Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

|

|

|

- Gerald Singleton

- 6 years ago

- Views:

Transcription

1 Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More Navigating the New Reporting Requirements and Avoiding Compliance Errors WEDNESDAY, MAY 14, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you must: Participate in the program on your own computer connection and phone line (no sharing) if you need to register additional people, please call customer service at x10 (or x10). Strafford accepts American Express, Visa, MasterCard, Discover. Respond to verification codes presented throughout the seminar. If you have not printed out the Official Record of Attendance, please print it now. (see Handouts tab in Conference Materials box on left-hand side of your computer screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found on the Official Record of Attendance form. Complete and submit the Official Record of Attendance for Continuing Education Credits, which is available on the program page along with the presentation materials. Instructions on how to return it are included on the form. To earn full credit, you must remain on the line for the entire program. WHOM TO CONTACT For Additional Registrations: -Call Strafford Customer Service x10 (or x10) For Assistance During the Program: - On the web, use the chat box at the bottom left of the screen - On the phone, press *0 ( star zero) If you get disconnected during the program, you can simply call or log in using your original instructions and PIN.

2 Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial and enter your PIN when prompted. Otherwise, please send us a chat or sound@straffordpub.com immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

3 Program Materials FOR LIVE EVENT ONLY If you have not printed the conference materials for this program, please complete the following steps: Click on the ^ symbol next to Conference Materials in the middle of the lefthand column on your screen. Click on the tab labeled Handouts that appears, and there you will see a PDF of the slides and the Official Record of Attendance for today's program. Double-click on the PDF and a separate page will open. Print the slides by clicking on the printer icon.

4 Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More May 14, 2014 Ted R. Batson, Jr., Renaissance Joe Carter, Oklahoma City Community Foundation Donna J. Jackson, Attorney at Law,

5 5

6 6

7 7

8 8

9 9

10 10

11 11

12 12

13 13

14 14

15 15

16 16

17 17

18 18

19 19

20 20

21 21

22 22

23 23

24 24

25 25

26 26

27 27

28 28

29 Slide Intentionally Left Blank

30 Ted R. Batson, Jr., J.D., M.B.A., CPA, CFP, Renaissance Administration LLC TAX CONSEQUENCES AND RECENT DEVELOPMENTS

31 Topics Covered Income and transfer tax considerations: Charitable remainder trust (CRT) Charitable lead trust (CLT) Form 5227 presentation Compliance reminders Applicable Private foundation excise taxes Public inspection rules Unrelated business income (UBI) Hedge funds Debt financed income Advantages & planning 3.8% Medicare tax issues 31

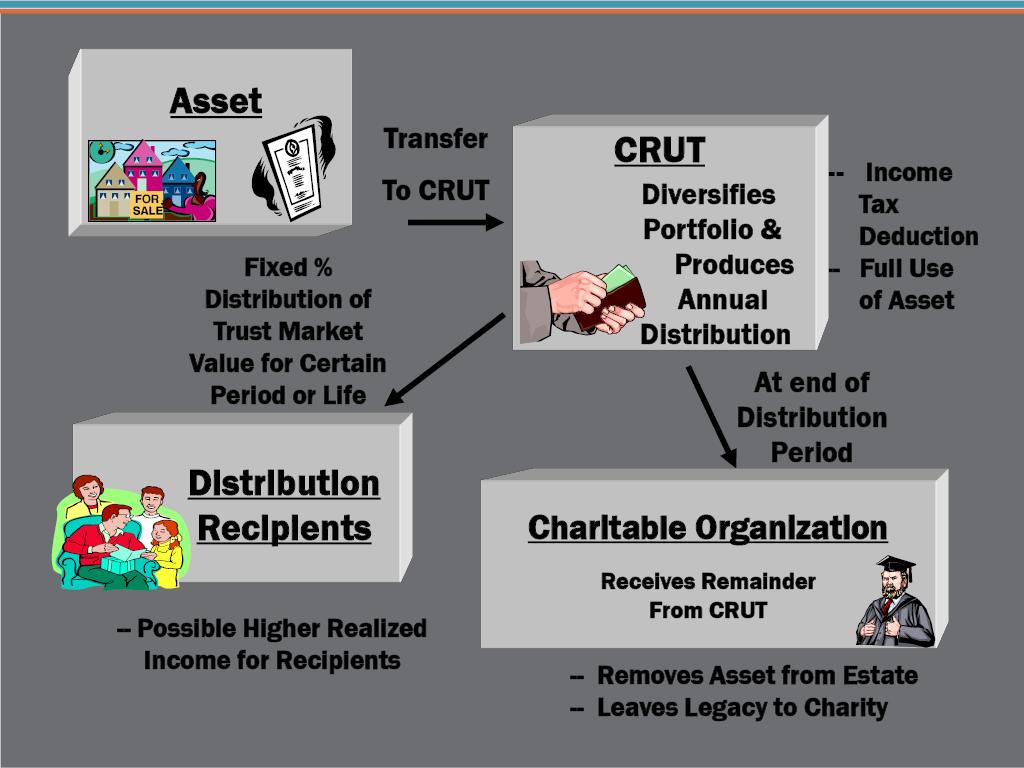

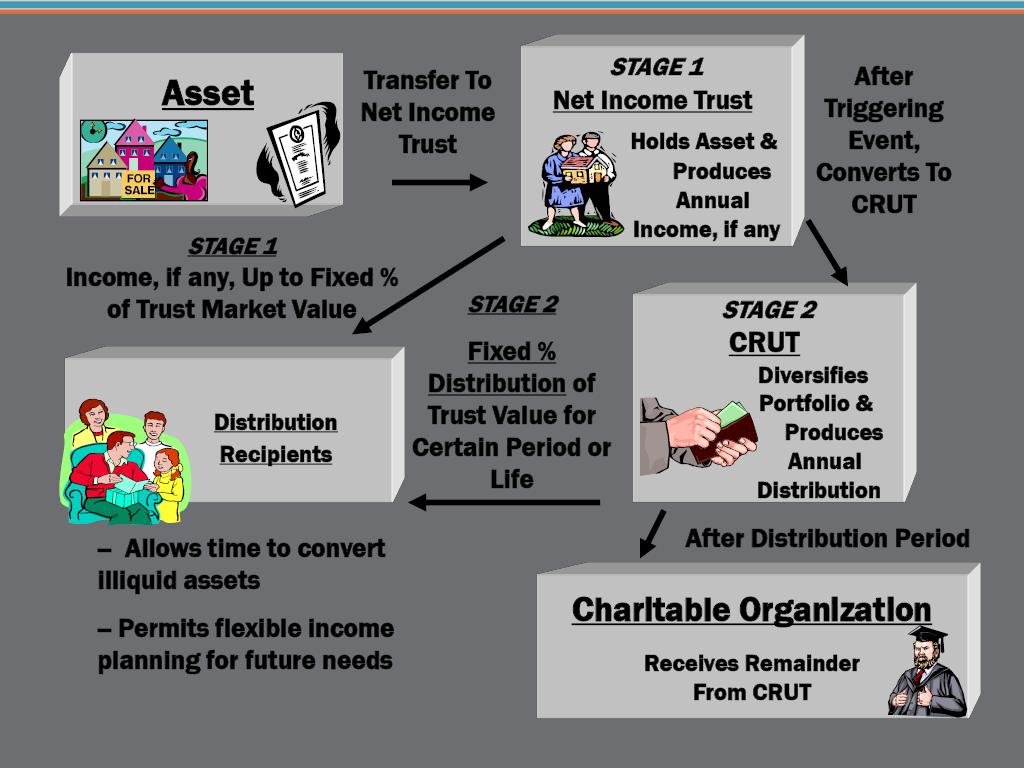

32 Charitable Remainder Trust (CRT) Donor (Income Beneficiary) Donor receives an immediate income tax deduction for present value of the remainder interest (must be at least 10% of the value of the assets originally contributed) Transfer of highlyappreciated assets Annual (or more frequent) payments for life (or a term of years) CRT Public Charity (Remainder Beneficiary) At the donor s death (or at the end of the trust term), the charity receives the residual assets held in the trust 32

33 Income Tax Consequences - CRT Formation: A donor receives no charitable income tax deduction for a gift of a remainder interest to charity unless the trust is a CRT described in Section 664. Intervivos CRT - The grantor is entitled to an immediate income tax deduction in the amount of the present value of the remainder interest passing to charity. Testamentary CRT - The estate of the decedent whose will created a CRT is entitled to an estate tax deduction for the present value of the remainder interest passing to charity. 33

34 Charitable Contribution Deduction - CRT CRAT - At the time a CRAT is formed, the donor may deduct the fair market value of the property placed in trust less the present value of the annuity as a charitable contribution on his or her individual tax return and for estate and gift taxes Additional contributions cannot be made to a CRAT because the annuity amount is based on the value of the assets only valued as of creation. The governing instrument of the CRAT must prohibit additional contributions. CRUT - the deduction is the present value of the remainder interest Additional contributions can be made to a CRUT as long as the governing instrument provides a formula upon which to base the unitrust amount, which takes into account the additional contribution. 34

35 Charitable Contribution Deduction The value of the donor's federal income tax deduction is a function of: 1. The type of charitable remainderman; 2. The kind of property contributed to the CRT; and 3. Whether, at the end of the non-charitable term, the assets are: a) Distributed outright to the charitable remainderman; or b) Held in trust for the benefit of the charitable remainderman 35

36 Type Of Charitable Remainderman A public charity including churches, educational institutions, hospitals and medical institutions University endowment funds, governmental units, publicly supported organizations under Sections 170(c)(2) & 509(a)(2) (i.e., museums, drama companies, ballet companies, etc.) Supporting organizations under Section 509(a)(3) Private operating foundations Two types of non-operating private foundations: Distributing foundations Foundations that maintain a common fund 36

37 Impact Of Kind Of Property Contributed - CRT The donor gets a federal income tax deduction for the fair market value of the remainder interest passing to charity subject to the following percentage limitations. Gift of cash and non-appreciated property Passes outright to public charity at end of non-charitable term In the year of the gift, the donor's fair market value charitable income tax deduction is limited to 50% of his/her adjusted gross income (AGI) with a five-year carryforward. Held in trust for the benefit of public charity at end of non-charitable term In the year of the gift, the donor's fair market value charitable income tax deduction is limited to 30% of his/her AGI with a five-year carryforward. 37

38 Impact Of Kind Of Property Contributed CRT (Cont.) Gift of appreciated property Passes outright to public charity at end of non-charitable term In the year of the gift, the donor's fair market value charitable income tax deduction is limited to 30% of his/her AGI with a five-year carryforward. Held in trust for the benefit of public charity at end of non-charitable term In the year of the gift, the donor's fair market value charitable income tax deduction is limited to 20% of his/her AGI with a five-year carryforward 38

39 Income Tax Consequences - CRT Annually annuity recipient The distributions to the recipient of the annuity amount or unitrust amount are includable in the recipient's gross income reportable on Schedule K-1 Tiered structure - the highest-taxed items are deemed to be distributed first in the following order: Ordinary income to the extent of the CRT's ordinary income for that year and undistributed ordinary income from prior years Capital gains to the extent of the CRT's capital gains for that year and undistributed capital gains from prior years (short term gains first) Current and undistributed tax exempt income Corpus non-taxable 39

40 Income Tax Consequences CRT (Cont.) Annually annuity recipient (Cont): Net income make-up charitable remainder unitrust (NIMCRUT) The unitrust payment from a NIMCRUT is based on a fixed percentage of the value of the trust assets at the beginning of the year, but is limited to the trust's annual fiduciary accounting income. If the trust income is less than the payment based on the fair market value of trust assets, the trust may increase payments to the beneficiary in subsequent years to compensate for a prior deficiency. But only if the trust s fiduciary accounting income in that later year exceed the fixed percentage amount Tiered distribution rules still apply 40

41 Income Tax Consequences CRT (Cont.) Annually annuity recipient (Cont): CRAT and the fixed-percentage CRUT: The trustee may be forced to make a distribution in kind if the income is insufficient to satisfy the annuity amount of the CRAT or the unitrust amount of the fixed percentage CRUT A distribution in kind is deemed to be a sale of the property so distributed causing the recipient to recognize capital gain on the in-kind property distributed. For example, if a donor funds a fixed percentage CRUT with closely held C stock and then the stock cannot be sold after such funding, the trustee will be obligated to distribute enough stock to the donor to meet the annual fixed percentage and the CRUT will realize the capital gain on that stock even though it was not sold; that capital gain will be passed through to the recipient under the income tax characterization rules above causing the recipient to recognize gain. 41

42 Income Tax Consequences CRT (Cont.) Annually annuity recipient (Cont): CRAT and the fixed-percentage CRUT: If NIMCRUT, the trustee will not be forced to make a distribution in kind. Rather, the trustee can satisfy the unitrust amount based on the income earned by the CRUT. Obviously, if a non-income earning asset, such as real estate, is used to fund a CRT, it is best to choose a CRUT with the lesser of income feature. 42

43 Income Tax Consequences CRT (Cont.) Annually trust: A CRT is a tax exempt entity; therefore, the CRT pays no income tax on its income unless it has unrelated business taxable income (UBTI). A CRT is not taxed on any retained gain it realizes upon selling appreciated property, whether donated by the grantor or appreciation occurring after the donation. 43

44 Transfer Tax Consequences - CRT The retention of a right to revoke by the donor results in the CRT assets being includable in the donor's estate at his/her death The gift tax consequences is based on the recipient of the annuity amount or unitrust amount: Just the donor: The donor gets a charitable gift tax deduction for the value of the remainder interest passing to charity. The donor and spouse only: The donor has made a gift to his/her spouse of the value of the annuity amount or unitrust amount going to his/her spouse but such gift is shielded by the marital deduction. The donor also gets a charitable gift tax deduction for the value of the remainder interest passing to charity 44

45 Transfer Tax Consequences CRT (Cont.) The gift tax consequences is based on the recipient of the annuity amount or unitrust amount (Cont): Spouse and others (e.g. the donor, then spouse and then children) - The donor has made a gift to his/her spouse that does not qualify for the marital deduction. Further, the donor has made a gift to his/her children. However, the donor can retain the right to revoke by will his/her spouse and children's rights to the annuity amount or unitrust amount without disqualifying the trust as a CRT and if so, the gifts are incomplete. Someone other than the donor's spouse: The donor has made a gift to that person in the amount of the present value of the annuity amount or unitrust amount unless the donor retains the right to revoke by will that person's right to the annuity amount or unitrust amount. 45

