Mastering the Rules of S Corporation Shareholder-Employee Compensation

|

|

|

- Cori Clark

- 6 years ago

- Views:

Transcription

1 FOR LIVE PROGRAM ONLY Mastering the Rules of S Corporation Shareholder-Employee Compensation WEDNESDAY, JANUARY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours. To earn credit you must: Participate in the program on your own computer connection (no sharing) if you need to register additional people, please call customer service at ext.1 (or ext. 1). Strafford accepts American Express, Visa, MasterCard, Discover. Listen on-line via your computer speakers. Respond to five prompts during the program plus a single verification code. To earn full credit, you must remain connected for the entire program. WHO TO CONTACT DURING THE LIVE EVENT For Additional Registrations: -Call Strafford Customer Service x1 (or x1) For Assistance During the Live Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN.

2 Tips for Optimal Quality FOR LIVE PROGRAM ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please immediately so we can address the problem.

3 Mastering the Rules of S Corporation Shareholder-Employee Compensation JANUARY 31, 2018 Stephen D. Kirkland, CPA, CMC, CFC, CFF Atlantic Executive Consulting, Columbia, S.C. stephen.kirkland@aecg.biz Paul S. Hamann, President RCReports, Denver phamann@rcreports.com

4 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

5 Mastering the Rules of S Corporation Shareholder-Employee Compensation Stephen Kirkland Paul Hamann 5

6 This session includes only general information for discussion and education purposes. The presenters may play devil s advocate to stimulate thought. If any point is not covered as thoroughly as you would like, please contact the presenters afterwards for more information. 6

7 Owner Pay One of the most interesting topics in business today. Large amounts Subjective Personal Controversial Complex issues 7

8 Today we will cover Tax rules and IRS positions Comparability Data Examples and a case study Court Cases Incentive Compensation Deferred Compensation Equity Compensation Tax Cuts and Jobs Act Preparer Penalties 8

9 IRS Position Distributions and other payments by an S corporation to a shareholder must be treated as wages to the extent the amounts are reasonable compensation for services rendered to the corporation. 9

10 Reasonable for services actually rendered Code Section 162(a)(1) Reasonable compensation is the amount as would ordinarily be paid for like services by like enterprises under like circumstances IRS Reg. Section 162-7(b)(3) Replacement Cost Fair Market Value 10

11 11

12 The key to establishing reasonable compensation is determining what the shareholder-employee did for the S corporation 1. Services of non-shareholder employees 2. Capital and equipment 3. Services of shareholders 12

13 Services of non-shareholder employees, or Capital and equipment 13

14 Services of shareholder In addition to the shareholder-employee direct generation of gross receipts, the shareholder-employee should also be compensated for administrative work performed 14

15 W-2 or 1099 Revenue Ruling 74-44; IRC states: An officer of a corporation is considered an EMPLOYEE Employee or Independent Contractor Under common-law rules, anyone who performs services for you is your employee if you can control what will be done and how it will be done. 15

16 Talk to your clients early and often. Ask for all related parties to be identified (long-term clients may assume you know). Document! 16

17 Three Approaches to Valuation Cost Approach replacement cost for job segments (many hats) Market Approach Industry comparison Income Approach Independent Investor Test 17

18 The Factors Examples The employee s qualifications, including education and experience The nature and scope of the employee s duties Amounts paid for similar services by similar businesses Prevailing economic conditions 18

19 The Factors Examples The character/complexity/condition of the business Conflicts of interest Intent to compensate/retain the employee Internal consistency of compensation Covenants and guaranties 19

20 Gathering the Facts Responsibilities in all areas? How were the historical amounts determined? Any deferred compensation? 20

21 Ask Specific and Open-ended Questions: Are you multi-lingual? Are you good with technology? How do your spend your time? Would you be difficult to replace? Why? 21

22 Reliable Sources? Interviews, financial statements, tax returns, websites Can you confirm the facts? 22

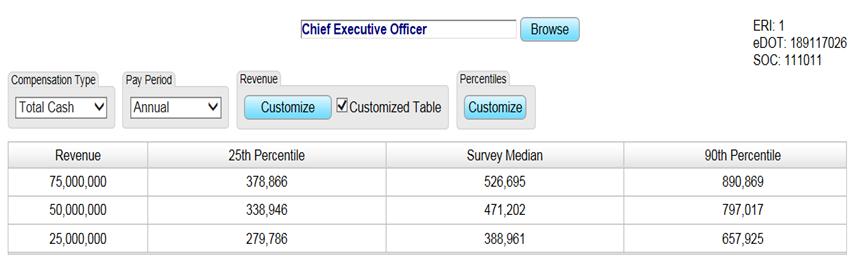

23 Comparability Data 23

24 Comparability Data Title / Job description Location Company size / Years of experience Industry 24

25 Industry Codes 25

26 One Potential Source of Comparability Data: Publicly-Traded Companies Larger? More diversified? More layers of management? Narrower duties? 26

27 27

28 Other Sources of Compensation Comparability Data 28

29 Case Study Road construction company owned by the CEO Located in Portland, Oregon Owner s 25-year-old son says he is a VP but he has basic duties; he works 40 hours per week Annual revenue is $50 million 29

30 Economic Research Institute screenshot 30

31 ERI screenshot 31

32 RCReports.com for the Son The son has various basic duties... 32

33 RCReports.com for the Son We break down his time and enter his proficiency 33

34 Attributes 2017 Multnomah County, Oregon Hours worked: 2080 Some college no degree Employees: NAICS: Highway, Street, and Bridge Construction 34

35 The Son s Replacement Compensation 35

36 There are many Sources of Compensation Data Trade Associations 36

37 For any Source of Comparability Data: Do you understand their methodology? Do you know where they got their data? What quality controls do they have in place? How did they deal with outliers? 37

38 Sources of Comparability Data 38

39 Deferred Comp (Catch-up Pay) Does the liability exist anywhere other than in the owner s head? Documented in corporate minutes? Internal Revenue Code section 409A. 39

40 Incentive Compensation Total compensation is considered by the IRS Each year usually stands alone except for deferred compensation The owners incentives are compared to those of nonowner employees, and year-by-year comparisons may be made (consistent?) Unreasonable formulas produce unreasonable amounts Compensation agreements Covenants Bonus withholding just before year end 40

41 Equity Compensation Beware of sharing equity Now more common at start-ups Noncash compensation is taxable Treatment of equity compensation to service provider employees Section 83 41

42 Employee Benefits Adjust cash pay for excessive or minimal welfare and retirement benefits? 42

43 S Corporations in Court IRS 25-1* versus 43

44 Court Cases DAVID E. WATSON, P.C., V. UNITED STATES OF AMERICA (2010) Low Salary versus Profit Distributions 2002 Profit = $203, Salary = $24, Profit = $175, Salary = $24,000 44

45 DAVID E. WATSON, P.C., V. UNITED STATES OF AMERICA (2010) IRS Objected: Education Graduate Degree Experience Time 20 Years Full Time (35-45 hours per week) 45

46 DAVID E. WATSON, P.C., V. UNITED STATES OF AMERICA (2010) Reasonable Compensation $91,044 for 2002 $91,044 for

47 DAVID E. WATSON, P.C., V. UNITED STATES OF AMERICA (2010) Reasonable Compensation $91,044 $91,044 Actual Salary Paid $24,000 $24,000 Re-Characterized $67,044 $67,044 Total Re-Characterization = $134,088 47

48 DAVID E. WATSON, P.C., V. UNITED STATES OF AMERICA (2010) $48,521 $20,000 48

49 DAVID E. WATSON, P.C., V. UNITED STATES OF AMERICA (2010) IRS: Graduate Degree 20 Years experience Full Time employee Various Job Duties: CPA/Accountant Partner Re-structured businesses No Research and No Documentation 49

50 Appeal Denied 50

51 SEAN MCALARY LTD, INC. v. COMMISSIONER (2013) McAlary Ltd = Real Estate Company 2006 Net Income = $231, Distribution = $240, Salary = Zero 51

52 IRS Calculation in McAlary $100,755 Primary Job Function Real Estate Broker Full Time (12 hour days 6-7 days per week) Compared McAlary LTD performance with peers in the real estate industry 52

53 IRS Calculation in McAlary $100,755 Replacement Cost McAlary LTD could expect to pay $48.44/hour to another individual in exchange for the services Mr. McAlary performed Fair Market Value $100,755 would be FMV of the services Mr. McAlary performed for his S Corp 53

54 IRS Calculation in McAlary $100,755 $48.44 X 2,080 The Bureau of Labor Statistics defines Year-Round, Full-Time employment as 2,080 hours per year. 40 Hour Work Week X 52 Weeks/Year McAlary often worked 12 hour days with few days off 54

55 McAlary s Position $24,000 Compensation Agreement BOD Meeting Minutes Increases Based on Number of Agents 55

56 The Court s Calculation $83,200 Various Services Wage Range Hourly Wage = $ ,080 X $40.00 = $83,200 56

57 McAlary Court Calculation 2,080 X $40.00 = $83,200 Compensation Agreement We are not persuaded that the remuneration agreement represents a sound measure of the value of the services that Mr. McAlary provided The agreement clearly was not the product of an arm's-length negotiation. Industry Comparison (IRS Expert) did not explain how a comparison of compensation measured as a percentage of gross receipts with compensation measured as a percentage of net sales would aid the Court In the end, we do not find this portion of (the experts) report to be persuasive or helpful. 57

