THE ACCOUNTING INFORMATION SYSTEM

|

|

|

- Harvey Wiggins

- 5 years ago

- Views:

Transcription

systems. are economic events that require recording in the financial statements.")

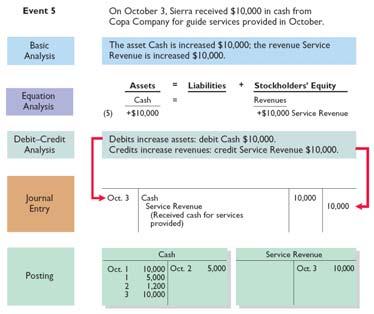

1 Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process. 3. Define debits and credits and explain how they are used to record business transactions. 4. Identify the basic steps in the recording process. 5. Explain what a journal is and how it helps in the recording process. 6. Explain what a ledger is and how it helps in the recording process. 7. Explain what posting is and how it helps in the recording process. 8. Explain the purposes of a trial balance. 9. Classify cash activities as operating, investing, or financing Financial Accounting, Sixth Edition 3-3 Accounting Information System Accounting Information System System of collecting and processing transaction data and communicating financial information to decision makers. Most businesses use computerized accounting (EDP) systems. are economic events that require recording in the financial statements. Not all activities represent transactions. Assets, liabilities, or stockholders equity items change as a result of some economic event. Dual effect on the accounting equation. Question: Are the following events recorded in the accounting records? Event Criterion Record/ Don t Record Purchased a computer. Discuss guided trip options with potential customer. Illustration 3-1 Pay rent. Is the financial position (assets, liabilities, or stockholders equity) of the company changed? Analyzing Analyzing Illustration: 1. On October 1, cash of $10,000 is invested in Sierra Corporation by investors in exchange for $10,000 of common stock. process of identifying the specific effects of economic events on the accounting equation. Illustration 3-2 Expanded accounting equation Basic Accounting Equation Assets =

2 2. On October 1, Sierra borrowed $ from Castle Bank by signing a 3-month, 12%, $ note payable. 3. On October 2, Sierra purchased equipment by paying $ cash to Superior Equipment Sales Co. 4. On October 2, Sierra received a $1,200 cash advance from R. Knox, a client On October 3, Sierra received $10,000 in cash from Copa Company for guide services performed. 6. On October 3, Sierra Corporation paid its office rent for the month of October in cash, $ On October 4, Sierra paid $600 for a one-year insurance policy that will expire next year on September On October 5, Sierra purchased supplies on account from Aero Supply for $2, On October 20, Sierra paid a $500 dividend. 11. Employees have worked two weeks, earning $4,000 in salaries, which were paid on October ,500 +2, ,500 +2, ,500 +2, ,000-4,

3 Account Account Debit and Credit Procedures Account An Account can be illustrated in a T-Account form. Record of increases and decreases in a specific asset, liability, equity, revenue, or expense item. Debit = Left Credit = Right Account Name Debit and Credit Procedures Double-entry entry system Each transaction must affect two or more accounts to keep the basic accounting equation in balance. done by debiting at least one account and crediting another. DEBITS must equal CREDITS. If Debits are greater than Credits, the account will have a debit balance. Transaction #1 Transaction #3 Account Name $10,000 $3,000 Transaction #2 8,000 $ SO 2 Explain what an account is and how it helps in the recording process Debit and Credit Procedures Dr./Cr. Procedures for Assets and Liabilities Dr./Cr. Procedures for Stockholders Equity If Credits are greater than Debits, the account will have a credit balance. Transaction #1 Account Name $10,000 $3,000 Transaction #2 Assets Assets - Debits should exceed credits. Liabilities Credits should exceed debits. Stockholders Equity Owner s investments and revenues increase stockholder s equity (credit). Dividends and expenses decrease stockholder s equity (debit). 8,000 Transaction #3 $1,000 Liabilities normal balance is on the increase side. Common Stock Retained Earnings Dividends Dr./Cr. Procedures for Revenue and Expense Revenue Expense purpose of earning revenues is to benefit the stockholders. effect of debits and credits on revenue accounts is the same as their effect on stockholders equity. Expenses have the opposite effect: expenses decrease stockholders equity. Stockholders Equity Relationships Illustration 3-15 Summary of of Debit/Credit Rules Normal Debit Assets Expense Normal Credit Stockholders Equity Liabilities Revenue

4 Summary of Debit/Credit Rules Debit Credit Sheet Income Statement Asset = Liability + Equity Revenue - Expense = Summary of Debit/Credit Rules Debits: a. increase both assets and liabilities. b. decrease both assets and liabilities. c. increase assets and decrease liabilities. d. decrease assets and increase liabilities. Summary of Debit/Credit Rules Accounts that normally have debit balances are: a. assets, expenses, and revenues. b. assets, expenses, and equity. c. assets, liabilities, and dividends. d. assets, dividends, and expenses Steps in the Steps in the Illustration 3-17 Journal Book of original entry. recorded in chronological order. Contributions to the recording process: Analyze each transaction Enter transaction in a journal Transfer journal information to ledger accounts 1. Discloses the complete effects of a transaction. Source documents, such as a sales slip, a check, a bill, or a cash register tape, provide evidence of the transaction. 2. Provides a chronological record of transactions. 3. Helps to prevent or locate errors because the debit and credit amounts can be easily compared SO 4 Identify the basic steps in the recording process Journal Journalizing Journalizing Journalizing - Entering transaction data in the journal. Sierra issued common stock in exchange for $10,000 cash. Sierra borrowed $ by signing a note. Illustration: Presented below is information related to Sierra Corporation. Sierra issued common stock in exchange for $10,000 cash. 1 2 Sierra borrowed $ by signing a note. Sierra purchased office equipment for $. Instructions - Journalize these transactions. Date General Journal Account Title Ref. Debit Credit Cash Common stock 10,000 10,000 Date General Journal Account Title Ref. Debit Credit Cash Notes payable

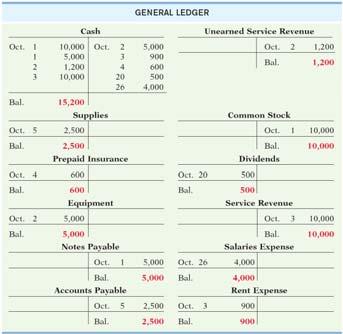

5 Journalizing Steps in the Steps in the Oct. 2 Sierra purchased equipment for $. Ledger contains the entire group of accounts maintained by a company. Chart of Accounts listing of accounts used by a company to record transactions. Illustration 3-19 Date Oct. 2 General Journal Account Title Ref. Debit Credit Equipment Cash SO 6 Explain what a ledger is and how it helps in the recording process SO 6 Explain what a ledger is and how it helps in the recording process. Steps in the Posting: a. normally occurs before journalizing. b. transfers ledger transaction data to the journal. c. is an optional step in the recording process. d. transfers journal entries to ledger accounts. Follow these steps: 1. Determine what type of account is involved. 2. Determine what items increased or decreased and by how much. 3. Translate the increases and decreases into debits and credits. Follow these steps: 1. Determine what type of account is involved. 2. Determine what items increased or decreased and by how much. 3. Translate the increases and decreases into debits and credits. Illustration 3-21 Illustration Follow these steps: 1. Determine what type of account is involved. 2. Determine what items increased or decreased and by how much. 3. Translate the increases and decreases into debits and credits. Illustration Illustration 3-24 Illustration

6 Illustration 3-26 Illustration 3-28 Illustration Illustration 3-29 Illustration 3-30 Illustration SO 7 Summary Illustration of Journalizing Illustration 3-32 Summary Illustration of Journalizing Illustration 3-32 Summary Illustration of Posting Illustration

7 Trial Trial Trial A list of accounts and their balances at a given time. Purpose is to prove that debits equal credits. Limitations of a Trial trial balance may balance even when 1. a transaction is not journalized, 2. a correct journal entry is not posted, 3. a journal entry is posted twice, 4. incorrect accounts are used in journalizing or posting, or 5. offsetting errors are made in recording the amount of a transaction. A trial balance will not balance if: a. a correct journal entry is posted twice. b. the purchase of supplies on account is debited to Supplies and credited to Cash. c. a $100 cash dividends is debited to the Dividends account for $1,000 and credited to Cash for $100. d. a $450 payment on account is debited to Accounts Payable for $45 and credited to Cash for $45. Illustration SO 8 Explain the purposes of a trial balance SO 8 Explain the purposes of a trial balance. Copyright Copyright 2011 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. purchaser may make back-up copies for his/her own use only and not for distribution or resale. Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein. 3-58

The Recording Process

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

The Recording Process

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Chapter 2 The Accounting Information System

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

CHAPTER 3. Analyze the effect of business transactions on the basic accounting equation.

CHAPTER 3 The Accounting Information System Study Objectives Analyze the effect of business transactions on the basic accounting equation. Explain what an account is and how it helps in the recording process.

CHAPTER 3 The Accounting Information System Study Objectives Analyze the effect of business transactions on the basic accounting equation. Explain what an account is and how it helps in the recording process.

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounts. Date Description Increase Decrease Balance. Jan. 1, 20X3 Balance forward $ 50,000. Jan. 2, 20X3 Collected receivable $ 10,000 60,000

Accounting System A system where transactions and events are reliably processed and summarized into financial statements and reports Manual or Automated Basic Processing Tools: Accounts Debits and Credits

Accounting System A system where transactions and events are reliably processed and summarized into financial statements and reports Manual or Automated Basic Processing Tools: Accounts Debits and Credits

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis 2/2017 Sub Topics 1. Accounting Cycles 2. Accounting Entry Principle 3. Transaction Analysis 1 1. ACCOUNTING CYCLE Identify

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis 2/2017 Sub Topics 1. Accounting Cycles 2. Accounting Entry Principle 3. Transaction Analysis 1 1. ACCOUNTING CYCLE Identify

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

2 The Recording Process

JWCL165_c02_050-095.qxd 7/29/09 4:52 PM Page 50 Chapter 2 The Recording Process STUDY OBJECTIVES The Navigator After studying this chapter, you should be Scan Study Objectives able to: Read Feature Story

JWCL165_c02_050-095.qxd 7/29/09 4:52 PM Page 50 Chapter 2 The Recording Process STUDY OBJECTIVES The Navigator After studying this chapter, you should be Scan Study Objectives able to: Read Feature Story

C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

WILEY. The Recording Process IFRS EDITION PREVIEW OF CHAPTER 2 LEARNING OBJECTIVES. Financial Accounting IFRS 3rd Edition Weygandt Kimmel Kieso

WILEY IFRS EDITION Prepared by Coby Harmon University of California, Santa Barbara 2-1 Westmont College PREVIEW OF CHAPTER 2 2-2 Financial Accounting IFRS 3rd Edition Weygandt Kimmel Kieso 2 CHAPTER The

WILEY IFRS EDITION Prepared by Coby Harmon University of California, Santa Barbara 2-1 Westmont College PREVIEW OF CHAPTER 2 2-2 Financial Accounting IFRS 3rd Edition Weygandt Kimmel Kieso 2 CHAPTER The

The Accounting Information System

2918T_c03_100-159.qxd 8/11/08 10:09 PM Page 100 chapter 3 The Accounting Information System the navigator Scan Study Objectives study objectives Read Feature Story After studying this chapter, you should

2918T_c03_100-159.qxd 8/11/08 10:09 PM Page 100 chapter 3 The Accounting Information System the navigator Scan Study Objectives study objectives Read Feature Story After studying this chapter, you should

CHAPTER2. The Recording Process. Study Objectives. Feature Story. [The Navigator]

![CHAPTER2. The Recording Process. Study Objectives. Feature Story. [The Navigator]](/thumbs/73/69073986.jpg "CHAPTER2. The Recording Process. Study Objectives. Feature Story. [The Navigator]") CHAPTER2 Study Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and credits and explain their use

CHAPTER2 Study Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and credits and explain their use

Chapter 8: Investments in Equity Securities

1 Chapter 8: Investments in Equity Securities 2 Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion as a

1 Chapter 8: Investments in Equity Securities 2 Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion as a

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Chapter. Chapter. Accounting and the Time Value of Money. Time Value of Money. Basic Time Value Concepts. Basic Time Value Concepts

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

The Recording Process

The Recording Process Chapter 2 THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 53 p. 56 p. 67 p. 71 Work Demonstration

The Recording Process Chapter 2 THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 53 p. 56 p. 67 p. 71 Work Demonstration

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Introduction to Fund Accounting

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Chapter 16: Dilutive Securities and Earnings per Share

Intermediate Accounting, 11th ed. Kieso, Weygandt, and Warfield Chapter 16: Dilutive Securities and Earnings per Share Prepared by Jep Robertson and Renae Clark New Mexico State University Chapter 16:

Intermediate Accounting, 11th ed. Kieso, Weygandt, and Warfield Chapter 16: Dilutive Securities and Earnings per Share Prepared by Jep Robertson and Renae Clark New Mexico State University Chapter 16:

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

The Recording Process

Chapter 2 The Recording Process STUDY OBJECTIVES The Navigator After studying this chapter, you should be Scan Study Objectives able to: Read Feature Story 1 Explain what an account is and how it Read

Chapter 2 The Recording Process STUDY OBJECTIVES The Navigator After studying this chapter, you should be Scan Study Objectives able to: Read Feature Story 1 Explain what an account is and how it Read

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS. Balance Sheet and Statement of of Cash Flows. Usefulness of the Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Chapter 3: Double-Entry Bookkeeping

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

Accounting for Receivables

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

THE RECORDING PROCESS

7566dc02_042-085 12/12/00 8:43 PM Page 42 2 THE RECORDING PROCESS THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On

7566dc02_042-085 12/12/00 8:43 PM Page 42 2 THE RECORDING PROCESS THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On

Posting from a General Journal to a General Ledger. Tuesday, October 26, :48:47 PM ET

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Learning Objectives. Chapter 2 The Accounting Cycle: During the Period INSTRUCTOR S MANUAL

Financial Accounting 4th Edition SOLUTIONS MANUAL Spiceland Thomas Herrmann Full download at: https://testbankreal.com/download/financial-accounting-4th-editionsolutions-manual-spiceland-thomas-herrmann/

Financial Accounting 4th Edition SOLUTIONS MANUAL Spiceland Thomas Herrmann Full download at: https://testbankreal.com/download/financial-accounting-4th-editionsolutions-manual-spiceland-thomas-herrmann/

PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

Accounting for Receivables

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 2 Recording Business Transactions

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Chapter 4. Posting to a General Ledger

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

The Recording Process

8961dch02.qxd 9/24/03 11:58 AM Page 43 Mac113 mac113:122_edl: The Recording Process Chapter 2 THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text

8961dch02.qxd 9/24/03 11:58 AM Page 43 Mac113 mac113:122_edl: The Recording Process Chapter 2 THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Corporate Work Sheets, Taxes, and Dividends

21 Corporate Work Sheets, Taxes, and Dividends DEMONSTRATION PROBLEM The Stockholders Equity section of the balance sheet for Moore Company as of December 31, 20, is as follows: Stockholders' Equity Paid-in

21 Corporate Work Sheets, Taxes, and Dividends DEMONSTRATION PROBLEM The Stockholders Equity section of the balance sheet for Moore Company as of December 31, 20, is as follows: Stockholders' Equity Paid-in

Name: Date: Period: Standard 2: Students will list and identify characteristics of the three basic accounting equation elements.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

PREVIEW OF CHAPTER 20-2

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Chapter 11. Notes, Bonds, and Leases

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

Investments. 1. Discuss why corporations invest in debt and share securities.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Chapter 5: Using Financial Statement Information

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

Chapter 8. Portfolio Selection. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

Chapter 14. Statement of Cash Flows

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

CHAPTER 2 THE RECORDING PROCESS CHAPTER LEARNING OBJECTIVES

CHAPTER 2 THE RECORDING PROCESS CHAPTER LEARNING OBJECTIVES 1. Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset,

CHAPTER 2 THE RECORDING PROCESS CHAPTER LEARNING OBJECTIVES 1. Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset,

True / False Questions

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Accounting Terms Chap 1-8

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 5. Page 1. How Securities Are Traded. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 5 How Securities Are Traded Learning Objectives Explain the role of brokerage firms and stockbrokers.

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 5 How Securities Are Traded Learning Objectives Explain the role of brokerage firms and stockbrokers.

Chapter 2: Measurement Concepts: Recording Business Transactions

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 9 ACCOUNTING FOR RECEIVABLES Hey Sabres Accountants of Tomorrow, look for

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 9 ACCOUNTING FOR RECEIVABLES Hey Sabres Accountants of Tomorrow, look for

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

TH E ACCO U NTI NG LEARNING OBJECTIVES. Needed: A Reliable Information System. After studying this chapter, you should be able to:

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

Financial Statement Analysis

14-1 Chapter 14 Financial Statement Analysis 14-2 Learning Objectives After studying this chapter, you should be able to: 1. Discuss the need for comparative analysis. 2. Identify the tools of financial

14-1 Chapter 14 Financial Statement Analysis 14-2 Learning Objectives After studying this chapter, you should be able to: 1. Discuss the need for comparative analysis. 2. Identify the tools of financial

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about