ZIONS BANK PUBLIC FINANCE

|

|

|

- Derrick Mosley

- 5 years ago

- Views:

Transcription

1 Tremonton, Utah WATER Impact Fee Analysis Noticing DRAFT Prepared By January 21, 2014

2 Table of Contents List of Figures... 2 Executive Summary... 3 Growth and ERU Projections... 3 Level of Service Definitions... 3 Proportionate Share Analysis... 3 Existing Infrastructure and Capacity to Serve New Growth (Buy-Inn Component)... 4 Future Capital Improvements... 4 Outstanding and Future Debt... 4 Calculated Fee... 4 Chapter 1: Impact Fee Overview... 4 Project Overview... 5 Why Is the City Updating the Previous Impact Fee Analysis?... 5 What is an Impact Fee?... 5 How Willl New Growth Affect the City? Why Are Impact Fees Necessary?... 7 Where Will the Impact Fees Be Assessed?... 7 What Costs are Included in the Impact Fee?... 8 What Costs Are Not Included in the Impact Fee?... 8 How Are Impact Fees Calculated?... 8 What is the Current Level of Service?... 9 How are Schools Considered in this Analysis? What is the Maximum Legal Culinary Water Impact Fee Amounts?... 9 Chapter 2: Future Capital Projects and Level of Service Impact Fee Analysis Requirements Growth and ERU Projections Level of Service Definitions Existing Infrastructure and Capacity to Serve New Growth (Buy-Inn Component) Impact Fee Facilities Plan Future Capital Projects Chapter 3: Proportionate Share Analysis Calculated Fee Chapter 4: Certification and Appendices Appendices

3 LIST OF FIGURES Figure ES1: ERUs... 3 Figure ES2: Maximum Legal Fee per ERU... 4 Figure 1: Projected Growth in Population and Culinary Water ERUs... 6 Figure 2: Service Area Map... 8 Figure 3: Maximum Legal Culinary Water Impact Fee Amount... 9 Figure 4: ERUs Figure 5: Capital Projects Figure 6: Fee per ERU

4 EXECUTIVE SUMMARY Zions Bank Public Finance (Zions) is pleased to provide Tremonton (thee City) with an updated Impact Fee Analysis (IFA) fo the City s Culinary Water System. The following executive summary pages summarize the IFA,tables included. The intent is to provide a concise summary of the calculation and identification of the maximumm legal impact fee that the City can enact. Growth and ERU Projections As of 2013 the City has a total of 2,885 equivalent residential units (ERUs) 1 within the Culinary Water System. The following table identifies the current and future ERUs in a single City-Wide Service Area. The analysis considers growth over the next six to ten years. Between now and 2020, ERUs will increase by 380 to reach 3,265. The full growth table can be found in Appendix 1 of this document. Figure ES1: ERUs Current ERCs 1 Culinary Water Current 2,885 Buildout 10,491 Level of Service Definitions Jones & Associates Consulting Engineers defined the City s level of service in the Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan. This plan states the following: Culinary Water: 1,512 gallons per Equivalent Residential Unit per day. 2 However, it must be considered that although this is the average day ERU, the system must be sized adequately to meet peak, not average, demand. PROPORTIONATE SHARE ANALYSIS The Impact Fees Act, Title 11-36a of Utah Code requires that the Impact Fee Analysiss estimate the proportionate share of the costs for existing capacity that will be recouped and the costs of impacts on system improvements that are reasonably related to the new development activity. Part of the proportionate share analysiss is a consideration of the manner of funding existing public facilities. A City typically funds existing infrastructure through several different fundingg sources including: General Fund Revenues User Fees Grants Bond Proceeds Developer Exactions Impact Fees 2 Page 7 Jones & Associates Consulting Engineers Capital Facilities Plan and Impact Fee Facilities Plan 3

5 Historically the City has funded its existing Culinary Water System through User Fees (rate revenues), impact fees and developer exactions and donations. All of these funding sources (with exception of developer contributions/donations) are impact fee qualifying expenses to be considered for buy in purposes. In consideration of future capital improvements, the City will continue using similar funding sources; no grants are being considered or are available at this time. Using impact fees places a burden on future users that is equal to the burden that was borne in the past by existing users. 3 Existing Infrastructure and Capacity to Serve New Growth (Buy-In Component) The City provided Zions with a list of all City owned assets for the Culinary Water System. The documented historic cost of the facilities is $4,227, Only the original costs of the improvements have been considered. See Appendix 3 for the detailed list of assets for the collection system. An analysis has been completed too identify the capacity to serve new growth and the amount of funds which can be charged as a buy-in for future users. This will be discussed in greater detail later in this document and can be found in Appendix 4 of this document. Future Capital Improvements In the Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan (IFFP) prepared by Jones & Associates Consulting Engineers a list of likely capital projects to be constructed in the next six to ten years was provided. Table of the IFFP identify the most likely capital improvement projects to be constructt the amount of the project that will benefit growth through the next six to ten years. The 2013 fiscal year total of capitall improvements in the Table of the IFFP is $6,725,875. Zions Bank Public Finance has added a 2.43% 5 inflation factor and a future value has been calculated equaling $7,236,611. Eighty five percent of the future value will bee included into the impact fee, or $6,181,446. Outstanding and Future Debt There is no outstanding Culinary Water related debt in Tremonton. It is currently not anticipated thatt the City will bond for water in the next six to ten years. CALCULATED FEE F The impact fees have been calculated with all the above considerations for the City-Wide Service Area, which also includes area that is included in the Tremonton City Annexation Declaration. The fee is calculated per ERU. For multifamily and non-residential land uses, fee payers will be assessed per ERU of water generation. Figure ES2: Maximum Legal Fee per ERU 6 Cost % Impact Fee Qualifying Impact Fee Qualifying Cost ERUs to be Served Cost per ERU IFFP Projects Buy In - Existing Assets Professional Expesnes Subtotal Total Impact Fee Per ERU Impact Fee 4,476,513 4,227,132 32,696 8,736,344 83% 100% 100% 91% 3,722,641 4,227,132 32,696 7,982,469 4,264 10,491 4,264 $ ,284 1,284 3 Utah Impact Fees Act, 11-36a-304(2) (c) (d) 4 Tremonton Depreciation Schedule 5 Based on 10 years average cost of inflation using the Bureau of Labor Statistics. 4

6 CHAPTER 1: IMPACT FEE OVERVIEW PROJECT OVERVIEW Zions Bank Public Finance (Zions) is pleased to provide Tremonton (thee City) with an updated Impact Fee Analysis (IFA) fo the City s Culinary Water System. Tremonton realizes that due to the age of its current analysis, as well as changes to the Impact Fees Act, required updates and review of its impact fees ass well as its facility planning were needed. The City is still growing and has many capital needs. The update to the Impact Fee Analysis (IFA) is an intensive collaborative effort that meets the needs of City Stakeholders and the City. The information used to create this IFA was provided by City staff, Zions Bank Public Finance and Jones & Associates Consulting Engineers. The goal of the Impact Feee e Analysis is to calculate the maximum impact fee that may be assessed to new development and ensuree the fee meets the requirements of the Impact Fees Act, Utah Code 11-36a-101 et seq. The sections and subsectionss of the Impact Fee Analysis will directly address the following items, required by the Utah Code: Impact Fee Analysis Requirements (Utah Code 11-36a-304) o Identify Existing Capacity to serve growth Proportionate Share Analysis o Identify the level of service o Identify the impact of future development on exisitng and future improvements Calculated Fee (Utah Code 11-36a-305) Certification (Utah Code 11-36a-306) WHY IS THE CITY UPDATING THE PREVIOUS IMPACT FEE ANALYSIS? The City has commissioned this culinary water Impact Fee Analysis amendment to accomplish the following: Determine the maximum impact fee that may be assessed to new development; Update capital need projections and account for historic costs of facilities; Put the analysis in compliance with the changes to the Impact Fees Act effective May 2011; Include an Impact Fee Facilities Plan (IFFP) with a ten year capital planning horizon; and More clearly define the current level of service and the future level of service that the City will provide. WHAT IS AN IMPACT FEE? An impact fee is an one-time exaction ( Utah Code 10-9a-508 (1)) in the form of a fee charged to new development to recover the City s cost of constructing Culinary Water System with capacity to serve new growth. The fee is typically assessed at the time of building permit issuance and/or as a condition of development approval. The calculation of the impact fee must strictly follow the Impact Fees Act, Title 11-36a of Utah Code to ensure that the fee is equitable and fair. This Impact Fee Analysis shows that there is a fair comparison between the maximum legal impact fee charged to new development and the impact the new development will have upon the system s capacity. Impact fees are charged to development according to the water meter size, which is a realistic measure of the potential water demands that each user will add to the system.? HOW WILL NEW GROWTH AFFECT THE CITY? According to the Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan, the City s ERUs total 2,885 and this plan estimates that by 2020 the City will have approximatelyy 3,265 ERUs. The City will add approximately 380 new ERUs. When Tremonton City (the Service Area) is built out in the year 2070, it is anticipated that there will be 10,491 ERUs. Theree is a large amount of vacant land left within the City s current boundariess as well as in unincorporated areas around the City that is a part of the City s Annexation Declaration. 5

7 This new growth will generally increase water demands as the density of developmentt increases, and extending collection system and other facilities as development stretches farther away. Inn the case of the City the capacity needed for new growth is found in both existing facilities that the City has built ahead of the growth and in the future capital projects that will be constructed in the next six to ten years. The recommended impact fee willl balance the cost of capacity that is already in the system and new projects that are needed to serve the additional anticipated growth. Population is important in the Capital Facilities and Impact Fee Facilities planning ass population, and other factors, drive project need and timing. However, this impact fee analysis is nott population dependent. The driving force is the Equivalent Residential Unit (ERU), which also considers the impact of Non-residential development. The impact fee is based on capacity available in the existing system and on future projects required too service growth and are not directly dependent upon population growth. In summary, the existing infrastructure expense will be considered and future capital project costs will be spread across capacity provided and not population growth over the next six to ten years. Figure 1: Projected Growth in Population and Culinary Water ERUs ERU Projections ,, , ,, , ,, , ,, , ,, , ,, , ,, , ,, , ,, , ,, , ,, ,, ,, ,, ,, ,, ,, ,, ,,133 6

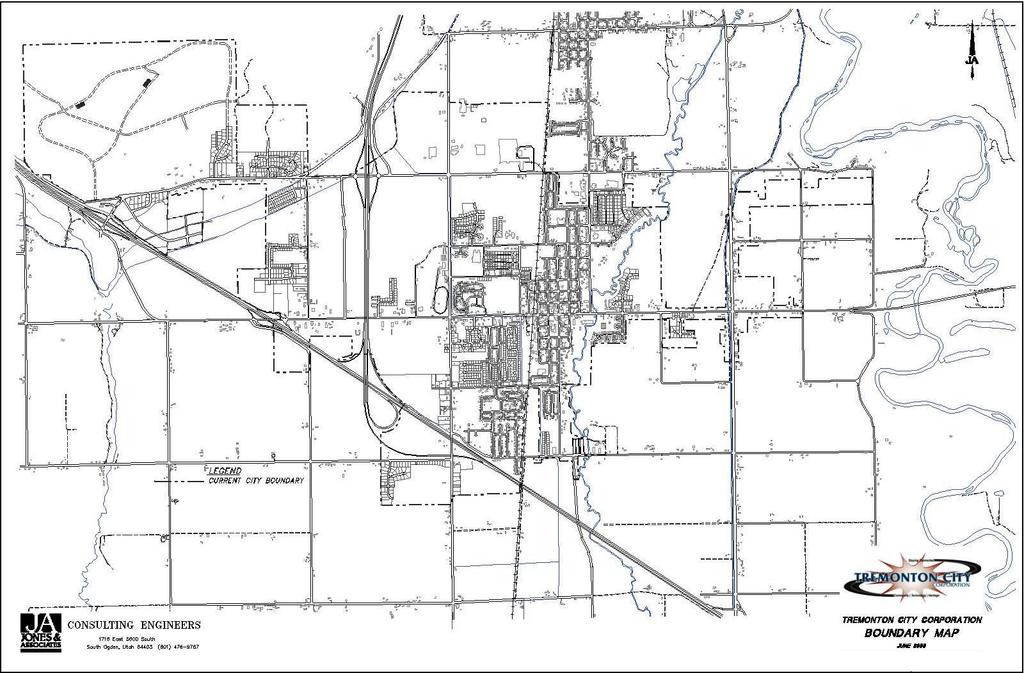

8 WHY ARE IMPACT FEES NECESSARY? Impact fees are necessary to allocate the costs of unused the City s Culinary Water System capacity that is reserved for future developments that will benefit from the unused capacity. Impact fees help to shield existing userss from shouldering the burden of paying not only for the capacity that they usee but also from funding the cost of capacity needed for future development to occur. WHERE WILL THE IMPACT FEES BE ASSESSED? The impact fees will be assessed within the City s Water Service Area, which includess the current City incorporated limits and City s future annexation areas to which the City will provide culinary water service. Figure 2 below is a detailed map of the current Service Area. This map is also included in the attachedd appendix. In short, if a developer is requesting a building permit and will be served by the City s Culinary Water System then that property is included in the Servicee Area. The proposed impact fees will be assessed throughout the entire Impact Fee Service Area. 7

9 Figure 2: Service Area Map WHAT COSTS ARE INCLUDED IN THE IMPACT FEE? Impact fee revenues may not be spent on capital projects or associated costs, such as financing interest expense that constitute repair and replacement, cure any existing deficiencies, or r maintain the existing level of service for current users. Impact fees cannot fund operational expenses. The impact fees proposed in this analysiss are calculated based upon: Costs of replacement facilities thatt are needed too perpetuate unused capacity in the system that growth will require; New capital infrastructure that provides new capacity for growth; Historic costs of existing improvements that providee capacity that will serve new development; and Cost of professional services for engineering, planning services and preparation of the Impact Fee Facilities Plan and Impact Fee Analysis. WHAT COSTS ARE A NOT INCLUDED IN THE IMPACT FEE? The costs, both direct capital and financing, that cannot be included inn the impact fee are as follows: Projects that cure deficiencies for existing users; Projects that increase the level of service above thatt which is currently provided; Operations and maintenance costs; Costs of facilities funded by grants or other funds that the City does not have to repay; and Costs of reconstructionn of facilities that do not havee capacity to serve new growth. HOW ARE IMPACT FEES CALCULATED? To calculate a fair impact fee the Impact Fee Analysis determined a growth related cost of existing and future facilities and divide that by the number of new units that will benefit from the unused capacity. A cost per equivalent residential unit is calculated by dividing impact feee qualifying cost by the amount of capacity. This cost per equivalent residential unit of capacity is then multiplied by the amount of demand that a typical single-family detachedd residential home or ERU would utilize. The general impact fee methodology splits the capacity in existing facilities and future capital projects between that which already benefits existing users and capacity that which is available to benefit new growth. A cost is assigned to 8

10 the capacity that is available for new growth based upon the historic cost of Culinary Water System and the future eligible costs of the Culinary Water System.. A final fee for residential or non-residential land use is calculated by multiplying the cost by the water meter size. WHAT IS THE CURRENT C LEVEL OF SERVICE?? Jones & Associates Consulting Engineers defined the City s level of service in the Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan. This plan states the following: The requirements for the water system are as follows: Peak water production during the months of July and August is used to define an ERU since all planning for the distribution system, storage, and production must be able to meet the peak demand. The peak water production during July and August was averaged over the last 4 years and the amount used by large, commercial water users was subtracted from that amount. The remaining amount was assumedd to be the amount used by average single ERU connection.. Therefore, the City has defined the current level of servicee as: Water: 1,512 gallons per Equivalent Residential Unitt per day. 7 The impact fee will be based on an average day ERU, but projects will be designed at the state defined peaking standards, discussed more in the CFP/IFFP. HOW ARE SCHOOLS CONSIDERED IN THIS ANALYSIS? The Impact Fees Act, Title 11-36a of the Utah Code allows the Cityy the ability to charge an impact fee for a school facilities impact on the City s Culinary Water Systems. The Culinary Water Impact fee analysis quantifies the cost per ERU. The school could be assessed an impact fee based on the numberr of ERUs generated. WHAT IS THE MAXIMUM M LEGAL CULINARY WATER W IMPACT FEE AMOUNTS?? Figure 3: Maximum Legal Culinary Water Impact Fee Amount Cost % Impact Fee Qualifying Impact Fee Qualifying Cost ERUs to be Served Cost per ERU IFFP Projects Buy In - Existing Assets Professional Expesnes Subtotal Total Impact Fee Per ERU Impact Fee 4,476,513 4,227,132 32,696 8,736,344 83% 100% 100% 91% 3,722,641 4,227,132 32,696 7,982,469 4,264 10,491 4,264 $ ,284 1,284 The Tremonton City Council has the discretion to set the actual impact fees to be assessed, but they may not exceed the maximum allowable fee calculated of $1,562 per ERU. The City may, on a case by case basis, work directly with a developer to adjust the standard impact fee to respond to unusual circumstancess and ensure that impact fees are imposed fairly. This adjusted impact feee calculation will be based on the cost per r equivalent residential unit defined above, multiplied by the number of units created by the applicable development type. 7 Page 2 Jones & Associates Consulting Engineers Capital Facilities Plan and Impact Fee Facilities Plan 9

11 CHAPTER 2: FUTURE CAPITAL PROJECTS AND LEVEL OF SERVICE IMPACT FEE ANALYSIS REQUIREMENTS Growth and ERU Projections According to the Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan and the growth projections completed by Zions, the 2010 population was 7, Population is important in the Capital Facilities and Impact Fee Facilities planning as population, and other factors, drive project need and timing. However, this impact fee analysis is not population dependent. The driving force is the Equivalent Residential Unit (ERU),, which also considers the impact of Non-residential development. The Impact Fee Facilities Plan defines an ERU as 1,512 gallons per day usage 9. Currently the City has 2,885 equivalent units. In the next six years it is anticipated that the City will grow to 3,265 ERUs (an increase of 380 ERUs). The ERUs increases are displayed below. Figure 4: ERUs ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,, ,,133 ERU Projections , , , , , , , , , ,226 There will be significant growth expected within the City s boundaries and increased demand on the City s Culinary Water System which will require new Culinary Water projects to meet further demand. Level of Service Definitions The Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan has defined the current level of service in Tremonton as: Water: 1,512 gallons per day per ERU Census Data 9 Jones & Associates Consulting Engineers Tremonton Impact Fee Facilities Plan 10

12 Existing Infrastructure and Capacity to Serve New Growth (Buy-In Component) Appendix 3 provides an expense report for the assets owned and operated by Tremonton. Included with the assets are the original dates of construction or acquisition and the original cost of the collection component of the Culinary Water System. An analysis has been completed to identify the capacity to serve new growth. The existing facilities historic costs are spread across all users through buildout in order to calculate an average cost per ERU for existing infrastructure. Impact Fee Facilities Plan Future Capital Projects The Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan developed the following capital projects, and helped (along with City staff) determine the timing and identified what was growth related, and of that amount, how much of the total capacity will be realized in the next ten years (percentage Impact Fee Qualifying & Non-Impact Fee Qualifying Cost). Figure 5: Capital Projects Project Name Replacee existing 12 & 10 waterlines with new 18 & 24 lines on 1000 North from 2300 West to the I-15 northbound offramp. Replacee main trunk inlet/outlet lines from the lower reservoirs on west hillside bench. Replacee existing 12 line with a new 20 line from the City s springss in the Bear River bottoms to SR-13 along 1000 North Year to be Constructed Cost (PV) , , ,773,200 Cost (FV) 579, ,050 1,816,342 % Impact Fee Qualifying Impact Fee Qualifying Cost ERU's Served 95% 550,947 1,350 70% 684,635 1, % 1,083, Construct 1.5 million gallon reservoir, pump line, and pump station on the west hillside. The reservoir will serve the pressure zone(s) directly above the current highest pressure zone served. Develop new water sources at locations that willl be determined at the time of construction. It is anticipated that this will involve the drilling of new wells Construct line from 750,0000 gallon reservoir trunk line to the upper end of Country View Estates ,761,500 1,540, ,200 Culinary Total $ 6,725,875 $ 1,939,288 1,737, ,211 7,236, % 1,939,288 1, % 1,737, % 186, % $ 6,181,446 5,334 11

13 CHAPTER 3: PROPORTIONATE SHARE ANALYSIS A The Impact Fees Act requires that the impact fee analysis estimatee the proportionate share of the costs for existing capacity that will be recouped; and the costs of impacts on system improvements ( as defined by the Utah Impact Fees Act)that are reasonably related to the future development activity. Tremonton continues to grow and there is still expansionn in the area. The Culinary Water System Capital Facilities Plan & Impact Fee Facilities Plan clearly defines what projects are growth related, repair and replacement, or pipe upsizing (the upsizing may include some element of growth). Part of the proportionate share analysis is a consideration of the manner of funding existing public facilities. Historically the City has funded existing infrastructure through several different funding sources such as: General Fund Revenues User Rates Grants Bond Proceeds Developer Exactions Impact Fees In calculating the buy-in component (for existing Culinary Water System capacity) of this analysis no grant funded infrastructure has been included. Once the grant funded projects have been removed, all remaining infrastructure has been funded by existing residents. In order to ensure fairness to existing users, impact fees are an appropriate means of funding future capital infrastructure. Using impact fees places a burden on future users that is equal to the burden that was borne in the past by existing users (Utah Impact Fees Act, 11-36a-304(2)(c)(d))different means; it is required by the Impact Fees Act to evaluate all means of funding future improvements to the Culinary Water System. There are positives and negative aspectss to the Just as existing infrastructure has been funded through various forms of funding. It is important to evaluate each. General Fund/User Rates The general fund and user rates have both been funded in one form or another by existing users. It would be an additional burden to existing users to use this revenue source to fund future improvements to meet the needs of future users. This is not an equitable policy and can place tooo much stress on the tight budgets of the general fund and other user rate funds. The water rates in Tremonton are dedicated to fund operation and maintenance, repair and replacement and ensuring a stable reserve for maintaining a good credit rating. If rate revenues are required to supplement the capital required by growth, the City will reimburse the user rate fund with impact fees as they are collected and act as a loan to the impact fee fund to be repaid. Property Taxes It is true that property taxes may be a stable source of income. However, property taxes are not based on impact placed upon a system. Property taxes are based upon property valuation. Usingg property taxess to fund future capital again places too much burden on existing users and subsidizes growth. The financial audits for the City do not show a line item for property taxes as a revenue stream for a Water Fund Utility, thus any property taxes collected on the property being developed is not being used to fund infrastructure or operation and maintenance of the Culinary Water System. Bond Proceeds Based on lack of impact fee reserves and cash funding available for r the sewer projects needed for the future, the City anticipates issuing debt for capital projects. It is important to note that it is anticipated the impact fees will fund the eligible portions of the proposed debt. 12

14 Impact Fees Impact fees are a fair and equitable means of providing expansion of the Culinary Water System for future development. Impact fees provide a rational nexus between the costs borne in the past and the costs required in the future. The Impact Fees Act ensures that future development is not paying any more than what future growth will demand. Existing users and future users receive equal treatment; therefore, impact fees are the optimal funding mechanism for future growth related improvements of the Culinary Water System. Developer Credits If a project included in the Impact Fee Facilities Plan (or a project that will offset thee demand for a system improvement as defined by the Utah Impact Fees Act, which is listed in the IFFP) is constructed by a developer that developer is entitled to a credit against impact fees owed. (Utah Impact Fees Act, 11-36a-304(2)( (f)) Time-Price Differential Utah Code 11-36a-301(2) )(h) allows for the inclusion of a time-price differential in order to create fairness for amounts paid at different times. To address the time-price differential, thiss analysis includes an inflationary component to account for construction inflation for future projects. Projects constructed after thee year 2013 will be calculated at a future value with a 2.43% inflation rate. All users who pay an impact fee today or within the next six to ten years will benefit from projects to be constructed and included in the fee. Other In this particular analysis, there is also a credit for unspent impact feee revenues collected in the past. The current impact fee fund balance for the Culinary Water System was credited against the fee. CALCULATED FEE F The impact fees have been calculated with all the above considerations for the City-wide Servicee Area, including the City s areas in the Annexation Declaration. The fee is calculated perr a single ERU.. The fees per ERU can be found in Figure 6. These tables can also be found in Appendix 4. Figure 6: Fee per ERU Cost % Impact Fee Qualifying Impact Fee Qualifying Cost ERUs to be Served Cost per ERU IFFP Projects Buy In - Existing Assets Professional Expesnes Subtotal Total Impact Fee Per ERU Impact Fee 4,476,513 4,227,132 32,696 8,736,344 83% 100% 100% 91% 3,722,641 4,227,132 32,696 7,982,469 4,264 10,491 4,264 $ ,284 1,284 The City will assess the impact fee on a per ERU basis for all residential, multifamily and nonresidential land uses. 13

15 CHAPTER 4: CERTIFICATION AND APPENDICES In accordance with Utah Code Annotated, 11-36a-306( 2), Tenille Tingey on behalf off Zions Bank Public Finance, makes the following certification: I certify that the attached impact fee analysis: 1. includes only the cost of public facilities that are: a. allowed under the Impact Fees Act; and b. actually incurred; or c. projected to be incurred or encumbered within six years after the day on which each impact fee is paid; 2. does not include: a. costs of operation and maintenance of public facilities; b. cost of qualifying public facilities that will raise the level of service for the facilities, through impact fees, above the level of service that is supported by existing residents; c. an expense for overhead, unlesss the expense iss calculated pursuant to a methodology that is consistent with generally accepted costt accounting practices and the methodological standards set forth by the federal Office of Management and Budget for federal grant reimbursement; 3. offset costs with grants or other alternate sources of payment; and 4. complies in each and every relevant respect withh the Impact Fees Act. Tenille Tingey makes this certification with the following caveats: 1. All of the recommendations for implementations of the Impactt Fee Facilities Plans ( IFFPs ) made in the IFFP documents or in the Impact Fee Analysis (IFA) documents are followed in their entirety by Tremonton staff and elected officials. 2. If all or a portion of the IFFPs or IFA are modifiedd or amended, this certification is no longer valid. 3. All information provided to Zions Bank Public Finance, its contractors or suppliers is assumed to be correct, complete and accurate. This includes information provided by Tremonton and outside sources. Copies of letters requesting data are included as appendices to the IFFPs and the IFA. Dated: January 21, 2014 ZIONS BANK PUBLIC FINANCE By Tenille Tingey 14

16 TREMONTON CITY:

17 PUBLIC NOTICE Public Body: Tremonton City Council Subject: Impact Fee Enactment Notice Title: Notice to Adopt Impact Feee Enactment, ncluding but not limited to thee Impact Fee Ordinance and Impact Fee Analysis Notice Type: Notice to Adopt Impact Fee Enactment Notice Date: January 17, 2014 Description/Agenda: Tremonton City Corporation, Utah in accordance with the requirementss of Utah Code Annotated 11-36a-504, gives public notice to adopt an Impact Fee Enactment including but not limited to Impact Fee Ordinance and Impact Fee Analysis for culinary water impact fee, sanitary sewer collection impact fee, storm drain impact fee, parks, recreation, trails and open space impact fee, and public safety impact fee for fire/ems and law enforcement. The location(s) that will be included in the Impact Fee Enactment is the entire area of the incorporated limits of Tremonton City and any area outside of the Tremonton City, which may hereafter be annexed into Tremonton City orr serviced by any Tremonton City Public Facility. A public hearing shall be held by the City Council on February 4, 2014 at 7:00 pm or soon thereafter in the Tremonton City Council Chambers located at 102 S. Tremont Street, Tremonton, Utah to receivee public comment on the adoption of the aforementioned Impact Fee Enactment. Draft copies of: (1) the Impact Fee Enactment Ordinance; (2) summaries of the Impact Fee Analysis for the aforementioned impact fees; and (3) complete drafts of the Impact Fee Analysis for the aforementioned impact fees will be available on or before Januaryy 24, 2014 att or at the Tremonton City Library located at 210 N. Tremont Street, Tremonton, Utah or the Satellite Library Branch located in the Bear River Valley Senior Center located at 510 West 1000 North, Tremonton, Utah during regular business hours. Additionally, on or before January 24, 2014 copies of the aforementioned documents are available to the public at the Tremonton City Recorder s Office located at 102 S. Tremont Street, Tremonton Utah during regular business hours. The public may file written objection associated with the adoption of an Impact Fee Enactment for the Tremonton City Council s consideration. Written objections, questions pertaining to this notice, or contents of the Impact Fee Enactment may be directed to Shawn Warnke, Tremonton City Manager (435) , swarnke@tremontoncity.com, or mailed to Shawn Warnke, 102 S. Tremont St. Tremonton, UT Notice of Special Accommodations: If you need special accommodations to participate in a City Council Meeting, please call the City Recorder, Darlene S. Hess, at Please provide att least 24 hours notice for adequate arrangements to be made. Notice of Electronic or telephone participation: Tremonton City passedd Ordinance No approving Electron Meeting Procedures in accordance with Section of Utah Code Annotated. 16

18 (This Page Intentionally Left Blank) 17

19 1/21/2014 Appendix 1: CURRENT AND FUTURE ERUs A B C D E F G H 1 Culinary Water ERU Projections 1 2 Current Buildout , , Current ERCs 1 2,881 10, , , , , Jones & Associates 2013 CFP & IFFP , , , , ERUs Added Per Year , , , , , , , , , , , , , , , , Total , , , A B C D E F G H

20 1/21/ Appendix 2: CAPITAL PROJECTS - IMPACT FEE FACILITIES PLAN Inflation Rate* 2% A B C D E F G Year to be Constructed Current Cost (PV) 2013 Construction Cost (FV) % Impact Fee Qualifying Impact Fee Qualifying Cost Project Name ERU's Served Replace existing 12 & 10 waterlines with new 18 & 24 lines on 1000 North from 2300 West to 2 the I-15 northbound offramp , ,913 95% 574,638 1, Replace and upsize main trunk inlet/outlet lines from the lower reservoirs on west hillside bench , ,050 70% 684,635 1, Water System Phase 1 - Replace existing 12 line with a new 20 line from the City s springs in the Bear River bottoms to SR-13 along 1000 North , ,094 57% 553, Develop new water sources at locations that will be determined at the time of construction. It is anticipated that this will involve the drilling of new wells ,540,500 1,737, % 1,737, Construct line from 750,000 gallon reservoir trunk line to the upper end of Country View Estates , ,211 93% 172, Culinary Total $ 4,163,713 $ 4,476,513 83% $ 3,722,641 4, *Based on 10 years average cost of inflation using the Buruea of Labor Statistics 8 A B C D E F G 1

21 1/21/2014 Appendix 3: ASSETS A B C 1 1 Date Acquired Description Historic Cost South Spring - 1 MG East Reservoir - 14" AC Pipeline 4-miles North Pump House West - Main St. to Rocket Rd West West North - 12-inch Main East to Pump House 47, North & I-15 Waterline Relocate & Improvements West North to 1000 North North 100 West to 300 East Iowa String (Main Street to 1000 North) 57, Northwest Annexation Water Project - (1000 North I-84 to 2300 West) 125, Iowa String South - Main St. Water Project 150, South Tremont St. Water Project 114, Water Project - Sandalwood & North Tremont St. 200, ,000 Gallons Water Tank & Pump Station - West Hill 687, Radio Read Meter Change-Out 229, West Side Secondary System 180, Bear River Water Line Crossing 121, West Water 317, Cedar Ridge New Well & Pipeline Project 893, Million Gallon Tank Project 1,101, Impact Fee Qualifying $ 4,227, A B C 22

22 1/21/2014 Appendix 4: BASE FEE PER ERU Tremonton Impact Fee A B C D E F 1 Cost % Impact Fee Qualifying Impact Fee Qualifying Cost ERUs to be Served Cost per ERU 1 2 Impact Fee 2 3 IFFP Projects 4,476,513 83% 3,722,641 4, Buy In - Existing Assets 4,227, % 4,227,132 10, Professional Expesnes 32, % 32,696 4, Subtotal 8,736,344 91% 7,982,469 1, Total Impact Fee Per ERU $ 1,284 6 A B C D E F

23 1/21/2014 Appendix 5: INFLATION RATE A B C D E F G H I J K L M N 1 30 Year Historical Inflation Rate Data 1 2 Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Annual % 2.87% 2.65% 2.30% 1.70% 1.66% 1.41% 1.69% 1.99% 2.16% % 2.11% 2.68% 3.16% 3.57% 3.56% 3.63% 3.77% 3.87% 3.53% 3.39% 2.96% 3.16% % 2.14% 2.31% 2.24% 2.02% 1.05% 1.24% 1.15% 1.14% 1.17% 1.14% 1.50% 1.64% % 0.24% -0.38% -0.74% -1.28% -1.43% -2.10% -1.48% -1.29% -0.18% 1.84% 2.72% -0.34% % 4.03% 3.98% 3.94% 4.18% 5.02% 5.60% 5.37% 4.94% 3.66% 1.07% 0.09% 3.85% % 2.42% 2.78% 2.57% 2.69% 2.69% 2.36% 1.97% 2.76% 3.54% 4.31% 4.08% 2.85% % 3.60% 3.36% 3.55% 4.17% 4.32% 4.15% 3.82% 2.06% 1.31% 1.97% 2.54% 3.24% % 3.01% 3.15% 3.51% 2.80% 2.53% 3.17% 3.64% 4.69% 4.35% 3.46% 3.42% 3.39% % 1.69% 1.74% 2.29% 3.05% 3.27% 2.99% 2.65% 2.54% 3.19% 3.52% 3.26% 2.68% % 2.98% 3.02% 2.22% 2.06% 2.11% 2.11% 2.16% 2.32% 2.04% 1.77% 1.88% 2.27% % 1.14% 1.48% 1.64% 1.18% 1.07% 1.46% 1.80% 1.51% 2.03% 2.20% 2.38% 1.59% % 3.53% 2.92% 3.27% 3.62% 3.25% 2.72% 2.72% 2.65% 2.13% 1.90% 1.55% 2.83% % 3.22% 3.76% 3.07% 3.19% 3.73% 3.66% 3.41% 3.45% 3.45% 3.45% 3.39% 3.38% % 1.61% 1.73% 2.28% 2.09% 1.96% 2.14% 2.26% 2.63% 2.56% 2.62% 2.68% 2.19% % 1.44% 1.37% 1.44% 1.69% 1.68% 1.68% 1.62% 1.49% 1.49% 1.55% 1.61% 1.55% % 3.03% 2.76% 2.50% 2.23% 2.30% 2.23% 2.23% 2.15% 2.08% 1.83% 1.70% 2.34% % 2.65% 2.84% 2.90% 2.89% 2.75% 2.95% 2.88% 3.00% 2.99% 3.26% 3.32% 2.93% % 2.86% 2.85% 3.05% 3.19% 3.04% 2.76% 2.62% 2.54% 2.81% 2.61% 2.54% 2.81% % 2.52% 2.51% 2.36% 2.29% 2.49% 2.77% 2.90% 2.96% 2.61% 2.67% 2.67% 2.61% % 3.25% 3.09% 3.23% 3.22% 3.00% 2.78% 2.77% 2.69% 2.75% 2.68% 2.75% 2.96% % 2.82% 3.19% 3.18% 3.02% 3.09% 3.16% 3.15% 2.99% 3.20% 3.05% 2.90% 3.03% % 5.31% 4.90% 4.89% 4.95% 4.70% 4.45% 3.80% 3.39% 2.92% 2.99% 3.06% 4.25% % 5.26% 5.23% 4.71% 4.36% 4.67% 4.82% 5.62% 6.16% 6.29% 6.27% 6.11% 5.39% % 4.83% 4.98% 5.12% 5.36% 5.17% 4.98% 4.71% 4.34% 4.49% 4.66% 4.65% 4.83% % 3.94% 3.93% 3.90% 3.89% 3.96% 4.13% 4.02% 4.17% 4.25% 4.25% 4.42% 4.08% % 2.10% 3.03% 3.78% 3.86% 3.65% 3.93% 4.28% 4.36% 4.53% 4.53% 4.43% 3.66% % 3.11% 2.26% 1.59% 1.49% 1.77% 1.58% 1.57% 1.75% 1.47% 1.28% 1.10% 1.91% % 3.52% 3.70% 3.69% 3.77% 3.76% 3.55% 3.35% 3.14% 3.23% 3.51% 3.80% 3.55% % 4.60% 4.80% 4.56% 4.23% 4.22% 4.20% 4.29% 4.27% 4.26% 4.05% 3.95% 4.30% % 3.49% 3.60% 3.90% 3.55% 2.58% 2.46% 2.56% 2.86% 2.85% 3.27% 3.79% 3.22% % 7.62% 6.78% 6.51% 6.68% 7.06% 6.44% 5.85% 5.04% 5.14% 4.59% 3.83% 6.16% % 11.41% 10.49% 10.00% 9.78% 9.55% 10.76% 10.80% 10.95% 10.14% 9.59% 8.92% 10.35% % 14.18% 14.76% 14.73% 14.41% 14.38% 13.13% 12.87% 12.60% 12.77% 12.65% 12.52% 13.58% % 9.86% 10.09% 10.49% 10.85% 10.89% 11.26% 11.82% 12.18% 12.07% 12.61% 13.29% 11.22% % 6.43% 6.55% 6.50% 6.97% 7.41% 7.70% 7.84% 8.31% 8.93% 8.89% 9.02% 7.62% % 5.91% 6.44% 6.95% 6.73% 6.87% 6.83% 6.62% 6.60% 6.39% 6.72% 6.70% 6.50% % 6.29% 6.07% 6.05% 6.20% 5.97% 5.35% 5.71% 5.49% 5.46% 4.88% 4.86% 5.75% % 11.23% 10.25% 10.21% 9.47% 9.39% 9.72% 8.60% 7.91% 7.44% 7.38% 6.94% 9.20% % 10.02% 10.39% 10.09% 10.71% 10.86% 11.51% 10.86% 11.95% 12.06% 12.20% 12.34% 11.03% % 3.87% 4.59% 5.06% 5.53% 6.00% 5.73% 7.38% 7.36% 7.80% 8.25% 8.71% 6.16% % 3.51% 3.50% 3.49% 3.23% 2.71% 2.95% 2.94% 3.19% 3.42% 3.67% 3.41% 3.27% *Source: Bureau of Labor Statistics 30 Year Average 4.42% Year Average 2.43% 45 A B C D E F G H I J K L M N

24

SPRINGVILLE CITY CULINARY WATER IMPACT FEE ANALYSIS (IFA) MAY 2014

MAY 2014") SPRINGVILLE CITY CULINARY WATER IMPACT FEE ANALYSIS (IFA) MAY 2014 Adopted May 20, 2014 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 SECTION 1: EXECUTIVE SUMMARY... 4 PROPOSED CULINARY WATER IMPACT

SPRINGVILLE CITY CULINARY WATER IMPACT FEE ANALYSIS (IFA) MAY 2014 Adopted May 20, 2014 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 SECTION 1: EXECUTIVE SUMMARY... 4 PROPOSED CULINARY WATER IMPACT

Millcreek City. DRAFT Parks, Recreation, Trails and Open Space Impact Fee Analysis

Millcreek City DRAFT Parks, Recreation, Trails and Open Space Impact Fee Analysis May 2, 2018 Table of Contents Table of Contents... 2 Summary of Impact Fee Analysis (IFA)... 3 Impact on Consumption of

Millcreek City DRAFT Parks, Recreation, Trails and Open Space Impact Fee Analysis May 2, 2018 Table of Contents Table of Contents... 2 Summary of Impact Fee Analysis (IFA)... 3 Impact on Consumption of

SPRINGVILLE CITY PRESSURIZED IRRIGATION IMPACT FEE ANALYSIS (IFA) MAY 2014

MAY 2014") SPRINGVILLE CITY PRESSURIZED IRRIGATION IMPACT FEE ANALYSIS (IFA) MAY 2014 Adopted May 20, 2014 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 SECTION 1: EXECUTIVE SUMMARY... 4 PROPOSED PRESSURIZED IRRIGATION

SPRINGVILLE CITY PRESSURIZED IRRIGATION IMPACT FEE ANALYSIS (IFA) MAY 2014 Adopted May 20, 2014 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 SECTION 1: EXECUTIVE SUMMARY... 4 PROPOSED PRESSURIZED IRRIGATION

Hurricane Valley Fire Special Service District, Utah

Hurricane Valley Fire Special Service District, Utah NOTICING DR A FT Fire protection Impact Fee Analysis PRovided By ZIONS PUBLIC FINANCE, Inc. September 19, 2016 CONTENTS Executive Summary... 3 Impact

Hurricane Valley Fire Special Service District, Utah NOTICING DR A FT Fire protection Impact Fee Analysis PRovided By ZIONS PUBLIC FINANCE, Inc. September 19, 2016 CONTENTS Executive Summary... 3 Impact

Culinary and Pressure Irrigation Water System. Capital Facilities Plan

Culinary and Pressure Irrigation Water System Capital Facilities Plan September 2009 Prepared By: J-U-B ENGINEERS, Inc. 240 West Center St., Ste. 200 Orem, Utah 84057 (801) 226-0393 SANTAQUIN CITY CULINARY

Culinary and Pressure Irrigation Water System Capital Facilities Plan September 2009 Prepared By: J-U-B ENGINEERS, Inc. 240 West Center St., Ste. 200 Orem, Utah 84057 (801) 226-0393 SANTAQUIN CITY CULINARY

PLEASANT GROVE, UTAH TRANSPORTATION IMPACT FEE FACILITIES PLAN AND ANALYSIS

PLEASANT GROVE, UTAH TRANSPORTATION IMPACT FEE FACILITIES PLAN AND OCTOBER 2012 PREPARED BY: LEWIS YOUNG ROBERTSON & BURNINGHAM IMPACT FEE CERTIFICATION Impact Fee Facilities Plan (IFFP) Certification

PLEASANT GROVE, UTAH TRANSPORTATION IMPACT FEE FACILITIES PLAN AND OCTOBER 2012 PREPARED BY: LEWIS YOUNG ROBERTSON & BURNINGHAM IMPACT FEE CERTIFICATION Impact Fee Facilities Plan (IFFP) Certification

PARK AND RECREATION IMPACT FEE ANALYSIS (IFA) MANTUA, UT JUNE 2018 DRAFT

MANTUA, UT JUNE 2018 DRAFT") PARK AND RECREATION IMPACT FEE ANALYSIS (IFA) MANTUA, UT JUNE 2018 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 DEFINITIONS... 4 SECTION 1: EXECUTIVE SUMMARY... 5 SECTION 2: GENERAL IMPACT FEE METHODOLOGY...

PARK AND RECREATION IMPACT FEE ANALYSIS (IFA) MANTUA, UT JUNE 2018 TABLE OF CONTENTS IMPACT FEE CERTIFICATION... 3 DEFINITIONS... 4 SECTION 1: EXECUTIVE SUMMARY... 5 SECTION 2: GENERAL IMPACT FEE METHODOLOGY...

NOTICING DRAFT. Fire protection Impact Fee Facilities Plan. Hurricane Valley Fire Special Service District, Utah. ZIONS PUBLIC FINANCE, Inc.

Hurricane Valley Fire Special Service District, Utah NOTICING DRAFT Fire protection Impact Fee Facilities Plan Prepared By ZIONS PUBLIC FINANCE, Inc. September 19, 2016 Contents Executive Summary... 3

Hurricane Valley Fire Special Service District, Utah NOTICING DRAFT Fire protection Impact Fee Facilities Plan Prepared By ZIONS PUBLIC FINANCE, Inc. September 19, 2016 Contents Executive Summary... 3

TAUSSIG DEVELOPMENT IMPACT FEE JUSTIFICATION STUDY CITY OF ESCALON. Public Finance Public Private Partnerships Urban Economics Clean Energy Bonds

DAVID TAUSSIG & ASSOCIATES, INC. DEVELOPMENT IMPACT FEE JUSTIFICATION STUDY CITY OF ESCALON B. C. SEPTEMBER 12, 2016 Public Finance Public Private Partnerships Urban Economics Clean Energy Bonds Prepared

DAVID TAUSSIG & ASSOCIATES, INC. DEVELOPMENT IMPACT FEE JUSTIFICATION STUDY CITY OF ESCALON B. C. SEPTEMBER 12, 2016 Public Finance Public Private Partnerships Urban Economics Clean Energy Bonds Prepared

City Services Appendix

Technical vices 1.0 Introduction... 1 1.1 The Capital Facilities Plan... 1 1.2 Utilities Plan... 2 1.3 Key Principles Guiding Bremerton s Capital Investments... 3 1.4 Capital Facilities and Utilities Addressed

Technical vices 1.0 Introduction... 1 1.1 The Capital Facilities Plan... 1 1.2 Utilities Plan... 2 1.3 Key Principles Guiding Bremerton s Capital Investments... 3 1.4 Capital Facilities and Utilities Addressed

Impact Fees for Wastewater Systems

2013 Impact Fees for Wastewater Systems Final Report City of Kalispell 12/13/2013 Contents Executive Summary... 4 2 Introduction... 4 Financial Objective of Impact Fees... 4 Impact Fee Criteria... 4 The

2013 Impact Fees for Wastewater Systems Final Report City of Kalispell 12/13/2013 Contents Executive Summary... 4 2 Introduction... 4 Financial Objective of Impact Fees... 4 Impact Fee Criteria... 4 The

2017 UTILITY RATE STUDY WORK SESSION #2: BACKGROUND, EDUCATIONAL/INFORMATIONAL

2017 UTILITY RATE STUDY WORK SESSION #2: BACKGROUND, EDUCATIONAL/INFORMATIONAL Receive a presentation from Lewis Young Robertson & Burningham regarding the 2017 Utility Rate Study The purpose of the Council

2017 UTILITY RATE STUDY WORK SESSION #2: BACKGROUND, EDUCATIONAL/INFORMATIONAL Receive a presentation from Lewis Young Robertson & Burningham regarding the 2017 Utility Rate Study The purpose of the Council

City of Redding, California Development Impact Mitigation Fee Nexus Study

, California Development Impact Mitigation Fee Nexus Study December 5, 2017 Prepared by helping communities fund to morrow This page intentionally left blank. TABLE OF CONTENTS Executive Summary...1 Background

, California Development Impact Mitigation Fee Nexus Study December 5, 2017 Prepared by helping communities fund to morrow This page intentionally left blank. TABLE OF CONTENTS Executive Summary...1 Background

2017 WATER AND WASTEWATER IMPACT FEE STUDY CITY OF AZLE, TEXAS

2017 WATER AND WASTEWATER IMPACT FEE STUDY CITY OF AZLE, TEXAS JULY 2017 Prepared by: Weatherford Office Address: 1508 Santa Fe Drive, Suite 203 Weatherford, Texas 76086 (817) 594-9880 www.jacobmartin.com

2017 WATER AND WASTEWATER IMPACT FEE STUDY CITY OF AZLE, TEXAS JULY 2017 Prepared by: Weatherford Office Address: 1508 Santa Fe Drive, Suite 203 Weatherford, Texas 76086 (817) 594-9880 www.jacobmartin.com

Millcreek City. Parks, Recreation, Trails and Open Space Impact Fee Facilities Plan DRAFT

Millcreek City s, Recreation, Trails and Open Space Impact Fee Facilities Plan DRAFT May 2, 2018 Contents Contents... 2 Summary... 3 Background... 3 Identify the Existing and Proposed Levels of Service

Millcreek City s, Recreation, Trails and Open Space Impact Fee Facilities Plan DRAFT May 2, 2018 Contents Contents... 2 Summary... 3 Background... 3 Identify the Existing and Proposed Levels of Service

Fiscal Year 2018 Project 1 Annual Budget

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

Toronto Water Budget BU Recommended Operating Budget Recommended Capital Plan 2017 Recommended Water Rate

2017 BU25.1 Toronto Water Budget 2017 Recommended Operating Budget 2017 2026 Recommended Capital Plan 2017 Recommended Water Rate Lou Di Gironimo, General Manager, Toronto Water Budget Committee, November

2017 BU25.1 Toronto Water Budget 2017 Recommended Operating Budget 2017 2026 Recommended Capital Plan 2017 Recommended Water Rate Lou Di Gironimo, General Manager, Toronto Water Budget Committee, November

BODEGA BAY PUBLIC UTILITY DISTRICT Water and Wastewater Rate Study

BODEGA BAY PUBLIC UTILITY DISTRICT Water and Wastewater Rate Study FINAL REPORT March 22, 2018 BARTLE WELLS ASSOCIATES Independent Public Finance Advisors 1889 Alcatraz Avenue Berkeley, CA 94703-2714 Tel.

BODEGA BAY PUBLIC UTILITY DISTRICT Water and Wastewater Rate Study FINAL REPORT March 22, 2018 BARTLE WELLS ASSOCIATES Independent Public Finance Advisors 1889 Alcatraz Avenue Berkeley, CA 94703-2714 Tel.

GRASS VALLEY TRANSPORTATION IMPACT FEE PROGRAM NEXUS STUDY

HEARING REPORT GRASS VALLEY TRANSPORTATION IMPACT FEE PROGRAM NEXUS STUDY Prepared for: City of Grass Valley Prepared by: Economic & Planning Systems, Inc. March 2008 EPS #17525 S A C R A M E N T O 2150

HEARING REPORT GRASS VALLEY TRANSPORTATION IMPACT FEE PROGRAM NEXUS STUDY Prepared for: City of Grass Valley Prepared by: Economic & Planning Systems, Inc. March 2008 EPS #17525 S A C R A M E N T O 2150

CHAPTER 11. CAPITAL FACILITIES PLAN ELEMENT

CHAPTER 11. CAPITAL FACILITIES PLAN ELEMENT 11.1 INTRODUCTION A is one of eight elements required by the Growth Management Act (GMA) to be included in Yakima County s comprehensive plan. The reason for

CHAPTER 11. CAPITAL FACILITIES PLAN ELEMENT 11.1 INTRODUCTION A is one of eight elements required by the Growth Management Act (GMA) to be included in Yakima County s comprehensive plan. The reason for

Maurice Kaufman, Director of Public Works / City Engineer Bartle Wells Associates DATE: September 7, 2016 MEMORANDUM

TO: FROM: Maurice Kaufman, Director of Public Works / City Engineer Bartle Wells Associates DATE: September 7, 2016 SUBJECT: - MEMORANDUM Introduction The (City) provides sewer sanitary collection services

TO: FROM: Maurice Kaufman, Director of Public Works / City Engineer Bartle Wells Associates DATE: September 7, 2016 SUBJECT: - MEMORANDUM Introduction The (City) provides sewer sanitary collection services

2015 Update of Water and Wastewater Impact Fees

2015 Update of Water and Wastewater Impact Fees Prepared for the City of Georgetown Prepared by: Georgetown Utility Services and Chisholm Trail Special Utility District Capital Improvements Advisory Committees

2015 Update of Water and Wastewater Impact Fees Prepared for the City of Georgetown Prepared by: Georgetown Utility Services and Chisholm Trail Special Utility District Capital Improvements Advisory Committees

Presented By: L. Carson Bise II, AICP President

Impact Fee Basics: Methodology and Fee Design Presented By: L. Carson Bise II, AICP President Basic Options for One-Time Infrastructure Charges Funding from broad-based revenues (general taxes) Growth

Impact Fee Basics: Methodology and Fee Design Presented By: L. Carson Bise II, AICP President Basic Options for One-Time Infrastructure Charges Funding from broad-based revenues (general taxes) Growth

Village of Baltimore Water & Wastewater Analysis. July 2018

Village of Baltimore Water & Wastewater Analysis July 2018 Table of Contents Introductory Summary... 1 Data... 1 Water Treatment Plant (WTP)... 1 Production... 2 Costs & Debts... 2 Wastewater Treatment

Village of Baltimore Water & Wastewater Analysis July 2018 Table of Contents Introductory Summary... 1 Data... 1 Water Treatment Plant (WTP)... 1 Production... 2 Costs & Debts... 2 Wastewater Treatment

Spheria Australian Smaller Companies Fund

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

$180 $160 $140 $120 $100 $80 $60 $40 $20 $ Single Fam -New Apts -New

2012 REVENUE FORECAST Presented by Brian Henshaw September 26, 2011 1 Economic Conditions Housing starts Federal & State deficits Sovereign-debt crisis Bankruptcies Unemployment Stock Market volatility

2012 REVENUE FORECAST Presented by Brian Henshaw September 26, 2011 1 Economic Conditions Housing starts Federal & State deficits Sovereign-debt crisis Bankruptcies Unemployment Stock Market volatility

September 2014 Monthly Financial Report PREPARED BY

September 2014 Monthly Financial Report PREPARED BY Financial Accounting & Reporting Division City of Phoenix Monthly Financial Report September 2014 Table of Contents by Programs Page Performance Status

September 2014 Monthly Financial Report PREPARED BY Financial Accounting & Reporting Division City of Phoenix Monthly Financial Report September 2014 Table of Contents by Programs Page Performance Status

City of Cocoa FY 2010 Utility Rate Study. Final Report. Water, Sewer & Reclaimed Water Rates, Fees & Charges Study. Prepared by:

p FY 2010 Utility Rate Study Water, Sewer & Reclaimed Water Rates, Fees & Charges Study June 29, 2010 Prepared by: June 29, 2010 W.E. Mack Finance Director 65 Stone Street Cocoa, FL 32922 Re: FY 2010

p FY 2010 Utility Rate Study Water, Sewer & Reclaimed Water Rates, Fees & Charges Study June 29, 2010 Prepared by: June 29, 2010 W.E. Mack Finance Director 65 Stone Street Cocoa, FL 32922 Re: FY 2010

Town of Rocky Mountain House: Offsite Levy Review

Town of Rocky Mountain House: Offsite Levy Review Version 6 October 25 th, 2016 Presented to: Todd Becker, CAO Town of Rocky Mountain House PO Box 1509 Rocky Mountain House AB T4T 1B2 (403) 845-2866 tbecker@rockymtnhouse.com

Town of Rocky Mountain House: Offsite Levy Review Version 6 October 25 th, 2016 Presented to: Todd Becker, CAO Town of Rocky Mountain House PO Box 1509 Rocky Mountain House AB T4T 1B2 (403) 845-2866 tbecker@rockymtnhouse.com

Glacial Lakes Sanitary Sewer & Water District Utility Rate Study. Shelly Eldridge Ehlers Jeanne Vogt - Ehlers

Glacial Lakes Sanitary Sewer & Water District Utility Rate Study Shelly Eldridge Ehlers Jeanne Vogt - Ehlers 05/30/2017 1 Background What are Utility Funds Utility funds are used to pay for operations,

Glacial Lakes Sanitary Sewer & Water District Utility Rate Study Shelly Eldridge Ehlers Jeanne Vogt - Ehlers 05/30/2017 1 Background What are Utility Funds Utility funds are used to pay for operations,

Rates and Fees for New Connections (Developer Fees)

") Rates and Fees for New Connections (Developer Fees) Table V: New Connection (Developer) Rates and Fees Effective Date 1/1/2019 1/1/2020 1/1/2021 A. Plan Review Fees Per Linear Foot (LF) - Water $0.65 $0.65

Rates and Fees for New Connections (Developer Fees) Table V: New Connection (Developer) Rates and Fees Effective Date 1/1/2019 1/1/2020 1/1/2021 A. Plan Review Fees Per Linear Foot (LF) - Water $0.65 $0.65

F I S C A L & E C O N O M I C U P D A T E

W A S H I N G T O N C O U N T Y, M A R Y L A N D S E P T E M B E R 2 1 5 F I S C A L & E C O N O M I C U P D A T E M A J O R E C O N O M I C T R E N D S Inside this Report: Employment Data 1 The following

W A S H I N G T O N C O U N T Y, M A R Y L A N D S E P T E M B E R 2 1 5 F I S C A L & E C O N O M I C U P D A T E M A J O R E C O N O M I C T R E N D S Inside this Report: Employment Data 1 The following

SELF-STORAGE FOR SALE

PURCHASE PRICE: $495,000 CAP RATE: 8.68% OCCUPANCY: 86.4% NOI: $42,973 LOT SIZE: 1.462ac (combined) BLDG CLASS: C OVERVIEW Multi-building storage facility in a rapidly growing area. The land offers over

PURCHASE PRICE: $495,000 CAP RATE: 8.68% OCCUPANCY: 86.4% NOI: $42,973 LOT SIZE: 1.462ac (combined) BLDG CLASS: C OVERVIEW Multi-building storage facility in a rapidly growing area. The land offers over

Discussion of Discounting in Oil and Gas Property Appraisal

Discussion of Discounting in Oil and Gas Property Appraisal Because investors prefer immediate cash returns over future cash returns, investors pay less for future cashflows; i.e., they "discount" them.

Discussion of Discounting in Oil and Gas Property Appraisal Because investors prefer immediate cash returns over future cash returns, investors pay less for future cashflows; i.e., they "discount" them.

Washington Gas Light Company Utility Rate Requests District of Columbia Formal Case No Decision May 15, 2013

Washington Gas Light Company Utility Rate Requests District of Columbia Formal Case No. 1093 Decision May 15, 2013 July 25, 2013 Update to AOBA Utility Committee Meeting 1 Formal Case No. 1093 Base Rate

Washington Gas Light Company Utility Rate Requests District of Columbia Formal Case No. 1093 Decision May 15, 2013 July 25, 2013 Update to AOBA Utility Committee Meeting 1 Formal Case No. 1093 Base Rate

Water Operations Current Month - November 2018

November 2018 Water Operations Current Month - November 2018 $8.0 Net Operating Revenue (Net of Bad Debt) $8.1 $8.6 $8.0 2.0 1.5 Volumes Billions of Gallons Sold 1.8 1.7 1.6 $6.0 1.0 $4.0 $2.0 0.5 Actual

November 2018 Water Operations Current Month - November 2018 $8.0 Net Operating Revenue (Net of Bad Debt) $8.1 $8.6 $8.0 2.0 1.5 Volumes Billions of Gallons Sold 1.8 1.7 1.6 $6.0 1.0 $4.0 $2.0 0.5 Actual

Common stock prices 1. New York Stock Exchange indexes (Dec. 31,1965=50)2. Transportation. Utility 3. Finance

2. Transportation. Utility 3. Finance") Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Richard Pearson, Community Development Director Tim Tucker, City Engineer

CITY OF MARTINEZ CITY COUNCIL AGENDA February 21, 2007 TO: FROM: PREPARED BY: SUBJECT: Mayor and City Council Don Blubaugh, City Manager Richard Pearson, Community Development Director Tim Tucker, City

CITY OF MARTINEZ CITY COUNCIL AGENDA February 21, 2007 TO: FROM: PREPARED BY: SUBJECT: Mayor and City Council Don Blubaugh, City Manager Richard Pearson, Community Development Director Tim Tucker, City

Policy CIE The following are the minimum acceptable LOS standards to be utilized in planning for capital improvement needs:

Vision Statement: Provide high quality public facilities that meet and exceed the minimum level of service standards. Goals, Objectives and Policies: Goal CIE-1. The City shall provide for facilities and

Vision Statement: Provide high quality public facilities that meet and exceed the minimum level of service standards. Goals, Objectives and Policies: Goal CIE-1. The City shall provide for facilities and

City of Antioch Development Impact Fee Study

Report City of Antioch Development Impact Fee Study Prepared for: City of Antioch Prepared by: Economic & Planning Systems, Inc. February 2014 EPS #20001 Table of Contents 1. INTRODUCTION AND RESULTS...

Report City of Antioch Development Impact Fee Study Prepared for: City of Antioch Prepared by: Economic & Planning Systems, Inc. February 2014 EPS #20001 Table of Contents 1. INTRODUCTION AND RESULTS...

Cash & Liquidity The chart below highlights CTA s cash position at January 2018 compared to January 2017.

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for January 2018 Date: March 14, 2018 I. Summary CTA s financial results are $1.7 million unfavorable

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for January 2018 Date: March 14, 2018 I. Summary CTA s financial results are $1.7 million unfavorable

Tooele County. Financial Recovery Plan 3rd Quarter 2014 Update

Tooele County Financial Recovery Plan 3rd Quarter 2014 Update Original Projection 14,000,000 Tooele County Cash 2009-2015 12,000,000 10,000,000 8,000,000 6,000,000 4,000,000 2,000,000 - Ahead of Projection

Tooele County Financial Recovery Plan 3rd Quarter 2014 Update Original Projection 14,000,000 Tooele County Cash 2009-2015 12,000,000 10,000,000 8,000,000 6,000,000 4,000,000 2,000,000 - Ahead of Projection

REQUEST FOR PROPOSALS

REQUEST FOR PROPOSALS Water & Sewer Utilities Optimization City of Wichita Public Works & Utilities May 14, 2015 PROJECT DEFINITION The City of Wichita is seeking proposals for assistance with the risk,

REQUEST FOR PROPOSALS Water & Sewer Utilities Optimization City of Wichita Public Works & Utilities May 14, 2015 PROJECT DEFINITION The City of Wichita is seeking proposals for assistance with the risk,

CROMWELL FIRE DISTRICT

CROMWELL, CONNECTICUT BASIC FINANCIAL STATEMENTS AS OF TOGETHER WITH INDEPENDENT AUDITORS REPORT REQUIRED SUPPLEMENTARY INFORMATION, OTHER SUPPLEMENTARY INFORMATION, AND GOVERNMENTAL AUDITING STANDARDS

CROMWELL, CONNECTICUT BASIC FINANCIAL STATEMENTS AS OF TOGETHER WITH INDEPENDENT AUDITORS REPORT REQUIRED SUPPLEMENTARY INFORMATION, OTHER SUPPLEMENTARY INFORMATION, AND GOVERNMENTAL AUDITING STANDARDS

UTILITY RATE STUDY. Public Hearing

UTILITY RATE STUDY Public Hearing. Public January 23, 2018 Resources Management Group, Inc. Utility, Rate, Financial, and Management Consultants Rate Guiding Principles Recognized Revenues Should Be Sufficient

UTILITY RATE STUDY Public Hearing. Public January 23, 2018 Resources Management Group, Inc. Utility, Rate, Financial, and Management Consultants Rate Guiding Principles Recognized Revenues Should Be Sufficient

CITY OF CALISTOGA WATER RATE STUDY FINAL REPORT

CITY OF CALISTOGA WATER RATE STUDY FINAL REPORT February 2, 218 This page was intentionally left blank. City of Calistoga Water Rate Study Report Page 2 February 2, 218 Dylan Feik City Manager City of

CITY OF CALISTOGA WATER RATE STUDY FINAL REPORT February 2, 218 This page was intentionally left blank. City of Calistoga Water Rate Study Report Page 2 February 2, 218 Dylan Feik City Manager City of

SAUSALITO-MARIN CITY SANITARY DISTRICT 1 EAST ROAD SAUSALITO, CALIFORNIA Telephone: (415) Fax: (415)

Fax: (415)") 1 EAST ROAD SAUSALITO, CALIFORNIA Telephone: (415) 332-0244 Fax: (415) 332-0453 Budget FY 2017/18 Adopted by Board on June 5, 2017 BUDGET EXECUTIVE SUMMARY FISCAL YEAR 2017/18 DISTRICT OVERVIEW The Sausalito-Marin

1 EAST ROAD SAUSALITO, CALIFORNIA Telephone: (415) 332-0244 Fax: (415) 332-0453 Budget FY 2017/18 Adopted by Board on June 5, 2017 BUDGET EXECUTIVE SUMMARY FISCAL YEAR 2017/18 DISTRICT OVERVIEW The Sausalito-Marin

LAFCo 509 W. WEBER AVENUE SUITE 420 STOCKTON, CA 95203

SAN JOAQUIN LOCAL AGENCY FORMATION COMMISSION AGENDA ITEM NO. 2 LAFCo 509 W. WEBER AVENUE SUITE 420 STOCKTON, CA 95203 REVISED EXECUTIVE OFFICER S REPORT March 10, 2016 TO: FROM: SUBJECT: LAFCo Commissioners

SAN JOAQUIN LOCAL AGENCY FORMATION COMMISSION AGENDA ITEM NO. 2 LAFCo 509 W. WEBER AVENUE SUITE 420 STOCKTON, CA 95203 REVISED EXECUTIVE OFFICER S REPORT March 10, 2016 TO: FROM: SUBJECT: LAFCo Commissioners

FINAL PROJECT PLAN TAX INCREMENT DISTRICT FOR RED ROCK WATER RESERVOIR CITY OF RAPID CITY. Prepared by the

FINAL PROJECT PLAN TAX INCREMENT DISTRICT FOR RED ROCK WATER RESERVOIR CITY OF RAPID CITY Prepared by the Rapid City Planning Department September 2003 Tax Increment District 43 Project Plan FINAL INTRODUCTION

FINAL PROJECT PLAN TAX INCREMENT DISTRICT FOR RED ROCK WATER RESERVOIR CITY OF RAPID CITY Prepared by the Rapid City Planning Department September 2003 Tax Increment District 43 Project Plan FINAL INTRODUCTION

Tremonton City Corporation City Council Budget Workshop May 20, 2009 Meeting held at 102 South Tremont Street CITY COUNCIL BUDGET WORKSHOP

Tremonton City Corporation City Council Budget Workshop May 20, 2009 Meeting held at 102 South Tremont Street Members Present: David Deakin Roger Fridal Jeff Reese Max Weese, Mayor Darlene Hess, Recorder

Tremonton City Corporation City Council Budget Workshop May 20, 2009 Meeting held at 102 South Tremont Street Members Present: David Deakin Roger Fridal Jeff Reese Max Weese, Mayor Darlene Hess, Recorder

PHOENIX ENERGY MARKETING CONSULTANTS INC. HISTORICAL NATURAL GAS & CRUDE OIL PRICES UPDATED TO July, 2018

Jan-01 $12.9112 $10.4754 $9.7870 $1.5032 $29.2595 $275.39 $43.78 $159.32 $25.33 Feb-01 $10.4670 $7.8378 $6.9397 $1.5218 $29.6447 $279.78 $44.48 $165.68 $26.34 Mar-01 $7.6303 $7.3271 $5.0903 $1.5585 $27.2714

Jan-01 $12.9112 $10.4754 $9.7870 $1.5032 $29.2595 $275.39 $43.78 $159.32 $25.33 Feb-01 $10.4670 $7.8378 $6.9397 $1.5218 $29.6447 $279.78 $44.48 $165.68 $26.34 Mar-01 $7.6303 $7.3271 $5.0903 $1.5585 $27.2714

bae urban economics Memorandum Fee Analysis for General Plan Update Cost Recovery and for General Plan Implementation

bae urban economics Memorandum To: Vacaville City Council From: Matt Kowta, Principal, MCP Date: July 10, 2016 Re: Fee Analysis for General Plan Update Cost Recovery and for General Plan Implementation

bae urban economics Memorandum To: Vacaville City Council From: Matt Kowta, Principal, MCP Date: July 10, 2016 Re: Fee Analysis for General Plan Update Cost Recovery and for General Plan Implementation

CITY OF MODESTO COMMUNITY FACILITIES DISTRICT NO (HETCH HETCHY) CFD REPORT

CFD REPORT") CITY OF MODESTO COMMUNITY FACILITIES DISTRICT NO. 2005-1 (HETCH HETCHY) CFD REPORT September 23, 2005 Goodwin Consulting Group, Inc. 555 University Avenue, Suite 280 Sacramento, California 95825 Phone

CITY OF MODESTO COMMUNITY FACILITIES DISTRICT NO. 2005-1 (HETCH HETCHY) CFD REPORT September 23, 2005 Goodwin Consulting Group, Inc. 555 University Avenue, Suite 280 Sacramento, California 95825 Phone

CPA Australia Plan Your Own Enterprise Competition

Financial Plan Your financial plan should include: 1. A list of Start-Up Costs and how these will be paid for (eg from savings, bank loan or family loan) 2. A Breakeven Analysis, which includes: a list

Financial Plan Your financial plan should include: 1. A list of Start-Up Costs and how these will be paid for (eg from savings, bank loan or family loan) 2. A Breakeven Analysis, which includes: a list

Earned Value Management An Overview March 2014

Earned Value Management An Overview March 2014 SAVE International Cascadia Chapter Introduction What is Earned Value? Why is Earned Value important? What is required? Earned Value Definitions & Process

Earned Value Management An Overview March 2014 SAVE International Cascadia Chapter Introduction What is Earned Value? Why is Earned Value important? What is required? Earned Value Definitions & Process

CAPITAL IMPROVEMENTS ELEMENT

Goals, Objectives and Policies CAPITAL IMPROVEMENTS ELEMENT GOAL 9.1.: USE SOUND FISCAL POLICIES TO PROVIDE ADEQUATE PUBLIC FACILITIES TO ALL RESIDENTS WITHIN THE CITY. FISCAL POLICIES MUST PROTECT INVESTMENTS

Goals, Objectives and Policies CAPITAL IMPROVEMENTS ELEMENT GOAL 9.1.: USE SOUND FISCAL POLICIES TO PROVIDE ADEQUATE PUBLIC FACILITIES TO ALL RESIDENTS WITHIN THE CITY. FISCAL POLICIES MUST PROTECT INVESTMENTS

CITY OF ROSEBURG, OREGON TABLE OF CONTENTS ENTERPRISE FUNDS

TABLE OF CONTENTS ENTERPRISE FUNDS Storm Drainage Fund... 121-124 Off Street Parking Fund... 125-126 Airport Fund... 127-131 Water Service Fund... 132-145 STORM DRAINAGE FUND CURRENT OPERATIONS This fund

TABLE OF CONTENTS ENTERPRISE FUNDS Storm Drainage Fund... 121-124 Off Street Parking Fund... 125-126 Airport Fund... 127-131 Water Service Fund... 132-145 STORM DRAINAGE FUND CURRENT OPERATIONS This fund

STORM WATER USER RATE STUDY

LY STORM WATER USER RATE STUDY STORM WATER UTILITY OREM CITY, UTAH JANUARY 2016 PREPARED BY LEWIS YOUNG ROBERTSON & BURNINGHAM, INC. TABLE OF CONTENTS SECTION I: EXECUTIVE SUMMARY... 3 SECTION II: OVERVIEW

LY STORM WATER USER RATE STUDY STORM WATER UTILITY OREM CITY, UTAH JANUARY 2016 PREPARED BY LEWIS YOUNG ROBERTSON & BURNINGHAM, INC. TABLE OF CONTENTS SECTION I: EXECUTIVE SUMMARY... 3 SECTION II: OVERVIEW

SANITARY SEWER FUND PUBLIC WORKS

285 2015 2016 2017 2017 2018 Actual Actual Budget Estimate Budget Beginning Net Position $ 1,556,256 $ 2,133,912 $ 3,537,945 $ 3,537,945 $ 3,333,823 Operating Revenue 5,758,183 6,475,486 6,751,246 6,681,766

285 2015 2016 2017 2017 2018 Actual Actual Budget Estimate Budget Beginning Net Position $ 1,556,256 $ 2,133,912 $ 3,537,945 $ 3,537,945 $ 3,333,823 Operating Revenue 5,758,183 6,475,486 6,751,246 6,681,766

HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN (UTILITY IMPROVEMENTS)

") HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN (UTILITY IMPROVEMENTS) SEPTEMBER 15, 2009 HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT

HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT PLAN (UTILITY IMPROVEMENTS) SEPTEMBER 15, 2009 HACKBERRY HIDDEN COVE PUBLIC IMPROVEMENT DISTRICT NO. 2 SERVICE AND ASSESSMENT

WATER RATE STUDY CITY OF SALIDA. Revised March West Sixth Street, Suite 200 Glenwood Springs, CO

WATER RATE STUDY CITY OF SALIDA Revised March 2011 Prepared by Tyler Harpel, PE In Conjunction with City Staff 118 West Sixth Street, Suite 200 Glenwood Springs, CO 81601 970.945.1004 970.945.5948 fax

WATER RATE STUDY CITY OF SALIDA Revised March 2011 Prepared by Tyler Harpel, PE In Conjunction with City Staff 118 West Sixth Street, Suite 200 Glenwood Springs, CO 81601 970.945.1004 970.945.5948 fax

Corporate Accounting: Earnings and Distribution

Chapter 20 Corporate Accounting: Earnings and Distribution Net income of a corporation and corporate income taxes Cash dividends Stock dividends Stock splits Appropriations of retained earnings Retained

Chapter 20 Corporate Accounting: Earnings and Distribution Net income of a corporation and corporate income taxes Cash dividends Stock dividends Stock splits Appropriations of retained earnings Retained

CITY OF ANN ARBOR WATER & SEWER COST OF SERVICE STUDY

1 CITY OF ANN ARBOR WATER & SEWER COST OF SERVICE STUDY 12.20.2017 Overview 1. Sufficiency 2. Rate Classification 3. to Serve 4. Rate Structures 5. Customer Impacts 6. Affordability Program Foundation

1 CITY OF ANN ARBOR WATER & SEWER COST OF SERVICE STUDY 12.20.2017 Overview 1. Sufficiency 2. Rate Classification 3. to Serve 4. Rate Structures 5. Customer Impacts 6. Affordability Program Foundation

January 2015 Monthly Financial Report PREPARED BY

January 2015 Monthly Financial Report PREPARED BY Financial Accounting & Reporting Division City of Phoenix Monthly Financial Report January 2015 Table of Contents by Programs Page Performance Status

January 2015 Monthly Financial Report PREPARED BY Financial Accounting & Reporting Division City of Phoenix Monthly Financial Report January 2015 Table of Contents by Programs Page Performance Status

Accountant s Compilation Report

Tel: 817-738-2400 Fax: 817-738-1995 www.bdo.com 6050 Southwest Blvd, Suite 300 Fort Worth, TX 76109 Accountant s Compilation Report Joseph Portugal Town Administrator Town of Westover Hills, Texas Management

Tel: 817-738-2400 Fax: 817-738-1995 www.bdo.com 6050 Southwest Blvd, Suite 300 Fort Worth, TX 76109 Accountant s Compilation Report Joseph Portugal Town Administrator Town of Westover Hills, Texas Management

CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)

![CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)](/thumbs/93/114312533.jpg "CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)") CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES Goal 1: [CI] (EFF. 7/16/90) To use sound fiscal policies to provide adequate public facilities concurrent with, or prior to development in order

CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES Goal 1: [CI] (EFF. 7/16/90) To use sound fiscal policies to provide adequate public facilities concurrent with, or prior to development in order

Cash & Liquidity The chart below highlights CTA s cash position at March 2017 compared to March 2016.

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for March 2017 Date: May 10, 2017 I. Summary CTA s financial results are $0.6 million favorable to budget

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for March 2017 Date: May 10, 2017 I. Summary CTA s financial results are $0.6 million favorable to budget

Quigley Canyon Ranch Cost/Benefit Study Update

Quigley Canyon Ranch Cost/Benefit Study Update April 26, 2012 RICHARD CAPLAN & ASSOCIATES Mayor Fritz Haemmerle Hailey City Council 115 Main Street Hailey, ID 83333 April 26, 2012 Dear Mayor Haemmerle

Quigley Canyon Ranch Cost/Benefit Study Update April 26, 2012 RICHARD CAPLAN & ASSOCIATES Mayor Fritz Haemmerle Hailey City Council 115 Main Street Hailey, ID 83333 April 26, 2012 Dear Mayor Haemmerle

Ivory Development, LLC, et. al. vs. Timpanogos Special Service District

To: From: Craig Call, Esq. Jon Call, Esq. Anderson, Call & Wilkinson Attorneys for the Plaintiffs Christine Richman, MBA GSBS Richman Consulting Date: November 7, 2014 Re: Ivory Development, LLC, et. al.

To: From: Craig Call, Esq. Jon Call, Esq. Anderson, Call & Wilkinson Attorneys for the Plaintiffs Christine Richman, MBA GSBS Richman Consulting Date: November 7, 2014 Re: Ivory Development, LLC, et. al.

GENERAL FUND AT A GLANCE Category Budget YTD Actual % % Year Passed Resources 8.33% Uses 8.33% $0 $1,330,750

City of Edmond Monthly Financial Report FY 2008/2009 Through the Month Ended Unaudited - Intended for Management Purposes Only The following is a summary of the City's financial results for operating funds.

City of Edmond Monthly Financial Report FY 2008/2009 Through the Month Ended Unaudited - Intended for Management Purposes Only The following is a summary of the City's financial results for operating funds.

TABLE OF CONTENTS LIST OF TABLES

TABLE OF CONTENTS A. GOALS, OBJECTIVES, AND POLICIES... 3 B. SUMMARY... 17 LIST OF TABLES Table IX 1: City of Winter Springs Five-Year Schedule of Capital Improvements (SCI) FY 2013/14-2017/18... 11 Table

TABLE OF CONTENTS A. GOALS, OBJECTIVES, AND POLICIES... 3 B. SUMMARY... 17 LIST OF TABLES Table IX 1: City of Winter Springs Five-Year Schedule of Capital Improvements (SCI) FY 2013/14-2017/18... 11 Table

PETERS TOWNSHIP SANITARY AUTHORITY 2011 BUDGET WORKSHOP. November 30, 2010

PETERS TOWNSHIP SANITARY AUTHORITY 2011 BUDGET WORKSHOP November 30, 2010 Agenda A. 2010 Budget Performance Summary B. 2011 Budget Request C. 2011 Capital Plan D. Consulting Engineer s Annual Report Preliminary

PETERS TOWNSHIP SANITARY AUTHORITY 2011 BUDGET WORKSHOP November 30, 2010 Agenda A. 2010 Budget Performance Summary B. 2011 Budget Request C. 2011 Capital Plan D. Consulting Engineer s Annual Report Preliminary

Large Commercial Rate Simplification

Large Commercial Rate Simplification Presented to: Key Account Luncheon Red Lion Hotel Presented by: Mark Haddad Assistant Director/CFO October 19, 2017 Most Important Information First There is no rate

Large Commercial Rate Simplification Presented to: Key Account Luncheon Red Lion Hotel Presented by: Mark Haddad Assistant Director/CFO October 19, 2017 Most Important Information First There is no rate

Fiscal Year 2010 Packwood Annual Operating Budget

Fiscal Year 2010 Packwood Annual Operating Budget Table of Contents Table Page Summary 3 Key Assumptions/Qualifications 4 Summary of Operating and Capital Costs Table 1 5 Summary of Revenues Table 2 6

Fiscal Year 2010 Packwood Annual Operating Budget Table of Contents Table Page Summary 3 Key Assumptions/Qualifications 4 Summary of Operating and Capital Costs Table 1 5 Summary of Revenues Table 2 6

MESA ROYALTY TRUST FEDERAL INCOME TAX INFORMATION

MESA ROYALTY TRUST 2006 FEDERAL INCOME TAX INFORMATION MESA ROYALTY TRUST (The Trust ) 2006 FEDERAL INCOME TAX INFORMATION Instructions for Schedules A, B and C Schedule A For Certificate Holders who

MESA ROYALTY TRUST 2006 FEDERAL INCOME TAX INFORMATION MESA ROYALTY TRUST (The Trust ) 2006 FEDERAL INCOME TAX INFORMATION Instructions for Schedules A, B and C Schedule A For Certificate Holders who

Impact of Rising Construction Costs on State Highway Construction Programs

Impact of Rising Construction Costs on State Highway Construction Programs By William Buechner, PhD. VP for Economics and Research American Road & Transportation Builders Association September 11, 2007

Impact of Rising Construction Costs on State Highway Construction Programs By William Buechner, PhD. VP for Economics and Research American Road & Transportation Builders Association September 11, 2007

FUNDING SOURCES Restricted vs. Un-Restricted Funding Sources Fund Balances and Projected Funding Availability IBank Loan

FUNDING SOURCES The following section discusses the major funding sources available to fund projects. ing amounts included in the s column are those that are available for use as of preparation of this

FUNDING SOURCES The following section discusses the major funding sources available to fund projects. ing amounts included in the s column are those that are available for use as of preparation of this

WESTERN MASSACHUSETTS

Page 1 of 5 PART A - TOTAL DELIVERY RATES (1) Reconciling Rates = Sum of Part B Rates MDPU Service Rate Base Reconciling Total Revenue Energy Efficiency Charge (EEC) Renewable Total Schedule No. Area Component

Page 1 of 5 PART A - TOTAL DELIVERY RATES (1) Reconciling Rates = Sum of Part B Rates MDPU Service Rate Base Reconciling Total Revenue Energy Efficiency Charge (EEC) Renewable Total Schedule No. Area Component

General Provisions (CY 12-mo Components)

") WATER RATE HISTORICAL DATA Prop Prop Prop Prop Prop Prop Prop Prop Prop Prop Prop Prop General Provision Tier Classes Description Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18

WATER RATE HISTORICAL DATA Prop Prop Prop Prop Prop Prop Prop Prop Prop Prop Prop Prop General Provision Tier Classes Description Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18

Kirkwood Meadows Public Utility District Finance Committee REGULAR MEETING NOTICE

Kirkwood Meadows Public Utility District Finance Committee REGULAR MEETING NOTICE NOTICE IS HEREBY GIVEN that the Finance Committee of the Kirkwood Meadows Public Utility District has called a Special

Kirkwood Meadows Public Utility District Finance Committee REGULAR MEETING NOTICE NOTICE IS HEREBY GIVEN that the Finance Committee of the Kirkwood Meadows Public Utility District has called a Special

Overview. Highland Creek Wastewater Treatment Plant. R.C. Harris Water Treatment Plant

Presentation to Budget Committee October 19, 2009 2010 Operating Budget 2010-20192019 Capital Budget 1 Overview Serves 3.1 million residents and businesses in Toronto, and portions of York and Peel Over

Presentation to Budget Committee October 19, 2009 2010 Operating Budget 2010-20192019 Capital Budget 1 Overview Serves 3.1 million residents and businesses in Toronto, and portions of York and Peel Over

Department of Public Welfare (DPW)

") Department of Public Welfare (DPW) Office of Income Maintenance Electronic Benefits Transfer Card Risk Management Report Out-of-State Residency Review FISCAL YEAR 2014-2015 September 2014 (June, July and

Department of Public Welfare (DPW) Office of Income Maintenance Electronic Benefits Transfer Card Risk Management Report Out-of-State Residency Review FISCAL YEAR 2014-2015 September 2014 (June, July and

XML Publisher Balance Sheet Vision Operations (USA) Feb-02

Feb-02") Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Quarterly Financial Report. Reporting financial results for the first quarter ended September 30, 2014