will CPA/ABV/CFF, CFE Sound Familiar? The accompanying financial

Texas Society of CPAs Title Austin - Heading Chapter Risk Management and the Emerging Profession: Risks and Rewards Presented by Duncan Will CPA/ABV/CFF, CFE Sound Familiar? The accompanying financial

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Everything You Didn t Want To Know About Employee Crime

Everything You Didn t Want To Know About Employee Crime It's something employers don't want to have to think about: employee crime. Finding out that trusted, long-term employees have been stealing from

Everything You Didn t Want To Know About Employee Crime It's something employers don't want to have to think about: employee crime. Finding out that trusted, long-term employees have been stealing from

IIA Fraud Conference. Case studies from recent investigations. 8 April 2015

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE GLObAL FrAUD STUDy

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

5/15/2015. Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace

Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace by Donna M. Ingram, CPA, CFE, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Luca Pacioli, the "Father of Accounting",

Using Financial Data and Ratios to Drive Performance and Detecting Fraud in the Workplace by Donna M. Ingram, CPA, CFE, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Luca Pacioli, the "Father of Accounting",

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

November 2017 ICPAK FORENSIC AUDIT SEMINAR

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

Internal Controls over Expenditures

Internal Controls over Expenditures Trainer: Anthony Gerharz, CPA 1 Materials/Disclaimer Please note that these materials are incomplete without the accompanying oral comments by the trainer(s). These

Internal Controls over Expenditures Trainer: Anthony Gerharz, CPA 1 Materials/Disclaimer Please note that these materials are incomplete without the accompanying oral comments by the trainer(s). These

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE M I D D L E E AST AN D N O RT H AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6

7/21/2015. July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT. Lessons from the Trenches. Angela Morelock Partner

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

Fraud Examination. Prevention, Detection, and Investigation. Steven M. Bragg

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

COVERAGE FRAUD IN EMPLOYEE BENEFIT PLANS 5/15/2014. Where employee benefit fraud is likely. Internal controls that help prevent fraud

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD EXAMINERS MANUAL

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE FOREWORD Bruce Dorris, J.D., CFE, CPA President and CEO, Association of Certified Fraud Examiners With the publication of the 2018

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE FOREWORD Bruce Dorris, J.D., CFE, CPA President and CEO, Association of Certified Fraud Examiners With the publication of the 2018

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations

NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations Allan Bachman, CFE Retired Education Manager ACFE Agenda The ACFE & Mission ACFE 2016 Report to

NABCA 23 rd Annual Administrators Conference The Forensics of Fraud: Conducting Financial Investigations Allan Bachman, CFE Retired Education Manager ACFE Agenda The ACFE & Mission ACFE 2016 Report to

Annie Chan Managing Director Forensic & Investigation Services FCPA, LLB, LLM, MBA,CFE

Forensic Accounting and Fraud Risks for MNCs in China Presented by: Annie Chan Managing Director Forensic & Investigation Services FCPA, LLB, LLM, MBA,CFE What is Forensic Accounting A discipline that

Forensic Accounting and Fraud Risks for MNCs in China Presented by: Annie Chan Managing Director Forensic & Investigation Services FCPA, LLB, LLM, MBA,CFE What is Forensic Accounting A discipline that

Using Data Analytics to Detect Fraud

Using Data Analytics to Detect Fraud Data Analysis Tests for Detecting Corruption 2018 Association of Certified Fraud Examiners, Inc. Corruption Schemes Involve employees use of their influence in a business

Using Data Analytics to Detect Fraud Data Analysis Tests for Detecting Corruption 2018 Association of Certified Fraud Examiners, Inc. Corruption Schemes Involve employees use of their influence in a business

Crime Pays Recovering Employee-Dishonesty Claims.

Crime Pays Recovering Employee-Dishonesty Claims. September 23,2014 Today s Speakers CHRISTOPHER GIOVINO Global Practice Leader for forensic investigations, crime and fidelity claims and Cyber Evaluation

Crime Pays Recovering Employee-Dishonesty Claims. September 23,2014 Today s Speakers CHRISTOPHER GIOVINO Global Practice Leader for forensic investigations, crime and fidelity claims and Cyber Evaluation

Fraud in the Revenue Cycle

Fraud in the Revenue Cycle 2018 MMGMA Winter Conference March 7, 2018 Depend On Our People Count On Our Advice Why are we here? Consumer Payments to Providers have increased: 2011 to 2014-193% 2013 to

Fraud in the Revenue Cycle 2018 MMGMA Winter Conference March 7, 2018 Depend On Our People Count On Our Advice Why are we here? Consumer Payments to Providers have increased: 2011 to 2014-193% 2013 to