58 Court Calculation 2,080 X $40.00 = $83,200 Various Services Management; Supervision; Recruiting; Sales; Advertising; Purchasing; Bookkeeper; Record Keeping Experience Low; New to the Industry COESS-BLS Range $32.99 to $64.28 Determining an employee's reasonable compensation is dependent upon a number of factors and is far from an exact science. 58

59 GLASS BLOCKS UNLIMITED v. COMMISSIONER (2013) How an S Corp can Lose Money and Still be Required to Pay Reasonable Compensation 59

60 Glass Blocks Unlimited Fredrick Blodgett 2007 Net Income = $ Transferred in = $45, Transferred out = $30, Salary = Zero 60

61 IRS Position in Glass Blocks Transfer in was a contribution to capital (basis). Transfer out was a distribution (return of basis). Reasonable Compensation must be paid before a distribution can be made. 61

62 Glass Blocks Position Transfer in was a shareholder loan to company. Transfer out was a repayment of the shareholder loan. Reasonable Compensation does not apply. 62

63 Court Finding Transfers in question were capital contributions and not bona fide loans: No written agreements or promissory notes No interest charged No security (collateral) No fixed repayment schedule 63

64 Court Finding Where the expectation of repayment depends solely on the success of the borrower's business, rather than on an unconditional obligation to repay, the transaction has the appearance of a capital contribution. 64

65 Math Net Income - before $877 Wages $-30,844 Employment Taxes $-2,360 Penalty & Interest $-1, Net Income (Loss) - after $(34,250) 65

66 DAVIS v. UNITED STATES (1994) Mile High Calcium Carol L. Davis Henry Adams (husband) Transfers In and Out Assessed Taxes + Interest & Penalties of $39,220 66

67 DAVIS v. UNITED STATES (1994) Henry Adams President Not an Employee No Active Participation Worked for outside employers Officer in name only There is an exception for officers who perform only minor services (Treas. Reg (d)-(1)(b)) 67

68 DAVIS v. UNITED STATES (1994) Carol L. Davis Was an Employee 12 hours per month (2.77 per week) $8.00 per hour $39,220.$647 68

69 Allen L. Davis, et al v. Commissioner (2011) $37 million of compensation was determined to be reasonable largely because other shareholders had agreed to it and they were adversarial to Mr. Davis. 69

70 Beware Disproportionate distributions Other shareholders Lenders/investors 70

71 71

72 Preparing Analyses for IRS Scrutiny Facts, Analyses, Conclusions, Bases for conclusions Accepted Methodology? Reliable Sources of data? Assumptions what did you assume and why? 72

73 Changes in Tax Cuts and Jobs Act Limitations on executive compensation deductions at publicly-traded companies and tax-exempt entities may influence comparability data. 73

74 Changes in Tax Cuts and Jobs Act New 20% deduction in Code section 199A (available at the shareholder level) - Exception for certain types of businesses 74

75 Changes in Tax Cuts and Jobs Act New 20% deduction in Code section 199A - Exception for certain types of businesses - Income exception 75

76 Changes in Tax Cuts and Jobs Act New 20% deduction in Code section 199A - Exception for certain types of businesses - Income exception - Second incentive to keep compensation at the low end of the range? 76

77 Changes in Tax Cuts and Jobs Act New 20% deduction in Code section 199A - Exception for certain types of businesses - Income exception - Second incentive to keep compensation at the low end of the range? - May want to raise compensation, to increase SEP contribution thereby reducing TI below cut-off - Create new/separate entities so one can qualify? 77

78 Tax Preparer Penalties $5,000 Code Section 6694(b) IRS expects preparers to have appropriate checklists IRS does not expect the preparer to merely accept the information IRS requires the preparer to be proactive Penalties can and will be imposed on preparers 78

79 No Tax Court for Reasonable Compensation Notice of Employment Tax Determination under IRC Additional Compensation to Officer Employees No resolution at appeals Cannot proceed to Tax Court Pay Tax Sue for refund 79

80 Documentation protects you and your clients. 80

81 The IRS Job Aid on Reasonable Compensation Guide for IRS auditors and valuation professionals Now available on the IRS website (It is 96 pages and the Appendix is 26 pages) 81

82 Thank You! Paul S. Hamann RCReports.com Stephen Kirkland CompensationOpinion.com 82

Reasonable Compensation for Shareholder-Employees of S Corps

Reasonable Compensation for Shareholder-Employees of S Corps Presented by RCReports, Inc. Reasonable Compensation Simplified Webcast Agenda About the Presenters Distribution V. Wages Reasonable Compensation

Reasonable Compensation for Shareholder-Employees of S Corps Presented by RCReports, Inc. Reasonable Compensation Simplified Webcast Agenda About the Presenters Distribution V. Wages Reasonable Compensation

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

FOR LIVE PROGRAM ONLY Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return THURSDAY, MAY 19, 2016, 1:00-2:50

Tax Planning and Reporting for Partnership Equity Compensation Grants

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Tax Planning and Reporting for Partnership Equity Compensation Grants FOR LIVE PROGRAM ONLY WEDNESDAY, MAY 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

New FASB ASU Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs

New FASB ASU 2014-09 Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

New FASB ASU 2014-09 Revenue Recognition Standards for Nonprofit Entities: Implementing ASC 606 for NFPs FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

IRC Section 734 Adjustments: Applying the 754 Election to Distributions of Partnership Property

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

FOR LIVE PROGRAM ONLY Partnership Terminations: Mastering Section 708 Filing Short Year Returns, Revisiting Elections, Amortization Opportunities, Basis Adjustments and More WEDNESDAY, JANUARY 25, 2017,

IMPORTANT INFORMATION

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

UDFI for Exempt Organizations: Reporting Unrelated Debt-Financed Income on Form 990-T Avoiding Costly Allocation Mistakes in the Sale of Encumbered Property WEDNESDAY, FEBRUARY 3, 2016, 1:00-2:50 pm Eastern

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Form 8621 PFIC Reporting: Navigating the Complex IRS Passive Foreign Investment Company Rules FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reporting and Reconciliation of Hedge Fund and Other Alternative Investment Fund K-1s Navigating Footnotes and Tying Information to the Tax Return MAY 21, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

GILTI Calculations for Individual CFC Shareholders: New Section 951A Tax on Foreign Intangible Income FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

New Accounting Method Rules for Small Business Taxpayers Under IRC 448

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption

(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption") New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption FOR LIVE PROGRAM ONLY TUESDAY, JULY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

New IRC 864(c)(8) Withholding Rules on Partnership Sales: Calculations and Affidavit of Exemption FOR LIVE PROGRAM ONLY TUESDAY, JULY 31, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 29, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

New Guidance on Calculating UBTI for Separate Trades or Businesses Under Tax Reform FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 29, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules

FOR LIVE PROGRAM ONLY Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules THURSDAY, JANUARY 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Final Section 385 Regs: Navigating State and Local Tax Impact of New Debt-to-Equity Reclassification Rules THURSDAY, JANUARY 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Basis Calculations in Section 368 Reorganizations: Tax Deferral Benefits For Subsidiary Shareholders THURSDAY, DECEMBER 14, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform

and Form 1041 Trust Deduction Rules Post-Tax Reform") New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities

FOR LIVE PROGRAM ONLY S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities TUESDAY, MAY 10, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY S-Corporations Owning Multiple Entities: Mastering Tax Reporting and Planning Opportunities TUESDAY, MAY 10, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

FOR LIVE PROGRAM ONLY Subpart F Income Rules and Sections 956, 958 and 1248: Meeting the Reporting Challenges of Controlled Foreign Corporations THURSDAY, JULY 21, 2016, 1:00-2:50 pm Eastern IMPORTANT

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Form 8621 PFIC Reporting: Navigating the Highly Complex IRS Passive Foreign Investment Company Rules Determining Which Assets Require PFIC Reporting, Calculating Tax and Interest,

FOR LIVE PROGRAM ONLY Form 8621 PFIC Reporting: Navigating the Highly Complex IRS Passive Foreign Investment Company Rules Determining Which Assets Require PFIC Reporting, Calculating Tax and Interest,

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 20, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 1041 Compliance for Special Needs Trusts: First-Party vs. Third-Party, Qualified Disability Trusts FOR LIVE PROGRAM ONLY TUESDAY, NOVEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor

Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor") Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

IC-DISC Compliance: Exporter Challenges in the Federal Tax Break

FOR LIVE PROGRAM ONLY IC-DISC Compliance: Exporter Challenges in the Federal Tax Break THURSDAY, DECEMBER 21, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

FOR LIVE PROGRAM ONLY IC-DISC Compliance: Exporter Challenges in the Federal Tax Break THURSDAY, DECEMBER 21, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Section 1291 Excess Distribution Calculations for PFIC Tax and Interest Reporting

Section 1291 Excess Distribution Calculations for PFIC Tax and Interest Reporting FOR LIVE PROGRAM ONLY TUESDAY, JUNE 19, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Section 1291 Excess Distribution Calculations for PFIC Tax and Interest Reporting FOR LIVE PROGRAM ONLY TUESDAY, JUNE 19, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units

FOR LIVE PROGRAM ONLY New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units THURSDAY, NOVEMBER 30, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY New IRC 987 Regs and Foreign Currency Translation: Income Calculation for Qualified Business Units THURSDAY, NOVEMBER 30, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences

FOR LIVE PROGRAM ONLY Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Alternative Investments for Nonprofits and Exempt Organizations: Avoiding Unforeseen Tax Consequences TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

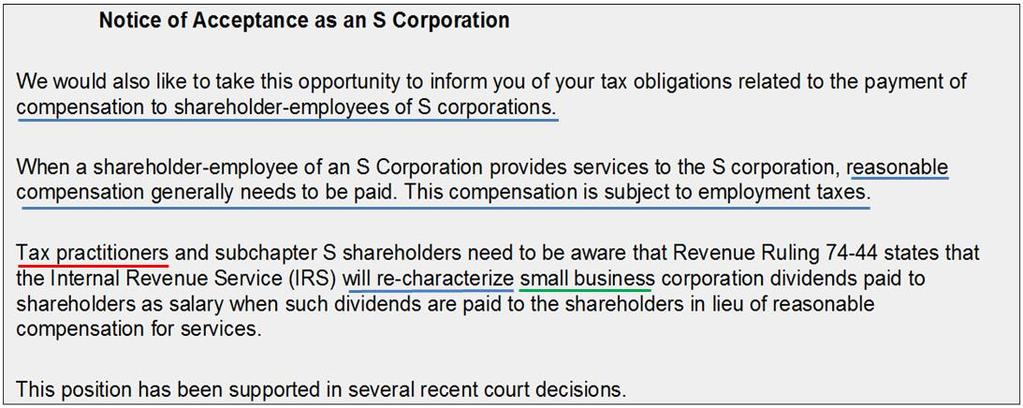

(Un)Reasonable Compensation and S Corporations

Reasonable Compensation and S Corporations") (Un)Reasonable Compensation and S Corporations By Stephen D. Kirkland, CPA, CMC, CFC, CFF Atlantic Executive Consulting Group, LLC When shareholders take funds out of their S corporations, they need to

(Un)Reasonable Compensation and S Corporations By Stephen D. Kirkland, CPA, CMC, CFC, CFF Atlantic Executive Consulting Group, LLC When shareholders take funds out of their S corporations, they need to

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Mastering U.S. Permanent Establishment Tax Under New OECD Guidance vs. General Tax Treaty Approach Navigating Income Attribution Rules in the U.S. Model Income Tax Convention and Recently Signed Tax Treaties

Mastering U.S. Permanent Establishment Tax Under New OECD Guidance vs. General Tax Treaty Approach Navigating Income Attribution Rules in the U.S. Model Income Tax Convention and Recently Signed Tax Treaties

Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges Navigating Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions

And Subpart F Income Inclusions") Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II THURSDAY, OCTOBER 20, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II THURSDAY, OCTOBER 20, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Reporting UBTI and UBIT in Partnerships and S Corporations: Mastering K-1 Disclosures for Exempt Org Partners Key Box 20V Reporting, Footnotes and Separate Disclosures, and UDFI Exemptions THURSDAY, SEPTEMBER

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance

Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance") Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

FOR LIVE PROGRAM ONLY Form 4720 Private Foundation Excise Tax Return: Reporting Taxable Violations THURSDAY, JULY 12, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

State Income Tax Treatment of Nonresident Trusts: Compliance Challenges and Planning Opportunities

State Income Tax Treatment of Nonresident Trusts: Compliance Challenges and Planning Opportunities FOR LIVE PROGRAM ONLY TUESDAY, JULY 24, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

State Income Tax Treatment of Nonresident Trusts: Compliance Challenges and Planning Opportunities FOR LIVE PROGRAM ONLY TUESDAY, JULY 24, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance WEDNESDAY, SEPTEMBER 2, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Section 704, Targeted Allocations and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance WEDNESDAY, SEPTEMBER 2, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

Section 704, Targeted Allocations, and the Distribution Waterfall: Overcoming Challenges Absent IRS Guidance Understanding the Economic Effect Test and How to Allocate Income or Loss Using Targeted Allocations

International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Presenting a 90-minute encore presentation featuring live Q&A. Today s faculty features:

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

IRC Sect. 704(b): Partnership Allocations

: Partnership Allocations") IRC Sect. 704(b): Partnership Allocations Navigating Complex Rules to Determine Valid Allocation of Income, Gain, Loss, Deductions or Credits THURSDAY, OCTOBER 3, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

IRC Sect. 704(b): Partnership Allocations Navigating Complex Rules to Determine Valid Allocation of Income, Gain, Loss, Deductions or Credits THURSDAY, OCTOBER 3, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities

FOR LIVE PROGRAM ONLY Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities TUESDAY, MAY 1, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities TUESDAY, MAY 1, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY S Corporation Stock Sales: Mastering Tax Reporting, Income/Loss Allocation and Section 1377 Elections WEDNESDAY, FEBRUARY 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 23, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 23, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment FOR LIVE PROGRAM ONLY TUESDAY, FEBRUARY 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment THURSDAY, FEBRUARY 21, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Multistate Allocation of Trust Distributable Net Income: Income Sourcing and Apportionment THURSDAY, FEBRUARY 21, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

IRC 751 "Hot Asset" Treatment: New Rules for Calculating Ordinary Income Recharacterization

Presenting a live 90-minute webinar with interactive Q&A IRC 751 "Hot Asset" Treatment: New Rules for Calculating Ordinary Income Recharacterization New IRS Proposal on Determining Partners' Share of Section

Presenting a live 90-minute webinar with interactive Q&A IRC 751 "Hot Asset" Treatment: New Rules for Calculating Ordinary Income Recharacterization New IRS Proposal on Determining Partners' Share of Section

New Section 199A: Structuring Real Estate Transactions to Take Advantage of the Qualified Business Income Deduction

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Structuring Real Estate Transactions to Take Advantage of the Qualified Business Income Deduction THURSDAY, JANUARY 17, 2019

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Structuring Real Estate Transactions to Take Advantage of the Qualified Business Income Deduction THURSDAY, JANUARY 17, 2019

Presenting a 90 minute encore presentation featuring live Q&A. Today s faculty features:

Presenting a 90 minute encore presentation featuring live Q&A New Section 951A: GILTI Rules for Individual and Non C Corporation CFC Shareholders Treatment of CFC income, Reporting Requirements, Planning

Presenting a 90 minute encore presentation featuring live Q&A New Section 951A: GILTI Rules for Individual and Non C Corporation CFC Shareholders Treatment of CFC income, Reporting Requirements, Planning

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

GST and Form 709: Fundamentals of Generation-Skipping Transfer Tax Reporting FOR LIVE PROGRAM ONLY THURSDAY, DECEMBER 20, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program

Mastering Form 5500 Schedule H: Avoiding Audit Triggers

FOR LIVE PROGRAM ONLY Mastering Form 5500 Schedule H: Avoiding Audit Triggers Financial Information Reporting Requirements, Identifying Valuation Challenges and Expanded Compliance Questions THURSDAY,

FOR LIVE PROGRAM ONLY Mastering Form 5500 Schedule H: Avoiding Audit Triggers Financial Information Reporting Requirements, Identifying Valuation Challenges and Expanded Compliance Questions THURSDAY,

New FASB ASU on Not-For-Profit Financial Reporting and Disclosures: Are You Ready?

FOR LIVE PROGRAM ONLY New FASB ASU 2016-14 on Not-For-Profit Financial Reporting and Disclosures: Are You Ready? TUESDAY, MARCH 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY New FASB ASU 2016-14 on Not-For-Profit Financial Reporting and Disclosures: Are You Ready? TUESDAY, MARCH 7, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Sales and Use Tax Reserves: Reconciling ASC 450/FAS 5 Reserve Requirements With IAS 37 Standard for Foreign Activities

Sales and Use Tax Reserves: Reconciling ASC 450/FAS 5 Reserve Requirements With IAS 37 Standard for Foreign Activities THURSDAY, APRIL 6, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Sales and Use Tax Reserves: Reconciling ASC 450/FAS 5 Reserve Requirements With IAS 37 Standard for Foreign Activities THURSDAY, APRIL 6, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Brian E. Hammell, Esq., Sullivan & Worcester, Boston

Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax,

Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax,

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040 WEDNESDAY, JANUARY 18, 2017, 1:00-2:50 pm Eastern IMPORTANT

Mastering Reporting of Publicly Traded Partnership and MLP K-1s on Partners' Returns Navigating MLP K-1 Footnotes and Tying Information to the 1040 WEDNESDAY, JANUARY 18, 2017, 1:00-2:50 pm Eastern IMPORTANT

Broker Dealer Auditing: Mastering New SEC and PCAOB Rules and Standards

Broker Dealer Auditing: Mastering New SEC and PCAOB Rules and Standards Complying With Changed Regulatory Framework for Conducting Audits and Attesting to Internal Controls WEDNESDAY, JANUARY 7, 2015,

Broker Dealer Auditing: Mastering New SEC and PCAOB Rules and Standards Complying With Changed Regulatory Framework for Conducting Audits and Attesting to Internal Controls WEDNESDAY, JANUARY 7, 2015,

Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report

FOR LIVE PROGRAM ONLY Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report WEDNESDAY, NOVEMBER 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY Short Year 1065 Returns for Terminated Partnerships: Avoiding Penalties For Failure to Report WEDNESDAY, NOVEMBER 8, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

U.S.-Canadian Dual Taxation Pitfalls: Reporting Issues and Planning Opportunities for U.S. Taxpayers Navigating Tax Treaties to Minimize Tax on Passive Income and Pass-Through Income THURSDAY, APRIL 27,

U.S.-Canadian Dual Taxation Pitfalls: Reporting Issues and Planning Opportunities for U.S. Taxpayers Navigating Tax Treaties to Minimize Tax on Passive Income and Pass-Through Income THURSDAY, APRIL 27,

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,

Form 8903: Domestic Production Activities Deduction for Pass-Thrus and Other Business Entities Mastering Complex Determinations, Calculations and Reporting Challenges for the DPAD WEDNESDAY, FEBRUARY 25,

Mastering Form 990 Schedule A: Protecting Public Charity Status, IRC 509 Public Support Test Calculations and Reporting

FOR LIVE PROGRAM ONLY Mastering Form 990 Schedule A: Protecting Public Charity Status, IRC 509 Public Support Test Calculations and Reporting TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY Mastering Form 990 Schedule A: Protecting Public Charity Status, IRC 509 Public Support Test Calculations and Reporting TUESDAY, OCTOBER 17, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities Determining Whether to File Composite Returns, Dealing With Withholding Requirements FOR

Composite Returns and Nonresident Withholding for Pass-Through Entities: Navigating the Multistate Complexities Determining Whether to File Composite Returns, Dealing With Withholding Requirements FOR

Tax Strategies for Real Estate LLC and LP Agreements: Capital Commitments, Tax Allocations, Distributions, and More

Presenting a live 90-minute webinar with interactive Q&A Tax Strategies for Real Estate LLC and LP Agreements: Capital Commitments, Tax Allocations, Distributions, and More Structuring Provisions to Achieve

Presenting a live 90-minute webinar with interactive Q&A Tax Strategies for Real Estate LLC and LP Agreements: Capital Commitments, Tax Allocations, Distributions, and More Structuring Provisions to Achieve

Tax Reporting of Bitcoin and Other Cryptocurrency: Calculating Basis, Income and Gain

Tax Reporting of Bitcoin and Other Cryptocurrency: Calculating Basis, Income and Gain FOR LIVE PROGRAM ONLY TUESDAY, JUNE 26, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Tax Reporting of Bitcoin and Other Cryptocurrency: Calculating Basis, Income and Gain FOR LIVE PROGRAM ONLY TUESDAY, JUNE 26, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Tax Reform and U.S. Foreign Reporting for Individuals: New Cross-Border Repatriation and Inclusion Provisions

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities THURSDAY, MAY 8, 2014,

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities THURSDAY, MAY 8, 2014,

Executive Compensation: Tax and Other Considerations for Restricted Stock Awards

Presenting a live 90-minute webinar with interactive Q&A Executive Compensation: Tax and Other Considerations for Restricted Stock Awards Strategies for Navigating Substantial Risk of Forfeiture Analysis,

Presenting a live 90-minute webinar with interactive Q&A Executive Compensation: Tax and Other Considerations for Restricted Stock Awards Strategies for Navigating Substantial Risk of Forfeiture Analysis,

Presenting a live 110-minute teleconference with interactive Q&A

Presenting a live 110-minute teleconference with interactive Q&A Valuation Challenges With $10 Million-and-Under Businesses Avoiding Mistakes With Built-In Gains and Taxes, Misuse of Market Data and Other

Presenting a live 110-minute teleconference with interactive Q&A Valuation Challenges With $10 Million-and-Under Businesses Avoiding Mistakes With Built-In Gains and Taxes, Misuse of Market Data and Other

Calculating Trust Fiduciary Accounting Income: Interpreting Operating Documents, Applying UPIA and State Law

Calculating Trust Fiduciary Accounting Income: Interpreting Operating Documents, Applying UPIA and State Law FOR LIVE PROGRAM ONLY OCTOBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Calculating Trust Fiduciary Accounting Income: Interpreting Operating Documents, Applying UPIA and State Law FOR LIVE PROGRAM ONLY OCTOBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

U.K.-Based Retirement Accounts for U.S. Taxpayers: Mastering Reporting, Maximizing Planning Opportunities Utilizing Treaty Provisions to Achieve Optimal Tax Results While Complying With Foreign Reporting

U.K.-Based Retirement Accounts for U.S. Taxpayers: Mastering Reporting, Maximizing Planning Opportunities Utilizing Treaty Provisions to Achieve Optimal Tax Results While Complying With Foreign Reporting

Form 1040NR for Foreign Trusts: Income Tax Reporting for Foreign Non-Grantor Trusts

FOR LIVE PROGRAM ONLY Form 1040NR for Foreign Trusts: Income Tax Reporting for Foreign Non-Grantor Trusts WEDNESDAY, JULY 19, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY Form 1040NR for Foreign Trusts: Income Tax Reporting for Foreign Non-Grantor Trusts WEDNESDAY, JULY 19, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

Tax Challenges With Private Equity Management Fee Waivers Given Newly Heightened IRS Scrutiny

Presenting a live 90-minute webinar with interactive Q&A Tax Challenges With Private Equity Management Fee Waivers Given Newly Heightened IRS Scrutiny Structuring Waiver Arrangements in Light of the Proposed

Presenting a live 90-minute webinar with interactive Q&A Tax Challenges With Private Equity Management Fee Waivers Given Newly Heightened IRS Scrutiny Structuring Waiver Arrangements in Light of the Proposed

Structuring Equity Compensation for Partnerships and LLCs Navigating Capital and Profits Interests Plus Section 409A and Tax Consequences

Presenting a live 90-minute webinar with interactive Q&A Structuring Equity Compensation for Partnerships and LLCs Navigating Capital and Profits Interests Plus Section 409A and Tax Consequences TUESDAY,

Presenting a live 90-minute webinar with interactive Q&A Structuring Equity Compensation for Partnerships and LLCs Navigating Capital and Profits Interests Plus Section 409A and Tax Consequences TUESDAY,

Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Mastering IRC 2632 GST Exemption Allocation Rules: Identifying GST Trusts and Indirect Skips THURSDAY, JUNE 22, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Mastering Foreign Tax Credits for Corporations and Individuals: Calculations, Carrybacks, Carryforwards and Limitations

Mastering Foreign Tax Credits for Corporations and Individuals: Calculations, Carrybacks, Carryforwards and Limitations FOR LIVE PROGRAM ONLY WEDNESDAY, SEPTEMBER 7, 2016, 1:00-2:50 pm Eastern IMPORTANT

Mastering Foreign Tax Credits for Corporations and Individuals: Calculations, Carrybacks, Carryforwards and Limitations FOR LIVE PROGRAM ONLY WEDNESDAY, SEPTEMBER 7, 2016, 1:00-2:50 pm Eastern IMPORTANT

Partnership Exchanges: Structuring "Drop and Swap" and "Mixing Bowl" Transactions Minimizing the Risk of an Unfavorable Audit Outcome

Presenting a live 90-minute webinar with interactive Q&A Partnership Exchanges: Structuring "Drop and Swap" and "Mixing Bowl" Transactions Minimizing the Risk of an Unfavorable Audit Outcome WEDNESDAY,

Presenting a live 90-minute webinar with interactive Q&A Partnership Exchanges: Structuring "Drop and Swap" and "Mixing Bowl" Transactions Minimizing the Risk of an Unfavorable Audit Outcome WEDNESDAY,

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval MONDAY, DECEMBER 21, 2015, 1:00-2:50 pm Eastern IMPORTANT

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval MONDAY, DECEMBER 21, 2015, 1:00-2:50 pm Eastern IMPORTANT

Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Form 8865 Reporting of Foreign Partnership Income and Navigating Rules for Allocable Share of Foreign Income THURSDAY, AUGUST 3, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Page Related Parties - Compensation and Loans 1

Page 121-144 07 - Related Parties - Compensation and Loans 1 Page 121 I. Owner Compensation Issues in General Some basic facts we know but our clients do not: A. All shareholders MUST take a reasonable

Page 121-144 07 - Related Parties - Compensation and Loans 1 Page 121 I. Owner Compensation Issues in General Some basic facts we know but our clients do not: A. All shareholders MUST take a reasonable

Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges

Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Section 988 Foreign Currency Transaction Reporting Rules for Options, Straddles and Hedges FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Private Investment Funds and Tax Reform

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

401k Annual Audits: Anticipating Serious and Costly Errors, Evaluating Alternative Solutions

FOR LIVE PROGRAM ONLY 401k Annual Audits: Anticipating Serious and Costly Errors, Evaluating Alternative Solutions TUESDAY, APRIL 11, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY 401k Annual Audits: Anticipating Serious and Costly Errors, Evaluating Alternative Solutions TUESDAY, APRIL 11, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

State Sales Tax on Drop Shipments: Navigating Various States' Rules on Registrations and Exemptions

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Mastering Form 8937 and Section 6045B:

Presenting a live 110 minute teleconference with interactive Q&A Mastering Form 8937 and Section 6045B: An Ongoing Obligation Complying With Reporting Requirements Arising From Activities Affecting Tax

Presenting a live 110 minute teleconference with interactive Q&A Mastering Form 8937 and Section 6045B: An Ongoing Obligation Complying With Reporting Requirements Arising From Activities Affecting Tax

Are You Ready? Navigating the New IRS Process and Competency Exams

Presenting a live 110 minute webinar with interactive Q&A New Federal Tax Return Preparer Registration: Are You Ready? Navigating the New IRS Process and Competency Exams THURSDAY, OCTOBER 28, 2010 1pm

Presenting a live 110 minute webinar with interactive Q&A New Federal Tax Return Preparer Registration: Are You Ready? Navigating the New IRS Process and Competency Exams THURSDAY, OCTOBER 28, 2010 1pm