Posting from a General Journal to a General Ledger. Tuesday, October 26, :48:47 PM ET

|

|

|

- Ross Payne

- 5 years ago

- Views:

Transcription

1 Posting from a General Journal to a General Ledger

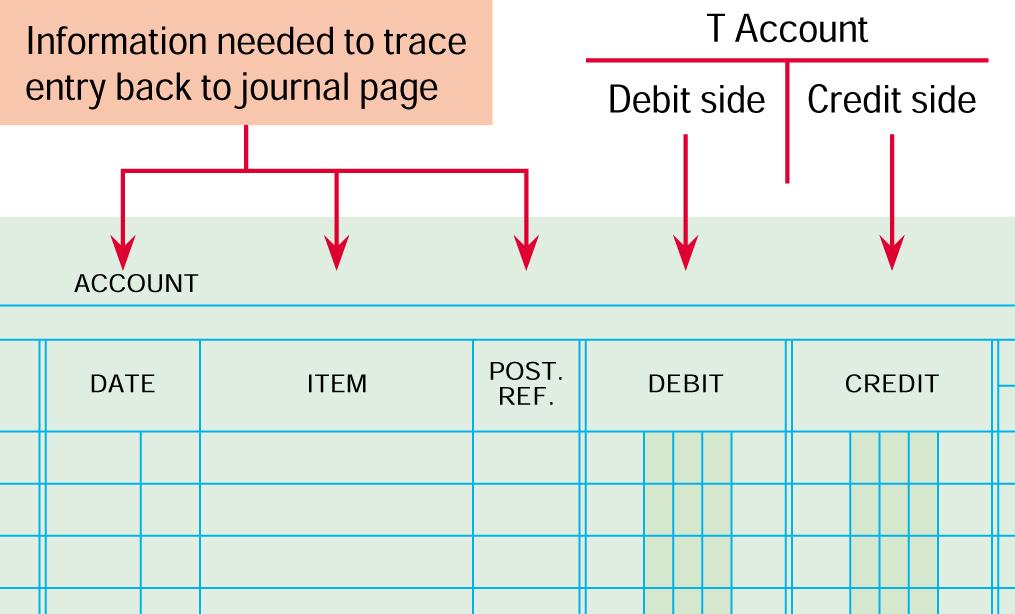

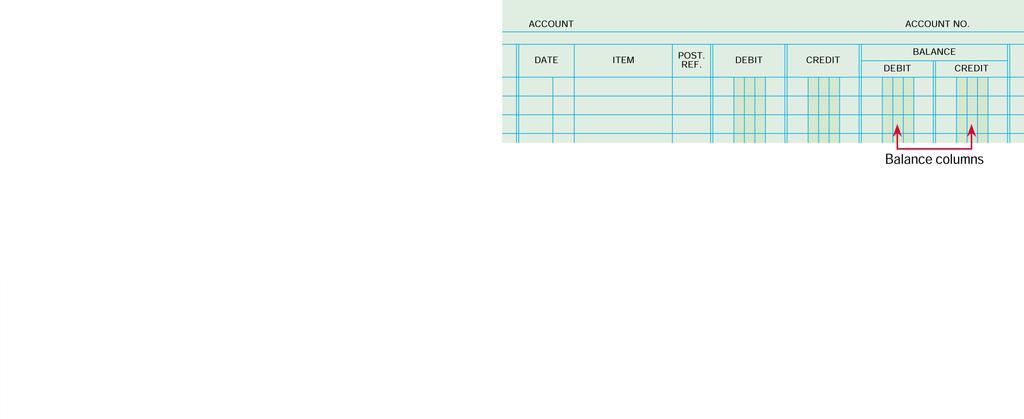

2 Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns for the debit and credit balance. The account balance is calculated as each entry is recorded in the account.

3

4 Ledger A group of accounts. General Ledger A ledger that contains all accounts needed to prepare financial statements. Account Number The number assigned to an account. Chart of Accounts A list of account titles and numbers showing the location of each account in a ledger.

5

6 Account numbers are assigned by 10s so that new accounts can be added easily. Expense accounts are arranged alphabetically When a new account is added the new number account number should be the middle, unused number.

7 Write the account title. 2. Write the account number.

8 p. 100 Audit Your Understanding p. 100 (p. 65) Work Together p. 100 (p. 66) On Your Own p. 113 (p. 77) Application Problem 5-1

9 Posting from a General Journal to a General Ledger

10 Posting Transferring information from a journal entry to a ledger account. All changes to an account are brought together in that account. Each amount in the Debit and Credit columns of a general journal is posted to the account written in the Account Title column.

11 Post References The numbers in the Post Ref. columns of the general journal and general ledger serve three purposes: 1. An entry in an account can be traced to its source in a journal. 2. An entry in a journal can be traced to where it was posted in an account. 3. If posting is interrupted, the accounting personnel can easily see what entries still need to be posted. The Post Reference is always recorded last.

12 August 1. Received cash from owner as an investment, $10, Receipt No. 1.

13 Write the date. 2. Write journal page number. 3. Write the debit amount. 4. Write new account balance. 5. Write the account number in the Post. Ref. column of the journal.

14 Write the date. 2. Write the journal page number. 3. Write the credit amount. 4. Write the new account balance. 5. Write the account number in the Post. Ref. column of the journal.

15 August 7. Bought supplies on account from Ling Music Supplies, $2, Memorandum No.1.

16 August 11. Paid cash on account to Ling Music Supplies, $1,360.00, Check No. 3.

17 1. Write the date Write the journal page number. 3. Write the debit amount. 4. Write the new account balance. 5. Write the account number in the Post. Ref. column of the journal.

18 p. 105 Audit Your Understanding p. 105 (p ) Work Together p. 105 (p ) On Your Own p. 113 (p ) Application Problem 5-2

19 Completed General Ledger, Proving Cash, and Making Correcting Entries

20 Proving Cash Determining that the amount of cash agrees with the balance of the cash account in the accounting records. Always prove Cash at the end of the month Compare the cash balance in a Checkbook with the cash balance in the Cash account.

21 Correcting Entries A journal entry made to correct an error in the ledger.

22 November 13. Discovered that a payment of cash for advertising in October was journalized and posted in error as a debit to Miscellaneous Expense instead of Advertising Expense, $ Memorandum No. 45. Advertising Expense 1. Which accounts are affected? Advertising Expense Miscellaneous Expense 2. How is each account classified? Advertising Expense is an expense account. Miscellaneous Expense is an expense account. 3. How is each classification changed? Expenses are increased. Expenses are decreased. 4. How is each amount entered in the accounts? Expense accounts increase on the debit side. Expense accounts decrease on the credit side. Debit Normal Balance Miscellaneous Expense Debit Normal Balance

23 Write the date. 2. Debit Advertising Expense. 3. Credit Miscellaneous Expense. 4. Write the source document number. 4

24 p. 111 Audit Your Understanding p. 111 (p. 75) Work Together p. 111 (p. 76) On Your Own p. 113 (p. 83) Application Problem 5-3 P. 114 ( p ) Mastery Problem 5-4 P. 114 ( p ) Challenge Problem 5-5

Chapter 4. Posting to a General Ledger

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Journalizing Sales and Cash Receipts Using Special Journals. Friday, February 25, :53:53 AM ET

Journalizing Sales and Cash Receipts Using Special Journals Customer A person or business to whom merchandise or services are sold. Sales Tax A tax on a sale of merchandise or services. Businesses must

Journalizing Sales and Cash Receipts Using Special Journals Customer A person or business to whom merchandise or services are sold. Sales Tax A tax on a sale of merchandise or services. Businesses must

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

RECORDING TRANSACTIONS

RECORDING TRANSACTIONS Instructions: 1. Use page 1 of the general journal. Journalize the following transactions completed during September of the current year. September 1 September 2 No. 1. Received

RECORDING TRANSACTIONS Instructions: 1. Use page 1 of the general journal. Journalize the following transactions completed during September of the current year. September 1 September 2 No. 1. Received

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

SECOND REVISED REINFORCEMENT ACTIVITY 1. Name Date Class. PART A, p. 147

Bst-acta--.qxd 0//0 : PM Page Name Date Class PART A, p. An Accounting Cycle for a Proprietorship: Journalizing and Posting Transactions.,.,. TITLE DOC. NO. JOURNAL PAGE GENERAL SALES CASH 0 0 0 0 Reinforcement

Bst-acta--.qxd 0//0 : PM Page Name Date Class PART A, p. An Accounting Cycle for a Proprietorship: Journalizing and Posting Transactions.,.,. TITLE DOC. NO. JOURNAL PAGE GENERAL SALES CASH 0 0 0 0 Reinforcement

ACCOUNTING I Chapter 10 Reading Guide. 1. What are the two major activities of merchandising businesses?

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Recording Departmental Sales and Cash Receipts

Recording Departmental Sales and Cash Receipts Departmental Sales on Account and Sales Returns and Allowances MasterSport records all departmental sales on account in a Sales Journal. The Sales Journal

Recording Departmental Sales and Cash Receipts Departmental Sales on Account and Sales Returns and Allowances MasterSport records all departmental sales on account in a Sales Journal. The Sales Journal

Name: Date: Period: Standard 2: Students will list and identify characteristics of the three basic accounting equation elements.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

A Business Simulation

A Business Simulation This simulation covers the transactions completed by Rico Sanchez, Disc Jockey, a service business organized as a proprietorship. Rico Sanchez, the owner, began his disc jockey business

A Business Simulation This simulation covers the transactions completed by Rico Sanchez, Disc Jockey, a service business organized as a proprietorship. Rico Sanchez, the owner, began his disc jockey business

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS. Assign Students to Read Ch. 9 and complete the terms p. 234

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS Assign Students to Read Ch. 9 and complete the terms p. 234 (Students may hand-write them on handout or do on word processor) Discuss Section

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS Assign Students to Read Ch. 9 and complete the terms p. 234 (Students may hand-write them on handout or do on word processor) Discuss Section

Journalizing Transactions

LESSON Journalizing Transactions CENTURY ACCOUNTING Thomson/South-Western Objectives:. Define accounting terms related to journalizing transactions.. Identify accounting concepts and practices related

LESSON Journalizing Transactions CENTURY ACCOUNTING Thomson/South-Western Objectives:. Define accounting terms related to journalizing transactions.. Identify accounting concepts and practices related

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

LESSON Journalizing Purchases Using a Purchases Journal

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

11-7. CHALLENGE PROBLEM, pp. 333, 334. Name Date Class. Journalizing and posting business transactions 1., 2. SALES JOURNAL 1., 3.

-7 CHALLENGE PROBLEM, pp., Journalizing and posting business transactions.,. ED SALES JOURNAL SALE NO. PAGE S RECEIVABLE SALES SALES TAX PAYABLE.,. PURCHASES JOURNAL PAGE ED PURCH. NO. PURCHASES DR. ACCTS.

-7 CHALLENGE PROBLEM, pp., Journalizing and posting business transactions.,. ED SALES JOURNAL SALE NO. PAGE S RECEIVABLE SALES SALES TAX PAYABLE.,. PURCHASES JOURNAL PAGE ED PURCH. NO. PURCHASES DR. ACCTS.

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

FUNDAMENTAL ACCOUNTING (01)

") 14 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional - 2007 Multiple Choice (30 @ 3 points each) Account Identification (15 @ 3 points each) Production Portion Problem 1: Financial

14 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional - 2007 Multiple Choice (30 @ 3 points each) Account Identification (15 @ 3 points each) Production Portion Problem 1: Financial

Journalizing Sales and Cash Receipt Using Special Journals

Chapter 10 Journalizing Sales and Cash Receipt Using Special Journals Objectives 1. Define accounting terms related to sales and cash receipts for a merchandising business. 2. Identify accounting concepts

Chapter 10 Journalizing Sales and Cash Receipt Using Special Journals Objectives 1. Define accounting terms related to sales and cash receipts for a merchandising business. 2. Identify accounting concepts

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number FUNDAMENTAL ACCOUNTING (01) Regional 2005 Time Rank Multiple Choice Questions (30 @ 5 pts. each) Definitions Matching (10 @ 5 pts. each) (150 points) (50 points) Production Portion

13 Pages Contestant Number FUNDAMENTAL ACCOUNTING (01) Regional 2005 Time Rank Multiple Choice Questions (30 @ 5 pts. each) Definitions Matching (10 @ 5 pts. each) (150 points) (50 points) Production Portion

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2009 Multiple Choice (30 @ 2 points each) Account Identification (39 @ 1 point each) Production Portion Problem 1: Journalizing

13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2009 Multiple Choice (30 @ 2 points each) Account Identification (39 @ 1 point each) Production Portion Problem 1: Journalizing

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2006 Multiple Choice (30 @ 3 points each) Account Identification (15 @ 3 points each) Production Portion Problem 1: Financial Transactions

13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2006 Multiple Choice (30 @ 3 points each) Account Identification (15 @ 3 points each) Production Portion Problem 1: Financial Transactions

Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form.

Opening Entries Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form. The journal is the book of original entry. The journal

Opening Entries Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form. The journal is the book of original entry. The journal

LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check.

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Cash Control Systems

Chapter 5 Cash Control Systems Objectives: 1. Define accounting terms related to using a checking account and a petty cash fund. 2. Identify accounting concepts and practices related to using a checking

Chapter 5 Cash Control Systems Objectives: 1. Define accounting terms related to using a checking account and a petty cash fund. 2. Identify accounting concepts and practices related to using a checking

The Expanded Ledger: Revenue, Expense, and Drawings

Revenue, Expense, and Drawings Remember the following before proceeding to the next slide!! Up until now, we have been recording transactions to the Capital account in the Owner s Equity section. Here

Revenue, Expense, and Drawings Remember the following before proceeding to the next slide!! Up until now, we have been recording transactions to the Capital account in the Owner s Equity section. Here

Analyzing the Accounting Equation

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

Accounting 1. Lesson Plan. Topic: Recording Sales and Cash Receipts Using Special Journals Unit: 4 Chapter 20

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Recording Sales and Cash Receipts Using Special Journals Unit: 4 Chapter 20 I. Objective(s): By the end of today s lesson, the student will

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Recording Sales and Cash Receipts Using Special Journals Unit: 4 Chapter 20 I. Objective(s): By the end of today s lesson, the student will

Exercise 2-1. Exercise 2-2. Exercise 2-3. Name. = Liabilitiy Acounts + Debit Credit. Asset Acounts. Stockholders Equity Acounts Debit. Credit.

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

FUNDAMENTAL ACCOUNTING (01) Regional 2013

Regional 2013") Page 1 of 11 Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Secondary Regional 2013 Multiple Choice Account Identification Problem 1 Journalizing Problem 2 Income Statement Problem 3 Closing Entries

Page 1 of 11 Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Secondary Regional 2013 Multiple Choice Account Identification Problem 1 Journalizing Problem 2 Income Statement Problem 3 Closing Entries

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting I PRECISION EXAMS DESCRIPTION. EXAM INFORMATION Items

PRECISION EXAMS EXAM INFORMATION Items 67 Points 73 Prerequisites NONE Course Length ONE SEMESTER DESCRIPTION The first summative assessment in a series, measures the knowledge and skills necessary for

PRECISION EXAMS EXAM INFORMATION Items 67 Points 73 Prerequisites NONE Course Length ONE SEMESTER DESCRIPTION The first summative assessment in a series, measures the knowledge and skills necessary for

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Accounting 1. Lesson Plan. Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

> DO IT! Chapter 2 The Recording Process. Recording Business Activities D-7

Chapter 2 The Recording Process Normal Balances Kate Browne has just rented space in a shopping mall. In this space, she will open a hair salon to be called Hair It Is. A friend has advised Kate to set

Chapter 2 The Recording Process Normal Balances Kate Browne has just rented space in a shopping mall. In this space, she will open a hair salon to be called Hair It Is. A friend has advised Kate to set

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Assessment Schedule 2011 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224)

") NEA Level 2 Accounting (90224) 2011 page 1 of 6 Assessment Schedule 2011 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Statement Part A $ $ Bowling

NEA Level 2 Accounting (90224) 2011 page 1 of 6 Assessment Schedule 2011 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Statement Part A $ $ Bowling

LESSON Recording A Payroll. CENTURY 21 ACCOUNTING Thomson/South-Western

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

LESSON 2-1. Departmental Sales on Account and Sales Returns and Allowances. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

LESSON 2-1 Departmental Sales on Account and Sales Returns and Allowances 2 Departmental Sales on Account Sales on account are recorded by department in order to help management make decisions Sales on

LESSON 2-1 Departmental Sales on Account and Sales Returns and Allowances 2 Departmental Sales on Account Sales on account are recorded by department in order to help management make decisions Sales on

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY. Y. Chang Company COVER SHEET

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

Chapter 2. Ex a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit. Ex.

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

HS Accounting I 2013 Business and Technology

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Chapter 2: Measurement Concepts: Recording Business Transactions

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Consolidated Balance Sheet (Law No Section 33)

") ASSETS Page 1 of 5 A. CASH AND DUE FROM BANKS 13.359.149 10.276.572.Cash 2.582.869 2.815.005.Banks and Correspondents 10.776.280 7.461.567.BCRA 10.490.468 7.227.804.Other Argentine 33.118 37.752.Foreign

ASSETS Page 1 of 5 A. CASH AND DUE FROM BANKS 13.359.149 10.276.572.Cash 2.582.869 2.815.005.Banks and Correspondents 10.776.280 7.461.567.BCRA 10.490.468 7.227.804.Other Argentine 33.118 37.752.Foreign

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

The General Ledger. The 4 th step of the accounting cycle is to post to the ledger.

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chapter 5: Cash Control Systems

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

ACCOUNTING LIFEPAC 10 BUSINESS SIMULATION

Unit 10 ACCOUNTING LIFEPAC 10 BUSINESS SIMULATION CONTENTS BUSINESS SIMULATION FOR LARSON S TOURS Introduction........................................ 3 Chart of Accounts...................................

Unit 10 ACCOUNTING LIFEPAC 10 BUSINESS SIMULATION CONTENTS BUSINESS SIMULATION FOR LARSON S TOURS Introduction........................................ 3 Chart of Accounts...................................

Basic Book-keeping Skills for Learners

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum Learning Resources Corner Course 1: Contemporary Perspectives on Accounting

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum Learning Resources Corner Course 1: Contemporary Perspectives on Accounting

MATH WORK SHEET CHAPTER 4

Math Work Sheets and Solutions 1 Name Date Class CHAPTER 4 Calculating New Account Balances Calculate and record the new balance for each of the following accounts. ACCOUNT Cash ACCOUNT NO. 110.... 1,

Math Work Sheets and Solutions 1 Name Date Class CHAPTER 4 Calculating New Account Balances Calculate and record the new balance for each of the following accounts. ACCOUNT Cash ACCOUNT NO. 110.... 1,

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Organizational Structures & Journaling Notes. 1. List the 3 types of business ownership. a. Sole proprietorship

Organizational Structures & Journaling Notes 1. List the 3 types of business ownership. a. Sole proprietorship b. Partnership c. Corporation 2. How does the ownership differ between each type of ownership?

Organizational Structures & Journaling Notes 1. List the 3 types of business ownership. a. Sole proprietorship b. Partnership c. Corporation 2. How does the ownership differ between each type of ownership?

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Activity 1: Transactions

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Accounting for Merchandising Businesses

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Ch.6 Internal Control and Accounting for Cash

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases