Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

|

|

|

- Irene Sabrina Kelly

- 6 years ago

- Views:

Transcription

1 Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you must: Participate in the program on your own computer connection (no sharing) if you need to register additional people, please call customer service at x10 (or x10). Strafford accepts American Express, Visa, MasterCard, Discover. Listen on-line via your computer speakers. Respond to five prompts during the program plus a single verification code. You will have to write down only the final verification code on the attestation form, which will be ed to registered attendees. To earn full credit, you must remain connected for the entire program. WHO TO CONTACT For Additional Registrations: -Call Strafford Customer Service x10 (or x10) For Assistance During the Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN.

2 Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please immediately so we can address the problem. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

3 Form 5227 Reporting Aug. 20, 2015 Ted R. Batson, Jr., Executive Vice President Renaissance Joe Carter, Director of Planned Giving Oklahoma City Community Foundation

4 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

5 Form 5227 Reporting 5

6 6

7 7

8 8

9 9

10 10

11 11

12 12

13 13

14 14

15 15

16 16

17 17

18 18

19 19

20 20

21 21

22 22

23 23

24 24

25 25

26 26

27 27

28 28

29 29

30 30

31 Preparing Form 5227 Renaissance Administration Ted R. Batson, Jr, J.D., M.B.A., CPA, CFP August 20, 2015

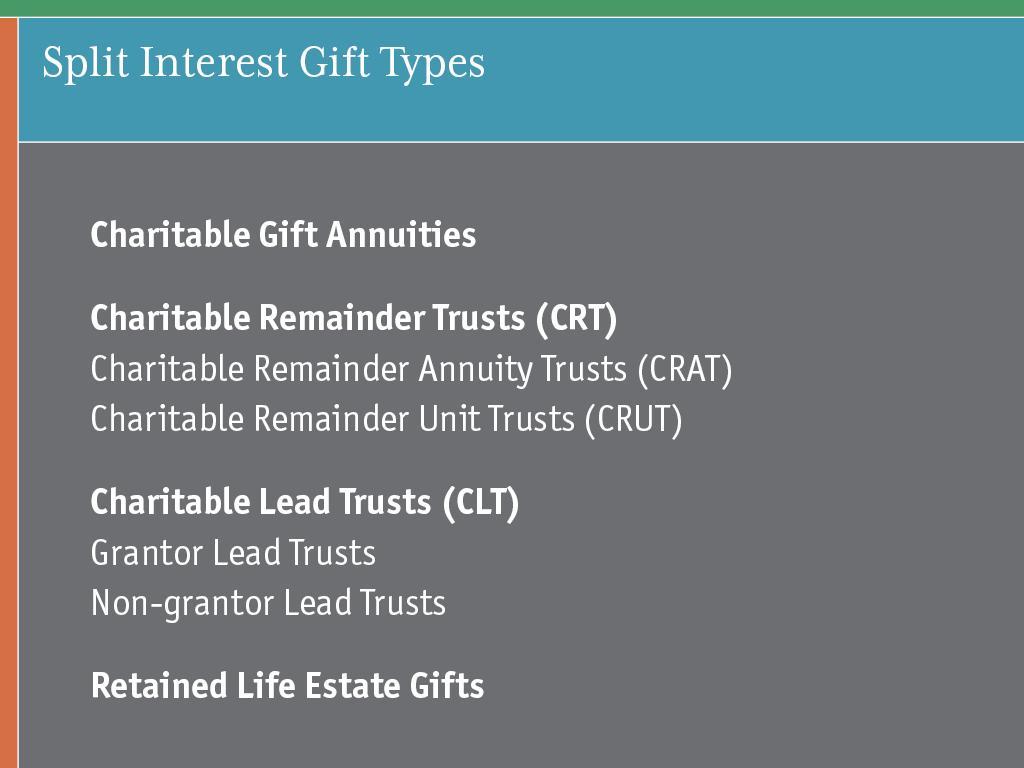

32 Substantiation Rules Transfers to CRTs and CLTs are exempt from the contemporaneous written acknowledgment rules that normally apply to charitable gifts By regulation, a statement must be attached to return on which a donor claims a gift for a transfer to a CRT showing the computation of the present value of a remainder interest Prudence dictates a similar approach should be taken for a CLT This statement is not required to be provided by the trustee, but rather is the responsibility of the settlor However, many charities and administrators own the software to produce this statement and will do so 32

