Apollo Ty Apollo res res Lt d Lt Exh x i h b i i b t 1: Con o so n l so ilda d t a e t d f d inan an ial i s and s and val v ua u ti a on o

|

|

|

- Ashley Richard

- 6 years ago

- Views:

Transcription

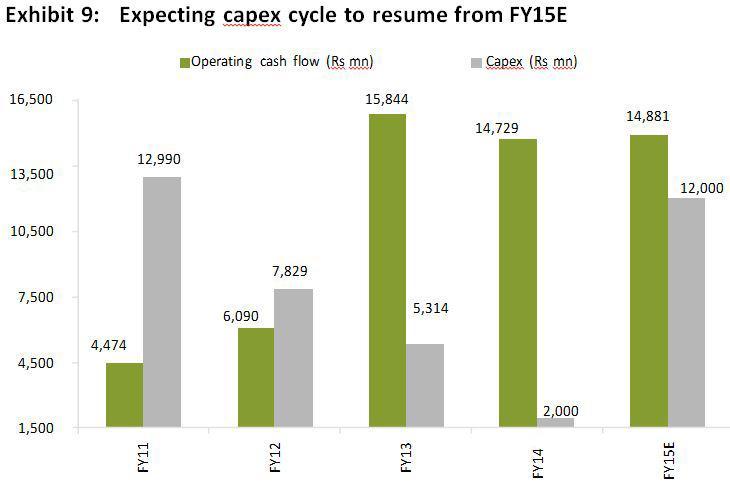

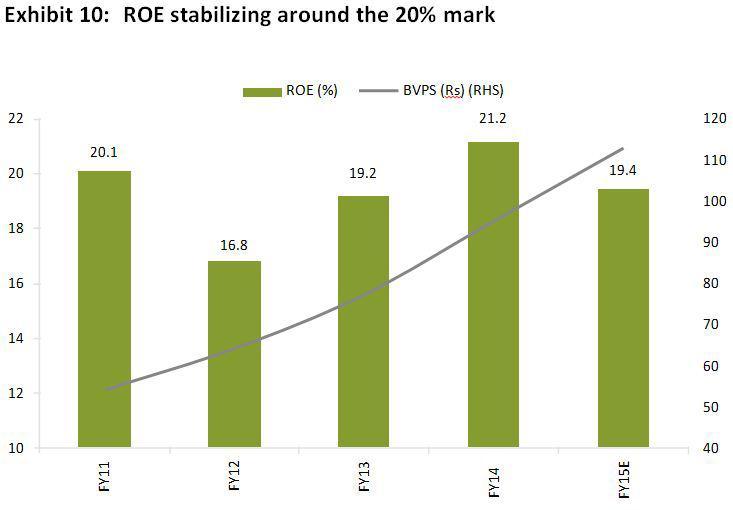

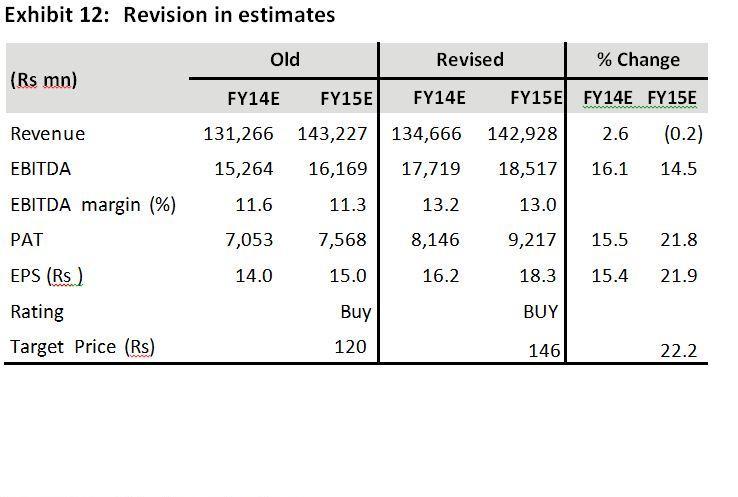

1 Apollo Tyres Ltd Focus back on core business; robust margin to drive cash flows We recommend BUY with a PT of Rs255 based on 11.45x FY15E EPS. We have increased our FY15E EPS by 22% led by healthier margin visibility amid weak demand. We maintain our target earnings multiple at 8x vs 10x for global peers. We have increased our EBITDA margin assumption by ~160bp for both FY14E & FY15E led by visibility of subdued raw material basket (RMB) prices & steady pricing discipline. We expect deleveraging to continue even after factoring resumption of capex cycle from FY15E on back of robust cash flows amid weak demand. With favourable district court judgment, we don t expect any liability from Cooper deal call off. Robust margin and demand recovery in EU to result in strong cash flow generation: Internationalisation has its benefits The company expects a) strong performance in Europe (38% of EBITDA) aided by market recovery and marketshare gains, b) below-trend demand scenario in India (60% of EBITDA) until 1HFY15, c) overall margins to be maintained at current levels (c13%) in the medium term driven by stable raw material prices and a virtually dormant pricing environment. In the medium to long term, the company expects to drive growth from capacity expansion in Europe and expanding its sales presence in South-East Asia, Latin America and the Middle East. Standalone business to operate ~80-85% capacity in FY15E; capex in the key markets to be back soon: With Vredestein running at optimal utilisation and India operations running at ~75-80% utlisation, the capex cycle is expected to resume from FY15E to take care of the next level of growth in FY16-17E. As a matter of financial prudency, a APTY may adopt the organic capex route for the next business cycle by re-initiating plans of green field capacities in east Europe & Thailand. Standalone capacity is presently around 1,500 TPD with FY14E expected sales at ~75% of it. Now with the uncertainity over the Cooper done with; we do not expect any exit penalty for APTY: With APTY getting an exit from the Cooper merger deal, the only element of uncertainty remaining will be the quantum of exit penalty. It can be safely assumed that with APTY getting favorable judgement from local legal authority, chances of any substantial cash outflow from APTY seems slim. However, one cannot rule out PTY s intention of entering any such large ticket deal in future, but apparently at least for the near term till FY16E, APTY will aim to grow through the organic capex led route and thus initiate its capex cycle aggressively from FY15E post a gap of a couple of years. BUY Rs 197 Reuters: APLO.BO Bloomberg: APTY IN 12-month price target Rs 255 Chandraveer Singh chandraveer.singh@kslindia.com Pranav Khandwala pranavk@kslindia.com Market cap Rs Cr 52 week high/low Rs /54.60 Share o/s: 504 mn Share o/s (fully diluted) : 504 mn Avg daily trading vol (3m) : 9,375 ('000) Source: Bloomberg KHANDWALA vs Consensus (Rs) PT EPS (FY14) Mean High Low KHANDWALA Buy(s) Hold(s) Sell(s) Nos Source: Bloomberg Shareholding pattern (%) Sep 13 Jun 13 Mar 13 Promoters FIIs MF/s/FIs/Banks Others Source: BSE Price movement (Rs) vs the Sensex Valuation: We put a BUY on APTY with a PT of Rs255 from the current Rs203. We have increased our FY15E EPS by 22%, and we maintain our target earnings multiple at 11.45x, with similar global peers trading at ~14x forward earnings. Risks: Higher than expected RMB price, continued weak demand in India/EU, fresh acquisition plans & larger penalty/legal expenses for Cooper deal call off are risks to our call & estimates. Source: Bloomberg Exhibit 1: Consolidated financials and valuation Year Ended (Cr's) 12-Mar 13-Mar 14-Mar 15-Mar (E) 16-Mar (E) Revenue EBITDA EBITDA growth (%) Net Income EPS P/E Adj PAT 11,662 14,569 10,521 18,517 32,590 PAT margin P a g e 1 7 J u n e

2 E E Apollo Tyres: focus back on core business; robust margin to drive cash flows 2 P a g e 1 7 J u n e

3 3 P a g e 1 7 J u n e

4 Key financials Apollo Tyres: focus back on core business; robust margin to drive cash flows 4 P a g e 1 7 J u n e

5 Apollo Tyres: focus back on core business; robust margin to drive cash flows Rating history - Apollo Tyres Future prospects Apollo Tyres is planning to expand its capacity at its Chennai facility. Moreover, the company is also in the process of setting up a R&D centre in the same complex. The new Centre will take up R&D works related to commercial vehicles for all the Apollo plants, across the World. At present, the Chennai plant manufacture radial tyres for truck and capacity of the plant is 6,000 trucks tyres and 15,000 passenger car tyres a day and the capacity utilisation of around 70-75%. The facility caters to both domestic and export markets. Apollo Tyres produces the entire range of automotive tyres for ultra and high speed passenger cars, truck and bus, farm, off-the-road, industrial and specialty applications like mining, retreaded tyres and retreading material. These are produced across Apollo s eight manufacturing locations in India, Netherlands and Southern Africa. As of Jun 06, 2014, the consensus forecast amongst 44 polled investment analysts covering Apollo Tyres Ltd advises that the company will outperform the market. This has been the consensus forecast since the sentiment of investment analysts improved on February 16, The previous consensus forecast advised investors to hold their position in Apollo Tyres Ltd. NOW, Sectors having high EVF should benefit the most during a recovery We use fixed costs/pbt ratios of bear and bull cycles to arrive at an Earnings Volatility Factor (EVF). Sectors with high operating leverage, inability to control fixed costs during downcycles, and low margins have typically witnessed high EVF. Typically, sectors having EVF above 1.4x demonstrate this characteristic. This implies that if one has an outlook of an improving business cycle, operating leverage for sectors/stocks with high EVF should improve materially. These sectors should thus witness the highest improvement in earnings with improving business cycles. However, we believe even in the event of a recovery, stock performance will vary. We prefer stocks that meet two criteria: high EVF (Earnings Volatility Factor), to identify stocks that would witness high earnings recovery, and high ECS (Early Cycle Score) to identify stocks that would respond fastest to a recovery. Apollo tyres fits both the criteria. We prefer early cyclicals. As per our analysis, companies with high ECS respond quickly to even short cycles of an economic recovery: stocks within durables, commercial vehicles (CV), four-wheelers (4W) stand out, while investment cycle-driven sectors recover with a lag, indicating that the full negative impact of their operating leverage may not have played out as yet. We prefer stocks with high fixed costs. We note that companies with high fixed costs, inability to control them during downcycles and low margins witness a disproportionate increase in earnings during upcycles. We measure this through EVF. Sectors with high EVF: CVs, 4Ws, Durables, Cement, Retailing, Construction and Industrial Products stand out on this parameter. Likely winners and losers. Assuming India is at the cusp of an economic recovery, we would invest in stocks with high ECS and high EVF. We screen companies with ECS>5x and EVF>1.4x; Apollo Tyres should be a key beneficiary of a potential economic recovery. 5 P a g e 1 7 J u n e

6 Ratings and other definitions Institutional Equities Research coverage universe - distribution of ratings Stock rating system BUY. We expect the stock to deliver >15% absolute returns. ACCUMULATE. We expect the stock to deliver 6-15% absolute returns. REDUCE. We expect the stock to deliver +5% to -5% absolute returns. SELL. We expect the stock to deliver negative absolute returns of >5%. Not Rated (NR). We have no investment opinion on the stock. Sector rating system Overweight. We expect the sector to relatively outperform the Sensex. Underweight. We expect the sector to relatively underperform the Sensex. Neutral. We expect the sector to relatively perform in line with the Sensex. Analyst certification We, Chandraveer Singh and Pranav Khandwala, hereby certify all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly/indirectly, related to the specific recommendations or views expressed in this report." 6 P a g e 1 7 J u n e

7 IMPORTANT DISCLOSURE Khandwala Securities Limited and its affiliates are a full-service, integrated investment banking, investment management and brokerage group. We along with our affiliates are leading underwriter of securities and participants in virtually all securities trading markets in India. We and our affiliates have investment banking and other business relationships with a significant percentage of the companies covered by our Investment Research Department. Our research professionals provide important input into our investment banking and other business selection processes. Investors should assume that Khandwala Securities Limited and/or its affiliates are seeking or will seek investment banking or other business from the company or companies that are the subject of this material and that the research professionals who were involved in preparing this material may participate in the solicitation of such business. Our research professionals are paid in part based on the profitability of Khandwala Securities Limited, which include earnings from investment banking and other business. Khandwala Securities Limited generally prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. Additionally, Khandwala Securities Limited generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. We are not soliciting any action based on this material. It is for the general information of clients of Khandwala Securities Limited. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, clients should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. Khandwala Securities Limited does not provide tax advise to its clients, and all investors are strongly advised to consult with their tax advisers regarding any potential investment. Certain transactions -including those involving futures, options, and other derivatives as well as non-investment-grade securities - give rise to substantial risk and are not suitable for all investors. The material is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed are our current opinions as of the date appearing on this material only. We endeavour to update on a reasonable basis the information discussed in this material, but regulatory, compliance, or other reasons may prevent us from doing so. We and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance of this material, may from time to time have long or short positions in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein. For the purpose of calculating whether Khandwala Securities Limited and its affiliates holds beneficially owns or controls, including the right to vote for directors, 1% of more of the equity shares of the subject issuer of a research report. Khandwala Securities Limited and its affiliates may, to the extent permissible under applicable laws, have acted on or used this research to the extent that it relates to issuers, prior to or immediately following its publication. Foreign currency denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of or income derived from the investment. In addition, investors in securities such as ADRs, the value of which are influenced by foreign currencies affectively assume currency risk. In addition options involve risks and are not suitable for all investors. Please ensure that you have read and understood the current derivatives risk disclosure document before entering into any derivative transactions. This report has been prepared by Khandwala Securities Limited (KSL). KSL has reviewed the report and, in so far as it includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. 7 P a g e 1 7 J u n e

BUY SREI (SREI) Banks/Financial Institutions

Banks/Financial Institutions") .dot SREI (SREI) Banks/Financial Institutions Buoyancy in infrastructure to drive business, upgrade to BUY. We find Srei s stock attractive at the current levels on account of (1) its inexpensive valuations,

.dot SREI (SREI) Banks/Financial Institutions Buoyancy in infrastructure to drive business, upgrade to BUY. We find Srei s stock attractive at the current levels on account of (1) its inexpensive valuations,

3QFY09 revenues in line but adjusted margins beat KIE. No changes in estimates for FY E

India Daily Summary - January 29, 2009 LUPIN January 29, 2009 Pharmaceuticals LUPN.BO, Rs562 Rating Sector coverage view Target Price (Rs) BUY Attractive 950 52W High -Low (Rs) 782-438 Market Cap (Rs bn)

India Daily Summary - January 29, 2009 LUPIN January 29, 2009 Pharmaceuticals LUPN.BO, Rs562 Rating Sector coverage view Target Price (Rs) BUY Attractive 950 52W High -Low (Rs) 782-438 Market Cap (Rs bn)

BUY. Suprajit Engineering (SEL) Automobiles

Automobiles") Suprajit Engineering (SEL) Automobiles Strong performance. Suprajit Engineering reported a consolidated net profit of `210 mn in 3QFY16, which was 2% higher than our estimates. Phoenix Lamps was consolidated

Suprajit Engineering (SEL) Automobiles Strong performance. Suprajit Engineering reported a consolidated net profit of `210 mn in 3QFY16, which was 2% higher than our estimates. Phoenix Lamps was consolidated

Mahindra & Mahindra. Source: Company Data; PL Research

Tractors drive Q2 performance; Accumulate November 11, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating Accumulate Price Rs1,242 Target Price Rs1,503 Implied Upside 21.0% Sensex 26,819 Nifty

Tractors drive Q2 performance; Accumulate November 11, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating Accumulate Price Rs1,242 Target Price Rs1,503 Implied Upside 21.0% Sensex 26,819 Nifty

Key estimate revision. Year FY14 23,28,609 3,48,027 1,40, FY15E 25,74,029 3,94,133 1,69,

: price: EPS: How does our one year outlook change? We retain our positive stance on TTMT driven by continued strong performance at JLR on both revenues & margins and expected reduction in losses at standalone

: price: EPS: How does our one year outlook change? We retain our positive stance on TTMT driven by continued strong performance at JLR on both revenues & margins and expected reduction in losses at standalone

TVS Motors. Source: Company Data; PL Research

Margins trajectory looking up ; Accumulate November 01, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs709

Margins trajectory looking up ; Accumulate November 01, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs709

MRF BUY. Performance Highlights. CMP `9,407 Target Price `11,343. Company Update Automobile. Key financials

Company Update Automobile February 22, 212 MRF Performance Highlights Y/E Sept. (` cr) 1QSY12 1QSY11 % chg (yoy) 4QSY11 % chg (qoq) Net sales 2,875 2,167 32.7 2,62 9.8 EBITDA 258 243 5.9 181 42.6 EBITDA

Company Update Automobile February 22, 212 MRF Performance Highlights Y/E Sept. (` cr) 1QSY12 1QSY11 % chg (yoy) 4QSY11 % chg (qoq) Net sales 2,875 2,167 32.7 2,62 9.8 EBITDA 258 243 5.9 181 42.6 EBITDA

Bharat Forge. Exports remain subdued, outlook better. Source: Company Data; PL Research

Exports remain subdued, outlook better November 08, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating BUY Price Rs850 Target Price Rs957 Implied Upside 12.6% Sensex 27,591 Nifty 8,544 (Prices

Exports remain subdued, outlook better November 08, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating BUY Price Rs850 Target Price Rs957 Implied Upside 12.6% Sensex 27,591 Nifty 8,544 (Prices

Maruti Suzuki. Source: Company Data; PL Research

Healthy operating performance; Accumulate October 28, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating Accumulate Price Rs5,860 Target Price Rs6,356 Implied Upside 8.5% Sensex 27,916 Nifty

Healthy operating performance; Accumulate October 28, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating Accumulate Price Rs5,860 Target Price Rs6,356 Implied Upside 8.5% Sensex 27,916 Nifty

Cummins India. Growth/margin bottoming. Source: Company Data; PL Research

Growth/margin bottoming May 25, 2018 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Shreyans Jain shreyansjain@plindia.com +91 22 66322256 Rating BUY Price Rs704 Target Price Rs928 Implied Upside 31.8%

Growth/margin bottoming May 25, 2018 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Shreyans Jain shreyansjain@plindia.com +91 22 66322256 Rating BUY Price Rs704 Target Price Rs928 Implied Upside 31.8%

Thermax. Source: Company Data; PL Research

Near term outlook muted, working on building a strong base November 11, 2016 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price

Near term outlook muted, working on building a strong base November 11, 2016 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price

Goodyear India ACCUMULATE. Performance Highlights. CMP Target Price `326 `374. 1QCY2012 Result Update Tyres. Key financials

1QCY212 Result Update Tyres June 6, 212 Goodyear India Performance Highlights Y/E December (` cr) 1QCY212 1QCY211 % chg (yoy) 4QCY211 % chg (qoq) Net sales 331 336 (1.6) 395 (16.2) EBITDA 2 24 (18.6) 34

1QCY212 Result Update Tyres June 6, 212 Goodyear India Performance Highlights Y/E December (` cr) 1QCY212 1QCY211 % chg (yoy) 4QCY211 % chg (qoq) Net sales 331 336 (1.6) 395 (16.2) EBITDA 2 24 (18.6) 34

Ramco Cement. Rating: Target price: EPS: Rating CMP. Target BUY. Rs.415. Rs. 360

: price: EPS: How does our one year outlook change? We maintain our positive stance on s (TRCL). The company is one of the largest cement producers in South and remains among the best plays on Southern

: price: EPS: How does our one year outlook change? We maintain our positive stance on s (TRCL). The company is one of the largest cement producers in South and remains among the best plays on Southern

Key estimate revision. Financial summary. Year FY14 391,088 45,198 34, FY15E 354,262 35,426 23,

: price: EPS: How does our one year outlook change? We retain our negative stance on the stock. We expect s revenue to de-grow by 9% y-o-y on the back of muted execution (client side and clearance delays)

: price: EPS: How does our one year outlook change? We retain our negative stance on the stock. We expect s revenue to de-grow by 9% y-o-y on the back of muted execution (client side and clearance delays)

Apollo Tyres. Profitability likely to improve. Source: Company Data; PL Research

Profitability likely to improve November 09, 2011 Surjit Arora surjitarora@plindia.com +91-22-66322235 Rating Accumulate Price Rs59 Target Price Rs66 Implied Upside 11.9% Sensex 17,362 (Prices as on November

Profitability likely to improve November 09, 2011 Surjit Arora surjitarora@plindia.com +91-22-66322235 Rating Accumulate Price Rs59 Target Price Rs66 Implied Upside 11.9% Sensex 17,362 (Prices as on November

Kaveri Seed Company Overhang of Royalty issue to remain; cut target price: maintain BUY

Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 1QFY16 Result Review (Wholly owned subsidiary of Bank of Baroda) BUY Kaveri Seed Company Overhang of Royalty issue to

Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 1QFY16 Result Review (Wholly owned subsidiary of Bank of Baroda) BUY Kaveri Seed Company Overhang of Royalty issue to

ITC. Rating: Target price: EPS: Relative better visibility despite the smoke, Maintain BUY CMP. Target. Rating. Rs.389. Buy. Rs.

: price: EPS: Relative better visibility despite the smoke, Maintain BUY ITC reported revenues of Rs.~87.2bn (+13% y-o-y), operating profits of Rs.32.8bn (+15% y-o-y) and PAT of Rs.~23.8bn (+16% y-o-y).

: price: EPS: Relative better visibility despite the smoke, Maintain BUY ITC reported revenues of Rs.~87.2bn (+13% y-o-y), operating profits of Rs.32.8bn (+15% y-o-y) and PAT of Rs.~23.8bn (+16% y-o-y).

Key estimate revision. Financial summary. Year FY16E 29, % 3,583 2, FY17E 26, % 3,478 2,

: price: EPS: How does our one year outlook change? We maintain our negative stance on SKF India due to the absence of significant growth momentum drivers over the medium term. While railways could be

: price: EPS: How does our one year outlook change? We maintain our negative stance on SKF India due to the absence of significant growth momentum drivers over the medium term. While railways could be

Key estimate revision. Financial summary. Year

: price: EPS: How does our one year outlook change? We retain our positive outlook on WIL and believe that revival in MHCV industry, increasing content per vehicle and opportunity in exports would drive

: price: EPS: How does our one year outlook change? We retain our positive outlook on WIL and believe that revival in MHCV industry, increasing content per vehicle and opportunity in exports would drive

Maruti Suzuki. In a league of its own ; Buy. Source: Company Data; PL Research

In a league of its own ; Buy October 28, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating BUY Price Rs8,115 Target Price Rs9,250

In a league of its own ; Buy October 28, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating BUY Price Rs8,115 Target Price Rs9,250

Sanghvi Movers Ltd. Results above estimates. Figure 1: Actual Vs Religare Estimates. Financial highlights. Valuations and Recommendation

Institutional Equity Research Key data 3 June 28 Sector Capital Goods Market Cap Rs9bn/US$.2bn 52 Wk H/L (Rs) 337/15.5 BSE Avg. daily vol. (6m) 4,437 BSE Code 5373 NSE Code SANGHVIMOV Bloomberg SGM IN

Institutional Equity Research Key data 3 June 28 Sector Capital Goods Market Cap Rs9bn/US$.2bn 52 Wk H/L (Rs) 337/15.5 BSE Avg. daily vol. (6m) 4,437 BSE Code 5373 NSE Code SANGHVIMOV Bloomberg SGM IN

BUY APOLLO TYRES LTD. CMP Target Price AUGUST 12 th, Highlights. Result Update (CONSOLIDATED BASIS): Q1 FY16

: Q1 FY16") BUY CMP 187.50 Target Price 215.00 APOLLO TYRES LIMITED Result Update (CONSOLIDATED BASIS): Q1 FY16 AUGUST 12 th, 2015 ISIN: INE438A01022 Stock Data Sector Tyres & Tubes BSE Code 500877 Face Value 1.00

BUY CMP 187.50 Target Price 215.00 APOLLO TYRES LIMITED Result Update (CONSOLIDATED BASIS): Q1 FY16 AUGUST 12 th, 2015 ISIN: INE438A01022 Stock Data Sector Tyres & Tubes BSE Code 500877 Face Value 1.00

Century Plyboards (India)

") : price: EPS: How does our one year outlook change? Century Plyboards (India) (CPBI) 2QFY17 revenues grew by 6% yoy driven by 2% yoy growth in plywood products and 11% yoy growth in laminate products.

: price: EPS: How does our one year outlook change? Century Plyboards (India) (CPBI) 2QFY17 revenues grew by 6% yoy driven by 2% yoy growth in plywood products and 11% yoy growth in laminate products.

Bharat Forge. Result Update. Q4FY13 Result Highlights. Valuation. No Respite in Sight May 29, Institutional Research 1

[ Result Update Equity India Forging & Industrials Bharat Forge Ltd. No Respite in Sight May 29, 2013 CMP (`) Target (`) 241 238 Potential Upside Absolute Rating (1.24)% HOLD Market Info (as on May 28,

[ Result Update Equity India Forging & Industrials Bharat Forge Ltd. No Respite in Sight May 29, 2013 CMP (`) Target (`) 241 238 Potential Upside Absolute Rating (1.24)% HOLD Market Info (as on May 28,

Cummins India Ltd Bloomberg Code: KKC IN

Company Update Margins Under Pressure; Domestic Recovery Underway Half-yearly revenue was flat; margins were under pressure: Cummins India revenue, EBITDA and PAT for H1FY17 reached to Rs.24,784mn, Rs.4,649mn

Company Update Margins Under Pressure; Domestic Recovery Underway Half-yearly revenue was flat; margins were under pressure: Cummins India revenue, EBITDA and PAT for H1FY17 reached to Rs.24,784mn, Rs.4,649mn

Crompton Greaves. Looking to exit overseas Power segment! Source: Company Data; PL Research

Looking to exit overseas Power segment! May 29, 2015 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price Rs166 Target Price Rs204

Looking to exit overseas Power segment! May 29, 2015 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price Rs166 Target Price Rs204

Maruti Suzuki. Source: Company Data; PL Research

Run continues, Royalty reduction positive ; Buy January 29, 2018 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating BUY Price Rs9,277

Run continues, Royalty reduction positive ; Buy January 29, 2018 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating BUY Price Rs9,277

Kalpataru Power. Rating: Target price: EPS: Rating CMP. Target BUY. Rs Rs.256

: price: EPS: How does our one year outlook change? We expect KPP s revenue (standalone) to grow by 21% y-o-y in FY17E backed by an order book of Rs. 91bn (1.7x FY17E book-to-bill). Both Transmission line

: price: EPS: How does our one year outlook change? We expect KPP s revenue (standalone) to grow by 21% y-o-y in FY17E backed by an order book of Rs. 91bn (1.7x FY17E book-to-bill). Both Transmission line

Mphasis. Increased confidence on margins. Source: Company Data; PL Research

Increased confidence on margins July 25, 2016 Govind Agarwal govindagarwal@plindia.com +91 22 66322300 Rating BUY Price Rs540 Target Price Rs570 Implied Upside 5.6% Sensex 28,095 Nifty 8,636 (Prices as

Increased confidence on margins July 25, 2016 Govind Agarwal govindagarwal@plindia.com +91 22 66322300 Rating BUY Price Rs540 Target Price Rs570 Implied Upside 5.6% Sensex 28,095 Nifty 8,636 (Prices as

Maruti Suzuki (RHS) BUY. Operationally In Line; Reiterate Buy. Automobiles October 31, 2014 RESULT REVIEW. Outlook & Valuation.

BUY. Operationally In Line; Reiterate Buy. Automobiles October 31, 2014 RESULT REVIEW. Outlook & Valuation.") Oct13 Dec13 Jan14 Feb14 Apr14 May14 Jun14 Aug14 Sep14 Oct14 India Research Automobiles RESULT REVIEW Bloomberg: MSIL IN Reuters: MRTI.BO BUY Operationally In Line; Reiterate Buy India s (MSIL) Revenue/EBIDTA/PAT

Oct13 Dec13 Jan14 Feb14 Apr14 May14 Jun14 Aug14 Sep14 Oct14 India Research Automobiles RESULT REVIEW Bloomberg: MSIL IN Reuters: MRTI.BO BUY Operationally In Line; Reiterate Buy India s (MSIL) Revenue/EBIDTA/PAT

APOLLO TYRES LTD. October 19 th, CMP (Rs.) 194. Key Developments

194. Key Developments") Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 s. APOLLO TYRES LTD.. October 19 th, 2015 BSE Code: 500877 NSE Code: APOLLOTYRE Reuters Code: APLO.NS Bloomberg

Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 s. APOLLO TYRES LTD.. October 19 th, 2015 BSE Code: 500877 NSE Code: APOLLOTYRE Reuters Code: APLO.NS Bloomberg

Asian Paints. Source: Company Data; PL Research

Premium valuations to sustain, Accumulate October 4, 17 Amnish Aggarwal amnishaggarwal@plindia.com +91 Gaurav Jogani gauravjogani@plindia.com +91 8 Rating Accumulate Price Rs1,1 Target Price Rs1,9 Implied

Premium valuations to sustain, Accumulate October 4, 17 Amnish Aggarwal amnishaggarwal@plindia.com +91 Gaurav Jogani gauravjogani@plindia.com +91 8 Rating Accumulate Price Rs1,1 Target Price Rs1,9 Implied

Near-term pressure, but long-term outlook positive

INDUSTRY IT CMP (as on 2 Nov 2015) Rs 1,812 Target Price Rs 2,050 Nifty 8,051 Sensex 26,559 KEY STOCK DATA Bloomberg ECLX IN No. of Shares (mn) 30 MCap (Rs bn) / ($ mn) 55/843 6m avg traded value (Rs mn)

INDUSTRY IT CMP (as on 2 Nov 2015) Rs 1,812 Target Price Rs 2,050 Nifty 8,051 Sensex 26,559 KEY STOCK DATA Bloomberg ECLX IN No. of Shares (mn) 30 MCap (Rs bn) / ($ mn) 55/843 6m avg traded value (Rs mn)

Apollo Tyres BUY. Performance Highlights. CMP Target Price `71 `82. 4QFY2011Result Update Tyre. Key financials (Consolidated)

") 4QFY211Result Update Tyre Apollo Tyres Performance Highlights Y/E March (Standalone) 4QFY11 4QFY1 % chg (yoy) Angel est. % diff. Net sales (` cr) 1,762 1,313 34.2 1,49 18.2 EBITDA (` cr) 146 185 (2.7)

4QFY211Result Update Tyre Apollo Tyres Performance Highlights Y/E March (Standalone) 4QFY11 4QFY1 % chg (yoy) Angel est. % diff. Net sales (` cr) 1,762 1,313 34.2 1,49 18.2 EBITDA (` cr) 146 185 (2.7)

Asian Paints. Source: Company Data; PL Research

Premium Valuations to sustain, Accumulate May, 17 Amnish Aggarwal amnishaggarwal@plindia.com +91 Gaurav Jogani gauravjogani@plindia.com +91 8 Rating Accumulate Price Rs1,18 Target Price Rs1,171 Implied

Premium Valuations to sustain, Accumulate May, 17 Amnish Aggarwal amnishaggarwal@plindia.com +91 Gaurav Jogani gauravjogani@plindia.com +91 8 Rating Accumulate Price Rs1,18 Target Price Rs1,171 Implied

Cummins India. Source: Company Data; PL Research

Technology leadership, cost optimization key focus October 28, 2016 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price Rs852

Technology leadership, cost optimization key focus October 28, 2016 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price Rs852

Ambuja Cements. Rating: Target price: EPS: Rating CMP. Target BUY. Rs.225. Rs. 195

: price: EPS: How does our one year outlook change? We maintain our positive stance on ACEM. We expect ACEM to be a big beneficiary of the restructuring of LafargeHolcim s global operations. The long pending

: price: EPS: How does our one year outlook change? We maintain our positive stance on ACEM. We expect ACEM to be a big beneficiary of the restructuring of LafargeHolcim s global operations. The long pending

SpiceJet. Healthy operating performance in Q2. Source: Company Data; PL Research

Healthy operating performance in Q2 November 28, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating BUY Price Rs65 Target Price Rs115 Implied Upside 76.9% Sensex 26,316 Nifty 8,114 (Prices

Healthy operating performance in Q2 November 28, 2016 Rohan Korde rohankorde@plindia.com +91 22 66322235 Rating BUY Price Rs65 Target Price Rs115 Implied Upside 76.9% Sensex 26,316 Nifty 8,114 (Prices

Eicher Motors. Continues to ride high! Accumulate. Source: Company Data; PL Research

Continues to ride high! Accumulate November 14, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs30,083 Target

Continues to ride high! Accumulate November 14, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs30,083 Target

Equitas Holdings. Rating: Target price: ABV: Target CMP. Rating. Rs Rs. 226 BUY

: price: ABV: How does our one year outlook change? Remains a idea in the SFB space owing to a well-diversified product profile, prudence in approaching the MFI space marked by the lowest ticket size amongst

: price: ABV: How does our one year outlook change? Remains a idea in the SFB space owing to a well-diversified product profile, prudence in approaching the MFI space marked by the lowest ticket size amongst

JK Tyre & Industries Ltd.

Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18. Volume No.. II Issue No. 177 JK Tyre & Industries Ltd. June 11, 2018 BSE Code: 530007 NSE Code: JKTYRE Reuters

Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18. Volume No.. II Issue No. 177 JK Tyre & Industries Ltd. June 11, 2018 BSE Code: 530007 NSE Code: JKTYRE Reuters

JK Lakshmi Cement. Source: Company Data; PL Research

Expansions on schedule; lower costs to aid margins June 28, 2016 Kamlesh Bagmar kamleshbagmar@plindia.com +91 22 66322237 Ankit Shah ankitshah@plindia.com +91 22 66322244 Rating BUY Price Rs385 Target

Expansions on schedule; lower costs to aid margins June 28, 2016 Kamlesh Bagmar kamleshbagmar@plindia.com +91 22 66322237 Ankit Shah ankitshah@plindia.com +91 22 66322244 Rating BUY Price Rs385 Target

Bloomberg Code: ATA IN

Auto OEM: 3-Wheelers Atul Feb Auto 03, 2015 Ltd India Research Stock Broking Bloomberg Code: ATA IN Stable quarter led by surge in exports volumes (TP revised ) : Operating revenue, EBITDA and PAT grew

Auto OEM: 3-Wheelers Atul Feb Auto 03, 2015 Ltd India Research Stock Broking Bloomberg Code: ATA IN Stable quarter led by surge in exports volumes (TP revised ) : Operating revenue, EBITDA and PAT grew

Marico Kaya BUY RESULTS REVIEW 4QFY15 29 APR 2015

RESULTS REVIEW 4QFY15 29 APR 2015 Marico Kaya INDUSTRY FMCG CMP (as on 28 Apr 2015) Rs 1,635 Target Price Rs 1,823 Nifty 8,240 Sensex 27,226 KEY STOCK DATA Bloomberg MAKA IN No. of Shares (mn) 13 MCap

RESULTS REVIEW 4QFY15 29 APR 2015 Marico Kaya INDUSTRY FMCG CMP (as on 28 Apr 2015) Rs 1,635 Target Price Rs 1,823 Nifty 8,240 Sensex 27,226 KEY STOCK DATA Bloomberg MAKA IN No. of Shares (mn) 13 MCap

Coal India. Source: Company Data; PL Research

Misses estimates; Higher costs dims hope for earnings recovery February 13, 2017 Kamlesh Bagmar kamleshbagmar@plindia.com +91 22 66322237 Rating Reduce Price Rs325 Target Price Rs320 Implied Upside 1.5%

Misses estimates; Higher costs dims hope for earnings recovery February 13, 2017 Kamlesh Bagmar kamleshbagmar@plindia.com +91 22 66322237 Rating Reduce Price Rs325 Target Price Rs320 Implied Upside 1.5%

BUY CMP (Rs.) 297 Target (Rs.) 385 Potential Upside 30%

297 Target (Rs.) 385 Potential Upside 30%") Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May- Jun-16 Jul-16 Aug-16 Aug-16 Sep-16 Oct-16. Volume No.. I Issue No. 95 Dewan Housing Finance Corporation (DHFL) Nov. 4, 2016 BSE Code: 511072 NSE Code: DHFL

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May- Jun-16 Jul-16 Aug-16 Aug-16 Sep-16 Oct-16. Volume No.. I Issue No. 95 Dewan Housing Finance Corporation (DHFL) Nov. 4, 2016 BSE Code: 511072 NSE Code: DHFL

Indraprastha Gas. Growth traction continues. Source: Company Data; PL Research

Growth traction continues June 28, 216 Avishek Datta avishekdatta@plindia.com +91 22 66322254 Rating BUY Price Rs65 Target Price Rs632 Implied Upside 4.5% Sensex 26,43 Nifty 8,95 (Prices as on June 27,

Growth traction continues June 28, 216 Avishek Datta avishekdatta@plindia.com +91 22 66322254 Rating BUY Price Rs65 Target Price Rs632 Implied Upside 4.5% Sensex 26,43 Nifty 8,95 (Prices as on June 27,

Siemens. Railways and T&D driving inflows. Source: Company Data; PL Research

Railways and T&D driving inflows November 23, 2016 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price Rs1,055 Target Price Rs1,230

Railways and T&D driving inflows November 23, 2016 Kunal Sheth kunalsheth@plindia.com +91 22 66322257 Samir Bendre samirbendre@plindia.com +91 22 66322256 Rating Accumulate Price Rs1,055 Target Price Rs1,230

MARUTI SUZUKI INDIA LTD RESEARCH

EQUITY November 17, 2008 RESULTS REVIEW Maruti Suzuki India Limited Hold Share Data Market Cap Rs. 158.8 bn Price Rs. 549.80 BSE Sensex 9,291.01 Reuters Bloomberg Avg. Volume (52 Week) MRTI.BO MSIL IN

EQUITY November 17, 2008 RESULTS REVIEW Maruti Suzuki India Limited Hold Share Data Market Cap Rs. 158.8 bn Price Rs. 549.80 BSE Sensex 9,291.01 Reuters Bloomberg Avg. Volume (52 Week) MRTI.BO MSIL IN

SIEMENS INDIA LIMITED RESEARCH

RESULTS REVIEW Siemens India Limited Hold Share Data Market Cap Rs. 196.1 bn Price Rs. 581.6 BSE Sensex 14,961.07 Reuters Bloomberg Avg. Volume (52 Week) SIEM.BO SIEM IN 0.2 mn 52-Week High/Low Rs. 1,142.5

RESULTS REVIEW Siemens India Limited Hold Share Data Market Cap Rs. 196.1 bn Price Rs. 581.6 BSE Sensex 14,961.07 Reuters Bloomberg Avg. Volume (52 Week) SIEM.BO SIEM IN 0.2 mn 52-Week High/Low Rs. 1,142.5

Key estimate revision. Financial summary. Year

: price: ABV: How does our one year outlook change? While we continue to believe that SUF is a multi-year compounding opportunity in the asset and home financing segments, we take note of the under-performance

: price: ABV: How does our one year outlook change? While we continue to believe that SUF is a multi-year compounding opportunity in the asset and home financing segments, we take note of the under-performance

Mahindra and Mahindra Maintain Outperformer. (Rs mn) Mar 14 Mar 15 YoY (%) Dec 14 QoQ (%) FY14 FY15P YoY (%) FY16E YoY (%) FY17E YoY (%)

Mar 14 Mar 15 YoY (%) Dec 14 QoQ (%) FY14 FY15P YoY (%) FY16E YoY (%) FY17E YoY (%)") Batlivala & Karani RESULT UPDATE Mahindra and Mahindra Maintain Outperformer LARGE CAP Share Data Reuters code Bloomberg code MAHM.BO MM IN Market cap. (US$ mn) 12,243 6M avg. daily turnover (US$ mn) 21.0

Batlivala & Karani RESULT UPDATE Mahindra and Mahindra Maintain Outperformer LARGE CAP Share Data Reuters code Bloomberg code MAHM.BO MM IN Market cap. (US$ mn) 12,243 6M avg. daily turnover (US$ mn) 21.0

Century Plyboards (India)

") : price: EPS: How does our one year outlook change? We continue to maintain our positive stance on Century Plyboards (CPBI) as it is one of the leading players in the organized plywood market and third

: price: EPS: How does our one year outlook change? We continue to maintain our positive stance on Century Plyboards (CPBI) as it is one of the leading players in the organized plywood market and third

GMM Pfaudler Limited BUY. Performance Update CMP. `945 Target Price ` QFY2019 Result Update Industrial Machinery. Investment Period 12 Months

2QFY2019 Result Update Industrial Machinery October 26, 2018 GMM Pfaudler Limited Performance Update Standalone (` cr) Q2FY19 Q2FY18 % yoy Q1FY19 % qoq Net sales 99.2 93.2 29.8% 76.4 6.4% EBITDA 16.0 15.3

2QFY2019 Result Update Industrial Machinery October 26, 2018 GMM Pfaudler Limited Performance Update Standalone (` cr) Q2FY19 Q2FY18 % yoy Q1FY19 % qoq Net sales 99.2 93.2 29.8% 76.4 6.4% EBITDA 16.0 15.3

Apollo Tyres BUY. Performance Highlights. CMP Target Price `56 `65. 3QFY2011Result Update Tyre. Key Financials (Consolidated)

") 3QFY211Result Update Tyre Apollo Tyres Performance Highlights Y/E March (Standalone) 3QFY11 3QFY1 % chg (yoy) Angel est. % diff. Net sales (` cr) 1,432 1,323 8.2 1,259 13.7 EBITDA (` cr) 149 25 (27.4)

3QFY211Result Update Tyre Apollo Tyres Performance Highlights Y/E March (Standalone) 3QFY11 3QFY1 % chg (yoy) Angel est. % diff. Net sales (` cr) 1,432 1,323 8.2 1,259 13.7 EBITDA (` cr) 149 25 (27.4)

Advisory Desk. TVS Srichakra Ltd. BUY CMP. `355 Target Price `468. Investment rationale. Outlook and valuation. Investment Period 12 Months

Ltd. Ltd. (TVSSL), a part of TVS Group, is a leading manufacturer of two and three-wheeler tyres with a 25% market share. Two-wheeler demand growth (~16% yoy YTD) continues to be insulated from the current

Ltd. Ltd. (TVSSL), a part of TVS Group, is a leading manufacturer of two and three-wheeler tyres with a 25% market share. Two-wheeler demand growth (~16% yoy YTD) continues to be insulated from the current

Apollo Tyres Ltd. Investment Positives Robust Domestic Sales. Market Leadership to fuel growth. 13 Sep, 2010

H O L D 13 Sep, 2010 Key Data (`) CMP 85 Target Price 89 Key Data Bloomberg Code APTY IN Reuters Code APLO.BO BSE Code 500877 NSE Code APOLLOTYRE Face Value (`) 1 Market Cap. (` Bn.) 42.8 52 Week High

H O L D 13 Sep, 2010 Key Data (`) CMP 85 Target Price 89 Key Data Bloomberg Code APTY IN Reuters Code APLO.BO BSE Code 500877 NSE Code APOLLOTYRE Face Value (`) 1 Market Cap. (` Bn.) 42.8 52 Week High

India Cements Rating: Target price:

: price: EPS: Another weak quarter; Maintain SELL ICEM reported weak 2QFY14 results, with a revenue de-growth of 3.3% y-o-y and EBITDA de-growth of 37.8% y-o-y. Volumes de-grew by 3% y-o-y to 4mt. Realisations

: price: EPS: Another weak quarter; Maintain SELL ICEM reported weak 2QFY14 results, with a revenue de-growth of 3.3% y-o-y and EBITDA de-growth of 37.8% y-o-y. Volumes de-grew by 3% y-o-y to 4mt. Realisations

Key estimate revision. Financial summary. Year FY15 121, % 16, % FY16E 137, % 20,

: price: EPS: How does our one year outlook change? We maintain rating on Aurobindo post the company s 3QFY16 results. Revenue growth for the quarter was 10% yoy: US sales of $238mn (vs. estimate of $251mn

: price: EPS: How does our one year outlook change? We maintain rating on Aurobindo post the company s 3QFY16 results. Revenue growth for the quarter was 10% yoy: US sales of $238mn (vs. estimate of $251mn

Praj Industries (PRAIN)

") Result Update October 18, 211 Rating matrix Rating : Buy Target : 96 Target Period : 12-15 months Potential Upside : 25% WHAT S CHANGED Praj Industries (PRAIN) 77 Key Financials Crore FY1 FY11 FY12E FY13E

Result Update October 18, 211 Rating matrix Rating : Buy Target : 96 Target Period : 12-15 months Potential Upside : 25% WHAT S CHANGED Praj Industries (PRAIN) 77 Key Financials Crore FY1 FY11 FY12E FY13E

HCC BUY. Infrastructure April 10, QIP step in the right direction EVENT UPDATE. India Research. Bloomberg: HCC IN Reuters: HCNS.

Jan-14 Mar-14 Apr-14 May-14 Jul-14 Aug-14 Sep-14 Nov-14 Dec-14 Jan-15 India Research Infrastructure April 10, 2015 EVENT UPDATE Bloomberg: IN Reuters: HCNS.BO BUY QIP step in the right direction has successfully

Jan-14 Mar-14 Apr-14 May-14 Jul-14 Aug-14 Sep-14 Nov-14 Dec-14 Jan-15 India Research Infrastructure April 10, 2015 EVENT UPDATE Bloomberg: IN Reuters: HCNS.BO BUY QIP step in the right direction has successfully

Allcargo Logistics. Source: Company Data; PL Research

Slow capex continue to impact PES, weak show continues May 24, 2018 Keyur Pandya keyurpandya@plindia.com +912266322247 R Sreesankar rsreesankar@plindia.com +912266322214 Rating Accumulate Price Rs120 Target

Slow capex continue to impact PES, weak show continues May 24, 2018 Keyur Pandya keyurpandya@plindia.com +912266322247 R Sreesankar rsreesankar@plindia.com +912266322214 Rating Accumulate Price Rs120 Target

Indag Rubber Ltd Bloomberg Code: IDR IN

Industrials-Transportation Equipment-Commercial Vehicles Bloomberg Code: IDR IN India Research - Stock Broking Set to Ride on Commercial Vehicle Growth with Strong Cash Flows and Balance Sheet Recovery

Industrials-Transportation Equipment-Commercial Vehicles Bloomberg Code: IDR IN India Research - Stock Broking Set to Ride on Commercial Vehicle Growth with Strong Cash Flows and Balance Sheet Recovery

NTPC Ltd. Results in line with estimates, BUY for attractive valuations. Power. EBITDA margins up at 26% (+700bps QoQ): EBITDA margins

: EBITDA margins") Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 NTPC Ltd 11 May 2012 105 Power Result Review Rating: BUY Current Price: Rs 148 Target Price: Rs 189 Upside:

Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 NTPC Ltd 11 May 2012 105 Power Result Review Rating: BUY Current Price: Rs 148 Target Price: Rs 189 Upside:

MCX Ltd. Rating: Target price: EPS: Is commodity option a game changer for MCX? - Unlikely. Target. Rating CMP. Rs. 1,080 SELL. Rs.

: price: EPS: Is commodity option a game changer for MCX? - Unlikely In the union budget 2015-16, the Finance Minister announced the much anticipated merger of SEBI and FMC. Given the powers accorded to

: price: EPS: Is commodity option a game changer for MCX? - Unlikely In the union budget 2015-16, the Finance Minister announced the much anticipated merger of SEBI and FMC. Given the powers accorded to

Key estimate revision. Year CY14 87,383 11,148 6, CY15E 1,20,126 17,838 9,

: price: EPS: How does our one year outlook change? We retain our positive view on EIM on the back of expected improvement in volume and margin at Royal Enfield (RE) and expected revival in VECV on the

: price: EPS: How does our one year outlook change? We retain our positive view on EIM on the back of expected improvement in volume and margin at Royal Enfield (RE) and expected revival in VECV on the

PI Industries. 1QFY17 Result Review HOLD. Better performance continued, valuations stretch; maintain HOLD. Sector: AGRI

1QFY17 Result Review HOLD PI Industries Ltd. Better performance continued, valuations stretch; maintain HOLD PI Industries Ltd (PI) reported strong 1QFY17 result with a revenue growth of ~15.4%/12.9% YoY/QoQ,

1QFY17 Result Review HOLD PI Industries Ltd. Better performance continued, valuations stretch; maintain HOLD PI Industries Ltd (PI) reported strong 1QFY17 result with a revenue growth of ~15.4%/12.9% YoY/QoQ,

Karnataka Bank. Rating: BUY. Bank - Private. Short Note. Brief Financials

Karnataka Bank Bank - Private Date June 11, 2018 CMP (Rs.) 120 Target (Rs.) 163 Potential Upside 37% BSE Sensex 35484 NSE Nifty 10787 Scrip Code Bloomberg KBLIN Reuters KBNK.BO BSE Group A BSE Code 532652

Karnataka Bank Bank - Private Date June 11, 2018 CMP (Rs.) 120 Target (Rs.) 163 Potential Upside 37% BSE Sensex 35484 NSE Nifty 10787 Scrip Code Bloomberg KBLIN Reuters KBNK.BO BSE Group A BSE Code 532652

MCX Ltd. Rating: Target price: EPS: Tepid volume growth continues. Target. Rating CMP. Rs. 1,080 SELL. Rs. 1,176

: price: EPS: Tepid volume growth continues 4QFY15 traded volumes in MCX showed a small improvement sequentially whereas declined yoy. FY15 traded Values are at a sever year low. We retain our cautious

: price: EPS: Tepid volume growth continues 4QFY15 traded volumes in MCX showed a small improvement sequentially whereas declined yoy. FY15 traded Values are at a sever year low. We retain our cautious

Bharat Forge. Growth on all fronts; Accumulate. Source: Company Data; PL Research

Growth on all fronts; Accumulate November 08, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs728 Target Price

Growth on all fronts; Accumulate November 08, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs728 Target Price

Fineotex Chemical Ltd

Company Update Decent Performance under Macroeconomic Pressure; Business Traction to Continue: Fineotex Chemical recorded decent set of result as consolidated sales grew by 1.1% YoY (largely in line) to

Company Update Decent Performance under Macroeconomic Pressure; Business Traction to Continue: Fineotex Chemical recorded decent set of result as consolidated sales grew by 1.1% YoY (largely in line) to

Bharat Petroleum Corporation Ltd

Institutional Equity Research Key data 19 June 2008 Sector Oil& Gas Market Cap Rs.7bn/US$2.3bn 52 Wk H/L (Rs) 560/260.25 Avg. daily vol. (6 month) 799,179 BSE Code 500547 NSE Code BPCL Bloomberg BPCLIN

Institutional Equity Research Key data 19 June 2008 Sector Oil& Gas Market Cap Rs.7bn/US$2.3bn 52 Wk H/L (Rs) 560/260.25 Avg. daily vol. (6 month) 799,179 BSE Code 500547 NSE Code BPCL Bloomberg BPCLIN

ULTRAMARINE & PIGMENTS LTD

02 December 2016 ULTRAMARINE & PIGMENTS LTD CMP INR 170 Initiating Coverage (BUY) Target Price INR 226 Stock Details Industry SPECIALTY CHEMICALS Bloomberg Code UMP:IN BSE Code 506685 Face Value (Rs.)

02 December 2016 ULTRAMARINE & PIGMENTS LTD CMP INR 170 Initiating Coverage (BUY) Target Price INR 226 Stock Details Industry SPECIALTY CHEMICALS Bloomberg Code UMP:IN BSE Code 506685 Face Value (Rs.)

Coal India. Source: Company Data; PL Research

Realisations drive the beat; E auction to surprise positively in H2 November 13, 2015 Kamlesh Bagmar kamleshbagmar@plindia.com +91 22 66322237 Ankit Shah ankitshah@plindia.com +91 22 66322244 Rating BUY

Realisations drive the beat; E auction to surprise positively in H2 November 13, 2015 Kamlesh Bagmar kamleshbagmar@plindia.com +91 22 66322237 Ankit Shah ankitshah@plindia.com +91 22 66322244 Rating BUY

HDFC Bank. BUY CMP (Rs.) 1,807 Target (Rs.) 2,000 Potential Upside 11%

1,807 Target (Rs.) 2,000 Potential Upside 11%") Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17. Volume No.. I Issue No. 147 HDFC Bank Oct. 31, 2017 BSE Code: 500180 NSE Code: HDFCBANK Reuters Code: HDBK.NS

Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17. Volume No.. I Issue No. 147 HDFC Bank Oct. 31, 2017 BSE Code: 500180 NSE Code: HDFCBANK Reuters Code: HDBK.NS

Dr Reddy s Laboratories

: price: EPS: How does our one year outlook change? We maintain rating on DRRD post the company s 3QFY16 results Revenue growth for the quarter was muted (3% yoy) due to disappointing performances in Russia

: price: EPS: How does our one year outlook change? We maintain rating on DRRD post the company s 3QFY16 results Revenue growth for the quarter was muted (3% yoy) due to disappointing performances in Russia

Financial summary. Year

: price: ABV: How does our one year outlook change? We retain our positive outlook on KVB, led by an improving margin profile and cost containment kicking in, while our key thesis - a proven sole banking

: price: ABV: How does our one year outlook change? We retain our positive outlook on KVB, led by an improving margin profile and cost containment kicking in, while our key thesis - a proven sole banking

Key estimate revision. Financial summary. Year

: price: ABV: How does our one year outlook change? Retain our positive view on the stock. We continue to believe that SUF is a multi-year compounding opportunity in the asset and home financing segments.

: price: ABV: How does our one year outlook change? Retain our positive view on the stock. We continue to believe that SUF is a multi-year compounding opportunity in the asset and home financing segments.

Britannia Industries

Sustains momentum; Input cost gains peaked out November 09, 2015 Amnish Aggarwal amnishaggarwal@plindia.com +91 22 66322233 Gaurav Jogani gauravjogani@plindia.com +91 22 66322238 Rating Accumulate Price

Sustains momentum; Input cost gains peaked out November 09, 2015 Amnish Aggarwal amnishaggarwal@plindia.com +91 22 66322233 Gaurav Jogani gauravjogani@plindia.com +91 22 66322238 Rating Accumulate Price

Elgi Equipments. Analyst Meet Update. CMP Rs Key takeaways from the analyst meet

Analyst Meet Update We attended the analyst meet organized by (ELEQ), a key manufacturer of air compressors with a market share of > 2% in India. Elgi s total revenues grew at a healthy CAGR of 2% in the

Analyst Meet Update We attended the analyst meet organized by (ELEQ), a key manufacturer of air compressors with a market share of > 2% in India. Elgi s total revenues grew at a healthy CAGR of 2% in the

Navneet Education. ILL loss hurts consolidated earnings growth. Source: Company Data; PL Research

ILL loss hurts consolidated earnings growth May 14, 2018 Keyur Pandya keyurpandya@plindia.com +91 22 66322247 R Sreesankar rsreesankar@plindia.com +91 22 66322214 Rating Accumulate Price Rs140 Target Price

ILL loss hurts consolidated earnings growth May 14, 2018 Keyur Pandya keyurpandya@plindia.com +91 22 66322247 R Sreesankar rsreesankar@plindia.com +91 22 66322214 Rating Accumulate Price Rs140 Target Price

Symphony. Q3FY18 Result Update Strong performance; valuations expensive. Sector: Consumer Durable CMP: ` 1,970. Recommendation: HOLD

Symphony Q3FY18 Result Update Strong performance; valuations expensive Sector: Consumer Durable CMP: ` 1,970 Recommendation: HOLD Market statistics Current stock price (`) 1,970 Shares O/S (cr.) 7.0 Mcap

Symphony Q3FY18 Result Update Strong performance; valuations expensive Sector: Consumer Durable CMP: ` 1,970 Recommendation: HOLD Market statistics Current stock price (`) 1,970 Shares O/S (cr.) 7.0 Mcap

HFC NEUTRAL. Performance Highlights CMP. `678 Target Price - 1QFY2013 Result Update HFC. Investment Period - Key financials

1QFY2013 Result Update HFC July 11, 2012 HDFC Performance Highlights Particulars (` cr) 1QFY13 4QFY12 % chg (qoq) 1QFY12 % chg (yoy) NII 1,258 1,681 (25.1) 998 26.0 Preprov. profit 1,420 1,849 (23.2) 1194

1QFY2013 Result Update HFC July 11, 2012 HDFC Performance Highlights Particulars (` cr) 1QFY13 4QFY12 % chg (qoq) 1QFY12 % chg (yoy) NII 1,258 1,681 (25.1) 998 26.0 Preprov. profit 1,420 1,849 (23.2) 1194

Bharat Petroleum Corporation

Higher inventory loss drag earnings August 14, 2017 Avishek Datta avishekdatta@plindia.com +91 22 66322254 Rating BUY Price Rs479 Target Price Rs553 Implied Upside 15.4% Sensex 31,449 Nifty 9,794 (Prices

Higher inventory loss drag earnings August 14, 2017 Avishek Datta avishekdatta@plindia.com +91 22 66322254 Rating BUY Price Rs479 Target Price Rs553 Implied Upside 15.4% Sensex 31,449 Nifty 9,794 (Prices

SpiceJet BUY. Performance Highlights CMP. `32 Target Price `43. 1QFY2013 Result Update Airlines. Investment Period 12 Months.

1QFY213 Result Update Airlines July 31, 212 SpiceJet Performance Highlights Particulars (` cr) 1QFY213 1QFY212 %chg (yoy) 4QFY212 %chg (qoq) Net sales 1,467 946 55.1 1,113 31.8 EBITDA 76 (67) 214 (2) 138

1QFY213 Result Update Airlines July 31, 212 SpiceJet Performance Highlights Particulars (` cr) 1QFY213 1QFY212 %chg (yoy) 4QFY212 %chg (qoq) Net sales 1,467 946 55.1 1,113 31.8 EBITDA 76 (67) 214 (2) 138

UltraTech Cement (ULTCEM)

") April 20, 2009 Cement Company Update UltraTech Cement (ULTCEM) Current Price Rs 546 Potential upside 15.4% Target Price Rs 630 Time Frame 12-15 months Powered by savings Historically, UltraTech Cement

April 20, 2009 Cement Company Update UltraTech Cement (ULTCEM) Current Price Rs 546 Potential upside 15.4% Target Price Rs 630 Time Frame 12-15 months Powered by savings Historically, UltraTech Cement

TTK Prestige. Q2FY18 Result Update Healthy Sales growth; Margins expands. Sector: Consumer Durable CMP: ` 6,145. Recommendation: HOLD

TTK Prestige Q2FY18 Result Update Healthy Sales growth; Margins expands Sector: Consumer Durable CMP: ` 6,145 Recommendation: HOLD Market statistics Current stock price (`) 6,145 Shares O/S (cr.) 1.2 Mcap

TTK Prestige Q2FY18 Result Update Healthy Sales growth; Margins expands Sector: Consumer Durable CMP: ` 6,145 Recommendation: HOLD Market statistics Current stock price (`) 6,145 Shares O/S (cr.) 1.2 Mcap

GE Shipping (GESHIP) Striking valuation. Result Update. Rs 262 WHAT S CHANGED. Valuation. February 8, Rating matrix.

Striking valuation. Result Update. Rs 262 WHAT S CHANGED. Valuation. February 8, Rating matrix.") Result Update Rating matrix Rating : Strong Buy Target : Rs 37 Target Period : 1 months Potential Upside : 4% Key Financials (Rs Crore) FY9 FY1E FY11E FY1E Net Sales 3. 3. 3379.9 33. EBITDA 166.1 916.4

Result Update Rating matrix Rating : Strong Buy Target : Rs 37 Target Period : 1 months Potential Upside : 4% Key Financials (Rs Crore) FY9 FY1E FY11E FY1E Net Sales 3. 3. 3379.9 33. EBITDA 166.1 916.4

Emkay. Bonding strongly; Upgrade to BUY. Pidilite Industries. Stellar all-round show

Pidilite Industries India Equity Research Consumers February 3, 2016 Result Update Emkay Your success is our success Bonding strongly; Upgrade to BUY CMP Rs567 Target Price Rs670 ( ) Rating Upside BUY

Pidilite Industries India Equity Research Consumers February 3, 2016 Result Update Emkay Your success is our success Bonding strongly; Upgrade to BUY CMP Rs567 Target Price Rs670 ( ) Rating Upside BUY

Ashok Leyland. Source: Company Data; PL Research

Short term headwinds, structural story intact; Accumulate November 09, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate

Short term headwinds, structural story intact; Accumulate November 09, 2017 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate

Ahluwalia Contracts (India)

") May-14 Jul-14 Aug-14 Sep-14 Oct-14 Dec-14 Jan-15 Feb-15 Apr-15 May-15 India Research Infrastructure May 22, 215 QUARTERLY REVIEW Bloomberg: AHLU IN Reuters: AHLU.BO BUY Better performance ahead ACIL posted

May-14 Jul-14 Aug-14 Sep-14 Oct-14 Dec-14 Jan-15 Feb-15 Apr-15 May-15 India Research Infrastructure May 22, 215 QUARTERLY REVIEW Bloomberg: AHLU IN Reuters: AHLU.BO BUY Better performance ahead ACIL posted

MRF BUY. Performance Highlights. CMP `40,703 Target Price `47,548. 1QSY2015 Result Update Tyre

1QSY2015 Result Update Tyre February 13, 2015 MRF Performance Highlights Y/E Sept. (` cr) 1QSY2015 1QSY2014 % chg (yoy) 4QSY2014 % chg (qoq) Net sales 3,353 3,201 4.8 3,361 (0.2) EBITDA 626 419 49.5 608

1QSY2015 Result Update Tyre February 13, 2015 MRF Performance Highlights Y/E Sept. (` cr) 1QSY2015 1QSY2014 % chg (yoy) 4QSY2014 % chg (qoq) Net sales 3,353 3,201 4.8 3,361 (0.2) EBITDA 626 419 49.5 608

ABB LTD (INDIA) RESEARCH

RESEARCH") RESULTS REVIEW Share Data Market Cap Rs. 168.6 bn Price Rs. 795.80 BSE Sensex 16,741.30 Reuters Bloomberg Avg. Volume (52 Week) ABB.BO ABB IN 0.11 mn 52-Week High/Low Rs. 856.95 / 344 Shares Outstanding

RESULTS REVIEW Share Data Market Cap Rs. 168.6 bn Price Rs. 795.80 BSE Sensex 16,741.30 Reuters Bloomberg Avg. Volume (52 Week) ABB.BO ABB IN 0.11 mn 52-Week High/Low Rs. 856.95 / 344 Shares Outstanding

DABUR INDIA LIMITED RESEARCH

RESULTS REVIEW Dabur India Limited Hold Share Data Market Cap Rs. 79.5 bn Price Rs. 91.95 BSE Sensex 14,577.87 Reuters Bloomberg Avg. Volume (52 Week) DABU.BO DABUR IN 0.3mn 52-Week High/Low Rs. 134 /

RESULTS REVIEW Dabur India Limited Hold Share Data Market Cap Rs. 79.5 bn Price Rs. 91.95 BSE Sensex 14,577.87 Reuters Bloomberg Avg. Volume (52 Week) DABU.BO DABUR IN 0.3mn 52-Week High/Low Rs. 134 /

SHRIRAM TRANSPORT FINANCE COMPANY LTD

27 June 2017 SHRIRAM TRANSPORT FINANCE COMPANY LTD CMP INR 975 Initiating Coverage (BUY) Target Price INR 1225 Stock Details Industry Finance (including NBFCs) Bloomberg Code SHTF:IN BSE Code 511218 Face

27 June 2017 SHRIRAM TRANSPORT FINANCE COMPANY LTD CMP INR 975 Initiating Coverage (BUY) Target Price INR 1225 Stock Details Industry Finance (including NBFCs) Bloomberg Code SHTF:IN BSE Code 511218 Face

Apollo Tyres. Rating: BUY. Result Update Q1 FY16

Change in Estimates Rating Target Q1 FY16 Apollo Tyres Consolidated revenues at Rs. 2,845cr lower by 12.4% yoy; lower than our estimates Standalone operations see 7.3% yoy decline in revenues to Rs. 2,137cr

Change in Estimates Rating Target Q1 FY16 Apollo Tyres Consolidated revenues at Rs. 2,845cr lower by 12.4% yoy; lower than our estimates Standalone operations see 7.3% yoy decline in revenues to Rs. 2,137cr

All the more bullish, TP upgraded

Sterlite Tech India Equity Research Small & Mid Cap April 18, 2017 Company Update Emkay Your success is our success All the more bullish, TP upgraded CMP Target Price Rs150 Rs208 ( ) Rating Upside BUY

Sterlite Tech India Equity Research Small & Mid Cap April 18, 2017 Company Update Emkay Your success is our success All the more bullish, TP upgraded CMP Target Price Rs150 Rs208 ( ) Rating Upside BUY

Vadodara II PPA yet to be signed; TP revised upward to Rs126 on FY19x

Gujarat Industries Power India Equity Research Power February 10, 2017 Result Update Emkay Your success is our success Vadodara II PPA yet to be signed; TP revised upward to Rs126 on FY19x CMP Target Price

Gujarat Industries Power India Equity Research Power February 10, 2017 Result Update Emkay Your success is our success Vadodara II PPA yet to be signed; TP revised upward to Rs126 on FY19x CMP Target Price

Eicher Motors. Source: Company Data; PL Research

Good show continues; In line quarter! Accumulate May 09, 2018 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs30,305

Good show continues; In line quarter! Accumulate May 09, 2018 Saksham Kaushal sakshamkaushal@plindia.com +91 22 66322235 Poorvi Banka poorvibanka@plindia.com +91 22 66322426 Rating Accumulate Price Rs30,305

SQS India BFSI Ltd HOLD. Impact of Macro Headwinds Still Hurting; Revenue from US May Pick up in FY18E

Company Update Impact of Macro Headwinds Still Hurting; Revenue from US May Pick up in FY18E EBITDA Margins recovered by 618 bps QoQ: The company has witnessed many challenges over the year FY17 starting

Company Update Impact of Macro Headwinds Still Hurting; Revenue from US May Pick up in FY18E EBITDA Margins recovered by 618 bps QoQ: The company has witnessed many challenges over the year FY17 starting