Lecture Notes for How to Steal $500 Million

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT MODERATOR: LAURIE DE ARMOND TIM MOHR, MIKE SORRELLS AND RANDAL SIMONETTI DECEMBER 9, 2013 BDO USA, LLP, a Delaware limited liability partnership,

PROTECTING YOUR NONPROFIT ORGANIZATION FROM FRAUD AND EMBEZZLEMENT MODERATOR: LAURIE DE ARMOND TIM MOHR, MIKE SORRELLS AND RANDAL SIMONETTI DECEMBER 9, 2013 BDO USA, LLP, a Delaware limited liability partnership,

Procurement Fraud s Anatomy. By Tom Caulfield CFE/CIG/CIGI

Procurement Fraud s Anatomy By Tom Caulfield CFE/CIG/CIGI LEARNING OBJECTIVES 1. Identify statutes, regulations, and key personnel associated with the contracting process. 2. Identify the primary acquisition

Procurement Fraud s Anatomy By Tom Caulfield CFE/CIG/CIGI LEARNING OBJECTIVES 1. Identify statutes, regulations, and key personnel associated with the contracting process. 2. Identify the primary acquisition

INTRODUCTION TO FRAUD EXAMINATION

TABLE OF CONTENTS I. INTRODUCTION TO FRAUD EXAMINATION Introduction... 1 Axioms of Fraud Examination... 1 Fraud Is Hidden... 1 Reverse Proof... 1 Existence of Fraud... 2 Predication... 2 Fraud Theory Approach...

TABLE OF CONTENTS I. INTRODUCTION TO FRAUD EXAMINATION Introduction... 1 Axioms of Fraud Examination... 1 Fraud Is Hidden... 1 Reverse Proof... 1 Existence of Fraud... 2 Predication... 2 Fraud Theory Approach...

Cyber Insecurity - Making Sense of Payment Fraud

Cyber Insecurity - Making Sense of Payment Fraud James Richardson Head of Pre-Sales & Consulting Thursday 23 February 2017 BCS, Chartered Institute for IT Businesses and Banks rely on Bottomline for domestic

Cyber Insecurity - Making Sense of Payment Fraud James Richardson Head of Pre-Sales & Consulting Thursday 23 February 2017 BCS, Chartered Institute for IT Businesses and Banks rely on Bottomline for domestic

Delivering Financial Oversight: Strengthening Your Policies and Procedures

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Delivering Financial Oversight: Strengthening Your Policies and Procedures Aaron J. Mansfield, CPA, CFE, Manager October 13, 2014 1 Dennis, Gartland & Niergarth Certified Public Accountants/Business Advisors

Lecture notes for: Corporate Cons

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

T H E A S S O C I A T I O N

A B O U T T H E A S S O C I A T I O N Since 1988 there has been only one organization whose main focus is to train anti-fraud professionals in their fight against economic crime: the Association of Certified

A B O U T T H E A S S O C I A T I O N Since 1988 there has been only one organization whose main focus is to train anti-fraud professionals in their fight against economic crime: the Association of Certified

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Anti-Fraud Policy. Version: 8.0 Approval Status: Approved. Document Owner: Graham Feek. Review Date: 07/12/2018

Anti-Fraud Policy Version: 8.0 Approval Status: Approved Document Owner: Graham Feek Classification: External Review Date: 07/12/2018 Last Reviewed: 09/12/2016 Table of Contents 1. Policy Statement...

Anti-Fraud Policy Version: 8.0 Approval Status: Approved Document Owner: Graham Feek Classification: External Review Date: 07/12/2018 Last Reviewed: 09/12/2016 Table of Contents 1. Policy Statement...

Don t be a Victim of Fraud: Profile of Perpetrator Dr. Peter Hughes, Assistant Auditor-Controller, Los Angeles County Harriet Richardson, City

Profile of Perpetrator Dr Peter Hughes, Assistant Auditor-Controller, Los Angeles County Harriet Richardson, City Auditor, City of Palo Alto Mark Cousineau, Director, MGO CPAs and Advisors Presenters Harriet

Profile of Perpetrator Dr Peter Hughes, Assistant Auditor-Controller, Los Angeles County Harriet Richardson, City Auditor, City of Palo Alto Mark Cousineau, Director, MGO CPAs and Advisors Presenters Harriet

Fraud Prevention and Detection. Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar

Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar") Fraud Prevention and Detection Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar Opening Remarks Fraud - what is it? Fraud Risk Management Fraud

Fraud Prevention and Detection Lisa dewit, Sr Project Manager (3-5631) Formation Review 20 Oct 17 Prepared for: IIA Annual Fraud Seminar Opening Remarks Fraud - what is it? Fraud Risk Management Fraud

ABOUT THE PROGRAMME. The FCPA certification programme consists of 5 papers:

ABOUT THE PROGRAMME The Forensic Certified Public Accountant (FCPA) programme is a certification program developed by the FCPA Society of the United States of America. It is an internationally accepted

ABOUT THE PROGRAMME The Forensic Certified Public Accountant (FCPA) programme is a certification program developed by the FCPA Society of the United States of America. It is an internationally accepted

Demystifying Forensic Accounting

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com AdrianSierra,CPA,CFE,CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining and

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com AdrianSierra,CPA,CFE,CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining and

Demystifying Forensic Accounting

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com Adrian Sierra, CPA, CFE, CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining

Demystifying Forensic Accounting Michael T. Dyer, CFE Phone: (312) 961 2711 mike.dyer@sfg global.com Adrian Sierra, CPA, CFE, CFF, CGMA Phone: (312) 451 4502 adrian.sierra@sfg global.com AGENDA Defining

STURM, RUGER & COMPANY, INC. CODE OF BUSINESS CONDUCT AND ETHICS

STURM, RUGER & COMPANY, INC. CODE OF BUSINESS CONDUCT AND ETHICS Sturm, Ruger & Company, Inc. (the "Company") maintains an extensive "Corporate Compliance Program" which governs the obligation of all employees,

STURM, RUGER & COMPANY, INC. CODE OF BUSINESS CONDUCT AND ETHICS Sturm, Ruger & Company, Inc. (the "Company") maintains an extensive "Corporate Compliance Program" which governs the obligation of all employees,

The Procurement Fraud Equation. Tom Caulfield

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

1/24/14. Fraud Detec/on and Preven/on. Agenda. Fraud Cases in Minnesota - Schools

February 7, 2014 Fraud Detec/on and Preven/on Presented by: Steve Wischmann, CPA, CFE, CFF, CCFE, MAFF Agenda 1. Actual Minnesota School Cases in the News 2. Definition of Fraud 3. Fraud Statistics-ACFE

February 7, 2014 Fraud Detec/on and Preven/on Presented by: Steve Wischmann, CPA, CFE, CFF, CCFE, MAFF Agenda 1. Actual Minnesota School Cases in the News 2. Definition of Fraud 3. Fraud Statistics-ACFE

Internal Routine & Controls (IRC) & Fraud New York Region Directors College

& Fraud New York Region Directors College") Internal Routine & Controls (IRC) & Fraud 2015 New York Region Directors College Discussion Topics Fraud: What It Is and Why People Commit It Fundamentals of IRC and Fraud Prevention Insider Fraud Fraud

Internal Routine & Controls (IRC) & Fraud 2015 New York Region Directors College Discussion Topics Fraud: What It Is and Why People Commit It Fundamentals of IRC and Fraud Prevention Insider Fraud Fraud

The Role of Internal Controls in the Fight Against Fraud. John Tonsick, CFE, CPA Association of Certified Fraud Examiners, Inc.

The Role of Internal Controls in the Fight Against Fraud John Tonsick, CFE, CPA 2015 Association of Certified Fraud Examiners, Inc. The Role of Internal Controls in the Fight Against Fraud The Conjurer

The Role of Internal Controls in the Fight Against Fraud John Tonsick, CFE, CPA 2015 Association of Certified Fraud Examiners, Inc. The Role of Internal Controls in the Fight Against Fraud The Conjurer

Fraud/Not Fraud. The University of Texas Approach. 13 th Annual Fraud Summit. March 23, 2018

Fraud/Not Fraud The University of Texas Approach 13 th Annual Fraud Summit Benefitting the UT Dallas Center for Internal Auditing Excellence March 23, 2018 Agenda Definitions Collaboration and Coordination

Fraud/Not Fraud The University of Texas Approach 13 th Annual Fraud Summit Benefitting the UT Dallas Center for Internal Auditing Excellence March 23, 2018 Agenda Definitions Collaboration and Coordination

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE AS I A- PACI F I C E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations 8

Fraud: How to Get Your District Free Publicity

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

CSMFO CONFERENCE 2018

CSMFO CONFERENCE 2018 Fraud: A Story of Embezzlement, Response, and Resilience February 22, 2018 Presented by: Damien Arrula City of Placentia Kenneth H. Pun The Pun Group, LLP 1 Objectives Hear a real

CSMFO CONFERENCE 2018 Fraud: A Story of Embezzlement, Response, and Resilience February 22, 2018 Presented by: Damien Arrula City of Placentia Kenneth H. Pun The Pun Group, LLP 1 Objectives Hear a real

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Forensic Accounting. Ms. Dhir. Forensic Accountant (FoA) #IMASLC17

#IMASLC17") Forensic Accounting Ms. Dhir Forensic Accountant (FoA) OUTLINE Introduction Definitions History Today (Industry, Public Accounting, Government (Crimes) ) Engagements Qualifications (Skills & Certifications,

Forensic Accounting Ms. Dhir Forensic Accountant (FoA) OUTLINE Introduction Definitions History Today (Industry, Public Accounting, Government (Crimes) ) Engagements Qualifications (Skills & Certifications,

Supplementary Study Guide to Accompany the Quarterly CPE Exam on Topics Addressed in the Journal of Accountancy Second Quarter (April June), 2017

, 2017") Highly educated young people are tutored, taught, and monitored in all aspects of their lives except the most important, which is character-building. But without character and courage, nothing else lasts....david

Highly educated young people are tutored, taught, and monitored in all aspects of their lives except the most important, which is character-building. But without character and courage, nothing else lasts....david

Blockchain & Cryptocurrencies Forensic Services Implications. October 25, 2018

Blockchain & Cryptocurrencies Forensic Services Implications October 25, 2018 Agenda: Forensics and Blockchain & Cryptocurrencies 1. Stolen funds used to purchase cryptocurrencies 2. Employee misappropriation

Blockchain & Cryptocurrencies Forensic Services Implications October 25, 2018 Agenda: Forensics and Blockchain & Cryptocurrencies 1. Stolen funds used to purchase cryptocurrencies 2. Employee misappropriation

A positive outlook on auto-enrolment contributions phasing. High

A positive outlook on auto-enrolment contributions phasing High Summary UK businesses are focusing on securing the organisation s future by strengthening their competitive position, increasing revenue

A positive outlook on auto-enrolment contributions phasing High Summary UK businesses are focusing on securing the organisation s future by strengthening their competitive position, increasing revenue

POLICY: FRAUD PREVENTION. October 2017

POLICY: October 2017 CONTENTS 1. PURPOSE P3 2. SCOPE P3 3. LEGISLATION AND CORPORATE GOVERNANCE REQUIREMENTS REFERENCE 4. POLICY STATEMENT AND INTERNAL STANDARDS P3 P4 4.1 Background P4 4.2 Actions constituting

POLICY: October 2017 CONTENTS 1. PURPOSE P3 2. SCOPE P3 3. LEGISLATION AND CORPORATE GOVERNANCE REQUIREMENTS REFERENCE 4. POLICY STATEMENT AND INTERNAL STANDARDS P3 P4 4.1 Background P4 4.2 Actions constituting

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY Letter from the President In 1996, Dr. Joseph T. Wells, CFE, CPA, founder and Chairman of the ACFE, directed the publication

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY Letter from the President In 1996, Dr. Joseph T. Wells, CFE, CPA, founder and Chairman of the ACFE, directed the publication

Fraud and corruption prevention and control policy of the International Federation of Red Cross and Red Crescent Societies

www.ifrc.org Saving lives, changing minds. Fraud and corruption prevention and control policy of the International Federation of Red Cross and Red Crescent Societies Document Issued On: [insert date] Approved

www.ifrc.org Saving lives, changing minds. Fraud and corruption prevention and control policy of the International Federation of Red Cross and Red Crescent Societies Document Issued On: [insert date] Approved

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE S U B - SAHAR AN AF R I CA E DI T I O N CONTENTS Introduction 3 How Occupational Fraud Is Committed 4 Detection 6 Victim Organizations

Identity theft and abuse of information in fraud and corruption

Identity theft and abuse of information in fraud and corruption Steven Powell FISA Conference September 2018 overview What is identity theft Elements of fraud The consequences The reality EFT fraud How

Identity theft and abuse of information in fraud and corruption Steven Powell FISA Conference September 2018 overview What is identity theft Elements of fraud The consequences The reality EFT fraud How

CRIMESTAR. commercial crime from a different angle

CRIMESTAR commercial crime from a different angle CRIMESTAR commercial crime from a different angle THE IMPORTANCE OF BROAD COVER FOR DIFFERENT TYPES OF FRAUD The motivation for fraud is triggered by a

CRIMESTAR commercial crime from a different angle CRIMESTAR commercial crime from a different angle THE IMPORTANCE OF BROAD COVER FOR DIFFERENT TYPES OF FRAUD The motivation for fraud is triggered by a

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

ANTI FRAUD, BRIBERY AND CORRUPTION POLICY

ANTI FRAUD, BRIBERY AND CORRUPTION POLICY St Alban Catholic Academies Trust Anti-Fraud, Bribery and Corruption Policy 1. Introduction The Scheme of Delegation and/or the Financial Regulations Handbook

ANTI FRAUD, BRIBERY AND CORRUPTION POLICY St Alban Catholic Academies Trust Anti-Fraud, Bribery and Corruption Policy 1. Introduction The Scheme of Delegation and/or the Financial Regulations Handbook