The General Journal and the General Ledger

|

|

|

- Jayson Porter

- 5 years ago

- Views:

Transcription

1 chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1

2 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2

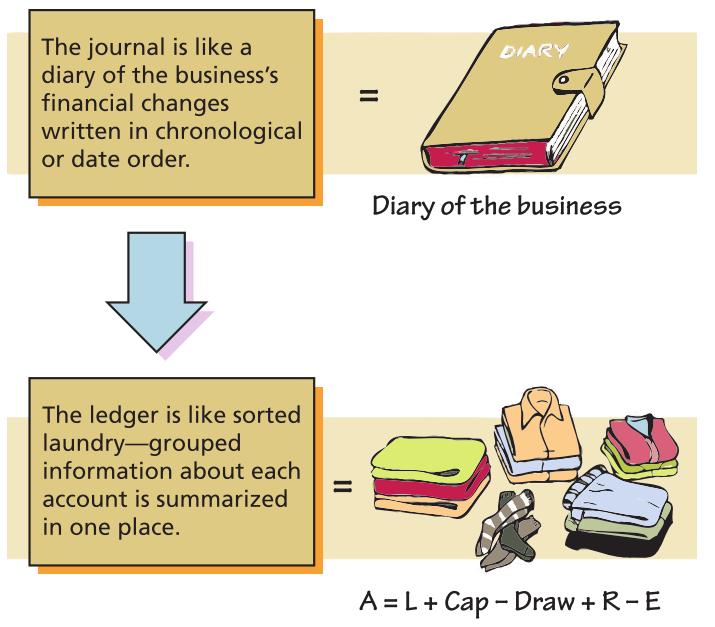

3 The General Journal The process of recording business transactions in a journal is called journalizing. In the journal, both the debits and the credits of the entire transaction are recorded in one place. A journal is called a book of original entry because the first place an entry is recorded is in the journal. A journal is a book in which business transactions are recorded as they happen. Information about transactions come from source documents that furnish proof that a transaction has taken place. The basic journal form is the two-column general journal. 3 3

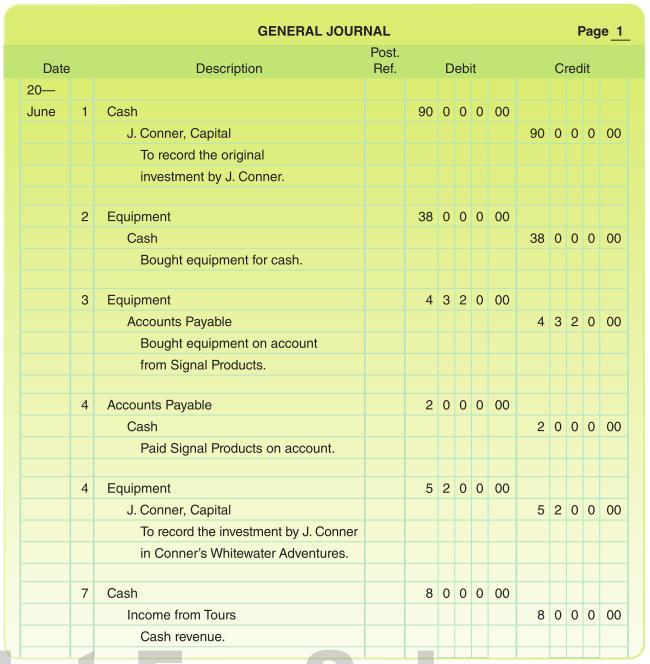

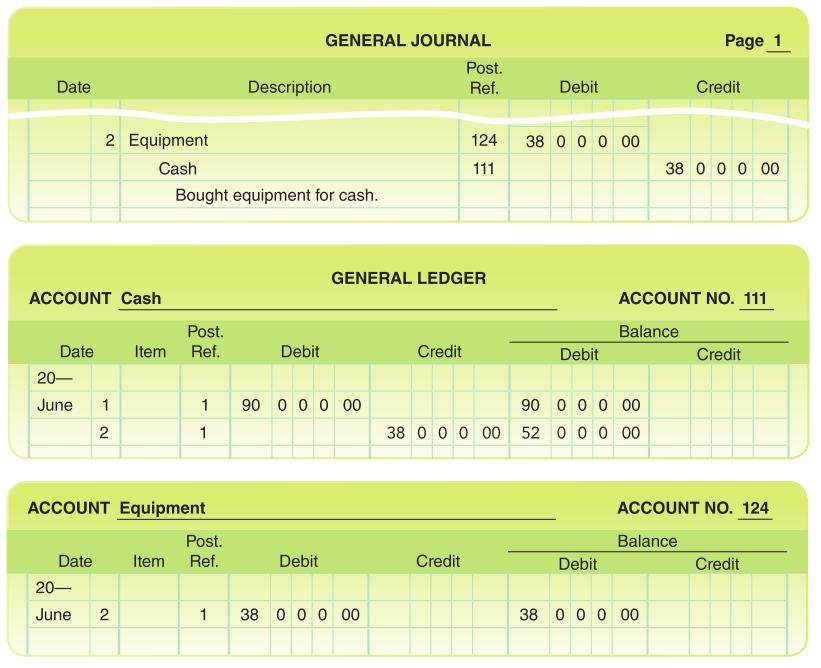

4 Transaction (a) June1: J. Conner deposited $90,000 in a bank account in the name of Conner s Whitewater Adventures. 3 4

5 Decide which accounts should be debited and credited Step 1: Decide which accounts are involved. Step 2: Classify the accounts involved. Step 3: Decide if the accounts involved are increased or decreased. Step 4: Write the transactions as a debit to one account (or accounts) and a credit to another account (or accounts). Step 5: Check to see if the equation is in balance. 3 5

6 Analyze the Transaction Using the T- Account Approach i n c r e a s e Cash increases, so it is debited i n c r e a s e J. Conner, Capital increases, so it is credited 3 6

7 Journal Entry 2: Date 3: Debit account title 3: Debit amount 1: Page number 4: Indent credit account title 5: Indent further explanation 4: Credit amount 3 7

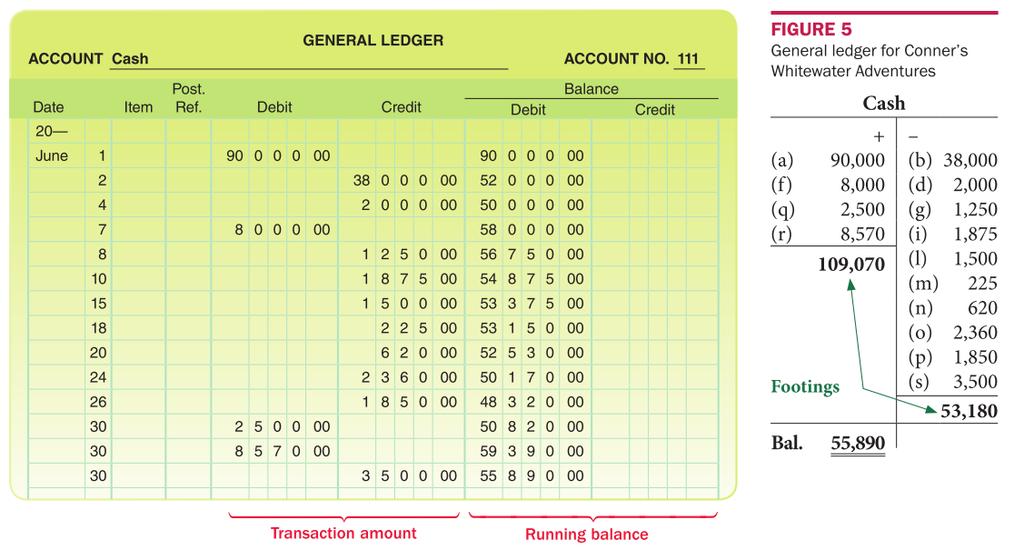

8 Transaction (b) June 2: Conner s Whitewater Adventures bought equipment, paying cash, $38,000. Skip a line between entries in your homework 3 8

9 The Cost Principle When a business buys an asset, the asset should be recorded at the actual cost (the agreed amount of a transaction). This is called the cost principle. Assume in Transaction (c) that Signal Products had been asking $7,500 for the equipment. The cost of the equipment to Conner s Whitewater Adventures is $4,320, so that is the amount recorded. 3 9

10 Transaction (c) June 3: Conner s Whitewater Adventures bought equipment on account from Signal Products, $4,320. Note that the month and year are not repeated unless they change or a new journal page begins 3 10