33 What is Form 5227? An information return No tax due with the return For split-interest trusts Charitable remainder trusts Charitable lead trusts Pooled income funds Other trusts for which a deduction was allowed for an amount transferred in trust after May 26, 1969 by one of the sections listed in IRC 4947(a)(2) Sections 170, 545(b)(2), 642(c), 2055, 2106(a)(2), or 2522 Split-interests trusts have not been required to file Form 1041-A since

34 Subject to Public Inspection Form 5227 is subject to public inspection Information about trusts that filed Form 5227 has been included in the IRS Business Master File Commercial companies downloaded this list and created publicly searchable databases Search for your client s CRT, CLT, or PIF on Google! Consider not using the client s name in the name of the trust But note that the trustee s name and address are disclosable Portions of the return are not disclosable Trust agreement (including amendments), Schedule A, Schedules(s) K-1, attachments referencing contributor info 34

35 When and Where to File Due April 15 Trusts that file Form 5227 must use a calendar year Make sure distributions are paid before filing the return Use Form 8868 to request an extension of time to file An automatic extension is available to July 15 IRS may grant a second, non-automatic extension to October 15 TRAP: Forms 4720 and 8870 may be required and require their own extension The need to file an extension request may not be apparent until after April 15 File using this address Department of the Treasury Internal Revenue Service Ogden, UT

36 Attaching a Copy of the Trust Instrument Attach a copy of the trust instrument to the return in the first year Include a declaration signed under penalty of perjury that the copy is a true and complete copy Attach a copy of any amendments to the trust instrument to the return covering the year in which the amendment is made 36

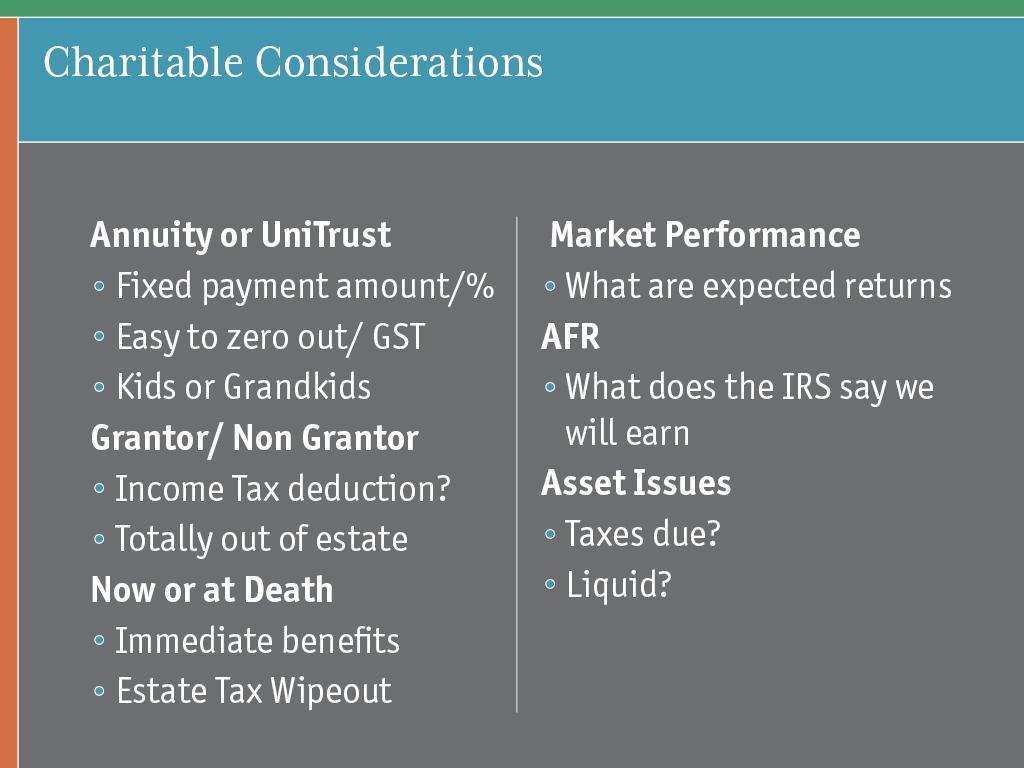

37 Consequences of Failing to File The general rule is a daily delinquency penalty of $20 per day up to a maximum of $10,000 Exception: If the trust s gross income exceeds $250,000, the penalty is $100 per day up to a maximum of $50,000 The penalty is imposed on the trust Exception: Knowingly failing to file the return results in the additional imposition of the penalty on the person who knowingly failed to file and they are personally liable for this additional penalty For 2015 and beyond, the penalty amounts described above are indexed for inflation Amounts of $5,000 or more will increase in $500 increments Amounts less than $5,000 will increase in $5 increments 37

38 Common Mistakes Failing to read the trust agreement Misidentifying the type of trust Incorrectly computing the amount of required distributions Paying the fixed percentage unitrust amount instead of the lesser of that amount and TAI Not reviewing the document for relevant TAI provisions Failing to note that excess income is to be distributed in a CLT Completing parts that aren t required or omitting parts that are required See roadmap in Appendix A Filing a Form 1041 when not required 38

39 Form Overview Part I Income and Deductions Part II Schedule of Distributable Income Part IIIA Distributions of Principal for Charitable Purposes Part IIIB Accumulated Income Set Aside and Income Distributions for Charitable Purposes Part IV Balance Sheet Part V CRAT and CRUT Information Part VI Statements Regarding Activities (including those for Which Form 4720 May Be Required ) Part VII Questionnaire for CLTs, PIFs, and CRTs 39

40 Qualified Dividends The Internal Revenue Code includes CRTs among the list of entities for which investment firms are not required to issue Forms 1099 See IRC 6042 and 6049(b)(4)(L)(i) We ve specifically encountered this issue with American Funds Is anyone in the group familiar with other investment firms that follow this practice? The AICPA has submitted a legislative proposal to address this issue 40

41 Four-Tier Rules The Four-Tiers are an accumulation schedule Four-tier accounting only apply to CRTs Accumulated balances are used to characterize distributions to trust beneficiaries The face of the form is insufficient to fully track and maintain the four-tier balances Tax prep software helps But a separate workpaper may be required to fully track the interaction of the four-tiers 41

42 Four-Tier Rules (continued) The four-tier rules are described at Treas. Reg (d)(1) and (2) Maintain four categories (Tiers) Ordinary Income Capital Gains Other (Nontaxable) Income Principal, or Corpus Special capital gain netting rules apply These are described in the regs A special guidance is provided in the instructions for applying the netting rules 42

43 Four-Tier Rules (continued) Within the tiers maintain Classes based on highest potentially applicable tax rate Pre-2013 dollars are maintained in classes that do not include the net investment income tax (Excluded) Post-2012 dollars are maintained in classes that include the net investment income tax Income types within each class (e.g., U.S. Gov t interest, corporate bond interest, nonqualified dividends, qualified dividends) When preparing each beneficiary s Schedule K-1, relieve the categories in highest to lowest tax rate order Similarly, relieve tax rate classes in highest to lowest tax rate order 43

44 Part IV- Balance Sheet Column (c) Fair Market Value All forms of CRUTs (CRUT, NICRUT, NIMCRUT, Flip-CRUT) must complete column (c) Use the value on the date used to compute the unitrust (fixed percentage) amount Make sure to read the Trust Agreement to determine the relevant date(s) 44

45 Net Investment Income Tax A CRT is not subject to the Net Investment Income Tax Beneficiaries are subject to the tax to the extent their distributions include NII amounts Undistributed amounts from prior to 2013 are not included in NII A CLT and a PIF are not exempt from the tax But amounts of income distributed to charitable and noncharitable beneficiaries carry out NII and reduce the trust s taxable amount For PIFs the deduction for long-term capital gains permanently set aside for charitable purposes reduces the trust s taxable amount These deductions often reduce the trust s taxable amount below the threshold amount 45

46 Net Investment Income Tax (continued) Two methods are allowed for CRTs to capture Net Investment Income Tax information Section 664 Method: This method integrates with the category and class system to create tax rate classes that are the sum of the income tax rate and the 3.8% net investment income tax rate Then as each tax rate class is drawn from, net investment income taxable amounts flow out to the beneficiary 46

47 47 Section 664 Method Illustrated

48 Net Investment Income Tax (continued) 48 Simplified Method: This method operates outside the category/class structure Cumulative totals of net investment income and non-net investment income buckets are maintained Only post-2012 amounts are treated as net investment income Each year the amount of the distribution that is net investment income is determined by First looking to the cumulative, undistributed net investment income If the distribution is larger than the cumulative, undistributed net investment income, then look to the cumulative, undistributed non-net investment income For trusts created prior to 2013, the Simplified Method had to be adopted on the 2013 return. The Simplified Method can be elected on an amended return so long as the year to be amended and all intervening years for both the CRT and the beneficiaries are open

49 Net Investment Income Tax (continued) For trusts created after 2012, the Simplified Method must be elected the first year the trust is required to file Form

