Accounting Summative: Journalopoly. Mrs. Van Dam

|

|

|

- Raymond Hopkins

- 5 years ago

- Views:

Transcription

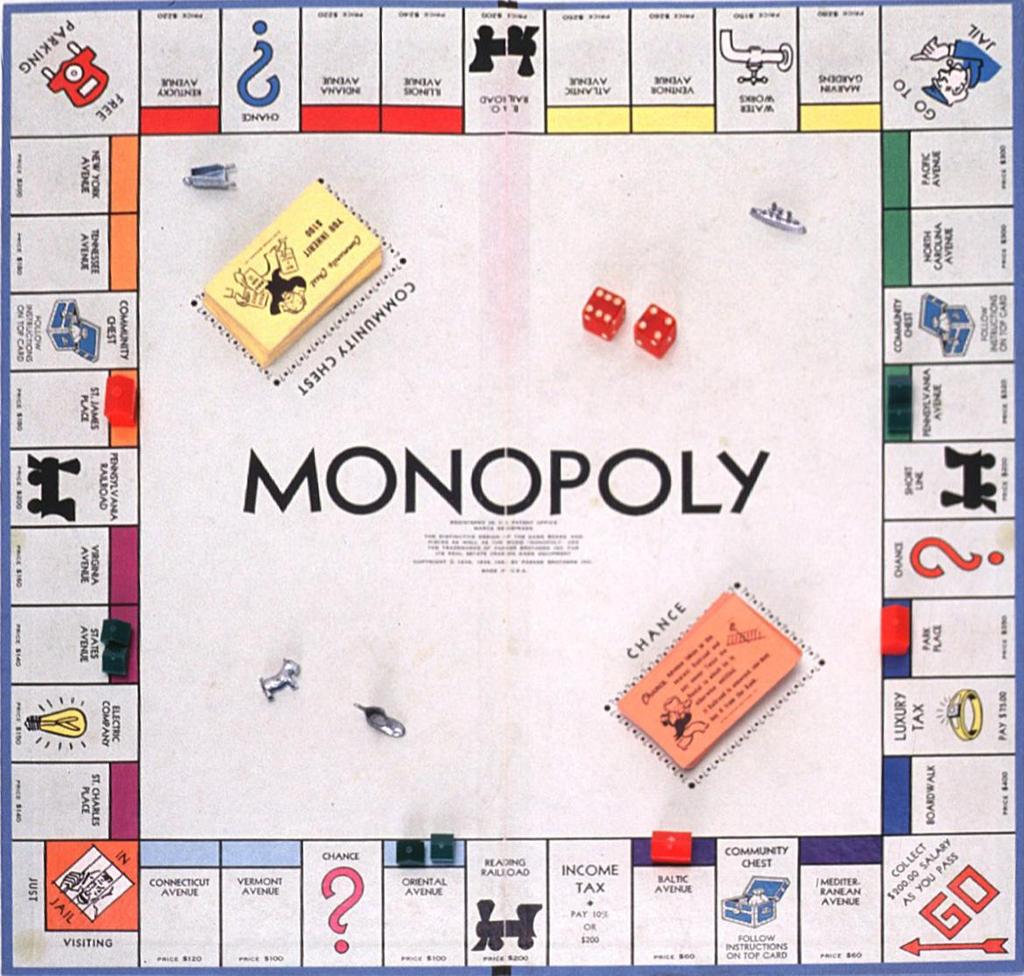

1 Accounting Summative: Journalopoly Mrs. Van Dam

2 Review Rules, Requirements & Materials Let s read through all of this: Objectives Rules Procedures Let s see what Materials are in the packet Let s see what the summative requirements are! (this is what must be handed in!) Now let s circle back

Students should be able to maintain a set of accounting records in operating a partnership Students should be able to complete the accounting cycle for a service business operating as a partnership")

3 Objectives Students should be able to perform procedures necessary in setting up a partnership business (i.e. choosing a name, creating a partnership agreement, setting up accounts, etc.) Students should be able to maintain a set of accounting records in operating a partnership Students should be able to complete the accounting cycle for a service business operating as a partnership Students should be able to work effectively with another member when running a partnership business.

4 Playing the Game!

in capital.")

5 Playing the game: Beginning The students in the class will divide up into teams of two or three (only if needed) to create a partnership. Each partner starts the game with $1,500 each (or if 3 partners then $1,000 each) in capital. Bank is debited $3,000 In the synoptic journal: Roll the dice, move your token (one token per team)

6 Transactions Type: Property Purchase You land on Connecticut and decide to buy Property 120 Bank 120

7 Transactions Type: Pay Rent You land on St James and have to pay rent Include the name of the property in your journal Rent Expense 14 Bank 14

8 Transactions Type: Getting out of Jail You must pay to get out of Jail! Drawings 50 Bank 50

9 Transactions Type: Special Luxury Tax and Income Tax Drawings, Van Dam 75 Bank 75 Free Parking, or Pass Go Bank 200 Capital, Van Dam 200

10 Transactions Type: Houses and Hotels Can purchase a house anytime Include property name in particulars Each team must purchase a minimum of 3 houses Building 200 Bank 200 Purchase a hotel after 4 houses Include property name in particulars Building 200 Bank 200

250 Bank 300 Property 250 Gain on sale/trade")

11 Transactions Type: Trading properties Can only initiate a trade during your turn Both parties record the transaction Bank 200 Loss on Sale/Trade 50 Property (at cost) 250 Bank 300 Property 250 Gain on sale/trade 50

12 Transactions Type: Chance & Community Chest (CC) Pay Chance/CC Expense 200 Bank 200 Earn Bank 200 Chance/CC Revenue 200

13 Transactions Type: Audited Your records will be audited, if they are NOT in order you will be fined $200 (a debit to the individual partners drawings acct) If they ARE in order, $100 Bonus will be awarded (a credit to the individual partner s capital acct) Fined! Drawings 200 Bank 200 Bonus! Bank 100 Capital 100

14 Finishing Each Day! To be completed 10 minutes before class end.

15 Day s End: Daily Cash Count Count Cash, record your cash amount Record where you & your opponents are on the board Opposing team member must validate cash count Mrs. Van Dam MUST SIGN your Daily Cash Count Sheet

16 Procedures: Each day is one month Day 1 ends January 31 Day 2 ends February 28 Day 3 ends March 31 The partner who journalizes during the day will post all transactions to the general ledger Each partner must complete this once during the activity The posting must be completed before the next playing day.

17 Procedures Continued If the daily cash count sheet does not agree with the bank account in the general ledger, then a correcting entry must be made. if cash is SHORT, you lost money somewhere. This is like an expense and will be recoded as a debit If cash is OVER, you have gained money somewhere. This is like a revenue and will be recoded as a credit. SHORT! Cash short & over 135 Bank 135 OVER! Bank 62 Cash short & over 62 * You MUST properly forward balances to new accounts

18 Your Deliverables!

19 Summative Requirements Title Page Name of company (think something Real Estate Company) Partnership agreement (see page & next slide) Daily Cash Count Sheets, Property check list, Synoptic journal, General Ledger Trial March 31, 2017 Schedule of Properties listed alphabetically + real estate portfolio with cost = property ledger control 8 Column worksheet, adjustments as follows: Building depreciate at 15% Interest on bank Loans Interest expense is calculated at 7% Interest on Mortgages Interest expense is calculated at 5% Partnership Financial Stmts Income statements (service firm) Statement of Distribution of Net Income* Statement of Changes in Partner Equity* *partnership notes Classified Balance Sheet, incl Partners Equity Journalize & post adjusting entries Journalize & post closing entries Revenue to Income Statement Summary Expenses to Income Statement Summary I/S to Capital Drawing to Capital Post-Closing Trial Balance Consider Neatness, Use Excel

