HOMEOWNERS PROGRAM WEST VIRGINIA

|

|

|

- Lucy Sanders

- 5 years ago

- Views:

Transcription

1 FARMERS MUTUAL INSURANCE COMPANY HOMEOWNERS PROGRAM WEST VIRGINIA

2 FARMERS MUTUAL INSURANCE COMPANY HOMEOWNERS PROGRAM UNDERWRITING RULES 1. BINDING AUTHORITY A. You may bind coverage for any risk meeting the underwriting rules outlined in the manual. Maximum coverage A amount may not exceed $300,000. B. Premium payments on canceled cannot be accepted without prior approval from an underwriter. A signed statement of no loss is required to reinstate a policy. C. Minimum Coverage: Form 1 $30,000 Form 2 $50,000 Form 3 $100,000 Form 4 $10, STRUCTURE A. Foundation Form 1 Pier with skirting/underpinning acceptable Form 2 & 3 Continuous solid masonry required B. Heating Form 1 Form 2 Form 3 Space heaters Floor Furnace, circulating & baseboard heat acceptable Central heat 25 years old or less (thermostatically controlled & vented with ductwork in each room). This includes wood furnaces. C. Roof Form 1 & 2 Shingle, metal, slate, clay acceptable Form 3 Shingle or metal required, must be within 25 yrs old No rolled or Ondura roofing for this package D. Occupancy Form 1 & 2 One & two family acceptable Form 3 One family only E. Plumbing Form 1 Galvanized Form 2 & 3 Copper or Plastic required Rev. 5/18 HO-UND-1

3 F. Dwelling Dwellings under construction or total renovation: Must be written under the dwelling fire program Hybrid homes (mobile homes w/rm additions): Must be written under the mobile home owners program if owner occupied or under the dwelling fire program is tenant or seasonal occupied Townhomes: Acceptable if fire division separates each unit. The fire division can be a masonry wall of an approved dead air space. G. Electric Form 1 Form 2 Form 3 Fuse Breaker Breaker: must be 25 years old or less 3. RISK CRITERIA A. Mailed applications: Completed with signatures, payment & photos of all insured structures. On line applications: All screens completed, with payment information & photos. (Signatures to be retained in agent office) B. When extending liability to other structures photos are required C. When individuals are co-habitating, all individuals must be shown on the policy as named insured s. D. Farmer s comprehensive liability is mandatory for properties in excess of 5 acres whether in one or more tract of land & whether farming is done or not. Additional premium is required for each separate tract of land. You will use the ML29 endorsement. Location of each additional/separate tract required. E. Handrails required on all steps of 4 or more risers. In-ground pools must be fenced & locked. Above ground pools must be enclosed with railing, gated & locked or fenced. F. Mortgages: No more than two (2) per policy. G. Dwellings in estate must be written under the dwelling fire program. Rev. 5/18 HO-UND-2

4 4. WOOD STOVE GUIDELINES A. Wood stoves vented into a metal UL approved triple wall or double wall insulated chimney acceptable. B. Wood stoves vented into a fireplace must have the vent pipe extended to the top of the chimney. C. Wood stoves vented into a chimney located on or within an external wall must be built from the ground up & have a tile or metal liner. D. A completed wood stove questionnaire & photo of the wood stove must accompany the application. 5. UNACCEPTABLE RISKS/EXPOSURES A. Dwellings using wood stove as sole source of heat. OR kerosene space heaters being used. B. Vacant or unoccupied dwellings C. Mobile homes or hybrid dwellings D. Vicious dogs, including any dog that bitten previously or any risk with a: Rottweiler, Pit Bull, Chow, Doberman Pinscher, German Shepherd, Akita or any mix of these E. Trampolines, broken steps, missing handrails or unfenced pools. F. Applicants who have been canceled, non-renewed or declined by another company in the past five (5) years. G. Applicants who have had a total loss or a theft claim H. Check with underwriting if the applicant has had any losses I. Structures originally constructed for occupancies other than residential purposes J. Student housing Farmers Mutual reserves the right to change or alter the underwriting rules for any risk, including but not limited to the coverage amount, form type, &/or deductible based upon the underwriter s discretion. Rev. 5/18 HO-UND-3

5 FARMERS MUTUAL INSURANCE COMPANY PREFERRED DOUBLE WIDE MOBILE HOMEOWNERS PROGRAM UNDERWRITING RULES & AUTHORITIES 1. ELIGIBILITY-DOUBLE WIDE A. 15 model-years old or less B. Limit of Insurance: New - Current & 3 prior years at purchase price with a copy of the bill of sale Others -We will use the E2Value to determine value of mobile home, porches, decks & room additions. C. Maximum Coverage A limit: $200,000. D. Fireplaces-Factory installed fireplaces & pellet stoves: No surcharge applied but photo must be submitted. Woodstoves prohibited E. Foundation Solid- continuous block (or) Block pier on concrete pads, enclosed with skirting 2. PROPERTY & LIABILITY COVERAGE A. Refer to the Homeowners manual for forms & rates 3. RISK CRITERIA A. Mailed applications: completed with signatures, payment & photos of all insured structures. On line applications: All screens completed, with payment information & photos (retain signature in your office) B. When extending liability to other structures photos are required. C. In situations where individuals are co-habitating, all individuals must be shown on the policy as named insured s. Rev 5/18 PMH-1

6 FARMERS MUTUAL INSURANCE COMPANY PREFERRED DOUBLE WIDE MOBILE HOMEOWNERS PROGRAM UNDERWRITING RULES & AUTHORITIES D. Farmers comprehensive liability is mandatory for properties in excess of 5 acres whether in one or more tract of land & whether farming is done or not. Additional premium is required for each separate tract of land. You will use the ML29 endorsement. Location of each additional tract required. E. Handrails required on all steps of 4 or more risers. In-ground pools must be fenced & locked. Above ground pools must be enclosed with railing, gated & locked or fenced. F. Mortgages-No more than 2 per policy. 4. UNACCEPTABLE RISKS OR EXPOSURES A. Woodstoves or kerosene space heat as sole source of heat B. Vacant or unoccupied dwellings C. Vicious dogs, including any dog that has bitten previously or any risk with the following: Rottweiler, Pit Bull, Doberman Pinscher, German Shepherd, Chow, Akita or any mix of these D. Existence of trampoline, broken steps, missing handrails or unfenced pools E. Applicants who have been canceled, non-renewed or declined by another company in the last 5 years F. Applicants who have had a total loss or a theft claim G. Check with underwriting if applicant s have had any losses Farmers Mutual reserves the right to change or alter the underwriting rules for any risk, including but not limited to the coverage amount, form type &/or deductible, based upon the underwriter s discretion. Rev 5/18 PMH-2

7 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES EXPANDED COVERAGE PROGRAM FORMS AND ENDORSEMENTS WEST VIRGINIA HOMEOWNERS BOOKLET FORMS Form Basic Form Form Broad Form Form Special Form Form Contents Broad Form MANDATORY ENDORSEMENTS CL Flood Coverage Notice West Virginia CL Coal Mine Subsidence Coverage Part Non Dwelling CL Coal Mine Subsidence Coverage Part-Dwelling GL Care Provided for Others A Business Activity ML West Virginia Loss Payment Endorsement ML Punitive Damage Exclusion ML Lead Liability Exclusion ML Pollution Liability Exclusions ML Calendar Date or Time Failure Exclusion ML Amendatory Endorsement - Farm Exposure Exclusion ML Amendment of Policy Terms Exclusion of Motorized Vehicles ML Limited Coverage for Injury or Damage Arising from a Dog ML All-Terrain Vehicle Exclusion ML Limited Fungi, Wet or Dry Rot, or Bacteria Coverage ML Amended Vandalism or Malicious Mischief Exclusion (Controlled Substance Exclusion) OTHER ENDORSEMENTS ML Actual Cash Value ML Farm Liability Coverage ML Incidental Property Coverages - Higher Limits ML Additional Insured ML Office, Professional, Private School or Studio Occupancy ML Change Endorsement ML Personal Injury ML Related Private Structures ML Loss Assessment Coverage ML Earthquake Loss Assessment ML Earthquake Coverage ML Replacement Value Loss Settlement Terms ML Scheduled Personal Property Coverage ML- 61A 1.0 Scheduled Personal Property Coverage - Schedule ML Coverage C - Higher Limits on Certain Property ML Scheduled Glass ML Additional Residential Premises Rented to Others - Liability Coverage Only ML Business Activities ML Watercraft REV HO - Expanded Coverage - 1 AAIS

8 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES EXPANDED COVERAGE PROGRAM FORMS AND ENDORSEMENTS WEST VIRGINIA HOMEOWNERS ML Increased Coverage A Limit - No Private Structures ML Snowmobile - Liability Coverage Only ML Computer Coverage ML Rating Information ML Insurance by More Than One Company ML Water Damage - Sewers, Drains and Sumps OTHER ENDORSEMENTS ML Waterbed Liability ML Premises Alarm or Fire Protection System ML Ordinance or Law ML Employer's Liability - Farm Employees ML Incidental Farming ML Animal Collision ML Debris Removal ML Accidental Discharge or Overflow Coverage - Water-Filled Furniture ML Dwelling Under Construction - Theft ML Golf Cart Liability Coverage REV HO - Expanded Coverage - 2 AAIS

9 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA This manual contains rules, definitions, rating information, and a listing of forms and endorsements filed and approved for the Homeowners Program in this state. Any special rules, definitions, rating information, forms, or endorsements filed by or on behalf of the Company apply in lieu of those referred to in this manual. Refer to the Company for homeowners coverages not available through this manual. RULES TABLE OF CONTENTS Eligibility Program Description Policywriting Instructions Premium Determination Deductibles Premium Modifications Optional Coverages Property Coverages Liability Coverages Farm Coverages -- Liability DEFINITIONS Construction Definitions Fire Protection Definitions Territorial Definitions RATING INFORMATION Basic Policy Rating Information Rating Information for Optional Coverages REV 13.0 AAIS Includes copyrighted material with permission of American Association of Insurance Services