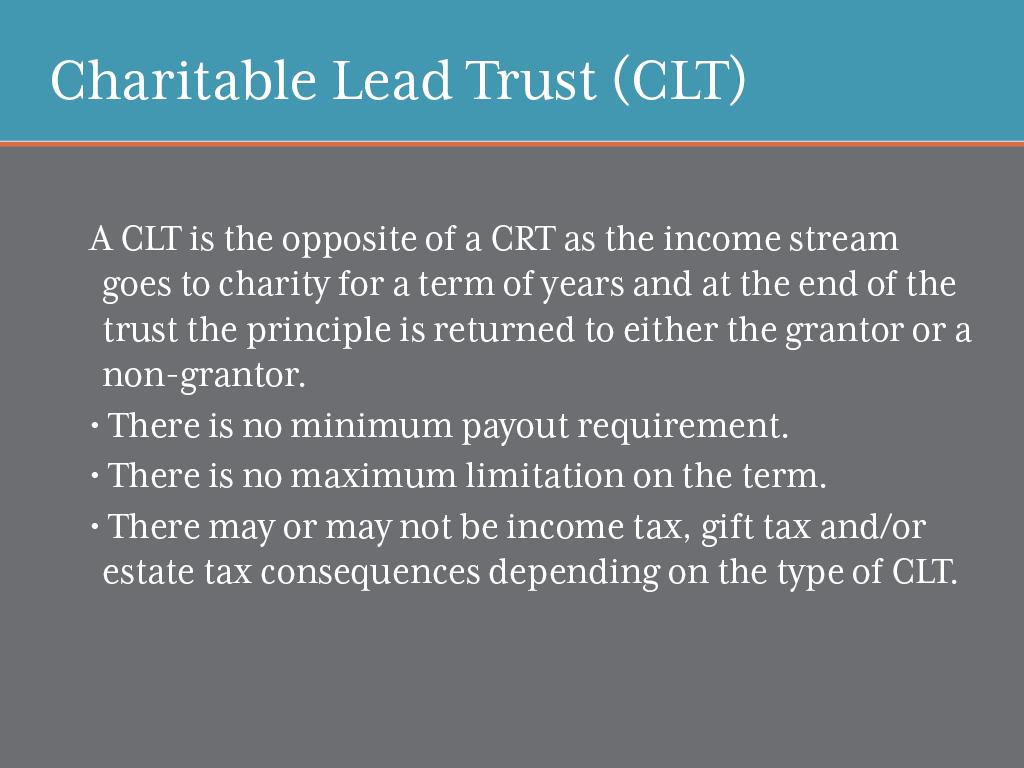

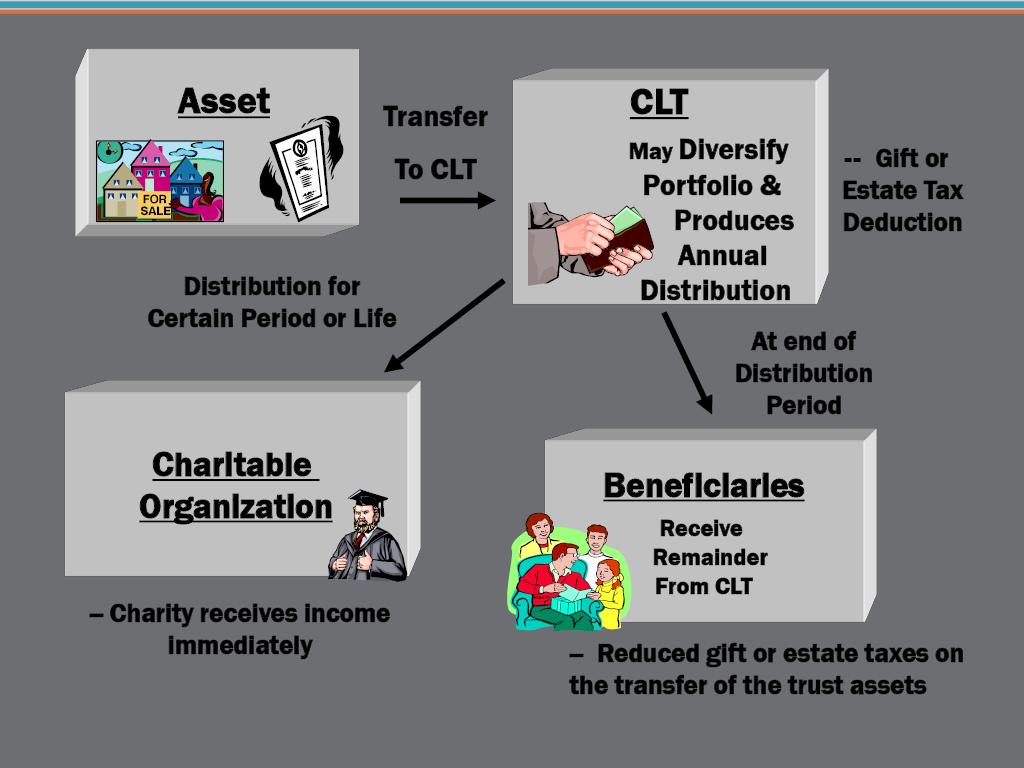

46 Donor (Income Beneficiary) Charitable Lead Trust (CLT) Transfer of cash, stock and/or other assets At the donor s death (or at the end of the trust term), the remainder beneficiaries receive the residual assets held in the trust CLT Donor s Children 46 (Remainder Beneficiary) Annual (or more frequent) payments for life (or a term of years) Public Charity (Income Beneficiary) 46

47 Types Of CLTs Grantor or non-grantor trust depending on whether the grantor retains the power to control beneficial enjoyment, the power to revoke the trust, or any of the attributes described in IRC sections A retained reversionary interest triggers grantor trust treatment if the reversion is valued at more than 5% of the trust property's fair market value at the time the trust is formed 47

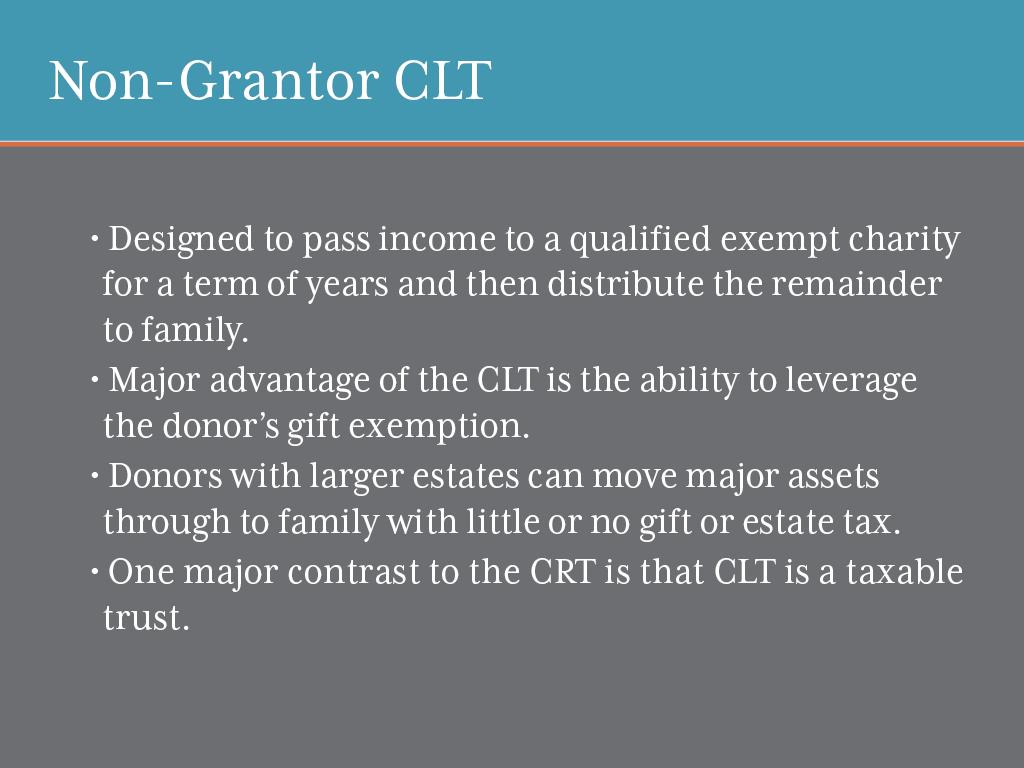

48 Income And Transfer Tax Consequences - CLT Income tax: Formation Annually Transfer tax: Inter Vivos - Gift tax Testamentary - Estate Grantor Grantor can deduct the present value of the income interest, subject to charitable contribution limits Grantor will include trust income on individual income tax return, but no deduction for charitable contributions made by the trust Grantor deducts the present value of the income interest at the time of formation. No deduction is allowed as the payments are made to the charity by the trust. Not applicable No deduction Nongrantor Trust recognizes income offset by the annuity or unitrust payment each year, but cannot deduct any excess contribution Grantor deducts the present value of the income interest at the time of formation. No deduction is allowed as the payments are made to the charity by the trust. Estate deducts the present value of the income interest at the time of formation. The trust cannot deduct charitable contributions as they are made. 48

49 Form 5227 Compliance Reminders Due date April 15 extended with Form 8868 (not 7004) for up to six months three months at a time (i.e. until July 15 and then October 15) All filed with IRS Center in Ogden, UT Copy of trust instrument must be attached to initial return Balance sheet (Part IV) all trusts must complete columns a and b based on the accounting method the trust uses in keeping its books and records Column c only applies to CRUTs and should be completed as of the valuation date valuation date and method must be used each year Short tax years the annuity or unitrust amount for short tax year is computed by multiplying the full year annuity or unitrust amount by the number of days in the trust s tax year divided by 365 or 366 for leap years 49

50 Applicable Private Foundation Excise Taxes Since some but not all of the unexpired interest are charitable the following private foundation excise taxes also apply to CRTs and CLTs: Self-dealing (Section 4941) Excess business holdings (Section 4943) Investments that jeopardize charitable purposes (Section 4944) Taxable expenditures (Section 4945) and political expenditures (Section 4955) 50

51 Self-Dealing The trust must not be involved in self-dealing. This includes any of the following direct or indirect transactions between the trusts and a disqualified person: Sale, exchange, or leasing of property; Lending of money or extension of credit; Furnishing of goods, services, or facilities, unless such goods, services, or facilities are made available to the general public on at least as favorable a basis as they are made to the disqualified person, Payment of compensation (or payment or reimbursement of expenses), unless it is for personal services and such compensation is reasonable and necessary to carry out the exempt purpose and is not excessive; Transfer to, or use by or for the benefit of, a disqualified person of the income or assets of the trust 51

52 Disqualified Person A disqualified person is: A substantial contributor to the trust, Persons owning more than 20% of an entity that is a substantial contributor to the trust A foundation manager or trustee, A family member of a substantial contributor, foundation manager, or trustee (i.e. spouse, ancestors, descendants, and spouses of descendants), or Certain businesses or trusts in which a substantial contributor, foundation manager, or trustee together with all his or her disqualified relatives has a greater than 35% interest A substantial contributor is an individual, trust, estate, corporation, or partnership who contributes an aggregate amount in excess of $5,000 to the trust, if his or her total contributions are more than 2% of the total contributions received 52

53 Example Of Potential Self-Dealing Reimbursement to disqualified persons for travel expenses Could cause the trust and the disqualified person to be potentially liable for penalty taxes for self-dealing, for making non-charitable expenditures, or possibly both. Such reimbursement of expenses will not be subject to the excise tax if the expenses are reasonable and necessary to carrying out the exempt purposes of the trust and are not excessive. The Code does not explain what is "reasonable and necessary follow guidance under business expense deductions rules include travel fares, meals, lodging, and expenses incident to travel. Travel expenses are not reasonable and necessary if the trip is primarily personal in nature. An amount spent on director's services will not be deemed "excessive" if it is only such as would be paid "for like services by like enterprises under like circumstances. 53

54 Example Of Potential Self-Dealing (Cont.) Attendance by grantor/trustee at fundraising event for one of trust s charitable beneficiaries where donor benefits are received. The grantor/trustee who participated in the event should reimburse the trust for the value assigned to the benefits received so as to minimize appearance of self dealing. If the trustee reimbursement comes after year end then reflect as an accounts receivable on the balance sheet 54

55 Consequences To Self-Dealing Any disqualified person who engages in an act of self-dealing is assessed an excise tax of 10% of that amount involved in the transaction for each year that the transaction is uncorrected. A trustee who knows that the act is prohibited but approves it may also be subject to a tax of 5% of the amount involved (up to $20,000 for each such act) for each year that the transaction is uncorrected. If the transaction is not timely corrected and the 5% was initially assessed, the disqualified person is subject to being assessed an additional tax of 200% of the amount involved. Any trustee who does not correct the transaction may also be subject to an additional assessment of 50% of the amount involved (up to $20,000 for each such act.) 55

56 Excess Business Holdings Section 4943 Section 4943 imposes an excise tax on the value of the "excess business holdings" of the trust. A trust created after May 26, 1969 has excess business holdings to the extent that it, together with all disqualified persons, owns in the aggregate more than 20% of the voting stock of an incorporated business enterprise (or corresponding interests in non-incorporated business enterprises). In general, where a trust acquires excess business holdings by gift or bequest, the trust has five years from the date it acquires such holdings to dispose of them 56

57 Jeopardizing Investments Section 4944 Section 4944 imposes an excise tax on a trust (and under some circumstances trustees) for investing any amount in such a manner as to jeopardize the carrying out of its exempt purposes. The imposition of an excise tax on "jeopardy" investments is intended to assure that the trustees adopt a "prudent person" approach toward the investment of trust assets. The test is imposed on the portfolio as a whole and not on individual investment choices 57

58 Exceptions To Sections 4943 And 4944 The excess business holdings provisions of Section 4943 and the "jeopardy investment" provisions of Section 4944 do not apply to a splitinterest trust if either: All of the income interests (and none of the remainder interests) (i.e., a CLT) of the trust are devoted solely to charitable purposes and all amounts in trust for which a charitable deduction was allowed have an aggregate value of not more than 60% of the aggregate fair market value of all amounts in trust; or A charitable deduction was allowed for amounts payable under the terms of the trust to every remainder beneficiary, but not to any income beneficiary, as is the case with the majority of CRTs. 58

59 Public Inspection Requirements Form 5227 is open to public inspection, except for information related to noncharitable trust beneficiaries, which is disclosed on Schedule A, which is not open to public inspection. To inspect a return, the petitioner must submit a written request to the IRS that must include the name of the trust, the trustee s address, the type of return and the year for which the return was filed. 59

60 Slide Intentionally Left Blank

61 Unrelated Business Income (UBI) Prior To 2006 The CRT s tax exempt status would be suspended for any year that the CRT generated UBTI forcing the trust to pay tax on the entire amount of income for that year. The CRT would be taxed as a complex trust with an allowable deduction for amounts required to be distributed to the beneficiary. Any remaining income would be subject to income tax at the appropriate trust tax rates. 61

