Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral

|

|

|

- Elizabeth Hunt

- 6 years ago

- Views:

Transcription

1 Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you must: Participate in the program on your own computer connection (no sharing) if you need to register additional people, please call customer service at x10 (or x10). Strafford accepts American Express, Visa, MasterCard, Discover. Listen on-line via your computer speakers. Respond to five prompts during the program plus a single verification code. You will have to write down only the final verification code on the attestation form, which will be ed to registered attendees. To earn full credit, you must remain connected for the entire program. WHO TO CONTACT For Additional Registrations: -Call Strafford Customer Service x10 (or x10) For Assistance During the Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN.

2 Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please immediately so we can address the problem. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

3 Section 1202 Qualified Small Business Stock Aug. 27, 2015 Christopher A. Karachale Hanson Bridgett LLP Raymond L. Leung Leung Louie Ip & Co. David B. Strong Morrison & Foerster

4 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

5 Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral Strafford Webinar CLE Program Thursday, August 27 th, 2015 (1:00-2:50pm EDT) Presented by: David B. Strong Christopher A. Karachale Raymond L. Leung, CPA Partner Senior Counsel Leung, Louie Ip & Co. Co-Chair Tax Practice Hanson Bridgett, LLP Daly City, CA Morrison & Foerster, LLP San Francisco, CA Denver, CO / New York, NY

6 Outline of Presentation 1. Executive Summary 2. General Benefits and Eligibility 3. Overview of Section 1202 / QSBS Requirements 4. Corporate Stock Acquired at Original Issuance 5. Qualified Small Business Requirement 6. Active Business Requirement 7. Five-Year Holding Period Requirement 8. Amount of Gain Subject to Exclusion 9. Potential Rollover of Gain Section Practical Planning Considerations 11. Examples / Reporting 6

7 1. Executive Summary 7

8 Section 1202 / QSBS This presentation provides general information regarding U.S. federal income tax incentives available to non-corporate holders of qualified small business stock ( QSBS or QSB stock ) as defined under Section 1202 of the Internal Revenue Code. In general, under current law Section 1202 allows a non-corporate taxpayer to potentially exclude up to 100% of the gain realized from the sale or exchange of QSB stock held for more than five years. In addition, Section 1045 allows a taxpayer to potentially roll-over gain from the sale of QSB stock that has been held for more than 6 months. Unless otherwise specified, all Section references are to the U.S. Internal Revenue Code of 1986, as amended (the Code ), or applicable Treasury Regulations promulgated thereunder. 8

9 2. General Benefits and Eligibility a. Determining the amount of the exclusion b. Stock held by a non-corporate taxpayer in a qualifying C-corporation 9

10 Determining the amount of the exclusion The exclusion for QSBS is currently 50% (subject to the AMT), but the 100% exclusion may again be extended for The Small Business Jobs Act of 2010 amended Section 1202 to provide for a temporary 100% exclusion from gross income for regular income tax purposes for QSBS purchased after September 27, 2010 and before January 1, 2011, and comparable 100% exclusion for AMT purposes. The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010, extended the January 1, 2011 end-date for acquiring QSBS eligible for the 100% regular income tax and AMT exclusion to January 1, The 100% exclusion was again later extended for all of 2012, 2013, and 2014, reverting back to a 50% exclusion (subject to the AMT) as of January 1, The Obama administration has previously discussed making a 100% exclusion permanent, but the status of any future proposals is uncertain. Historically, Section 1202 provided for other exclusion percentages (50%, 60% or 75%), depending on when stock was acquired and the type of business, and also provided for varying percentages of the Section 1202 exclusion to be treated as a preference item for AMT purposes. 10

11 Stock held by a non-corporate taxpayer in a C-corporation In general, in order to qualify for the benefits of Section 1202 a non-corporate taxpayer must acquire and hold stock in a qualifying C-corporation. The benefits of Section 1202 do not directly apply to equity interests acquired and held in pass-through entities, such as S-corporations or partnerships. However, as discussed in more detail later in this presentation, an individual taxpayer s allocable share of gain attributable to a sale of QSBS by a pass-through entity may potentially qualify as gain eligible for the Section 1202 exclusion. 11

12 3. Overview of Requirements a. Stock of a C-corporation acquired at original issuance b. Qualified small business requirement c. Active business requirement d. Five-year holding period 12

13 Primary requirements for Section 1202 QSBS There are four main requirements that must be satisfied before gain on the sale of stock is potentially eligible for the exclusion under Section (1) Stock of a C-corporation acquired at original issuance (2) Qualified small business requirement (3) Active business requirement (4) Five-year holding period 13

14 4. Stock of a C-corpration Acquired at Original Issuance a. Stock of a C-corporation b. Original issuance requirement 14

the issuing corporation must also be an eligible corporation as defined in Section 1202(e)(4).")

15 Stock of a C-corporation For purposes of Section 1202(c)(1), the issuing corporation must be a C-corporation. In addition, it should be noted that for purposes of the active business requirement of Section 1202(e) the issuing corporation must also be an eligible corporation as defined in Section 1202(e)(4). Section 1202(e)(4) defines an eligible corporation as any domestic corporation other than: (i) a DISC (a domestic international sales corporation as defined in Section 992(a)) or former DISC; (ii) a corporation with respect to which an election under Section 936 is in effect or which has a direct or indirect subsidiary with respect to which such an election is in effect; (iii) a RIC (regulated investment company), REIT (real estate investment trust), or REMIC (real estate mortgage investment conduit); and (iv) a cooperative. 15

16 Original issuance Pursuant to Section 1202(c)(1)(B), QSB stock must generally be acquired at original issue (directly or through an underwriter) in exchange for money or other property, or as compensation for services performed for such corporation (other than services performed as an underwriter of such stock). The concept of property Restrictions on redemptions Incorporation of a partnership Section 83(b) elections Convertible securities, options, warrants Stock acquired by gift or upon death of holder Stock received in certain corporate transactions Stock held through pass-through entities 16

17 5. Qualified Small Business Requirement a. In general b. Aggregate gross assets test c. Submission of reports to the IRS 17

18 In general Section 1202(d)(1) defines a qualified small business as a domestic C corporation if: (i) the aggregate gross assets of such corporation (or any predecessor thereof), at all times on or after the date of the enactment of the Revenue Reconciliation Act of 1993 and before the issuance of the stock being tested for potential qualification as QSB stock, do not exceed $50 million; (ii) the aggregate gross assets of such corporation immediately after the issuance of the stock being tested for potential qualification as QSB stock (determined by taking into account amounts received in the issuance) do not exceed $50 million; and (iii) such corporation agrees to submit to the IRS and its shareholders any reports that the IRS may require to carry out the purposes of Section

19 Aggregate gross assets test For purposes of Section 1202(d)(1), the term aggregate gross assets means the sum of the amount of cash and the aggregate adjusted bases of all other property of the corporation (with the adjusted basis of any property contributed to the corporation being determined as if the basis of the property contributed to the corporation were equal to its fair market value as of the time of such contribution). However, stock that otherwise qualifies as QSB stock as of the date of issuance will not lose that status solely by virtue of the fact that a corporation subsequently exceeds the $50 million threshold. In addition, and also for purposes of aggregate gross asset test of Section 1202(d)(1), certain aggregation rules under Section 1202(d)(3)(A) provide that corporations that are part of a parent-subsidiary controlled group shall be treated as one corporation. Section 1202(d)(3)(B) defines a parent-subsidiary controlled group as any controlled group of corporations as defined under Section 1563(a)(1) (except that more than 50% shall be substituted for at least 80% in each place where appears and Section 1563(a)(4) shall not apply). In general, Section 1563(a)(1), as modified by Section 1202(d)(3)(B), effectively defines a parent-subsidiary controlled group as consisting of one or more chains of corporations connected with a common parent corporation through more than 50% stock ownership, as determined by voting power or by value. Section 1563(e)(2) also provides that, for purposes of Section 1563(a)(1), stock owned directly or indirectly by a partnership shall be considered as owned by any partner having an interest of 5% or more in the capital or profits of the partnership in proportion to his or her interest in capital or profits, which ever such proportion is higher. 19

20 Submission of reports to the IRS To date, the IRS has not promulgated any guidance relating to either the timing or required content of any reporting requirements that may apply for purposes of Section 1202(d)(1)(C). 20

21 6. Active Business Requirement a. In general b. Special Rules c. PLR

22 In general For purposes of Section 1202(c)(2)(A), a corporation shall be treated as satisfying the active business requirement of Section 1202(e) for any period if during such period (i) at least 80% (by value) of the assets of such corporation are used by such corporation in the active conduct of one or more qualified trades or businesses (as defined in Section 1202(e)(3)) and (ii) such corporation is an eligible corporation (as defined in Section 1202(e)(4)). Under Section 1202(e)(3), the term qualified trade or business means any trade or business other than: (A) any trade or business involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees; (B) any banking, insurance, financing, leasing, or similar business; (C) any farming business (including the business of raising or harvesting trees); (D) any business involving the production or extraction of products of a character with respect to which a deduction is allowable under Section 613 or 613A; and (E) any business of operating a hotel, motel, restaurant, or similar business. 22

23 Special rules Start-up and R&D activities Stock in other corporations Working capital Real estate holdings Computer software royalties 23

24 PLR The facts of the Ruling involved a company that operated in the pharmaceutical industry and aided clients in the commercialization of experimental drugs. The company s main business activities were researching the effectiveness of drug formulations, conducting clinical tests, and manufacturing drugs. The company also helped clients develop successful drug-manufacturing processes and solve other problems encountered in the pharmaceutical industry. The company s assets included manufacturing and clinical facilities along with intellectual property assets, such as a patent portfolio. The company also possessed several valuable relationships in the pharmaceutical industry. In analyzing whether the company was engaged in a qualified trade or business under Section 1202(e)(3), the IRS explained that the thrust of 1202(e)(3) is that businesses are not qualified trades or businesses if they offer value to customers primarily in the form of services, whether those services are the providing of hotel rooms, for example, or in the form of individual expertise (law firm partners). The IRS noted that the company in the Ruling used its specific manufacturing and intellectual property assets to create value for customers, and was akin to a manufacturer of parts in the automobile industry. Accordingly, despite recognizing the company s connections to the pharmaceutical industry, which is a component of the health industry (a clearly prohibited field), the IRS ruled that the company s activities did not amount to the performance of services in the health industry within the meaning of Section 1202(e)(3). The Ruling specifically noted that the Company is not in the business of offering service in the form of individual expertise. 24

25 7. Five-Year Holding Period Requirement a. In general b. Offsetting short positions 25

26 In general In general, the holding period of QSB stock begins on the date of issuance whether or not the QSB stock was received in a taxable or non-taxable transaction. Special tacking rules, however, apply to the computation of the holding period if the QSB stock is converted into other stock of the same corporation, or if the QSB stock is acquired as a gift, by inheritance, or as a transfer from a partnership. In particular, the holding period of stock received in a conversion includes the holding period for the converted stock and the holding period of stock received by gift, inheritance or from a partnership includes the period the stock was held by the donor, decedent or partnership. The holding period also tacks in the case of QSB stock exchanged for stock of another corporation that is treated as QSB stock in a transaction described under Sections 351 or 368. The holding period of stock acquired in a Section 1045 rollover transaction generally includes the holding period of the QSB stock disposed of in the rollover transaction. 26

27 Offsetting short positions Section 1202(j) provides that if a taxpayer has an offsetting short position with respect to any QSB stock, Section 1202(a) shall not apply to any gain from the sale or exchange of such stock unless (i) such stock was held by the taxpayer for more than 5 years as of the first day on which there was such a short position, and (ii) the taxpayer elects to recognize gain as if such stock were sold on such first day for its fair market value. Section 1202(j)(2) provides that the taxpayer shall be treated as having an offsetting short position with respect to any QSB stock if: (i) the taxpayer has made a short sale of substantially identical property; (ii) the taxpayer has acquired an option to sell substantially identical property at a fixed price; or (iii) to the extent provided in Treasury Regulations, the taxpayer has entered into any other transaction which substantially reduces the risk of loss from holding such QSB stock. In addition, for purposes of Section 1202(j)(2), any reference to the taxpayer includes a reference to any person who is related (within the meaning of Section 267(b) or Section 707(b) ) to the taxpayer. 27

28 8. Amount of Gain Subject to Exclusion a. Section 1202(a) exclusion b. Section 1202(b) limitation on taxpayer s eligible gain c. Section 1202(i) basis rules 28

29 Section 1202(a) exclusion Section 1202(a)(1) provides that in the case of a taxpayer other than a corporation gross income shall not include 50% of any gain from the sale or exchange of QSBS held for more than five years. Section 57(a)(7) treats 7% of the amount excluded under Section 1202 as a preference item for alternative minimum tax purposes. Section 1202(a)(4), added by the Small Business Jobs Act of 2010, provides that in the case of stock acquired after September 27, 2010 and before January 1, 2011: (i) the Section 1202(a) exclusion shall be 100%; (ii) Section 1202(a)(2) (dealing with certain empowerment zone businesses) shall not apply; and (iii) Section 57(a)(7) (providing that 7% of the amount excluded under Section 1202 shall be treated as a preference item for alternative minimum tax purposes) shall not apply. It should also again be noted that on December 17, 2010, pursuant to Pub. Law No , the benefits afforded under Section 1202(a)(4) were extended through December 31, 2011, and later extensions were also granted for all of 2012, 2013, and

30 Section 1202(b) limitation on taxpayer s eligible gain In general, Section 1202(b)(1) provides that the aggregate amount of excludable eligible gain effectively allowable under Section 1202(a) with respect to QSB stock issued by a corporation and disposed of by a taxpayer in any given taxable year equals the greater of: (i) $10 million (reduced by the aggregate amount of any eligible gain previously excluded by the taxpayer for prior taxable years as a result of dispositions of QSB stock issued by the corporation); or (ii) 10 times the aggregate adjusted bases of QSB stock issued by the corporation and disposed of by the taxpayer during the taxable year. For purposes of Section 1202(b), the term eligible gain means any gain from the sale or exchange of QSB stock held for more than 5 years. In addition, gains in QSB stock attributable to post-issuance periods are generally eligible for exclusion, subject to the ceiling discussed above. As previously discussed, certain limitations may apply to gain recognized on stock that is received in exchange for QSB stock in a transaction described in Section 351 (corporate formation) or Section 368 (a tax-free reorganization). The entire amount of any gain on a subsequent sale or exchange is eligible for the exclusion if the stock received is stock in another qualified small business. However, if the stock is not in a qualified small business, the exclusion only applies to the extent of the gain which would have been recognized at the time of the transfer if Section 351 or Section 368 had not applied. 30

31 Section 1202(i) basis rules Section 1202(i) provides that, for purposes of Section 1202, when the taxpayer transfers property (other than money or stock) to a corporation in exchange for stock in such corporation, such stock shall (i) be treated as having been acquired by the taxpayer on the date of such exchange, and (ii) the basis of such stock in the hands of the taxpayer shall in no event be less than the fair market value of the property exchanged. One critical aspect of the basis equals fair market value rule of Section 1202(i) (that is not readily apparent from the plain statutory language of Section 1202) is that the amount of any previously unrecognized gain that is carried over to the QSB stock will be taxed in full at the time of the subsequent sale or exchange (such that only subsequent appreciation in the QSB stock constitutes eligible gain for purposes of Section 1202(b)(1)). 31

32 9. Potential Rollover of Gain Section 1045 a. In general b. Specific requirements c. Rollover of gain in partnership context 32

on the sale exceeds the cost of replacement QSB stock purchased by the taxpayer, and the basis of the replacement QSB stock is reduced by the amount of the unrecognized gain.")

33 In general Section 1045 allows a taxpayer to defer recognition of gain from the sale of QSB stock if the taxpayer purchases replacement QSB stock within a 60 day period beginning on the date of the sale. Provided that all the requirements of Section 1045 are satisfied, gain recognized from the sale of QSB stock is limited to the extent to which the amount realized (i.e., gross proceeds) on the sale exceeds the cost of replacement QSB stock purchased by the taxpayer, and the basis of the replacement QSB stock is reduced by the amount of the unrecognized gain. Section 1045 also incorporates by reference the special basis rules in Section Thus, in general, the amount of any gain attributable to periods prior to the receipt of the QSB stock is not eligible for roll over and must be recognized at the time of the sale or exchange. Only gain accrued after the time of receipt of the QSB stock can be deferred. Further, if QSB stock is exchanged in a Section 351 or Section 368 transaction for stock of Newco or the Acquiring Corporation, and Newco or the Acquiring Corporation is not itself a qualified small business, the amount of gain which may be rolled over under Section 1045 is limited to the gain that would have been recognized at the time of the Section 351 or Section 368 transaction if the original QSB stock had been sold in a taxable transaction at that time. 33

34 Specific requirements Non-corporate taxpayer Sale of QSB stock Six-month holding period Section 1045 election Character of gain Purchase of replacement QSB stock within 60-day period 34

35 Rollover of gain in partnership context Rollover by partnership Rollover by partner Rollover of directly held QSB stock through a purchasing partnership Other partnership transactions 35

36 10. Practical Planning Considerations a. Pre-investment planning b. Making the investment c. Issues requiring ongoing evaluation / operational covenants d. Planning for exit e. Tax filing requirements and document retention 36

37 Pre-investment planning In addition to the wide variety of traditional factors (both tax and non-tax) that should be evaluated when structuring an investment, the potential benefits that may be available under Section 1202 should be seriously considered. In general, attempting to plan into Section 1202 may make sense in a situation where, among other things: (i) a five-year holding period is at least a possibility (particularly given the longer investment holds experienced in recent years following the economic downturn); (ii) the aggregate gross asset value of the business is expected to be equal to or less than $50 million; (iii) the general profile of the expected business operations are such that the active business requirement of Section 1202(e) should be satisfied; (iv) there is not a current need to extract after-tax cash flow from the business during the operational phase (such that a double corporate-level tax on distributions would not be an issue); (v) the expected overall equity growth of the business, and related potential benefits under Section 1202 on exit, are sufficient to overcome a corporate-level tax during the operational phase; (vi) the expected investor base is composed of non-corporate taxpayers that can actually potentially benefit from Section 1202; and (vii) the expected investor base and/or management has the ability to commit the necessary amount of time and resources to ensure that the applicable requirements of Section 1202 are satisfied at all relevant times prior to exit. 37

38 Making the investment Once a decision has been made to affirmatively structure an investment with a view toward potentially obtaining the benefits of Section 1202, the parties should consult with their tax and other advisors to ensure that the relevant requirements are satisfied and that important information is properly documented at the outset. For example, a third-party valuation of the business would generally be advisable, both for purposes of ensuring that the $50 million aggregate asset value threshold is not exceeded and to establish a fair market value basis with respect to any property contributions being made by investors. In addition, service providers that receive restricted stock should also use any valuation data to assess whether it may be advantageous to make a Section 83(b) election with respect to such stock. Finally, the parties should also decide whether they wish to be bound by any operational covenants that are intended to facilitate the preservation of the requirements of Section

39 Issues requiring ongoing evaluation / operational covenants In general, following an investment the investor base and/or management must continue to monitor the ongoing operations of the business in order to ensure that the requirements of Section 1202 are continuously satisfied (along with any specific operational covenants that the parties may have agreed to in connection with such requirements). In addition, sufficient records should be maintained in the event that any information requests are ultimately made by the IRS pursuant to Section 1202(d)(1)(C). Although the parties are likely to focus upon the general satisfaction of the active business requirement of Section 1202(e), there are a variety of subsidiary issues embedded in Section 1202(e) (as well as other issues) that the parties may inadvertently overlook. These issues include: Availability of look-through rule for subsidiaries No portfolio stock or securities Subsequent infusions of cash; working capital Maximum real estate holdings Shareholder holding periods Redemptions Subsequent transactions / restructurings Subsequent changes in law or changes in interpretation 39

40 Planning for exit Exits before the expiration of the 5-year holding period Exits after the expiration of the 5-year holding period Tax filing requirements and document retention 40

41 11. Examples / Reporting a. Example #1 $10 million gain exclusion b. Example #2 10x basis gain exclusion c. Example #3 gain rollover 41

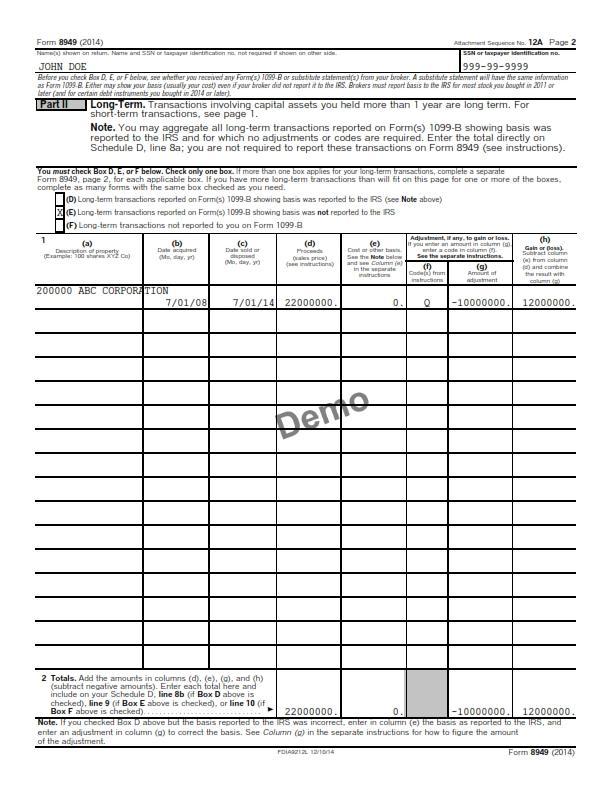

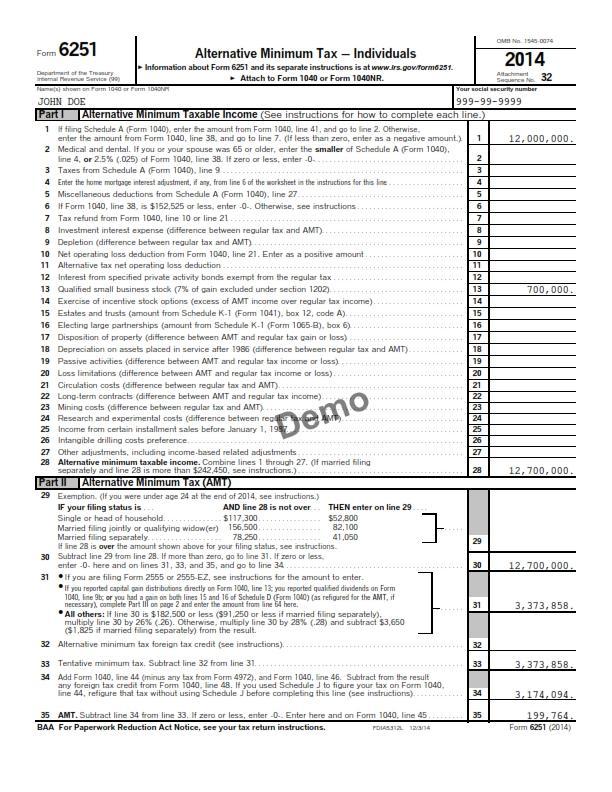

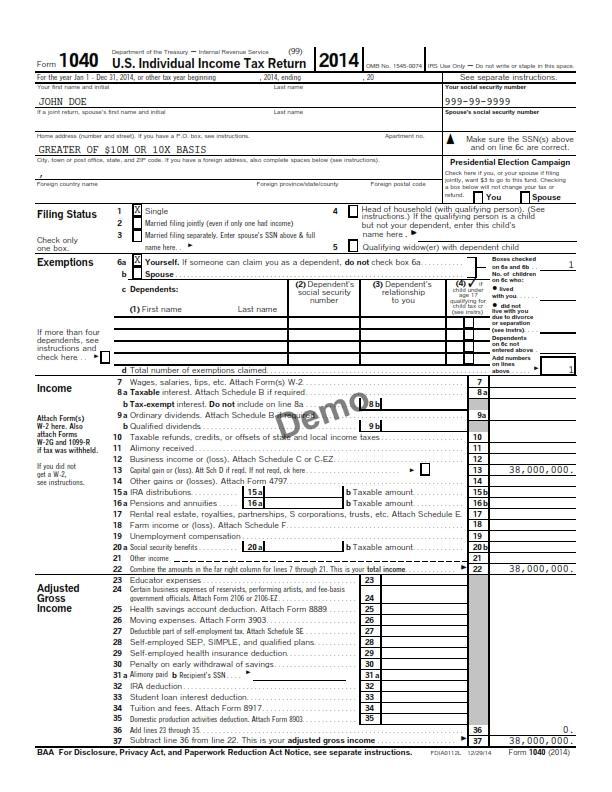

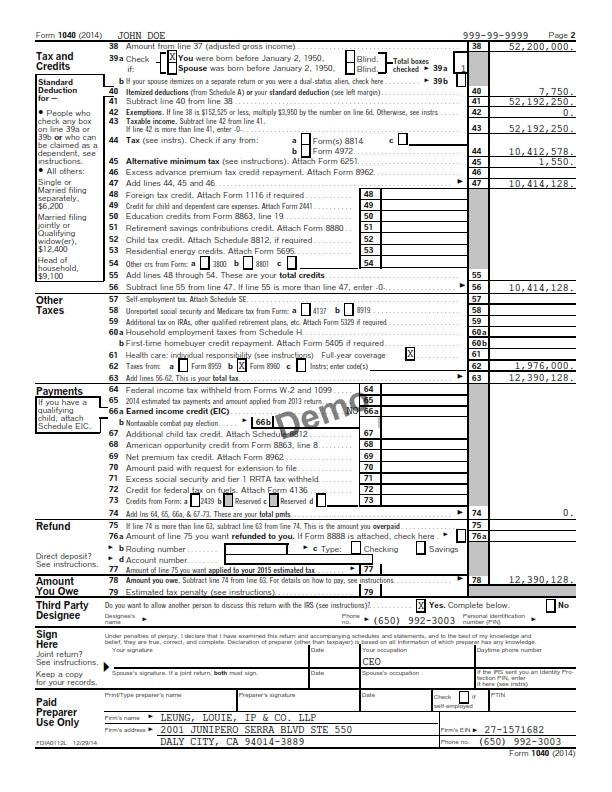

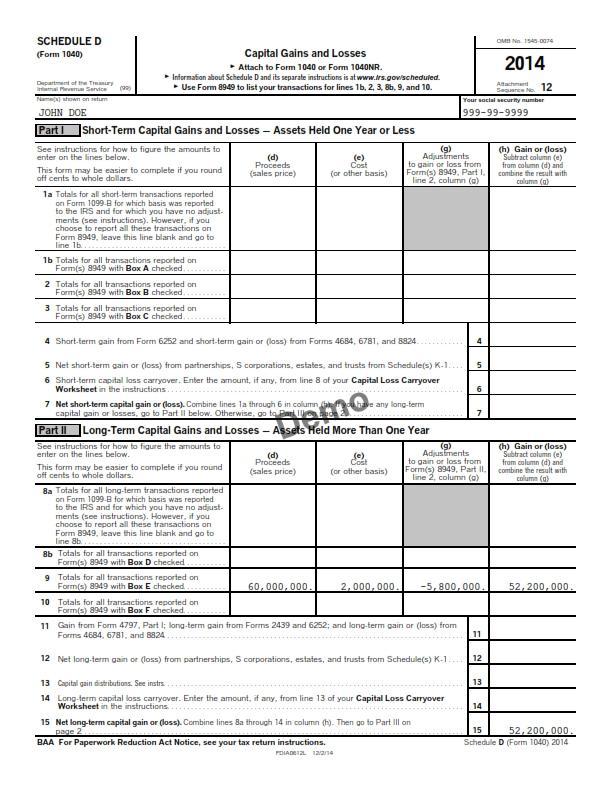

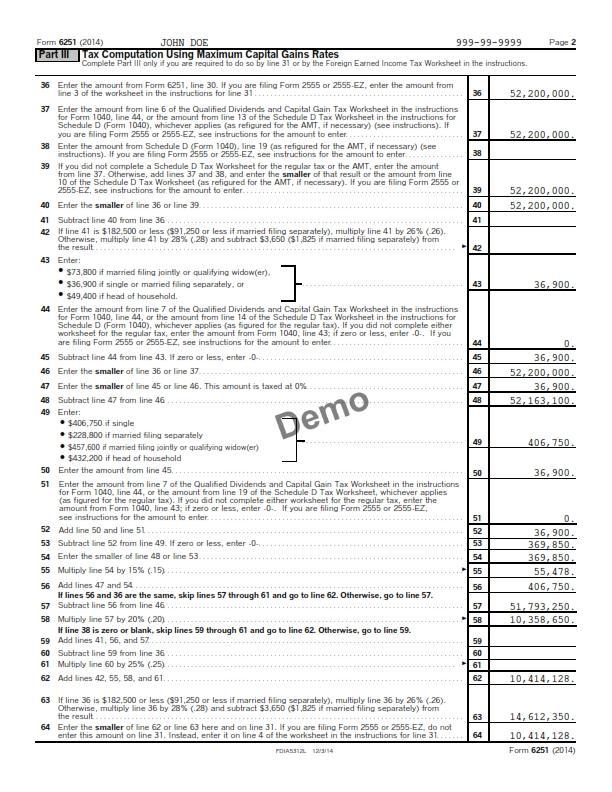

42 Examples / Reporting Example #1 - $10M Gain Exclusion: 1. On 7/1/2008, John invested 40 cents to buy 200K shares of ABC Corp. (QSBS) 2. On 7/1/2014 (6 yrs later), John sold all 200K shares for $22M. 3. John realized $22M LTCG. 4. John qualified for the $10M QSBS gain exclusion. Example #2 10X Basis Gain Exclusion: 1. On 7/1/2008, John invested $2M to buy 200K shares of ABC Corp. (QSBS) 2. On 7/1/2014 (6 yrs later), John sold all 200K shares for $60M. 3. John realized $58M LTCG. 4. John qualified for a $20M (10X Basis) QSBS gain exclusion. Example #3 Gain Roll Over: 1. Same facts as Example #2. 2. Except John originally invested on 7/1/2012, not meeting the 5-year holding period for gain exclusion. 3. On 8/1/2014, John invested $6M (10% of the $60M proceeds) in another QSBS. 4. John qualified for the 1045 gain roll over because he reinvested within 60 days from the date of the QSBS sale. 42

43 43

44 44

45 45

46 46

47 47

48 48

49 49

50 50

51 51

52 52

53 53

54 54

55 55

56 56

57 57

58 58

59 59

60 60

61 61

62 62

63 63

64 64

65 65

66 66

67 67

68 Disclaimer These materials have been prepared in connection with a continuing legal education program and solely for the purpose of enhancing practitioners professional knowledge on federal tax matters. No part of these materials constitutes written tax advice that may be either used or relied upon by any person for any purpose. 68

Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Internal Revenue Code Section 1202 Partial exclusion for gain from certain small business stock.

Internal Revenue Code Section 1202 Partial exclusion for gain from certain small business stock. CLICK HERE to return to the home page (a) Exclusion. In the case of a taxpayer other than a corporation,

Internal Revenue Code Section 1202 Partial exclusion for gain from certain small business stock. CLICK HERE to return to the home page (a) Exclusion. In the case of a taxpayer other than a corporation,

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IMPORTANT INFORMATION

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

STATE OF NEW JERSEY. SENATE, No th LEGISLATURE

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED MARCH, 0 Sponsored by: Senator PAUL A. SARLO District (Bergen and Passaic) Senator STEVEN V. OROHO District (Morris, Sussex and Warren) SYNOPSIS

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED MARCH, 0 Sponsored by: Senator PAUL A. SARLO District (Bergen and Passaic) Senator STEVEN V. OROHO District (Morris, Sussex and Warren) SYNOPSIS

The following is an interesting question that

May June 2011 Private Equity & Hedge Fund Corner By Joseph J. Bergthold and Thomas C. Lenz 1 How Private Equity Fund Managers Can Cash in on Tax Benefits of Qualified Small Business Stock Thomas C. Lenz

May June 2011 Private Equity & Hedge Fund Corner By Joseph J. Bergthold and Thomas C. Lenz 1 How Private Equity Fund Managers Can Cash in on Tax Benefits of Qualified Small Business Stock Thomas C. Lenz

Presenting a 90-minute encore presentation featuring live Q&A. Today s faculty features:

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

Failing to qualify for Section 1202 has serious tax consequences. A. Summary

MEMORANDUM TO: FROM: Tim Keane, Golden Angels Investors Godfrey & Kahn, S.C. DATE: October 20, 2016 RE: Failing to qualify for Section 1202 has serious tax consequences A. Summary An owner of C corporation

MEMORANDUM TO: FROM: Tim Keane, Golden Angels Investors Godfrey & Kahn, S.C. DATE: October 20, 2016 RE: Failing to qualify for Section 1202 has serious tax consequences A. Summary An owner of C corporation

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Capital Gains Exclusion for Small Business Stock Held for More Than 5 Years. By Stephen D. D. Hamilton, July 2011

Capital Gains Exclusion for Small Business Stock Held for More Than 5 Years I. Background. By Stephen D. D. Hamilton, July 2011 A. Enactment of exemption. The Creating Small Business Jobs Act of 2010,

Capital Gains Exclusion for Small Business Stock Held for More Than 5 Years I. Background. By Stephen D. D. Hamilton, July 2011 A. Enactment of exemption. The Creating Small Business Jobs Act of 2010,

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

IRC Section 734 Adjustments: Applying the 754 Election to Distributions of Partnership Property

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

New Accounting Method Rules for Small Business Taxpayers Under IRC 448

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Form 8621 PFIC Reporting: Navigating the Highly Complex IRS Passive Foreign Investment Company Rules Determining Which Assets Require PFIC Reporting, Calculating Tax and Interest,

FOR LIVE PROGRAM ONLY Form 8621 PFIC Reporting: Navigating the Highly Complex IRS Passive Foreign Investment Company Rules Determining Which Assets Require PFIC Reporting, Calculating Tax and Interest,

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance

Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance") Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report

FOR LIVE PROGRAM ONLY Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report WEDNESDAY, NOVEMBER 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report WEDNESDAY, NOVEMBER 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Section 1202 Capital Gains Tax Exclusion Nick Gruidl and David Sterling September 26, 2013

Nick Gruidl and David Sterling September 26, 2013 Presenters David Sterling, Partner and National Leader of M&A Tax Practice Experienced in consolidated returns, C corporations, S corporations, partnerships,

Nick Gruidl and David Sterling September 26, 2013 Presenters David Sterling, Partner and National Leader of M&A Tax Practice Experienced in consolidated returns, C corporations, S corporations, partnerships,

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II THURSDAY, OCTOBER 20, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II THURSDAY, OCTOBER 20, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Tax Reform for Pass-Through Entities: Impact of New Tax Law on Partnerships, LLCs and S-Corporations

Presenting a live 90-minute webinar with interactive Q&A Tax Reform for Pass-Through Entities: Impact of New Tax Law on Partnerships, LLCs and S-Corporations Planning Techniques, Loopholes, Qualified Business

Presenting a live 90-minute webinar with interactive Q&A Tax Reform for Pass-Through Entities: Impact of New Tax Law on Partnerships, LLCs and S-Corporations Planning Techniques, Loopholes, Qualified Business

Tax Planning and Reporting for Partnership Equity Compensation Grants

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 23, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 23, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,

Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules

FOR LIVE PROGRAM ONLY Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules THURSDAY, JANUARY 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules THURSDAY, JANUARY 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

New FASB ASU on Not-For-Profit Financial Reporting and Disclosures: Are You Ready?

FOR LIVE PROGRAM ONLY New FASB ASU 2016-14 on Not-For-Profit Financial Reporting and Disclosures: Are You Ready? TUESDAY, MARCH 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY New FASB ASU 2016-14 on Not-For-Profit Financial Reporting and Disclosures: Are You Ready? TUESDAY, MARCH 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Private Investment Funds and Tax Reform

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

New FASB ASU Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs

New FASB ASU 2014-09 Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

New FASB ASU 2014-09 Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

IC-DISC Compliance: Exporter Challenges in the Federal Tax Break

FOR LIVE PROGRAM ONLY IC-DISC Compliance: Exporter Challenges in the Federal Tax Break THURSDAY, DECEMBER 21, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

FOR LIVE PROGRAM ONLY IC-DISC Compliance: Exporter Challenges in the Federal Tax Break THURSDAY, DECEMBER 21, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

New Section 199A: Structuring Real Estate Transactions to Take Advantage of the Qualified Business Income Deduction

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Structuring Real Estate Transactions to Take Advantage of the Qualified Business Income Deduction THURSDAY, JANUARY 17, 2019

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Structuring Real Estate Transactions to Take Advantage of the Qualified Business Income Deduction THURSDAY, JANUARY 17, 2019

Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption

(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption") New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption FOR LIVE PROGRAM ONLY TUESDAY, JULY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption FOR LIVE PROGRAM ONLY TUESDAY, JULY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor

Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor") Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Goodwill in Corporate Asset Sales: Tax Planning Opportunities Distinguishing Between Personal and Corporate Goodwill, Navigating Allocation and

Presenting a live 90-minute webinar with interactive Q&A Goodwill in Corporate Asset Sales: Tax Planning Opportunities Distinguishing Between Personal and Corporate Goodwill, Navigating Allocation and

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Selling Your Business Income Tax-Free: The Qualified Small Business Stock Election

Selling Your Business Income Tax-Free: The Qualified Small Business Stock Election By Karin Prangley 18 / OWNER to OWNER Selling shares in a business completely (or partially) income tax-free sounds too

Selling Your Business Income Tax-Free: The Qualified Small Business Stock Election By Karin Prangley 18 / OWNER to OWNER Selling shares in a business completely (or partially) income tax-free sounds too

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Structuring Contributions of Appreciated Property to Partnerships: Avoiding Tax Recognition on Built-in Gain Assets Navigating Allocation Challenges,

Presenting a live 90-minute webinar with interactive Q&A Structuring Contributions of Appreciated Property to Partnerships: Avoiding Tax Recognition on Built-in Gain Assets Navigating Allocation Challenges,

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Mastering Form 5500 Schedule H: Avoiding Audit Triggers

FOR LIVE PROGRAM ONLY Mastering Form 5500 Schedule H: Avoiding Audit Triggers Financial Information Reporting Requirements, Identifying Valuation Challenges and Expanded Compliance Questions THURSDAY,

FOR LIVE PROGRAM ONLY Mastering Form 5500 Schedule H: Avoiding Audit Triggers Financial Information Reporting Requirements, Identifying Valuation Challenges and Expanded Compliance Questions THURSDAY,

Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

COMMENTARY. Update on Qualified Small Business Stock: New Federal Legislation and Status of California Rules JONES DAY

March 2013 JONES DAY COMMENTARY Update on Qualified Small Business Stock: New Federal Legislation and Status of California Rules Eligible investors in qualified small businesses are entitled to certain

March 2013 JONES DAY COMMENTARY Update on Qualified Small Business Stock: New Federal Legislation and Status of California Rules Eligible investors in qualified small businesses are entitled to certain

New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units

FOR LIVE PROGRAM ONLY New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units THURSDAY, NOVEMBER 30, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units THURSDAY, NOVEMBER 30, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040 WEDNESDAY, JANUARY 18, 2017, 1:00-2:50 pm Eastern IMPORTANT

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040 WEDNESDAY, JANUARY 18, 2017, 1:00-2:50 pm Eastern IMPORTANT

International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Section 704(c): Contributions of Appreciated or Depreciated Property to Partnerships and LLCs

: Contributions of Appreciated or Depreciated Property to Partnerships and LLCs") Section 704(c): Contributions of Appreciated or Depreciated Property to Partnerships and LLCs Navigating Complex Allocation Rules, Curative and Remedial Allocations, Elections, and Anti-Abuse Rules THURSDAY,

Section 704(c): Contributions of Appreciated or Depreciated Property to Partnerships and LLCs Navigating Complex Allocation Rules, Curative and Remedial Allocations, Elections, and Anti-Abuse Rules THURSDAY,

Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences

FOR LIVE PROGRAM ONLY Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Tax Reform: Impact on REITs, Real Estate Businesses and Investors Pass-Through Business and Interest Deductions, Cost Recovery, Carried Interest,

Presenting a live 90-minute webinar with interactive Q&A Tax Reform: Impact on REITs, Real Estate Businesses and Investors Pass-Through Business and Interest Deductions, Cost Recovery, Carried Interest,

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Sales and Use Tax Reserves: Reconciling ASC 450/FAS 5 Reserve Requirements With IAS 37 Standard for Foreign Activities

Sales and Use Tax Reserves: Reconciling ASC 450/FAS 5 Reserve Requirements With IAS 37 Standard for Foreign Activities THURSDAY, APRIL 6, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Sales and Use Tax Reserves: Reconciling ASC 450/FAS 5 Reserve Requirements With IAS 37 Standard for Foreign Activities THURSDAY, APRIL 6, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Qualified Small Business Stock: The Next Big Bang (Queries, Qualms, and Qualifications)

") Qualified Small Business Stock: The Next Big Bang (Queries, Qualms, and Qualifications) January 15, 2019 Paul S. Lee, J.D., LL.M. Global Fiduciary Strategist The Northern Trust Company New York, NY PSL6@ntrs.com

Qualified Small Business Stock: The Next Big Bang (Queries, Qualms, and Qualifications) January 15, 2019 Paul S. Lee, J.D., LL.M. Global Fiduciary Strategist The Northern Trust Company New York, NY PSL6@ntrs.com

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Executive Compensation: Tax and Other Considerations for Restricted Stock Awards

Presenting a live 90-minute webinar with interactive Q&A Executive Compensation: Tax and Other Considerations for Restricted Stock Awards Strategies for Navigating Substantial Risk of Forfeiture Analysis,

Presenting a live 90-minute webinar with interactive Q&A Executive Compensation: Tax and Other Considerations for Restricted Stock Awards Strategies for Navigating Substantial Risk of Forfeiture Analysis,

Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Calculating Depreciation Recapture Under IRC 1245 and 1250: Minimizing Tax Through Transaction Planning

FOR LIVE PROGRAM ONLY Calculating Depreciation Recapture Under IRC 1245 and 1250: Minimizing Tax Through Transaction Planning TUESDAY, AUGUST 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Calculating Depreciation Recapture Under IRC 1245 and 1250: Minimizing Tax Through Transaction Planning TUESDAY, AUGUST 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform

and Form 1041 Trust Deduction Rules Post-Tax Reform") New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions

And Subpart F Income Inclusions") Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Mastering U.S. Permanent Establishment Tax Under New OECD Guidance vs. General Tax Treaty Approach Navigating Income Attribution Rules in the U.S. Model Income Tax Convention and Recently Signed Tax Treaties

Mastering U.S. Permanent Establishment Tax Under New OECD Guidance vs. General Tax Treaty Approach Navigating Income Attribution Rules in the U.S. Model Income Tax Convention and Recently Signed Tax Treaties

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 29, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 29, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities

FOR LIVE PROGRAM ONLY S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities TUESDAY, MAY 10, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities TUESDAY, MAY 10, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

ERISA Pre-Approved and Customized Benefit Plans: Overhauled IRS Procedures and Determination Letter Process

Presenting a live 90-minute webinar with interactive Q&A ERISA Pre-Approved and Customized Benefit Plans: Overhauled IRS Procedures and Determination Letter Process TUESDAY, NOVEMBER 14, 2017 1pm Eastern

Presenting a live 90-minute webinar with interactive Q&A ERISA Pre-Approved and Customized Benefit Plans: Overhauled IRS Procedures and Determination Letter Process TUESDAY, NOVEMBER 14, 2017 1pm Eastern

Tax Treatment of Carried Interest: Planning Opportunities for Tax, Private Equity and Real Estate Professionals

Presenting a 90-minute encore presentation featuring live Q&A Tax Treatment of Carried Interest: Planning Opportunities for Tax, Private Equity and Real Estate Professionals IRC Section 1061, Capital Contributions,

Presenting a 90-minute encore presentation featuring live Q&A Tax Treatment of Carried Interest: Planning Opportunities for Tax, Private Equity and Real Estate Professionals IRC Section 1061, Capital Contributions,

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval MONDAY, DECEMBER 21, 2015, 1:00-2:50 pm Eastern IMPORTANT

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval MONDAY, DECEMBER 21, 2015, 1:00-2:50 pm Eastern IMPORTANT

Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities Determining Whether to File Composite Returns, Dealing With Withholding Requirements FOR

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities Determining Whether to File Composite Returns, Dealing With Withholding Requirements FOR

Memorandum TM. Old Dogs and New Tricks: 1202, New Tax Rules, and Entity Choice

Memorandum TM Reproduced with permission from, Vol. 59, No. 5, p. 63, 03/05/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Old Dogs and New Tricks: 1202,

Memorandum TM Reproduced with permission from, Vol. 59, No. 5, p. 63, 03/05/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Old Dogs and New Tricks: 1202,

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

U.S.-Canadian Dual Taxation Pitfalls: Reporting Issues and Planning Opportunities for U.S. Taxpayers Navigating Tax Treaties to Minimize Tax on Passive Income and Pass-Through Income THURSDAY, APRIL 27,

U.S.-Canadian Dual Taxation Pitfalls: Reporting Issues and Planning Opportunities for U.S. Taxpayers Navigating Tax Treaties to Minimize Tax on Passive Income and Pass-Through Income THURSDAY, APRIL 27,

State Sales Tax on Drop Shipments: Navigating Various States' Rules on Registrations and Exemptions

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Choice of Entity Under the Tax Cuts and Jobs Act

Choice of Entity Under the Tax Cuts and Jobs Act By S. Kyle Agee The recent enactment of the Tax Cuts and Jobs Act (the TCJA ) resulted in two significant changes for business entities: the corporate tax

Choice of Entity Under the Tax Cuts and Jobs Act By S. Kyle Agee The recent enactment of the Tax Cuts and Jobs Act (the TCJA ) resulted in two significant changes for business entities: the corporate tax

Presenting a 90 minute encore presentation featuring live Q&A. Today s faculty features:

Presenting a 90 minute encore presentation featuring live Q&A New Section 951A: GILTI Rules for Individual and Non C Corporation CFC Shareholders Treatment of CFC income, Reporting Requirements, Planning

Presenting a 90 minute encore presentation featuring live Q&A New Section 951A: GILTI Rules for Individual and Non C Corporation CFC Shareholders Treatment of CFC income, Reporting Requirements, Planning

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

1998 Instructions for Schedule D, Capital Gains and Losses

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

Financing Multi-Family Housing: Structuring the Low Income House Tax Credit and Tax-Exempt Bonds Documenting Transactions for Investors and Developers

Presenting a live 90-minute webinar with interactive Q&A Financing Multi-Family Housing: Structuring the Low Income House Tax Credit and Tax-Exempt Bonds Documenting Transactions for Investors and Developers

Presenting a live 90-minute webinar with interactive Q&A Financing Multi-Family Housing: Structuring the Low Income House Tax Credit and Tax-Exempt Bonds Documenting Transactions for Investors and Developers

IC-DISC: Compliance Challenges in the Federal Tax Break for Exporters

IC-DISC: Compliance Challenges in the Federal Tax Break for Exporters TUESDAY, OCTOBER 21, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

IC-DISC: Compliance Challenges in the Federal Tax Break for Exporters TUESDAY, OCTOBER 21, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

2002 Instructions for Schedule D, Capital Gains and Losses

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance WEDNESDAY, SEPTEMBER 2, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance WEDNESDAY, SEPTEMBER 2, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Leveraging Earnings-Stripping Regs for Foreign Investments: Maximizing Tax Savings, Minimizing IRS Scrutiny

Presenting a live 110-minute teleconference with interactive Q&A Leveraging Earnings-Stripping Regs for Foreign Investments: Maximizing Tax Savings, Minimizing IRS Scrutiny THURSDAY, FEBRUARY 6, 2014 1pm