10 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA INDEX Rules Page Accidental Discharge -- Water-filled Furniture...23 Actual Cash Value...15 Additional Interests...10 Alarm Systems...17 Animal Collision...29 Assignment...11 Basic Limits... 8 Burglary Alarm Credit...17 Business Activities...32 Business Property...24 Calculation of Premium...14 Cancellation...11 Care Provided For Others Liability...34 Property...22 Changes in Limits...15 Coal Mine Subsidence...13 Computers...25 Conditional Endorsements...13 Construction Definitions...Def-1 Contributing Insurance...11 Co-owner Occupancy... 2 Coverages (Basic) and Amounts (Minimum)... 8 Coverage B -- Extension of Coverage A...12 Coverage C Increased Limits...21 Credit Card and Depositors Forgery...25 Debris Removal -- Expanded...18 Deductibles...16 Definitions Construction...Def-1 Fire Protection...Def-2 Territorial Definitions...Def-2 REV 13.0 Index - i AAIS

11 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Rules Page Domestic Employees...30 Dwellings Under Construction Eligibility... 3 Theft Coverage...21 Earthquake...20 Electronic Devices...24 Eligibility... 1 Endorsements...10 Farm Coverage Options...36 Farm Personal Liability...36 Fire Alarm Credit...17 Fire Department Service Charge...26 Fire Protection Definitions...Def-2 Golf Carts Property...28 Guns...23 Inception Time... 9 Incidental Farming...36 Ineligible Risks... 3 Interpolation...12 Individual Risk Premium Modification...19 Jewelry, Watches, and Furs...23 Liability Coverage Options Farm...36 Personal...30 Loss Assessment...27 Loss Settlement Provisions... 5 Mid-Term Changes...15 Minimum Premium...10 REV 13.0 Index - ii AAIS

12 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Rules Page Modified Loss Settlement Terms...15 Money and Securities...23 Office, Professional, Private School, or Studio Occupancy...33 Ordinance or Law -- Expanded...17 Package Policy Requirements... 8 Perils Insured Against... 6 Personal Injury...34 Policy Term... 9 Policywriting Instructions... 9 Preferred Mobile Homeowners... Und. Guide Supplement Premium Determination...14 Premium Modifications...17 & 19 Premium Rounding...12 Principal Coverages Liability... 7 Property... 4 Private Structures Extension of Coverage A...12 Optional Coverages...21 Program Description... 4 Property Coverage Options...20 Protective Devices...17 Refrigerated Food Spoilage...25 Replacement Value -- Coverage C...18 Restriction of Coverage...11 Scheduled Glass...27 Scheduled Personal Property...26 Silverware, Goldware, and Pewterware...24 Smoke Detectors...17 Snowmobiles...33 Sprinkler Systems...17 REV 13.0 Index - iii AAIS

13 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Rules Page Tenant's Improvements...25 Tenant's Personal Property -- Special Coverage...15 Territorial Definitions...Def-3 Townhouses... Und. Guide Page 2 Transfer of Policy...11 Vandalism...20 Waiver of Premium...12 Water Damage -- Sewers, Drains, and Sumps...27 Waterbed Liability...31 Watercraft...34 REV 13.0 Index - iv AAIS

14 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL RULE 1 -- ELIGIBILITY 1.1 Owner Occupied WEST VIRGINIA A policy may be issued to an owner-occupant of a dwelling used only for private residential purposes, except as permitted in Rule 1.5, and occupied by no more than two families and no more than two boarders or roomers per family. Use Form 1, 2, or Preferred Mobile Homeowners Program (Doublewide Mobile Homes) Refer to Rule 1.1. Use form 3 only and attach ML Tenant Occupied A policy may be issued to the tenant (non-owner) of a dwelling or apartment if the residence occupied by the insured is used only for residential purposes, except as permitted in Rule 1.5, and is occupied by no more than one additional family or two boarders or roomers. Use Form Unit-Owners This rule does not apply. REV 13.0 RULES - 1 AAIS

15 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 1.4 Co-owner Occupancy WEST VIRGINIA A policy may be issued to one of the co-owners of a two family dwelling provided each co-owner occupies a separate apartment within the dwelling. The dwelling must be used only for private residential purposes, except as permitted in Rule 1.5. Coverage for the other co-owner's interest in the dwelling and related private structures and for premises liability may be provided by endorsement ML-41. Use Form 1, 2, or 3. A Form 4 policy providing coverage for personal property, additional living costs, and personal liability may be issued to the other coowner(s). 1.5 Incidental Business Occupancies An insured may engage in certain business activities on the insured premises without affecting the eligibility status, provided that the premises is occupied principally for private residential purposes. Refer to the company for eligible business occupancies. 1.6 Other Occupancies At the option of the company, a policy may be issued to: -- an occupant of a dwelling under a life estate arrangement; or -- an occupant of a dwelling who is purchasing the dwelling under a long-term contract. The seller, who retains title until the contract is satisfied, must not act as mortgagee. The dwelling must be used only for private residential purposes, except as permitted in Rule 1.5, and must be occupied by no more than two families and no more than two boarders or roomers per family. REV 13.0 Rules - 2 AAIS

16 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Coverage for the owner's/seller's interest in the dwelling and related private structures and for premises liability may be provided by endorsement ML-41. Use Form 1, 2 or Dwellings Under Construction A policy may be issued to cover the interest of the intended owneroccupant of a dwelling under construction. The dwelling must be intended to be used only for private residential purposes, except as permitted in Rule 1.5, and occupied by no more than two families and no more than two boarders or roomers per family. Refer to the company for additional guidelines. Use Form 1, 2, or Seasonal Dwellings This rule does not apply. 1.9 Ineligible Risks The following are ineligible for coverage under this manual: -- Mobile homes, trailer homes, or house trailers, whether or not set on foundations or otherwise made stationary. This does not apply to the Preferred Mobile Homeowners Program. -- Property to which farm forms or rates apply, except as permitted in Rules 7.26 and 9. REV 13.0 Rules - 3 AAIS

17 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 2 -- PROGRAM DESCRIPTION The following is a general description of the coverages provided by the homeowners policy forms. The policy forms state the complete conditions. 2.1 Policy Forms The following forms are used to provide homeowners coverage. Form 1 -- Basic Form Form 2 -- Broad Form Form 3 -- Special Form Form 4 -- Contents Broad Form 2.2 Principal Property Coverages (Mandatory) Forms 1, 2, and 3 provide all of the principal coverages described below. Form 4 includes only Coverages C and D Coverage A -- Residence Coverage A covers the residence on the insured premises, including additions and built-in components Coverage B -- Related Private Structures Coverage B covers unattached structures on the insured premises that are related to the residence, other than structures used for business purposes. Coverage also applies to fences, driveways, sidewalks, and other permanently installed outdoor fixtures on the insured premises. REV 13.0 Rules - 4 AAIS

18 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Coverage C Personal Property Coverage C covers personal property owned by or in the care of an insured. Coverage for an insured s personal property usually at a residence other than the insured premises is limited to 10% of the coverage C limit Coverage D Additional Living Costs & Loss of Rent Coverage D covers increased living costs & loss of rent or fair rental value that occur when an insured loss makes the insured premises unfit for use. 2.3 Loss Settlement Coverage A & B Forms 1 & 2: Buildings must be covered on an actual cash value basis. Attach endorsement ML-15 & establish the limit for Coverage A on an actual cash value basis. Form 3: Claims are settled based on replacement cost loss settlement terms for buildings covered under Coverage A & B. Preferred Mobile Homeowners Program: The mobile home & all other structures are covered on an actual cash value basis Coverage C Loss to property covered under Coverage C is settled on an actual cash value basis. REV 10/13 Rules 5 AAIS

19 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 2.4 Perils Insured Against WEST VIRGINIA Forms 1 and 2 insure property covered under Coverages A, B, and C and the related costs covered under Coverage D against risks of direct physical loss by the perils indicated below. Perils Covered Form 1 Form 2 Fire or Lightning X X Windstorm or Hail X X Explosion X X Riot or Civil Commotion X X Aircraft X X Vehicles X X Smoke X X Sinkhole Collapse X X Volcanic Action X X Vandalism X X Theft X X Falling Objects X Weight of Ice, Snow, or Sleet X Sudden and Accidental Tearing Apart, Burning, or Bulging X Accidental Discharge of Liquids or SteamX Freezing X Sudden and Accidental Damage from Electrical Currents X Form 3 insures property covered under Coverages A and B and the related costs covered under Coverage D against all risks of direct physical loss, with certain exceptions. Property covered under Coverage C is insured against risks of direct physical loss by the perils shown for Form 2. REV 13.0 Rules - 6 AAIS

20 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Form 4 insures property covered under Coverage C, the insured's interest in building improvements and betterments, and the related costs covered under Coverage D against risks of direct physical loss by the perils shown for Form Principal Liability Coverages (Mandatory) Coverage L -- Personal Liability -- Coverage L pays on behalf of the insured for damages due to bodily injury or property damage caused by an occurrence related to the insured premises or the insured's personal activities. Coverage M -- Medical Payments to Others -- Coverage M pays medical expenses incurred by persons who are not insureds if bodily injury occurs in connection with the insured premises or the insured's personal activities. Coverages L and M can be omitted when contributing insurance applies or when the policy is written to cover an additional or secondary location. See Rules 3.9 and 10. REV 13.0 Rules - 7 AAIS

21 FARMERS MUTUAL INSURANCE COMPANY WV AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 2.6 BASIC LIMITS The following basic limits apply to the coverage s provided by the homeowner s policy: Property Coverage Form 1 Form 2 Form 3 Form 4 Residence $30,000 $40,000 $75,000 $10,000 Private Structures % of limit on residence Personal Property % of limit on residence $10,000 Additional Living Costs & loss of rent % of limit on residence % of limit on Personal property Liability Coverage Coverage L Coverage M All Forms $50,000 per occurrence $ 1,000 per person, $25,000 per accident Rev 11/11 Rules-8 AAIS

22 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 3 -- POLICYWRITING INSTRUCTIONS 3.1 Inception Time The policy may be issued to take effect at 12:01 A.M. Show the inception time on the declarations. 3.2 Policy Term Annual Rating information for annual policies is shown in this manual. Policies may not be written for terms of less than one year except as specified in the rules shown below. It is permissible to extend a policy for successive annual terms by extension certificate using the rating information, forms, and endorsements in effect on the renewal date Three-Year Prepaid This rule does not apply Three-Year Deferred This rule does not apply Less Than One Year A policy may be written for a term of less than one year in order to maintain common anniversary dates with other policies Renewal Plan This rule does not apply. REV 13.0 Rules - 9 AAIS

23 FARMERS MUTUAL INSURANCE COMPANY WV AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 3.3 Minimum Premium A minimum annual premium charge applies to each policy. The minimum annual premium for Form 1, 2 & 3 is $100. For Form 4 is $ Endorsements Information called for as entries on endorsements can instead be shown on the declarations or A supplemental schedule 3.5 Additional Interests A homeowners policy can be endorsed to cover the interests of co-owners, executors, administrators, trustees or beneficiaries in the insured premises or the interests of other residents of the insured premises Interests in Coverages A & B & Premises Liability Forms 1, 2 & 3 A policy can be endorsed to cover the insurable interests of others in the covered property & their liability arising out of the insured premises. ENDORSEMENT ML-41 Make entries to show the location of the premises, the names & addresses of the additional insured s & the extent of their interests Residents of the Household THIS RULE DOES NOT APPLY Landlords THIS RULE DOES NOT APPLY Rev 1/12 Rules-10 AAIS

24 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 3.6 Transfer or Assignment WEST VIRGINIA A policy can not be endorsed to effect: -- transfer to another location within the same state; or -- assignment from one insured to another in the event of transfer of title of the dwelling. 3.7 Restriction of Coverage If a policy would not be issued because of unusual exposures, the applicant may request a restriction of coverage at no reduction of premium. The request, signed by the applicant, must be referred to the company. 3.8 Cancellation or Changes in Limits or Coverages Policies must be canceled in accordance with the terms of all applicable cancellation provisions. Mandatory coverages may not be canceled unless the entire policy is canceled. If a policy is canceled or the limits are reduced, the amount of any return premium due is calculated on a pro rata basis, subject to any minimum premium requirement. 3.9 Contributing Insurance Coverage under the property section of the policy can be divided between two or more companies. -- All policies must contain the same deductible. -- All additional limits and coverages that apply to the property coverages must be divided between the companies. Coverage for scheduled personal property can be shared at the option of the companies. REV 13.0 Rules - 11 AAIS

25 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA -- All liability coverage must be assumed entirely by one of the companies. Subtract the liability credit shown in this manual from the total premium and divide the remaining premium between the companies. The company assuming the liability coverage adds to their premium the liability amount that was subtracted as well as any premium for additional liability limits and/or coverages. -- All policies must include the policy number and company names and must identify the company providing the liability coverage. Attach endorsement ML-178 and make the necessary entries Extension of Coverage A -- No Private Structures -- Forms 1, 2, and 3 If the combined replacement cost of all covered related private structures does not exceed $1,000, an amount equal to the Coverage B limit may be added to the Coverage A limit for no additional premium charge. Attach endorsement ML Waiver of Premium An additional or return premium due when a policy is endorsed after its inception may be waived, however, return premiums must be refunded at the request of the insured. Refer to the company for the amount that may be waived Premium Rounding Premiums shown on the declarations may be rounded. Refer to the company for rounding procedures Interpolation Rating information for a limit that is between two limits shown in this manual can be developed by interpolation. REV 13.0 Rules - 12 AAIS

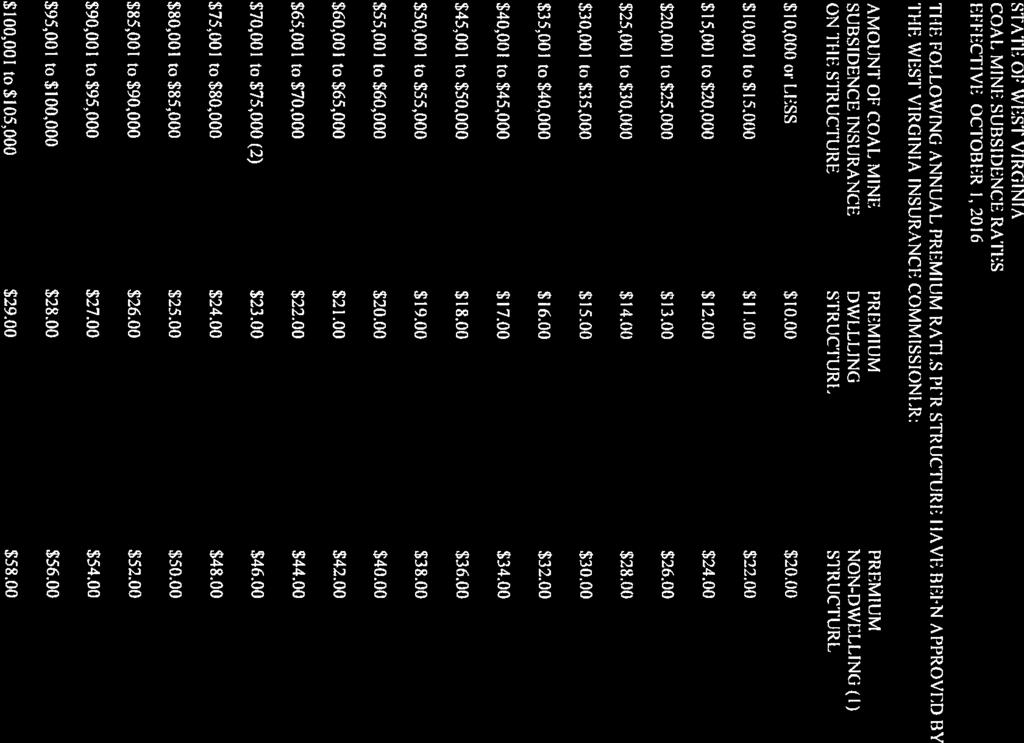

26 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 3.14 Conditional Endorsements Coal Mine Subsidence Coverage Unless waived by the insured, coverage for loss caused by mine subsidence must be provided for structures located in certain counties in this state. In all other counties, coverage for loss to structures caused by mine subsidence must be provided at the request of the insured. Use the rating information shown in this manual. Attach endorsement CL0334 Rev 3/17 Rules 13 AAIS

27 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 4 -- PREMIUM DETERMINATION The basic policy rating information shown in this manual contemplates the property and liability coverages described in Rule 2. Unless liability coverage is deleted, coverage for the following liability exposures is required if they exist: -- all domestic employees of an insured not covered or not required to be covered by Workers' Compensation Insurance; -- all additional or secondary residence premises where an insured maintains a residence, other than business or farm properties; and -- incidental office, professional, private school, or studio occupancies by an insured on residential premises of an insured. Use the rating information shown in this manual. 4.1 Calculation of Premium The premium is computed as follows: Step 1 -- Determine the basic policy premium based on the amount of Coverage A or Coverage C, as applicable, using the basic policy rating information shown in this manual. Step 2 -- Adjust the basic policy premium to reflect the desired deductible. Step 3 -- Adjust the result of Step 2 by any applicable premium modification factors. Step 4 -- Add the result of Step 3 to the charges for any other mandatory or optional property or liability coverages that apply. REV 13.0 Rules - 14 AAIS

28 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 4.2 Modified Loss Settlement Terms -- Coverages A and B -- Forms 1, 2, and 3 This rule does not apply. 4.3 Tenant's Personal Property -- Special Coverage This rule does not apply. 4.4 Unit-Owner's Personal Property -- Special Coverage This rule does not apply. 4.5 Changes in Limits or Addition of Coverages Policy limits may be increased or coverages added during the policy term. Compute the additional premium due on a pro rata basis using the same forms, endorsements, rules, and rating information in effect when the current policy premiums were calculated. REV 13.0 Rules - 15 AAIS

29 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL RULE 5 -- DEDUCTIBLES WEST VIRGINIA A deductible amount is subtracted from all covered property losses, except those losses covered by the following Incidental Property Coverages: Emergency Removal; Fire Department Service Charge; Credit Card, Forgery, and Counterfeit Money; Grave Markers; Loss Assessment; Refrigerated Food Spoilage; and, if applicable, Lock and Garage Door Transmitter Replacement. The deductible amount is subtracted only once per occurrence at each location, regardless of the number of covered items affected. 5.1 Flat Deductibles -- All Perils The policy may be issued with a single deductible amount that applies to all perils. The following flat deductible options are available: Deductible Amount $ 500 1,000 2,500 Use the factors shown in this manual to adjust the premium and show the deductible amount on the declarations. 5.2 $250 Theft Deductible for Coverage C -- Forms 1, 2, 3, and 4 This rule does not apply. 5.3 Higher Windstorm or Hail Deductibles -- Forms 1, 2, 3, 5, and 8 This rule does not apply. REV 1/03 Rules - 16 AAIS

30 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 6 -- PREMIUM MODIFICATIONS 6.1 Protective Devices Use the protective device factors shown in this manual to adjust the premium for the installation of the following approved and properly maintained alarm and/or sprinkler systems: -- Central Station Burglary and/or Fire Alarms -- Fire Department and/or Police Department Alarms -- Local Alarms, including smoke and/or gas detection -- Sprinkler Systems Attach endorsement ML Fire Resistive and Specifically Rated Buildings This rule does not apply. 6.3 Row and Townhouses This rule does not apply. 6.4 Expanded Ordinance or Law Coverage - Forms 1, 2, and 3 (Form 4 -- See Rule 7.17) The limitation that applies to the incidental coverage for ordinance or law (25% of the limit that applies to damaged property) can be removed. When the limitation is removed, the limit that applies to covered property includes coverage for the increased cost which results from the enforcement of a code, ordinance, or law which regulates the use, construction, repair, demolition, or removal of property following a covered loss. If the covered loss plus the increased cost is more than the applicable limit, an extra 10% of the applicable limit is available to cover the increased cost. Use the factor shown in this manual to adjust the premium. Attach endorsement ML-257. REV 13.0 Rules - 17 AAIS

31 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 6.5 Replacement Value -- Personal Property The loss settlement provisions that apply to personal property and various miscellaneous items can be converted from actual cash value coverage to replacement cost coverage. When this option is selected, the personal property limit may not be reduced below the limit specified in Rule 2.6. Use the factors shown in this manual to adjust the premium. Minimum limit for Coverage A is $35,000. And for Form 4, minimum limit for Coverage C is $6,000. Attach endorsement ML Automatic Adjustment of Limits -- Forms 1, 2, 3, 5, and 8 This rule does not apply. 6.7 Expanded Debris Removal Coverage -- Forms 1, 2, and 3 The limitation that applies to the incidental coverage for debris removal (25% of the limit that applies to the damaged property) can be removed. When the limitation is removed, the limit that applies to covered property includes coverage for the cost of removing the debris of that property following a covered loss. If the covered loss plus the cost of debris removal is more than the applicable limit, an extra 5% of the applicable limit is available to cover debris removal. Use the factor shown in this manual to adjust the premium. Attach endorsement ML-420. REV 13.0 Rules - 18 AAIS

32 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 6.8 Individual Risk Premium Modifications This rule is to be applied to recognize special characteristics of the risk that are not fully reflected in the rates. Underwriter discretion (submit to company for review) -40% to +40% REV 04/02 Rules - 19 AAIS

33 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 7 -- OPTIONAL PROPERTY COVERAGES 7.1 Vandalism -- Form 8 Only This rule does not apply. 7.2 Earthquake Coverage for direct physical loss caused by earthquake can be added. Coverage for exterior masonry veneer is optional. A special deductible provision applies to loss caused by earthquake. Forms 1, 2, and 3 -- Apply the rating information shown in this manual to the Coverage A limit shown on the declarations. If the limit that applies to property covered under Coverage C has been increased (including any increase from the attachment of endorsement ML-55), apply the applicable earthquake rating information to the increased amount(s). If any of the optional endorsements for private structures (ML-42, ML-48, or ML-157) are attached, apply the applicable earthquake rating information to the limit shown on the endorsement for each private structure. Form 4 -- Apply the rating information shown in this manual to the Coverage C limit shown on the declarations. If the limit that applies to property covered under the incidental coverage for tenant's improvements has been increased, apply the applicable earthquake rating information to the increased amount(s). For all forms, attach endorsement ML-54. If coverage is provided for exterior masonry veneer, make an entry to show that the masonry veneer exclusion does not apply. REV 13.0 Rules - 20 AAIS

34 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 7.3 Dwelling Under Construction -- Theft Coverage can be provided for theft or attempted theft in or to a residence being built or a newly constructed residence before it is occupied. Coverage also applies to theft of materials and supplies used in construction of the residence. Use the rating information shown in this manual. Attach endorsement ML-422 and make an entry to show the limit that applies. 7.4 Private Structures -- Forms 1, 2, and Increased Limit An additional amount of insurance can be provided for specific private structures that are covered under Coverage B. Use the rating information shown in this manual. Attach endorsement ML-48 and make entries to describe the covered structures and show the additional amount of coverage that applies to each structure Rented to Others This rule does not apply With Incidental Occupancies Coverage for private structures on the described premises with an office, professional, private school, or studio occupancy can be provided. Use the rating information shown in this manual. Attach endorsement ML-42 and make entries to describe the business, describe the covered structures, and show the amount of coverage that applies to each structure. REV 13.0 Rules - 21 AAIS

35 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Care Provided For Others Coverage for private structures on the described premises used in conjunction with providing care for others can be added if liability coverage for the care of others also applies. Use the rating information shown in this manual. Attach endorsement ML-157 and make entries to describe the covered structures and show the amount of coverage that applies to each structure Away From Premises -- Coverage B Extension This rule does not apply Away From Premises -- Specifically Scheduled Structures This rule does not apply. 7.5 Personal Property Increased Limit -- Forms 1, 2, and 3 The Coverage C limit can be increased. Use the rating information shown in this manual. Show the Coverage C limit on the declarations Reduced Limit -- Forms 1, 2, 3, 5, and 8 This rule does not apply In Residences Occasionally Rented (Not applicable to Form 4 with ML-430, Form 5, Form 6 with ML-429, or Form 8) This rule does not apply In Units Regularly Rented to Others -- Form 6 only (Not applicable if ML-429 is attached) This rule does not apply. REV 13.0 Rules - 22 AAIS

36 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 7.6 Accidental Discharge -- Water-filled Furniture Coverage can be provided for direct physical loss to covered property caused by the accidental discharge or overflow of liquids from waterfilled furniture. Use the rating information shown in this manual. Attach endorsement ML Money and Securities The special limits under Coverage C that apply to loss to money, securities, and related items can be increased. Use the rating information shown in this manual. Attach endorsement ML-65 and make entries to show the amount of each increase and the total limits that apply. 7.8 Unscheduled Jewelry, Watches, and Furs -- Forms 1, 2, 3, and 4 The special limit under Coverage C that applies to loss to unscheduled jewelry, watches, and furs can be increased. Use the rating information shown in this manual. Attach endorsement ML-65 and make an entry to show the amount of the increase and the total limit that applies. 7.9 Guns -- Forms 1, 2, 3, and 4 The special limit under Coverage C that applies to loss to guns can be increased. Use the rating information shown in this manual. Attach endorsement ML-65 and make an entry to show the amount of the increase and the total limit that applies. REV 13.0 Rules - 23 AAIS

37 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 7.10 Silverware, Goldware, and Pewterware -- Forms 1, 2, 3, and 4 The special limit under Coverage C that applies to loss to silverware, goldware, and pewterware can be increased. Use the rating information shown in this manual. Attach endorsement ML-65 and make an entry to show the amount of the increase and the total limit that applies Business Property The special limit under Coverage C for loss to personal property used for business purposes while on the insured premises can be increased. Use the rating information shown in this manual. The special limit that applies to personal property used for business purposes while away from the insured premises is automatically increased to 10% of the total limit that applies to personal property used for business purposes while on the insured premises. Attach endorsement ML-65 and make an entry to show the amount of the increase and the total limit that applies Electronic Devices The special limit under Coverage C that applies to loss to electronic devices, accessories, and antennas that can be operated from the electrical system of a motorized vehicle or watercraft and other sources of power can be increased. Use the rating information shown in this manual. Attach endorsement ML-65 and make an entry to show the amount of the increase and the total limit that applies. REV 13.0 Rules - 24 AAIS

38 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 7.13 Computers WEST VIRGINIA Coverage for computer data processing equipment and software can be provided for all risks of direct physical loss, with certain exceptions. Use the rating information shown in this manual. Attach endorsement ML-170 and make entries to describe the covered property and show the limits that apply Refrigerated Food Spoilage The limit that applies to the incidental coverage for refrigerated food spoilage can be increased. Use the rating information shown in this manual. Attach endorsement ML-30 and make an entry to show the amount of the increase and the total limit that applies Additional Living Costs and Loss of Rent This rule does not apply Credit Cards and Depositors Forgery The limit that applies to the incidental coverage for loss by forgery or alteration of credit cards, checks or drafts, or acceptance of counterfeit paper currency can be increased. Use the rating information shown in this manual. Attach endorsement ML-30 and make an entry to show the amount of the increase and the total limit that applies Tenant's Improvements -- Form 4 only The limit that applies to the incidental coverage for tenant's improvements (10% of the Coverage C limit) can be increased. Use the rating information shown in this manual. REV 13.0 Rules - 25 AAIS

39 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA When establishing the limit for tenant's improvements, consider that the limit includes coverage for the increased cost which results from the enforcement of a code, ordinance, or law which regulates the use, construction, repair, demolition, or removal of property following a covered loss. Attach endorsement ML-30 and make an entry to show the amount of the increase and the total limit that applies Fire Department Service Charge The limit that applies to the incidental coverage for fire department service charges can be increased. Use the rating information shown in this manual. Attach endorsement ML-30 and make an entry to show the amount of the increase and the total limit that applies Scheduled Personal Property Coverage for scheduled personal property can be provided against all risks of direct physical loss, with certain exceptions. New items over $2,000 require a Bill of Sale. Items over one year old and over $2,000 require a current appraisal. Any scheduled personal property item over $5,000 requires company approval to bind. Use the rating information shown in this manual. Attach endorsements ML-61 and ML-61A and make entries to describe the covered property and show the limits that apply Scheduled Recreational Motor Vehicles Coverage for recreational motor vehicles can be provided for direct physical loss caused by any of the Coverage C perils. Use the rating information shown in the State Rate Pages. Describe the covered recreational motor vehicles on Endorsement ML-504 and make entries to show the limits that apply. REV 13.1 Rules - 26 AAIS

40 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 7.20 Scheduled Glass -- Forms 1, 2, and 3 Coverage for scheduled glass that is part of a building covered under Coverages A or B can be provided against all risks of direct physical loss, with certain exceptions. Use the rating information provided by the company. Attach endorsement ML-68 and make entries to describe the covered glass and show the limits that apply Water Damage -- Sewers, Drains, and Sumps Coverage for direct physical loss caused by water that backs up through sewers or drains or overflows from a sump can be added for property covered under Coverages A, B, and C. A $250 deductible applies, and coverage is limited to $5,000. Use the rating information shown in this manual. Attach endorsement ML Loss Assessment Increased Limit -- Described Location The limit that applies to the incidental property and liability coverages for loss assessment arising out of the described location can be increased. Coverage for assessments resulting from a deductible in the insurance purchased by the association is limited to $1,500. Use the rating information shown in this manual. Attach endorsement ML-50 and make entries to show the amount of the increase and the total limit. REV 13.0 Rules - 27 AAIS

41 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Additional Locations The incidental property and liability coverages for loss assessment can be extended to apply to additional locations owned or rented by an insured. A specific limit applies at each additional location. Use the rating information shown in this manual. Attach endorsement ML-50 and make entries to show the location and amount of coverage that applies for each premises Earthquake Coverage for loss assessment arising from direct loss to property caused by earthquake can be added. Use the rating information shown for Rule 7.2 in this manual. Attach endorsement ML Coverage A Options -- Form 6 only This rule does not apply Golf Carts Coverage for direct physical loss to specified golf carts caused by a Coverage C peril or collision or overturn can be added. Use the rating information shown in this manual. Attach endorsement ML-431 and make entries to describe the covered property and show the limit that applies Expanded Replacement Cost -- Forms 1, 2, 3, and 5 (Not applicable if ML-15 is attached) This rule does not apply. REV 13.0 Rules - 28 AAIS

42 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 7.26 Animal Collision (Applicable only if ML-29 or ML-320 is attached) Coverage for loss by death to cattle, horses, mules, donkeys, hogs, sheep, or goats owned by the insured can be added to policies that include coverage for liability arising out of farming activities. Loss must occur while the animal is on a public road and must be caused or made necessary by collision between the animal and a vehicle not owned or operated by an insured. Use the rating information shown in this manual. Attach endorsement ML-337. REV 13.0 Rules - 29 AAIS

43 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 8 -- OPTIONAL LIABILITY COVERAGES All mandatory and optional liability coverages must be written at the same limit, except as noted in Rule Increased Limits -- Coverages L and M The limits for Coverages L and M can be increased. Use the rating information shown in this manual. 8.2 Reduced Coverage L Limit This rule does not apply. 8.3 Reduced Coverage M Limit This rule does not apply. 8.4 Three and Four Family Dwellings -- Forms 1, 2, 3, 5, and 8 This rule does not apply. 8.5 Domestic Employees Coverage for liability arising out of injuries sustained by domestic employees of an insured not covered or not required to be covered by Workers' Compensation Insurance is included under the liability section of the policy. A charge is required for each domestic employee in excess of two, except: -- employees working less than half of the customary full time; or -- employees to whom the policy's Coverage L exclusion for bodily injury to persons covered or required to be covered by workers' compensation insurance applies. Use the rating information shown in this manual. Make an entry on the declarations to show the number of domestic employees. REV 13.1 Rules - 30 AAIS

44 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 8.6 Additional Residence Premises -- Occupied by an Insured Coverage for liability arising out of all additional or secondary residence premises where an insured maintains a residence, other than business or farm properties, is required. Use the rating information shown in this manual. Make entries on the declarations to show the locations of all additional and secondary residence premises to which the liability coverages apply. 8.7 Additional Residence Premises -- Rented to Others Coverage for liability arising out of additional one to four family dwellings owned by the insured and rented or held for rental to others can be added. Use the rating information shown in this manual. Attach endorsement ML-70 and make entries to show the location(s) of the covered premises and to indicate the number of families at each premises. 8.8 Private Structures -- Rented to Others This rule does not apply. 8.9 Waterbed Liability -- Form 4 Coverage for liability for property damage arising out of the ownership or use of a waterbed on the insured premises can be added. Use the rating information shown in this manual. Attach endorsement ML-209. REV 13.0 Rules - 31 AAIS

45 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 8.10 Business Activities -- Business Not Owned by the Insured Coverage for liability arising out of an insured's business activities, other than activities related to a business of which the insured is sole owner or a partner, can be added. Use the rating information shown in this manual. Eligible business activities are classified as shown below. Make the appropriate charge for each covered person. Classifications: Clerical Office Employees Engaged wholly in office work and having no other duty in or about the employer's premises Salespersons, Collectors, or Messengers No installation, demonstration, or service operations Salespersons, Collectors, or Messengers Including installation, demonstration, or service operations Teachers Athletic, laboratory, manual training, physical training, or swimming instruction, excluding coverage for liability arising out of the corporal punishment of pupils Teachers Not otherwise classified, excluding coverage for liability arising out of the corporal punishment of pupils Teachers Coverage for liability arising out of the corporal punishment of pupils. The additional premium for this classification must be added to the premium for classifications or REV 13.0 Rules - 32 AAIS

46 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA Refer to the company for occupations not classified. Attach endorsement ML-71 and make entries to show the names of the covered persons and the covered business activities. If applicable, make an entry to show that coverage for liability arising out of the corporal punishment of pupils is included Office, Professional, Private School, or Studio Occupancy Coverage for liability arising out of an incidental office, professional, private school, or studio occupancy in the residence, in a related private structure on the insured premises, or at an additional residence premises occupied by the insured can be added when: -- the premises are occupied principally for residential purposes; -- the business is conducted by an insured; and -- there is no other business conducted on the premises. Use the rating information shown in this manual. Attach endorsement ML-42 and make entries to describe the business and its location Owned Snowmobiles -- Off Premises Coverage for liability arising out of the off-premises use of snowmobiles owned by an insured who resides in the named insured's household can be added. A separate charge applies for each covered snowmobile. Use the rating information shown in this manual. Attach endorsement ML-164 and make entries to describe each covered snowmobile. REV 13.0 Rules - 33 AAIS

47 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 8.13 Watercraft WEST VIRGINIA Coverage for liability arising out of the use of certain types of watercraft can be added. Use the rating information shown in this manual. For rating purposes, combine the horsepower of all outboard motors used together with any single watercraft owned by the insured. Classify sailboats that are 26 to 40 feet (inclusive) in length and are equipped with auxiliary power as inboard motor boats. Attach endorsement ML-75 and make entries to describe each covered watercraft Personal Injury -- Forms 1, 2, 3, and 4 Personal liability coverage can be extended to include coverage for personal injury. Personal injury means damages for which the insured is liable arising out of offenses such as false arrest, libel, slander, and invasion of privacy of another. Use the rating information shown in this manual. Attach endorsement ML Care Provided For Others Coverage for liability arising out of care provided by an insured for up to three persons on the insured premises as a business activity can be added. Use the rating information shown in this manual. The rating information shown reflects an annual aggregate limit that is equal to the Coverage L limit. Attach endorsement ML-157 and make entries to describe the location of the business and show the annual aggregate limit. REV 13.0 Rules - 34 AAIS

48 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL 8.16 Golf Cart Liability Coverage This rule does not apply. WEST VIRGINIA 8.17 Motorized Vehicle Liability Coverage This rule does not apply. REV 13.0 Rules - 35 AAIS

49 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE 9 -- OPTIONAL FARM COVERAGES -- LIABILITY All mandatory and optional liability coverages must be written at the same limit. 9.1 Incidental Farming When farming is not the business of the insured, coverage for liability arising out of an insured's incidental farming activities on or away from the insured premises can be added. Incidental farming includes activities such as the farming of garden plots and the grazing of small numbers of animals. Use the rating information shown in this manual. Attach endorsement ML-320 and make an entry to show the location of the farming activities. 9.2 Farm Personal Liability Coverage for liability arising out of farm premises located away from the insured premises can be added. The eligibility of the following risks must be determined by the company: -- farms where business activities other than farming are conducted; -- farms where horses are raised, boarded, or maintained; -- vacant or unoccupied farms; -- farms that are operated to supply agricultural commodities for manufacturing or processing by the insured for sale to others; -- farms involving the retail sale of farm products or farms that permit the picking of fruits or vegetables by the public; and REV 13.0 Rules - 36 AAIS

50 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL -- incorporated farms. WEST VIRGINIA Use the rating information shown in this manual. Charges must be made for the initial farm exposure and for each additional farm premises owned by or rented to an insured. Attach endorsement ML Initial Farm Exposure This includes: -- the initial farm premises, which is the largest parcel of farm land with outbuildings(s), whether owned and operated by an insured, owned by an insured and rented to others, or rented to an insured; and -- all additional farm premises without outbuildings maintained by an insured and used in conjunction with the above, including any otherwise unclassified vacant farm land. Any dwellings located on the farm premises and owned by or rented to an insured are to be rated as additional residence premises Each Additional Farm Premises This includes any additional farm premises with outbuildings(s), whether owned and operated by the insured, owned by the insured and rented to others, or rented to the insured. It also includes all vacant farm land used in conjunction with it. Any dwellings located on additional farm premises and owned by or rented to an insured are to be rated as additional residence premises. REV 13.0 Rules - 37 AAIS

51 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA 9.3 Employer's Liability -- Farm Employees (Applicable only if ML-29 is attached) Liability and medical payments coverage for injuries sustained by farm employees during the course of their employment can be added to policies that include farm personal liability coverage. Use the rating information shown in this manual. Attach endorsement ML-311 and make entries to show the rating basis and premium. 9.4 Custom Farming (Applicable only if ML-29 attached) This rule does not apply. 9.5 Fruit or Vegetable "Pick Your Own" Operations (Applicable only if ML-29 is attached) This rule does not apply. 9.6 Horse Boarding (Applicable only if ML-29 is attached) This rule does not apply. 9.7 Farm Chemical Limited Liability (Applicable only if ML-29 and a pollution exclusion endorsement are attached) This rule does not apply. 9.8 Crop Dusting (Applicable only if ML-29 is attached) This rule does not apply. 9.9 Products Aggregate Limit (Applicable only if ML-29 is attached) This rule does not apply. REV 13.0 Rules - 38 AAIS

52 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL WEST VIRGINIA RULE ADDITIONAL AND SECONDARY LOCATIONS This rule does not apply. REV 13.0 Rules - 39 AAIS

53 FARMERS MUTUAL INSURANCE COMPANY AMERICAN ASSOCIATION OF INSURANCE SERVICES HOMEOWNERS MANUAL Masonry WEST VIRGINIA CONSTRUCTION DEFINITIONS A building with walls of masonry veneered construction is to be classified as Masonry. Frame A building with walls of frame, or metal-sheathed or stuccoed frame construction, or with walls of metal or metal lath and plaster on combustible supports is to be classified as Frame. Mixed Construction A building is to be classed as Frame when the wall area of frame construction (including gables) exceeds 33-1/3% of the total wall area. REV 10/97 Def -1

54 FARMERS MUTUAL INSURANCE COMPANY WV HOMEOWNERS & PREFERRED MOBILE HOMEOWNERS TERRITORIAL DEFINITIONS Territory 1 Territory 2 Territory 3 Territory 4 Boone Brooke Cabell Lincoln Braxton Barbour Fayette Logan Berkeley Clay Nicholas McDowell Calhoun Gilmer Kanawha Mercer Doddridge Hancock Summers Mingo Grant Harrison Webster Wayne Greenbrier Marshall Wyoming Hampshire Mason Hardy Monroe Jackson Ohio Jefferson Putnam Lewis Raleigh Marion Roane Mineral Tyler Monongalia Wetzel Morgan Pendleton Pleasants Pocahontas Preston Randolph Ritchie Tucker Taylor Upshur Wirt Wood PROTECTION CLASS PROCEDURES CLASS 1-7 Protection class established throughout a specified area 8 Five miles or less from a fire dept & a hydrant within 1,000 feet 9 Five miles or less from a fire dept & a hydrant more than 1,000 feet 10 Over five miles from a fire dept Rev 11/11 DEF-2 FMIC

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class 10 15, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,044 85, ,098 90, ,157 95, , , , , ,309 1 Revised 01/01/2010

72 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class , , , , , ,027 1, , ,057 1,469 1 Revised 01/01/2010

73 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class 10 15, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,017 80, ,075 85, ,132 90, ,193 95, , , , , ,355 2 Revised 01/01/2010

74 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class , ,013 1, , ,053 1, , ,093 1, , ,133 1,555 2 Revised 01/01/2010

75 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class 10 15, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,017 75, ,063 80, ,122 85, ,183 90, ,247 95, , , , , ,007 1,410 3 Revised 01/01/2010

76 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class , ,037 1, , ,067 1, , ,097 1, , ,127 1,590 3 Revised 01/01/2010

77 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class 10 15, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,023 70, ,062 75, ,109 80, ,171 85, ,234 90, ,301 95, , , ,010 1, , ,050 1,459 4 Revised 01/01/2010

78 Farmer Mutual Insurance Company Preferred Double Wide Mobile Homeowners Form No Coverage Amount 3 Protection Class 1-7 Protection Class 8 Protection Class 9 Territory Protection Class , ,090 1, , ,130 1, , ,170 1, , ,210 1,659 4 Revised 01/01/2010

79 RULE 3.5 Additional Interests FARMERS MUTUAL INSURANCE COMPANY WV HOMEOWNERS RATES POLICYWRITING INSTRUCTIONS & PREMIUM DETERMINATION Interests in coverage A & B & premises liability- Form 1, 2 & 3 ATTACH ENDORSEMENT ML-41 $25. PER POLICY Residents of the household THIS RULE DOES NOT APPLY Landlords THIS RULE DOES NOT APPLY 3.9 Contributing insurance Credit for liability coverage $11. All policies must contain the same deductible. All additional limits & coverage must be divided between companies. Scheduled personal property can be shared at option of companies. Liability must be assumed by one company. All policies must include the policy number & must identify the company providing liability. See rule 3.9, page 11. ATTACH ENDORSEMENT ML Modified loss settlement terms THIS RULE DOES NOT APPLY 4.3 Tenants personal property Special coverage THIS RULE DOES NOT APPLY 4.4 Unit-owners personal property Special coverage THIS RULE DOES NOT APPLY Rev 1/12 Page 8

80 FARMERS MUTUAL INSURANCE COMPANY WEST VIRGINIA HOMEOWNERS RATES DEDUCTIBLES & PREMIUM MODIFICATIONS RULE 5.1 FLAT DEDUCTIBLES ALL PERILS $500 0% $1,000-10% $2,500-18% Deductible does not apply to all coverage. Use percentages to adjust the premium and show the deductible on the declarations. 5.2 $250 THEFT DEDUCTIBLE FOR COVERAGE C This rule does not apply 5.3 HIGHER WINDSTORM OR HAIL DEDUCTIBLE This rule does not apply 6.1 PROTECTIVE DEVICES Central station burglary and/or fire alarms 5% Fire department and/or police department alarms 3% Local alarms, including smoke and/or gas detection 2% Sprinkler systems 3% Use the protective device percentages to adjust the premium ATTACH ENDORSEMENT ML FIRE RESISTIVE & SPECIFICALLY RATED BUILDINGS This rule does not apply 6.3 ROW & TOWNHOUSES This rule does not apply Rev. 9/12 Page 9

81 FARMERS MUTUAL INSURANC COMPANY HOMEOWNERS RATES WV PREMIUM MODIFICATIONS RULE 6.4 EXPANDED ORDINANCE OR LAW Forms 1, 2 & 3 +10% Form 4 see rule 7.17 rules page 32 The use of this endorsement removes the 25% of damage limit & provides incurred cost for increased cost resulting from an ordinance or law. If damage exceeds limit an additional 10% is granted. Attach Endorsement ML REPLACEMENT VALUE PERSONAL PROPERTY $43 ANNUAL PREMIUM Personal property may be converted from ACV to replacement cost. Minimum limit requirements Form 1, 2 & 3 Coverage A $35,000 Form 4 Coverage C $ 6,000 Attach Endorsement ML AUTOMATIC ADJUSTMENT OF LIMITS THIS RULE DOES NOT APPLY 6.7 EXPANDED DEBRIS REMOVAL +5% The use of this endorsement removes the 25% of damage limit & provides incurred cost for debris removal. If damage exceeds limit, an additional 5% is granted. Attach Endorsement ML420 Rev. 4/1/12 HO-Page 10 AAIS

82 Farmers Mutual Insurance Company West Virginia Homeowners Rates PREMIUM MODIFICATIONS AND OPTIONAL PROPERTY COVERAGES RULE 6.8 INDIVIDUAL RISK PREMIUM MODIFICATIONS THIS RULE IS TO BE APPLIED TO RECOGNIZE SPECIAL CHARACTERISTICS OF THE RISK THAT ARE NOT FULLY REFLECTED IN THE RATES. UNDERWRITER DISCRETION (SUBMIT TO COMPANY FOR REVIEW -40% TO +40%) 7.1 VANDALISM - FORM 8 ONLY THIS RULE DOES NOT APPLY 7.2 EARTHQUAKE - RATING INFORMATION PER $1,000 OF INSURANCE* FRAME ALL OTHERS FORMS 1, 2, AND 3 $0.20 $0.40 AND LOSS ASSESSMENT (ML-53) FORM 4 INCLUDING HIGHER LIMITS OF TENANT'S IMPROVEMENTS AND COVERAGE A RELATED PRIVATE STRUCTURE OPTIONS COVERAGE FOR DIRECT PHYSICAL LOSS CAUSED BY AN EARTHQUAKE CAN BE ADDED * COVERAGE FOR MASONRY VENEER IS OPTIONAL, REFER TO ENDORSEMENT. IF THE VENEER EXCLUSION APPLIES, RATE AS "FRAME"; IF NOT, RATE AS ALL OTHERS. ATTACH ENDORSEMENT ML-54 04/02 Page 11

83 FARMERS MUTUAL INSURANCE COMPANY WV HOMEOWNERS RATES OPTIONAL PROPERTY COVEFRAGES RULE RATE PER AMT OF INS 7.3 DWELLING UNDER CONSTRUCTION THEFT $20 PER $1,000 Coverage for theft or attempted theft can be added to a residence being built or newly constructed residence before it is occupied, including building materials & supplies. ENDORSEMENT ML-422 MAKE ENTRY TO SHOW LIMIT THAT APPLIES 7.4 PRIVATE STRUCTURES INCREASED LIMITS $6 PER $1,000 ENDORSEMENT ML-48 Additional amount can be provided for specific structures covered under coverage B Description & photos of covered structure needed RENTED TO OTHERS THIS RULE DOES NOT APPLY WITH INCIDENTAL OCCUPANCIES $4 PER $1,000 ENDORSEMENT ML-42 Private structures on described premises with an office, professional, private school or studio Need description & photo of structure, description of business & amount of coverage CARE PROVIDED FOR OTHERS $4 PER $1,000 Coverage for private structures used in conjunction with providing care for others can be added If liability coverage for the care of others also applies AWAY FROM PREMISES COVERAGE B EXTENSION THIS RULE DOES NOT APPLY Rev 1/1/13 Page 12 AAIS

84 Farmers Mutual Insurance Company Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE Away from premises-specifically Scheduled structures RATE PER AMOUNT OF INSURANCE THIS RULE DOES NOT APPLY 7.5 Personal Property Increased Limit $1.05 per $1,000. Coverage C can be increased. Show on declarations Reduced Limit THIS RULE DOES NOT APPLY In residences Occasionally rented THIS RULE DOES NOT APPLY In units Regularly rented THIS RULE DOES NOT APPLY 7.6 Accidental discharge $10 per policy Water filled furniture Coverage can be provided for direct physical loss to covered property caused by accidental discharge or overflow of liquids from water filled furniture ATTACH ENDORSEMENT ML-421 Rev. 11/11 Page 13

85 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATING PER AMOUNT INFORMATION OF INSURANCE 7.7 MONEY AND SECURITIES MONEY $6.00 $100 AUTOMATIC COVERAGE OF $250 CAN BE INCREASED. SECURITIES $4.00 $100 AUTOMATIC COVERAGE OF $1,500 CAN BE INCREASED. ATTACH ENDORSEMENT ML UNSCHEDULED JEWELRY, WATCHES, AND FURS $9.00 $500 AUTOMATIC COVERAGE OF $2,500, FOR LOSS BY THEFT ONLY, CAN BE INCREASED. ATTACH ENDORSEMENT ML GUNS & GUN ACCESSORIES $2.00 $100 AUTOMATIC COVERAGE OF $2,500 FOR LOSS BY THEFT ONLY, CAN BE INCREASED. ATTACH ENDORSEMENT ML SILVERWARE, GOLDWARE, AND PEWTERWARE $0.50 $100 AUTOMATIC COVERAGE OF $2,500 FOR LOSS BY THEFT ONLY, CAN BE INCREASED. ATTACH ENDORSEMENT ML BUSINESS PROPERTY $1.00 $500 AUTOMATIC COVERAGE OF $2,500 WHILE ON INSURED PREMISES 10% OF BUSINESS PROPERTY COVERAGE APPLIES WHILE OFF PREMISES ATTACH ENDORSEMENT ML-65 10/97 Page 14

86 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATING PER AMOUNT INFORMATION OF INSURANCE 7.12 ELECTRONIC DEVICES $10.00 $500 AUTOMATIC COVERAGE OF $1,500 CAN BE INCREASED. ATTACH ENDORSEMENT ML COMPUTERS DATA PROCESSING EQUIPMENT $2.00 $100 SOFTWARE COVERAGE CAN BE PROVIDED FOR ALL RISKS OF DIRECT PHYSICAL LOSS, WITH CERTAIN EXCEPTIONS. NEED DESCRIPTION OF PROPERTY AND THE LIMIT. ATTACH ENDORSEMENT ML REFRIGERA TED FOOD SPOILAGE $5.00 $500 AUTOMATIC COVERAGE IS $500 ATTACH ENDORSEMENT ML ADDITIONAL LIVING COST AND LOSS OF RENT THIS RULE DOES NOT APPLY 7.16 CREDIT CARD AND DEPOSITORS FORGERY AMOUNT OF TOTAL RATING INFORMATION INCREASE LIMIT PER POLICY $1,000 $2,500 $2.00 3,500 5, ,000 7, ,500 10, $1,500 PER OCCURRENCE IS THE MOST THAT WILL BE PAID UNLESS A HIGHER LIMIT IS ADDED. ATTACH ENDORSEMENT ML-30 10/97 Page 15

87 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATE PER AMOUNT OF INSURANCE 7.17 TENANTS IMPROVEMENTS $3 PER $1,000 FORM 4 ONLY AUTOMATIC COVERAGE OF 10% OF COVERAGE C CAN BE INCREASED. WHEN ESTABLISHING LIMIT, CONSIDER THE LIMIT INCLUDES INCREASED COST WHICH RESULTS FROM THE ENFORCEMENT OF A CODE, ORDINANCE, OR LAW WHICH REGULATES THE USE, CONSTRUCTION, REPAIR, DEMOLITION, OR REMOVAL OF PROPERTY FOLLOWING A COVERED LOSS. ATTACH ENDORSEMENT ML FIRE DEPARTMENT $2 PER $100 SERVICE CHARGE AUTOMATIC COVERAGE OF $500 CAN BE INCREASED ATTACH ENDORSEMENT ML SCHEDULED PERSONAL PROPERTY 1. JEWELRY, AS SCHEDULED. $0.85 PER $ FURS AND GARMENTS TRIMMED WITH FUR $0.50 PER $100 OR CONSISTING PRINCIPALLY OF FUR AS SCHEDULED. 3. CAMERAS, PROJECTION MACHINES, FILMS, $1.80 PER $100 AND RELATED ARTICLES OF EQUIPMENT AS SCHEDULED. 4. MUSICAL INSTRUMENTS AND RELATED $0.65 PER $100 ARTICLES OF EQUIPMENT, AS SCHEDULED. 5. SILVERWARE, GOLDWARE, ITEMS PLATED $0.70 PER $100 WITH GOLD OR SILVER, AND PEWTE RWARE; AS SCHEDULED, BUT EXCLUDING PENS, PENCILS, FLASKS, SMOKING IMPLEMENTS AND JEWELRY. 6. GOLFERS' EQUIPMENT, MEANING GOLF BALLS, $1.00 PER $100 CLUBS AND BAGS; GOLF CLOTHING; AND OTHER GOLFING EQUIPMENT AS SCHEDULED. THIS INCLUDES STREET CLOTHES KEPT IN A LOCKER WHILE AN INSURED IS GOLFING. 10/97 Page 16

88 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATE PER AMOUNT OF INSURANCE 7.19 SCHEDULED PERSONAL PROPERTY (CONT'D) 7. FINE ARTS, AS SCHEDULED. THIS PREMIUM $0.65 PER $100 IS BASED ON YOUR STA TEMENT THAT THE COVERED PROPERTY IS AT THE LOCATION DESCRIBED IN THE ENDORSEMENT. 8. POSTAGE STAMPS, INCLUDING DUE, ENVELOPE $0.55 PER $100 OFFICIAL REVENUE, MATCH AND MEDICINE STAMPS, COVERS; LOCALS; REPRINTS; ESSAYS; PROOFS; AND OTHER PHILA TELIC PROPERTY AS SCHEDULED. INCLUDING THEIR BOOKS, PAGES, AND MOUNTINGS, OWNED BY OR IN THE CUSTODY OR CONTROL OF AN "INSURED". 9. RARE AND CURRENT COINS, MEDALS, PAPER $2.00 PER $100 MONEY BANK NOTES, TOKENS OF MONEY AND OTHER NUMISMATIC PROPERTY, INCLUDING COIN ALBUMS, CONTAINERS, FRAMES, CARDS, DISPLAY CABINETS IN USE WITH SUCH COLLECTION OWNED BY OR IN THE CUSTODY OR CONTROL OF AN "INSURED". 10. BICYCLES AND RELATED EQUIPMENT $1.00 PER $ OTHER PERSONAL PROPERTY AS SCHEDULED $1.00 PER $ GUNS AND GUN ACCESSORIES $2.50 PER $100 APPLIES TO ITEMS 1-12: COVERAGE CAN BE PROVIDED AGAINST ALL RISKS OF DIRECT PHYSICAL LOSS, WITH CERTAIN EXCEPTIONS. NEW ITEMS OVER $2,000 REQUIRE A BILL OF SALE. ITEMS OVER 1 YEAR OLD AND OVER $2,000 REQUIRE A CURRENT APPRAISAL. ANY SCHEDULED PERSONAL PROPERTY ITEM OVER $5,000 REQUIRES COMPANY APPROVAL TO BIND. ATTACH ENDORSEMENTS ML-61 AND ML-61A SCHEDULED RECREATIONAL MOTOR VEHICLES $35.00 PER $1,000 COVERA GE CAN BE PROVIDED FOR DIRECT PHYSICAL LOSS CAUSED BY ANY OF COVERAGE C PERILS. NEED DESCRIPTION OF RECREATIONAL VEHICLE AND THE LIMITS THAT APPLY ATTACH ENDORSEMENT ML-504 8/98 Page 17

89 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATE PER AMOUNT OR INSURANCE 7.20 SCHEDULED GLASS COVERAGE FOR SCHEDULED GLASS THAT IS PART OF A BUILDING COVERED UNDER COVERAGE A OR B CAN BE PROVIDED AGAINST ALL RISKS OF DIRECT PHYSICAL LOSS, WITH CERTAIN EXCEPTIONS ATTACH ENDORSEMENT ML WATER DAMAGE-SEWERS $25.00 PER POLICY DRAINS, AND SUMPS COVERAGE FOR DIRECT PHYSICAL LOSS CAUSED BY WATER THAT BACKS UP THROUGH SEWERS OR DRAINS OR OVERFLOWS FROM A SUMP CAN BE ADDED FOR PROPERTY COVERED UNDER A, B, AND C. $250 DEDUCTIBLE APPLIES AND COVERAGE IS LIMITED TO $5,000. ATTACH ENDORSEMENT ML LOSS ASSESSMENT INCREASED LIMIT AMOUNT OF TOTAL RATING INFORMATION INCREASE LIMIT PER POLICY $3,500 $5,000 $4.00 8,500 10, EACH ADD'L $5, THE LIMIT THAT APPLIES TO INCIDENTAL PROPERTY AND LIABILITY COVERAGE CAN BE INCREASED. COVERAGE FOR ASSESSMENTS RESULTING FROM A DEDUCTIBLE IN THE INSURANCE PURCHASED BY THE ASSOCIATION IS LIMITED TO $1,500. NEED AMOUNT OF INCREASE. ATTACH ENDORSEMENT ML-50 10/97 Page 18

90 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATING INFORMATION ADDITIONAL LOCATIONS PER POLICY LIMIT $1,500 $8.00 5, , EACH ADD'L $5, THE INCIDENTAL PROPERTY AND LIABILITY COVERAGE FOR LOSS ASSESSMENT CAN BE EXTENDED TO APPLY TO ADDITIONAL LOCATIONS OWNED OR RENTED BY AN INSURED. SPECIFIC LIMIT APPLIES AT EACH LOCATION. NEED LOCATION AND AMOUNT OF COVERAGE THAT APPLIES FOR EACH PREMISES. ATTACH ENDORSEMENT ML EARTHQUAKE - RATING INFORMATION PER $1,000 OF INSURANCE FRAME ALL OTHERS FORMS 1, 2, AND 3 AND LOSS ASSESSMENT (ML-53) $0.20 $0.40 FORM 4 INCLUDING HIGHER LIMITS OF TENANT'S IMPROVEMENTS AND COVERAGE A RELATED PRIVATE STRUCTURE OPTIONS ATTACH ENDORSEMENT ML-54 *COVERAGE FOR MASONRY VENEER IS OPTIONAL REFER TO ENDORSEMENT. IF THE VENEER EXCLUSION APPLIES, RATE AS "FRAME"; IF NOT, RATE AS ALL OTHERS. ATTACH ENDORSEMENT ML COVERAGE A OPTION THIS RULE DOES NOT APPLY 10/97 Page 19

91 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONAL PROPERTY COVERAGES RULE RATE PER AMOUNT OF INSURANCE 7.24 GOLF CARTS $0.50 PER $100 FORMS 1, 2, 3, AND 4 COVERAGE FOR DIRECT PHYSICAL LOSS TO SPECIFIED GOLF CARTS CAUSED BY COVERAGE C PERIL OR COLLISION OR OVERTURN CAN BE ADDED. NEED DESCRIPTION AND LIMIT. ATTACH ENDORSEMENT ML EXPANDED REPLACEMENT COST THIS RULE DOES NOT APPLY 7.26 ANIMAL COLLISION - $400 LIMIT PER ANIMAL ESTIMATED NO. OF HEAD RATING INFORMATION $ , COVERAGE FOR LOSS BY DEATH TO CATTLE, HORSES, MULES, DONKEYS, HOGS, SHEEP, OR GOATS OWNED BY THE INSURED CAN BE ADDED TO POLICIES THAT INCLUDE FARMING LIABILITY. (MUST HAVE ML-29, FARM LIABILITY OR ML-320, INCIDENTAL FARMING ADDED TO POLICY). ATTACH ENDORSEMENT ML /97 Page 20

92 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONS LIABILITY COVERAGES LIMITS INCLUDE $1,000 MED MAXIMUM ADD'L IS $5,000 EACH ADD'L RULE $25 $50 $100 $300 $500 $1MIL $1,000 MED 8.1 INCREASED LIMITS COVERAGE L AND M $0 $0 $14 $21 $26 $31 $3 8.2 REDUCED COVERAGE L LIMIT THIS RULE DOES NOT APPLY 8.3 REDUCED COVERAGE M LIMIT THIS RULE DOES NOT APPLY 8.4 THREE AND FOUR FAMILY DWELLINGS THIS RULE DOES NOT APPLY 8.5 DOMESTIC EMPLOYEES PER EMPLOYEE $3 $4 $5 $6 $7 $3 A CHARGE IS REQUIRED FOR EACH DOMESTIC EMPLOYEE IN EXCESS OF TWO, IF WORKING MORE THAN HALF OF THE CUSTOMARY FULL TIME; OR EMPLOYEES TO WHOM THE POLICY'S COVERAGE L EXCLUSION FOR BODILY INJURY TO PERSONS COVERED OR REQUIRED TO BE COVERED BY WORKERS COMP. NEED THE NUMBER OF EMPLOYEES. 8.6 ADDITIONAL RESIDENCE PREMISES OCCUPIED BY INSURED $4 $5 $6 $7 $8 $2 COVERAGE FOR LIABILITY FOR ALL ADDITIONAL OR SECONDARY RESIDENCE PREMISES WHERE AN INSURED MAINTAINS AS A RESIDENCE, OTHER THAN BUSINESS OR FARM PROPERTIES. NEED LOCATIONS OF ADDITIONAL OR SECONDARY RESIDENCE. 8.7 ADDITIONAL RESIDENCE PREMISES RENTED TO OTHERS CHARGE PER FAMILY UNIT $10 $10 $12 $14 $18 $22 $1 COVERAGE FOR LIABILITY ARISING OUT OF ADDITIONAL ONE TO FOUR FAMILY DWELLINGS OWNED BY THE INSURED AND RENTED TO OF ADDITIONAL DWELLINGS AND NUMBER OF FAMILIES AT EACH PREMISES. ATTACH ENDORSEMENT ML-70 10/2009 Page 21

93 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONS LIABILITY COVERAGES LIMITS: INCLUDE $1,000 MED MAXIMUM ADD'L IS $5,000 EACH ADD'L RULE $50 $100 $300 $500 $1MIL $1,000 MED 8.8 PRIVATE STRUCTURES RENTED TO OTHERS THIS RULE DOES NOT APPLY 8.9 WATERBED LIABILITY FORM 4 ONLY $18 $20 $22 $24 $26 COVERAGE FOR PROPERTY DAMAGE ARISING OUT OF OWNERSHIP OR USE OF A WATERBED ON THE INSURED PREMISES CAN BE ADDED MEDICAL PAYMENTS DOES NOT APPLY. ATTACH ENDORSEMENT ML BUSINESS ACTIVITIES COVERAGE FOR LIABILITY ARISING OUT OF AN INSURED'S BUSINESS ACTIVITIES, OTHER THAN ACTIVITIES RELATED TO A BUSINESS OF WHICH THE INSURED IS SOLE OWNER OR PARTNER CAN BE ADDED. CLASSIFICATIONS AND RATES ARE BELOW. MAKE CHARGE FOR EACH COVERED PERSON CLERICAL $2 $2 $3 $4 $5 $1 ENGAGED WHOLLY IN OFFICE WORK AND HAVING NO OTHER DUTY IN OR ABOUT THE EMPLOYER'S PREMISES SALESPERSONS NO INSTALLATION $2 $2 $3 $4 $5 $1 SALESPERSONS, COLLECTORS, OR MESSENGERS. NO INSTALLATION, DEMONSTRATION, OR SERVICE OPERATIONS SALESPERSONS WITH INSTALLATION $4 $5 $5 $6 $7 $1 INCLUDES INSTALLATION, DEMONSTRATION, OR SERVICE OPERATIONS TEACHERS $9 $9 $11 $13 $15 $1 ATHLETIC, LABORATORY, MANUAL TRAINING, PHYSICAL TRAINING, OR SWIMMING INSTRUCTION, EXCLUDES COVERAGE FOR LIABILITY DUE TO CORPORAL PUNISHMENT OR PUPILS. 10/97 Page 22

94 Farmers Mutual Insurance Company West Virginia Homeowners Rates OPTIONS LIABILITY COVERAGES LIMITS: INCLUDE $1,000 MED MAXIMUM ADD'L IS $5,000 EACH ADD'L RULE $50 $100 $300 $500 $1MIL $1,000 MED TEACHERS - NOC $3 $4 $4 $5 $6 $1 EXCLUDES COVERAGE FOR LIABILITY ARISING OUT OF CORPORAL PUNISHMENT OF PUPILS CORPORAL PUNISHMENT $4 $4 $5 $6 $7 COVERAGE FOR LIABILITY ARISING OUT OF THE CORPORAL PUNISHMENT OF PUPILS -- MEDICAL PAYMENTS DOES NOT APPLY. THE ADDITIONAL PREMIUM OF THIS CLASSIFICATION MUST BE ADDED TO THE PREMIUM OF CLASSIFICATIONS OR MAKE ENTRIES TO SHOW THE NAMES OF THE COVERED PERSONS AND THE BUSINESS ACTIVITIES. IF APPLICABLE, MAKE AN ENTRY TO SHOW IF LIABILITY FOR CORPORAL PUNISHMENT OF PUPILS IS INCLUDED. ATTACH ENDORSEMENT ML OFFICE PROFESSIONAL, PRIVATE SCHOOL OR STUDIO OCCUPANCY EACH EXPOSURE $8 $10 $12 $13 $15 $2 COVERAGE FOR LIABILITY ARISING OUT OF AN INCIDENTAL OFFICE, PROFESSIONAL, PRIVATE SCHOOL OR STUDIO OCCUPANCY IN THE RESIDENCE, RELATED PRIVATE STRUCTURE OR AT AN ADDITIONAL RESIDENCE PREMISES OCCUPIED BY AN INSURED CAN BE ADDED WHEN: 1. PREMISES ARE OCCUPIED PRINCIPALLY FOR RESIDENTIAL PURPOSES. 2 BUSINESS IS CONDUCTED BY AN INSURED. 3. THERE ARE NO OTHER BUSINESS CONDUCTED ON THE PREMISES. ATTACH ENDORSEMENT ML-42 10/97 Page 23