11 Transaction (d) June 4: Conner s Whitewater Adventures paid Signal Products, a creditor, on account,$2,

12 3 12

13 3 13

14 3 14

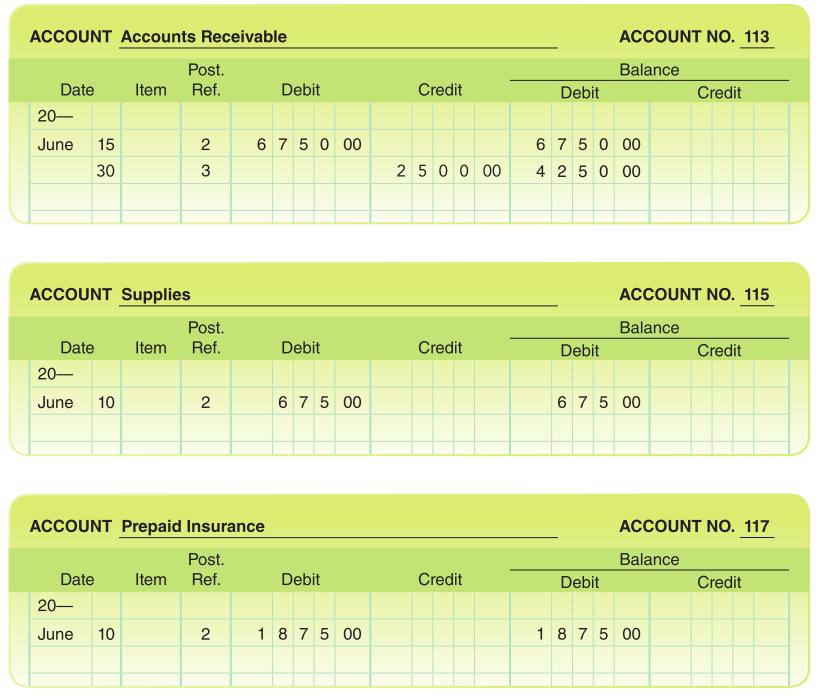

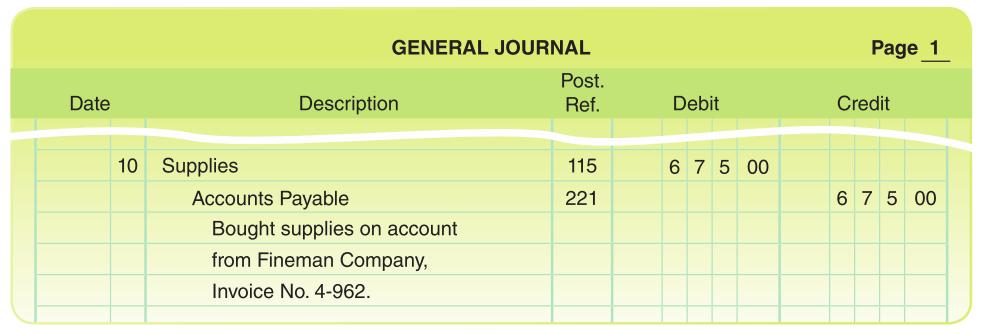

15 Posting to the General Ledger The journal is the book of original entry because each transaction must first be recorded in full in the journal. The ledger account gives us a complete record of the transactions recorded in each individual account. The general ledger contains all the accounts. The process of transferring information from the journal to the ledger is called posting. 3 15

16 3 16

17 3 17

18 The Posting Process STEP 1. Write the date of the transaction in the account s Date column. STEP 2. Write the amount of the transaction in the Debit or Credit column, and enter the balance in the Balance column under Debit or Credit. STEP 3. Write the page number of the journal in the Post. Ref. column of the ledger account. (This is a cross-reference; it tells you where the amount came from.) STEP 4. Record the ledger account number in the Post. Ref. column of the journal. 3 18

19 Date of transaction Amount of transaction Page number of the journal Ledger account number 3 19

20 Date of transaction Amount of transaction Page number of the journal Ledger account number 3 20

21 3 21

22

23

24

25

26

27 Preparation of the Trial Balance The trial balance is simply a list of accounts that have balances. Even when the debit and credit balances are equal, other types of errors may slip through for example, 1. Posting the correct debit or credit amounts to the incorrect account. 2. Neglecting to journalize or post an entire transaction. 3 27

28 Steps in the Accounting Process STEP 1. Record the transaction of a business in a journal. STEP 2. Post entries to the accounts in the ledger. STEP 3. Prepare a trial balance. 3 28

29 Source Documents 3 29

30 3 30

31 Manual Ruling Method An entry to record payment of $1,500 rent was incorrectly debited to Salary Expense. Manual Correcting Errors Before Posting Has Taken Place 3 31

32 Manual Ruling Method An entry for $120 payment for office supplies was recorded as $210. Manual Correcting Errors Before Posting Has Taken Place 3 32

33 Manual Ruling Method An entry to record cash received for professional fees was correctly journalized as $400. However, it was posted as a debit to Cash and a credit to Professional Fees for $4,000. Manual Correcting Errors After Posting Has Taken Place 3 33

34 Correcting Entry Method Manual or Computerized The correcting entry method is used when incorrectly journalized amounts have been posted. There are two correcting entry methods. One-step method. Simply make one entry that undoes the error and provides the correct account. Two-step method. The first step reverses the error made by the original entry. The second step includes the correct entry. 3 34

: A $620 payment for advertising was incorrectly journalized and posted as a debit to Miscellaneous Expense and a credit to")

35 Transaction (Jan. 9) : A $620 payment for advertising was incorrectly journalized and posted as a debit to Miscellaneous Expense and a credit to Cash for $620. The error was discovered on January 27. The following correction uses the one-step method: 3 35

36 The following correction uses the Two-step method 3 36

Posting from a General Journal to a General Ledger. Tuesday, October 26, :48:47 PM ET

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Chapter 4. Posting to a General Ledger

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

The General Ledger. The 4 th step of the accounting cycle is to post to the ledger.

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Chapter 02 - Analyzing and Recording Transactions. Chapter Outline

I. Analyzing and Recording Process A. The accounting process identifies business transactions and events, analyzes and records their effects, and summarizes and presents information in reports and financial

I. Analyzing and Recording Process A. The accounting process identifies business transactions and events, analyzes and records their effects, and summarizes and presents information in reports and financial

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Chapter 2 Recording Business Transactions

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Chapter 02 Analyzing and Recording Transactions

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY. Y. Chang Company COVER SHEET

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Errors Not Affecting the Trial Balance

Errors Not Affecting the Trial Balance With these types of errors, the debit and credit columns of the Trial Balance will still be the same total. These errors are corrected by means of JOURNAL ENTRIES.

Errors Not Affecting the Trial Balance With these types of errors, the debit and credit columns of the Trial Balance will still be the same total. These errors are corrected by means of JOURNAL ENTRIES.

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

RECORDING TRANSACTIONS

RECORDING TRANSACTIONS Instructions: 1. Use page 1 of the general journal. Journalize the following transactions completed during September of the current year. September 1 September 2 No. 1. Received

RECORDING TRANSACTIONS Instructions: 1. Use page 1 of the general journal. Journalize the following transactions completed during September of the current year. September 1 September 2 No. 1. Received

Accounts. Date Description Increase Decrease Balance. Jan. 1, 20X3 Balance forward $ 50,000. Jan. 2, 20X3 Collected receivable $ 10,000 60,000

Accounting System A system where transactions and events are reliably processed and summarized into financial statements and reports Manual or Automated Basic Processing Tools: Accounts Debits and Credits

Accounting System A system where transactions and events are reliably processed and summarized into financial statements and reports Manual or Automated Basic Processing Tools: Accounts Debits and Credits

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

Chapter 2. Ex a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit. Ex.

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Full file at Chapter 2: Analyzing Business Transactions

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

CHAPTER 2 THE RECORDING PROCESS CHAPTER LEARNING OBJECTIVES

CHAPTER 2 THE RECORDING PROCESS CHAPTER LEARNING OBJECTIVES 1. Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset,

CHAPTER 2 THE RECORDING PROCESS CHAPTER LEARNING OBJECTIVES 1. Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset,

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

How to Journalize using Data Entry

Steps Essential to Success 1. Print a copy of the Problem you intend to complete. To do so, go to the software log-in page and click on Download Student Manual button, click on the Problem to open it.

Steps Essential to Success 1. Print a copy of the Problem you intend to complete. To do so, go to the software log-in page and click on Download Student Manual button, click on the Problem to open it.

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Chapter 2 The Accounting Information System

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number FUNDAMENTAL ACCOUNTING (01) Regional 2005 Time Rank Multiple Choice Questions (30 @ 5 pts. each) Definitions Matching (10 @ 5 pts. each) (150 points) (50 points) Production Portion

13 Pages Contestant Number FUNDAMENTAL ACCOUNTING (01) Regional 2005 Time Rank Multiple Choice Questions (30 @ 5 pts. each) Definitions Matching (10 @ 5 pts. each) (150 points) (50 points) Production Portion

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

CHAPTER 2 ANALYZING TRANSACTIONS DISCUSSION QUESTIONS

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

CHAPTER 2 THE RECORDING PROCESS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT

CHAPTER 2 THE RECORDING PROCESS sg st SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 3 K 25.

CHAPTER 2 THE RECORDING PROCESS sg st SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 3 K 25.

Accounting for Business Transactions QUESTIONS

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

On October 1, 2010, Cody Doerr established Banyan Realty, which completed the following transaction during the month:

Pr 2-2 A page 91 On October 1, 2010, Cody Doerr established Banyan Realty, which completed the following transaction during the month: A. Cody Doerr transferred cash from a personal bank account to an

Pr 2-2 A page 91 On October 1, 2010, Cody Doerr established Banyan Realty, which completed the following transaction during the month: A. Cody Doerr transferred cash from a personal bank account to an

A. Unearned Revenue. B. Accounts Payable. C. Supplies. D. Accounts Receivable.

02 Student: 1. Which of the following would be listed as a long-term asset? A. Cash. B. Supplies. C. Buildings and equipment. D. Total assets. 2. Which of the following would be listed as a current liability?

02 Student: 1. Which of the following would be listed as a long-term asset? A. Cash. B. Supplies. C. Buildings and equipment. D. Total assets. 2. Which of the following would be listed as a current liability?

Problems: Set C. 8 chapter 3 The Accounting Information System

8 chapter 3 The Accounting Information System compute net income. (b) Net income $4,910 prepare financial statements. (a) Cash $12,680 Problems: Set C P3-1C New Dawn Window Washing Inc. was started on

8 chapter 3 The Accounting Information System compute net income. (b) Net income $4,910 prepare financial statements. (a) Cash $12,680 Problems: Set C P3-1C New Dawn Window Washing Inc. was started on

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Debit and Credit Rules Module 2 part I. T- Accounts Assets = Liabilities + OE. T- Accounts: Basic Patterns A = L + OE

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2009 Multiple Choice (30 @ 2 points each) Account Identification (39 @ 1 point each) Production Portion Problem 1: Journalizing

13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2009 Multiple Choice (30 @ 2 points each) Account Identification (39 @ 1 point each) Production Portion Problem 1: Journalizing

Fundamental Accounting Principles

Last revised: January 23, 2016. SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 15 th Canadian Edition by Larson/Jensen/Dieckmann Revised for the 15 th Edition by: Praise Ma, Kwantlen Polytechnic

Last revised: January 23, 2016. SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 15 th Canadian Edition by Larson/Jensen/Dieckmann Revised for the 15 th Edition by: Praise Ma, Kwantlen Polytechnic

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

Fundamental Accounting Principles

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 14 th Canadian Edition by Larson/Jensen Prepared by: Tilly Jensen, Athabasca University Wendy Popowich, Northern Alberta Institute of Technology

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 14 th Canadian Edition by Larson/Jensen Prepared by: Tilly Jensen, Athabasca University Wendy Popowich, Northern Alberta Institute of Technology

Exercise 2-1. Exercise 2-2. Exercise 2-3. Name. = Liabilitiy Acounts + Debit Credit. Asset Acounts. Stockholders Equity Acounts Debit. Credit.

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

9 Payments, and Banking Procedures. Cash Receipts, Cash

9-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Cash Receipts, Cash 9 Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts

9-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Cash Receipts, Cash 9 Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts

SOLUTIONS TO EXERCISES SET B

SOLUTIONS TO EXERCISES SET B EXERCISE 2-1B 1. False. An account is an accounting record of a specific asset, liability, or stockholders equity item. 2. True. 3. False. Each asset, liability, and stockholders

SOLUTIONS TO EXERCISES SET B EXERCISE 2-1B 1. False. An account is an accounting record of a specific asset, liability, or stockholders equity item. 2. True. 3. False. Each asset, liability, and stockholders

Chapter 2: Measurement Concepts: Recording Business Transactions

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

It would probably be useful to illustrate a few simple transactions using double-entry accounting, and to go over key terms.

DOWNLOAD FULL SOLUTION MANUAL FOR SURVEY OF ACCOUNTING 6TH EDITION BY WARREN Link download: https://testbankservice.com/download/solution-manual-forsurvey-of-accounting-6th-edition-by-warren APPENDIX A

DOWNLOAD FULL SOLUTION MANUAL FOR SURVEY OF ACCOUNTING 6TH EDITION BY WARREN Link download: https://testbankservice.com/download/solution-manual-forsurvey-of-accounting-6th-edition-by-warren APPENDIX A

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

CHAPTER 2 THE RECORDING PROCESS

CHAPTER 2 THE RECORDING PROCESS SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM S TAXONOMY Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT True-False Statements 1. 1 K 9. 2 K 17. 3 K 25. 5

CHAPTER 2 THE RECORDING PROCESS SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM S TAXONOMY Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT True-False Statements 1. 1 K 9. 2 K 17. 3 K 25. 5

Financial And Managerial Accounting, 2nd Edition TEST BANK Weygandt Kimmel Kieso

Financial And Managerial Accounting, 2nd Edition TEST BANK Weygandt Kimmel Kieso Full download at: https://testbankreal.com/download/financial -managerialaccounting-2nd-edition-test-bank-weygandt-kimmel-kieso/

Financial And Managerial Accounting, 2nd Edition TEST BANK Weygandt Kimmel Kieso Full download at: https://testbankreal.com/download/financial -managerialaccounting-2nd-edition-test-bank-weygandt-kimmel-kieso/

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Chapter 02 Analyzing Business Transactions

College Accounting A Contemporary Approach 4th Edition Haddock TEST BANK Full download at: https://testbankreal.com/download/college-accounting-contemporary-approach-4thedition-haddock-test-bank/ College

College Accounting A Contemporary Approach 4th Edition Haddock TEST BANK Full download at: https://testbankreal.com/download/college-accounting-contemporary-approach-4thedition-haddock-test-bank/ College

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions. Chapter Overview. Learning Objectives

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Name: Date: Period: Standard 2: Students will list and identify characteristics of the three basic accounting equation elements.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

THE RECORDING PROCESS

7566dc02_042-085 12/12/00 8:43 PM Page 42 2 THE RECORDING PROCESS THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On

7566dc02_042-085 12/12/00 8:43 PM Page 42 2 THE RECORDING PROCESS THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Paper 11 Question Number Key Question Number Key 1 B 16 B 2 C 17 B 3 D 18 D 4 C 19 A 5 B 20 B 6 B 21 A 7 C 22 D 8 D 23 A 9 B 24 B 10 A 25 C 11 D 26 D 12 A 27 C 13 C

PRINCIPLES OF ACCOUNTS Paper 7110/11 Paper 11 Question Number Key Question Number Key 1 B 16 B 2 C 17 B 3 D 18 D 4 C 19 A 5 B 20 B 6 B 21 A 7 C 22 D 8 D 23 A 9 B 24 B 10 A 25 C 11 D 26 D 12 A 27 C 13 C

The Recording Process

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

ANALYZING TRANSACTIONS

ANALYZING TRANSACTIONS objectives After studying this chapter, you should be able to: Explain why accounts are used to record and summarize the effects of transactions on financial statements. Describe

ANALYZING TRANSACTIONS objectives After studying this chapter, you should be able to: Explain why accounts are used to record and summarize the effects of transactions on financial statements. Describe

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis 2/2017 Sub Topics 1. Accounting Cycles 2. Accounting Entry Principle 3. Transaction Analysis 1 1. ACCOUNTING CYCLE Identify

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis 2/2017 Sub Topics 1. Accounting Cycles 2. Accounting Entry Principle 3. Transaction Analysis 1 1. ACCOUNTING CYCLE Identify

Accounting. Chapter 6

Accounting Chapter 6 Aim: What are four source documents and when would they be used? Do Now: Take a Do Now slip. Answer: Why do people use journals? Have you ever kept a daily journal of the things that

Accounting Chapter 6 Aim: What are four source documents and when would they be used? Do Now: Take a Do Now slip. Answer: Why do people use journals? Have you ever kept a daily journal of the things that