INTERNAL FRAUD PREVENTION:

|

|

|

- Myron Hoover

- 5 years ago

- Views:

Transcription

1 INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1

2 The Not Quite Yet Ex-Employee An accountant changed the direct deposit routing number and account number to three of her own bank accounts on six previously terminated employees. No one noticed until $250,000 and 7 months later, a former employee called asking why his W-2 reflected $50,000 more than he was paid! 2

3 THE GENIUS Kyle embezzled funds from his cooperative by increasing the tip amount on the customer s copy of restaurant credit card receipts by approximately $2 to $3 per meal. The actual restaurant copy of the receipt represented the actual lesser amount charged to the credit card. He would then attach the customer copy of the receipt to his expense report for reimbursement of charges to his personal credit card.

4 Why Prevention? I m a true believer that you have a moral obligation to keep your employees honest, and that is why you have controls; so I m never tempted or put in a position where I could do something to defraud my employer Frank Abagnale, Jr. because it is OUR responsibility!

5 Who is Committing Fraud? 5

6 The Common Victim Response Steve, I can t believe this happened to us and by him I trusted him; he s been here forever; he s the last person I would have suspected! 6

7 FRAUD? FRAUD RULE #1 Fraud and Stupid Look Just Alike Mens Rea (the criminal state of mind) Turns Stupid Into Fraud 7

8 As Long As It s Paid in Full The accountant used the cooperative credit card for personal purchases as well as for business purposes. She paid the business purpose portion of the balance with a cooperative check and the personal portion with a personal check. Is this fraud? 8

9 Internal Fraud The Three C s A criminal act has been Committed The Act has been Concealed The perpetrator Converted the results of the Act for personal gain (personal benefit) 9

10 Internal Fraud Mens Rea The Criminal State of Mind INTENT: A deliberate, purposeful resolve to bring about a particular result. Circumstantial evidence is allowed as support for intent. 10

11 Internal Fraud Mens Rea The Criminal State of Mind KNOWLEDGE: A perpetrator s deliberate indifference to his or her behavior that almost certainly creates a risk that results in a criminal outcome A perpetrator is aware of the nature of his conduct and didn t act through ignorance, mistake, or accident 11

12 Internal Fraud Mens Rea The Criminal State of Mind RECKLESS CONDUCT: Acting with a conscious disregard that exposes others to unjustifiable risk A gross deviation from a standard of care that a reasonable person would take in a given situation 12

13 As Long As It s Paid in Full The accountant used the cooperative credit card for personal purchases as well as for business purposes. She paid the business purpose portion of the balance with a cooperative check and the personal portion with a personal check for the most part she may have misclassified $30k, $40k, $50k of personal charges as business charges. 13

14 As Long As It s Paid in Full Evidence: Fictitious reports to the board regarding usage White-out on the credit card statements to conceal true nature of the charges Is this fraud? 14

15 CONTROL ACTIVITIES Raising the Walls of Protection

16 The Development of Control Activities Guiding Principles of Control Activities Design Design the internal control around the POSITION, never around the PERSON in that position The PERCEPTION OF DETECTION is the strongest internal control that can be implemented

17 The Shell Company Kyle, the Cooperative purchasing agent, stole over $3.8 million using a simple shell company fraud method: Created a separate company, Opened a separate bank account, Subscribed to a mail drop service, Obtained an endorsement stamp, Created invoices to his cooperative for fictitious transformer purchases