50 Unrelated Business Taxable Income (UBTI) Just $1 of UBTI triggers a tax The tax on UBTI is 100% of the UBTI amount Report the tax using IRS Form 4720 Return of Certain Excise Taxes Under Chapters 41 and 42 of the Internal Revenue Code Use Form 990-T as an attachment to provide relevant details Common sources of UBTI? Publicly Traded Partnerships (see Box 20, Code V) Unrelated debt financed income Trading on margin Mortgaged Property Remember the $1,000 specific deduction in arriving at taxable UBTI IRC 512(b)(12) 50

51 Self-Dealing and Other Chapter 42 Excise Taxes Split-Interest trusts are prohibited from Engaging in self-dealing IRC 4941 Purchase from, sale to, loan to/from, lease to/from, use of income or assets of trust by a disqualified person (see IRC 4946) Possessing excess business holdings IRC 4943 See exception for CRTs IRC 4947(b)(3)(B) See exception for certain CLTs IRC 4947(b)(3)(A) Purchasing jeopardizing investments IRC 4944 See exception for CRTs IRC 4947(b)(3)(B) See exception for certain CLTs IRC 4947(b)(3)(A) Making taxable expenditures IRC

52 Self-Dealing and Other Chapter 42 Excise Taxes (continued) Compliance (or lack of compliance) with these prohibited activities is self-reported in Part VI-B Exercise care in completing this portion of the return the trustee signs the return under penalty of perjury 52

53 Thank You Ted R. Batson, Jr., J.D., M.B.A., CPA, CFP Executive Vice President Renaissance 6100 W. 96 th St., Ste. 100 Indianapolis, IN ext

Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More

FOR LIVE PROGRAM ONLY Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 18, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 18, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More Navigating the New Reporting Requirements and Avoiding Compliance Errors WEDNESDAY, MAY 14, 2014, 1:00-2:50 pm

Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More Navigating the New Reporting Requirements and Avoiding Compliance Errors WEDNESDAY, MAY 14, 2014, 1:00-2:50 pm

IMPORTANT INFORMATION

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

IRC Section 734 Adjustments: Applying the 754 Election to Distributions of Partnership Property

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences

FOR LIVE PROGRAM ONLY Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Charitable Split-Interest Trusts and Form 5227

Charitable Split-Interest Trusts and Form 5227 Avoiding Compliance Pitfalls and Navigating Recent Regulatory Changes TUESDAY, SEPTEMBER 24, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program

Charitable Split-Interest Trusts and Form 5227 Avoiding Compliance Pitfalls and Navigating Recent Regulatory Changes TUESDAY, SEPTEMBER 24, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform

and Form 1041 Trust Deduction Rules Post-Tax Reform") New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

New Accounting Method Rules for Small Business Taxpayers Under IRC 448

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor

Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor") Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report

FOR LIVE PROGRAM ONLY Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report WEDNESDAY, NOVEMBER 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report WEDNESDAY, NOVEMBER 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities

FOR LIVE PROGRAM ONLY S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities TUESDAY, MAY 10, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities TUESDAY, MAY 10, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

Charitable Remainder and Pooled Income Trusts 541-B. Form 541-B C Side 1 ( )

") TAXABLE YEAR 2014 Name of trust Charitable Remainder and Pooled Income Trusts FEIN CALIFORNIA FORM 541-B Name of trustee(s) Date trust created (mm/dd/yyyy) Additional information (see instructions) Type

TAXABLE YEAR 2014 Name of trust Charitable Remainder and Pooled Income Trusts FEIN CALIFORNIA FORM 541-B Name of trustee(s) Date trust created (mm/dd/yyyy) Additional information (see instructions) Type

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Mastering Form 990 Schedule A: Protecting Public Charity Status, IRC 509 Public Support Test Calculations and Reporting

FOR LIVE PROGRAM ONLY Mastering Form 990 Schedule A: Protecting Public Charity Status, IRC 509 Public Support Test Calculations and Reporting TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY Mastering Form 990 Schedule A: Protecting Public Charity Status, IRC 509 Public Support Test Calculations and Reporting TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment THURSDAY, FEBRUARY 21, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment THURSDAY, FEBRUARY 21, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

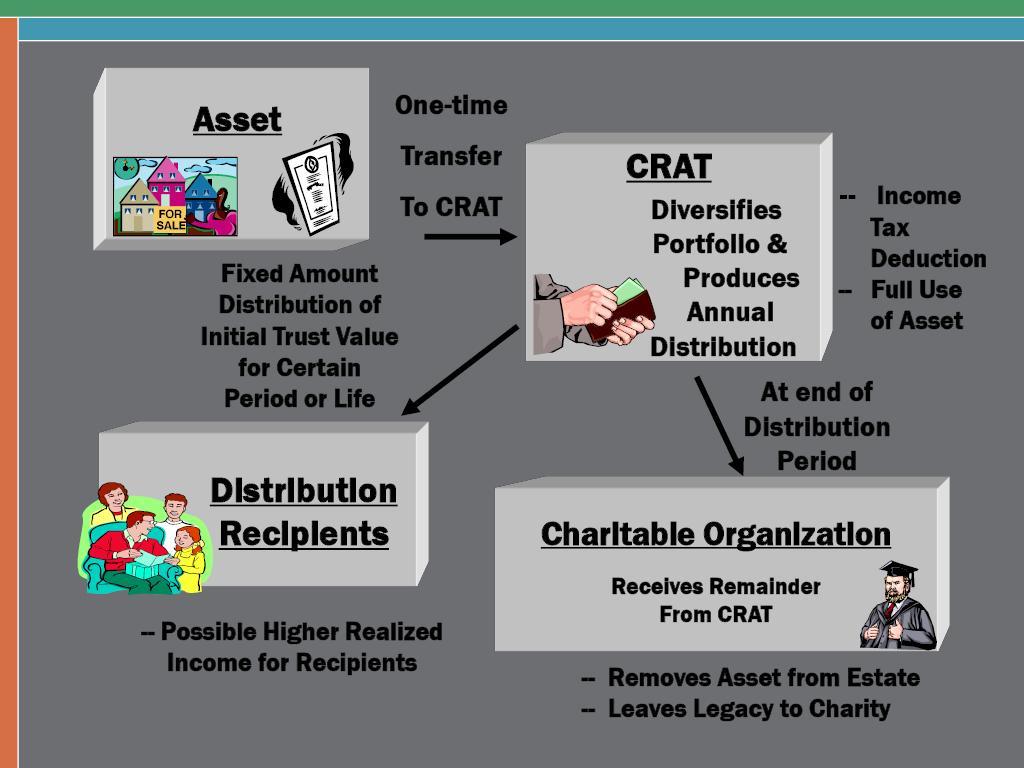

Four Tier Accounting for Charitable Remainder Trust. Richard C. Capasso, CPA, CFP, PFS

Four Tier Accounting for Charitable Remainder Trust Richard C. Capasso, CPA, CFP, PFS Charitable Remainder Trust Provide an option for dealing with appreciated property to philanthropic donors Trust is

Four Tier Accounting for Charitable Remainder Trust Richard C. Capasso, CPA, CFP, PFS Charitable Remainder Trust Provide an option for dealing with appreciated property to philanthropic donors Trust is

Tax Planning and Reporting for Partnership Equity Compensation Grants

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 23, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 23, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Presented by Richard D. Cirincione 677 Broadway Albany, NY Direct: Fax:

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance WEDNESDAY, SEPTEMBER 2, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance WEDNESDAY, SEPTEMBER 2, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II THURSDAY, OCTOBER 20, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II THURSDAY, OCTOBER 20, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Section 1291 Excess Distribution Calculations for PFIC Tax and Interest Reporting

Section 1291 Excess Distribution Calculations for PFIC Tax and Interest Reporting FOR LIVE PROGRAM ONLY TUESDAY, JUNE 19, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Section 1291 Excess Distribution Calculations for PFIC Tax and Interest Reporting FOR LIVE PROGRAM ONLY TUESDAY, JUNE 19, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance

Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance") Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption

(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption") New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption FOR LIVE PROGRAM ONLY TUESDAY, JULY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption FOR LIVE PROGRAM ONLY TUESDAY, JULY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

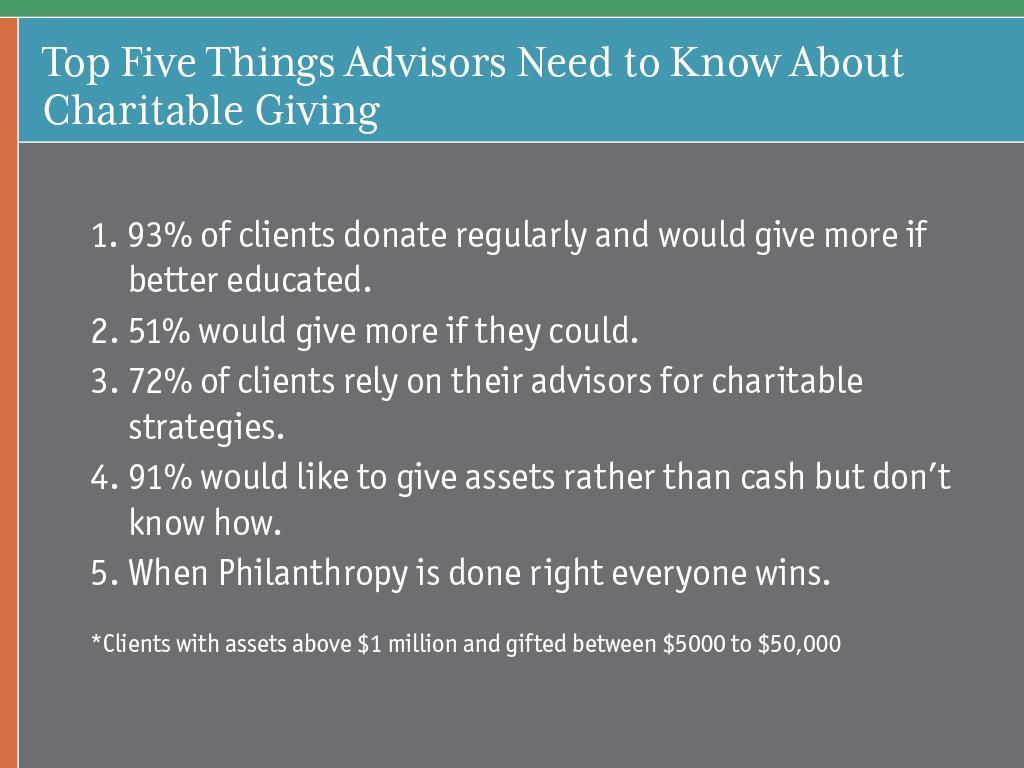

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

Mastering Form 5500 Schedule H: Avoiding Audit Triggers

FOR LIVE PROGRAM ONLY Mastering Form 5500 Schedule H: Avoiding Audit Triggers Financial Information Reporting Requirements, Identifying Valuation Challenges and Expanded Compliance Questions THURSDAY,

FOR LIVE PROGRAM ONLY Mastering Form 5500 Schedule H: Avoiding Audit Triggers Financial Information Reporting Requirements, Identifying Valuation Challenges and Expanded Compliance Questions THURSDAY,

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Tax Challenges for NPO Counsel: Excess Benefit Transactions for Executive Comp and Other Financial Dealings

Presenting a live 110-minute teleconference with interactive Q&A Tax Challenges for NPO Counsel: Excess Benefit Transactions for Executive Comp and Other Financial Dealings Identifying Prohibited Transactions

Presenting a live 110-minute teleconference with interactive Q&A Tax Challenges for NPO Counsel: Excess Benefit Transactions for Executive Comp and Other Financial Dealings Identifying Prohibited Transactions

Using Your Assets to Promote your Values. Lawrence M. Lehmann, JD, AEP, CAP Lehmann Norman & Marcus LC

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040 WEDNESDAY, JANUARY 18, 2017, 1:00-2:50 pm Eastern IMPORTANT

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040 WEDNESDAY, JANUARY 18, 2017, 1:00-2:50 pm Eastern IMPORTANT

Tax Allocation in Pass-Through Entities

Presenting a live 110-minute teleconference with interactive Q&A Tax Allocation in Pass-Through Entities Minimizing Tax Impact Through Strategic Allocation of Income, Gains, Losses and Liabilities THURSDAY,

Presenting a live 110-minute teleconference with interactive Q&A Tax Allocation in Pass-Through Entities Minimizing Tax Impact Through Strategic Allocation of Income, Gains, Losses and Liabilities THURSDAY,

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Form 8621 PFIC Reporting: Navigating the Highly Complex IRS Passive Foreign Investment Company Rules Determining Which Assets Require PFIC Reporting, Calculating Tax and Interest,

FOR LIVE PROGRAM ONLY Form 8621 PFIC Reporting: Navigating the Highly Complex IRS Passive Foreign Investment Company Rules Determining Which Assets Require PFIC Reporting, Calculating Tax and Interest,

Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis

Presenting a live 90-minute webinar with interactive Q&A Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis TUESDAY, JUNE 28, 2016 1pm Eastern 12pm

Presenting a live 90-minute webinar with interactive Q&A Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis TUESDAY, JUNE 28, 2016 1pm Eastern 12pm

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions

And Subpart F Income Inclusions") Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Calculating Trust Fiduciary Accounting Income: Interpreting Operating Documents, Applying UPIA and State Law

Calculating Trust Fiduciary Accounting Income: Interpreting Operating Documents, Applying UPIA and State Law FOR LIVE PROGRAM ONLY OCTOBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Calculating Trust Fiduciary Accounting Income: Interpreting Operating Documents, Applying UPIA and State Law FOR LIVE PROGRAM ONLY OCTOBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 29, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 29, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules

FOR LIVE PROGRAM ONLY Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules THURSDAY, JANUARY 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules THURSDAY, JANUARY 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Pointers in Selecting Assets to Fund Charitable Trusts

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

New FASB ASU Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs

New FASB ASU 2014-09 Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

New FASB ASU 2014-09 Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Attendees seeking CPE credit must listen to the audio over the telephone.

Presenting a live 110 minute teleconference with interactive Q&A New 3.8% Net Investment Income Tax: Planning for Closely Held Companies Navigating New Medicare Tax, Self Employment l Tax, and Capital

Presenting a live 110 minute teleconference with interactive Q&A New 3.8% Net Investment Income Tax: Planning for Closely Held Companies Navigating New Medicare Tax, Self Employment l Tax, and Capital

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Brian E. Hammell, Esq., Sullivan & Worcester, Boston

Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax,

Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax,

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Stupid Charitable Tricks:

Stupid Charitable Tricks: Charitable Planning Mistakes I Have Seen Ramsay Slugg November, 2017 Disclosure (use this if the next slide N/A) IMPORTANT: This presentation is designed to provide general information

Stupid Charitable Tricks: Charitable Planning Mistakes I Have Seen Ramsay Slugg November, 2017 Disclosure (use this if the next slide N/A) IMPORTANT: This presentation is designed to provide general information

New FASB ASU on Not-For-Profit Financial Reporting and Disclosures: Are You Ready?

FOR LIVE PROGRAM ONLY New FASB ASU 2016-14 on Not-For-Profit Financial Reporting and Disclosures: Are You Ready? TUESDAY, MARCH 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY New FASB ASU 2016-14 on Not-For-Profit Financial Reporting and Disclosures: Are You Ready? TUESDAY, MARCH 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

State Income Tax Treatment of Nonresident Trusts: Compliance Challenges and Planning Opportunities

State Income Tax Treatment of Nonresident Trusts: Compliance Challenges and Planning Opportunities FOR LIVE PROGRAM ONLY TUESDAY, JULY 24, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

State Income Tax Treatment of Nonresident Trusts: Compliance Challenges and Planning Opportunities FOR LIVE PROGRAM ONLY TUESDAY, JULY 24, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

State Sales Tax on Drop Shipments: Navigating Various States' Rules on Registrations and Exemptions

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Real Estate Transactions With REITs: Selling, Leasing or Lending to a REIT

Presenting a 90-Minute Encore Presentation of the Webinar with Live, Interactive Q&A Real Estate Transactions With REITs: Selling, Leasing or Lending to a REIT Navigating Unique Organizational, Operational

Presenting a 90-Minute Encore Presentation of the Webinar with Live, Interactive Q&A Real Estate Transactions With REITs: Selling, Leasing or Lending to a REIT Navigating Unique Organizational, Operational

Mastering the Rules of S Corporation Shareholder-Employee Compensation

FOR LIVE PROGRAM ONLY Mastering the Rules of S Corporation Shareholder-Employee Compensation WEDNESDAY, JANUARY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY Mastering the Rules of S Corporation Shareholder-Employee Compensation WEDNESDAY, JANUARY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1040NR for Foreign Trusts: Income Tax Reporting for Foreign Non-Grantor Trusts

FOR LIVE PROGRAM ONLY Form 1040NR for Foreign Trusts: Income Tax Reporting for Foreign Non-Grantor Trusts WEDNESDAY, JULY 19, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY Form 1040NR for Foreign Trusts: Income Tax Reporting for Foreign Non-Grantor Trusts WEDNESDAY, JULY 19, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

U.K.-Based Retirement Accounts for U.S. Taxpayers: Mastering Reporting, Maximizing Planning Opportunities Utilizing Treaty Provisions to Achieve Optimal Tax Results While Complying With Foreign Reporting

U.K.-Based Retirement Accounts for U.S. Taxpayers: Mastering Reporting, Maximizing Planning Opportunities Utilizing Treaty Provisions to Achieve Optimal Tax Results While Complying With Foreign Reporting

Mastering Tax Complexities in the Sale of Partnership and LLC Interests

Mastering Tax Complexities in the Sale of Partnership and LLC Interests WEDNESDAY, JUNE 17, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

Mastering Tax Complexities in the Sale of Partnership and LLC Interests WEDNESDAY, JUNE 17, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

Executive Compensation: Tax and Other Considerations for Restricted Stock Awards

Presenting a live 90-minute webinar with interactive Q&A Executive Compensation: Tax and Other Considerations for Restricted Stock Awards Strategies for Navigating Substantial Risk of Forfeiture Analysis,

Presenting a live 90-minute webinar with interactive Q&A Executive Compensation: Tax and Other Considerations for Restricted Stock Awards Strategies for Navigating Substantial Risk of Forfeiture Analysis,

Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law

Presenting a live 90-minute webinar with interactive Q&A Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law WEDNESDAY, FEBRUARY 7, 2018 1pm Eastern 12pm Central 11am Mountain

Presenting a live 90-minute webinar with interactive Q&A Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law WEDNESDAY, FEBRUARY 7, 2018 1pm Eastern 12pm Central 11am Mountain

IRC 645 Elections for Qualified Revocable Trusts: Mastering the DNI Separate Share Calculation Rules

FOR LIVE PROGRAM ONLY IRC 645 Elections for Qualified Revocable Trusts: Mastering the DNI Separate Share Calculation Rules THURSDAY, JUNE 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY IRC 645 Elections for Qualified Revocable Trusts: Mastering the DNI Separate Share Calculation Rules THURSDAY, JUNE 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Mastering U.S. Permanent Establishment Tax Under New OECD Guidance vs. General Tax Treaty Approach Navigating Income Attribution Rules in the U.S. Model Income Tax Convention and Recently Signed Tax Treaties

Mastering U.S. Permanent Establishment Tax Under New OECD Guidance vs. General Tax Treaty Approach Navigating Income Attribution Rules in the U.S. Model Income Tax Convention and Recently Signed Tax Treaties

Mastering Form 8937 and Section 6045B:

Presenting a live 110 minute teleconference with interactive Q&A Mastering Form 8937 and Section 6045B: An Ongoing Obligation Complying With Reporting Requirements Arising From Activities Affecting Tax

Presenting a live 110 minute teleconference with interactive Q&A Mastering Form 8937 and Section 6045B: An Ongoing Obligation Complying With Reporting Requirements Arising From Activities Affecting Tax

Presenting a live 110-minute teleconference with interactive Q&A

Presenting a live 110-minute teleconference with interactive Q&A Valuation Challenges With $10 Million-and-Under Businesses Avoiding Mistakes With Built-In Gains and Taxes, Misuse of Market Data and Other

Presenting a live 110-minute teleconference with interactive Q&A Valuation Challenges With $10 Million-and-Under Businesses Avoiding Mistakes With Built-In Gains and Taxes, Misuse of Market Data and Other

Private Investment Funds and Tax Reform

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Form 990-PF: Meeting IRS Demands for Fiscal, Grant and Other Data From Private Foundations

Form 990-PF: Meeting IRS Demands for Fiscal, Grant and Other Data From Private Foundations THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit

Form 990-PF: Meeting IRS Demands for Fiscal, Grant and Other Data From Private Foundations THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit

New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units

FOR LIVE PROGRAM ONLY New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units THURSDAY, NOVEMBER 30, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units THURSDAY, NOVEMBER 30, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Split-interest trusts make distributions to both

Data Release Split-interest trusts make distributions to both charitable and noncharitable beneficiaries. While the Internal Revenue Service does not classify split-interest trusts as tax-exempt entities,

Data Release Split-interest trusts make distributions to both charitable and noncharitable beneficiaries. While the Internal Revenue Service does not classify split-interest trusts as tax-exempt entities,

Presenting a 90-minute encore presentation featuring live Q&A. Today s faculty features:

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

401k Annual Audits: Anticipating Serious and Costly Errors, Evaluating Alternative Solutions

FOR LIVE PROGRAM ONLY 401k Annual Audits: Anticipating Serious and Costly Errors, Evaluating Alternative Solutions TUESDAY, APRIL 11, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY 401k Annual Audits: Anticipating Serious and Costly Errors, Evaluating Alternative Solutions TUESDAY, APRIL 11, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM