1Q14 MACRO THEMES MACRO TEAM. Updated for March 19, 2014

|

|

|

- Jeffery Jones

- 5 years ago

- Views:

Transcription

1 1Q14 MACRO THEMES MACRO TEAM Updated for March 19, 2014

2 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not make investment recommendations. This research does not constitute an offer to sell, or a solicitation of an offer to buy any security. This research is presented without regard to individual investment preferences or risk parameters; it is general information and does not constitute specific investment advice. This presentation is based on information from sources believed to be reliable. Hedgeye Risk Management is not responsible for errors, inaccuracies or omissions of information. The opinions and conclusions contained in this report are those of Hedgeye Risk Management, and are intended solely for the use of Hedgeye Risk Management s clients and subscribers. In reaching these opinions and conclusions, Hedgeye Risk Management and its employees have relied upon research conducted by Hedgeye Risk Management s employees, which is based upon sources considered credible and reliable within the industry. Hedgeye Risk Management is not responsible for the validity or authenticity of the information upon which it has relied. TERMS OF USE This report is intended solely for the use of its recipient. Re-distribution or republication of this report and its contents are prohibited. For more detail please refer to the appropriate sections of the Hedgeye Services Agreement and the Terms of Use at HEDGEYE 2

3 PROCESS SLIDE #1 OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT DIFFERENTIATED FROM THE HERD Macroeconomics and Global Macro Risk Management are two very different fields. We specialize in the latter. WE FOCUS ON THE SLOPES Everything that matters in Global Macro occurs on the margin. HEDGEYE 3

4 PROCESS SLIDE #2 OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT OUR FUNDAMENTAL PROCESS If you get the slopes of both growth and inflation right, you ll tend to get a lot of other things right particularly in your P&L. HISTORY MATTERS Analyzing intermediate-term trends within the context of long-term economic and political cycles helps us consistently front-run major asset class turns. HEDGEYE 4

5 PROCESS SLIDE #3 HEDGEYE QUANTITATIVE SETUP: US EQUITIES 1,900 S&P 500 TREND = 1813 TAIL = ,850 1,800 1,750 1,700 1,650 1,600 1,550 1,500 Data Source: Bloomberg ALL BACKSTOPPED BY A PROVEN QUANTITATIVE OVERLAY Multi-factor: Price, Volume and Volatility Multi-duration: TRADE (3 weeks or less), TREND (3 months or more) and TAIL (3 years or less) HEDGEYE 5

6 #INFLATIONACCELERATING

7 ARE COMMODITIES BASING? HEDGEYE QUANTITATIVE SETUP: COMMODITY COMPLEX 375 CRB INDEX TREND = 288 TAIL = Data Source: Bloomberg HEDGEYE 7

6% 40% 5% 30% 20% 4% 10% 3% 0% 2% -10% -20% -30% -40% -50% It s")

8 COMMODITY BASE EFFECT TAILWIND GLOBALLY, CPI READINGS SHOULD COME IN AT LEAST +100 BASIS POINTS HIGHER OVER THE INTERMEDIATE TERM 50% Thomson/Reuters CRB Commodities Index, Monthly Average YoY Compounded at +3% per Month From Here Compounded at +1% per Month From Here Median YoY CPI Reading of US, Eurozone and China (rhs) 6% 40% 5% 30% 20% 4% 10% 3% 0% 2% -10% -20% -30% -40% -50% It s worth noting that 0% YoY for the CRB Index corresponds perfectly with +2% for our CPI sample and +2% is a common goal for Price Stability among central banks. 1% 0% -1% -2% Data Source: Bloomberg. Forecasts for the CRB Index assume no change to current prices unless otherwise noted. HEDGEYE 8

3.2% 1.1x 3.2% 1.0x 3.2% 3.2% 3.1% 3.1% 1.0x 0.8x 0.9x 2.8% 0.1x 0.6x 3.1% 0.6x 2.9% 0.2x 2.6% 2.6% -0.4x -1.0x 2.5% 4% 3% 3% 2% 2% 1% -2.")

9 1.5x 1.0x 0.5x 0.0x -0.5x -1.0x -1.5x PLUS, COMPS GET EASIER GLOBALLY 3.1% 0.1x 2.8% 2.8% -0.5x Z-SCORE (TRAILING 3Y) OF SELECTED COMPARATIVE BASE (2Y COMP) FOR THE RESPECTIVE CPI REPORTING PERIOD -0.5x 2.4% -1.4x 2.1% 1.7% 1.4% 2.2% -0.7x WORLD 2Y COMP (rhs) 3.2% 1.1x 3.2% 1.0x 3.2% 3.2% 3.1% 3.1% 1.0x 0.8x 0.9x 2.8% 0.1x 0.6x 3.1% 0.6x 2.9% 0.2x 2.6% 2.6% -0.4x -1.0x 2.5% 4% 3% 3% 2% 2% 1% -2.0x -1.7x -1.9x -1.8x Recall that this period was the postcrisis peak in reported inflation globally. -1.7x 1% -2.5x 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 0% HEDGEYE 9

10 THE ACCELERATION HAS COMMENCED HEDGEYE 10

11 CRUDE OIL IS A WILD CARD HEDGEYE QUANTITATIVE SETUP: CRUDE OIL 113 BRENT CRUDE OIL ($/bbl.) TREND = TAIL = Data Source: Bloomberg HEDGEYE 11

12 THE DOLLAR IS AMERICA'S PROBLEM HEDGEYE QUANTITATIVE SETUP: US DOLLAR INDEX 85 US DOLLAR INDEX TREND = TAIL = Data Source: Bloomberg HEDGEYE 12

13 $USD DRIVES ENERGY/FOOD PRICES U.S. DOLLAR VS. FOOD & ENERGY INFLATION 10Y, MONTHLY Down Dollar almost always results in commodity inflation 20% 15% Food & Energy Inflation, YoY % INFLATION UP INFLATION DOWN -20% -15% -10% -5% 10% 5% 0% -5% -10% -15% 0% y = x x R² = % 10% 15% 20% 25% DOLLAR DOWN DXY (U.S. Dollar), YoY % DOLLAR UP HEDGEYE 13

14 & HEADLINE CPI TRACKS NON-CORE Headline CPI, Sequential Change in YoY % -15% HEADLINE CPI TRACKS THE SLOPE OF FOOD & ENERGY INFLATION 10Y, MONTHLY -10% -5% 3% 2% 1% 0% -1% -2% -3% 0% y = 0.227x + 5E-05 R² = Food & Energy Inflation, Sequential Change in YoY % 5% 10% HEDGEYE 14

15 SEASONALITY IN EXPECTATIONS SEASONALITY HAS DRIVEN INFLATION EXPECTATIONS IN RECENT YEARS 5Y Breakeven (LH Axis) CPI, YoY % (RH Axis)? 4.50% 4.00% 3.50% 3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00% HEDGEYE 15

16 INFLATIONARY PRESSURES BUILDING 20.0% CPI COMPS EASE WHILE CAPACITY UTILIZATION, SERVICES INFLATION, WAGE AND CREDIT GROWTH ARE BEGINNING TO BREAKOUT Household Debt, YoY % Private Sector Salaries & Wages, 2Y Ave Capacity Utilization, 2Y Ave (RH Axis) CPI, 2Y Ave CPI: Services less Energy, 2Y Ave % % % % % 65 HEDGEYE 16

17 NOT JUST A U.S. PROBLEM 50% 40% 30% 20% 10% 0% -10% -20% -30% -40% -50% -60% Jan-04 Apr-04 Jul-04 Oct-04 Jan-05 Apr-05 THE DOLLAR DRIVES COMMODITY INFLATION GLOBALLY NEGATIVE FOR COUNTRIES WHOSE CPI BASKET IS OVERWEIGHT COMMODITIES Jul-05 Oct-05 Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 CRB Index, YoY % DXY, YoY % Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 HEDGEYE 17

18 OVERWEIGHT TECH, ENERGY AND UTES AVERAGE PERFORMANCE OF SELECTED INDICES ACCORDING TO HEDGEYE MACRO GIP QUADRANT 7.0% Quad #2: Growth Accelerates as Inflation Accelerates Quad #3: Growth Slows as Inflation Accelerates Average 6.5% 6.0% 5.0% 4.5% 4.0% 3.0% 2.0% 1.0% 0.0% 1.4% 1.2% 1.0% 2.9% 1.7% 1.7% 1.1% 0.5% 0.6% 2.2% 3.6% 2.9% 1.1% 0.6% 0.2% 3.7% 3.1% 2.3% 2.0% 1.0% 0.9% 2.4% 0.8% 0.5% 0.1% 3.1% 0.7% -1.0% -2.0% -1.7% -3.0% S&P 500 S&P 500 Consumer Discretionary Index S&P 500 Consumer Staples Index S&P 500 Energy Index S&P 500 Financials Index S&P 500 Health Care Index S&P 500 Industrials Index S&P 500 Information Technology Index S&P 500 Materials Index S&P 500 Utilities Index HEDGEYE 18

19 CAN GROWTH WORK WITHOUT #RATESRISING? INTERMEDIATE-TERM PERFORMANCE OF SELECT STYLE FACTORS (TOP AND BOTTOM DECILES OF THE S&P 500 INDEX) HIGH Long-term EPS Growth HIGH NTM Sales Growth US Treasury 10Y Yield (%) Data Source: Bloomberg HEDGEYE 19

20 SPREADS CAN STILL COMPRESS 6.00 CORPORATE SPREADS STILL HAVE SOME ROOM TO TIGHTEN IG SPREAD (Corp BBB over 10Y Treasury Yield) Current LOW HEDGEYE 20

21 #GROWTHDIVERGENCES

22 ARE THE US AND JAPAN PEAKING? REAL GDP (YOY % CHANGE) 10.0 t₀-3q t₀-2q t₀-1q Latest Print (2.0) (1.2) (0.6) (1.6) (4.0) China (4Q13) Eurozone (4Q13) Germany (4Q13) Japan (4Q13) UK (4Q13) USA (4Q13) Data Source: Bloomberg HEDGEYE 22

23 1.5x EASY COMPS VS. HARD COMPS Z-SCORE (TRAILING 3Y) OF SELECTED COMPARATIVE BASE (2Y COMP) FOR THE RESPECTIVE GDP REPORTING PERIOD 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 1.2x 1.0x 0.8x 1.0x 0.7x 0.9x 0.9x 0.9x 0.7x 0.5x 0.4x 0.4x 0.1x 0.2x 0.3x 0.5x 0.5x 0.5x 0.4x 0.4x 0.4x 0.3x 0.3x 0.2x 0.0x -0.5x -0.4x -0.2x -0.5x -0.6x -1.0x -1.5x -0.9x -1.2x -1.2x -1.4x -1.5x -1.5x -1.0x -1.1x -0.9x -0.9x -2.0x China Eurozone Germany Japan United Kingdom United States Data Source: Bloomberg HEDGEYE 23

24 JAPAN IN POLE POSITION INDUSTRIAL PRODUCTION (YOY % CHANGE) 12.0 Trailing 12M Average Trailing 6M Average Trailing 3M Average Latest Print (0.3) (2.0) China (12/2013) Eurozone (1/2014) Germany (1/2014) Japan (1/2014) UK (1/2014) USA (2/2014) Data Source: Bloomberg HEDGEYE 24

25 STRONG POUND = STRONG UK CONSUMER RETAIL SALES (YOY % CHANGE) Trailing 12M Average Trailing 6M Average Trailing 3M Average Latest Print (0.6) (2.0) China (12/2013) Eurozone (1/2014) Germany (1/2014) Japan (1/2014) UK (1/2014) USA (2/2014) Data Source: Bloomberg HEDGEYE 25

26 CHINA SLOWING WHERE IT MATTERS MANUFACTURING PMI Trailing 12M Average Trailing 6M Average Trailing 3M Average Latest Print China (2/2014) Eurozone (2/2014) Germany (2/2014) Japan (2/2014) UK (2/2014) USA (2/2014) Data Source: Bloomberg HEDGEYE 26

27 #EUROBULLS NON-MANUFACTURING PMI Trailing 12M Average Trailing 6M Average Trailing 3M Average Latest Print China (2/2014) Eurozone (2/2014) Germany (2/2014) Japan (N/A) UK (2/2014) USA (2/2014) Data Source: Bloomberg HEDGEYE 27

28 GERMAN CONFIDENCE CLIMBING BENCHMARK CONSUMER CONFIDENCE INDEX Trailing 12M Average Trailing 6M Average Trailing 3M Average Latest Print (10.0) (30.0) China (NBS; 1/2014) Data Source: Bloomberg (13.7) (12.7) (16.8) Eurozone (European Commission; 2/2014) (10.0) -9.0 (7.0) (15.0) Germany (GFK; 2/2014) Japan (ESRI; 2/2014) UK (GFK; 2/2014) USA (Conference Board; 2/2014) HEDGEYE 28

29 WILL THE EUROZONE FOLLOW GERMANY'S LEAD? BENCHMARK BUSINESS CONFIDENCE INDEX Trailing 12M Average Trailing 6M Average Trailing 3M Average Latest Print (15.0) (35.0) (40.2) (55.0) (54.2) (75.0) (65.2) China (NBS; 12/2013) Eurozone (ZEW; 2/2014) Germany (IFO; 1/2014) Japan (Tankan; 12/2013) UK (Lloyds Bank; 1/2014) USA (NFIB; 1/2014) Data Source: Bloomberg HEDGEYE 29

30 US: HEADING TOWARDS QUAD #3 HEDGEYE 30

31 TRENDS ARE NEGATIVE; WILL THEY INFLECT? BLAME THE WEATHER? HEDGEYE 31

32 JAPAN: RECOVERY LOSING STEAM? HEDGEYE 32

33 CHINA: #GROWTHSTABILIZING? HEDGEYE 33

34 EUROZONE: #GROWTHACCELERATING HEDGEYE 34

35 GERMANY: #GROWTHACCELERATING HEDGEYE 35

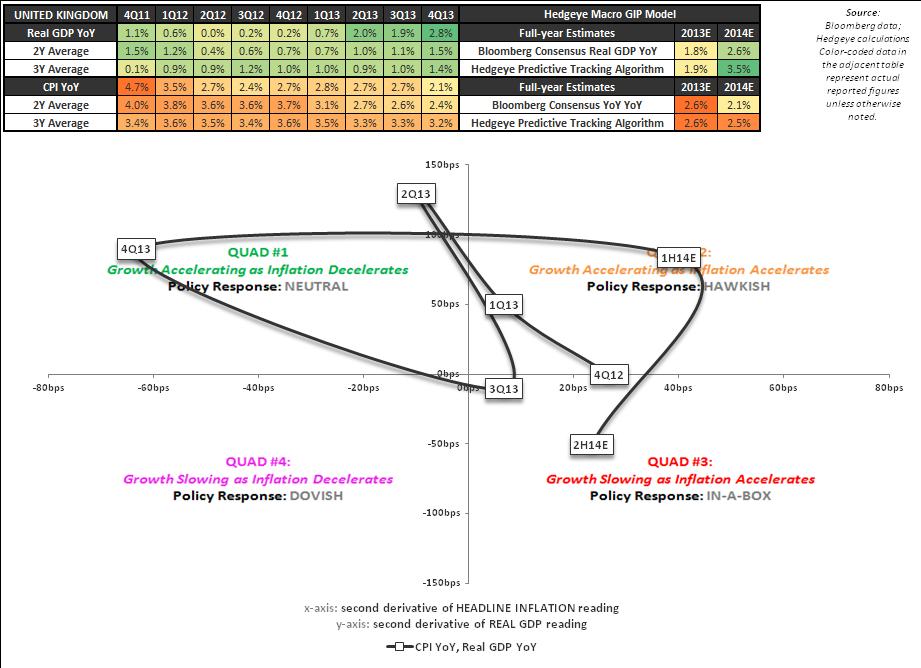

36 UK: #GROWTHACCELERATING HEDGEYE 36

37 #FLOWSHOW

38 3 TO 1 DEBT TO EQUITY HEDGEYE 38

39 BOND ALLOCATIONS TO MEAN REVERT LOWER 80% 70% 60% 50% 40% 30% 20% 10% 0% Ratio of Outstanding U.S. Bonds v. Outstanding U.S. Stocks In the year 1999 the ratio was 50/50% Now the ratio is 67/33% bonds to stocks U.S. Stocks Market Cap/Market Cap of Stocks & Bonds U.S. Bonds Market Cap/Market Cap of Stocks & Bonds DATA SOURCE: SIFMA; WILSHIRE 5000 HEDGEYE 39

40 FLOWS CHASE PERFORMANCE 50% 1 YR Performance 2 YR Performance 3 YR Performance 45% 43% 40% 35% 36% 30% 28% 25% 20% 20% 22% 15% 15% 10% 8% 9% 5% 0% S&P500 2% 0% 5% Bloomberg Global DM Sovereign Debt Bloomberg Global IG Corporate Index Index 4% Bloomberg Global HY Corporate Index HEDGEYE 40

41 BONDS: 1ST NEG. RETURN IN 14 YEARS HEDGEYE 41

42 = RECORD NOMINAL BOND FUND OUTFLOWS SOURCE: HEDGEYE FINANCIALS TEAM HEDGEYE 42

43 BUT THIS IS STILL THE SMALLEST OUTFLOW IN HISTORY ON A % BASIS 16.0% 14.0% Historical Fixed Income Outflows on Beginning Bond Fund AUM 14.0% 12.0% 10.0% 8.0% 6.0% 2013 saw a record net outflow from bond funds in nominal terms ($86B), yet as a percentage of starting AUM, 2013 s outflow was less than half the median outflow episode over the past 20Y! 5.0% 5.0% 4.0% 2.0% 2.3% 0.0% HEDGEYE 43

44 REVIEWING THE 1994 TURN: #CRITICAL HEDGEYE 44

45 TAPER = #RATESRISING HEDGEYE 45

46 #ASYMMETRY: THE QUEEN MARY CAN TURN! 16% U.S. GOVT 10 YR Bond Yield TAIL SUPPORT = 2.56% 50 YR Avg. 14% 12% 10% 8% 6% 4% 2% 0% HEDGEYE 46

47 DO YOU KNOW WHAT BOND OUTFLOWS LOOK LIKE? $3.00 $2.50 $2.00 $1.50 $1.00 $0.50 $- $(0.50) $(1.00) $(1.50) $(2.00) Net Inflow into Bonds versus Citi Big Bond Index Performance 16% 14% 12% 10% 8% 6% 4% 2% 0% -2% -4% 3 month Mov. Avg Bond flow over most recent month's beginning assets Y-o-Y total return on Citi Big Bond Index HEDGEYE 47

48 HOW ABOUT EQUITY INFLOWS? $50 $40 $30 $20 $10 $- $(10) $(20) $(30) $(40) Net Inflow into Stocks versus MSCI Global Stock Index Performance 80% 60% 40% 20% 0% -20% -40% -60% 6 month Mov. Avg of Global Equity Flow $BB Y-o-Y total return on MSCI Index HEDGEYE 48

49 INVESTMENT CONCLUSIONS LONGS OLD FORMAT = $800/SQUARE FT Bonds (BND) Long-term Treasuries (TLT) Gold (GLD) Commodities (DBC) Utilities (XLU) SHORTS NEW FORMAT = $1,300 SQ FT Kinder Morgan (KMI) Nationstar Mortgage Holdings (NSM) Potbelly (PBPB) US Consumer Discretionary (XLY) US Consumer Staples (XLP) HEDGEYE 49

50 FOR MORE INFORMATION CONTACT:

U.S. ECONOMIC UPDATE. MACRO February 5, 2014

U.S. ECONOMIC UPDATE MACRO February 5, 2014 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker

U.S. ECONOMIC UPDATE MACRO February 5, 2014 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker

ACTUALLY, VALUATION IS NOT A CATALYST

Hedgeye CEO & Founder: Keith McCullough ACTUALLY, VALUATION IS NOT A CATALYST November 7 th, 2017 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State

Hedgeye CEO & Founder: Keith McCullough ACTUALLY, VALUATION IS NOT A CATALYST November 7 th, 2017 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State

The Macro Show. Hedgeye Risk Management LLC

Hedgeye Risk Management LLC LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does

Hedgeye Risk Management LLC LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does

The Macro Show. Hedgeye Risk Management LLC

Hedgeye Risk Management LLC LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does

Hedgeye Risk Management LLC LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does

The Macro Show. Hedgeye Risk Management LLC

Hedgeye Risk Management LLC LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does

Hedgeye Risk Management LLC LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does

LEGAL DISCLAIMER TERMS OF USE

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM APRIL 22, 2015 UPDATE LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM APRIL 22, 2015 UPDATE LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM AUGUST 19, 2015 UPDATE LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM AUGUST 19, 2015 UPDATE LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management

LEGAL DISCLAIMER TERMS OF USE

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

LEGAL DISCLAIMER TERMS OF USE

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

The Asia Pacific Fund, Inc.

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

JONATHAN CASTELEYN, CFA JOSHUA STEINER, CFA LAZARD (LAZ) CYCLICAL COMPANY MODELED AS SECULAR. January 2016

CYCLICAL COMPANY MODELED AS SECULAR. January 2016") JONATHAN CASTELEYN, CFA JOSHUA STEINER, CFA LAZARD (LAZ) CYCLICAL COMPANY MODELED AS SECULAR January 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with

JONATHAN CASTELEYN, CFA JOSHUA STEINER, CFA LAZARD (LAZ) CYCLICAL COMPANY MODELED AS SECULAR January 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with

MACRO CHART BOOK Q2, 2016

Adaptive Investing MACRO CHART BOOK Q2, 2016 Upside Participation Downside Management For Investment Advisors and Institutions Only Content Summary US Economy Market Snapshot Asset Class Performance Equity

Adaptive Investing MACRO CHART BOOK Q2, 2016 Upside Participation Downside Management For Investment Advisors and Institutions Only Content Summary US Economy Market Snapshot Asset Class Performance Equity

THE GIG ECONOMY IS ALIVE AND GROWING

ABOUT EVERYTHING WITH NEIL HOWE THE GIG ECONOMY IS ALIVE AND GROWING THE NUMBER OF U.S. WORKERS WITH IRREGULAR JOBS IS INCREASING. August 9, 2016 LEGAL DISCLAIMER Hedgeye Risk Management is a registered

ABOUT EVERYTHING WITH NEIL HOWE THE GIG ECONOMY IS ALIVE AND GROWING THE NUMBER OF U.S. WORKERS WITH IRREGULAR JOBS IS INCREASING. August 9, 2016 LEGAL DISCLAIMER Hedgeye Risk Management is a registered

Hedgeye Risk Management LLC. All Rights Reserved.

DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment

DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment

The Compelling Case for Value

The Compelling Case for Value July 2, 2018 SOLELY FOR THE USE OF INSTITUTIONAL INVESTORS AND PROFESSIONAL ADVISORS 0 Jan-75 Jan-77 Jan-79 Jan-81 Jan-83 Jan-85 Jan-87 Jan-89 Jan-91 Jan-93 Jan-95 Jan-97

The Compelling Case for Value July 2, 2018 SOLELY FOR THE USE OF INSTITUTIONAL INVESTORS AND PROFESSIONAL ADVISORS 0 Jan-75 Jan-77 Jan-79 Jan-81 Jan-83 Jan-85 Jan-87 Jan-89 Jan-91 Jan-93 Jan-95 Jan-97

Key takeaways. What it may mean for investors WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS. Veronica Willis Investment Strategy Analyst

Veronica Willis Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS May 8, 2018 Monetary Policy Divergence Could Last a Little Longer Key takeaways» Recent economic improvement

Veronica Willis Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS May 8, 2018 Monetary Policy Divergence Could Last a Little Longer Key takeaways» Recent economic improvement

December 2014 Economic Outlook. All data as of November 30, 2014 unless otherwise noted.

December 2014 Economic Outlook All data as of November 30, 2014 unless otherwise noted. -4-2 0 2 4 6 8 10 12 14 16 18 20 22 24 Economic Outlook and Capital Markets Slow growth has characterized the current

December 2014 Economic Outlook All data as of November 30, 2014 unless otherwise noted. -4-2 0 2 4 6 8 10 12 14 16 18 20 22 24 Economic Outlook and Capital Markets Slow growth has characterized the current

MACAU REVIEW AND OUTLOOK SHORT TERM GAIN, LONG TERM????

MACAU REVIEW AND OUTLOOK SHORT TERM GAIN, LONG TERM???? GAMING/LODGING/LEISURE TEAM (Todd Jordan and Felix Wang) October 8, 2015 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor,

MACAU REVIEW AND OUTLOOK SHORT TERM GAIN, LONG TERM???? GAMING/LODGING/LEISURE TEAM (Todd Jordan and Felix Wang) October 8, 2015 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor,

[ ] WEEKLY CHANGES AGAINST THE USD

![[ ] WEEKLY CHANGES AGAINST THE USD](/thumbs/82/86622399.jpg "[ ] WEEKLY CHANGES AGAINST THE USD") February 19, 2018 [ ] MACRO & MARKETS COMMENTARY» Last week, Global stock markets witnessed one of their best weeks in almost six years after two consecutive weeks in the red. The last week rally was mainly

February 19, 2018 [ ] MACRO & MARKETS COMMENTARY» Last week, Global stock markets witnessed one of their best weeks in almost six years after two consecutive weeks in the red. The last week rally was mainly

MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2

10 2 3 6 8 9 13 14 MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2 Alpha Current Previous Alpha Current Previous Alpha Current Previous weight weight weight weight weight

10 2 3 6 8 9 13 14 MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2 Alpha Current Previous Alpha Current Previous Alpha Current Previous weight weight weight weight weight

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Impact of Potential Normalization of Interest Rates and Inflation on Global Sectors

Impact of Potential Normalization of Interest Rates and Inflation on Global Sectors ANTONIO DOCAL, CFA Executive Vice President Portfolio Manager, Research Analyst Templeton Global Equity Group Templeton

Impact of Potential Normalization of Interest Rates and Inflation on Global Sectors ANTONIO DOCAL, CFA Executive Vice President Portfolio Manager, Research Analyst Templeton Global Equity Group Templeton

Investment Challenges & Opportunities in the Current Environment

Investment Challenges & Opportunities in the Current Environment John Augustine, CFA Chief Economic & Market Strategist Fifth Third Bank March 213 Fifth Third Bank All Rights Reserved Fifth Third Bank

Investment Challenges & Opportunities in the Current Environment John Augustine, CFA Chief Economic & Market Strategist Fifth Third Bank March 213 Fifth Third Bank All Rights Reserved Fifth Third Bank

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

Key Commodity Themes. Maxwell Gold Director of Investment Strategy. Gradient Investments Elite Advisor Forum October 5 th, 2017

Key Commodity Themes Maxwell Gold Director of Investment Strategy Gradient Investments Elite Advisor Forum October 5 th, 2017 2001 2002 2002 2003 2004 2005 2006 2007 2007 2008 2009 2010 2011 2012 2012

Key Commodity Themes Maxwell Gold Director of Investment Strategy Gradient Investments Elite Advisor Forum October 5 th, 2017 2001 2002 2002 2003 2004 2005 2006 2007 2007 2008 2009 2010 2011 2012 2012

2011 Ringgit Bond Market Outlook

211 Ringgit Bond Market Outlook Wan Murezani Wan Mohamad Head Fixed Income Research 211 Investor Briefing 22 March 211 MALAYSIAN RATING CORPORATION BERHAD Clarity and Integrity www.marc.com.my Disclaimer

211 Ringgit Bond Market Outlook Wan Murezani Wan Mohamad Head Fixed Income Research 211 Investor Briefing 22 March 211 MALAYSIAN RATING CORPORATION BERHAD Clarity and Integrity www.marc.com.my Disclaimer

MAY 2018 Capital Markets Update

MAY 2018 Market commentary U.S. ECONOMICS The U.S. added 223,000 jobs to payrolls in May, well above the consensus estimate of 180,000 and the expansion average of around 200,000. Sector job gains were

MAY 2018 Market commentary U.S. ECONOMICS The U.S. added 223,000 jobs to payrolls in May, well above the consensus estimate of 180,000 and the expansion average of around 200,000. Sector job gains were

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM JUNE 17, 2015 UPDATE LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management

MACRO PLAYBOOK DARIUS DALE: MACRO TEAM JUNE 17, 2015 UPDATE LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management

Global House View: Market Outlook

HSBC GLOBAL ASSET MANAGEMENT September 29 Global House View: Market Outlook Contents 1688/HSB1395a Market performance Macro-economic Picture Market Views: high level asset allocation Market Views: Equity

HSBC GLOBAL ASSET MANAGEMENT September 29 Global House View: Market Outlook Contents 1688/HSB1395a Market performance Macro-economic Picture Market Views: high level asset allocation Market Views: Equity

Quarterly Economic and Market Update

Quarterly Economic and Market Update September 2017 Presented by Global Manager Research Table of Contents Past performance shown on the following slides does not guarantee future results. Market Returns..

Quarterly Economic and Market Update September 2017 Presented by Global Manager Research Table of Contents Past performance shown on the following slides does not guarantee future results. Market Returns..

The Asset Allocation Decision

The Asset Allocation Decision Kevin Headland, CIM Senior Investment Strategist Manulife Investments Agenda A Diverse History of Asset Allocation Asset Allocation in Practice How it Fits in Today s Market

The Asset Allocation Decision Kevin Headland, CIM Senior Investment Strategist Manulife Investments Agenda A Diverse History of Asset Allocation Asset Allocation in Practice How it Fits in Today s Market

Tracking the Growth Catalysts in Emerging Markets

Tracking the Growth Catalysts in Emerging Markets September 14, 2016 by Nick Niziolek of Calamos Investments The following is an excerpt of remarks made on August 30, 2016. The majority of the improved

Tracking the Growth Catalysts in Emerging Markets September 14, 2016 by Nick Niziolek of Calamos Investments The following is an excerpt of remarks made on August 30, 2016. The majority of the improved

DISCLAIMER DISCLAIMER

DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment

DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment

SEPTEMBER 2018 Capital Markets Update

SEPTEMBER 2018 Market commentary U.S. ECONOMICS Non-farm payrolls added 134,000 jobs in September, missing the consensus estimate of 185,000. However, net revisions to the two months prior totaled +87,000

SEPTEMBER 2018 Market commentary U.S. ECONOMICS Non-farm payrolls added 134,000 jobs in September, missing the consensus estimate of 185,000. However, net revisions to the two months prior totaled +87,000

Macro Strategy Chartbook

Macro Strategy Chartbook June 2018 Executive Summary Valuation data are mixed: equities appear cheap relative to current earnings forecasts, but expensive longer term. Higher interest rates represent a

Macro Strategy Chartbook June 2018 Executive Summary Valuation data are mixed: equities appear cheap relative to current earnings forecasts, but expensive longer term. Higher interest rates represent a

> Macro Investment Outlook

> Macro Investment Outlook Dr Shane Oliver Head of Investment Strategy and Chief Economist October 214 The challenge for investors how to find better yield and returns as bank deposit rates stay low 9

> Macro Investment Outlook Dr Shane Oliver Head of Investment Strategy and Chief Economist October 214 The challenge for investors how to find better yield and returns as bank deposit rates stay low 9

The increasing importance of multi asset solutions genuine diversification to reduce total risk

The increasing importance of multi asset solutions genuine diversification to reduce total risk Ariconsult Vermögensverwaltungs-Symposium 17 September 2014 Richard Batty Fund Manager, Multi Asset This

The increasing importance of multi asset solutions genuine diversification to reduce total risk Ariconsult Vermögensverwaltungs-Symposium 17 September 2014 Richard Batty Fund Manager, Multi Asset This

Monthly Market Snapshot

ly Market Snapshot OCTOBER 2016 The ly Market Snapshot publication provides commentary on the global economy and the performance of financial markets Key insights Domestic and international equities (unhedged)

ly Market Snapshot OCTOBER 2016 The ly Market Snapshot publication provides commentary on the global economy and the performance of financial markets Key insights Domestic and international equities (unhedged)

Global Market Overview

First Quarter 219 First Quarter 219: March Madness, or Just an Incredible Rebound? Global Market Overview MSCI All Country World S&P Russell 2 MSCI EAFE MSCI Emerging Markets MSCI ACWI ex USA Small BBgBarc

First Quarter 219 First Quarter 219: March Madness, or Just an Incredible Rebound? Global Market Overview MSCI All Country World S&P Russell 2 MSCI EAFE MSCI Emerging Markets MSCI ACWI ex USA Small BBgBarc

Economic and Market Outlook

Economic and Market Outlook Fourth Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Fourth Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Navigating a maturing bull market

Navigating a maturing bull market Asia Pacific Wealth Management March 2018 INVESTMENT PRODUCTS: NOT A BANK DEPOSIT. NOT GOVERNMENT INSURED. NO BANK GUARANTEE. MAY LOSE VALUE Market Review Market Performance

Navigating a maturing bull market Asia Pacific Wealth Management March 2018 INVESTMENT PRODUCTS: NOT A BANK DEPOSIT. NOT GOVERNMENT INSURED. NO BANK GUARANTEE. MAY LOSE VALUE Market Review Market Performance

20,000 - Check, What s next?

1 11 21 31 41 51 61 71 81 91 101 111 121 131 141 151 161 171 181 191 201 211 221 231 241 251 20,000 - Check, What s next? The Dow Jones Industrial Average crossed the psychological 20,000 barrier on January

1 11 21 31 41 51 61 71 81 91 101 111 121 131 141 151 161 171 181 191 201 211 221 231 241 251 20,000 - Check, What s next? The Dow Jones Industrial Average crossed the psychological 20,000 barrier on January

State Street Global Advisors SPDR ETFs Chart Pack

State Street Global Advisors SPDR ETFs Chart Pack April 2018 Edition For Public Use Please see Appendix C for more information on investment terms used in this Chart Pack. Chart Pack Table of Contents

State Street Global Advisors SPDR ETFs Chart Pack April 2018 Edition For Public Use Please see Appendix C for more information on investment terms used in this Chart Pack. Chart Pack Table of Contents

Outlook for 2014 Title 1. David Greene, Pioneer Investments

Outlook for 2014 Title 1 David Greene, Pioneer Investments 2014 A year of Transition Transitioning from fiscal tightening to less austerity. Transitioning from Euro-area recession to growth. Transitioning

Outlook for 2014 Title 1 David Greene, Pioneer Investments 2014 A year of Transition Transitioning from fiscal tightening to less austerity. Transitioning from Euro-area recession to growth. Transitioning

Global Investment Outlook Russ Koesterich, CFA Managing Director, Global Allocation

Global Investment Outlook Russ Koesterich, CFA Managing Director, Global Allocation 6 Asset performance YTD Source: Thomson Reuters Datastream, BlackRock Investment Institute. Apr, 6 Note: Total return

Global Investment Outlook Russ Koesterich, CFA Managing Director, Global Allocation 6 Asset performance YTD Source: Thomson Reuters Datastream, BlackRock Investment Institute. Apr, 6 Note: Total return

WEEKLY CHANGES AGAINST THE USD MACRO & MARKETS COMMENTARY

July 31, 2017 [ W E E K LY E C O N O M I C C O M M E N TA R Y ] WEEKLY ANALYSIS FOR THE MOST CRITICAL ECONOMIC AND FINANCIAL DEVELOPMENTS MACRO & MARKETS COMMENTARY» Federal Open Market Committee (FOMC)

July 31, 2017 [ W E E K LY E C O N O M I C C O M M E N TA R Y ] WEEKLY ANALYSIS FOR THE MOST CRITICAL ECONOMIC AND FINANCIAL DEVELOPMENTS MACRO & MARKETS COMMENTARY» Federal Open Market Committee (FOMC)

[ ] WEEKLY CHANGES AGAINST THE USD

![[ ] WEEKLY CHANGES AGAINST THE USD](/thumbs/80/81644725.jpg "[ ] WEEKLY CHANGES AGAINST THE USD") February 26, 2018 [ ] MACRO & MARKETS COMMENTARY» Federal Reserve officials see the economic growth and the acceleration of inflation as a good signal to continue to raise interest rate gradually over

February 26, 2018 [ ] MACRO & MARKETS COMMENTARY» Federal Reserve officials see the economic growth and the acceleration of inflation as a good signal to continue to raise interest rate gradually over

Additional series available. Morningstar TM Rating. Funds in category 363. Fixed income % of fixed income allocation

Sun Life BlackRock Canadian Balanced Fund Investment objective Series A $12.4584 Net asset value per security (NAVPS) as of August 20, 2018 $0.0128 0.10% Benchmark Blended benchmark Fund category Canadian

Sun Life BlackRock Canadian Balanced Fund Investment objective Series A $12.4584 Net asset value per security (NAVPS) as of August 20, 2018 $0.0128 0.10% Benchmark Blended benchmark Fund category Canadian

MACAU PREMIUM MASS THE STANDOUT NOVEMBER 9, 2016

TEAM TODD MEMBER JORDAN ONE TEAM SEAN MEMBER JENKINS TWO FELIX TEAM MEMBER WANG, CFA THREE TEAM MEMBER FOUR MACAU PREMIUM MASS THE STANDOUT NOVEMBER 9, 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management

TEAM TODD MEMBER JORDAN ONE TEAM SEAN MEMBER JENKINS TWO FELIX TEAM MEMBER WANG, CFA THREE TEAM MEMBER FOUR MACAU PREMIUM MASS THE STANDOUT NOVEMBER 9, 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management

Tick, Tick, Tick. Presented by: Jeffrey Gundlach CEO, DoubleLine Capital

Tick, Tick, Tick Presented by: Jeffrey Gundlach CEO, DoubleLine Capital TAB I The Fed Pete Carroll Janet Yellen Worst Years of Major Asset Classes Source: Bianco Research S&P 500 Index = Standard & Poor

Tick, Tick, Tick Presented by: Jeffrey Gundlach CEO, DoubleLine Capital TAB I The Fed Pete Carroll Janet Yellen Worst Years of Major Asset Classes Source: Bianco Research S&P 500 Index = Standard & Poor

Investment Perspectives. From The Global Investment Committee

Investment Perspectives From The Global Investment Committee Global Risk Aversion Reached Extreme Levels Morgan Stanley Standardized Global Risk Demand Index As of October 15, 2014 Complacent Extreme Fear

Investment Perspectives From The Global Investment Committee Global Risk Aversion Reached Extreme Levels Morgan Stanley Standardized Global Risk Demand Index As of October 15, 2014 Complacent Extreme Fear

Investment Outlook. [presentation_date] Our investment teams discuss current market opportunities and risks.

![Investment Outlook. [presentation_date] Our investment teams discuss current market opportunities and risks.](/thumbs/73/69162772.jpg "Investment Outlook. [presentation_date] Our investment teams discuss current market opportunities and risks.") Investment Outlook Our investment teams discuss current market opportunities and risks. [presentation_date] ACI-1309929 Non-FDIC Insured May Lose Value No Bank Guarantee This material has been prepared

Investment Outlook Our investment teams discuss current market opportunities and risks. [presentation_date] ACI-1309929 Non-FDIC Insured May Lose Value No Bank Guarantee This material has been prepared

Global Market Outlook 2018

Global Market Outlook 2018 Belinda Boa Head of Active Investments Asia Pacific and CIO of Emerging Markets Fundamental Active Equity, BlackRock January 2018 FOR PROFESSIONAL AND INSTITUTIONAL INVESTORS

Global Market Outlook 2018 Belinda Boa Head of Active Investments Asia Pacific and CIO of Emerging Markets Fundamental Active Equity, BlackRock January 2018 FOR PROFESSIONAL AND INSTITUTIONAL INVESTORS

Navigating the Fixed Income Minefield

Navigating the Fixed Income Minefield Jeffrey Sherman, CFA Portfolio Manager DoubleLine Capital February 20, 2014 When all the experts and forecasts agree -- something else is going to happen. - Bob Farrell

Navigating the Fixed Income Minefield Jeffrey Sherman, CFA Portfolio Manager DoubleLine Capital February 20, 2014 When all the experts and forecasts agree -- something else is going to happen. - Bob Farrell

State Street Global Advisors SPDR ETFs Chart Pack

State Street Global Advisors SPDR ETFs Chart Pack May 2018 Edition For Public Use Please see Appendix C for more information on investment terms used in this Chart Pack. Chart Pack Table of Contents I.

State Street Global Advisors SPDR ETFs Chart Pack May 2018 Edition For Public Use Please see Appendix C for more information on investment terms used in this Chart Pack. Chart Pack Table of Contents I.

How do we define cash on the sidelines? Global M2 minus M1 Money Supply ($ Millions) US Money Supply European Money Supply Chinese Money Supply

US Money Supply European Money Supply Chinese Money Supply") How do we define cash on the sidelines? Global M2 minus M1 Money Supply ($ Millions) 30000 25000 20000 15000 US Money Supply European Money Supply Chinese Money Supply 10000 5000 0 Source: Bloomberg, Credit

How do we define cash on the sidelines? Global M2 minus M1 Money Supply ($ Millions) 30000 25000 20000 15000 US Money Supply European Money Supply Chinese Money Supply 10000 5000 0 Source: Bloomberg, Credit

[ ] WEEKLY CHANGES AGAINST THE USD

![[ ] WEEKLY CHANGES AGAINST THE USD](/thumbs/82/86622376.jpg "[ ] WEEKLY CHANGES AGAINST THE USD") January 22, 2018 [ ] MACRO & MARKETS COMMENTARY» The U.S economy and inflation expanded at a Modest to Moderate pace during December 2017, while wages continued to push higher according to the Federal

January 22, 2018 [ ] MACRO & MARKETS COMMENTARY» The U.S economy and inflation expanded at a Modest to Moderate pace during December 2017, while wages continued to push higher according to the Federal

Economic Groundhog Day

Economic Groundhog Day Early Signs of Spring or Six More Months/Years of Economic Winter? May 2009 Columbia Management Group, LLC ( Columbia Management ) is the investment management division of Bank of

Economic Groundhog Day Early Signs of Spring or Six More Months/Years of Economic Winter? May 2009 Columbia Management Group, LLC ( Columbia Management ) is the investment management division of Bank of

LEGAL DISCLAIMER TERMS OF USE

HEDGEYE 1 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment

HEDGEYE 1 LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment

The Multiple Mystery: At what P/E should the market trade?

October 1, 2009 United States: Portfolio Strategy US Equity Views The Multiple Mystery: At what P/E should the market trade? Investor focus has shifted from earnings to valuation. We are now most often

October 1, 2009 United States: Portfolio Strategy US Equity Views The Multiple Mystery: At what P/E should the market trade? Investor focus has shifted from earnings to valuation. We are now most often

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 11, 2015 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 11, 2015 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

INVESTMENT OUTLOOK JUNE 2018 MACRO-ECONOMICS. Developed and Emerging Markets

INVESTMENT OUTLOOK JUNE 2018 MACRO-ECONOMICS Developed and Emerging Markets Trade tariffs and protectionist themes have dominated global markets throughout the year and risks have further heightened through

INVESTMENT OUTLOOK JUNE 2018 MACRO-ECONOMICS Developed and Emerging Markets Trade tariffs and protectionist themes have dominated global markets throughout the year and risks have further heightened through

Fixed Income Investing in a Low Yield World: High Yield Bonds Still Part of the Solution. Fall 2012

Fixed Income Investing in a Low Yield World: High Yield Bonds Still Part of the Solution Fall 2012 U.S. 10-Year Treasury Yields October 5, 2012 16 14 12 10 8 6 4 2 1.74% 0 Jan-82 Feb-86 Mar-90 May-94 Jun-98

Fixed Income Investing in a Low Yield World: High Yield Bonds Still Part of the Solution Fall 2012 U.S. 10-Year Treasury Yields October 5, 2012 16 14 12 10 8 6 4 2 1.74% 0 Jan-82 Feb-86 Mar-90 May-94 Jun-98

Global Markets Update QNB Economics 19 February 2017

Global Markets Update QNB Economics 19 February 2017 Executive Summary Key Takeaways Yields in advanced economies were stable while local factors dominated emerging market performance The Egyptian pound

Global Markets Update QNB Economics 19 February 2017 Executive Summary Key Takeaways Yields in advanced economies were stable while local factors dominated emerging market performance The Egyptian pound

Total

The following report provides in-depth analysis into the successes and challenges of the Northcoast Tactical Growth managed ETF strategy throughout 2017, important research into the mechanics of the strategy,

The following report provides in-depth analysis into the successes and challenges of the Northcoast Tactical Growth managed ETF strategy throughout 2017, important research into the mechanics of the strategy,

Roger Yuan Goldman Sachs (Asia) L.L.C. (+852)

L.L.C. (+852)") Goldman Sachs Research Precious Metals Gold caught in a tug-of-war May 2014 Roger Yuan Goldman Sachs (Asia) L.L.C. (+852) 2978-6128 roger.yuan@gs.com The Goldman Sachs Group, Inc. does and seeks to do

Goldman Sachs Research Precious Metals Gold caught in a tug-of-war May 2014 Roger Yuan Goldman Sachs (Asia) L.L.C. (+852) 2978-6128 roger.yuan@gs.com The Goldman Sachs Group, Inc. does and seeks to do

2008 Economic and Market Outlook

Economic and Market Outlook Presented by: Gareth Watson Warren Jestin Vincent Delisle December 7 Economic Outlook Warren Jestin The Global Economic Landscape is Changing Rapidly Gears Down Emerging Powerhouses

Economic and Market Outlook Presented by: Gareth Watson Warren Jestin Vincent Delisle December 7 Economic Outlook Warren Jestin The Global Economic Landscape is Changing Rapidly Gears Down Emerging Powerhouses

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

QUARTERLY INVESTMENT STRATEGY Third Quarter 15 19 APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers EMERGING ECONOMIES Purchasing Managers US Eurozone Japan Brazil Russia India China

QUARTERLY INVESTMENT STRATEGY Third Quarter 15 19 APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers EMERGING ECONOMIES Purchasing Managers US Eurozone Japan Brazil Russia India China

ASSET ALLOCATION FLASH

FOR PROFESSIONAL INVESTORS 25 June 2018 ASSET ALLOCATION FLASH BNPP AM Multi Asset, Quantitative and Solutions (MAQS) MID-YEAR REVERSALS Asset allocation overview: Christophe MOULIN Head of Multi Asset,

FOR PROFESSIONAL INVESTORS 25 June 2018 ASSET ALLOCATION FLASH BNPP AM Multi Asset, Quantitative and Solutions (MAQS) MID-YEAR REVERSALS Asset allocation overview: Christophe MOULIN Head of Multi Asset,

State Street Global Advisors SPDR ETFs Chart Pack

State Street Global Advisors SPDR ETFs Chart Pack June 2018 Edition For Public Use Please see Appendix C for more information on investment terms used in this Chart Pack. Chart Pack Table of Contents I.

State Street Global Advisors SPDR ETFs Chart Pack June 2018 Edition For Public Use Please see Appendix C for more information on investment terms used in this Chart Pack. Chart Pack Table of Contents I.

FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED MEMBERS OF THE PRESS ONLY, NOT FOR FURTHER DISTRIBUTION.

2018 Global Market Outlook Press Briefing GLOBAL FIXED INCOME Mark Vaselkiv Portfolio Manager, CIO, Fixed Income November 14, 2017 FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED

2018 Global Market Outlook Press Briefing GLOBAL FIXED INCOME Mark Vaselkiv Portfolio Manager, CIO, Fixed Income November 14, 2017 FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED

LEGAL DISCLAIMER TERMS OF USE

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

LEGAL DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice

Economic, Business & Markets Focus on Investors

1//13 Economic, Business & Markets Focus on Investors John Augustine, CFA Chief Economic & Market Strategist Fifth Third Bank November 13 Fifth Third Bank All Rights Reserved Fifth Third Bank Overview

1//13 Economic, Business & Markets Focus on Investors John Augustine, CFA Chief Economic & Market Strategist Fifth Third Bank November 13 Fifth Third Bank All Rights Reserved Fifth Third Bank Overview

John Deehan - Investment Sales Manager

The investment cycle The return of volatility & The importance of being selective for multi asset investors in the current environment John Deehan - Investment Sales Manager Multi-Asset Choice Cost efficient

The investment cycle The return of volatility & The importance of being selective for multi asset investors in the current environment John Deehan - Investment Sales Manager Multi-Asset Choice Cost efficient

B-GUIDE: Market Outlook

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

MARCH 2018 Capital Markets Update

MARCH 2018 Market commentary ECONOMIC CLIMATE Hiring slowed from its fast pace last month the U.S. added 103,000 jobs to nonfarm payrolls in March, below the consensus estimate of 185,000. The U-3 unemployment

MARCH 2018 Market commentary ECONOMIC CLIMATE Hiring slowed from its fast pace last month the U.S. added 103,000 jobs to nonfarm payrolls in March, below the consensus estimate of 185,000. The U-3 unemployment

US Economic Outlook Improving

Government Bonds Have Never Looked Less Attractive OUTLOOK Executive Summary Kenneth J. Taubes Chief Investment Officer, US Economic Outlook US GDP growth may lead growth among developed nations, at approximately

Government Bonds Have Never Looked Less Attractive OUTLOOK Executive Summary Kenneth J. Taubes Chief Investment Officer, US Economic Outlook US GDP growth may lead growth among developed nations, at approximately

[ ] WEEKLY CHANGES AGAINST THE USD

![[ ] WEEKLY CHANGES AGAINST THE USD](/thumbs/78/77362224.jpg "[ ] WEEKLY CHANGES AGAINST THE USD") January 15, 2018 [ ] MACRO & MARKETS COMMENTARY» The European central bank (ECB) has indicated it should revisit its communication stance in early 2018, according to the ECB s minutes of December meeting

January 15, 2018 [ ] MACRO & MARKETS COMMENTARY» The European central bank (ECB) has indicated it should revisit its communication stance in early 2018, according to the ECB s minutes of December meeting

INVESTMENT OUTLOOK. August 2017

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

Portfolio Discussions

MARKET INSIGHTS UK Q1 2018 Portfolio Discussions Considering trends and opportunities for investors with Guide to the Markets CONTENTS in the UK 2 in emerging markets 8 in Europe 14 in the US 20 Global

MARKET INSIGHTS UK Q1 2018 Portfolio Discussions Considering trends and opportunities for investors with Guide to the Markets CONTENTS in the UK 2 in emerging markets 8 in Europe 14 in the US 20 Global

2015 Market Review & Outlook. January 29, 2015

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

Economic & Financial Market Outlook. James W. Paulsen, Ph.D. - Wednesday

Economic & Financial Market Outlook James W. Paulsen, Ph.D. - Wednesday U.S. faces supply-side economic challenges!!! Annualized U.S. working age population growth by economic recovery Annualized U.S.

Economic & Financial Market Outlook James W. Paulsen, Ph.D. - Wednesday U.S. faces supply-side economic challenges!!! Annualized U.S. working age population growth by economic recovery Annualized U.S.

Macro Strategy Chartbook

Macro Strategy Chartbook September 2018 Executive Summary Valuation is presenting a mixed picture. Shorterterm, the S&P 500 appears cheap, but investors increasingly believe that we re approaching peak

Macro Strategy Chartbook September 2018 Executive Summary Valuation is presenting a mixed picture. Shorterterm, the S&P 500 appears cheap, but investors increasingly believe that we re approaching peak

Learning objectives. Investors should leave the presentation with an ability to discuss

Learning objectives Investors should leave the presentation with an ability to discuss the fundamentals and valuations of emerging markets economies in 2018 the key risks of emerging market debt in 2018

Learning objectives Investors should leave the presentation with an ability to discuss the fundamentals and valuations of emerging markets economies in 2018 the key risks of emerging market debt in 2018

2018 The year of promise

2018 The year of promise January 2018 Tushar Pradhan, Chief Investment Officer We have come a long way in 2017 Source: Kotak Institutional Equities Dec 2017 Key events and performance of the Indian market

2018 The year of promise January 2018 Tushar Pradhan, Chief Investment Officer We have come a long way in 2017 Source: Kotak Institutional Equities Dec 2017 Key events and performance of the Indian market

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries June 2009 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries June 2009 The World Bank Development Economics Prospects Group

JONATHAN CASTELEYN, CFA JOSHUA STEINER, CFA T. ROWE PRICE (TROW) PADDLING UPSTREAM BEST IDEAS SHORT. March 2016

PADDLING UPSTREAM BEST IDEAS SHORT. March 2016") JONATHAN CASTELEYN, CFA JOSHUA STEINER, CFA T. ROWE PRICE (TROW) PADDLING UPSTREAM BEST IDEAS SHORT March 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered

JONATHAN CASTELEYN, CFA JOSHUA STEINER, CFA T. ROWE PRICE (TROW) PADDLING UPSTREAM BEST IDEAS SHORT March 2016 DISCLAIMER DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered

HSBC Fund Update. HSBC GIF Global Emerging Markets Bond. March Summary. Market overview. market.

HSBC Fund Update March 2015 HSBC GIF Global Emerging Markets Bond Summary Market sentiment improved in February given supportive global developments including the interim agreement between Greece and its

HSBC Fund Update March 2015 HSBC GIF Global Emerging Markets Bond Summary Market sentiment improved in February given supportive global developments including the interim agreement between Greece and its

Ashmore Group plc. Results for year ending 30 June September

Ashmore Group plc Results for year ending 30 June 2016 6 September 2016 www.ashmoregroup.com Overview Weaker and more volatile markets in H1, strong recovery in H2 Consistent investment processes delivering:

Ashmore Group plc Results for year ending 30 June 2016 6 September 2016 www.ashmoregroup.com Overview Weaker and more volatile markets in H1, strong recovery in H2 Consistent investment processes delivering:

Week in Markets. FTSE Equity Indices Week MTD Jul 12 Jun 12 QTD YTD. MSCI Equity Indices Week MTD Jul 12 Jun 12 QTD YTD

Week ending 24 August, 20 Page 1 of 8 FTSE Equity Indices Week MTD Jul Jun QTD YTD UK FTSE All Share -1.3 3.2 1.3 4.8 4.6 8.0 15.5 FTSE -1.3 3.2 1.2 5.0 4.5 6.8 15.3 FTSE 250-1.4 3.0 2.1 3.8 5.2 15.6 17.5

Week ending 24 August, 20 Page 1 of 8 FTSE Equity Indices Week MTD Jul Jun QTD YTD UK FTSE All Share -1.3 3.2 1.3 4.8 4.6 8.0 15.5 FTSE -1.3 3.2 1.2 5.0 4.5 6.8 15.3 FTSE 250-1.4 3.0 2.1 3.8 5.2 15.6 17.5

Economic and Market Outlook

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Asset Allocation Monthly

For professional investors Asset Allocation Monthly October 2015 Joost van Leenders, CFA Chief Economist, Multi Asset Solutions joost.vanleenders@bnpparibas.com +31 20 527 5126 Uncertainty about US monetary

For professional investors Asset Allocation Monthly October 2015 Joost van Leenders, CFA Chief Economist, Multi Asset Solutions joost.vanleenders@bnpparibas.com +31 20 527 5126 Uncertainty about US monetary

Keynote Address: Jeff Gundlach Presenter Chief Executive Officer & Chief Investment Officer DoubleLine Capital

Keynote Address: Jeff Gundlach Presenter Chief Executive Officer & Chief Investment Officer DoubleLine Capital This Time It s Different 2 3 Past Fed Tightening Cycles Source: ValueWalk, Taking a Lesson

Keynote Address: Jeff Gundlach Presenter Chief Executive Officer & Chief Investment Officer DoubleLine Capital This Time It s Different 2 3 Past Fed Tightening Cycles Source: ValueWalk, Taking a Lesson

Investment Research Team Update

Economic & Market Commentary Market Update February 2015 February was a great month for global stocks! The S&P 500 ( large cap stocks) was up 5.7% and small stocks (Russell 2000) gained 5.9%. The jobs

Economic & Market Commentary Market Update February 2015 February was a great month for global stocks! The S&P 500 ( large cap stocks) was up 5.7% and small stocks (Russell 2000) gained 5.9%. The jobs

JPMorgan American Investment Trust plc Annual General Meeting. 13 May 2015

JPMorgan American Investment Trust plc Annual General Meeting 13 May 2015 Agenda Performance Review Current Economic and Market Data Current Asset Allocation and Fund Structure 1 2014 Results NAV return

JPMorgan American Investment Trust plc Annual General Meeting 13 May 2015 Agenda Performance Review Current Economic and Market Data Current Asset Allocation and Fund Structure 1 2014 Results NAV return

Is there still a case for European Small Caps?

This document is solely for the use of professionals and is not for general public distribution. The value of an investment and the income from it can fall as well as rise and you may not get back the

This document is solely for the use of professionals and is not for general public distribution. The value of an investment and the income from it can fall as well as rise and you may not get back the

Cavanal Hill Fixed Income Insights 1 st Quarter, 2018

Cavanal Hill Fixed Income Insights 1 st Quarter, 2018 Michael Maurer, CFA Senior Fixed Income Portfolio Manager Russell Knox, CFA Fixed Income Portfolio Manager Rich Williams Senior Tax Free Fixed Income

Cavanal Hill Fixed Income Insights 1 st Quarter, 2018 Michael Maurer, CFA Senior Fixed Income Portfolio Manager Russell Knox, CFA Fixed Income Portfolio Manager Rich Williams Senior Tax Free Fixed Income

WEEKLY CHANGES AGAINST THE USD MACRO & MARKETS COMMENTARY

July 03, 2017 [ W E E K LY E C O N O M I C C O M M E N TA R Y ] WEEKLY ANALYSIS FOR THE MOST CRITICAL ECONOMIC AND FINANCIAL DEVELOPMENTS MACRO & MARKETS COMMENTARY» Central banker s comments dominated

July 03, 2017 [ W E E K LY E C O N O M I C C O M M E N TA R Y ] WEEKLY ANALYSIS FOR THE MOST CRITICAL ECONOMIC AND FINANCIAL DEVELOPMENTS MACRO & MARKETS COMMENTARY» Central banker s comments dominated

International Economy Watch

International Economy Watch August AIB Treasury Economic Research Unit GDP Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- QoQ Change US......... -...... Eurozone -. -. -. -. -. -.......... German.... -.

International Economy Watch August AIB Treasury Economic Research Unit GDP Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- Q- QoQ Change US......... -...... Eurozone -. -. -. -. -. -.......... German.... -.