62 UBI After 2006 The Tax Relief and Health Care Act of 2006 (the 2006 Act ) changed the income tax rules on CRTs for any year in which the CRT incurs UBTI. No longer is the entire trust income subject to tax. Rather, an excise tax is imposed equal to 100% of the amount of the UBTI incurred by the CRT. The UBTI is considered income of the trust for purposes of determining the character of the distributions made to CRT beneficiaries, without a reduction of such income for the excise taxes paid by the CRT. Example: CRT with $4.5M of stocks & bonds and $500K in hedge funds. The investment return after deduction for the amounts paid to the beneficiary is a total of $240,000 of which $5,000 is UBTI. The CRT owes an excise tax of $5,000. Prior to 2006, the CRT tax obligation could have been as high as $84K. 62

63 Are Hedge Funds Appropriate For CRTs? A prudent fiduciary of a CRT should consider the following factors before adding hedge funds to the trust s investment portfolio: How much UBTI is present? Percentage of hedge fund return generated in the form of ordinary income an investment mix that promises to distribute a heavy annual dose of ordinary income or short term capital gain become less attractive than one which promises a lower tax cost to the non-charitable recipient Other investment considerations: Liquidity needs Risk of downside volatility Tolerance for fees and expenses Offshore fund reporting requirements 63

64 UBI Debt-Financed Income Unrelated business taxable income includes income from debt-financed property. A trust has debt-financed income it acquires realty subject to a mortgage. The trust will not have unrelated business taxable income if for a period of 10 years following the gift: The trust does not assume the debt or Meets all the following requirements: 1. The debt was placed on the property more than five years before the date of the gift; 2. The property was held by the donor for more than five years before making the gift; and 3. The CRT does not assume the debt. See PLR PLR

65 Advantages Of A CRT Non-recognition of capital gains A donor can contribute highly appreciated property to a CRT and benefit from the appreciated value of the asset because the donor's unitrust amount from a CRUT will be greater due to such assets high value not reduced by income tax on the appreciation. The donor benefits from the appreciation and at the same time the donor avoids immediate payment of the tax from the appreciation. The key is to make sure that as of the date of the funding (not just creation) of the CRT that there is no legal obligation to sell such asset. If, when the trust receives the asset, the trustee is subject to an obligation to sell, the IRS will ignore the gift to the CRT and treat the transaction as if the donor sold the asset. The donor then gets the worst of both worldspayment of tax and loss of the asset. 65

66 Advantages Of A CRT (Cont.) Growth of assets in a tax-exempt entity: Since a CRT is a tax-exempt entity, the value of the assets in the CRT can grow at a faster rate because gain realized on the sale of assets of the CRT is not recognized for income tax purposes in the CRT. The recipient of the unitrust amount from a CRUT gets the benefit from such growth since the fixed percentage is applied to a larger capital base. If family members are concerned that their inheritance will be reduced, the donor may use the tax savings created by the charitable contribution deduction to buy life insurance. This plan reduces the client's taxable estate and provides a liquid inheritance for heirs. 66

67 Advantages Of A CLT CLTs are attractive for clients with ample income seeking to transfer assets at minimal estate and gift taxes. By prolonging the payment period to the charitable beneficiary, the present value of the remainder interest is decreased and the value of the gift is reduced. In deciding whether to use a CLAT or CLUT, consider the donor's goals. If the donor seeks to maximize the payment that the non-charitable beneficiary will receive at the trust termination, a CLAT is preferable if the trust assets are expected to significantly appreciate in value. A CLAT also favors the remainderman if the amount paid to the charitable beneficiary is less than the trust's annual income, since the excess accumulates for the benefit of the non-charitable beneficiary. 67

68 Advantages Of A CLT (Cont.) A CLAT provides a fixed distribution, or annuity, to one or more charities in each year of the trust. Distributions can be the same each year or can increase annually at a rate established when the trust is put in place. Starting with a small annual payment but increasing the amount over the course of the trust may result in assets of greater value passing to the noncharitable beneficiary. For instance, a $1 million CLAT providing steady payments of $108,000 to charity for 10 years would result in $369,000 passing to the non-charitable beneficiary if it earned 6% per year. If, however, that $1 million CLAT started with an initial payment of $33,000, increasing by 25% each year for 10 years, $476,000 would pass to the non-charitable beneficiary. In both cases, the taxable value of the gift to the non-charitable beneficiary would be zero. 68

69 Advantages Of The Unitrust Appreciation in the value of trust assets causes unitrust payments to increase, maximizing the payment to the charity in a CLUT or to the non-charitable beneficiary in a CRUT. Alternatively, if trust assets in a unitrust decline in value, the noncharitable life tenant will receive a reduced annuity payment. The IRS has allowed early termination of CRUTs when the donor is dissatisfied with the annual return or needs access to the corpus. To avoid repayment of the tax benefits from the initial charitable contribution, the charity must receive the present value of its proportionate interest. Distributions made to the non-charitable beneficiary are taxed as longterm capital gains. NOTE: The annual valuation requirements for unitrusts increase administrative costs over annuities. 69

70 Recent Increase In Use Of CLTs The IRS discount rate is used to determine the assumed rate of return for assets contributed to a CLAT and affects the calculation of the lead payments (that is, how much must be paid to charities in order to zero out or eliminate the taxable gift component). When the discount rate is low, the annual payout to charity can be reduced. A trust funded with $1 million when the discount rate is 6% would need to pay the charitable recipient almost $136,000 per year for 10 years in order to have that stream of payments have a present value of $1 million. If, however, the discount rate is 1.4% (as it was in March 2012), the charitable recipient would need to be paid only $108,000 per year for the same result. That means that in today s environment, if this trust had an annualized return in excess of only 1.4%, it would not only be able to satisfy the annuity payment to charity but also would have funds remaining at the end of 10 years for the non-charitable beneficiaries. 70

71 Recent Increase In Use Of CLTs (Cont.) Low initial asset values might grow at a higher than expected rate, delivering more to your beneficiaries without increasing potential tax liability There is an expectation that the values of assets used to fund a CLT may be only temporarily depressed and that over an extended investment cycle, values will normalize and perhaps appreciate. 71

72 Preferable Assets To Fund CRT Low basis, highly appreciated, marketable securities - The sale proceeds can then be invested to produce payments to the recipient who benefits from the appreciation of his/her securities via the annuity amount or unitrust amount, but has no taxable recognition of the gain from the sale of the securities while the proceeds or those in that they are invested are held by the CRT. Investment by the CRT in tax free securities may not be wise if the CRT has accumulated undistributed ordinary or capital gains since the recipient still has to recognize the income therefrom under the tier approach applicable to distributions to recipients. It is not a good idea to transfer a donor's personal residence to a CRT, whether unencumbered or encumbered, because the donor cannot live in the residence without committing a prohibited act of self-dealing. Also using encumbered real estate caused unrelated business taxable income A CRT is not a qualified subchapter S shareholder, and therefore, a donor cannot use subchapter S stock to fund a CRT. 72

73 3.8% Medicare Tax Issues Use a CRT to harbor net investment income in a tax-exempt environment while at the same time leveling income over a longer period of time to keep modified adjusted gross income for the beneficiary below the threshold amount. Use a non-grantor CLT to offset net investment income against charitable deductions dollar-for-dollar in a tax-efficient manner. While a CRT itself is not subject to the 3.8% Medicare surtax on net investment income, distributions from the CRT to non-charitable beneficiaries will be potentially subject to the tax as the income is distributed. To avoid "unfairly" causing Medicare taxes to beneficiaries that receive income in 2013 or beyond that was actually created prior to the Medicare tax (and just not yet distributed), the new rules stipulate that only income in the trust that was created in 2013 or later will be treated as net investment income. 73

74 Changes to Form 5227 New Columns added to Part II, Schedule of Distributable Income to capture Accumulated Net Investment Income New question 92 added to Part VII, Section D. 74

75 Changes to Form 5227 New Columns added to Part II, Schedule of Distributable Income to capture Accumulated Net Investment Income 75

76 Slide Intentionally Left Blank

77 Financial Accounting Requirements Donna Jackson, CPA, JD, LLM Vineyard Blvd, Suite E Oklahoma City, OK (40) Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma

78 Financial Accounting Requirements A charitable remainder trust should not pay the estate tax or gift tax of the donor. The creation of an income interest for a person other than the donor creates a gift equal to the value of the property transferred less the APVRI. If the donor s spouse is the only person other than the donor to receive an income interest, then the gift tax marital deduction (IRC 2523(g)) eliminates most gift tax concerns. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 78

79 Define Principal and Income The definition of trust accounting income is a function of the language of the trust s governing instrument and the principal and income statute of the applicable state. Where one or more provisions of the trust s governing instrument are in conflict with the principal and income statute, the trust s governing instrument takes precedence. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 79

80 Trust Provisions A number of desirable optional provisions exist that can increase the utility and flexibility of a CRT. For example, the donor may: retain the power to change the charitable remainder beneficiary. provide the trustee with the ability to accelerate the distribution of principal to the charity spendthrift clause designed to restrict the income beneficiary s ability to alienate his or her interest give the income beneficiary the flexibility to make a charitable gift of his or her income interest Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 80

81 Proper Payments Several potential traps exist regarding the proper amount to pay the income beneficiary. A CRT must use the calendar year as its tax year. As a result, it will have a short tax year in the first and last year of the trust. For any short year, prorate the annuity or unitrust payment. The proration is done on a daily basis. Considerations for Leap-Year Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 81

82 Payment Traps Assuming that the current year s unitrust payment will be the same as the prior year s unitrust payment Paying the income beneficiary of a NIMCRUT or a Flip-CRUT (pre-flip) the full fixed percentage amount without regard to the trust s accounting income. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 82

83 Valuation Issues Unmarketable assets provide the greatest challenge. A CRT trustee will need to know the value of the trust s assets. For example: Valuing the initial contribution to the trust; Determining the annual valuation of the trust s assets and liabilities required to compute the unitrust amount; Valuing additional contributions for the incremental change in the unitrust amount; and Computing how much of an asset to transfer to make an in-kind distribution Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 83

84 Treas. Reg (a)(7) Two alternative methods for securing the value of a CRT s unmarketable assets. First, the valuation can be performed exclusively by an independent trustee. Second, the value can be determined by a current qualified appraisal. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 84

85 Compliance Ensure Continued Qualification of CRT be familiar with the laws and regulations governing CRTs Be familiar with terms of the trust monitor the activity of the trust for compliance. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 85

86 Areas of Concern trustee powers principal and income allocations prohibited investments self-dealing transactions transactions that could produce UBTI Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 86

87 Annual Reporting In some states, the trustee is required to make a periodic statement or accounting to the income beneficiaries, remainder beneficiaries, and/or a court. Charities that prepare financial statements in accordance with GAAP are required to include certain information about charitable remainder trusts. The type of information to be included depends on whether the charity serves as trustee (or not) and whether the charity s interest is revocable or irrevocable. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 87

88 Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 88

89 Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 89

90 Recording Balance Sheet Limitations Assets recorded at historical cost (does not show true value of asset) Use of cost estimates (not true financial position) Omission of valuable non-monetary assets Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 90

91 Reporting Financial statements Tax return presentation More requirements than fiduciary accounting to Court Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 91

92 Reporting A fiduciary accounting shall contain sufficient information to put the interested parties on notice as to all significant transactions affecting administration during the accounting period. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 92

93 Financial Accounting Requirements The presentation of the information in an account shall allow an interested party to follow the progress of the fiduciary s administration of assets during the accounting period without reference to an inventory or earlier accounting that is not included in the current account. An account is not complete if it does not itemize assets on hand at the beginning of the accounting period. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 93

94 Reporting The first account for a decedent s estate or a trust should detail the items received by the fiduciary and for which he is responsible. It should not simply refer to the total amount of an inventory filed elsewhere or assets described in a schedule attached to a deed of trust. In later accounts for an estate or trust, the opening balance should not simply refer to the total value of principal on hand as shown in detail in the prior account, but should list each item separately. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 94

95 Reporting Instead of retyping the complete list of assets in the opening balance, the accountant may prefer to attach as an exhibit a copy of the inventory, closing balance from last account, etc. Transactions shall be described in sufficient detail to give interested parties notice of their purpose and effect. Too much detail may be counterproductive to making the account understandable. In accounts covering long periods or dealing with extensive assets, consolidate information. Ie: securities being accounted for over a long period of time, a statement of the total dividends received on each security with appropriate indication of changes in the number of shares held will be more readily understandable and easier to check for completeness than a chronological listing of all dividends received. Although detail should generally be avoided for routine transactions, it will often be necessary to a proper understanding of an event that is somewhat out of the ordinary. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 95

96 Reporting Separately show and explain the following: Extraordinary appraisal costs Interest and penalties in connection with later filing of tax returns An extraordinary allocation between principal and income Computation of a formula marital deduction gift involving non-probate assets Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 96

97 Split Interest Agreements, Disclosure Requirements Separate disclosure in notes to the financial statements Contributions or changes in value of the splitinterest agreements are required to be (a) reported as separate line items in the statement of activities or (b) disclosed in the notes to the financial statements. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 97

98 Disclosures In addition, the following disclosures related to split-interest agreements are required: a) A summary of the terms of the agreements. b) The basis that the organization used for recognizing assets related to the split-interest agreements in the financial statements. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 98

99 Disclosures c) If present value techniques are used in reporting the assets and liabilities relating to split-interest agreements, information about the discount rates and actuarial assumptions that the organization used in determining present value amounts. d) Legally mandated reserves arising from split-interest agreements. e) For charitable gift annuity agreements, any limitations imposed by state law, such as limitations on the manner in which some net assets are invested. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 99

100 Carrying Values Carrying values based on date of death may be adjusted to reflect changes on audit of estate or inheritance tax returns. Where appropriate under applicable local law, a successor fiduciary may adjust the carrying value of assets to reflect values at the start of his administration. Assets received in kind in satisfaction of a pecuniary legacy should be carried at the value used for purposes of distribution. Though essential for accounting purposes, carrying values are commonly misunderstood by laymen as being a representation of actual values. To avoid this, the account should include both current values and carrying values Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 100

101 Other Accounting Considerations Gains and losses incurred during the accounting period shall be shown separately in the same schedule The account shall show significant transactions that do not affect the amount for which the fiduciary is accountable. Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 101

102 NFP Resources AICPA Audit and Accounting Guides AICPA Technical Practice Aids National Organization Guides AICPA Government Audit Quality Center Iknow.org, boardnetusa.org, foundationcenter.org, nonprofitquarterly.org, hrgpc.org, acga-web.org Donna J. Jackson, Attorney at Law, P.C., Oklahoma City, Oklahoma 102

Charitable Split-Interest Trusts and Form 5227

Charitable Split-Interest Trusts and Form 5227 Avoiding Compliance Pitfalls and Navigating Recent Regulatory Changes TUESDAY, SEPTEMBER 24, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program

Charitable Split-Interest Trusts and Form 5227 Avoiding Compliance Pitfalls and Navigating Recent Regulatory Changes TUESDAY, SEPTEMBER 24, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More

FOR LIVE PROGRAM ONLY Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 18, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 18, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor

Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor") Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives. 41st Annual MPGC Conference November 15-16, 2017

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

Charitable Lead Trusts

Charitable Lead Trusts Michael V. Bourland, Jeffrey N. Myers, and Deren L. Worrell A. Attributes Of Charitable Lead Trusts ( CLTs ) 1. Payment Charitable Lead Interest. Annual (or more often) payments

Charitable Lead Trusts Michael V. Bourland, Jeffrey N. Myers, and Deren L. Worrell A. Attributes Of Charitable Lead Trusts ( CLTs ) 1. Payment Charitable Lead Interest. Annual (or more often) payments

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Charitable Trusts. Charitable Trusts

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Using Your Assets to Promote your Values. Lawrence M. Lehmann, JD, AEP, CAP Lehmann Norman & Marcus LC

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law

Presenting a live 90-minute webinar with interactive Q&A Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law WEDNESDAY, FEBRUARY 7, 2018 1pm Eastern 12pm Central 11am Mountain

Presenting a live 90-minute webinar with interactive Q&A Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law WEDNESDAY, FEBRUARY 7, 2018 1pm Eastern 12pm Central 11am Mountain

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Presented by Richard D. Cirincione 677 Broadway Albany, NY Direct: Fax:

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

The Time is Right To Consider Charitable Lead Trusts

The Time is Right To Consider Charitable Lead Trusts May 13, 2016 2016 Day Pitney LLP Planned Giving Group of New England Jennifer M. Pagnillo, Esq. Day Pitney LLP 24 Field Point Road Greenwich, CT 06830

The Time is Right To Consider Charitable Lead Trusts May 13, 2016 2016 Day Pitney LLP Planned Giving Group of New England Jennifer M. Pagnillo, Esq. Day Pitney LLP 24 Field Point Road Greenwich, CT 06830

IMPORTANT INFORMATION

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

Impact of Tax Reform on ABLE Accounts and Special Needs Trusts: Guidance for Elder Law Attorneys

Presenting a live 90-minute webinar with interactive Q&A Impact of Tax Reform on ABLE Accounts and Special Needs Trusts: Guidance for Elder Law Attorneys THURSDAY, SEPTEMBER 27, 2018 1pm Eastern 12pm Central

Presenting a live 90-minute webinar with interactive Q&A Impact of Tax Reform on ABLE Accounts and Special Needs Trusts: Guidance for Elder Law Attorneys THURSDAY, SEPTEMBER 27, 2018 1pm Eastern 12pm Central

S-Corp Trusts in Estate Planning: Drafting Grantor, Testamentary, Qualified Sub S and Electing Small Business Trusts

Presenting a live 90-minute teleconference with interactive Q&A S-Corp Trusts in Estate Planning: Drafting Grantor, Testamentary, Qualified Sub S and Electing Small Business Trusts Navigating Interest

Presenting a live 90-minute teleconference with interactive Q&A S-Corp Trusts in Estate Planning: Drafting Grantor, Testamentary, Qualified Sub S and Electing Small Business Trusts Navigating Interest

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Grantor Trusts After Divorce: Tax Reform, Fiduciary Challenges, and Minimizing Tax for Trust Transfers to Former Spouse Gift Tax Exemption on Divorce

Presenting a live 90-minute webinar with interactive Q&A Grantor Trusts After Divorce: Tax Reform, Fiduciary Challenges, and Minimizing Tax for Trust Transfers to Former Spouse Gift Tax Exemption on Divorce

Pointers in Selecting Assets to Fund Charitable Trusts

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

CHARITABLE GIFTS. A charitable gift has a number of different tax benefits, which benefits differ if the gift is made during life or at death.

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

Stupid Charitable Tricks:

Stupid Charitable Tricks: Charitable Planning Mistakes I Have Seen Ramsay Slugg November, 2017 Disclosure (use this if the next slide N/A) IMPORTANT: This presentation is designed to provide general information

Stupid Charitable Tricks: Charitable Planning Mistakes I Have Seen Ramsay Slugg November, 2017 Disclosure (use this if the next slide N/A) IMPORTANT: This presentation is designed to provide general information

Kingdom Advisors Charitable Giving Tool Kit

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

How To Coordinate Charitable Contribution Planning Opportunities with Business Succession Planning: The Charitable Lead Trust

How To Coordinate Charitable Contribution Planning Opportunities with Business Succession Planning: The Charitable Lead Trust Michael V. Bourland Shannon G. Guthrie All section references are to the Internal

How To Coordinate Charitable Contribution Planning Opportunities with Business Succession Planning: The Charitable Lead Trust Michael V. Bourland Shannon G. Guthrie All section references are to the Internal

PRACTICAL CHARITABLE PLANNING EXAMPLES THAT DON T REQUIRE YOU TO BE A TAX EXPERT. THE ABCS OF CRATS, CRUTS, CLATS AND CLUTS.

PRACTICAL CHARITABLE PLANNING EXAMPLES THAT DON T REQUIRE YOU TO BE A TAX EXPERT. THE ABCS OF CRATS, CRUTS, CLATS AND CLUTS. IS THE ALPHABET REALLY THAT DIFFICULT? HOW TO PROVIDE FOR YOUR FURRY FRIENDS!

PRACTICAL CHARITABLE PLANNING EXAMPLES THAT DON T REQUIRE YOU TO BE A TAX EXPERT. THE ABCS OF CRATS, CRUTS, CLATS AND CLUTS. IS THE ALPHABET REALLY THAT DIFFICULT? HOW TO PROVIDE FOR YOUR FURRY FRIENDS!

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Brian E. Hammell, Esq., Sullivan & Worcester, Boston

Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax,

Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax,

Advanced Trust Drafting for Income Tax Minimization: Including Capital Gains in DNI, Push-Outs and More

Presenting a live 90-minute webinar with interactive Q&A Advanced Trust Drafting for Income Tax Minimization: Including Capital Gains in DNI, Push-Outs and More Managing the Disparity in Income Tax Treatment

Presenting a live 90-minute webinar with interactive Q&A Advanced Trust Drafting for Income Tax Minimization: Including Capital Gains in DNI, Push-Outs and More Managing the Disparity in Income Tax Treatment

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Dean C. Berry, Partner, Cadwalader Wickersham & Taft, New York

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Leaving a Legacy. Your Guide to Charitable Giving

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Structuring and Operating Family Limited Partnerships: Asset Protection and Income Tax Reduction Shifting Income Tax Burden to Lower-Taxed Family

Presenting a live 90-minute webinar with interactive Q&A Structuring and Operating Family Limited Partnerships: Asset Protection and Income Tax Reduction Shifting Income Tax Burden to Lower-Taxed Family

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

ALI-ABA Course of Study Estate Planning for the Family Business Owner

425 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

425 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis

Presenting a live 90-minute webinar with interactive Q&A Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis TUESDAY, JUNE 28, 2016 1pm Eastern 12pm

Presenting a live 90-minute webinar with interactive Q&A Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis TUESDAY, JUNE 28, 2016 1pm Eastern 12pm

Form 1120S Challenges for Tax Preparers

Form 1120S Challenges for Tax Preparers Navigating Computations-to-Adjustments Accounts and Determining Treatment of Dividends, Distributions and Fringe Benefits WEDNESDAY, DECEMBER 10, 2014, 1:00-2:50

Form 1120S Challenges for Tax Preparers Navigating Computations-to-Adjustments Accounts and Determining Treatment of Dividends, Distributions and Fringe Benefits WEDNESDAY, DECEMBER 10, 2014, 1:00-2:50

Is It a Grantor Chartable Lead Trust or Not - How the Grantor Trust Rules Interact with the Charitable Lead Trust, 30 J. Marshall L. Rev.

The John Marshall Law Review Volume 30 Issue 4 Article 7 Summer 1997 Is It a Grantor Chartable Lead Trust or Not - How the Grantor Trust Rules Interact with the Charitable Lead Trust, 30 J. Marshall L.

The John Marshall Law Review Volume 30 Issue 4 Article 7 Summer 1997 Is It a Grantor Chartable Lead Trust or Not - How the Grantor Trust Rules Interact with the Charitable Lead Trust, 30 J. Marshall L.

Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets

Presenting a live 90-minute webinar with interactive Q&A Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets WEDNESDAY, MARCH

Presenting a live 90-minute webinar with interactive Q&A Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets WEDNESDAY, MARCH

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Charitable Giving: Tax Benefits and Strategies

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

charitable contributions

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

Planned Giving. For Beginners

Planned Giving For Beginners What is Planned Giving? The integration of personal, financial and estate planning goals using lifetime or testamentary charitable giving with benefits to the donor ANNUAL

Planned Giving For Beginners What is Planned Giving? The integration of personal, financial and estate planning goals using lifetime or testamentary charitable giving with benefits to the donor ANNUAL

Private Investment Funds and Tax Reform

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Converting to Nongrantor Trusts to Minimize Income Tax: Maximizing Increased Exemption Benefits Switching Off Grantor Trust Features in Existing

Presenting a live 90-minute webinar with interactive Q&A Converting to Nongrantor Trusts to Minimize Income Tax: Maximizing Increased Exemption Benefits Switching Off Grantor Trust Features in Existing

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Arthritis Foundation Texas Chapter Planned Giving Seminar May 20, 2010 PLANNING WITH CHARITABLE REMAINDER TRUSTS

I. Generally. Arthritis Foundation Texas Chapter Planned Giving Seminar May 20, 2010 PLANNING WITH CHARITABLE REMAINDER TRUSTS R. Thomas Groves, Jr. Jackson Walker L.L.P. 901 Main Street, Suite 6000 Dallas,

I. Generally. Arthritis Foundation Texas Chapter Planned Giving Seminar May 20, 2010 PLANNING WITH CHARITABLE REMAINDER TRUSTS R. Thomas Groves, Jr. Jackson Walker L.L.P. 901 Main Street, Suite 6000 Dallas,

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER Patricia M. Annino, Attorney Prince Lobel Tye LLP Birmingham Estate Planning Council May 20, 2016 WHY IS IT IMPORTANT? Closely held business owners

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER Patricia M. Annino, Attorney Prince Lobel Tye LLP Birmingham Estate Planning Council May 20, 2016 WHY IS IT IMPORTANT? Closely held business owners

Drafting Income-Only Trusts for Medicaid Eligibility and Tax Planning

Presenting a live 90-minute webinar with interactive Q&A Drafting Income-Only Trusts for Medicaid Eligibility and Tax Planning Navigating Look-Back, Grantor Trust, Basis and Gift Tax Rules WEDNESDAY, OCTOBER

Presenting a live 90-minute webinar with interactive Q&A Drafting Income-Only Trusts for Medicaid Eligibility and Tax Planning Navigating Look-Back, Grantor Trust, Basis and Gift Tax Rules WEDNESDAY, OCTOBER

Tax Challenges for NPO Counsel: Excess Benefit Transactions for Executive Comp and Other Financial Dealings

Presenting a live 110-minute teleconference with interactive Q&A Tax Challenges for NPO Counsel: Excess Benefit Transactions for Executive Comp and Other Financial Dealings Identifying Prohibited Transactions

Presenting a live 110-minute teleconference with interactive Q&A Tax Challenges for NPO Counsel: Excess Benefit Transactions for Executive Comp and Other Financial Dealings Identifying Prohibited Transactions

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform

and Form 1041 Trust Deduction Rules Post-Tax Reform") New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Structuring Preferred Partnership Freezes in Estate Planning: Navigating IRC Chapter 14 Valuation Rules

Presenting a live 90-minute webinar with interactive Q&A Structuring Preferred Partnership Freezes in Estate Planning: Navigating IRC Chapter 14 Valuation Rules WEDNESDAY, MARCH 30, 2016 1pm Eastern 12pm

Presenting a live 90-minute webinar with interactive Q&A Structuring Preferred Partnership Freezes in Estate Planning: Navigating IRC Chapter 14 Valuation Rules WEDNESDAY, MARCH 30, 2016 1pm Eastern 12pm

Private Foundations in Estate Planning: Structuring Tax-Efficient Charitable Legacies

Presenting a live 90-minute webinar with interactive Q&A Private Foundations in Estate Planning: Structuring Tax-Efficient Charitable Legacies Minimizing Tax in Diversified Estates, Maximizing Charitable

Presenting a live 90-minute webinar with interactive Q&A Private Foundations in Estate Planning: Structuring Tax-Efficient Charitable Legacies Minimizing Tax in Diversified Estates, Maximizing Charitable

Robert S. Barnett, Partner, Capell Barnett Matalon & Schoenfeld, Jericho, N.Y.

Presenting a live 90-minute webinar with interactive Q&A Advanced Trust Drafting for Income Tax Minimization: Including Capital Gains in DNI, Push-Outs and More Managing the Disparity in Income Tax Treatment

Presenting a live 90-minute webinar with interactive Q&A Advanced Trust Drafting for Income Tax Minimization: Including Capital Gains in DNI, Push-Outs and More Managing the Disparity in Income Tax Treatment

Top 10 Income Tax Planning Ideas for 2013

Top 10 Income Tax Planning Ideas for 2013 Presented by: Robert S. Keebler, CPA, MST, AEP(Distinguished) Ph: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Ideas 1. Bracket Management 2.

Top 10 Income Tax Planning Ideas for 2013 Presented by: Robert S. Keebler, CPA, MST, AEP(Distinguished) Ph: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Ideas 1. Bracket Management 2.

Building Charitable Trusts Into A Client s Estate, Tax And Family Planning

Building Charitable Trusts Into A Client s Estate, Tax And Family Planning Publication: Practising Law Institute Introduction Charitable giving has become a significant consideration in the tax and estate

Building Charitable Trusts Into A Client s Estate, Tax And Family Planning Publication: Practising Law Institute Introduction Charitable giving has become a significant consideration in the tax and estate

HELD BUSINESS INTERESTS

PLANNED GIVING WITH CLOSELY HELD BUSINESS INTERESTS Gregory S. Williams, Esq. Carruthers & Roth, P.A. Phone: 336-478-1183 E-mail: gsw@crlaw.com Disclaimer The contents of this presentation have been prepared

PLANNED GIVING WITH CLOSELY HELD BUSINESS INTERESTS Gregory S. Williams, Esq. Carruthers & Roth, P.A. Phone: 336-478-1183 E-mail: gsw@crlaw.com Disclaimer The contents of this presentation have been prepared

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA Tel: (310) Fax: (310)

Fax: (310)") Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,