20 Partnership Agreement Firm s name and address Partners names, addresses & phone # s The date on which the partnership is formed January 12, 2017 Nature of the partnership business ie Real Estate Company Duties of the individual partners and the amount of time that they agree to devote to business activities Be specific here, suggest creating a table Duties Partner 1 Partner 2 1 Title page 2 Partner agreement 3 Journal Day 1 4 Post Day 1 5 Journal Day 2 Amount of capital to be contributed by each of the partners $1500 Salaries (if any) to be paid to each of the partners ie $100 Rate of interest (if any) to be paid on the partners capital account balances ie 2% How net income or net loss will be shared ie a fixed ratio 1:1 The procedure to be followed in case the partnership ends suddenly because of the death or bankruptcy of a partner liquidate assets, pay off creditors, divide remaining income An exit procedure for any partner wanting to leave the partnership Both partners must sign and date the agreement!!

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Instructions for Accounting

Instructions for Accounting Please read these instructions after playing Monopoly but before doing the accounting. Students that don't read these instructions make mistakes and take longer to complete

Instructions for Accounting Please read these instructions after playing Monopoly but before doing the accounting. Students that don't read these instructions make mistakes and take longer to complete

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Chapter 20 Notes Uncollectible Accounts Expense

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY. Y. Chang Company COVER SHEET

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

ACCT 652 Accounting. Review of last week. Review of last week (2) 12/29/15. Week 2 Charts of accounts, Journals, T-accounts, and special journals

12/29/15. Week 2 Charts of accounts, Journals, T-accounts, and special journals") ACCT 652 Accounting Week 2 Charts of accounts, Journals, T-accounts, and special journals Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of

ACCT 652 Accounting Week 2 Charts of accounts, Journals, T-accounts, and special journals Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Accounting COURSE SYLLABUS Course Description: Course Objectives:

Accounting COURSE SYLLABUS Course Description: The objective of this class is to introduce Accounting and the Accounting equation. The students will be able to Analyze Business source documents, Journalize

Accounting COURSE SYLLABUS Course Description: The objective of this class is to introduce Accounting and the Accounting equation. The students will be able to Analyze Business source documents, Journalize

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

RECORDING TRANSACTIONS THROUGH DEBITS AND CREDITS

RECORDING TRANSACTIONS THROUGH DEBITS AND CREDITS The process of recording the transaction in the books of accounts is called book keeping. The process ends with the preparation of financial statements

RECORDING TRANSACTIONS THROUGH DEBITS AND CREDITS The process of recording the transaction in the books of accounts is called book keeping. The process ends with the preparation of financial statements

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Examination Booklet Version 1. Bookkeeping

Examination Booklet Version 1 Bookkeeping The Accounting Equation When you feel confident that you have mastered the material in The Accounting Equation, go to and submit your answers online EXAMINATION

Examination Booklet Version 1 Bookkeeping The Accounting Equation When you feel confident that you have mastered the material in The Accounting Equation, go to and submit your answers online EXAMINATION

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

AccountAbility Edutools, USA, 2013, All Rights Reserved

(INX) LEDGER MANIA STUDENT INSTRUCTIONS Ledger Mania is an interactive classroom activity used to demonstrate the accounting cycle of a sole proprietorship or corporation. Students will physically record

(INX) LEDGER MANIA STUDENT INSTRUCTIONS Ledger Mania is an interactive classroom activity used to demonstrate the accounting cycle of a sole proprietorship or corporation. Students will physically record

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

Trial Balance. Format of Trial Balance. The under mention points may be noted for preparing a trial balance.

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Assessment schedule 2015 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2015 page 1 of 7 Assessment schedule 2015 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Evidence Question One (a) Depreciation

NCEA Level 2 Accounting (91176) 2015 page 1 of 7 Assessment schedule 2015 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Evidence Question One (a) Depreciation

Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

Activity 1: Transactions

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

Exercise 2-1. Exercise 2-2. Exercise 2-3. Name. = Liabilitiy Acounts + Debit Credit. Asset Acounts. Stockholders Equity Acounts Debit. Credit.

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Posting from a General Journal to a General Ledger. Tuesday, October 26, :48:47 PM ET

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Accounting. Chapter 6

Accounting Chapter 6 Aim: What are four source documents and when would they be used? Do Now: Take a Do Now slip. Answer: Why do people use journals? Have you ever kept a daily journal of the things that

Accounting Chapter 6 Aim: What are four source documents and when would they be used? Do Now: Take a Do Now slip. Answer: Why do people use journals? Have you ever kept a daily journal of the things that

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

LESSON Recording A Payroll. CENTURY 21 ACCOUNTING Thomson/South-Western

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

FINANCIAL STATEMENTS: INCOME STATEMENT & ASSET DISPOSAL 08 AUGUST 2013

FINANCIAL STATEMENTS: INCOME STATEMENT & ASSET DISPOSAL 08 AUGUST 2013 Lesson Description In this lesson we: Focus on income statement adjustments and calculating profit/loss on sale of asset. Questions

FINANCIAL STATEMENTS: INCOME STATEMENT & ASSET DISPOSAL 08 AUGUST 2013 Lesson Description In this lesson we: Focus on income statement adjustments and calculating profit/loss on sale of asset. Questions

ACCT Introduction to Accounting Chapter 6 - Closing Entries and the Post Closing Trial Balance Prof. Johnson

ACCT 100 - Introduction to Accounting Chapter 6 - Closing Entries and the Post Closing Trial Balance Prof. Johnson Purpose: The purpose of this handout is to summarize key concepts of Chapter 6. This represents

ACCT 100 - Introduction to Accounting Chapter 6 - Closing Entries and the Post Closing Trial Balance Prof. Johnson Purpose: The purpose of this handout is to summarize key concepts of Chapter 6. This represents

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Every data set has an average and a standard deviation, given by the following formulas,

Discrete Data Sets A data set is any collection of data. For example, the set of test scores on the class s first test would comprise a data set. If we collect a sample from the population we are interested

Discrete Data Sets A data set is any collection of data. For example, the set of test scores on the class s first test would comprise a data set. If we collect a sample from the population we are interested

Ledger and Trial Balance

Ledger and Trial Ledger is a book where all types of accounts are maintained and each account contains a summarized and classified record of all business transactions. Why is the Ledger necessary in presence

Ledger and Trial Ledger is a book where all types of accounts are maintained and each account contains a summarized and classified record of all business transactions. Why is the Ledger necessary in presence

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Accounting 1. Lesson Plan. Name: Terry Wilhelmi Day/Date:

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Chapter 4. Posting to a General Ledger

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything!

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

Problems: Set C. 8 chapter 3 The Accounting Information System

8 chapter 3 The Accounting Information System compute net income. (b) Net income $4,910 prepare financial statements. (a) Cash $12,680 Problems: Set C P3-1C New Dawn Window Washing Inc. was started on

8 chapter 3 The Accounting Information System compute net income. (b) Net income $4,910 prepare financial statements. (a) Cash $12,680 Problems: Set C P3-1C New Dawn Window Washing Inc. was started on

GRADE 11 TEST ON ADJUSTMENTS FOR MORE TESTS AND TASKS REFER TO THE GRADE 11 STUDY GUIDE

GRADE 11 TEST ON ADJUSTMENTS FOR MORE TESTS AND TASKS REFER TO THE GRADE 11 STUDY GUIDE FINANCIAL STATEMENTS (80 marks; 48 minutes) You are provided with information relating to BB Spaza, which is owned

GRADE 11 TEST ON ADJUSTMENTS FOR MORE TESTS AND TASKS REFER TO THE GRADE 11 STUDY GUIDE FINANCIAL STATEMENTS (80 marks; 48 minutes) You are provided with information relating to BB Spaza, which is owned

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Practice exercise solutions

Bookkeeping to Trial Balance Practice exercise solutions Learning Module: An introduction to business, bookkeeping and accounting Practice exercise 1a (ii) (iii) (iv) (v) (vi) (vii) (viii) (ix) (x) D M

Bookkeeping to Trial Balance Practice exercise solutions Learning Module: An introduction to business, bookkeeping and accounting Practice exercise 1a (ii) (iii) (iv) (v) (vi) (vii) (viii) (ix) (x) D M

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

FUNDAMENTAL ACCOUNTING (01) Regional 2013

Regional 2013") Page 1 of 11 Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Secondary Regional 2013 Multiple Choice Account Identification Problem 1 Journalizing Problem 2 Income Statement Problem 3 Closing Entries

Page 1 of 11 Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Secondary Regional 2013 Multiple Choice Account Identification Problem 1 Journalizing Problem 2 Income Statement Problem 3 Closing Entries

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Lesson FA Financial Accounting Fundamentals - Closing Entries and Post-Closing Trial Balance Part 1

Lesson FA-10-040-01 Financial Accounting Fundamentals - Closing Entries and Post-Closing Trial Balance Part 1 This workbook contains notes and worksheets to accompany the corresponding video lesson available

Lesson FA-10-040-01 Financial Accounting Fundamentals - Closing Entries and Post-Closing Trial Balance Part 1 This workbook contains notes and worksheets to accompany the corresponding video lesson available

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50

![NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50](/thumbs/95/123010063.jpg "NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50") NC 824 First Year B. C. A. Examination April / May 2003 Financial Accounting & Management Seat No. Time : 3 Hours] [Total Marks : 50 Instructions : (1) Figures to the right indicate marks. (2) Show calculations

NC 824 First Year B. C. A. Examination April / May 2003 Financial Accounting & Management Seat No. Time : 3 Hours] [Total Marks : 50 Instructions : (1) Figures to the right indicate marks. (2) Show calculations

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions. Chapter Overview. Learning Objectives

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Contents: Interview Summary...2. Assignment Text excerpt for Assignment Syllabus...11

College: Great Bay Community College Course: Introduction Dan Murphy Text: Fundamental Accounting Principles, 19 th Ed; Wild, Shaw, Chiappetta Contents: Interview Summary...2 Assignment 1...3 Text excerpt

College: Great Bay Community College Course: Introduction Dan Murphy Text: Fundamental Accounting Principles, 19 th Ed; Wild, Shaw, Chiappetta Contents: Interview Summary...2 Assignment 1...3 Text excerpt

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Money Management Financial Survivor: Understanding Credit and Banking

Money Management Financial Survivor: Understanding Credit and Banking In this workshop, youth will learn about credit, the importance of maintaining good credit, and how to access their credit report.

Money Management Financial Survivor: Understanding Credit and Banking In this workshop, youth will learn about credit, the importance of maintaining good credit, and how to access their credit report.

Name: Date: Period: Standard 2: Students will list and identify characteristics of the three basic accounting equation elements.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

LEDGER MANIA HOSPITALITY VERSION

LEDGER MANIA HOSPITALITY VERSION Ledger Mania is an interactive classroom activity used to demonstrate the accounting cycle of a hospitality company. Students will physically record transactions, post

LEDGER MANIA HOSPITALITY VERSION Ledger Mania is an interactive classroom activity used to demonstrate the accounting cycle of a hospitality company. Students will physically record transactions, post

Accounting 1. Lesson Plan. Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACCN1 (JUN09ACCN101) General Certificate of Education Advanced Subsidiary Examination June Introduction to Financial Accounting TOTAL

General Certificate of Education Advanced Subsidiary Examination June Introduction to Financial Accounting TOTAL") Centre Number Surname Candidate Number For Examiner s Use Other Names Candidate Signature Examiner s Initials Accounting General Certificate of Education Advanced Subsidiary Examination June 2009 ACCN1

Centre Number Surname Candidate Number For Examiner s Use Other Names Candidate Signature Examiner s Initials Accounting General Certificate of Education Advanced Subsidiary Examination June 2009 ACCN1

The General Ledger. The 4 th step of the accounting cycle is to post to the ledger.

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Completing the Accounting Cycle

4 Completing the Accounting Cycle 4-1 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a

4 Completing the Accounting Cycle 4-1 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a

COMSATS INSTITUTE OF INFORMATION TECHNOLOGY, ABBOTTABAD

COMSATS INSTITUTE OF INFORMATION TECHNOLOGY, ABBOTTABAD Registration # Signature Quiz # 2 and 3 Financial MBA 1(3.5) Instructions: 1. Borrowing of Calculator, Ruler etc. is not allowed 2. Switch off Mobile

COMSATS INSTITUTE OF INFORMATION TECHNOLOGY, ABBOTTABAD Registration # Signature Quiz # 2 and 3 Financial MBA 1(3.5) Instructions: 1. Borrowing of Calculator, Ruler etc. is not allowed 2. Switch off Mobile

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

MCA (Sem-1) Theory Examination, Accounting and Financial Management. Section - A

Theory Examination, Accounting and Financial Management. Section - A") MCA (Sem-1) Theory Examination, 2016-17 Accounting and Financial Management Section - A a) Ratio analysis is used to evaluate various aspects of a company's operating and financial performance such as

MCA (Sem-1) Theory Examination, 2016-17 Accounting and Financial Management Section - A a) Ratio analysis is used to evaluate various aspects of a company's operating and financial performance such as

GAUTENG DEPARTMENT OF EDUCATION PROVINCIAL EXAMINATION JUNE 2016 GRADE

GAUTENG DEPARTMENT OF EDUCATION PROVINCIAL EXAMINATION JUNE 2016 GRADE 11 ACCOUNTING TIME: 180 minutes MARKS: 300 14 pages ACCOUNTING GRADE 11 2 GAUTENG DEPARTMENT OF EDUCATION PROVINCIAL EXAMINATION ACCOUNTING

GAUTENG DEPARTMENT OF EDUCATION PROVINCIAL EXAMINATION JUNE 2016 GRADE 11 ACCOUNTING TIME: 180 minutes MARKS: 300 14 pages ACCOUNTING GRADE 11 2 GAUTENG DEPARTMENT OF EDUCATION PROVINCIAL EXAMINATION ACCOUNTING

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Index. Assets (continued) scrapping or disposal trading-in Auditing Profession Act 26 of

scrapping or disposal trading-in Auditing Profession Act 26 of") Index A Accounts balancing... 61 incomplete records... 369 Accounting balancing an account... 61 basic accounting equation... 27 cycle... 130 definition... 4, 13 developments... 5 domains... 14 function...

Index A Accounts balancing... 61 incomplete records... 369 Accounting balancing an account... 61 basic accounting equation... 27 cycle... 130 definition... 4, 13 developments... 5 domains... 14 function...

Debit and Credit Rules Module 2 part I. T- Accounts Assets = Liabilities + OE. T- Accounts: Basic Patterns A = L + OE

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

XI - ACCOUNTING REGULAR / PRIVATE

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

CHAPTER 7. Internal Control and Cash. Chapter Overview

CHAPTER 7 Internal Control and Cash Chapter Overview Chapter 7 discusses the purposes and characteristics of an effective system of internal control. The text describes four objectives that a company hopes

CHAPTER 7 Internal Control and Cash Chapter Overview Chapter 7 discusses the purposes and characteristics of an effective system of internal control. The text describes four objectives that a company hopes

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

ACCOUNTING 201. PRACTICE MIDTERM - (Covering Chapters 1-5)

") Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting