Optimal Labor Income Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

|

|

|

- Rosamond McCarthy

- 6 years ago

- Views:

Transcription

1 Optimal Labor Income Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1

2 TAXATION AND REDISTRIBUTION Key question: Do/should government reduce inequality using taxes and transfers? 1) Governments use taxes to raise revenue 2) This revenue funds transfer programs: a) Universal Transfers: Public Education, Health Care Benefits (only 65+ in the US), Retirement and Disability Benefits, Unemployment benefits b) Means-tested Transfers: In-kind (e.g., public housing or Medicaid in the US) and cash benefits Modern governments raise large fraction of GDP in taxes (30-50%) and spend significant fraction of GDP on transfers 2

3 FACTS ON US TAXES AND TRANSFERS References: Comprehensive description in: A) Taxes: (1) individual income tax (fed+state), (2) payroll taxes on earnings (fed, funds Social Security+Medicare), (3) corporate income tax (fed+state), (4) sales taxes (state)+excise taxes (state+fed), (5) property taxes (state) B) Means-tested Transfers: (1) refundable tax credits (fed), (2) in-kind transfers (fed+state): Medicaid, public housing, nutrition (SNAP), education, (3) cash welfare: TANF for single parents (fed+state), SSI for old/disabled (fed) 3

4 FEDERAL US INCOME TAX US income tax assessed on annual family income (not individual) [most other OECD countries have shifted to individual assessment] Sum all cash income sources from family members (both from labor and capital income sources) = called Adjusted Gross Income (AGI) Main exclusions: fringe benefits (health insurance, pension contributions), imputed rent of homeowners, interest from state+local bonds, unrealized capital gains 4

5 FEDERAL US INCOME TAX Taxable income = AGI - personal exemptions - deduction personal exemption = $ 3800 # family members (in 2012) deduction is max of standard deduction or itemized deductions Standard deduction is a fixed amount depending on family structure ($11.9K for couple, $5.95K for single in 2012) Itemized deductions: mortgage interest payments, charitable giving, state and local income taxes paid, various other small items [about 10% of AGI lost through itemized deductions, called tax expenditures] 5

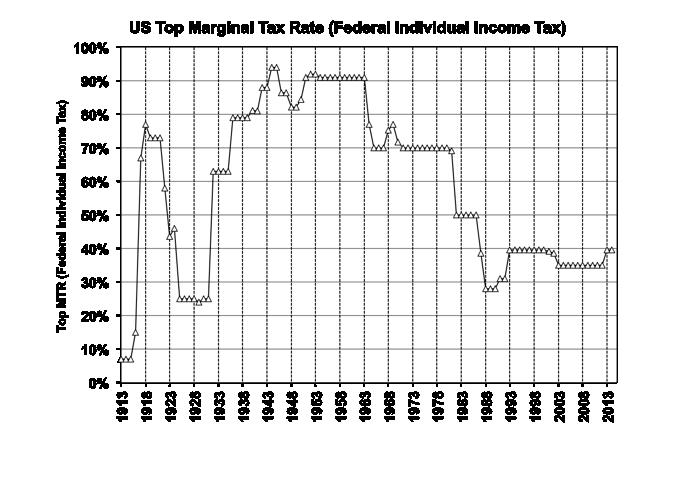

6 FEDERAL US INCOME TAX: TAX BRACKETS Tax T (z) is piecewise linear and continuous function of taxable income z with constant marginal tax rates (MTR) T (z) by brackets [draw graph] In 2013, 7 brackets with MTR 10%,15%,25%,28%,33%,35%, 39.6% (top bracket for z above $450K), indexed on price inflation Lower preferential rates (up to a max of 20%) apply to dividends (since 2003) and realized capital gains [in part to offset double taxation of corporate profits] Tax rates change frequently over time. Top MTRs have declined drastically since 1960s (as in most OECD countries) 6

7

8 FEDERAL US INCOME TAX: TAX CREDITS Tax credits: Additional reduction in taxes (1) Non refundable (cannot reduce taxes below zero): foreign tax credit, child care expenses, education credits, energy credits, and many others (2) Refundable (can reduce taxes below zero, i.e., be net transfers): EITC (earned income tax credit, up to $3.2K, $5K, $6K for working families with 1, 2, 3+ kids), Child Tax Credit ($1000 per kid, partly refundable) Refundable tax credits are now the largest means-tested cash transfer for low income families 8

9 FEDERAL US INCOME TAX: TAX FILING Taxes on year t earnings are withheld on paychecks during year t (pay-as-you-earn) Income tax return filed in Feb-April 15, year t + 1 [filers use either software or tax preparers, huge private industry, most OECD countries provide pre-populated returns] Most tax filers get a tax refund as withholdings > net taxes owed Payers (employers, banks, etc.) govt (3rd party reporting) send income information to 3rd party reporting + withholding at source is key for successful enforcement 9

10 MAIN MEANS-TESTED TRANSFER PROGRAMS 1) Traditional transfers: managed by welfare agencies, paid on monthly basis, high stigma and take-up costs low takeup rates (often only around 50%) Main programs: Medicaid (health insurance for low incomes), SNAP (former food stamps), public housing, TANF (welfare), SSI (aged+disabled) 2) Refundable income tax credits: managed by tax administration, paid as an annual lumpsum in year t + 1, low stigma and take-up cost high take-up rates Main programs: EITC and Child Tax Credit [large expansion since the 1990s] for low income working families with children 10

11 KEY CONCEPTS FOR TAXES/TRANSFERS Draw budget (z, z T (z)) which integrates taxes and transfers 1) Transfer benefit with zero earnings T (0) [sometimes called demogrant or lumpsum grant] 2) Marginal tax rate (or phasing-out rate) T (z): individual keeps 1 T (z) for an additional $1 of earnings (intensive labor supply response) 3) Participation tax rate τ p = [T (z) T (0)]/z: individual keeps fraction 1 τ p of earnings when moving from zero earnings to earnings z: z T (z) = T (0) + z (1 τ p ) (extensive labor supply response) 4) Break-even earnings point z : point at which T (z ) = 0 11

12 $50,000 US Tax/Transfer System, single parent with 2 children, 2009 $50,000 $40,000 $40,000 Welfare: TANF+SNAP Disposable arnings $30,000 $20,000 $10,000 $30,000 $20,000 $10,000 Tax credits: EITC+CTC Earnings after Fed+SSA taxes 45 Degree Line $0 $0 $0 $10,000 $20,000 $30,000 $40,000 $50,000 Gross Earnings (with employer payroll taxes) Source: Federal Govt

13 $50, Degree Line $40,000 US France Disposable income $30,000 $20,000 $10,000 $0 $0 $10,000 $20,000 $30,000 $40,000 $50,000 Gross Earnings (with employer payroll taxes)

14 Profile of Current Means-tested Transfers Traditional means-tested programs reduce incentives to work for low income workers Refundable tax credits have significantly increased incentive to work for low income workers However, refundable tax credits cannot benefit those with zero earnings Trade-off: US chooses to reward work more than most European countries (such as France) but therefore provides smaller benefits to those with no earnings 14

15 Optimal Taxation: Case with No Behavioral Responses Utility u(c) strictly increasing and concave Same for everybody where c is after tax income. Income is z and is fixed for each individual, c = z T (z) where T (z) is tax/transfer on z. N individuals with fixed incomes z 1 <... < z N Government maximizes Utilitarian objective: SW F = N i=1 u(z i T (z i )) subject to budget constraint N i=1 T (z i ) = 0 (taxes need to fund transfers) 15

16 Simple Model With No Behavioral Responses Replace T (z 1 ) = N i=2 T (z i ) from budget constraint: SW F = u z 1 + N i=2 T (z i ) + First order condition (FOC) in T (z i ): N i=2 u(z i T (z i )) 0 = SW F T (z i ) = u (z 1 T (z 1 )) u (z i T (z i )) = 0 u (z i T (z i )) = u (z 1 T (z 1 )) z i T (z i ) = constant across i Perfect equalization of after-tax income = 100% tax rate and redistribution. Utilitarianism with decreasing marginal utility leads to perfect egalitarianism [Edgeworth, 1897] Mathematically equivalent to perfect insurance result with risk aversion and no moral hazard 16

17 ISSUES WITH SIMPLE MODEL 1) No behavioral responses: Obvious missing piece: 100% redistribution would destroy incentives to work and thus the assumption that z is exogenous is unrealistic Optimal income tax theory incorporates behavioral responses 2) Issue with Utilitarianism: Even absent behavioral responses, many people would object to 100% redistribution [perceived as confiscatory] Citizens views on fairness impose bounds on redistribution govt can do [political economy / public choice theory] 17

18 EQUITY-EFFICIENCY TRADE-OFF Taxes can be used to raise revenue for transfer programs which can reduce inequality in disposable income Desirable if society feels that inequality is too large Taxes (and transfers) reduce incentives to work High tax rates create economic inefficiency if individual respond to taxes Size of behavioral response limits the ability of govt to redistribute with taxes/transfers Generates an equity-efficiency trade-off Empirical tax literature estimates the size of behavioral responses to taxation 18

19 Labor Supply Individual has utility over labor supply l and consumption c: u(c, l) increasing in c and decreasing in l [i.e., increasing in leisure] max u(c, l) subject to c = wl + R with w = w (1 τ) the net-of-tax wage ( w is before tax wage rate and τ is tax rate), and R non-labor income FOC w u c + u l = 0 Marshallian labor supply l = l(w, R) Uncompensated elasticity: Income effects: ε u = w l l w η = w l R 0 19

20 Labor Supply Substitution effects: Hicksian labor supply: l c (w, u) minimizes cost needed to reach u given slope w Compensated elasticity Slutsky equation ε c = w l lc w > 0 l c w = l w l l R εc = ε u η Tax rate τ discourages work through substitution effects (work pays less at the margin) Tax rate τ encourages work through income effects (taxes make you poorer and hence in more need of income) Net effect ambiguous (captured by sign of ε u ) 20

21 21.1 Taxation and Labor Supply Theory C H A P T E R 2 1 T A X E S O N L A B O R S U P P L Y Basic Theory The slope of Ava s budget constraint is now the after-tax wage. Public Finance and Public Policy Jonathan Gruber Third Edition Copyright 2010 Worth Publishers 5 of 29

22 21.1 Taxation and Labor Supply Theory C H A P T E R 2 1 T A X E S O N L A B O R S U P P L Y Basic Theory Substitution and Income Effects on Labor Supply Public Finance and Public Policy Jonathan Gruber Third Edition Copyright 2010 Worth Publishers 7 of 29

23 General nonlinear income tax [draw graph] With no taxes: c = z: consumption = earnings With taxes c = z T (z): consumption = earnings - net taxes T (z) 0 if individual pays taxes on net, T (z) 0 if individual receives transfers on net T (z) > 0 reduces net wage rate and reduces labor supply through substitution effects T (z) 0 reduces disposable income and increases labor supply through income effects T (z) 0 increases disposable income and decreases labor supply through income effects Transfer program such that T (z) < 0 and T (z) > 0 always discourages labor supply 22

24 OPTIMAL LINEAR TAX RATE: LAFFER CURVE c = (1 τ) z + R with τ linear tax rate and R fixed universal transfer funded by taxes τz with Z average earnings Individual i choose l to maximize u i ((1 τ) w i l i + R, l i ) labor supply choices l i determine individual earnings z i = w i l i which aggregate to average earnings Z(1 τ) = i z i /N Tax Revenue per person R(τ) = τ Z(1 τ) is inversely U- shaped with τ: R(τ = 0) = 0 (no taxes) and R(τ = 1) = 0 (nobody works): called the Laffer Curve 23

25 20.3 Optimal Income Taxes C H A P T E R 2 0 T A X I N E F F I C I E N C I E S A N D T H E I R I M P L I C A T I O N S F O R O P T I M A L T A X A T I O N General Model with Behavioral Effects Public Finance and Public Policy Jonathan Gruber Third Edition Copyright 2010 Worth Publishers 22 of 30

26 OPTIMAL LINEAR TAX RATE: LAFFER CURVE Top of the Laffer Curve is at τ maximizing tax revenue: 0 = R (τ ) = Z τ dz d(1 τ) τ 1 τ 1 τ dz Z d(1 τ) = 1 Revenue maximizing tax rate: τ = e with e = 1 τ Z dz d(1 τ) e is the elasticity of reported income with respect to the netof-tax rate 1 τ Inefficient to have τ > τ because decreasing τ would make taxpayers better off (they pay less taxes) and would increase tax revenue for the government If government is Rawlsian (maximizes welfare of the worstoff person with no earnings) then τ = 1/(1 + e) is optimal to make transfer R(τ) as large as possible 25

27 OPTIMAL LINEAR TAX RATE: FORMULA Government chooses τ to maximize utilitarian social welfare SW F = i u i ((1 τ)w i l i + τz(1 τ), l i ) taking into account that labor supply l i responds to taxation and hence that this affects the total tax revenue τ Z(1 τ) that is redistributed back as transfer Government first order condition: (using the envelope theorem as l i maximizes u i ): 0 = dsw F dτ = i u i c [ dz Z z i τ d(1 τ) ], 26

28 OPTIMAL LINEAR TAX RATE: FORMULA Hence, we have the following optimal linear income tax formula τ = 1 ḡ 1 ḡ + e with ḡ = i z i ui c Z i ui c 0 ḡ < 1 as ui c is decreasing with z i (marginal utility falls with consumption) τ decreases with elasticity e [efficiency] and with parameter ḡ [equity] ḡ is low and τ close to Laffer rate τ = 1/(1 + e) when (a) inequality is high (b) marginal utility decreases fast with income Formula captures the equity-efficiency trade-off 27

29 OPTIMAL TOP INCOME TAX RATE (Diamond and Saez JEP 11) In practice, individual income tax is progressive with brackets with increasing marginal tax rates. What is the optimal top tax rate? Consider constant MTR τ above fixed z. optimal τ Goal is to derive In the US in 2013, τ = 39.6% and z = $450, 000 ( top 1%). Denote by z(1 τ) average income of top bracket earners [depends on net-of-tax rate 1 τ], with elasticity e = [(1 τ)/z] dz/d(1 τ) Suppose the government wants to maximize tax revenue collected from top bracket taxpayers (e.g. marginal utility of consumption of top 1% earners is small relative to average) 28

30 Optimal Top Income Tax Rate (Mirrlees 71 model) Disposable Income c=z-t(z) Top bracket: Slope 1-τ z*-t(z*) Reform: Slope 1-τ dτ 0 Source: Diamond and Saez JEP'11 z* Market income z

31 Optimal Top Income Tax Rate (Mirrlees 71 model) Disposable Income c=z-t(z) Mechanical tax increase: dτ[z-z*] z*-t(z*) Behavioral Response tax loss: τ dz = - dτ e z τ/(1-τ) 0 z* z Market income z Source: Diamond and Saez JEP'11

32 OPTIMAL TOP INCOME TAX RATE Consider small dτ > 0 reform above z. 1) Mechanical increase in tax revenue: dm = [z z ]dτ 2) Behavioral response reduces tax revenue: db = τdz = τ dz d(1 τ) dτ = τ 1 τ 1 τ z db = τ 1 τ e z dτ dz d(1 τ) z dτ 30

33 OPTIMAL TOP INCOME TAX RATE dm + db = dτ Optimal τ such that dm + db = 0 Optimal top tax rate: τ = { [z z τ ] e 1 τ z a e } 1 τ τ = 1 e z z z with a = z z z Optimal τ decreases with e [efficiency] Optimal τ decrease with a [thinness of top tail] Empirically a 1.5, easy to estimate using distributional data Empirically e is harder to estimate [controversial] Example: If e =.25 then τ = 1/( ) = 1/1.75 = 73% 31

34 Empirical Pareto Coefficient z* = Adjusted Gross Income (current 2005 $) a=zm/(zm-z*) with zm=e(z z>z*) alpha=z*h(z*)/(1-h(z*)) Source: Diamond and Saez JEP'11

35 REAL VS. TAX AVOIDANCE RESPONSES Behavioral response to income tax comes not only from reduced labor supply but also shifts to other forms of income or activities: (untaxed fringe benefits, shift to corporate income tax base, shift toward tax favored capital gains, etc.) Real vs. tax avoidance responses matters for 2 reasons: 1) Government can control tax avoidance through other tools: closing loopholes, broadening the tax base Elasticity e is lower with no loopholes 2) Most tax avoidance responses create fiscal externalities in the sense that tax revenue increases at other time periods or in other tax bases: e.g., US top tax rate increased in 2013, taxpayers likely shifted part of their income to 2012 to avoid higher tax rates 33

36 REAL VS. AVOIDANCE RESPONSES Key policy question: Is it possible to eliminate avoidance responses using base broadening, etc.? or would new avoidance schemes keep popping up? a) Some forms of tax avoidance are due to poorly designed tax codes (preferential treatment for some income forms, deductions) b) Some forms of tax avoidance/evasion can only be addressed with international cooperation (off-shore tax evasion in tax heavens, multinational corporations shifting profits to low tax countries) c) Some forms of tax avoidance/evasion are due to technological limitations of tax collection (impossible to tax informal cash businesses, or fully control consumption within the firm) 34

37 OPTIMAL PROFILE OF TRANSFERS If individuals respond to taxes only through intensive margin (how much they work at the margin and not whether they work), optimal transfer at bottom takes the form of a Negative Income Tax : 1) Lumpsum grant T (0) for those with no earnings 2) High MTRs T (z) at the bottom to phase-out the lumpsum grant quickly Intuition: high MTRs at bottom are efficient because: (a) they target transfers to the most needy (b) earnings at the bottom are low to start with so intensive response does not generate large output losses 35

38 Optimal Transfers: Participation Responses Empirical literature shows that participation labor supply responses [whether to work or not] are large at the bottom [much larger and clearer than intensive responses] Participation depends on participation tax rate: τ p = [T (z) T (0)]/z: individual keeps fraction 1 τ p of earnings when moving from zero earnings to earnings z: z T (z) = T (0) + z (1 τ p ) Key result: in-work subsidies with T (z) < 0 (such as EITC) become optimal when labor supply responses are concentrated along extensive margin and govt cares about low income workers. 36

39 Starting from a Means-Tested Program Consumption c G 0 45 o w* Earnings w Source: revised version of Saez (2002), p. 1050

40 Consumption c Starting from a Means-Tested Program Introducing a small EITC is desirable for redistribution G 0 45 o w* Earnings w Source: revised version of Saez (2002), p. 1050

41 Consumption c Starting from a Means-Tested Program Introducing a small EITC is desirable for redistribution Participation response saves government revenue G 45 o w* 0 Earnings w Source: revised version of Saez (2002), p. 1050

42 ACTUAL TAX/TRANSFER SYSTEMS 1) Transfer programs used to be of the traditional form with high phasing-out rates (sometimes above 100%) No incentives to work (even with modest elasticities) Initially designed for groups not expected to work [widows in the US] but later attracting groups who could potentially work [single mothers] 2) In-work benefits have been introduced and expanded in OECD countries since 1980s (US EITC, UK Family Credit, etc.) and have been politically successful (a) Redistribute to low income workers, (b) improve incentives to work 38

43 IN-KIND REDISTRIBUTION Most means-tested transfers are in-kind and often rationed (health care, child care, education, public housing, nutrition subsidies) [care not cash San Francisco reform] 1) Rational Individual perspective: (a) If in-kind transfer is tradeable at market price in-kind equivalent to cash (b) If in-kind transfer non-tradeable in-kind inferior to cash Cash transfer preferable to in-kind transfer from individual perspective 39

44 IN-KIND REDISTRIBUTION 2) Social perspective: 4 justifications: a) Commodity Egalitarianism: some goods (education, health, shelter, food) seen as rights and ought to be provided to all b) Paternalism: society imposes its preferences on recipients [recipients prefer cash] c) Behavioral: Recipients do not make choices in their best interests (self-control, myopia) [recipients understand that inkind is better for them] d) Efficiency: It could be efficient to give in-kind benefits if it can prevent those who don t need them badly from getting them (i.e., force people to queue to get free soup) 40

45 FAMILY TAXATION: MARRIAGE AND CHILDREN Two important issues in policy debate: 1) Marriage: What is the optimal taxation of couples vs. singles? Should secondary earnings be treated differently? 2) Children: What should be the net transfer (transfer or tax reduction) for family with children (as a function of family income and structure)? 41

46 TAXATION OF COUPLES Three potentially desirable properties: (1) income tax should be based on resources (i.e., family income as families share their income) (2) income tax should be marriage neutral: no higher/lower tax when two single individuals marry (3) income tax should be progressive (i.e., higher incomes pay a larger fraction of their income in taxes) It is impossible to have a tax system that satisfies all 3 conditions simultaneously: Income tax that is based on family income and marriage neutral has to satisfy: T (z h + z w ) = T (z h ) + T (z w ) and hence be linear i.e. T (z) = τ z 42

47 TAXATION OF COUPLES (1) If marriage responds to tax/transfer differential better to reduce marriage penalty, i.e., move toward individualized system Particularly important when cohabitation is close substitute for marriage (Scandinavian countries) (2) If labor supply of secondary earners more elastic than labor supply of primary earner Secondary earnings should be taxed less (Boskin-Sheshinski JpubE 83) Labor supply elasticity differential is decreasing over time as earnings gender gap decreases 43

48 TRANSFERS OR TAX CREDITS FOR CHILDREN 1) Children reduce normalized income Children increase marginal utility of consumption Transfer for children T kid should be positive In practice, transfers for children are always positive 2) Should T kid (z) increase with income z? Pro: rich spend more on their kids than lower income families Cons: Lower income families need child transfers most In practice, T kid (z) is fairly constant with z Europe has much more generous pre-kindergarten child care benefits, US has more generous cash tax credits for families with children 44

49 REFERENCES Diamond, P. and E. Saez From Basic Research to Policy Recommendations: The Case for a Progressive Tax, Journal of Economic Perspectives, 25(4), 2011, (web) 45

Optimal Labor Income Taxation (follows loosely Chapters of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

131 Undergraduate Public Economics Emmanuel Saez UC Berkeley") Optimal Labor Income Taxation (follows loosely Chapters 20-21 of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Should government reduce

Optimal Labor Income Taxation (follows loosely Chapters 20-21 of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Should government reduce

Lecture 4: Optimal Labor Income Taxation

78 Lecture 4: Optimal Labor Income Taxation Stefanie Stantcheva Fall 2017 78 TAXATION AND REDISTRIBUTION Key question: Should government reduce inequality using taxes and transfers? 1) Governments use

78 Lecture 4: Optimal Labor Income Taxation Stefanie Stantcheva Fall 2017 78 TAXATION AND REDISTRIBUTION Key question: Should government reduce inequality using taxes and transfers? 1) Governments use

Top MTR. Threshold/Averag e Income. US Top Marginal Tax Rate and Top Bracket Threshold. Top MTR (Federal Individual Income Tax)

") Source: IRS, Statistics of Income Division, Historical Table 23 Top Marginal Tax Rate and Top Bracket Threshold Top MTR (Federal Individual Income Tax) 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% Top MTR

Source: IRS, Statistics of Income Division, Historical Table 23 Top Marginal Tax Rate and Top Bracket Threshold Top MTR (Federal Individual Income Tax) 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% Top MTR

Optimal Labor Income Taxation. Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011

Optimal Labor Income Taxation Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011 MODERN ECONOMIES DO SIGNIFICANT REDISTRIBUTION 1) Taxes:

Optimal Labor Income Taxation Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011 MODERN ECONOMIES DO SIGNIFICANT REDISTRIBUTION 1) Taxes:

Econ 230B Spring FINAL EXAM: Solutions

Econ 230B Spring 2017 FINAL EXAM: Solutions The average grade for the final exam is 45.82 (out of 60 points). The average grade including all assignments is 79.38. The distribution of course grades is:

Econ 230B Spring 2017 FINAL EXAM: Solutions The average grade for the final exam is 45.82 (out of 60 points). The average grade including all assignments is 79.38. The distribution of course grades is:

Lectures 9 and 10: Optimal Income Taxes and Transfers

Lectures 9 and 10: Optimal Income Taxes and Transfers Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 36 Agenda 1 Redistribution vs. Effi ciency 2 The Mirrlees optimal nonlinear

Lectures 9 and 10: Optimal Income Taxes and Transfers Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 36 Agenda 1 Redistribution vs. Effi ciency 2 The Mirrlees optimal nonlinear

Optimal tax and transfer policy

Optimal tax and transfer policy (non-linear income taxes and redistribution) March 2, 2016 Non-linear taxation I So far we have considered linear taxes on consumption, labour income and capital income

Optimal tax and transfer policy (non-linear income taxes and redistribution) March 2, 2016 Non-linear taxation I So far we have considered linear taxes on consumption, labour income and capital income

Theoretical Tools of Public Finance. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Theoretical Tools of Public Finance 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 THEORETICAL AND EMPIRICAL TOOLS Theoretical tools: The set of tools designed to understand the mechanics

Theoretical Tools of Public Finance 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 THEORETICAL AND EMPIRICAL TOOLS Theoretical tools: The set of tools designed to understand the mechanics

ECON 4624 Income taxation 1/24

ECON 4624 Income taxation 1/24 Why is it important? An important source of revenue in most countries (60-70%) Affect labour and capital (savings) supply and overall economic activity how much depend on

ECON 4624 Income taxation 1/24 Why is it important? An important source of revenue in most countries (60-70%) Affect labour and capital (savings) supply and overall economic activity how much depend on

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 REMINDER: Two General Rules for Government Intervention

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 REMINDER: Two General Rules for Government Intervention

Lecture 3: Optimal Income Taxation (II)

") 52 Lecture 3: Optimal Income Taxation (II) Stefanie Stantcheva Fall 2016 52 GOALS OF THIS LECTURE 1) Illustration of structural vs. policy elasticities using the example of the linear top tax rate. 2)

52 Lecture 3: Optimal Income Taxation (II) Stefanie Stantcheva Fall 2016 52 GOALS OF THIS LECTURE 1) Illustration of structural vs. policy elasticities using the example of the linear top tax rate. 2)

Econ 551 Government Finance: Revenues Winter 2018

Econ 551 Government Finance: Revenues Winter 2018 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture 8c: Taxing High Income Workers ECON 551: Lecture 8c 1 of 34

Econ 551 Government Finance: Revenues Winter 2018 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture 8c: Taxing High Income Workers ECON 551: Lecture 8c 1 of 34

Econ 131 Spring 2017 Emmanuel Saez. Problem Set 2. DUE DATE: March 8. Student Name: Student ID: GSI Name:

Econ 131 Spring 2017 Emmanuel Saez Problem Set 2 DUE DATE: March 8 Student Name: Student ID: GSI Name: You must submit your solutions using this template. Although you may work in groups, each student

Econ 131 Spring 2017 Emmanuel Saez Problem Set 2 DUE DATE: March 8 Student Name: Student ID: GSI Name: You must submit your solutions using this template. Although you may work in groups, each student

Public Finance and Public Policy: Responsibilities and Limitations of Government. Presentation notes, chapter 9. Arye L. Hillman

Public Finance and Public Policy: Responsibilities and Limitations of Government Arye L. Hillman Cambridge University Press, 2009 Second edition Presentation notes, chapter 9 CHOICE OF TAXATION Topics

Public Finance and Public Policy: Responsibilities and Limitations of Government Arye L. Hillman Cambridge University Press, 2009 Second edition Presentation notes, chapter 9 CHOICE OF TAXATION Topics

TAXES, TRANSFERS, AND LABOR SUPPLY. Henrik Jacobsen Kleven London School of Economics. Lecture Notes for PhD Public Finance (EC426): Lent Term 2012

: Lent Term 2012") TAXES, TRANSFERS, AND LABOR SUPPLY Henrik Jacobsen Kleven London School of Economics Lecture Notes for PhD Public Finance (EC426): Lent Term 2012 AGENDA Why care about labor supply responses to taxes and

TAXES, TRANSFERS, AND LABOR SUPPLY Henrik Jacobsen Kleven London School of Economics Lecture Notes for PhD Public Finance (EC426): Lent Term 2012 AGENDA Why care about labor supply responses to taxes and

GPP 501 Microeconomic Analysis for Public Policy Fall 2017

GPP 501 Microeconomic Analysis for Public Policy Fall 2017 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture October 3rd: Redistribution theory GPP501: Lecture

GPP 501 Microeconomic Analysis for Public Policy Fall 2017 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture October 3rd: Redistribution theory GPP501: Lecture

Introductory Economics of Taxation. Lecture 1: The definition of taxes, types of taxes and tax rules, types of progressivity of taxes

Introductory Economics of Taxation Lecture 1: The definition of taxes, types of taxes and tax rules, types of progressivity of taxes 1 Introduction Introduction Objective of the course Theory and practice

Introductory Economics of Taxation Lecture 1: The definition of taxes, types of taxes and tax rules, types of progressivity of taxes 1 Introduction Introduction Objective of the course Theory and practice

Public Economics (ECON 131) Section #4: Labor Income Taxation

Section #4: Labor Income Taxation") Public Economics (ECON 131) Section #4: Labor Income Taxation September 22 to 27, 2016 Contents 1 Implications of Tax Inefficiencies for Optimal Taxation 2 1.1 Key concepts..........................................

Public Economics (ECON 131) Section #4: Labor Income Taxation September 22 to 27, 2016 Contents 1 Implications of Tax Inefficiencies for Optimal Taxation 2 1.1 Key concepts..........................................

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics

Henrik Jacobsen Kleven London School of Economics") LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

PERSONAL INCOME TAXES

PERSONAL INCOME TAXES CHAPTER 35 WHERE PERSONAL INCOME TAXES FIT In 2008 the federal government collected $2,524 billion in taxes. $1,146 billion of that was collected from the personal income tax. The

PERSONAL INCOME TAXES CHAPTER 35 WHERE PERSONAL INCOME TAXES FIT In 2008 the federal government collected $2,524 billion in taxes. $1,146 billion of that was collected from the personal income tax. The

TAXABLE INCOME RESPONSES. Henrik Jacobsen Kleven London School of Economics. Lecture Notes for MSc Public Economics (EC426): Lent Term 2014

: Lent Term 2014") TAXABLE INCOME RESPONSES Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Economics (EC426): Lent Term 2014 AGENDA The Elasticity of Taxable Income (ETI): concept and policy

TAXABLE INCOME RESPONSES Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Economics (EC426): Lent Term 2014 AGENDA The Elasticity of Taxable Income (ETI): concept and policy

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK Mike Brewer, IFS Emmanuel Saez, UC Berkeley Andrew Shephard, UCL and IFS March 20, 2007 Abstract This paper proposes an

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK Mike Brewer, IFS Emmanuel Saez, UC Berkeley Andrew Shephard, UCL and IFS March 20, 2007 Abstract This paper proposes an

Optimal Progressivity

Optimal Progressivity To this point, we have assumed that all individuals are the same. To consider the distributional impact of the tax system, we will have to alter that assumption. We have seen that

Optimal Progressivity To this point, we have assumed that all individuals are the same. To consider the distributional impact of the tax system, we will have to alter that assumption. We have seen that

Chapter 3 Introduction to the General Equilibrium and to Welfare Economics

Chapter 3 Introduction to the General Equilibrium and to Welfare Economics Laurent Simula ENS Lyon 1 / 54 Roadmap Introduction Pareto Optimality General Equilibrium The Two Fundamental Theorems of Welfare

Chapter 3 Introduction to the General Equilibrium and to Welfare Economics Laurent Simula ENS Lyon 1 / 54 Roadmap Introduction Pareto Optimality General Equilibrium The Two Fundamental Theorems of Welfare

International Tax Competition: Zero Tax Rate at the Top Re-established

International Tax Competition: Zero Tax Rate at the Top Re-established Tomer Blumkin, Efraim Sadka and Yotam Shem-Tov April 2012, Munich Some Background The general setting examined in Mirrlees (1971)

International Tax Competition: Zero Tax Rate at the Top Re-established Tomer Blumkin, Efraim Sadka and Yotam Shem-Tov April 2012, Munich Some Background The general setting examined in Mirrlees (1971)

NBER WORKING PAPER SERIES THE ELASTICITY OF TAXABLE INCOME WITH RESPECT TO MARGINAL TAX RATES: A CRITICAL REVIEW

NBER WORKING PAPER SERIES THE ELASTICITY OF TAXABLE INCOME WITH RESPECT TO MARGINAL TAX RATES: A CRITICAL REVIEW Emmanuel Saez Joel B. Slemrod Seth H. Giertz Working Paper 15012 http://www.nber.org/papers/w15012

NBER WORKING PAPER SERIES THE ELASTICITY OF TAXABLE INCOME WITH RESPECT TO MARGINAL TAX RATES: A CRITICAL REVIEW Emmanuel Saez Joel B. Slemrod Seth H. Giertz Working Paper 15012 http://www.nber.org/papers/w15012

Taxable Income Elasticities. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Taxable Income Elasticities 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of

Taxable Income Elasticities 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of

Tax Policy for Low-Income Families: The Earned Income Tax Credit

Tax Policy for Low-Income Families: The Earned Income Tax Credit Hilary Hoynes, University of California, Davis Tax Policy in the Obama Era January 30, 2009 1 Overview and Issues In the last 15 years,

Tax Policy for Low-Income Families: The Earned Income Tax Credit Hilary Hoynes, University of California, Davis Tax Policy in the Obama Era January 30, 2009 1 Overview and Issues In the last 15 years,

State and Local Government Expenditures. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

State and Local Government Expenditures 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 FISCAL FEDERALISM optimal fiscal federalism: The question of which activities should take place at

State and Local Government Expenditures 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 FISCAL FEDERALISM optimal fiscal federalism: The question of which activities should take place at

THE ELASTICITY OF TAXABLE INCOME Fall 2012

THE ELASTICITY OF TAXABLE INCOME 14.471 - Fall 2012 1 Why Focus on "Elasticity of Taxable Income" (ETI)? i) Captures Not Just Hours of Work but Other Changes (Effort, Structure of Compensation, Occupation/Career

THE ELASTICITY OF TAXABLE INCOME 14.471 - Fall 2012 1 Why Focus on "Elasticity of Taxable Income" (ETI)? i) Captures Not Just Hours of Work but Other Changes (Effort, Structure of Compensation, Occupation/Career

Reflections on capital taxation

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Module 10. Lecture 37

Module 10 Lecture 37 Topics 10.21 Optimal Commodity Taxation 10.22 Optimal Tax Theory: Ramsey Rule 10.23 Ramsey Model 10.24 Ramsey Rule to Inverse Elasticity Rule 10.25 Ramsey Problem 10.26 Ramsey Rule:

Module 10 Lecture 37 Topics 10.21 Optimal Commodity Taxation 10.22 Optimal Tax Theory: Ramsey Rule 10.23 Ramsey Model 10.24 Ramsey Rule to Inverse Elasticity Rule 10.25 Ramsey Problem 10.26 Ramsey Rule:

Topic 2-3: Policy Design: Unemployment Insurance and Moral Hazard

Introduction Trade-off Optimal UI Empirical Topic 2-3: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 27 Introduction

Introduction Trade-off Optimal UI Empirical Topic 2-3: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 27 Introduction

Redistribution and Tax Expenditures: The Earned Income Tax Credit

Redistribution and Tax Expenditures: The Earned Income Tax Credit Nada Eissa, Georgetown University Hilary Hoynes, University of California, Davis Tax Expenditures Project Conference March 2008 1 Overview

Redistribution and Tax Expenditures: The Earned Income Tax Credit Nada Eissa, Georgetown University Hilary Hoynes, University of California, Davis Tax Expenditures Project Conference March 2008 1 Overview

Labor Supply Responses to Taxes and Transfers. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Labor Supply Responses to Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 MOTIVATION 1) Labor supply responses to taxation are of fundamental importance for income tax

Labor Supply Responses to Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 MOTIVATION 1) Labor supply responses to taxation are of fundamental importance for income tax

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK Mike Brewer, IFS Emmanuel Saez, UC Berkeley Andrew Shephard, UCL and IFS February 18, 2008 Abstract This paper proposes

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK Mike Brewer, IFS Emmanuel Saez, UC Berkeley Andrew Shephard, UCL and IFS February 18, 2008 Abstract This paper proposes

The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review

The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review Emmanuel Saez, University of California Berkeley and NBER Joel Slemrod, University of Michigan and NBER Seth H. Giertz,

The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review Emmanuel Saez, University of California Berkeley and NBER Joel Slemrod, University of Michigan and NBER Seth H. Giertz,

Economics 2450A: Public Economics Section 7: Optimal Top Income Taxation

Economics 2450A: Public Economics Section 7: Optimal Top Income Taxation Matteo Paradisi October 24, 2016 In this Section we study the optimal design of top income taxes. 1 We have already covered optimal

Economics 2450A: Public Economics Section 7: Optimal Top Income Taxation Matteo Paradisi October 24, 2016 In this Section we study the optimal design of top income taxes. 1 We have already covered optimal

Optimal Redistribution in an Open Economy

Optimal Redistribution in an Open Economy Oleg Itskhoki Harvard University Princeton University January 8, 2008 1 / 29 How should society respond to increasing inequality? 2 / 29 How should society respond

Optimal Redistribution in an Open Economy Oleg Itskhoki Harvard University Princeton University January 8, 2008 1 / 29 How should society respond to increasing inequality? 2 / 29 How should society respond

Econ 892 Taxation Sept 13, Introduction. First Welfare Theorem (illustration by the Edgeworth Box)

") Econ 892 Taxation Sept 13, 2011 Introduction First Welfare Theorem (illustration by the Edgeworth Box) The competitive equilibrium (the tangency) is Pareto efficient unless Public goods (positive externality)

Econ 892 Taxation Sept 13, 2011 Introduction First Welfare Theorem (illustration by the Edgeworth Box) The competitive equilibrium (the tangency) is Pareto efficient unless Public goods (positive externality)

Reported Incomes and Marginal Tax Rates, : Evidence and Policy Implications

Very Preliminary - Comments Welcome Reported Incomes and Marginal Tax Rates, 1960-2000: Evidence and Policy Implications Emmanuel Saez, UC Berkeley and NBER August 23, 2003 Abstract This paper use income

Very Preliminary - Comments Welcome Reported Incomes and Marginal Tax Rates, 1960-2000: Evidence and Policy Implications Emmanuel Saez, UC Berkeley and NBER August 23, 2003 Abstract This paper use income

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK Mike Brewer, IFS Emmanuel Saez, UC Berkeley Andrew Shephard, UCL and IFS December 20, 2007 Abstract This paper proposes

Optimal Household Labor Income Tax and Transfer Programs: An Application to the UK Mike Brewer, IFS Emmanuel Saez, UC Berkeley Andrew Shephard, UCL and IFS December 20, 2007 Abstract This paper proposes

Generalized Social Marginal Welfare Weights for Optimal Tax Theory

Generalized Social Marginal Welfare Weights for Optimal Tax Theory Emmanuel Saez, UC Berkeley Stefanie Stantcheva, MIT January 2013 AEA Meetings 1 MOTIVATION Welfarism is the dominant approach in optimal

Generalized Social Marginal Welfare Weights for Optimal Tax Theory Emmanuel Saez, UC Berkeley Stefanie Stantcheva, MIT January 2013 AEA Meetings 1 MOTIVATION Welfarism is the dominant approach in optimal

Do In-Work Tax Credits Serve as a Safety Net?

Do In-Work Tax Credits Serve as a Safety Net? Hilary W. Hoynes (UC Berkeley) Joint with Marianne Bitler (UC Irvine) Elira Kuka (UC Davis) Motivation In the past 2 decades, the safety net for low income

Do In-Work Tax Credits Serve as a Safety Net? Hilary W. Hoynes (UC Berkeley) Joint with Marianne Bitler (UC Irvine) Elira Kuka (UC Davis) Motivation In the past 2 decades, the safety net for low income

14.41 Final Exam Jonathan Gruber. True/False/Uncertain (95% of credit based on explanation; 5 minutes each)

") 14.41 Final Exam Jonathan Gruber True/False/Uncertain (95% of credit based on explanation; 5 minutes each) 1) The definition of property rights will eliminate the problem of externalities. Uncertain. Also

14.41 Final Exam Jonathan Gruber True/False/Uncertain (95% of credit based on explanation; 5 minutes each) 1) The definition of property rights will eliminate the problem of externalities. Uncertain. Also

The Theory of Taxation and Public Economics

louis kaplow The Theory of Taxation and Public Economics a princeton university press princeton and oxford 01_Kaplow_Prelims_p00i-pxxii.indd iii Summary of Contents a Preface xvii 1. Introduction 1 PART

louis kaplow The Theory of Taxation and Public Economics a princeton university press princeton and oxford 01_Kaplow_Prelims_p00i-pxxii.indd iii Summary of Contents a Preface xvii 1. Introduction 1 PART

Our Tax System Revealed. Lee R. Nackman, Ph.D. October 24, 2018

Our Tax System Revealed Lee R. Nackman, Ph.D. October 24, 2018!1 Topics Tax System Desiderata Follow the Money! Social Security Payroll Taxes Sales Taxes Federal Individual Income Taxes The Big Picture:

Our Tax System Revealed Lee R. Nackman, Ph.D. October 24, 2018!1 Topics Tax System Desiderata Follow the Money! Social Security Payroll Taxes Sales Taxes Federal Individual Income Taxes The Big Picture:

Lecture 4: Taxation and income distribution

Lecture 4: Taxation and income distribution Public Economics 336/337 University of Toronto Public Economics 336/337 (Toronto) Lecture 4: Income distribution 1 / 33 Introduction In recent years we have

Lecture 4: Taxation and income distribution Public Economics 336/337 University of Toronto Public Economics 336/337 (Toronto) Lecture 4: Income distribution 1 / 33 Introduction In recent years we have

3. The Deadweight Loss of Taxation

3. The Deadweight Loss of Taxation Laurent Simula ENS de Lyon 1 / 48 INTRODUCTION 2 / 48 The efficiency costs associated with taxation Government raises taxes for one of two reasons: 1. To raise revenue

3. The Deadweight Loss of Taxation Laurent Simula ENS de Lyon 1 / 48 INTRODUCTION 2 / 48 The efficiency costs associated with taxation Government raises taxes for one of two reasons: 1. To raise revenue

Lecture 9: Social Insurance: General Concepts

18 Lecture 9: Social Insurance: General Concepts Stefanie Stantcheva Fall 2017 18 DEFINITION Social insurance programs: Government interventions in the provision of insurance against adverse events: Examples:

18 Lecture 9: Social Insurance: General Concepts Stefanie Stantcheva Fall 2017 18 DEFINITION Social insurance programs: Government interventions in the provision of insurance against adverse events: Examples:

Public Economics Taxation II: Optimal Taxation

Public Economics Taxation II: Optimal Taxation Iñigo Iturbe-Ormaetxe U. of Alicante Winter 2012 I. Iturbe-Ormaetxe (U. of Alicante) Public Economics Taxation II: Optimal Taxation Winter 2012 1 / 98 Outline

Public Economics Taxation II: Optimal Taxation Iñigo Iturbe-Ormaetxe U. of Alicante Winter 2012 I. Iturbe-Ormaetxe (U. of Alicante) Public Economics Taxation II: Optimal Taxation Winter 2012 1 / 98 Outline

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings Raj Chetty, Harvard and NBER John N. Friedman, Harvard and NBER Emmanuel Saez, UC Berkeley and NBER April

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings Raj Chetty, Harvard and NBER John N. Friedman, Harvard and NBER Emmanuel Saez, UC Berkeley and NBER April

Sarah K. Burns James P. Ziliak. November 2013

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Lecture on Taxable Income Elasticities PhD Course in Uppsala

Lecture on Taxable Income Elasticities PhD Course in Uppsala Håkan Selin Institute for Evaluation of Labour Market and Education Policy Uppsala, May 15, 2014 1 TAXABLE INCOME ELASTICITIES Modern public

Lecture on Taxable Income Elasticities PhD Course in Uppsala Håkan Selin Institute for Evaluation of Labour Market and Education Policy Uppsala, May 15, 2014 1 TAXABLE INCOME ELASTICITIES Modern public

Corporate Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 24 24.1 What Are Corporations and Why Do We Tax Them? 24.2 The Structure of the Corporate Tax 24.3 The

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 24 24.1 What Are Corporations and Why Do We Tax Them? 24.2 The Structure of the Corporate Tax 24.3 The

Topic 11: Disability Insurance

Topic 11: Disability Insurance Nathaniel Hendren Harvard Spring, 2018 Nathaniel Hendren (Harvard) Disability Insurance Spring, 2018 1 / 63 Disability Insurance Disability insurance in the US is one of

Topic 11: Disability Insurance Nathaniel Hendren Harvard Spring, 2018 Nathaniel Hendren (Harvard) Disability Insurance Spring, 2018 1 / 63 Disability Insurance Disability insurance in the US is one of

Do Taxpayers Bunch at Kink Points?

Do Taxpayers Bunch at Kink Points? Emmanuel Saez University of California at Berkeley and NBER June 13, 2002 Abstract This paper uses individual tax returns micro data from 1960 to 1997 to analyze whether

Do Taxpayers Bunch at Kink Points? Emmanuel Saez University of California at Berkeley and NBER June 13, 2002 Abstract This paper uses individual tax returns micro data from 1960 to 1997 to analyze whether

Introduction and Literature Model and Results An Application: VAT. Malas Notches. Ben Lockwood 1. University of Warwick and CEPR. ASSA, 6 January 2018

Ben 1 University of Warwick and CEPR ASSA, 6 January 2018 Introduction Important new development in public economics - the sucient statistic approach, which "derives formulas for the welfare consequences

Ben 1 University of Warwick and CEPR ASSA, 6 January 2018 Introduction Important new development in public economics - the sucient statistic approach, which "derives formulas for the welfare consequences

Individual Income Taxation

Chapter 3 Individual Income Taxation 3.1 Introduction The individual income tax is the most important single tax in many countries. The basic principle of the individual income tax is that the taxpayer

Chapter 3 Individual Income Taxation 3.1 Introduction The individual income tax is the most important single tax in many countries. The basic principle of the individual income tax is that the taxpayer

Income Redistribution. Inequality, reasons for intervention, and social welfare programs

Income Redistribution Inequality, reasons for intervention, and social welfare programs Inequality and Poverty Income redistribution is justified on a number of different grounds Some want to lessen income

Income Redistribution Inequality, reasons for intervention, and social welfare programs Inequality and Poverty Income redistribution is justified on a number of different grounds Some want to lessen income

Labour Supply and Taxes

Labour Supply and Taxes Barra Roantree Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic how should

Labour Supply and Taxes Barra Roantree Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic how should

Welfare Reform in Switzerland

Welfare Reform in Switzerland A microsimulation case study for Basel Michael Gerfin University of Bern and IZA, Bonn This version: 24 May 2006 Please do not quote. Comments welcome. Acknowledgements: This

Welfare Reform in Switzerland A microsimulation case study for Basel Michael Gerfin University of Bern and IZA, Bonn This version: 24 May 2006 Please do not quote. Comments welcome. Acknowledgements: This

Taxation-Overview (Chapter 18)

") (Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

(Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

Political Economy. Pierre Boyer. Master in Economics Fall 2018 Schedule: Every Wednesday 08:30 to 11:45. École Polytechnique - CREST

Political Economy Pierre Boyer École Polytechnique - CREST Master in Economics Fall 2018 Schedule: Every Wednesday 08:30 to 11:45 Boyer (École Polytechnique) Political Economy Fall 2018 1 / 56 Outline

Political Economy Pierre Boyer École Polytechnique - CREST Master in Economics Fall 2018 Schedule: Every Wednesday 08:30 to 11:45 Boyer (École Polytechnique) Political Economy Fall 2018 1 / 56 Outline

Closed book/notes exam. No computer, calculator, or any electronic device allowed.

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income Hilary Hoynes, UC Berkeley Ankur Patel US Treasury April 2015 Overview The U.S. social safety net for

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income Hilary Hoynes, UC Berkeley Ankur Patel US Treasury April 2015 Overview The U.S. social safety net for

Chapter 7. Government Subsidies and Income Support for the Poor

Chapter 7 Government Subsidies and Income Support for the Poor Copyright 2002 Thomson Learning, Inc. Thomson Learning is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors of classes

Chapter 7 Government Subsidies and Income Support for the Poor Copyright 2002 Thomson Learning, Inc. Thomson Learning is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors of classes

Understanding Income Distribution and Poverty

Understanding Distribution and Poverty : Understanding the Lingo market income: quantifies total before-tax income paid to factor markets from the market (i.e. wages, interest, rent, and profit) total

Understanding Distribution and Poverty : Understanding the Lingo market income: quantifies total before-tax income paid to factor markets from the market (i.e. wages, interest, rent, and profit) total

INTRODUCTION TAXES: EQUITY VS. EFFICIENCY WEALTH PERSONAL INCOME THE LORENZ CURVE THE SIZE DISTRIBUTION OF INCOME

INTRODUCTION Taxes affect production as well as distribution. This creates a potential tradeoff between the goal of equity and the goal of efficiency. The chapter focuses on the following questions: How

INTRODUCTION Taxes affect production as well as distribution. This creates a potential tradeoff between the goal of equity and the goal of efficiency. The chapter focuses on the following questions: How

How Progressive is the U.S. (Federal) Tax System?

Tax System?") How Progressive is the U.S. (Federal) Tax System? Data is for 1999 or 2002 depending on the series First, some Definitions Regressive Tax System: Proportional Tax System: Progressive Tax System: A 1 st

How Progressive is the U.S. (Federal) Tax System? Data is for 1999 or 2002 depending on the series First, some Definitions Regressive Tax System: Proportional Tax System: Progressive Tax System: A 1 st

Topic 1: Policy Design: Unemployment Insurance and Moral Hazard

Introduction Trade-off Optimal UI Empirical Topic 1: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 39 Introduction Trade-off

Introduction Trade-off Optimal UI Empirical Topic 1: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 39 Introduction Trade-off

Social Security. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Social Security 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 13 Social Security: A federal program that taxes workers to provide income support to the elderly. 13.1 What

Social Security 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 13 Social Security: A federal program that taxes workers to provide income support to the elderly. 13.1 What

131: Public Economics Taxes on Capital and Savings

131: Public Economics Taxes on Capital and Savings Emmanuel Saez Berkeley 1 MOTIVATION 1) Capital income is about 25% of national income (labor income is 75%) but distribution of capital income is much

131: Public Economics Taxes on Capital and Savings Emmanuel Saez Berkeley 1 MOTIVATION 1) Capital income is about 25% of national income (labor income is 75%) but distribution of capital income is much

The theory of taxation/3 (ch. 19 Stiglitz, ch. 20 Gruber, ch.15 Rosen) Desirable characteristics of tax systems (optimal taxation)

Desirable characteristics of tax systems (optimal taxation)") The theory of taxation/3 (ch. 19 Stiglitz, ch. 20 Gruber, ch.15 Rosen) Desirable characteristics of tax systems (optimal taxation) 1 Optimal Taxation: Desirable characteristics of tax systems Optimal taxation

The theory of taxation/3 (ch. 19 Stiglitz, ch. 20 Gruber, ch.15 Rosen) Desirable characteristics of tax systems (optimal taxation) 1 Optimal Taxation: Desirable characteristics of tax systems Optimal taxation

Labour Supply, Taxes and Benefits

Labour Supply, Taxes and Benefits William Elming Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic

Labour Supply, Taxes and Benefits William Elming Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic

Chapter II: Labour Market Policy

Chapter II: Labour Market Policy Section 2: Unemployment insurance Literature: Peter Fredriksson and Bertil Holmlund (2001), Optimal unemployment insurance in search equilibrium, Journal of Labor Economics

Chapter II: Labour Market Policy Section 2: Unemployment insurance Literature: Peter Fredriksson and Bertil Holmlund (2001), Optimal unemployment insurance in search equilibrium, Journal of Labor Economics

NBER WORKING PAPER SERIES DIRECT OR INDIRECT TAX INSTRUMENTS FOR REDISTRIBUTION: SHORT-RUN VERSUS LONG-RUN. Emmanuel Saez

NBER WORKING PAPER SERIES DIRECT OR INDIRECT TAX INSTRUMENTS FOR REDISTRIBUTION: SHORT-RUN VERSUS LONG-RUN Emmanuel Saez Working Paper 8833 http://www.nber.org/papers/w8833 NATIONAL BUREAU OF ECONOMIC

NBER WORKING PAPER SERIES DIRECT OR INDIRECT TAX INSTRUMENTS FOR REDISTRIBUTION: SHORT-RUN VERSUS LONG-RUN Emmanuel Saez Working Paper 8833 http://www.nber.org/papers/w8833 NATIONAL BUREAU OF ECONOMIC

ECON 340/ Zenginobuz Fall 2011 STUDY QUESTIONS FOR THE FINAL. x y z w u A u B

ECON 340/ Zenginobuz Fall 2011 STUDY QUESTIONS FOR THE FINAL 1. There are two agents, A and B. Consider the set X of feasible allocations which contains w, x, y, z. The utility that the two agents receive

ECON 340/ Zenginobuz Fall 2011 STUDY QUESTIONS FOR THE FINAL 1. There are two agents, A and B. Consider the set X of feasible allocations which contains w, x, y, z. The utility that the two agents receive

Inflation. David Andolfatto

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

ECON 1100 Global Economics (Fall 2013) The Distribution Function of Government portions for Exam 4

The Distribution Function of Government portions for Exam 4") ECON 1100 Global Economics (Fall 2013) The Distribution Function of Government portions for Exam 4 Relevant Readings from the Required Textbooks: Economics Chapter 12, Income Distribution and Poverty Problems

ECON 1100 Global Economics (Fall 2013) The Distribution Function of Government portions for Exam 4 Relevant Readings from the Required Textbooks: Economics Chapter 12, Income Distribution and Poverty Problems

Closed book/notes exam. No computer, calculator, or any electronic device allowed.

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

The Review of Economic Studies, Vol. 68, No. 1. (Jan., 2001), pp

, pp") Using Elasticities to Derive Optimal Income Tax Rates Emmanuel Saez The Review of Economic Studies, Vol. 68, No. 1. (Jan., 2001), pp. 205-229. Stable URL: http://links.jstor.org/sici?sici=0034-6527%28200101%2968%3a1%3c205%3auetdoi%3e2.0.co%3b2-e

Using Elasticities to Derive Optimal Income Tax Rates Emmanuel Saez The Review of Economic Studies, Vol. 68, No. 1. (Jan., 2001), pp. 205-229. Stable URL: http://links.jstor.org/sici?sici=0034-6527%28200101%2968%3a1%3c205%3auetdoi%3e2.0.co%3b2-e

Unemployment, Consumption Smoothing and the Value of UI

Unemployment, Consumption Smoothing and the Value of UI Camille Landais (LSE) and Johannes Spinnewijn (LSE) December 15, 2016 Landais & Spinnewijn (LSE) Value of UI December 15, 2016 1 / 33 Motivation

Unemployment, Consumption Smoothing and the Value of UI Camille Landais (LSE) and Johannes Spinnewijn (LSE) December 15, 2016 Landais & Spinnewijn (LSE) Value of UI December 15, 2016 1 / 33 Motivation

Public Economics Lectures Part 1: Introduction

Public Economics Lectures Part 1: Introduction John Karl Scholz (borrowing from Raj Chetty and Gregory A. Bruich) University of Wisconsin - Madison Fall 2011 Public Economics Lectures () Part 1: Introduction

Public Economics Lectures Part 1: Introduction John Karl Scholz (borrowing from Raj Chetty and Gregory A. Bruich) University of Wisconsin - Madison Fall 2011 Public Economics Lectures () Part 1: Introduction

Graduate Public Finance

Graduate Public Finance Taxing Top Earners Owen Zidar Princeton Fall 2017 Lecture 5 Thanks to Emmanuel Saez and David Card for sharing his slides/notes, many of which are reproduced here. Stephanie Kestelman

Graduate Public Finance Taxing Top Earners Owen Zidar Princeton Fall 2017 Lecture 5 Thanks to Emmanuel Saez and David Card for sharing his slides/notes, many of which are reproduced here. Stephanie Kestelman

9. Real business cycles in a two period economy

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

Hilary Hoynes UC Davis EC230. Taxes and the High Income Population

Hilary Hoynes UC Davis EC230 Taxes and the High Income Population New Tax Responsiveness Literature Started by Feldstein [JPE The Effect of MTR on Taxable Income: A Panel Study of 1986 TRA ]. Hugely important

Hilary Hoynes UC Davis EC230 Taxes and the High Income Population New Tax Responsiveness Literature Started by Feldstein [JPE The Effect of MTR on Taxable Income: A Panel Study of 1986 TRA ]. Hugely important

The Role of Physical Capital

San Francisco State University ECO 560 The Role of Physical Capital Michael Bar As we mentioned in the introduction, the most important macroeconomic observation in the world is the huge di erences in

San Francisco State University ECO 560 The Role of Physical Capital Michael Bar As we mentioned in the introduction, the most important macroeconomic observation in the world is the huge di erences in

Lecture 3: Income & Wage Taxation Over Time & Across Countries (check on line for updated versions)

") Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2015-2016 Lecture 3: Income & Wage Taxation Over Time & Across Countries (check on line

Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2015-2016 Lecture 3: Income & Wage Taxation Over Time & Across Countries (check on line

Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities

Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities Thomas Piketty (PSE) Emmanuel Saez (Berkeley and NBER) Stefanie Stantcheva (MIT) November 2012 Piketty, Saez & Stantcheva () Three Elasticities

Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities Thomas Piketty (PSE) Emmanuel Saez (Berkeley and NBER) Stefanie Stantcheva (MIT) November 2012 Piketty, Saez & Stantcheva () Three Elasticities

ECON 3020 Intermediate Macroeconomics

ECON 3020 Intermediate Macroeconomics Chapter 5 A Closed-Economy One-Period Macroeconomic Model Instructor: Xiaohui Huang Department of Economics University of Virginia c Copyright 2014 Xiaohui Huang.

ECON 3020 Intermediate Macroeconomics Chapter 5 A Closed-Economy One-Period Macroeconomic Model Instructor: Xiaohui Huang Department of Economics University of Virginia c Copyright 2014 Xiaohui Huang.

Public Finance: The Economics of Taxation. The Economics of Taxation. Taxes: Basic Concepts

C H A P T E R 16 Public Finance: The Economics of Taxation Prepared by: Fernando Quijano and Yvonn Quijano The Economics of Taxation The primary vehicle that the government uses to finance itself is taxation.

C H A P T E R 16 Public Finance: The Economics of Taxation Prepared by: Fernando Quijano and Yvonn Quijano The Economics of Taxation The primary vehicle that the government uses to finance itself is taxation.

14.41 Problem Set #4 Solutions

14.41 Problem Set #4 Solutions 1) a) There are several possible reasons including but not limited to: Competition between MCO plans should reduce costs. Some politicians will hope that MCOs may make Medicaid

14.41 Problem Set #4 Solutions 1) a) There are several possible reasons including but not limited to: Competition between MCO plans should reduce costs. Some politicians will hope that MCOs may make Medicaid

The analysis of government intervention (Stiglitz ch.10; Gruber ch.2)

") The analysis of government intervention (Stiglitz ch.10; Gruber ch.2) How does the government intervene: some comparative data Effects of government interventions the importance of design features evaluating

The analysis of government intervention (Stiglitz ch.10; Gruber ch.2) How does the government intervene: some comparative data Effects of government interventions the importance of design features evaluating

Graduate Public Finance

Graduate Public Finance Measuring Income and Wealth Inequality Owen Zidar Princeton Fall 2018 Lecture 12 Thanks to Thomas Piketty, Emmanuel Saez, Gabriel Zucman, and Eric Zwick for sharing notes/slides,

Graduate Public Finance Measuring Income and Wealth Inequality Owen Zidar Princeton Fall 2018 Lecture 12 Thanks to Thomas Piketty, Emmanuel Saez, Gabriel Zucman, and Eric Zwick for sharing notes/slides,

THEORETICAL TOOLS OF PUBLIC FINANCE

Solutions and Activities for CHAPTER 2 THEORETICAL TOOLS OF PUBLIC FINANCE Questions and Problems 1. The price of a bus trip is $1 and the price of a gallon of gas (at the time of this writing!) is $3.

Solutions and Activities for CHAPTER 2 THEORETICAL TOOLS OF PUBLIC FINANCE Questions and Problems 1. The price of a bus trip is $1 and the price of a gallon of gas (at the time of this writing!) is $3.

Welfare Economics. Jan Abrell Centre for Energy Policy and Economics (CEPE) D-MTEC, ETH Zurich. Welfare Economics

D-MTEC, ETH Zurich. Welfare Economics") Welfare Economics Jan Abrell Centre for Energy Policy and Economics (CEPE) D-MTEC, ETH Zurich Welfare Economics 06.03.2018 1 Outline So far Basic Model Economic Efficiency Optimality Market Economy Partial

Welfare Economics Jan Abrell Centre for Energy Policy and Economics (CEPE) D-MTEC, ETH Zurich Welfare Economics 06.03.2018 1 Outline So far Basic Model Economic Efficiency Optimality Market Economy Partial

Notes on the Behavioral Implications of Tax Distortions

Economics 260: Notes on the Behavioral Implications of Tax Distortions Fall 2015 Casey B. Mulligan Notes on the Behavioral Implications of Tax Distortions Here we set up a simple model illustrating some

Economics 260: Notes on the Behavioral Implications of Tax Distortions Fall 2015 Casey B. Mulligan Notes on the Behavioral Implications of Tax Distortions Here we set up a simple model illustrating some

ECONOMICS PUBLIC SECTOR. of the JOSEPH E. STIGUTZ. Second Edition. W.W.NORTON & COMPANY-New York-London. Princeton University

ECONOMICS of the PUBLIC SECTOR a Second Edition JOSEPH E. STIGUTZ Princeton University W.W.NORTON & COMPANY-New York-London Contents Preface Part One xxi Introduction 1 The Public Sector in a Mixed Economy

ECONOMICS of the PUBLIC SECTOR a Second Edition JOSEPH E. STIGUTZ Princeton University W.W.NORTON & COMPANY-New York-London Contents Preface Part One xxi Introduction 1 The Public Sector in a Mixed Economy

2017 Year-End Tax Planning

& C O M PA N Y, L L C, C PA s 2017 Year-End Tax Planning 1101 Wootton Parkway, Suite 400 Rockville, MD 20852 Phone: (301) 260-0809 Fax: (202) 204-6322 950 North Washington, St Suite 238 Alexandria, VA

& C O M PA N Y, L L C, C PA s 2017 Year-End Tax Planning 1101 Wootton Parkway, Suite 400 Rockville, MD 20852 Phone: (301) 260-0809 Fax: (202) 204-6322 950 North Washington, St Suite 238 Alexandria, VA