Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

|

|

|

- Daniel Wade

- 5 years ago

- Views:

Transcription

1 FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours. To earn credit you must: Participate in the program on your own computer connection (no sharing) if you need to register additional people, please call customer service at x10 (or x10). Strafford accepts American Express, Visa, MasterCard, Discover. Listen on-line via your computer speakers. Respond to five prompts during the program plus a single verification code. You will have to write down only the final verification code on the attestation form, which will be ed to registered attendees. To earn full credit, you must remain connected for the entire program. WHO TO CONTACT DURING THE LIVE EVENT For Additional Registrations: -Call Strafford Customer Service x10 (or x10) For Assistance During the Live Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN.

2 Tips for Optimal Quality FOR LIVE PROGRAM ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please immediately so we can address the problem.

3 Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709 July 13, 2016 Tracy M. Child, J.D., LLM., Partner Joy Matak, J.D., LLM., Director Sherman Wells Sylvester & Stamelman CohnReznick

4 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

5 Gift Tax Returns What is gift tax return? If a Donor makes a gift worth more than the annual tax exclusion amount ($14,000 in 2015 and 2016), the Donor must file a gift tax return (Form 709). Who is responsible for filing gift tax return? All individuals who make a gift to another individual or entity that exceeds the annual exclusion amount must file a gift tax return. The Donor is responsible for paying the gift tax, except in certain circumstances in which IRS allows the gift recipient to pay the gift tax. What is the benefit of filing gift tax return? By filling the gift tax return, the government is formally advised of the transfer and less likely to challenge that transaction in the future. 5

6 Bea And Ben Generous 6

7 7

8 WHO IS A Donee? Each individual, trust or charity listed on Schedule A equals one donee. However, if the beneficiaries of a trust have a present interest in the gift (e.g., Crummey withdrawal rights), then each beneficiary of the trust is a donee. 8

9 Bea Generous Donees Forgiveness of indebtedness owed by Marion Money Gift to Juana B. Generous Gift to Community Foundation Charitable Organization Gift to Easy Living Qualified Personal Residence Trust Gift to Bea Generous 2013 GRAT Gift to Ivan Money 2013 Trust 529 Plan Gift to Xavier Money Non-gift disclosure of sale to Grandchildren s Generous Trust Gift to Bea Generous GST Trust for Robin Money Robin Money has a right of withdrawal Gift to Collette A. Day Gift to Generous Giving Family Trust The following three beneficiaries each have a right of withdrawal: Ben Generous Marion Money (already counted above) Owen Money Gift to Generous Dynasty Trust Gift to Ben Generous Spousal Access Trust GST Allocation to Ben Generous 2011 GRAT upon termination TOTAL: = = = = = = = = = 1 donee 1 donee 1 donee 1 donee 1 donee 1 donee 1 donee 1 donee 1 donee = = 1 donee 2 donees = = = 1 donee 1 donee 1 donee 15 donees 9

10 10

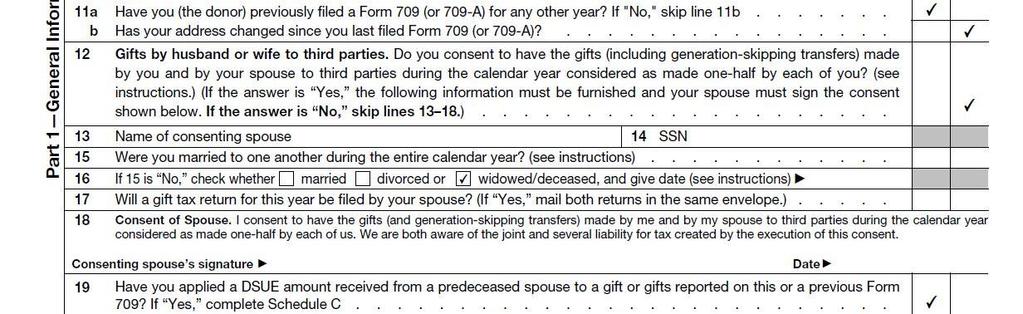

11 Basics A spouse of a donor may elect to be treated as the donor of one-half the value of the of the gifts made by the donor from the donor s separate funds. The spouse must sign the donor s gift tax return consenting to the election. If spouses choose to split gifts, they must split all eligible gifts. Spouses cannot split gifts made to a trust in which the other spouse has a beneficial interest, unless the other spouse s interest is ascertainable. 11

12 Example One Bea Generous creates a trust for the benefit of her husband, Ben Generous, and her descendants. The trustee has complete discretion to make distributions to the beneficiaries. The portion of the gift allocable to Ben is not ascertainable, so the election to split gifts to this trust would not be effective. 12

13 13

14 Example Two Bea Generous gifts $78,000 to a Crummey trust. Ben and two of Bea s children each have the right to withdraw $26,000. Because Ben s interest in the gift is ascertainable (i.e., $26,000), they may split all but $26,000 of the gift. 14

15 15

16 amount of gi split gst exemption allocation If spouses elect to split gifts and a portion of the gift cannot be split, as in the example above, the gift can still be fully split for GST exemption allocation purposes. In the example above, Ben is only reporting gifts of $28,000 to the trust beneficiaries, but he may allocate up to $42,000 of his GST exemption to the trust. 16

17 17

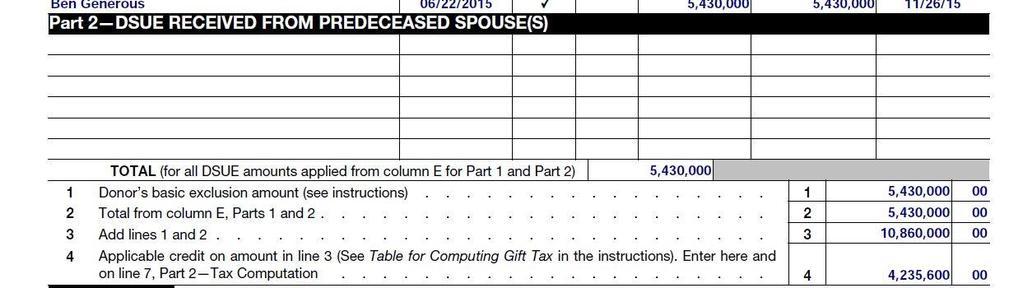

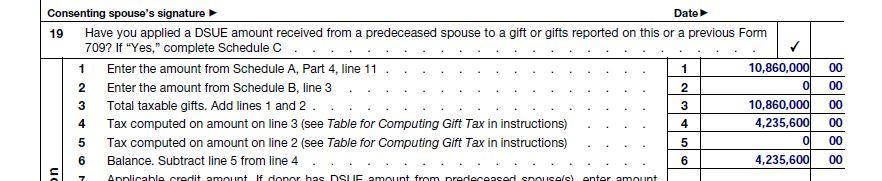

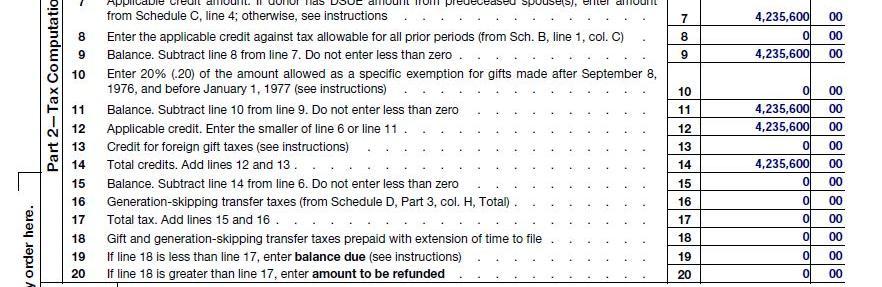

18 Deceased Spousal Unused Exclusion or Portability If a first-to-die spouse has not fully used the lifetime exclusion, the unused portion can be transferred or ported to the surviving spouse. Thereafter, for both gift and estate tax purposes, the surviving spouse s exclusion is the sum of his/her own exclusion (as such amount is inflation adjusted), plus the first-to-die s ported Deceased Spousal Unused Exclusion (DSUE) amount. Example: Ben and Bea Generous (U.S. citizens) have only been married to each other. Bea owns assets worth $5.43 million and Ben owns assets worth $5.43 million. Ben Generous dies in 2015 leaving his entire estate to Bea, using none of his lifetime exclusion. Ben s DSUE amount is $5.43 million (his exclusion of $5.43 million less the $0 used, because all of his assets were transferred to Bea, his spouse). Bea s exclusion in 2015, for gift and/or estate tax purposes, is $10.86 million (her own $5.43 million plus the $5.43 million ported DSUE amount). Bea could make gifts of $10.86 million in 2015 and fully shield those gifts from transfer. If Bea did not make gifts but died in 2015 with a $10.86 million estate, she could fully shield her estate from estate taxes. The general rule is that surviving spouse can use the DSUE amount of his/her last deceased spouse. This will be an issue only if the survivor marries again. 18

19 19

20 Schedule C Calculation of DSUE Amount 20

21 Applicable Credit Amount 21

22 Notes about DSUE Unused Generation Skipping Transfer Tax exemption cannot be used by a surviving spouse The DSUE may be affected on audit of a deceased spouse s prior gift tax returns or estate tax return, particularly in the case where closely held business interests were transferred. A surviving spouse may want to consider incorporating DSUE usage with formula gifting. 22

23 23

24 The IDGT: A Highly Effective Defective Trust Defective for Income Tax Purposes Effective for Estate Tax Purposes Income is taxable to the grantor or the beneficiaries Trust Corpus is excluded from Grantor s estate for estate tax purposes Sale to trust is a nontaxable event Taxes paid on income earned by the trust further reduces estate 24

25 IDGT: Best Ways to Break the Rules 674(a)- power to control beneficial enjoyment 675(1) power to deal with trust assets for less than full & adequate consideration 675(2) specific power of grantor to borrow trust assets without adequate security or adequate interest 675(3) actual borrowing of trust assets by the Grantor 675(4)(C) - power to substitute assets (exercisable in Non-Fiduciary capacity) 25

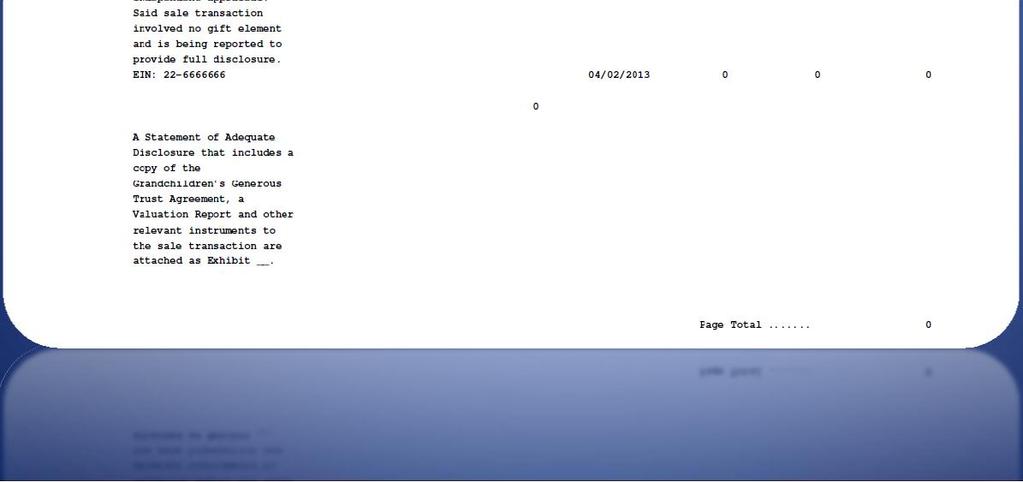

26 Sale to IDGT 1. Grantor makes seed gift of at least 10% (as a rule of thumb) of the purchase price to be paid by the IDGT 2. Grantor sells asset with expected future appreciation to IDGT 3. IDGT pays for asset with a Promissory Note, using the current applicable federal rate 4. No income tax on sale of asset to IDGT 5. Adequately disclose non-sale transaction on timely filed gift tax return 26

27 27

28 Statute of Limitations Generally, the IRS must assess tax within three years after a return is filed. If the value of omitted gifts exceeds 25% of the total amount of gifts reported on the return, the statute of limitations is six years. There is no statute of limitations barring assessment if no return is filed or if the return is false or fraudulent. The statute of limitations does not apply to gifts that are not adequately disclosed. 28

29 Adequate Disclosure Safe Harbor For Gifts A gift will generally be adequately disclosed if the return is full and complete and the return or an attached statement includes the following: A description of the transferred property and any consideration received by the donor; The identity of, and relationship between the donor and each donee; If the property is transferred to a trust, the trust s employer identification number and a brief description of the terms of the trust or a copy of the trust; and Either a qualified appraisal or detailed description of the method used to determine the fair market value of the gift. A statement describing any position taken that is contrary to any proposed, temporary or final Treasury regulations or revenue rulings published at the time of the transfer. 29

30 Qualified Appraiser Treas. Reg. Sect (c)(5)(iv) Qualified Appraiser CANNOT be: Transferor or Member of Transferor s/transferee s Family Party to the transaction Persons or business entities receiving or purchasing the transferred property Employee of a person or organization listed above Related Party as defined in IRC Sect. 267(c) Appraiser regularly used by excluded person who does not perform majority of appraisals for others 30

31 Disclosure of Non-Gift Transactions Non-gift transactions may be reported on a gift tax return to start the statute of limitations in which the IRS must determine if a taxable gift was in fact made. In order for a non-gift transaction to be considered adequately disclosed, it must meet all of the disclosure requirements for gifts listed above, plus an explanation as to why the transfer is not a transfer by gift under the Internal Revenue Code must be included. 31

32 32

33 Sample Statement of Disclosure 33

34 34

35 Generation Skipping Tax & Skip Person What is the Generation Skipping Tax? Generation-skipping transfer tax imposes a tax on both outright gifts and transfers in trust to or for the benefit of skip person. Who is a Skip Person? A skip person is a natural person assigned to a generation which is 2 or more generations below the generation assignment of the transferor (donor), or A trust, if all interests in such trust are held by skip person, or No person holds an interest in the trust, and at no time after the transfer to the trust, may a distribution be made to a non skip person. 35

36 Generation Assignment Unrelated Beneficiaries Related Beneficiaries Grantor's Parent Grantor's Uncles/Aunts Grantor Grantor's Brother/Sister Grantor's Cousin Grantor's Child Grantor's Nephew/Niece Cousin's Child Grantor's Grandchild Grantor's Grand Nephew/Niece Cousin's Grand Child 36

37 Direct skip vs. Indirect skip A direct skip is a property transfer made to a skip person that is subject to an estate of gift tax. An example of a direct skip would b a grandmother gifting property to a grandchild. The transferor, or his or her estate, is responsible for paying the GST tax for direct skips. Indirect skips involve transfers that have intermediate steps before reaching a skip person. There are two types of indirect skips, the taxable termination and the taxable distribution. Grandparent Grand Child Upon the death of child Trust with income beneficiary as child 37

38 What is GST Exemption (IRC Section 2632)? Under section 2631(a) each individual is allowed to give away during his or her lifetime up to $5,430,000 (for year 2015) without any federal gift or estate taxes due to the historically high exemption for federal transfer tax purposes. The same exemption amount applies for generation-skipping transfer (GST) tax purposes this year. Under section 2632(a), an allocation of an individual s GST exemption may be made at any time on or before the date prescribed for filing the estate tax return for the individual s estate (determined with regard to extensions). 38

39 Deemed Allocation IRC Sect. 2632(b) Section 2632 also provides deemed allocation rules pursuant to which an individual s available GST exemption is automatically allocated to certain kinds of transfers, without any action on the part of the transferor. Under section 2632(b), an individual s unused GST exemption is automatically allocated to transfers made during that individual s lifetime that are direct skips as defined in section 2612(c), to the extent necessary to make the inclusion ratio zero for the property transferred. The unused portion of an individual s GST exemption is that portion of such exemption which has not previously been allocated by such individual 39

40 GST Annual Exclusion Currently $14,000 Available to direct skips Available to trust if: During the life of the beneficiary, no distributions may be made to anyone but the beneficiary; and At the beneficiary's death, the trust assets will be included in the beneficiary s gross estate. 40

41 GST Annual Exclusion 41

42 Automatic Allocation IRC Sect. 2632(c) Under section 2632(c), in the case of a lifetime transfer made after December 31, 2000, that is an indirect skip, the transferor s available GST exemption is automatically allocated to the transfer to the extent necessary to make the inclusion ratio zero for the property transferred. Under section 2632(c)(5)(A)(i)(I), an individual may elect out of the deemed allocation rules so that GST exemption will not be allocated automatically to a particular transfer that is an indirect skip. Under section 2632(c)(5)(B)(i), this election out with regard to a particular indirect skip shall be deemed timely if made on a timely filed gift tax return for the calendar year in which the transfer was made, or deemed to have been made under section 2632(c)(4) with regard to trusts subject to an estate tax inclusion period, or on such later dates as may be prescribed in regulations. 42

43 Automatic Allocation Rules Direct skips Indirect: GST trusts A GST trust is a trust that could have a taxable termination or taxable distribution unless certain exceptions apply. Note: A conventional insurance trust where the spouse is a beneficiary and that provides for the possibility of trusts for descendents after the spouse s death is a GST trust. 43

44 IRC 2632(c)(3)(B) Definition of a GST Trust A Trust is a GST Trust unless: More than 25% of corpus distributable to non-skip person before such person attains the age of 46 More than 25% of corpus distributable to non-skip persons living on date of death of another person who is more than 10 years old than such non-skip persons More than 25% of corpus subject to general power of appointment held by non-skip persons Any portion of trust includable in estate of non-skip person if such person died immediately after transfer Certain types of charitable trusts (i.e. CLATs) 44

45 Sample Gift to Dynasty Trust 45

46 Opt Out / Opt In of Automatic Allocation The method for opting in or out of automatic allocation is the same. Check the 2632 election box. Attach a statement to the return that includes a description of the transfer and the extent to which the automatic allocation is to apply (or not apply). An election can be made for all future transfers to a particular trust (you can subsequently elect to have the allocation rules apply). Once an election is made, it is irrevocable after the due date of the return. 46

47 Timely vs. Late GST Allocations For timely allocations, the date-of-gift value is used. For late allocations, the value as of the first of the month when the return is filed is used. 47

48 Example Bea Generous makes a $150,000 gift to the Generous Dynasty Trust in 2009 but did not allocate GST Exemption on the gift tax return. Bea files a gift tax return in February 2014 in order to allocate GST exemption to the trust. Bea must use the value of the trust assets on February 1, 2014 to fully allocate GST exemption to the trust. 48

49 Late Allocations of GST Exemption Procedural Requirements File a Form 709 for the year of the transfer to the trust, regardless of whether a Form 709 had been previously filed for that year. State at the top of the Form 709 that the return is FILED PURSUANT TO REV. PROC Report on the Form 709 the value of the transferred property as of the date of the transfer. Allocate GST exemption to the trust by attaching a statement to the Form 709 entitled Notice of Allocation. The notice of allocation must contain the following information: clear identification of the trust, including the trust s identifying number, as defined in 6109 and the regulations thereunder, when applicable; the value of the property transferred as of the date of the transfer (adjusted to account for split gifts, if any); the amount of taxpayer s unused GST exemption at the time this Notice of Allocation is filed (taxpayers are reminded that they must have unused GST exemption at the time this Notice of Allocation is filed); the amount of GST exemption allocated to the transfer; the inclusion ratio of the trust after the allocation; and a statement that all of the requirements of section 3.01 of this revenue procedure have been met. 49

50 Important Remember to adjust the amount of GST exemption used in prior periods in which a gift tax return was not filed. 50

51 Example On her 2008 gift tax return, Bea Generous opted to have GST exemption allocated to all future gifts made to a Crummey trust. During 2009, 2010, 2011 and 2012, Bea only made annual exclusion gifts to the trust in the amount of $120,000, so she did not file gift tax returns for these years. When Bea files her 2013 return, the amount of GST exemption used for prior years should be increased by $480,000 (4 years x $120,000 per year), the amount automatically allocated during 2009, 2010, 2011 and

52 52

53 Overview of GRAT Under the terms of a grantor retained annuity trust ( GRAT ), a grantor transfers property to an irrevocable trust. Every year for a specified number of years (the annuity term ), the trustee pays the grantor a fixed annuity amount. The Annuity Amount which is expressed as a percentage of the initial fair market value of the property transferred to the GRAT is set so that the present value of the amount to be paid to the grantor over the annuity term equals the amount transferred to the GRAT, plus an assumed rate of return. At the end of the annuity term, the GRAT may continue to hold in trust property remaining in the GRAT (if any) for the benefit of persons other than the grantor (e.g., the grantor s children) on such terms as the grantor specifies in the trust instrument. The GRAT may distribute any remaining trust property outright to persons named in the trust instrument. 53

54 Zero-ing Out The GRAT A GRAT is zeroes out for gift tax purposes when the annuity amount paid by the trustee to the grantor is equal to the amount transferred to the GRAT. The result of such a zeroed-out GRAT is that any appreciation in the value of the property contributed to the GRAT in excess of an assumed rate of return can be distributed to the named beneficiaries at the end of the annuity term without any gift tax. If the property placed in the GRAT does not appreciate, or appreciates at a rate lower than the assumed rate of return, all of the property placed in the GRAT will be paid back to the grantor during the annuity term and nothing will be left for the intended beneficiaries. 54

55 Grantor Retained Annuity Trust Reporting on Schedule A part 1 55

56 Grantor Retained Annuity Trust Reporting on Schedule A part 3 56

57 57

58 Overview of ETIP An ETIP is the period during which, should death occur, the value of transferred property would be includible (other than by reason of section 2035) in the gross estate of (A) The transferor; or (B) The spouse of the transferor. The value of transferred property is not considered as being subject to inclusion in the gross estate of the transferor or the spouse of the transferor: If the possibility that the property will be included is so remote as to be negligible. A possibility is so remote as to be negligible if it can be ascertained by actuarial standards that there is less than a 5 percent probability that the property will be included in the gross estate. If the spouse possesses with respect to any transfer to the trust, a right to withdraw no more than the greater of $5,000 or 5 percent of the trust corpus, and such withdrawal right terminates no later than 60 days after the transfer to the trust. 58

59 Termination of an ETIP An ETIP terminates on the first to occur of: The death of the transferor The time at which no portion of the property is includible in the transferor's gross estate (other than by reason of section 2035) or, in the case of an individual who is a transferor solely by reason of an election under section 2513, the time at which no portion would be includible in the gross estate of the individual's spouse (other than by reason of section 2035) The time of a GST, but only with respect to the property involved in the GST; or In the case of an ETIP arising by reason of an interest or power held by the transferor's spouse and at the first to occur of (A) The death of the spouse; or (B) The time at which no portion of the property would be includible in the spouse's gross estate (other than by reason of section 2035). 59

60 Thank You For Attending! This presentation was not intended or written to be used, and cannot be used by any taxpayer, for the purpose of avoiding penalties under U.S. federal tax law. 60

61 Tracy M. Child, JD, LLM Sherman Wells Sylvester & Stamelman LLP 54 West 40th Street New York, NY Tracy Child is a partner at the law firm of Sherman Wells Sylvester & Stamelman, a New Jersey based full service firm. She is a member of the Firm s Trusts & Estates Group, where she assists individuals and families with a broad range of estate planning, estate administration, family business succession planning and related tax work. In the course of doing so, Tracy counsels clients on establishing an estate plan that meets their needs and objectives as tax-efficiently as possible. Prior to attending law school, Tracy was a senior tax associate with Deloitte and Touche LLP and at Arthur Andersen LLP. Tracy also serves as the partner-in-charge of the Firm s New York office. 61

62 Joy Matak, JD, LLM CohnReznick LLP 4 Becker Farm Road P.O. Box 954 Roseland, NJ joy.matak@cohnreznick.com Joy Matak, JD, LLM, is a tax director at CohnReznick and a member of the Firm s National Trusts and Estates Practice. Joy has more than 18 years of diversified experience with an extensive background in providing tax services to multigenerational wealth families, owners of closely-held businesses, and high-net-worth individuals and their trusts and estates. Joy has significant expertise providing her clients with diverse wealth transfer strategy planning to accomplish estate planning and business succession goals. She also performs tax compliance, including gift tax, estate tax, and income tax returns for trusts and estates, as well as consulting services related to generation skipping, including transfer tax planning, asset protection, life insurance structuring, and post-mortem planning. 62

Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

PREPARING GIFT TAX RETURNS

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Mastering GST Elections and Reporting: Minimizing Generation-Skipping Transfer Tax Through Indirect Skips

FOR LIVE PROGRAM ONLY Mastering GST Elections and Reporting: Minimizing Generation-Skipping Transfer Tax Through Indirect Skips TUESDAY, FEBRUARY 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Mastering GST Elections and Reporting: Minimizing Generation-Skipping Transfer Tax Through Indirect Skips TUESDAY, FEBRUARY 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Grantor Trusts After Divorce: Tax Reform, Fiduciary Challenges, and Minimizing Tax for Trust Transfers to Former Spouse Gift Tax Exemption on Divorce

Presenting a live 90-minute webinar with interactive Q&A Grantor Trusts After Divorce: Tax Reform, Fiduciary Challenges, and Minimizing Tax for Trust Transfers to Former Spouse Gift Tax Exemption on Divorce

Federal Estate, Gift and GST Taxes

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

A Primer on Portability

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Recent Developments in the Estate and Gift Tax Area. Annual Business Plan and the Proposed Regulations under Section 2642

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

Specialty Law Columns Estate and Trust Forum The Perilous Federal Gift Tax Return--Part II by Thomas L. Stover

The Colorado Lawyer December 1999 Vol. 28, No. 12 [Page 39] 1999 The Colorado Lawyer and Colorado Bar Association. All Rights Reserved. Specialty Law Columns Estate and Trust Forum The Perilous Federal

The Colorado Lawyer December 1999 Vol. 28, No. 12 [Page 39] 1999 The Colorado Lawyer and Colorado Bar Association. All Rights Reserved. Specialty Law Columns Estate and Trust Forum The Perilous Federal

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset.

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

IMPORTANT INFORMATION

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Estate Planning With Grantor Trusts: Leveraging GRATs and IDGTs to Minimize Taxes, Preserve and Transfer Assets

Presenting a live 90-minute webinar with interactive Q&A Estate Planning With Grantor Trusts: Leveraging GRATs and IDGTs to Minimize Taxes, Preserve and Transfer Assets THURSDAY, OCTOBER 15, 2015 1pm Eastern

Presenting a live 90-minute webinar with interactive Q&A Estate Planning With Grantor Trusts: Leveraging GRATs and IDGTs to Minimize Taxes, Preserve and Transfer Assets THURSDAY, OCTOBER 15, 2015 1pm Eastern

Tax Implications of Family Wealth Transfers

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

ESTATE PLANNING OPPORTUNITIES UNDER THE TAX RELIEF ACT OF

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS Mark Scott, Principal Kaufman Rossin Miami, FL January 19, 2019 #1 KNOW YOUR STARTING POINT Analyze Prior Gift

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS Mark Scott, Principal Kaufman Rossin Miami, FL January 19, 2019 #1 KNOW YOUR STARTING POINT Analyze Prior Gift

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015 Danielle R. Greene Loring, Wolcott & Coolidge Trust,

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015 Danielle R. Greene Loring, Wolcott & Coolidge Trust,

The Grandparent Tax Monica Haven, EA, JD, LLM 2015

The Grandparent Tax Monica Haven, EA, JD, LLM 2015 The Grandparent Tax Plan A Grandpa gifts $10 million to Dad $4 million tax Dad gifts $6 million to Grandson $2.4 million tax Net Gift to Grandson = $3.6

The Grandparent Tax Monica Haven, EA, JD, LLM 2015 The Grandparent Tax Plan A Grandpa gifts $10 million to Dad $4 million tax Dad gifts $6 million to Grandson $2.4 million tax Net Gift to Grandson = $3.6

Estate Planning for Small Business Owners

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Tricks and Traps of Planning and Reporting Generation-Skipping Transfers

Tricks and Traps of Planning and Reporting Generation-Skipping Transfers Diana S.C. Zeydel Greenberg Traurig, P.A. Miami, Florida GREENBERG TRAURIG, LLP ATTORNEYS AT LAW WWW.GTLAW.COM 2013 Greenberg Traurig,

Tricks and Traps of Planning and Reporting Generation-Skipping Transfers Diana S.C. Zeydel Greenberg Traurig, P.A. Miami, Florida GREENBERG TRAURIG, LLP ATTORNEYS AT LAW WWW.GTLAW.COM 2013 Greenberg Traurig,

Estate and gift tax provision highlights

Legislative Update Tax Cuts and Jobs Act Estate and gift tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key provisions

Legislative Update Tax Cuts and Jobs Act Estate and gift tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key provisions

1.0 Law & Legal CLE Credit A/V Approval # Recording Date October 19, 2017 Recording Availability October 12, 2018

1.0 Law & Legal CLE Credit A/V Approval #1082780 Recording Date October 19, 2017 Recording Availability October 12, 2018 Meeting Location Date Time Topic King County Bar Association 1200 Fifth Avenue -

1.0 Law & Legal CLE Credit A/V Approval #1082780 Recording Date October 19, 2017 Recording Availability October 12, 2018 Meeting Location Date Time Topic King County Bar Association 1200 Fifth Avenue -

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Estate Tax Planning Opportunities in 2012 Maximizing Benefits Under Current Gift and Estate Tax Law: Portability, Lifetime Exemptions, Trust Use

Presenting a live 90-minute webinar with interactive Q&A Estate Tax Planning Opportunities in 2012 Maximizing Benefits Under Current Gift and Estate Tax Law: Portability, Lifetime Exemptions, Trust Use

New Accounting Method Rules for Small Business Taxpayers Under IRC 448

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX

CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX January 2013 JANUARY 2013 CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX Dear Clients and Friends: On January 2, 2013,

CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX January 2013 JANUARY 2013 CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX Dear Clients and Friends: On January 2, 2013,

Gift Taxes. An overlooked law

Gift Taxes An overlooked law By Patricia J. Villano, CPA, MBA, AEP and Joseph L. LiPari, CPA, MBA Gift taxes are too often an overlooked area of tax law. Most clients aren t aware the tax exists and are

Gift Taxes An overlooked law By Patricia J. Villano, CPA, MBA, AEP and Joseph L. LiPari, CPA, MBA Gift taxes are too often an overlooked area of tax law. Most clients aren t aware the tax exists and are

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Tax Planning and Reporting for Partnership Equity Compensation Grants

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets

Presenting a live 90-minute webinar with interactive Q&A Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets WEDNESDAY, MARCH

Presenting a live 90-minute webinar with interactive Q&A Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets WEDNESDAY, MARCH

Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis

Presenting a live 90-minute webinar with interactive Q&A Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis TUESDAY, JUNE 28, 2016 1pm Eastern 12pm

Presenting a live 90-minute webinar with interactive Q&A Springing the Delaware Tax Trap: Drafting Limited Powers of Appointment to Increase Asset Income Tax Basis TUESDAY, JUNE 28, 2016 1pm Eastern 12pm

WEALTH STRATEGIES. GRATs and Sale to IDGTs: Estate Freeze Techniques

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA GRATs and Sale to IDGTs: Estate Freeze Techniques FREQUENTLY ASKED QUESTIONS ESTATE PLANNING How do two of the techniques used by wealthy clients

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA GRATs and Sale to IDGTs: Estate Freeze Techniques FREQUENTLY ASKED QUESTIONS ESTATE PLANNING How do two of the techniques used by wealthy clients

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

IRC 645 Elections for Qualified Revocable Trusts: Mastering the DNI Separate Share Calculation Rules

FOR LIVE PROGRAM ONLY IRC 645 Elections for Qualified Revocable Trusts: Mastering the DNI Separate Share Calculation Rules THURSDAY, JUNE 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY IRC 645 Elections for Qualified Revocable Trusts: Mastering the DNI Separate Share Calculation Rules THURSDAY, JUNE 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law

Presenting a live 90-minute webinar with interactive Q&A Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law WEDNESDAY, FEBRUARY 7, 2018 1pm Eastern 12pm Central 11am Mountain

Presenting a live 90-minute webinar with interactive Q&A Estate Planning and Tax Reform: Wealth Transfer Structures Under the New Tax Law WEDNESDAY, FEBRUARY 7, 2018 1pm Eastern 12pm Central 11am Mountain

Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012

Month Year Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012 BY RENEE M. GABBARD, LISA M. LAFOURCADE & MEGAN S. ACOSTA It appears that the current favorable estate, gift

Month Year Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012 BY RENEE M. GABBARD, LISA M. LAFOURCADE & MEGAN S. ACOSTA It appears that the current favorable estate, gift

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform

and Form 1041 Trust Deduction Rules Post-Tax Reform") New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Specialty Law Columns Estate and Trust Forum The Perilous Federal Gift Tax Return--Part I by Thomas L. Stover

The Colorado Lawyer November 1999 Vol. 28, No. 11 [Page 71] 1999 The Colorado Lawyer and Colorado Bar Association. All Rights Reserved. Editor's Note: Specialty Law Columns Estate and Trust Forum The Perilous

The Colorado Lawyer November 1999 Vol. 28, No. 11 [Page 71] 1999 The Colorado Lawyer and Colorado Bar Association. All Rights Reserved. Editor's Note: Specialty Law Columns Estate and Trust Forum The Perilous

KEVIN MATZ & ASSOCIATES PLLC

KEVIN MATZ & ASSOCIATES PLLC An abridged version of this article was published in the February 2013 issue of Tax Stringer. So What Does It Mean To Have a Permanent Estate and Gift Tax System Anyway? --

KEVIN MATZ & ASSOCIATES PLLC An abridged version of this article was published in the February 2013 issue of Tax Stringer. So What Does It Mean To Have a Permanent Estate and Gift Tax System Anyway? --

Memorandum. LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes. 1. Overview of Federal Transfer Tax System

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS Brian Malec Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth P.A. Orlando, FL Mark Scott Kaufman Rossin Miami,

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS Brian Malec Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth P.A. Orlando, FL Mark Scott Kaufman Rossin Miami,

S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Law.com Home Newswire LawJobs CLE Center LawCatalog Our Sites Advertise

Page 1 of 6 Law.com Home Newswire LawJobs CLE Center LawCatalog Our Sites Advertise Home Advertising Classifieds Public Notices About Contact Free Limited Access Home > This Week's News > Free: Estate

Page 1 of 6 Law.com Home Newswire LawJobs CLE Center LawCatalog Our Sites Advertise Home Advertising Classifieds Public Notices About Contact Free Limited Access Home > This Week's News > Free: Estate

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS The Estate Planning Council of Greater Miami October 20, 2016 Louis Nostro, Esquire Nostro Jones, P.A. Miami, Florida lnostro@nostrojones.com

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS The Estate Planning Council of Greater Miami October 20, 2016 Louis Nostro, Esquire Nostro Jones, P.A. Miami, Florida lnostro@nostrojones.com

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ Fax

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

11/9/2012. Estate and Charitable Planning Before the End of IRS Circular 230. Historical Estate Tax Rates and Exemptions

Estate and Charitable Planning Before the End of 2012 SOL S. REIFER, J.D., LL.M. KYLE C. POST, J.D., LL.M. WRIGHT GINSBERG BRUSILOW P.C. 14755 PRESTON ROAD, SUITE 600 DALLAS, TEXAS 75254 972-788-1600 sreifer@wgblawfirm.com

Estate and Charitable Planning Before the End of 2012 SOL S. REIFER, J.D., LL.M. KYLE C. POST, J.D., LL.M. WRIGHT GINSBERG BRUSILOW P.C. 14755 PRESTON ROAD, SUITE 600 DALLAS, TEXAS 75254 972-788-1600 sreifer@wgblawfirm.com

THE GST TAX A DEEP DIVE: WHAT EVERY DEVELOPMENT OFFICER NEEDS TO KNOW

THE GST TAX A DEEP DIVE: WHAT EVERY DEVELOPMENT OFFICER NEEDS TO KNOW Nancy E. Dempze Charles R. Platt Hemenway & Barnes LLP Boston, Massachusetts 960826 Hemenway & Barnes 2014 Background Transfer Taxes

THE GST TAX A DEEP DIVE: WHAT EVERY DEVELOPMENT OFFICER NEEDS TO KNOW Nancy E. Dempze Charles R. Platt Hemenway & Barnes LLP Boston, Massachusetts 960826 Hemenway & Barnes 2014 Background Transfer Taxes

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.

and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.") Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Memorandum FILE. Naim D. Bulbulia, Esq. Estate Planning Primer

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Session 1: Estate Planning Hot Topics: 2016

Session 1: Estate Planning Hot Topics: 2016 Christopher T. Rogers In this presentation we will review several current estate planning/estate tax topics, including (i) an introduction to the Beneficiary

Session 1: Estate Planning Hot Topics: 2016 Christopher T. Rogers In this presentation we will review several current estate planning/estate tax topics, including (i) an introduction to the Beneficiary

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Estate Planning under the New Tax Law

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

PREPARING THE 709 AND ALLOCATING THE GST EXEMPTION

The Blum Firm, P.C. 420 Throckmorton, Suite 650, Fort Worth, Texas 76102 Attorneys at Law (817) 334-0066 fax (817) 334-0078 PREPARING THE 709 AND ALLOCATING THE GST EXEMPTION TEXAS SOCIETY OF CERTIFIED

The Blum Firm, P.C. 420 Throckmorton, Suite 650, Fort Worth, Texas 76102 Attorneys at Law (817) 334-0066 fax (817) 334-0078 PREPARING THE 709 AND ALLOCATING THE GST EXEMPTION TEXAS SOCIETY OF CERTIFIED

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

IRC Section 734 Adjustments: Applying the 754 Election to Distributions of Partnership Property

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Strategies for Reducing Wealth and Transfer Taxes. By, Pattie S. Christensen, Esq

Strategies for Reducing Wealth and Transfer Taxes By, Pattie S. Christensen, Esq A. Lifetime Gifts The current gift tax program permits a person to transfer up to $13,000 worth of gifts of a present interest

Strategies for Reducing Wealth and Transfer Taxes By, Pattie S. Christensen, Esq A. Lifetime Gifts The current gift tax program permits a person to transfer up to $13,000 worth of gifts of a present interest

Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

Advanced Wealth Transfer Strategies

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Understanding the Transfer Tax and Its Impact on Estate Planning

Understanding the Transfer Tax and Its Impact on Estate Planning 2016 Skills Training for Estate Planners Sponsored by the Real Property, Trust and Estate Law Section of the American Bar Association New

Understanding the Transfer Tax and Its Impact on Estate Planning 2016 Skills Training for Estate Planners Sponsored by the Real Property, Trust and Estate Law Section of the American Bar Association New

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Estate Planning. Uncertain Times. IRS Circular 230 Disclosure

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment THURSDAY, FEBRUARY 21, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment THURSDAY, FEBRUARY 21, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

ESTATE PLANNING 1 / 11

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Adaptable Planning Advice and Beyond. Louisiana Estate Planning Council March 8, All Rights Reserved

Adaptable Planning Advice for 2012 and Beyond Louisiana Estate Planning Council March 8, 2012 Charles Douglas All Rights Reserved Who said? It is not the strongest of the species that survives, nor the

Adaptable Planning Advice for 2012 and Beyond Louisiana Estate Planning Council March 8, 2012 Charles Douglas All Rights Reserved Who said? It is not the strongest of the species that survives, nor the

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

TRUSTS & ESTATES ADVISORY

Estate Planning Techniques In A Low Interest Rate Environment Interest rates remain at historic lows and it seems that rates will not be rising as quickly as most commentators once thought. Consequently,

Estate Planning Techniques In A Low Interest Rate Environment Interest rates remain at historic lows and it seems that rates will not be rising as quickly as most commentators once thought. Consequently,

Planning After ATRA: The CPA s Guide to Financial and Estate Planning Portability A Planning Game-Changer But Not as Simple as It Appears

Planning After ATRA: The CPA s Guide to Financial and Estate Planning Portability A Planning Game-Changer But Not as Simple as It Appears Presented by: Steven G. Siegel, JD, LLM 1 Introduction About the

Planning After ATRA: The CPA s Guide to Financial and Estate Planning Portability A Planning Game-Changer But Not as Simple as It Appears Presented by: Steven G. Siegel, JD, LLM 1 Introduction About the

GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper

![GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper](/thumbs/89/98748865.jpg "GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper") GIFTING A Private Clients Group White Paper Among the goals of most comprehensive estate plans is the reduction of federal and state inheritance taxes. For this reason, a carefully prepared Will or Revocable

GIFTING A Private Clients Group White Paper Among the goals of most comprehensive estate plans is the reduction of federal and state inheritance taxes. For this reason, a carefully prepared Will or Revocable

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

MARKET TREND: With the enactment of exemption portability, clients may dismiss the need for lifetime estate planning, to their detriment.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Issuance of Temporary Portability Regulations - Practical

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Issuance of Temporary Portability Regulations - Practical

The BDIT (Beneficiary Defective Inheritor's Trust)

") Estate Planning Hot Topics: 2016 (Beneficiary Defective Inheritor's Trust) Is a version of the Intentionally Defective Grantor Trust Grantor (Parent): (a) creates trust fbo next generation and (b) Grantor/Parent

Estate Planning Hot Topics: 2016 (Beneficiary Defective Inheritor's Trust) Is a version of the Intentionally Defective Grantor Trust Grantor (Parent): (a) creates trust fbo next generation and (b) Grantor/Parent

Intentionally Defective (?) Grantor Trusts

Grantor Trusts") Intentionally Defective (?) Grantor Trusts Owen@GivnerKaye.com 1 What We Will Cover [Part 1]: 1. How Did The Grantor Trust Rules Originate? P. 3 2. Common Examples of Grantor Trusts. P. 4 3. What Do We

Intentionally Defective (?) Grantor Trusts Owen@GivnerKaye.com 1 What We Will Cover [Part 1]: 1. How Did The Grantor Trust Rules Originate? P. 3 2. Common Examples of Grantor Trusts. P. 4 3. What Do We

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reunion Weekend 2018

Presented by B. Howard Pearson, J.D. Lecturer, Stanford University Law School Development Legal Counsel and Senior Philanthropic Advisor Stanford University Reunion Weekend 2018 2 Changes Affecting Estate

Presented by B. Howard Pearson, J.D. Lecturer, Stanford University Law School Development Legal Counsel and Senior Philanthropic Advisor Stanford University Reunion Weekend 2018 2 Changes Affecting Estate

BASIC ESTATE PLANNING FOR YOU AND YOUR CLIENTS

BASIC ESTATE PLANNING FOR YOU AND YOUR CLIENTS I. INTRODUCTION The purpose of this manuscript is to revisit basic estate planning concepts and techniques. The manuscript will revisit basic estate planning

BASIC ESTATE PLANNING FOR YOU AND YOUR CLIENTS I. INTRODUCTION The purpose of this manuscript is to revisit basic estate planning concepts and techniques. The manuscript will revisit basic estate planning

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax MARKET TREND: As planning approaches and products become more complex, care must be taken to avoid the retention or acquisition

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax MARKET TREND: As planning approaches and products become more complex, care must be taken to avoid the retention or acquisition