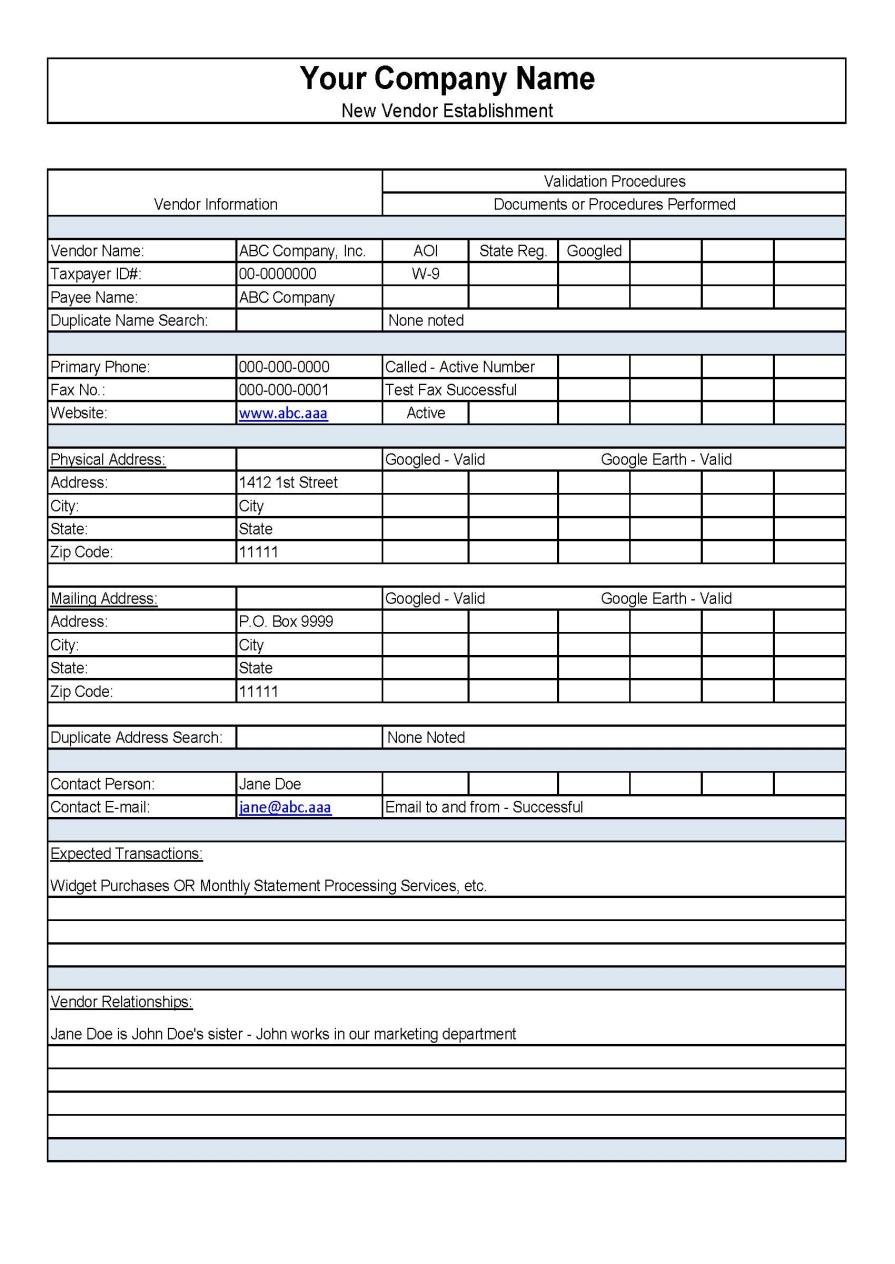

18 The Shell Company Fraud New Vendor Establishment Causing your employer to make disbursements to a company that you own, without your employer s knowledge that you own that company for either legitimate costs or for bogus costs.

19 The Shell Company Fraud New Vendor Establishment Creation of a fictitious vendor or a vendor not necessary to the business Names of the vendors can be similar to existing valid vendors ABC Company, Inc. ABC Company ABC Co., Inc. ABC, Inc.

20 Control Considerations for New Vendor Establishment New Vendor Establishment Process / Form Conflict of Interest Form Compliance Audit Procedures

21

22 SCOTCO, Inc. Conflict of Interest Form To be completed annually by all employees, owners, and members of the governing body. If there are any questions as to what category a relationship should be included, select one and management shall determine any necessary reclassifications. Name: Title: Signature Please provide individual names, company names, and the nature of the relationships that may exist with organizations that our company does business with or that you could reasonably expect our company could potentially enter into a relationship with, as relates to:

23 SCOTCO, Inc. Conflict of Interest Form Family Relationships: Personal Relationships: Business Relationships: Financial Relationships:

24

25 Your Company Name New Vendor Establishment Vendor Information Validation Procedures Documents or Procedures Performed Vendor Name: ABC Company, Inc. AOI State Reg. Googled Taxpayer ID#: W-9 Payee Name: ABC Company Duplicate Name Search: None noted Primary Phone: Called - Active Number Fax No.: Test Fax Successful Website: Active

26 Your Company Name New Vendor Establishment Vendor Information Validation Procedures Documents or Procedures Performed Physical Address: Googled - Valid Google Earth - Valid Address: st Street City: City State: State Zip Code: Mailing Address: Googled - Valid Google Earth - Valid Address: P.O. Box 9999 City: City State: State Zip Code: Duplicate Address Search: None Noted Contact Person: Jane Doe Contact jane@abc.aaa to and from - Successful

27 Your Company Name New Vendor Establishment Vendor Information Validation Procedures Documents or Procedures Performed Expected Transactions: Widget Purchases OR Monthly Statement Processing Services, etc. Vendor Relationships: Jane Doe is John Doe's sister - John works in our marketing department

28 SCOTCO, Inc. Anti-fraud Program Documentation of Control Activities Dated: September 16, 20xx New Vendor Establishment Procedures Control Activities 1 A Master Vendor File will be maintained and updated on a regular basis 2 A New Vendor Establishment Form will be initiated within the accounts payable department for all new vendors 3 Information to be obtained for the form will be requested from the new vendor and completed by Accounts Payable Clerk #1 4 Accounts Payable Clerk #1 will forward the information completed portion of the New Vendor Establishment form to Accounts Payable Clerk #2 Accounts Payable Clerk #2 will then validate the information on the form. Validation and verification will include: Phone calls to numbers provided 5 Test message to the provided Web based search engine inquiries State tax base searches Online mapping or Google Earth searches of address provided 6 Accounts Payble Clerk #2 will forward the completed New Vendor Establishment Form to Management for approval 7 The approved New Vendor Establishment form, along with any other documentation from the vendor, will be added to the Master Vendor File 8 As a part of the formal monitoring program, compliance with the review of the supporting documentation and form completion for the Master Vendor File will be audited annually to determine the level of adherance to that control activity. The audit will be conducted by the board audit committee

29 Control Considerations for New Vendor Establishment Processes MUST include the requirement for periodic Master Vendor File compliance testing to determine that vendors listed in the vendor master file have been subjected to these internal controls

30 The Front Counter: Accounts Receivable Lapping Suppose the cooperative has three member customers, A, B, and C. When A s payment is received, the perpetrator steals it instead of posting it to A s account.

31 The Front Counter: Accounts Receivable Lapping Member A expects that his account will be credited with the payment he has made. If not, he will almost certainly complain. To avoid this, the perpetrator must take some action to make it appear that the payment was posted.

32 The Front Counter: Accounts Receivable Lapping When B s check arrives, the perpetrator posts this money to A s account. Payments now appear to be up-to-date on A s account, but B s account is behind. When C s payment is received, the perpetrator applies it to B s account.

33 The Front Counter: Accounts Receivable Lapping This process continues indefinitely until one of three things happens: (1) someone discovers the scheme, (2) restitution is made to the accounts, (3) some concealing entry is made to adjust the accounts receivable balances.

34 Control Considerations for Accounts Receivable Lapping Segregate cash handling from cash recording Periodic verification of cash drawer, noting personal checks in the drawer Mandatory vacation

35 Control Considerations for Accounts Receivable Lapping Stamp all checks for deposit only Control credit memos and receivable write-offs Periodically audit for no mail statements Establish a lock-box payment system

36 Control Considerations for Accounts Receivable Lapping Rotate employees Periodic matching of daily deposit to accounts receivable posting

37 The Front Counter: Cash Theft from Deposit It is what it is Checks received = $500 Cash received = 100 Deposit should be = $600 Cash stolen = $75 Deposit is actually = $525

38 The Front Counter: Cash Theft from Deposit Concealment: Personal checks in the drawer to balance Credit memos / AR Adjustments Accounts receivable write-offs Other non-standard journal entries

39 Control Considerations for Cash Theft from Deposit Periodic verification of cash drawer, noting personal checks in the drawer Stamp all checks for deposit only Control credit memos and receivable write-offs Establish a lock-box payment system

40 Control Considerations for Cash Theft from Deposit Rotate employees duties Match bank stamped deposit slip to copy of deposit slip as prepared Surveillance Camera

41 Other Recurring Cases Have you been to an Office Depot lately?... Home Depot?... Staples Etc, Etc An employee cost his cooperative $200,000 over a 4 year period by charging personal items to these types of accounts. Payments on these accounts were accomplished by both paper check and online bill payment.

42 Control Activities The Absolutes Pre-employment Background and Reference Checks Required Annual Completion of the Conflict of Interest Form Required Use of Vacation Time Required Supporting Documentation and Approval for Non-standard Journal Entries Physical Inventory Count

43 Control Activities The Absolutes Proper Approval of Inventory Write-offs Proper Approval of Accounts Receivable / Debit Balance Accounts Payable Write-offs Proper Approval for Billing Adjustments/Credit Memos or Other Nonpayment Credits to Accounts Receivable Proper Disbursement Approval Procedures New Vendor Establishment Processes

44 Monitoring and Routine Maintenance: The Compliance Audit Function

45 Monitoring and Routine Maintenance The 2 Questions of Monitoring Are processes and controls working as intended? Are there processes or activities that we need to refine, add, or delete?

46 Monitoring and Routine Maintenance Compliance Auditing Compliance Audits: The Absolutes Authorized check approval process Accounts receivable charge-off process Inventory write-off process Journal entry approval and documentation process Master vendor file audit Contract procurement audit

47 FRAUD RISK ASSESSMENT Laying the Ground Floor

48 FRAUD RISK ASSESSMENT The process aimed at proactively identifying and addressing the cooperative s vulnerabilities to internal fraud

49 FRAUD RISK ASSESSMENT Goal: To Identify the Areas Vulnerable to the Risk of Fraud in Our Cooperative The Objective is not to prevent fraud the Objective is to determine what frauds need to be prevented. Control activities have the objective of preventing fraud.

50 FRAUD RISK ASSESSMENT The Simple Technique Lock yourselves in a room and BRAINSTORM! Brainstorm GENERAL Processes Brainstorm SPECIFIC Processes

51 FRAUD RISK ASSESSMENT General Processes General Processes Are Simply Identified by: How money comes in, and How money goes out.

52 FRAUD RISK ASSESSMENT Specific Processes Specific Processes Are Simply Identified by: Financial Statement Line Items Cash in Bank Accounts Receivable Inventory Fixed Assets Sales Etc.

53 SUMMARY Fraud is Happening! Shell Company Fraud Cash Fraud Disbursement Fraud Consider the Control Absolutes Attempt a Risk Assessment Process (you may be surprised at what you find)

54 INTERNAL FRAUD PREVENTION: Common Frauds and the Absolutes of Internal Control Design STEVE DAWSON, CPA, CFE Dawson Forensic Analytics, P.L.L.C. d/b/a DAWSON FORENSIC GROUP P.O. Box Lubbock, Texas

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Chapter 2 Skimming. 2. To a fraudster, the principle advantage of skimming is the difficulty with which the scheme is detected. a. True b.

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Lecture notes for: Corporate Cons

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

ACFE CFEX. Certified Fraud Examiner (CFEX)

") ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

Looking for Fraud Through Rose-Colored Glasses

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Looking for Fraud Through Rose-Colored Glasses April 11, 2016 Presented by: James Mihills, CPA Disclaimer of Liability Weaver provides the information in this presentation for general guidance only, and

Insights Into Accounting Schemes and Scams

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

Insights Into Accounting Schemes and Scams HFMA Arkansas Chapter Spring Conference April 16, 2015 Presented by: Jeffrey Roberts, CPA, CFE, CFF BKD, LLP Forensics and Valuation Services @BKDForensics Agenda

Fraud Prevention for Nonprofits

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Good From The Inside Out. Saturday, April 8, 2017

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Chapter 2 Skimming 1

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Paul D. Vanchiere, MBA

Paul D. Vanchiere, MBA Theft-Proof Your Practice PEDIATRIC MANAGEMENT INSTITUTE Disclosures Pediatric Management Institute Consulting services for Pediatric Practices PhysicianIntelligence.com Business

Paul D. Vanchiere, MBA Theft-Proof Your Practice PEDIATRIC MANAGEMENT INSTITUTE Disclosures Pediatric Management Institute Consulting services for Pediatric Practices PhysicianIntelligence.com Business

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

Lecture Notes for How to Steal $500 Million

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Presented by: Michael Moreau, CFE, CIA, CFSA Manager, Credit Union Group Macpage LLC mpm@macpage.com 978-760-0195 Capability Diamond Capability can they do it? Necessary position and authority Sufficient

Protecting against check fraud perspectives and best practices

Protecting against check fraud perspectives and best practices Presenter Name Corp Title, Functional Title Date of presentation 2016 Wells Fargo Bank, N.A. All rights reserved. For public use. Agenda Check

Protecting against check fraud perspectives and best practices Presenter Name Corp Title, Functional Title Date of presentation 2016 Wells Fargo Bank, N.A. All rights reserved. For public use. Agenda Check

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

Grant Fraud. Leslie Les Hollie Assistant Inspector General For Investigations

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: C-06 Page: 1 of 5 General: The adequacy of internal control over cash receipts depends primarily on the business manager's ability to segregate the responsibilities for the performance of certain

No.: C-06 Page: 1 of 5 General: The adequacy of internal control over cash receipts depends primarily on the business manager's ability to segregate the responsibilities for the performance of certain

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

EXERCISES. The complete AICPA summary of Section 404 of Sarbanes-Oxley is as follows: Section 404: Management Assessment of Internal Controls.

EXERCISES Ex. 7 1 Section 404 requires management s internal control report to: (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures

EXERCISES Ex. 7 1 Section 404 requires management s internal control report to: (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

OCCUPATIONAL FRAUD 9/20/2018

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

Course 4200: Detecting and Investigating Financial Statement Fraud (2 days)

") Course 4200: Detecting and Investigating Financial Statement Fraud (2 days) Course introduction This two-day immersion course provides an in-depth examination of financial statement fraud how it is defined,

Course 4200: Detecting and Investigating Financial Statement Fraud (2 days) Course introduction This two-day immersion course provides an in-depth examination of financial statement fraud how it is defined,

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

Business Services Cash Handling: Department Manual

Business Services Cash Handling: Department Manual Deborah Michaels Associate Director, Business Services Cash Management Tina Cripe Administrative Program Assistant, Banking Specialist http://www.sou.edu/bus_serv/bursar/index.html

Business Services Cash Handling: Department Manual Deborah Michaels Associate Director, Business Services Cash Management Tina Cripe Administrative Program Assistant, Banking Specialist http://www.sou.edu/bus_serv/bursar/index.html

Safeguarding the Financial Assets of Your Church. Indiana Conference of the United Methodist Church

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

(385) ; TTY / fax. Scope and Methodology. May 22, 2018

; TTY / fax. Scope and Methodology. May 22, 2018") Salt Lake County Library Services 8030 South 1825 West West Jordan, UT 84088 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

Salt Lake County Library Services 8030 South 1825 West West Jordan, UT 84088 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

Improving the Effectiveness of Your Claims Auditing Process. How is cash usually stolen?

Improving the Effectiveness of Your Claims Auditing Process Jobriath Zebrowski, Associate Examiner Division of Local Government and School Accountability 1 How is cash usually stolen? Most cash is stolen

Improving the Effectiveness of Your Claims Auditing Process Jobriath Zebrowski, Associate Examiner Division of Local Government and School Accountability 1 How is cash usually stolen? Most cash is stolen

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

7/21/2015. July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT. Lessons from the Trenches. Angela Morelock Partner

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

Finacial Statement Fraud. Peter N Munachewa, CFE Risk Management Consultant

Finacial Statement Fraud Peter N Munachewa, CFE Risk Management Consultant What is FSF Falsification, alteration, or manipulation of material financial records, supporting documents, or business transactions

Finacial Statement Fraud Peter N Munachewa, CFE Risk Management Consultant What is FSF Falsification, alteration, or manipulation of material financial records, supporting documents, or business transactions

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

MIS 520 Data Analytics for IT Auditors

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

Delivering Confidence PAGE 1

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

Diocese of Oregon. The Episcopal Church in Western Oregon. Audit Program for Parishes and Missions February 26th, 2011

Diocese of Oregon The Episcopal Church in Western Oregon Audit Program for Parishes and Missions February 26th, 2011 HOW TO USE THIS MANUAL This booklet has been prepared for use as a manual. Please do

Diocese of Oregon The Episcopal Church in Western Oregon Audit Program for Parishes and Missions February 26th, 2011 HOW TO USE THIS MANUAL This booklet has been prepared for use as a manual. Please do

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

Accounting Solutions & Practices

Accounting Solutions & Practices Presenters Pastor Tina Egans and Chaundra Perry, CPA, CTP Scripture Focus 20For we are on our guard, intending that no one should find anything for which to blame us in

Accounting Solutions & Practices Presenters Pastor Tina Egans and Chaundra Perry, CPA, CTP Scripture Focus 20For we are on our guard, intending that no one should find anything for which to blame us in

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

1/18/2018. Fraud Prevention and Detection: Special Investigations, Information and Examples. Office of the State Auditor Role and Responsibility

Fraud Prevention and Detection: Special Investigations, Information and Examples 2018 MACO Annual Winter Conference Thursday, February 15, 2018 10:15-12:00 Mark Kerr, JD, CFE Special Investigations Director

Fraud Prevention and Detection: Special Investigations, Information and Examples 2018 MACO Annual Winter Conference Thursday, February 15, 2018 10:15-12:00 Mark Kerr, JD, CFE Special Investigations Director

BASIC POLICY STATEMENT

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

Employee Dishonesty Lessons Learned: Internal Controls

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

MIS 5208 Lecture 05 Recognizing the Symptoms of Fraud. Ed Ferrara, MSIA, CISSP Copyright 2018 Edward S.

MIS 5208 Lecture 05 Recognizing the Symptoms of Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu Learning Objectives Fraud symptoms (as we have discussed) help you recognize fraud. If fraud symptoms are

MIS 5208 Lecture 05 Recognizing the Symptoms of Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu Learning Objectives Fraud symptoms (as we have discussed) help you recognize fraud. If fraud symptoms are

A Model for Calculating User-Identity Trustworthiness in Online Transactions

A Model for Calculating User-Identity Trustworthiness in Online Transactions Brian A. Soeder Suzanne Barber 2015 UT CID Report #1505 This UT CID research was supported in part by the following organizations:

A Model for Calculating User-Identity Trustworthiness in Online Transactions Brian A. Soeder Suzanne Barber 2015 UT CID Report #1505 This UT CID research was supported in part by the following organizations:

Fraud: How to Get Your District Free Publicity

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

INTERSERVE PLC POLICY ON FRAUD

INTERSERVE PLC POLICY ON FRAUD Interserve Plc ( The Company ) is committed to the highest standards of personal and corporate behaviour. We will not tolerate any incidence of fraud committed by workers

INTERSERVE PLC POLICY ON FRAUD Interserve Plc ( The Company ) is committed to the highest standards of personal and corporate behaviour. We will not tolerate any incidence of fraud committed by workers

Internal Bank Fraud Schemes & Scams in an Economic Downturn. Fictitious Loans. Bank Fraud Investigations. Tracking spreadsheet Affidavit 1 Affidavit 2

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

acumen Internal Bank Fraud Schemes & Scams in an Economic Downturn Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant insight ideas attention reach expertise depth agility

Everyone (no matter the size) can have internal controls. By Peter S. Olsen, CPA

can have internal controls. By Peter S. Olsen, CPA") Everyone (no matter the size) can have internal controls By Peter S. Olsen, CPA Introduction This is me.. Agenda 1. Define small nonprofits 2. Detective vs. Preventive controls 3. Discuss the most important

Everyone (no matter the size) can have internal controls By Peter S. Olsen, CPA Introduction This is me.. Agenda 1. Define small nonprofits 2. Detective vs. Preventive controls 3. Discuss the most important

Chart 1 How Fraudulently Used Consumer Information is Obtained M A Y

M A Y 2 0 0 6 Payments Fraud: Consumer Considerations by Terri Bradford, Payments System Research Specialist, Federal Reserve Bank of Kansas City, and Bruce Cundiff, Research Analyst, Javelin Strategy

M A Y 2 0 0 6 Payments Fraud: Consumer Considerations by Terri Bradford, Payments System Research Specialist, Federal Reserve Bank of Kansas City, and Bruce Cundiff, Research Analyst, Javelin Strategy

Rockdale ISD Accounts Payable Procedures

Accounts payable checks should be processed on a weekly basis for release by Thursday morning, or earlier dependent upon work schedules or holidays. Cut-off date for weekly processing is noon on Tuesday.

Accounts payable checks should be processed on a weekly basis for release by Thursday morning, or earlier dependent upon work schedules or holidays. Cut-off date for weekly processing is noon on Tuesday.

Watching the Vault: Employee Dishonesty

Watching the Vault: Employee Dishonesty Managing your most pressing risks NCOFCU 2016 Conference CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group,

Watching the Vault: Employee Dishonesty Managing your most pressing risks NCOFCU 2016 Conference CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group,

Banking Basics 101. How to Manage Your Finances and Still Have Money Left Over For a Night Out. Course objectives learn about:

Banking Basics 101 Course objectives learn about: Using a checking account Various types of payment vehicles Benefits of a savings account How to Manage Your Finances and Still Have Money Left Over For

Banking Basics 101 Course objectives learn about: Using a checking account Various types of payment vehicles Benefits of a savings account How to Manage Your Finances and Still Have Money Left Over For

Financial Transactions and Fraud Schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Revision date: September 21, 2018 Responsible Agent(s): Controller and Treasurer Original effective date: Scope: All Campuses

: Controller and Treasurer Original effective date: Scope: All Campuses") Name of Policy: Receipt of cash Policy Number: 3364-40-22 Approving Officer: Executive Vice President for Finance & Administration/Chief Financial Officer (CFO) or equivalent position Revision date: September

Name of Policy: Receipt of cash Policy Number: 3364-40-22 Approving Officer: Executive Vice President for Finance & Administration/Chief Financial Officer (CFO) or equivalent position Revision date: September

Mitigating Fraud. June 22, Sept. 21, 2014

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Weber State University. Cash Handling Training

Weber State University Cash Handling Training Cash Handling It s your responsibility Whether you take in a lot of money or you collect pennies ..it is important to maintain good cash handling procedures:

Weber State University Cash Handling Training Cash Handling It s your responsibility Whether you take in a lot of money or you collect pennies ..it is important to maintain good cash handling procedures:

Fraud Risk Assessment Awareness in Employee Benefit Plans

Fraud Risk Assessment Awareness in Employee Benefit Plans Tyler Geiman, CPA, CFE, CFF Novak Francella, LLC Phone: (443) 832-4009 Fax: (443) 393-0323 Web: www.novakfrancella.com Fraud is any intentional

Fraud Risk Assessment Awareness in Employee Benefit Plans Tyler Geiman, CPA, CFE, CFF Novak Francella, LLC Phone: (443) 832-4009 Fax: (443) 393-0323 Web: www.novakfrancella.com Fraud is any intentional

Lackland ISD Accounts Payable Procedures

Accounts payable checks should be processed on a weekly basis for release by Friday morning, or earlier dependent upon work schedules or holidays. General Instructions: All invoices shall be entered separately

Accounts payable checks should be processed on a weekly basis for release by Friday morning, or earlier dependent upon work schedules or holidays. General Instructions: All invoices shall be entered separately

Executive Protection Portfolio SM Crime Coverage Renewal Application

BY COMPLETING THIS APPLICATION YOU ARE APPLYING FOR COVERAGE WITH EXECUTIVE RISK INDEMNITY INC. (THE COMPANY ) NOTICE: THE COVERAGE AFFORDED UNDER THIS COVERAGE SECTION DIFFERS IN SOME RESPECTS FROM THAT

BY COMPLETING THIS APPLICATION YOU ARE APPLYING FOR COVERAGE WITH EXECUTIVE RISK INDEMNITY INC. (THE COMPANY ) NOTICE: THE COVERAGE AFFORDED UNDER THIS COVERAGE SECTION DIFFERS IN SOME RESPECTS FROM THAT

Financial Policies and Procedures

1.0 Cash Receipts Each day that the Library is open and there is mail delivery, the Library Director or the Circulation Manager check the mail. Checks and credit card payments are either given directly

1.0 Cash Receipts Each day that the Library is open and there is mail delivery, the Library Director or the Circulation Manager check the mail. Checks and credit card payments are either given directly

WASATCH FRONT REGIONAL COUNCIL/WASATCH FRONT ECONOMIC DEVELOPMENT DISTRICT ACCOUNTING AND ADMINISTRATIVE POLICY 10/26/2017 (revised)

") WASATCH FRONT REGIONAL COUNCIL/WASATCH FRONT ECONOMIC DEVELOPMENT DISTRICT ACCOUNTING AND ADMINISTRATIVE POLICY 10/26/2017 (revised) DESIGNATION OF THE TREASURER AND CLERK In compliance with Utah Code

WASATCH FRONT REGIONAL COUNCIL/WASATCH FRONT ECONOMIC DEVELOPMENT DISTRICT ACCOUNTING AND ADMINISTRATIVE POLICY 10/26/2017 (revised) DESIGNATION OF THE TREASURER AND CLERK In compliance with Utah Code

Parish Financial System

Parish Financial System 1. Financial Objectives A. The parish must establish a financial system that will accomplish the following objectives: 1) Identify, record and report all transactions of the parish

Parish Financial System 1. Financial Objectives A. The parish must establish a financial system that will accomplish the following objectives: 1) Identify, record and report all transactions of the parish

Crime Coverage Section Application (Large Public Company > $1B revenues)

") Crime Coverage Section Application (Large Public Company > $1B revenues) BY COMPLETING THIS CRIME APPLICATION THE APPLICANT IS APPLYING FOR COVERAGE WITH CHUBB INSURANCE COMPANY OF CANADA (THE COMPANY

Crime Coverage Section Application (Large Public Company > $1B revenues) BY COMPLETING THIS CRIME APPLICATION THE APPLICANT IS APPLYING FOR COVERAGE WITH CHUBB INSURANCE COMPANY OF CANADA (THE COMPANY

COVERAGE FRAUD IN EMPLOYEE BENEFIT PLANS 5/15/2014. Where employee benefit fraud is likely. Internal controls that help prevent fraud

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

Defending Against the Latest Fraud Trends

Defending Against the Latest Fraud Trends Joni Lovingood, CRM, CFE Corporate Property & Casualty Sales Specialist CUNA Mutual Group joni.lovingood@cunamutual.com CUNA Mutual Group Proprietary Reproduction,

Defending Against the Latest Fraud Trends Joni Lovingood, CRM, CFE Corporate Property & Casualty Sales Specialist CUNA Mutual Group joni.lovingood@cunamutual.com CUNA Mutual Group Proprietary Reproduction,

Internal Controls: Best Practices

Internal Controls: Best Practices Christie Rice Diocese of Des Moines What are internal controls? Systems of checks and balances: Detect errors Discourage/reveal fraud Why do we need them? Maintain accurate

Internal Controls: Best Practices Christie Rice Diocese of Des Moines What are internal controls? Systems of checks and balances: Detect errors Discourage/reveal fraud Why do we need them? Maintain accurate

Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags

Forensic Services Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags 2 What % of revenues are lost to fraud? 5% Source: 2016 ACFE Report to the Nations 3 Has your

Forensic Services Financial Crime - Early Warning Signs the role of Internal Audit in recognizing red flags 2 What % of revenues are lost to fraud? 5% Source: 2016 ACFE Report to the Nations 3 Has your

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

Credit Card Handling Security Standards

Credit Card Handling Security Standards Overview This document is intended to provide guidance regarding the processing of charges and credits on credit and/or debit cards. These standards are intended

Credit Card Handling Security Standards Overview This document is intended to provide guidance regarding the processing of charges and credits on credit and/or debit cards. These standards are intended

The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

City of Lawrence, Kansas. Purchasing Card Guidelines

City of Lawrence, Kansas Purchasing Card Guidelines Updated 2011 Table of Contents OVERVIEW... 1 REQUESTING YOUR PURCHASING CARD... 2 RESPONSIBILITIES... 2 CARDHOLDER... 2 DEPARTMENT COORDINATORS... 4

City of Lawrence, Kansas Purchasing Card Guidelines Updated 2011 Table of Contents OVERVIEW... 1 REQUESTING YOUR PURCHASING CARD... 2 RESPONSIBILITIES... 2 CARDHOLDER... 2 DEPARTMENT COORDINATORS... 4

CASH FUND TRAINING. TTUHSC Accounting Services

TTUHSC Accounting Services Updated May 2003 Categories of Cash Funds Change Funds Maintained in currency and coins Used strictly for making change Petty Cash Funds Usually maintained in a bank account

TTUHSC Accounting Services Updated May 2003 Categories of Cash Funds Change Funds Maintained in currency and coins Used strictly for making change Petty Cash Funds Usually maintained in a bank account

FRAUD EXAMINERS MANUAL

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

Employee Benefit Plan Fraud Examples

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

Tax-Related Identity Theft

Tax-Related Identity Theft Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 (214) 984-3410 Jason@FreemanLaw-Pllc.com www.freemanlaw-pllc.com Copyright Freeman

Tax-Related Identity Theft Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 (214) 984-3410 Jason@FreemanLaw-Pllc.com www.freemanlaw-pllc.com Copyright Freeman

Jason B. Freeman, J.D., CPA

Tax Related Identity Theft Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 (214) 984 3410 Jason@FreemanLaw Pllc.com www.freemanlaw Pllc.com Copyright Freeman

Tax Related Identity Theft Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 (214) 984 3410 Jason@FreemanLaw Pllc.com www.freemanlaw Pllc.com Copyright Freeman

Fiscal Policies and Procedures for County Councils. Responsibilities

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

IIA Fraud Conference. Case studies from recent investigations. 8 April 2015

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

To establish NUAMES policy and procedure governing the initiation, authorization, and review of all expenditures of the school.

NUAMES Cash Disbursement Policy Approved: 23 October 2013 1. PURPOSE AND PHILOSOPHY To establish NUAMES policy and procedure governing the initiation, authorization, and review of all expenditures of the

NUAMES Cash Disbursement Policy Approved: 23 October 2013 1. PURPOSE AND PHILOSOPHY To establish NUAMES policy and procedure governing the initiation, authorization, and review of all expenditures of the

How to Prevent and Detect Fraud: Implementing Internal Controls

How to Prevent and Detect Fraud: Implementing Internal Controls League of Minnesota Cities 2018 Clerks Orientation Conference June 21, 2018 St. Cloud, Minnesota Mark F. Kerr, JD, CFE Special Investigations

How to Prevent and Detect Fraud: Implementing Internal Controls League of Minnesota Cities 2018 Clerks Orientation Conference June 21, 2018 St. Cloud, Minnesota Mark F. Kerr, JD, CFE Special Investigations