The Truth About Trusts To Trust or not to Trust: That is the Question

|

|

|

- Pierce White

- 5 years ago

- Views:

Transcription

1 The Truth About Trusts To Trust or not to Trust: That is the Question Tim Mezhlumov, EA Melissa Simmons, CPA, EA Presented to North Texas Chapter of EAs, August 5, 2017

2 What is a Trust? A. A trust is traditionally used for minimizing estate taxes and can offer other benefits as part of a well-crafted estate plan. B. A trust is a fiduciary arrangement that allows a third party, or trustee, to hold assets on behalf of a beneficiary or beneficiaries. C. Trusts can be arranged in many ways and can specify exactly how and when the assets pass to the beneficiaries.

3 What is a Trust? D. Since trusts usually avoid probate, your beneficiaries may gain access to these assets more quickly than they might to assets that are transferred using a will. Additionally, if it is an irrevocable trust, it may not be considered part of the taxable estate, so fewer taxes may be due upon your death. E. Assets in a trust may also be able to pass outside of probate, saving time, court fees, and potentially reducing estate taxes as well.

4 What is a Trust? F. Other benefits of trusts include: 1. Control of your wealth. You can specify the terms of a trust precisely, controlling when and to whom distributions may be made. You may also, for example, set up a revocable trust to that the trust assets remain accessible to you during your lifetime while designating to whom the remaining assets will pass thereafter, even when there are complex situations such as children from more than one marriage.

5 What is a Trust? 2. Protection of your legacy. A properly constructed trust can help protect your estate from your heirs creditors or from beneficiaries who may not be adept at money management. 3. Privacy and probate savings. Probate is a matter of public record; a trust may allow assets to pass outside of probate and remain private, in addition to possibly reducing the amount lost to court fees and taxes in the process.

6 Creating Trusts Created when a donor transfers property to a fiduciary or trustee for the benefit of one or more beneficiaries Trust property is called corpus or principal A trust may be: Revocable: This type of trust may be changed by the grantor at any point during his or her lifetime. Irrevocable: This type of trust may be created either by will (testamentary trust) or by the grantor during his/her lifetime (inter-vivos).

7 Basic Types of Trusts Marital or A trust: Designed to provide benefits to a surviving spouse; generally included in the taxable estate of the surviving spouse Bypass or B trust: Also known as credit shelter trust, established to bypass the surviving spouse s estate in order to make full use of any federal estate tax exemption for each spouse

8 Basic Types of Trusts Testamentary Trust: Outlined in a will and created through the will after the death, with funds subject to probate and transfer taxes; often continues to be subject to probate court supervision thereafter Irrevocable life insurance trust (ILIT): Irrevocable trust designed to exclude life insurance proceeds from the deceased s taxable estate while providing liquidity to the estate and/or the trusts beneficiaries.

9 Basic Types of Trusts Charitable lead trust: Allows certain benefits to go to a charity and the remainder to your beneficiaries. Charitable remainder trust: Allows you to receive an income stream for a defined period of time and stipulate that any remainder to a charity Generation-skipping trust: Using the generation-skipping tax exemption, permits trust assets to be distributed to grandchildren or later generations without incurring either a generation-skipping tax or estate taxes on the subsequent death of your children.

10 Basic Types of Trusts Qualified Terminable Interest Property (QTIP) trust: Used to provide income for a surviving spouse. Upon the spouse s death, the assets then go to additional beneficiaries named by the deceased. Often used in second marriage situations, as well as to maximize estate and generation-skipping tax or estate tax planning flexibility

11 Basic Types of Trusts Grantor Retained Annuity Trust (GRAT): Irrevocable trust funded by gifts by its grantor; designed to shift future appreciation on quickly appreciating assets to the next generation during the grantor s lifetime Qualified Disability Trusts: Non-grantor trust created solely for the benefit of a disabled individual under age 65. All the beneficiaries of the trust as of the close of the taxable year are determined by the Commission of Social Security to have been disabled (within the meaning of section 1614(a)(3) of the Social Security Act, 42 U.S.C. 1382c(a)(3)) for some portion of such year.

12 Basic Types of Trusts Electing Small Business Trust (ESBT): An ESBT is a statutory creature established by Congress in the Small Business Job Protection Act of 1996 (P.L ). A trust may own S Corporation shares if it meets the requirements of an ESBT. A trust may qualify as an electing small business trust and as an S Corporation shareholder even if the trustee does not distribute all of the trust s income annually to its beneficiaries. An election must be made to be treated as an ESBT.

13 Basic Types of Trusts Grantor type trust: A grantor trust is one in which the creator (or grantor) retains some power or interest over the income and/or corpus of the trust. Created by a living individual, group of individuals, or other entity, this type of trust is not recognized as a separate taxable entity apart from its grantor for income tax purposes. Therefore, income earned by the assets of the trust is directly reported on the grantor or owner s income tax return. Accordingly, the grantor is deprived of any possible income tax advantages that might occur if the trust were taxed separately, such as lower marginal tax rates and a standard exemption amount.

14 Basic Types of Trusts Qualified Funeral Trust (QFT): A qualified funeral trust arises as a result of a contract with a person engaged in the trade or business of providing funeral or burial services or property necessary to provide such services. The sole purpose of the trust is to hold, invest, and reinvest funds in the trust and to use such funds solely to make payments for such services or property for the benefit of the beneficiaries of the trust. The only beneficiaries of QFTs are individuals with respect to whom such services or property are to be provided at their death under the contract. The only contributions to the trust are contributions by or for the benefit of such beneficiaries. The trustee of the trust must make an election to be treated as a QFT.

15 Basic Types of Trusts Split-Interest Charitable Trusts: Splitinterest means that the interest in the property is split into two parts: an income interest and a remainder interest. The income interest is separate from the remainder interest. Both interests can be assigned to a charity of charities, one or more non-charitable beneficiaries, or both depending on the type of splitinterest charitable trust.

16 Basic Types of Trusts In Addition, charitable trusts engaging in business activities but organized to benefit charities are subject to the rules on unrelated business income. Based on the method and timing of distributions, split-interest charitable trusts are divided into the following four categories:

17 Basic Types of Trusts 1. Charitable remainder annuity trusts: Distribute income in a series of fixed payments to one or more non-charitable beneficiaries for a defined period of time, after which the remaining value of the trust is transferred to a charitable beneficiary. 2. Charitable remainder unitrusts: Distribute a percentage of the fair market value to one or more non-charitable beneficiaries for a defined period of time, after which remaining value of the trust is transferred to a charitable beneficiary.

18 Basic Types of Trusts 3. Charitable Lead Trusts: Distribute a sequence of payments to a charitable beneficiary for a period of time, after which the remaining trust assets are transferred to a non-charitable beneficiary. 4. Pooled Income Funds: Allow donors to donate assets to a charity. The pooled assets are invested as a group and each donor receives income based on the ration of his or her contribution to the total value of the investment pool. After the death of the donor, his or her prorated share of the investment pool is withdrawn and given to the charitable organization.

19 Basic Types of Trusts Pet Trusts: A legally sanctioned arrangement providing for the care and maintenance of one or more companion animals in the event of a grantor s disability or death. Miller Trust: A Miller Trust makes Social Security and other income exempt from calculations of income and resources if the state is reimbursed from the trust for Medicaid expenses upon the recipient s death.

20 Benefits of Generation-skipping Trust Not just for the wealthy: This type of trust provides a great way to safeguard any family s assets from excess tax, creditors and ex-spouses looking for their share of the estate. Good choice for wealthier families to be able to transfer their assets from the older generation to their grandchildren or great grandchildren without making their assets vulnerable to estate or so-called death tax.

21 Benefits of Generation-skipping Trust Allows all descendants to benefit the most from assets in the trust without the harsh imposition of estate or death tax when the children die, and then again when the grandchildren pass away.

22 Benefits of Generation-skipping Trust Protects assets from second generation problems: 1. Let s assume that a child in the second generation has gone through a less than amicable divorce. Because the assets in the generation skipping trust won t legally belong to the exspouse, the divorcing spouse will never be able to claim a share of the trust s assets. 2. If a child starts a company and the company later goes under, the assets in the trust cannot be tapped into to pay the debts of the child as the child does not own the assets.

23 Benefits of Generation-skipping Trust 3. Protects assets from other financial catastrophes that may occur, such as an uninsured car accident or a large gambling debt 4. For a child that might be a spendthrift, this trust will allow the child to have access to trust assets but not be in control over the timing of distributions of those assets.

24 Generation-skipping Trust Limitations Limit that can be transferred is $2 million per person that can be left in the trust. Transfers to the trust can be made in amounts up to $1 million. Some professionals request their parents put their estates into a generation skipping trust. For example, a doctor who has an enhanced risk of liability may see the generation skipping trust as a way for his parent s estate to be protection from creditors while the assets are still available to him.

25 Revocability Donor control May be irrevocable Donor gives up control over property May be revocable Donor may revoke trust and take back property Treated as grantor trust with donor taxable on all income even if trust is not revoked

26 Separate Legal Entity Under State Law A trust must meet both state law and federal law requirements to be so recognized. The Internal Revenue Code contains no definition of a trust; only state law governs trusts. The trustor (grantor or settlor) is the person who transfers property to the trustee. The trustee then manages the property for the benefit of the beneficiaries named and distributes income and principal in accordance with the trust agreement.

27 Trusts - Nontax Purposes May get professional management through use of a corporate trustee, such as a bank Useful for providing for beneficiaries incapable of managing property, such as children Useful if lifetime beneficiaries are different from remaindermen Lifetime Beneficiary: Entitled to receive income and possibly principal from the trust property Remainderman: Entitled to receive a portion of the principal at termination of the life interest. Trusts may be useful in minimizing estate costs and can offer other benefits as part of a well-crafted estate plan.

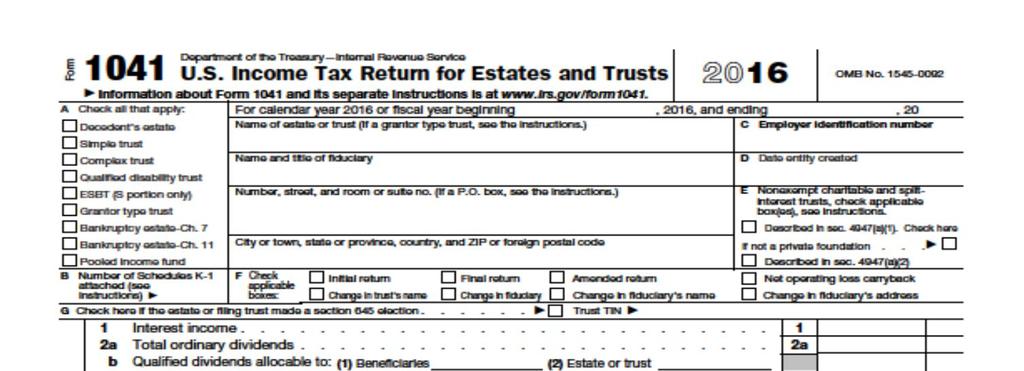

28 Trusts Simple trust Trust required to distribute all of its accounting income Trust does not allow amounts to be paid, permanently set aside or used in the tax year for charitable purposes Trust does not distribute amounts from the principal of the trust (corpus) Complex trust Any trust that is not a simple trust

29 Simple vs. Complex Trusts A. An irrevocable trust may be either simple or complex. B. The terms simple and complex are not found in the Internal Revenue Code. C. They are, however, to be found in the regulations and on the form 1041 tax return and instructions and are frequently used in practice.

30 Simple vs. Complex Trusts D. For a trust to qualify as a simple trust in any year, it must meet all three of the following criteria ( ) 1. The trust requires that all fiduciary accounting income must be distributed currently to the beneficiaries; and 2. The trust does not make charitable contributions; and 3. The trust does not distribute principal.

31 Simple vs. Complex Trusts E. The phrase all accounting income be distributed currently means that all fiduciary accounting income is required by the terms of the trust instrument to be distributed in the year that it is received. F. The trustee must be under a duty to distribute the income currently. G. The fact that the actual distribution is not made until after the close of the taxable year does not eliminate status of a simple trust.

32 Simple vs. Complex Trusts H. If the trust requires all income to be distributed currently, then it is deemed to have been distributed (Reg. 1.65(a)-2). I. If the trust does not qualify as a simple trust, then it is, by definition, a complex trust ( ). The distinction is important in computing the distribution deduction for the trust.

33 Worksheet Simple vs. Complex Trust Determination For a trust to qualify as a SIMPLE TRUST, all answers to the following questions MUST BE YES IRC The Trust requires that all fiduciary accounting income must be distributed currently Yes No 2. The trust does not allow amounts to be paid, permanently set aside or used in the tax year for charitable purposes 3. The trust does not distribute amounts from the principal of the trust If you answered NO to ANY of the above Questions, the trust does not qualify as a simple trust. It is a COMPLEX TRUST, IRC , for the current year.

34 Charitable Trusts Complex Trusts Have charitable and non-charitable beneficiaries Charitable Remainder Trust Charity gets the remainder at the end of trust term Charitable Lead Trust Charity gets income during trust term

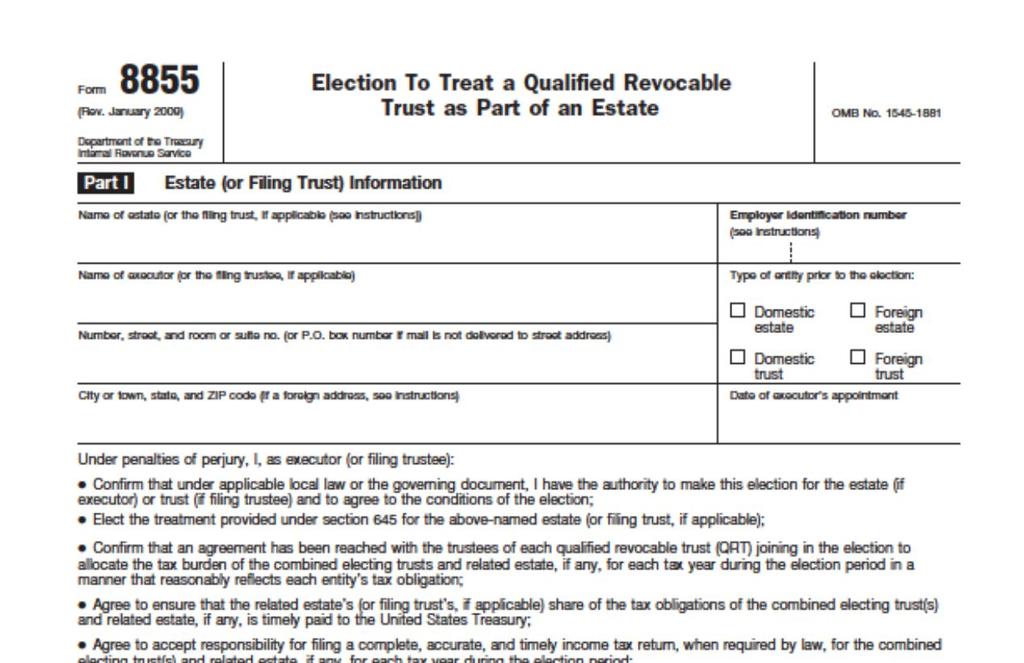

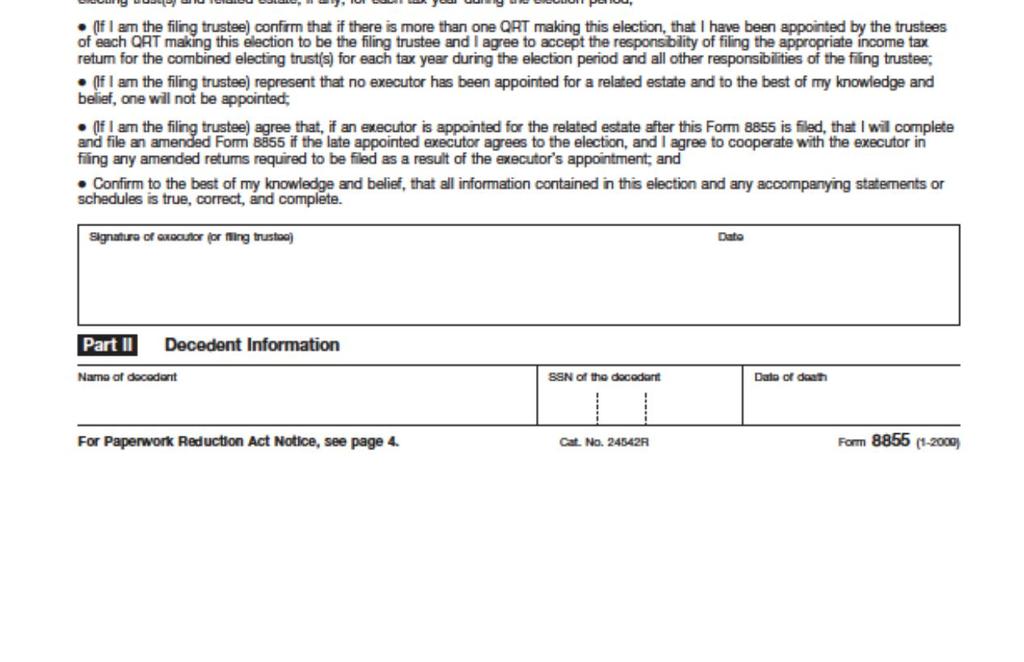

35 Tax Professional Alerts To attempt to prepare a trust tax return (form 941) the tax professional needs a minimum of two documents, the Last Will and Testament and the Trust Agreement. A trust can be a simple trust one year and a complex trust the next year All trusts will be treated as complex trusts in the final year, as the trust must distribute principal at the time of the final return. An election can be made for a qualified revocable trust (QRT) to be treated as part of and estate (IRC 645). A QRT is a trust, or portion of a trust, treated as owned by a decedent because the decedent had the power to revoke the trust on the date of death. (See form 8855)

36

37 Trust Filing Requirements Any taxable income for the tax year Gross income of $600 or more (regardless of taxable income) A beneficiary who is a nonresident alien

38 Trust Due Date Trusts must use a calendar year unless the trust is treated as wholly owned by a grantor, or falls under IRC section 501(a) tax-exempt trusts and IRC section 4947(a)(1) charitable trusts. Deadline is the 15 th day of the fourth month after the close of the tax year, ie April 15 th?? Extensions are granted for 5 ½ months using form 7004

39 States with Inheritance Tax Connecticut Delaware District of Columbia Hawaii Illinois Iowa Kentucky Maine Maryland Massachusetts Minnesota Nebraska New Jersey New York Oregon Pennsylvania Rhode Island Tennessee Vermont Washington

40 Trust Accounting Income Importance: determines the amount paid to income beneficiaries each year. Categories of income (interest, dividends, capital gains, etc.) and expenses are assigned to income or principal. If trust document is silent on allocation, state law controls, usually determined by the state s principal and income act. cs/pr/htm/pr.116.htm

41 Common Allocations Income Interest, dividends, rents, royalties Operating income Operating expense Taxes levied on income Principal Capital gains and losses on investments Casualty losses and insurance recoveries Extraordinary repairs Taxes levied on principal

42 Example of Accounting Income Income and Expenses Accounting Income Interest $ 3, $ 3, Dividends $10, $10, Capital Gains $ 7, $ -0- Trustee Fees $(2,000.00) $(1,000.00) Tax Preparation $ (400.00) $ (200.00) $17,600 $11,800.00

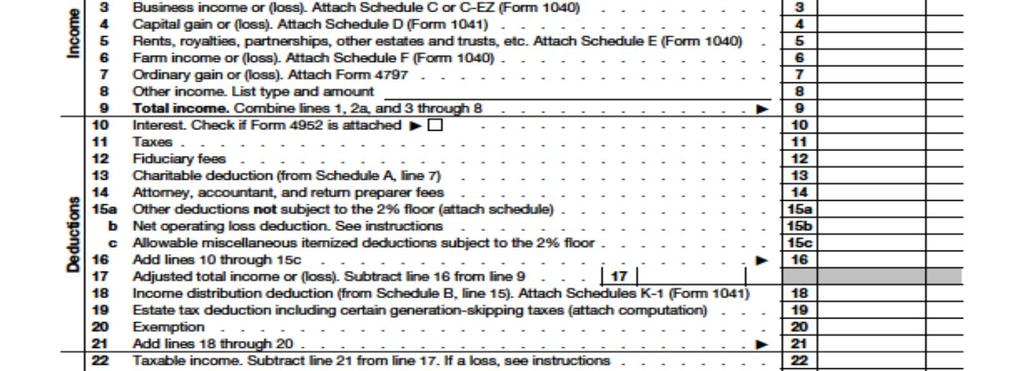

43 Trust Taxable Income Computed in a manner similar to individual taxable income No adjusted gross income concept No standard deduction

44 Trust Taxable Income Calculation Step 1: Calculate trust accounting income Step 2: Calculate trust taxable income before income distribution deduction Step 3: Compute distributable net income (DNI) and the distribution deduction Step 4: Subtract the distribution deduction from the amount in step 2 to determine trust taxable income

45 Trust Taxable Income Calculation (continued) Step 5: Calculate trust tax liability Step 6: Allocated DNI and the distribution deduction to the beneficiaries to determine the amount and character of income taxed to each beneficiary

46 Depreciation May be deductible by trust, beneficiaries or allocated between them Trust document controls If document silent, depreciation apportioned based on share of trust accounting income In such a situation a simple trust would allocate all depreciation to beneficiaries

47 Other Expenses Any expense attributable to earning taxexempt income is nondeductible Indirect expenses such as trust administration fees must be allocated between taxable and tax-exempt income based upon their proportion of total income

48 Example of Tax-Exempt Allocation of Expenses Total Income Accounting Income Interest & Div $ 4, $ 4, Rental Income $14, $14, Muni Bond interest $ 6, $ 6, Gross $24, $24, Capital Gains $ 7, $ -0- Rental Expenses $(9,000.00) $(9,000.00) Trustee Fees $(3,000.00) $ (750.00) Rental expenses are directly allocable to taxable income and are deducted in full. Trustee Fees of $3,000 must be allocated: $3000 expense x $6,000 tax-exempt interest/$24,000 Gross accounting income = $750 Reduction Line 12 (form 1041) deduction = $3,000 - $750 = $2,250 Capital gains are included in gross accounting income only if allocated to income.

49

50 Exemptions All trusts entitled to a personal exemption except in final year Trusts required to distribute all income annually receive an exemption of $300 Other trusts receive $100 exemption

51 Distributable Net Income (DNI) Defines the maximum possible income distribution deduction and maximum possible income from trust taxable to beneficiaries Distributable does not necessarily means that it was actually distributed Trust document may dictate distributions Examples: minors, spendthrift, incapacitation

52 Distributable Net Income Calculation Start: Add: Taxable income before distribution deduction Personal exemption Subtract: Capital gains allocated to principal Add: Add: Capital losses allocated to principal Tax-exempt interest Subtract: Expenses allocated to tax-exempt income

53 Trust Tax Liability Tax rates are steeply progressive reaching the maximum rate of 39.6% with only $12,500 of taxable income in 2017 Often beneficiaries are in lower rate brackets

54 Additional Tax Liability 3.8% surtax applies to lesser of: 1) undistributed net investment income or 2) excess of AGI over $12,500 (2017)

55 Character of Income If more than one type of income is distributed from a complex trust, it must be allocated proportionately among income beneficiaries

56 Trust Property Distributions Property passes out at its adjusted basis Trust does not recognize gain or loss on distribution Beneficiary takes carryover basis Holding period tacks

57 Trust Property Distributions At the option of the trustee, the trust may elect to recognize gain on distributions of appreciated property Distribution treated as made at fair market value to beneficiary Holding period begins on date of the distribution

58 Questions?? Contact information: Melissa Simmons Some of the material used for this presentation was taken from NCPE, National Center for Professional Education, Inc. and NCPE Fellowship s 2017 presentation of What s Happening in the World of Tax. Permission granted by Beanna Whitlock, EA.

Trusts and Other Planning Tools

Trusts and Other Planning Tools Today, We Will Discuss: Estate planning fundamentals Wills and probate Taxes Trusts Life insurance Alternate decision makers How we can help Preliminary Considerations Ask

Trusts and Other Planning Tools Today, We Will Discuss: Estate planning fundamentals Wills and probate Taxes Trusts Life insurance Alternate decision makers How we can help Preliminary Considerations Ask

Advisory. Will and estate planning considerations for Canadians with U.S. connections

Advisory Will and estate planning considerations for Canadians with U.S. connections Canadian citizens and residents may be exposed to U.S. estate, gift, and generation-skipping transfer tax (together,

Advisory Will and estate planning considerations for Canadians with U.S. connections Canadian citizens and residents may be exposed to U.S. estate, gift, and generation-skipping transfer tax (together,

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts

National Society of Tax Professionals presents Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts Developed and Written by Paul La Monaca, CPA, MST NSTP Director of

National Society of Tax Professionals presents Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts Developed and Written by Paul La Monaca, CPA, MST NSTP Director of

Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

US Individual Income Tax and Transfer Taxes After US Tax Reform. STEP Israel Conference 20 June GLENN G. FOX BAKER McKENZIE, NY, NY

US Individual Income Tax and Transfer Taxes After US Tax Reform STEP Israel Conference 20 June 2018 GLENN G. FOX BAKER McKENZIE, NY, NY STANLEY BARG KOZUSKO HARRIS DUNCAN, NY, NY 1 US Estate, Gift, GST

US Individual Income Tax and Transfer Taxes After US Tax Reform STEP Israel Conference 20 June 2018 GLENN G. FOX BAKER McKENZIE, NY, NY STANLEY BARG KOZUSKO HARRIS DUNCAN, NY, NY 1 US Estate, Gift, GST

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2017 (Connecticut) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2017 (Connecticut) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your

Estate Planning Strategies for the Business Owner

National Life Group is a trade name of of National Life Insurance Company, Montpelier, VT and its affiliates. TC74345(0613)1 Estate Planning Strategies for the Business Owner Presented by: Connie Dello

National Life Group is a trade name of of National Life Insurance Company, Montpelier, VT and its affiliates. TC74345(0613)1 Estate Planning Strategies for the Business Owner Presented by: Connie Dello

The Universal Planning Tool

Trusts: The Universal Planning Tool Presented by Carla Wigen, Sr. Regional Fiduciary Manager Karen Josephson, Sr. Wealth Planner Wells Fargo Private Bank provides financial services and products through

Trusts: The Universal Planning Tool Presented by Carla Wigen, Sr. Regional Fiduciary Manager Karen Josephson, Sr. Wealth Planner Wells Fargo Private Bank provides financial services and products through

TABLE OF CONTENTS LOUISIANA GIFT AND INHERITANCE TAXES. Page 2 of 250

TABLE OF CONTENTS CHAPTER 1 COMMUNITY PROPERTY 1.01 In General 1.02 Marriage Contracts 1.03 Management of Community Property 1.04 Termination of Community 1.05 Special Property - Life Insurance - Retirement

TABLE OF CONTENTS CHAPTER 1 COMMUNITY PROPERTY 1.01 In General 1.02 Marriage Contracts 1.03 Management of Community Property 1.04 Termination of Community 1.05 Special Property - Life Insurance - Retirement

Revocable Trust Vs. Irrevocable Trust

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

Estate Planning under the New Tax Law

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Understanding the Transfer Tax and Its Impact on Estate Planning

Understanding the Transfer Tax and Its Impact on Estate Planning 2016 Skills Training for Estate Planners Sponsored by the Real Property, Trust and Estate Law Section of the American Bar Association New

Understanding the Transfer Tax and Its Impact on Estate Planning 2016 Skills Training for Estate Planners Sponsored by the Real Property, Trust and Estate Law Section of the American Bar Association New

Estate And Legacy Planning

Estate And Legacy Planning An Overview of the Estate Planning Process By: Samuel S. Stalsberg Sjoberg & Tebelius, P.A. 2145 Woodlane Drive, Suite 101 Woodbury, Minnesota 55125 Phone: 651-738-3433 sam@stlawfirm.com

Estate And Legacy Planning An Overview of the Estate Planning Process By: Samuel S. Stalsberg Sjoberg & Tebelius, P.A. 2145 Woodlane Drive, Suite 101 Woodbury, Minnesota 55125 Phone: 651-738-3433 sam@stlawfirm.com

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES 13.1 AN OVERVIEW OF SUBCHAPTER J What is a Trust? 1. A trust is an arrangement created by a will or by a lifetime declaration, through which

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES 13.1 AN OVERVIEW OF SUBCHAPTER J What is a Trust? 1. A trust is an arrangement created by a will or by a lifetime declaration, through which

Chapter 27. Income Taxation of Trusts and Estates. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 27 Income Taxation of Trusts and Estates Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Using Trusts (slide 1 of 5)

Chapter 27 Income Taxation of Trusts and Estates Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Using Trusts (slide 1 of 5)

Estate (cont.) IRC 2033 includes in the gross estate all probate assets IRC includes in the gross estate all non-probate assets

IRC 2033 includes in the gross estate all probate assets IRC includes in the gross estate all non-probate assets") Overview Certain entities are created for planning purposes. These entities are separate and apart from individuals or businesses. Income in these entities needs to be accounted for and taxed if held within

Overview Certain entities are created for planning purposes. These entities are separate and apart from individuals or businesses. Income in these entities needs to be accounted for and taxed if held within

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

Creates the trust. Holds legal title to the trust property and administers the trust. Benefits from the trust.

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Understanding the Uses of Trusts WEALTH TRANSFER OVERVIEW. The purpose of this brochure is to provide a general discussion of basic trust principles.

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Understanding the Uses of Trusts WEALTH TRANSFER OVERVIEW. The purpose of this brochure is to provide a general discussion of basic trust principles.

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning Where Were We vs. Where Are We Now 2017 2018 (Pre-Act) 2018 (Post-Act) Transfer Tax Rate 40% 40% 40% Estate/Gift Tax Exemption $5.49 million

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning Where Were We vs. Where Are We Now 2017 2018 (Pre-Act) 2018 (Post-Act) Transfer Tax Rate 40% 40% 40% Estate/Gift Tax Exemption $5.49 million

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

Charitable Trusts. Charitable Trusts

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

White Paper Trusts Overview

White Paper Overview www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents...

White Paper Overview www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents...

Bypass Trust (also called B Trust or Credit Shelter Trust)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Individual year-end planning and tax law updates

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

Bring SPF. Take CPE. JULY 6, 7, & 8. Ocean City, MD Clarion Resort Fontainebleau Hotel

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

CHAPTER 14: ESTATE PLANNING

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

Types of Trusts- The Ultimate Guide

Types of Trusts- The Ultimate Guide A/B Trusts Asset Protection Trusts By-Pass Trusts Credit Shelter Trusts Charitable Trusts Charitable Split-Interest Trusts Charitable Lead Trusts Charitable Remainder

Types of Trusts- The Ultimate Guide A/B Trusts Asset Protection Trusts By-Pass Trusts Credit Shelter Trusts Charitable Trusts Charitable Split-Interest Trusts Charitable Lead Trusts Charitable Remainder

Individual Retirement Accounts as Estate Planning Tools: Opportunities and Pitfalls

Individual Retirement Accounts as Estate Planning Tools: Opportunities and Pitfalls December 2010 This material is provided for educational purposes only. This material is not intended to constitute legal,

Individual Retirement Accounts as Estate Planning Tools: Opportunities and Pitfalls December 2010 This material is provided for educational purposes only. This material is not intended to constitute legal,

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

Law Offices of Jack S. Johal. Fall 2016 Bulletin DYNASTY TRUSTS MAY BE EVEN MORE POWERFUL AFTER CHANGES IN TRANSFER TAX

The tax and creditor protection advantages of dynasty trusts will make these trusts more attractive as family wealth preservation tools in the event of repeal of the estate and GST taxes, or if the estate

The tax and creditor protection advantages of dynasty trusts will make these trusts more attractive as family wealth preservation tools in the event of repeal of the estate and GST taxes, or if the estate

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

the Private Trust Company gain peace of mind Simplified Trust Solutions

the Private Trust Company gain peace of mind Simplified Trust Solutions What is a Trust? As the nation s leading independent broker/dealer*, LPL Financial serves the independent financial advisor with

the Private Trust Company gain peace of mind Simplified Trust Solutions What is a Trust? As the nation s leading independent broker/dealer*, LPL Financial serves the independent financial advisor with

2) An estate represents a deceased person's assets after all debts are paid. Answer: TRUE Diff: 1 Question Status: Previous edition

An estate represents a deceased person's assets after all debts are paid. Answer: TRUE Diff: 1 Question Status: Previous edition") Personal Finance, 6e (Madura) Chapter 20 Estate Planning 20.1 Purpose of a Will 1) Two key goals of estate planning are to ensure that your estate passes to the proper beneficiaries and to ensure that

Personal Finance, 6e (Madura) Chapter 20 Estate Planning 20.1 Purpose of a Will 1) Two key goals of estate planning are to ensure that your estate passes to the proper beneficiaries and to ensure that

Gregory W. Sampson Looper Reed & McGraw, P.C

Gregory W. Sampson Looper Reed & McGraw, P.C 469-320-6097 GSampson@LRMLaw.com www.lrmlaw.com 2010 Looper Reed & McGraw, P.C. The information contained herein is subject to change without notice Basic Estate

Gregory W. Sampson Looper Reed & McGraw, P.C 469-320-6097 GSampson@LRMLaw.com www.lrmlaw.com 2010 Looper Reed & McGraw, P.C. The information contained herein is subject to change without notice Basic Estate

Gift Planning Glossary of Terms

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Session 2: Estate and Tax Planning with Trusts

Session 2: Estate and Tax Planning with Trusts I. Overview a. What is a Trust? Trav Baxter i. A trust is a fiduciary arrangement that is governed by an agreement (i.e. a trust agreement) between a grantor

Session 2: Estate and Tax Planning with Trusts I. Overview a. What is a Trust? Trav Baxter i. A trust is a fiduciary arrangement that is governed by an agreement (i.e. a trust agreement) between a grantor

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

GLOSSARY. Compiled by Carolyn Paseneaux

GLOSSARY Compiled by Carolyn Paseneaux AB TRUST A trust giving a surviving spouse or mate a life estate interest in property of a deceased spouse or mate. It is used to save eventual taxes on the estate.

GLOSSARY Compiled by Carolyn Paseneaux AB TRUST A trust giving a surviving spouse or mate a life estate interest in property of a deceased spouse or mate. It is used to save eventual taxes on the estate.

Estate & Charitable Planning After the Tax Cuts & Jobs Act of 2017

Estate & Charitable Planning After the Tax Cuts & Jobs Act of 2017 by Forest J. Dorkowski, J.D., LL.M. Tual Graves Dorkowski, PLLC Sponsored by St. Jude Children s Research Hospital 2018 ALSAC/St. Jude

Estate & Charitable Planning After the Tax Cuts & Jobs Act of 2017 by Forest J. Dorkowski, J.D., LL.M. Tual Graves Dorkowski, PLLC Sponsored by St. Jude Children s Research Hospital 2018 ALSAC/St. Jude

Federal Income Tax Concepts Needed to Prepare Fiduciary Form 1041 and the Final Form 1040 of the Decedent

Michigan Society of Enrolled Agents MiSEA presents Federal Income Tax Concepts Needed to Prepare Fiduciary Form 1041 and the Final Form 1040 of the Decedent at the Bavarian Inn Lodge and Conference Center

Michigan Society of Enrolled Agents MiSEA presents Federal Income Tax Concepts Needed to Prepare Fiduciary Form 1041 and the Final Form 1040 of the Decedent at the Bavarian Inn Lodge and Conference Center

GLOSSARY OF FIDUCIARY TERMS

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

PLANNING WITH CONFIDENCE. Simplified Trust Solutions

PLANNING WITH CONFIDENCE Simplified Trust Solutions Named the largest of America s Most AdvisorFriendly Trust Companies by The Trust Advisor magazine,* we are dedicated to serving families and individual

PLANNING WITH CONFIDENCE Simplified Trust Solutions Named the largest of America s Most AdvisorFriendly Trust Companies by The Trust Advisor magazine,* we are dedicated to serving families and individual

FINANCIAL PROFESSIONAL USE ONLY NOT FOR USE WITH THE PUBLIC

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

USING TRANSAMERICA S ANNUITIES IN IRREVOCABLE TRUSTS

USING TRANSAMERICA S ANNUITIES IN IRREVOCABLE TRUSTS Annuities may lose value and are not insured by the FDIC or any federal government agency. They are not a deposit of or guaranteed by any bank, bank

USING TRANSAMERICA S ANNUITIES IN IRREVOCABLE TRUSTS Annuities may lose value and are not insured by the FDIC or any federal government agency. They are not a deposit of or guaranteed by any bank, bank

Bryan Health March 27, 2014 Wills, Trusts and Fiduciary Administration (and Other Life and Death Issues)

") CLINE WILLIAMS WRIGHT JOHNSON & OLDFATHER, L.L.P. ATTORNEYS AT LAW ESTABLISHED 1857 Bryan Health March 27, 2014 Wills, Trusts and Fiduciary Administration (and Other Life and Death Issues) Presented by:

CLINE WILLIAMS WRIGHT JOHNSON & OLDFATHER, L.L.P. ATTORNEYS AT LAW ESTABLISHED 1857 Bryan Health March 27, 2014 Wills, Trusts and Fiduciary Administration (and Other Life and Death Issues) Presented by:

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.

and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.") Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

CHARITABLE GIFTS. A charitable gift has a number of different tax benefits, which benefits differ if the gift is made during life or at death.

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

Wealth structuring and estate planning. Your vision and your legacy. Life s better when we re connected

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts. Philip M. Lindquist, Dallas, TX

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts Philip M. Lindquist, Dallas, TX Copyright 2014 by K&L Gates LLP. All rights reserved. Introduction

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts Philip M. Lindquist, Dallas, TX Copyright 2014 by K&L Gates LLP. All rights reserved. Introduction

Personal Trust Services

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

WILLS. a. If you die without a will you forfeit your right to determine the distribution of your probate estate.

WILLS 1. Do you need a will? a. If you die without a will you forfeit your right to determine the distribution of your probate estate. b. The State of Arkansas decides by statute how your estate is distributed.

WILLS 1. Do you need a will? a. If you die without a will you forfeit your right to determine the distribution of your probate estate. b. The State of Arkansas decides by statute how your estate is distributed.

TEXAS TRUST BASICS Once you have a basic understanding of trusts, you may find that a trust would make an excellent addition to your own estate plan.

TEXAS TRUST BASICS Once you have a basic understanding of trusts, you may find that a trust would make an excellent addition to your own estate plan. STEPHEN A MENDEL Houston Texas Estate Planning Attorney

TEXAS TRUST BASICS Once you have a basic understanding of trusts, you may find that a trust would make an excellent addition to your own estate plan. STEPHEN A MENDEL Houston Texas Estate Planning Attorney

ESTATE PLANNING 101:

Introduction ESTATE PLANNING 101: THE IMPORTANCE OF DEVELOPING AN ESTATE PLAN At some point, most people will contemplate estate planning. Often, this is prior to or shortly after a significant life event,

Introduction ESTATE PLANNING 101: THE IMPORTANCE OF DEVELOPING AN ESTATE PLAN At some point, most people will contemplate estate planning. Often, this is prior to or shortly after a significant life event,

Estate Planning. Insight on. Keep future options open with powers of appointment

Insight on Estate Planning October/November 2011 Keep future options open with powers of appointment A trust that keeps on giving Create a dynasty to make the most of today s exemptions Charitable IRA

Insight on Estate Planning October/November 2011 Keep future options open with powers of appointment A trust that keeps on giving Create a dynasty to make the most of today s exemptions Charitable IRA

Charitable Giving Techniques

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Estate Planning. Farm Credit East, ACA Stephen Makarevich

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 stephen.makarevich@farmcrediteast.com 1 What is Estate Planning? 2 Estate

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 stephen.makarevich@farmcrediteast.com 1 What is Estate Planning? 2 Estate

7 th Edition ESTATE PLANNING. Michael A. Dalton Thomas P. Langdon. CHAPTER 8: TRUSTS Estate Planning Money Education CH 8 Trusts

7 th Edition ESTATE PLANNING Michael A. Dalton Thomas P. Langdon CHAPTER 8: TRUSTS Introduction Trusts are used for: The management of assets Flexibility in the operation of the estate plan (except charitable

7 th Edition ESTATE PLANNING Michael A. Dalton Thomas P. Langdon CHAPTER 8: TRUSTS Introduction Trusts are used for: The management of assets Flexibility in the operation of the estate plan (except charitable

Bring SPF. Take CPE. JULY 6, 7, & 8. Ocean City, MD Clarion Resort Fontainebleau Hotel

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

Income Tax Planning Is The New Estate Tax Planning

Income Tax Planning Is The New Estate Tax Planning Potpourri of Income Tax Planning Ideas, Including State Trust Income Tax Planning and ING Trusts Keith Herman Greensfelder, Hemker & Gale, P.C. 314-345-4711

Income Tax Planning Is The New Estate Tax Planning Potpourri of Income Tax Planning Ideas, Including State Trust Income Tax Planning and ING Trusts Keith Herman Greensfelder, Hemker & Gale, P.C. 314-345-4711

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs

& Rolling GRATs") Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

ESTATE PLANNING DICTIONARY

ESTATE PLANNING DICTIONARY Administrator For estates administered prior to April 1, 2012, the fiduciary appointed by the Probate Court to settle your estate if you die without a Will (intestate). Attorney-in-fact

ESTATE PLANNING DICTIONARY Administrator For estates administered prior to April 1, 2012, the fiduciary appointed by the Probate Court to settle your estate if you die without a Will (intestate). Attorney-in-fact

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset.

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

Creative Estate Planning for Clients Under $10 Million

Creative Estate Planning for Clients Under $10 Million Presented by Missia H. Vaselaney Taft Partner October, 2017 Created by Jeremiah W. Doyle, IV, Senior Vice President, BYN Mellon Wealth Management

Creative Estate Planning for Clients Under $10 Million Presented by Missia H. Vaselaney Taft Partner October, 2017 Created by Jeremiah W. Doyle, IV, Senior Vice President, BYN Mellon Wealth Management

GOALS OF ESTATE PLANNING 12/12/2011 SUCCESSION PLANNING SUCCESSION PLANNING IMPEDIMENTS TO ACHIEVING ESTATE PLANNING GOALS

SUCCESSION PLANNING Why is succession planning so important Avoid sacrificing land for liquidity http://bit.ly/vwx5jn SUCCESSION PLANNING 1. Discuss your vision and goals for the land with your spouse

SUCCESSION PLANNING Why is succession planning so important Avoid sacrificing land for liquidity http://bit.ly/vwx5jn SUCCESSION PLANNING 1. Discuss your vision and goals for the land with your spouse

Charitable Giving Techniques

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

CHAPTER 8 Trusts DISCUSSION QUESTIONS

CHAPTER 8 Trusts DISCUSSION QUESTIONS 1. Why are trusts used in estate planning? Trusts are used in estate planning to provide for the management of assets and flexibility in the operation of the estate

CHAPTER 8 Trusts DISCUSSION QUESTIONS 1. Why are trusts used in estate planning? Trusts are used in estate planning to provide for the management of assets and flexibility in the operation of the estate

WEALTH STRATEGY REPORT

WEALTH STRATEGY REPORT The 3.8% Surtax on Investment Income - Trusts INTRODUCTION Beginning in 2013, net investment income (NII, as defined in the statute) is subject to an additional 3.8% surtax to the

WEALTH STRATEGY REPORT The 3.8% Surtax on Investment Income - Trusts INTRODUCTION Beginning in 2013, net investment income (NII, as defined in the statute) is subject to an additional 3.8% surtax to the

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

FIDUCIARY INCOME TAXES

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

Estate Planning in 2012

ESTATE PLANNING IN 2012 Overview and Goals of Estate Planning in 2012 Generally, there are three basic goals of estate, generation skipping transfer, and gift tax planning: (1) the reduction of estate

ESTATE PLANNING IN 2012 Overview and Goals of Estate Planning in 2012 Generally, there are three basic goals of estate, generation skipping transfer, and gift tax planning: (1) the reduction of estate

Understanding Dynasty Trusts

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

Understanding TRUSTS. A Summary of Trusts for Estate Planning VLC

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Section 11 Probate Glossary

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Framing Your Legacy. With Transfer Tax Certainty, It Is Time to Consider Your Estate And Life Insurance Planning MKT13-65

Framing Your Legacy With Transfer Tax Certainty, It Is Time to Consider Your Estate And Life Insurance Planning MKT13-65 This material is not intended to be used, nor can it be used by any taxpayer, for

Framing Your Legacy With Transfer Tax Certainty, It Is Time to Consider Your Estate And Life Insurance Planning MKT13-65 This material is not intended to be used, nor can it be used by any taxpayer, for

Estate Planning Basics

Your Retirement Advisor 508-798-5115 lynnt@yourretirementadvisor.com www.yourretirementadvisor.com Estate Planning Basics Page 1 of 12, see disclaimer on final page What Is Estate Planning? Estate planning

Your Retirement Advisor 508-798-5115 lynnt@yourretirementadvisor.com www.yourretirementadvisor.com Estate Planning Basics Page 1 of 12, see disclaimer on final page What Is Estate Planning? Estate planning

TABLE OF CONTENTS. Simple will with residue pouring over to inter vivos trust

TABLE OF CONTENTS Preface Form I Form II Form III Form IIIA Form IV Form V Form VI Form VII Form VIII Form IX Form IXA Form X Form XI Form XII Form XIII Form XIV Form XV Form XVI Form XVII Form XVIII Form

TABLE OF CONTENTS Preface Form I Form II Form III Form IIIA Form IV Form V Form VI Form VII Form VIII Form IX Form IXA Form X Form XI Form XII Form XIII Form XIV Form XV Form XVI Form XVII Form XVIII Form

FIDUCIARY INCOME TAX: ISSUES AND OPPORTUNITIES. Milwaukee Estate Planning Forum November 4, 2015

FIDUCIARY INCOME TAX: ISSUES AND OPPORTUNITIES Milwaukee Estate Planning Forum November 4, 2015 Attorney Philip J. Miller Whyte Hirschboeck Dudek S.C. 555 East Wells Street, Suite 1900 Milwaukee, Wisconsin

FIDUCIARY INCOME TAX: ISSUES AND OPPORTUNITIES Milwaukee Estate Planning Forum November 4, 2015 Attorney Philip J. Miller Whyte Hirschboeck Dudek S.C. 555 East Wells Street, Suite 1900 Milwaukee, Wisconsin

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Please understand that this podcast is not intended to be legal advice. As always, you should contact your WEALTH TRANSFER STRATEGIES

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

Multigenerational Retirement Distribution Planning. Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs

Multigenerational Retirement Distribution Planning Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs Overview Qualified plans, IRAs and other tax-deferred plans often constitute

Multigenerational Retirement Distribution Planning Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs Overview Qualified plans, IRAs and other tax-deferred plans often constitute

White Paper: Dynasty Trust

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

2. What will happen to my property if I die without a will or trust?

1. What is estate planning? Estate planning is the accumulation, the preservation, and the distribution of your assets. It is accomplishing your personal family goals and easing the management of your

1. What is estate planning? Estate planning is the accumulation, the preservation, and the distribution of your assets. It is accomplishing your personal family goals and easing the management of your

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens Presented by I. Richard Gershon University of Mississippi School of Law I. What is a Third-Party Special Needs Trust? A. Difference

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens Presented by I. Richard Gershon University of Mississippi School of Law I. What is a Third-Party Special Needs Trust? A. Difference

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Living Trusts to Avoid Probate. POAs. Asset Protection. HIPAAs. Health Care Directives. Divorce & Asset. Family Limited Partnerships

Asset Protection Planning Strategies Grantor Retained Annuity Section 1035 Rescues Prenuptial Planning Gift for Children BERT! The Wonder Trust Wyoming Close LLCs Sales to IDOTs Gift for Grandchildren

Asset Protection Planning Strategies Grantor Retained Annuity Section 1035 Rescues Prenuptial Planning Gift for Children BERT! The Wonder Trust Wyoming Close LLCs Sales to IDOTs Gift for Grandchildren

Estate Planning for Small Business Owners

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

ALI-ABA Course of Study Estate Planning for the Family Business Owner

425 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

425 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

Title 12 - Decedents' Estates and Fiduciary Relations. Part VI Allocation of Principal and Income

Part VI Allocation of Principal and Income Chapter 61 DELAWARE UNIFORM PRINCIPAL AND INCOME ACT Subchapter I Definitions and General Principles 61-101 Short title. Subchapters I through VI of this chapter

Part VI Allocation of Principal and Income Chapter 61 DELAWARE UNIFORM PRINCIPAL AND INCOME ACT Subchapter I Definitions and General Principles 61-101 Short title. Subchapters I through VI of this chapter

Trusts That Affect Estate Administration

Trusts That Affect Estate Administration NBI Estate Administration Boot Camp September 22-23, 2016 Baltimore, Maryland By: Jill A. Snyder, Esq. Law Office of Jill A. Snyder, LLC 410-864- 8788 1 I. When

Trusts That Affect Estate Administration NBI Estate Administration Boot Camp September 22-23, 2016 Baltimore, Maryland By: Jill A. Snyder, Esq. Law Office of Jill A. Snyder, LLC 410-864- 8788 1 I. When

Estate Planning. Uncertain Times. IRS Circular 230 Disclosure

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Introduction. 1. Bequests Charitable Gift Annuity Charitable Remainder Annuity Trust Charitable Remainder Unitrus 6-7

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.