Lecture 3: Income & Wage Taxation Over Time & Across Countries (check on line for updated versions)

|

|

|

- Joel Kelley

- 6 years ago

- Views:

Transcription

1 Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year Lecture 3: Income & Wage Taxation Over Time & Across Countries (check on line for updated versions)

2 Roadmap of lecture 3 The rise of the modern progressive income tax Effective tax rates vs marginal tax rates Taxing individuals or couples? Illustration with French and US income tax rates The top marginal tax rate in history From an elite tax to a mass tax Income tax in China and India

3 The modern progressive income tax vs previous forms of income taxation The modern progressive income tax was created in 1909 in the UK, 1913 in the US, 1914 in France, 1922 in India, 1932 in Argentina, etc., and is based upon the principle of a comprehensive tax base Comprehensive income tax: t = t(y) with y = total income from all income categories (wages + pensions + self-employment income + rent + dividend + interest + etc.) schedular income tax: different tax rates for different income categories (UK system in 19 c )

4 One also finds older forms of income taxation (sometime with fixed tax payments by income brackets) in many countries prior to 19c. See e.g. 18 c France: Touzery, L invention de l impôt sur le revenu La taille tarifée , French Revolution: income tax viewed as very intrusive, replaced during French revolution by taxes on property that were viewed as less intrusive. Creation of new tax system based upon «les quatre vieilles contributions»: Contribution foncière (tax on housing, buildings and land) Contribution des patentes (based upon business assets) Contribution sur les portes et fenêtres (number of doors and windows) Contribution personelle-mobilière (based upon rental values) (+ droits de mutation (inheritance tax)

5 During 19c: with industrialization, many new forms of wealth creation are untaxed >> creation of modern income tax: tax reforms in UK 1840s-1850s, France IRVM 1872, and finally everywhere in See e.g. Mehrotra, Making the Modern American Fiscal State. Law, Politics, and the Rise of Progressive Taxation, , CUP 2013; J. Witte, The Politics and Development of the Federal Income Tax, University of Wisconsin Press, 1985 Every society always needs to find its own mix between different forms of taxes on capital, income and consumption

6 The rise of income & wage taxation If we consider all forms of income and wage taxation in general (putting together income taxes with social contributions), then we typically have 60-65% of total tax revenues for income and wage taxation in today s developed countries (vs % for VAT and other consumption taxes, and 5-10% for wealth & property taxes) The rise of the modern fiscal state (from <10% Y in tax revenues until WW1 to 40% today) comes almost entirely from the rise of income and wage taxation See EU 28: income taxes + social contributions = 24.6% GDP out of 39.4% GDP for total taxes (2012) France: 27.8% GDP out of 45.0% for total taxes (progressive income tax strictly speaking <4% GDP)

7

8

9

10 Effective vs. Marginal tax rates Effective or average tax rate = t(y)/y t(y) progressive if and only if t(y)/y rises with y Marginal tax rate = t (y) t(y) convex = t (y)>0, i.e. t (y) rises with y Convexity implies progressivity (but not necessary: as we will see, U-shaped pattern of marginal tax rates when transfers are taken into account) Most progressive income taxes use a bracket system: fixed marginal tax rates within income brackets But one can also use continuous system Exemple of computations using tax schedules from France and the US: see excel file

11 Taxing individuals or couples? In many European countries (Scandinavia, UK, Italy, Spain,.), income tax t(y) is based upon individual income y: whether one lives in a couple or not is irrelevant In France, Germany & US (for bottom half of pop), income tax is computed at the level of married couples using «split» system («quotient conjugual»): income tax = 2 x t[ (y 1 +y 2 )/2 ], with y 1,y 2 = spouses incomes With t(y) convex, this favours unequal couples; if y 1 =y 2, there is no tax advantage at all Key question: unitary household or not? The split system can reinforce gender inequality; the individual system favours female labor supply

12 Marginal vs average tax rates: illustration with French 2013 Income Tax French 2013 income tax schedule Income brackets Marginal tax rate (applied to 2012 incomes) ( ) (%) (barème de l'impôt sur le revenu (IR)) ,0% (see ,5% French "quotient familial" (QF) sytem: ,0% ,0% ,0% ,0% y = taxable income = annual income - standard deduction for profesional expenses (10%) n = number of units of QF (nombre de parts de QF): n=1 if single, n=2 if couple, n=2.5 if couple with 1 kid, etc. y/n = taxable income per QF unift (revenu imposable par part de QF) Income tax = n x t(y/n) (because t(y) is convex, it is better to have a high n)

13 Exemple with an annual income y = and n=2,5 (couple with one kid) (about P99): % x = (standard deduction for profesional expenses of wage earners: 10%) / 2,5 = = taxable income per QF unit >>> marginal income tax rate = 30% Income tax per QF unit = 5.5% x ( ) + 14% x ( ) + 30% x ( ) = Total income tax = 2,5 x = >>> average income tax rate = / = 10,1% >>> average effective tax rate taking into account tax credits etc. = 0,85 x 10,1% = 8,6% >>>>> 8,6% << 30,0%, i.e. average rate << marginal rate

14 U.S. Federal income tax rates applied to 2013 incomes Note: This does not include the personal tax exemption ($3,900 for singles & $7,800 for couples), the standard deduction ($6,100 for singles & $12,200 for couples), and the earned income tax credit (EITC) (tax rebate for low incomes) I.e. singles start paying federal income taxes above 10,000$ and couples above 20,000$ See Internal revenue service (IRS) web site for complete tax rates and schedules Marginal tax rate Single Married Filing Jointly or Qualified Widow(er) Married Filing Separately 10% 15% 25% 28% 33% 35% 39,6% $0 $8,925 $0 $17,850 $0 $8,925 $8,925 $36,250 $17,850 $72,500 $8,925 $36,250 $36,250 $87,850 $72,500 $146,400 $36,250 $73,200 $87,850 $183,250 $146,400 $223,050 $73,200 $111,525 $183,250 $398,350 $223,050 $398,350 $111,525 $199,175 $398,350 $400,000 $398,350 $450,000 $199,175 $225,000 $400,000+ $450,000+ $225,000+

15 (10/10/2012) U.S. Federal income tax rates applied to 2012 incomes Note: This does not include the personal tax exemption ($3,800 for singles & $7,600 for couples), the standard deduction ($5,950 for singles & $11,900 for couples), and the earned income tax credit (EITC) (tax rebate for low incomes) I.e. singles start paying federal income taxes above 9,750$ and couples above 19,500$ See Internal revenue service (IRS) web site for complete tax rates and schedules Marginal tax rate Single Married Filing Jointly or Qualified Widow(er) Married Filing Separately 10% 15% 25% 28% 33% 35% $0 $8,700 $0 $17,400 $0 $8,700 $8,701 $35,350 $17,401 $70,700 $8,701 $35,350 $35,351 $85,650 $70,701 $142,700 $35,351 $71,350 $85,651 $178,650 $142,701 $217,450 $71,351 $108,725 $178,651 $388,350 $217,451 $388,350 $108,726 $194,175 $388,351+ $388,351+ $194,176+

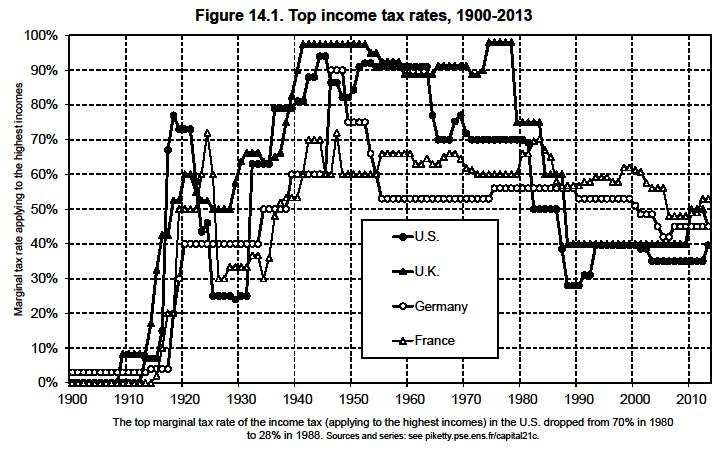

16 The top marginal tax rate in history Top marginal tax rate = marginal tax rate applying to the highest incomes Chaotic history during past century US and UK invented confiscatory tax rates for very high incomes; then big reversal since 1980s Same pattern for top inheritance tax rates: US-UK invented confiscatory top rates, then big reversal since 1980s (see Lectures 6-7) Until 1970s, top tax rates on «unearned income» (capital income) often higher than top tax rate on «earned income» (labor income) Reversal since 1980s: free capital flows with no exchange of information, special tax regimes for capital income >>> regressivity at the top (see France 2010)

17

18

19 100% Figure 3: Top Income Tax Rates: Earned (Labor) vs Unearned (Capital) 90% 80% 70% 60% 50% 40% 30% 20% 10% U.S. (earned income) U.S. (unearned income) U.K. (earned income) U.K. (unearned income) 0%

20 From an elite tax to a mass tax In every country, the income tax at the time it is created is targeted on the top 1-2% of the population; then it is gradually extended to the entire population (or at least to 50-60% of the population). This makes tax revenues much more significant: the mass income tax is an important part of the rise of the modern fiscal state See e.g. graph on fraction of pop subject to tax in France. See my 2001 book (chapters 4-5) for a complete politico-economic history of the French income tax Explanations for this transition from elite to mass tax? Is it happening everywhere in developing countries?

21

22 Explanations: Economics/Technology (rise of large corporations and wage-earner status >> easier to tax) or Politics (social acceptability of tax, fiscal consent)? Probably both: politics and culture are about choosing different ways to regulate, organize and provide meaning and sense to economic and technological change. On the political economy of fiscal development: Besley-Persson, On the Origins of State Capacity, 2009 ; Why do developing countries tax so little?, JEP 2014 Kleven-Kreiner-Saez, Why Can Modern Governments Tax so much?, 2009; How Can Scandinavians Tax So Much?, JEP 2014

23 Income tax in India and China An interesting contrast: income tax in India and China Income tax started much earlier in India (1922), but remained a small elite tax until the present day In constrast, it very quickly became a mass tax in China; why? This illustrates the different mechanisms: politics (limited democracy in China/limited political pressures by the rich to index the brackets; but income tax not very transparent), legal-fiscal-social modernization (limited fraction of formal wage labor in India, more difficult to generalize income taxation) See T. Piketty & N. Qian, «Income inequality and progressive income taxation in China and India: », AEJ 2009 [article in pdf format]

24

25

26

27

Lecture 4: Income Taxes Over Time & Across Countries

Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2014-2015 Lecture 4: Income Taxes Over Time & Across Countries (January 27 th 2015)

Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2014-2015 Lecture 4: Income Taxes Over Time & Across Countries (January 27 th 2015)

Should the Rich Pay for Fiscal Adjustment? Income and Capital Tax Options

Should the Rich Pay for Fiscal Adjustment? Income and Capital Tax Options Thomas Piketty Paris School of Economics Brussels, ECFIN Workshop, October 18 2012 This talk: two points 1. The rise of European

Should the Rich Pay for Fiscal Adjustment? Income and Capital Tax Options Thomas Piketty Paris School of Economics Brussels, ECFIN Workshop, October 18 2012 This talk: two points 1. The rise of European

Labor Supply and Taxation in Europe

Labor Supply and Taxation in Europe Fabrizio Colonna - Banca d Italia Stefania Marcassa - Paris School of Economics November 16, 2010 Motivation Observe differences in Female Labor Force Participation

Labor Supply and Taxation in Europe Fabrizio Colonna - Banca d Italia Stefania Marcassa - Paris School of Economics November 16, 2010 Motivation Observe differences in Female Labor Force Participation

Rethinking Wealth Taxation

Rethinking Wealth Taxation Thomas Piketty (Paris School of Economics Gabriel Zucman (London School of Economics) November 2014 This talk: two points Wealth is becoming increasingly important relative to

Rethinking Wealth Taxation Thomas Piketty (Paris School of Economics Gabriel Zucman (London School of Economics) November 2014 This talk: two points Wealth is becoming increasingly important relative to

Capital in the 21 st century

Capital in the 21 st century Thomas Piketty Paris School of Economics Lisbon, April 27 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book

Capital in the 21 st century Thomas Piketty Paris School of Economics Lisbon, April 27 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book

Capital in the 21 st century

Capital in the 21 st century Thomas Piketty Paris School of Economics Santiago de Chile, January 13 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014)

Capital in the 21 st century Thomas Piketty Paris School of Economics Santiago de Chile, January 13 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014)

Inequality and growth Thomas Piketty Paris School of Economics

Inequality and growth Thomas Piketty Paris School of Economics Bercy, January 23 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Inequality and growth Thomas Piketty Paris School of Economics Bercy, January 23 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Income Inequality in France, : Evidence from Distributional National Accounts (DINA)

") Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest, and

Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest, and

Inequality and Social Mobility. Econ 101

Inequality and Social Mobility Econ 101 Much of the following is taken from Capital in the Twenty-First Century by Thomas Piketty Special Thanks Key Concepts Wealth (stock, savings) Inequality The richest

Inequality and Social Mobility Econ 101 Much of the following is taken from Capital in the Twenty-First Century by Thomas Piketty Special Thanks Key Concepts Wealth (stock, savings) Inequality The richest

Capital in the 21 st century. Thomas Piketty Paris School of Economics Cologne, December 5 th 2013

Capital in the 21 st century Thomas Piketty Paris School of Economics Cologne, December 5 th 2013 This lecture is based upon Capital in the 21 st century (Harvard Univ. Press, March 2014) This book studies

Capital in the 21 st century Thomas Piketty Paris School of Economics Cologne, December 5 th 2013 This lecture is based upon Capital in the 21 st century (Harvard Univ. Press, March 2014) This book studies

Inequality Dynamics in France, : Evidence from Distributional National Accounts (DINA)

") Inequality Dynamics in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest,

Inequality Dynamics in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest,

Discussion: Accounting for Wealth Inequality Dynamics: Methods, Estimates and Simulations for France ( )

") Discussion: Accounting for Wealth Inequality Dynamics: Methods, Estimates and Simulations for France (1800-2014) Philip Vermeulen European Central Bank DG-Research Fifth Conference on Household Finance

Discussion: Accounting for Wealth Inequality Dynamics: Methods, Estimates and Simulations for France (1800-2014) Philip Vermeulen European Central Bank DG-Research Fifth Conference on Household Finance

Capital in the 21 st century. Thomas Piketty Paris School of Economics Visby, June

Capital in the 21 st century Thomas Piketty Paris School of Economics Visby, June 30 2014 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Capital in the 21 st century Thomas Piketty Paris School of Economics Visby, June 30 2014 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

STATISTICS. Taxing Wages DIS P O NIB LE E N SPECIAL FEATURE: PART-TIME WORK AND TAXING WAGES

AVAILABLE ON LINE DIS P O NIB LE LIG NE www.sourceoecd.org E N STATISTICS Taxing Wages «SPECIAL FEATURE: PART-TIME WORK AND TAXING WAGES 2004-2005 2005 Taxing Wages SPECIAL FEATURE: PART-TIME WORK AND

AVAILABLE ON LINE DIS P O NIB LE LIG NE www.sourceoecd.org E N STATISTICS Taxing Wages «SPECIAL FEATURE: PART-TIME WORK AND TAXING WAGES 2004-2005 2005 Taxing Wages SPECIAL FEATURE: PART-TIME WORK AND

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates)

") Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates) Emmanuel Saez March 2, 2012 What s new for recent years? Great Recession 2007-2009 During the

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates) Emmanuel Saez March 2, 2012 What s new for recent years? Great Recession 2007-2009 During the

French taxation. For those who are resident in France there are five tax rates and bands on net taxable income, as follows:

French taxation Income Tax Rates/Bands 2018 For those who are resident in France there are five tax rates and bands on net taxable income, as follows: Income Share Tax Rate Up to 9,807 0% Between 9,807-27,086

French taxation Income Tax Rates/Bands 2018 For those who are resident in France there are five tax rates and bands on net taxable income, as follows: Income Share Tax Rate Up to 9,807 0% Between 9,807-27,086

Income Inequality and Progressive Income Taxation in China and India, Thomas Piketty and Nancy Qian

Income Inequality and Progressive Income Taxation in China and India, 1986-2015 Thomas Piketty and Nancy Qian Abstract: This paper evaluates income tax reforms in China and India. The combination of fast

Income Inequality and Progressive Income Taxation in China and India, 1986-2015 Thomas Piketty and Nancy Qian Abstract: This paper evaluates income tax reforms in China and India. The combination of fast

LECTURE 14: THE INEQUALITY OF CAPITAL OWNERSHIP IN EUROPE AND THE USA

LECTURE 14: THE INEQUALITY OF CAPITAL OWNERSHIP IN EUROPE AND THE USA Dr. Aidan Regan Email: aidan.regan@ucd.ie Website: www.aidanregan.com Teaching blog: www.capitalistdemocracy.wordpress.com Twitter:

LECTURE 14: THE INEQUALITY OF CAPITAL OWNERSHIP IN EUROPE AND THE USA Dr. Aidan Regan Email: aidan.regan@ucd.ie Website: www.aidanregan.com Teaching blog: www.capitalistdemocracy.wordpress.com Twitter:

Taxable Income Elasticities. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Taxable Income Elasticities 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of

Taxable Income Elasticities 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of

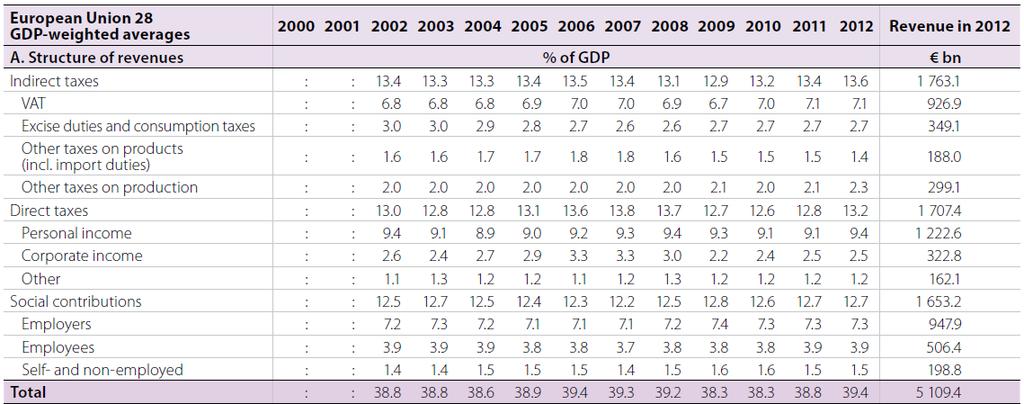

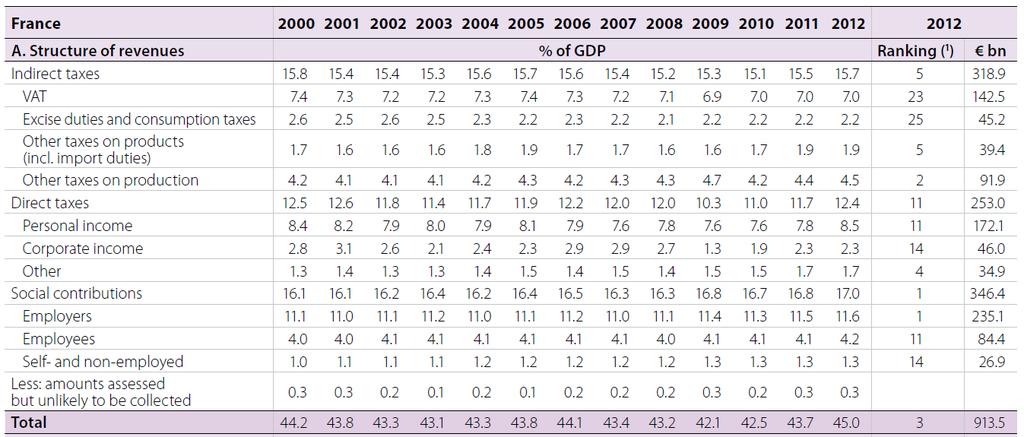

2 National tax systems: Structure and recent developments

France Structure and development of tax revenues Table FR.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Ranking Revenue (billion euros) A. Structure by type of tax

France Structure and development of tax revenues Table FR.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Ranking Revenue (billion euros) A. Structure by type of tax

Distributional National Accounts DINA

Distributional National Accounts DINA Facundo Alvaredo Anthony B. Atkinson Thomas Piketty Emmanuel Saez Gabriel Zucman Meeting of Providers of OECD IDD Data OECD, Paris, February 18-19, 2016 Envision a

Distributional National Accounts DINA Facundo Alvaredo Anthony B. Atkinson Thomas Piketty Emmanuel Saez Gabriel Zucman Meeting of Providers of OECD IDD Data OECD, Paris, February 18-19, 2016 Envision a

Graduate Public Finance

Graduate Public Finance Measuring Income and Wealth Inequality Owen Zidar Princeton Fall 2018 Lecture 12 Thanks to Thomas Piketty, Emmanuel Saez, Gabriel Zucman, and Eric Zwick for sharing notes/slides,

Graduate Public Finance Measuring Income and Wealth Inequality Owen Zidar Princeton Fall 2018 Lecture 12 Thanks to Thomas Piketty, Emmanuel Saez, Gabriel Zucman, and Eric Zwick for sharing notes/slides,

NBER WORKING PAPER SERIES GLOBAL INEQUALITY DYNAMICS: NEW FINDINGS FROM WID.WORLD

NBER WORKING PAPER SERIES GLOBAL INEQUALITY DYNAMICS: NEW FINDINGS FROM WID.WORLD Facundo Alvaredo Lucas Chancel Thomas Piketty Emmanuel Saez Gabriel Zucman Working Paper 23119 http://www.nber.org/papers/w23119

NBER WORKING PAPER SERIES GLOBAL INEQUALITY DYNAMICS: NEW FINDINGS FROM WID.WORLD Facundo Alvaredo Lucas Chancel Thomas Piketty Emmanuel Saez Gabriel Zucman Working Paper 23119 http://www.nber.org/papers/w23119

Capital is Back: Wealth-Income Ratios in Rich Countries Thomas Piketty & Gabriel Zucman Paris School of Economics October 2012

Capital is Back: Wealth-Income Ratios in Rich Countries 1870-2010 Thomas Piketty & Gabriel Zucman Paris School of Economics October 2012 How do aggregate wealth-income ratios evolve in the long run, and

Capital is Back: Wealth-Income Ratios in Rich Countries 1870-2010 Thomas Piketty & Gabriel Zucman Paris School of Economics October 2012 How do aggregate wealth-income ratios evolve in the long run, and

SOME MAJOR CHANGES DID AFFECT THE ALL TAXATION SYSTEM IN FRANCE SINCE GENERAL PRESIDENTIAL ELECTION AND NEW CHAMBERS

April 2019 SOME MAJOR CHANGES DID AFFECT THE ALL TAXATION SYSTEM IN FRANCE SINCE GENERAL PRESIDENTIAL ELECTION AND NEW CHAMBERS Among several changes made: The repeal of wealth tax on every asset which

April 2019 SOME MAJOR CHANGES DID AFFECT THE ALL TAXATION SYSTEM IN FRANCE SINCE GENERAL PRESIDENTIAL ELECTION AND NEW CHAMBERS Among several changes made: The repeal of wealth tax on every asset which

LECTURE 11: INCOME INEQUALITY IN EUROPE AND THE USA

LECTURE 11: INCOME INEQUALITY IN EUROPE AND THE USA Dr. Aidan Regan Email: aidan.regan@ucd.ie Website: www.aidanregan.com Teaching blog: www.capitalistdemocracy.wordpress.com Twitter: @aidan_regan #CapitalUCD

LECTURE 11: INCOME INEQUALITY IN EUROPE AND THE USA Dr. Aidan Regan Email: aidan.regan@ucd.ie Website: www.aidanregan.com Teaching blog: www.capitalistdemocracy.wordpress.com Twitter: @aidan_regan #CapitalUCD

ECON 361: Income Distributions and Problems of Inequality

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 7, 2018 1/1 Last class... Top income share in Canada- Veall (2012) Income inequality in the U.S. - Piketty

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 7, 2018 1/1 Last class... Top income share in Canada- Veall (2012) Income inequality in the U.S. - Piketty

Lecture 6: Taxable Income Elasticities

1 40 Lecture 6: Taxable Income Elasticities Stefanie Stantcheva Fall 2017 40 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation

1 40 Lecture 6: Taxable Income Elasticities Stefanie Stantcheva Fall 2017 40 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation

Optimal Labor Income Taxation. Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011

Optimal Labor Income Taxation Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011 MODERN ECONOMIES DO SIGNIFICANT REDISTRIBUTION 1) Taxes:

Optimal Labor Income Taxation Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011 MODERN ECONOMIES DO SIGNIFICANT REDISTRIBUTION 1) Taxes:

Wealth, inequality & assets: where is Europe heading?

Wealth, inequality & assets: where is Europe heading? Thomas Piketty Paris School of Economics DG ECFIN Annual Research Conference Brussels, November 23 rd 2010 Can we study macro issues without looking

Wealth, inequality & assets: where is Europe heading? Thomas Piketty Paris School of Economics DG ECFIN Annual Research Conference Brussels, November 23 rd 2010 Can we study macro issues without looking

From Communism to Capitalism: Private vs. Public Property and Rising. Inequality in China and Russia

From Communism to Capitalism: Private vs. Public Property and Rising Inequality in China and Russia Filip Novokmet (Paris School of Economics) Thomas Piketty (Paris School of Economics) Li Yang (Paris

From Communism to Capitalism: Private vs. Public Property and Rising Inequality in China and Russia Filip Novokmet (Paris School of Economics) Thomas Piketty (Paris School of Economics) Li Yang (Paris

Sarah K. Burns James P. Ziliak. November 2013

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Econ 133 Global Inequality and Growth. Inequality between labor and capital. Gabriel Zucman

Econ 133 Global Inequality and Growth Inequality between labor and capital zucman@berkeley.edu 1 What we ve learned so far: All income derives from labor or capital The share of income that goes to capital

Econ 133 Global Inequality and Growth Inequality between labor and capital zucman@berkeley.edu 1 What we ve learned so far: All income derives from labor or capital The share of income that goes to capital

ECON 361: Income Distributions and Problems of Inequality

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 9, 2017 1/35 Last class... Top income share in Canada- Veall (2012( Income inequality in the U.S. - Piketty

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 9, 2017 1/35 Last class... Top income share in Canada- Veall (2012( Income inequality in the U.S. - Piketty

Understanding the Effects of the 2001, 2003, and 2004 Income Tax Cuts

Understanding the Effects of the 2001, 2003, and 2004 Income Tax Cuts The major tax laws of the past 4-5 years have probably had a significant impact on your paycheck and your overall tax bill. Among other

Understanding the Effects of the 2001, 2003, and 2004 Income Tax Cuts The major tax laws of the past 4-5 years have probably had a significant impact on your paycheck and your overall tax bill. Among other

Maurizio Franzini and Mario Planta

Maurizio Franzini and Mario Planta 2 premises: 1. Inequality is a burning issue for economic, ethical and political reasons (Sen, Stiglitz, Piketty and many others ) 2. Inequality is today a more complex

Maurizio Franzini and Mario Planta 2 premises: 1. Inequality is a burning issue for economic, ethical and political reasons (Sen, Stiglitz, Piketty and many others ) 2. Inequality is today a more complex

Global economic inequality: New evidence from the World Inequality Report

WID.WORLD THE SOURCE FOR GLOBAL INEQUALITY DATA Global economic inequality: New evidence from the World Inequality Report Lucas Chancel General coordinator, World Inequality Report Co-director, World Inequality

WID.WORLD THE SOURCE FOR GLOBAL INEQUALITY DATA Global economic inequality: New evidence from the World Inequality Report Lucas Chancel General coordinator, World Inequality Report Co-director, World Inequality

how can we explain the observed historical and comparative development of tax structures? A rapid survey about State s capacity to raise taxes

how can we explain the observed historical and comparative development of tax structures? A rapid survey about State s capacity to raise taxes Besley, Persson (2007a), The origin of state capacity: property

how can we explain the observed historical and comparative development of tax structures? A rapid survey about State s capacity to raise taxes Besley, Persson (2007a), The origin of state capacity: property

Capitalism, Inequality & Globalization. Public University of Navarre Pamplona, Spain May 21 st 2018 J. E. Stiglitz

Capitalism, Inequality & Globalization Public University of Navarre Pamplona, Spain May 21 st 2018 J. E. Stiglitz In many ways, most advanced economies not been performing well US worst example, most European

Capitalism, Inequality & Globalization Public University of Navarre Pamplona, Spain May 21 st 2018 J. E. Stiglitz In many ways, most advanced economies not been performing well US worst example, most European

Wealth, Inequality & Taxation T. Piketty, IMF Supplementary slides

Wealth, Inequality & Taxation T. Piketty, IMF 27-09-2012 Supplementary slides Decomposition results: 1870-2010 Annual series for US, Germany, France, UK, 1870-2010 Additive vs multiplicative decomposition

Wealth, Inequality & Taxation T. Piketty, IMF 27-09-2012 Supplementary slides Decomposition results: 1870-2010 Annual series for US, Germany, France, UK, 1870-2010 Additive vs multiplicative decomposition

Lecture 4: From capital/income ratios to capital shares

Economics of Inequality (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2014-2015 Lecture 4: From capital/income ratios to capital shares (Tuesday October 14 th 2014) (check

Economics of Inequality (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2014-2015 Lecture 4: From capital/income ratios to capital shares (Tuesday October 14 th 2014) (check

Tax Simplicity and Heterogeneous Learning

80 Tax Simplicity and Heterogeneous Learning Philippe Aghion (College de France) Ufuk Akcigit (Chicago) Matthieu Lequien (Banque de France) Stefanie Stantcheva (Harvard) 80 Motivation: The Value of Tax

80 Tax Simplicity and Heterogeneous Learning Philippe Aghion (College de France) Ufuk Akcigit (Chicago) Matthieu Lequien (Banque de France) Stefanie Stantcheva (Harvard) 80 Motivation: The Value of Tax

Reflections on capital taxation

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

The Economic Program. June 2014

The Economic Program TO: Interested Parties FROM: Alicia Mazzara, Policy Advisor for the Economic Program; and Jim Kessler, Vice President for Policy RE: Three Ways of Looking At Income Inequality June

The Economic Program TO: Interested Parties FROM: Alicia Mazzara, Policy Advisor for the Economic Program; and Jim Kessler, Vice President for Policy RE: Three Ways of Looking At Income Inequality June

Econ 133 Global Inequality and Growth. What is Income? Gabriel Zucman

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign 2. Income = labor + capital 3. Functional vs. personal distribution 4. Factor

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign 2. Income = labor + capital 3. Functional vs. personal distribution 4. Factor

Lecture notes 2: Physical Capital, Development and Growth

Lecture notes 2: Physical Capital, Development and Growth These notes are based on a draft manuscript Economic Growth by David N. Weil. All rights reserved. Lecture notes 2: Physical Capital, Development

Lecture notes 2: Physical Capital, Development and Growth These notes are based on a draft manuscript Economic Growth by David N. Weil. All rights reserved. Lecture notes 2: Physical Capital, Development

10 reasons to invest in France

October 2009 10 reasons to invest in France IFA Keys to understanding the new France 2 1 An economy with a global outlook Foreign companies employ over 2.8 million people in France at 23,000 different

October 2009 10 reasons to invest in France IFA Keys to understanding the new France 2 1 An economy with a global outlook Foreign companies employ over 2.8 million people in France at 23,000 different

Distributional National Accounts (DINA) Guidelines : Concepts and Methods used in WID.world

Guidelines : Concepts and Methods used in WID.world") WID.world WORKING PAPER SERIES N 2016/1 Distributional National Accounts (DINA) Guidelines : Concepts and Methods used in WID.world Facundo Alvaredo, Anthony Atkinson, Lucas Chancel, Thomas Piketty, Emmanuel

WID.world WORKING PAPER SERIES N 2016/1 Distributional National Accounts (DINA) Guidelines : Concepts and Methods used in WID.world Facundo Alvaredo, Anthony Atkinson, Lucas Chancel, Thomas Piketty, Emmanuel

Taxation of High Net Worth Individuals (HNWIs)

") Taxation of High Net Worth Individuals (HNWIs) 2 nd ATRN Congress, Seychelles Dr. Barbara Dutzler 07/09/2016 GFG in Africa Seite 1 Agenda 1) Why to tax HNWI 2) How to tax HNWI 3) How to boost compliance

Taxation of High Net Worth Individuals (HNWIs) 2 nd ATRN Congress, Seychelles Dr. Barbara Dutzler 07/09/2016 GFG in Africa Seite 1 Agenda 1) Why to tax HNWI 2) How to tax HNWI 3) How to boost compliance

The 2017 Tax Cuts and Jobs Act

70 East Lake Street Suite 1700 Chicago, IL 60601 www.ctbaonline.org The 2017 Tax Cuts and Jobs Act S A T U R D A Y, J A N U A R Y 1 3, 2 0 1 8 T A X S C A M T E A C H - IN S K O K I E P U B L I C L I B

70 East Lake Street Suite 1700 Chicago, IL 60601 www.ctbaonline.org The 2017 Tax Cuts and Jobs Act S A T U R D A Y, J A N U A R Y 1 3, 2 0 1 8 T A X S C A M T E A C H - IN S K O K I E P U B L I C L I B

The Elephant Curve of Global Inequality and Growth *

The Elephant Curve of Global Inequality and Growth * Facundo Alvaredo (Paris School of Economics, and Conicet); Lucas Chancel (Paris School of Economics and Iddri Sciences Po); Thomas Piketty (Paris School

The Elephant Curve of Global Inequality and Growth * Facundo Alvaredo (Paris School of Economics, and Conicet); Lucas Chancel (Paris School of Economics and Iddri Sciences Po); Thomas Piketty (Paris School

The Long-Run Determinants of Inequality: What Can We Learn From Top Income Data?

The Long-Run Determinants of Inequality: What Can We Learn From Top Income Data? Jesper Roine, Jonas Vlachos and Daniel Waldenström (paper at: www.anst.uu.se/danwa175 ) XXIV International Conference of

The Long-Run Determinants of Inequality: What Can We Learn From Top Income Data? Jesper Roine, Jonas Vlachos and Daniel Waldenström (paper at: www.anst.uu.se/danwa175 ) XXIV International Conference of

Fiscal Fact. Reversal of the Trend: Income Inequality Now Lower than It Was under Clinton. Introduction. By William McBride

Fiscal Fact January 30, 2012 No. 289 Reversal of the Trend: Income Inequality Now Lower than It Was under Clinton By William McBride Introduction Numerous academic studies have shown that income inequality

Fiscal Fact January 30, 2012 No. 289 Reversal of the Trend: Income Inequality Now Lower than It Was under Clinton By William McBride Introduction Numerous academic studies have shown that income inequality

Econ 133 Global Inequality and Growth. What is Income? Gabriel Zucman

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign income 2. Income = labor income + capital income 3. Functional vs. personal

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign income 2. Income = labor income + capital income 3. Functional vs. personal

Globalization, Inequality, and Tax Justice

Globalization, Inequality, and Tax Justice Gabriel Zucman (UC Berkeley) November 2017 How can we make globalization and tax justice compatible? One of the most pressing policy questions of our time: Globalization

Globalization, Inequality, and Tax Justice Gabriel Zucman (UC Berkeley) November 2017 How can we make globalization and tax justice compatible? One of the most pressing policy questions of our time: Globalization

Lecture 4: Optimal Labor Income Taxation

78 Lecture 4: Optimal Labor Income Taxation Stefanie Stantcheva Fall 2017 78 TAXATION AND REDISTRIBUTION Key question: Should government reduce inequality using taxes and transfers? 1) Governments use

78 Lecture 4: Optimal Labor Income Taxation Stefanie Stantcheva Fall 2017 78 TAXATION AND REDISTRIBUTION Key question: Should government reduce inequality using taxes and transfers? 1) Governments use

Income and Wealth Concentration in Switzerland over the 20 th Century

September 2003 Income and Wealth Concentration in Switzerland over the 20 th Century Fabien Dell, INSEE Thomas Piketty, EHESS Emmanuel Saez, UC Berkeley and NBER Abstract: This paper presents homogeneous

September 2003 Income and Wealth Concentration in Switzerland over the 20 th Century Fabien Dell, INSEE Thomas Piketty, EHESS Emmanuel Saez, UC Berkeley and NBER Abstract: This paper presents homogeneous

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

From Communism to Capitalism: Private Versus Public Property and Inequality in China and Russia

WID.world WORKING PAPERS SERIES N 2018/2 From Communism to Capitalism: Private Versus Public Property and Inequality in China and Russia Filip Novokmet Thomas Piketty Li Yang Gabriel Zucman January 2018

WID.world WORKING PAPERS SERIES N 2018/2 From Communism to Capitalism: Private Versus Public Property and Inequality in China and Russia Filip Novokmet Thomas Piketty Li Yang Gabriel Zucman January 2018

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 REMINDER: Two General Rules for Government Intervention

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 REMINDER: Two General Rules for Government Intervention

People Like Us. The interplay of class and status. The Bread Controversy. The (Not-So) Extreme Makeover

Extreme Makeover") Social Class People Like Us The interplay of class and status The Bread Controversy The (Not-So) Extreme Makeover TOP Different Images of the System of Social Class Gradational conception of social class

Social Class People Like Us The interplay of class and status The Bread Controversy The (Not-So) Extreme Makeover TOP Different Images of the System of Social Class Gradational conception of social class

IRA vs. Roth IRA. Comparison Analysis of Cash Flow and Plan Assets Preface. Presented By: [Licensed user's name appears here]

![IRA vs. Roth IRA. Comparison Analysis of Cash Flow and Plan Assets Preface. Presented By: [Licensed user's name appears here]](/thumbs/93/112012102.jpg "IRA vs. Roth IRA. Comparison Analysis of Cash Flow and Plan Assets Preface. Presented By: [Licensed user's name appears here]") vs. Comparison Analysis of Cash Flow and Preface The disadvantage of a instead of an is contributions to a Roth are not deductible. The two advantages of utilizing a instead of an are 1) tax free distributions

vs. Comparison Analysis of Cash Flow and Preface The disadvantage of a instead of an is contributions to a Roth are not deductible. The two advantages of utilizing a instead of an are 1) tax free distributions

2018 Edelman Trust Barometer

2018 Edelman Trust Barometer Australia #TrustBarometer 2018 Edelman Trust Barometer Methodology Online Survey in 28 Countries 18 years of data 33,000+ respondents total All fieldwork was conducted late

2018 Edelman Trust Barometer Australia #TrustBarometer 2018 Edelman Trust Barometer Methodology Online Survey in 28 Countries 18 years of data 33,000+ respondents total All fieldwork was conducted late

High incomes and personal taxation in Colombia

High incomes and personal taxation in Colombia 1993-2010 Facundo Alvaredo Nuffield College/EMod, Conicet & Paris School of Economics & Juliana Londoño Vélez UC Berkeley Commitment to Equity Conference

High incomes and personal taxation in Colombia 1993-2010 Facundo Alvaredo Nuffield College/EMod, Conicet & Paris School of Economics & Juliana Londoño Vélez UC Berkeley Commitment to Equity Conference

SETTING UP BUSINESS IN LUXEMBOURG

www.antea-int.com SETTING UP BUSINESS IN LUXEMBOURG 1 General Aspects Luxembourg is a unique gateway to the European market through its location in the centre of Europe, between Belgium, France and Germany.

www.antea-int.com SETTING UP BUSINESS IN LUXEMBOURG 1 General Aspects Luxembourg is a unique gateway to the European market through its location in the centre of Europe, between Belgium, France and Germany.

Applying Generalized Pareto Curves to Inequality Analysis

Applying Generalized Pareto Curves to Inequality Analysis By THOMAS BLANCHET, BERTRAND GARBINTI, JONATHAN GOUPILLE-LEBRET AND CLARA MARTÍNEZ- TOLEDANO* *Blanchet: Paris School of Economics, 48 boulevard

Applying Generalized Pareto Curves to Inequality Analysis By THOMAS BLANCHET, BERTRAND GARBINTI, JONATHAN GOUPILLE-LEBRET AND CLARA MARTÍNEZ- TOLEDANO* *Blanchet: Paris School of Economics, 48 boulevard

Inequality, Capitalism & Crisis in the Long Run. Thomas Piketty Paris School of Economics Paris, AFEP Conference, July 6 th 2012

Inequality, Capitalism & Crisis in the Long Run Thomas Piketty Paris School of Economics Paris, AFEP Conference, July 6 th 2012 Why inequality keeps rising? Long run distributional trends = key question

Inequality, Capitalism & Crisis in the Long Run Thomas Piketty Paris School of Economics Paris, AFEP Conference, July 6 th 2012 Why inequality keeps rising? Long run distributional trends = key question

Measuring inequality Issues to be addressed by the HLEG subgroup on income and wealth inequality

Measuring inequality Issues to be addressed by the HLEG subgroup on income and wealth inequality Thomas Piketty Paris School of Economics OECD, January 16 th 2014 «Work under the income and wealth inequality

Measuring inequality Issues to be addressed by the HLEG subgroup on income and wealth inequality Thomas Piketty Paris School of Economics OECD, January 16 th 2014 «Work under the income and wealth inequality

FIGURE I.1. Income inequality in the United States,

FIGURE I.1. Income inequality in the United States, 1910 2010 The top decile share in US national income dropped from 45 50 percent in the 1910s 1920s to less than 35 percent in the 1950s (this is the

FIGURE I.1. Income inequality in the United States, 1910 2010 The top decile share in US national income dropped from 45 50 percent in the 1910s 1920s to less than 35 percent in the 1950s (this is the

long run inequality History and Inequality University of Oslo

long run inequality History and Inequality University of Oslo 5 Figure 8.1. Income inequality in France, 1910-2010 Share of top decile in total (incomes or wages) 45% 4 35% 3 25% Share of top income

long run inequality History and Inequality University of Oslo 5 Figure 8.1. Income inequality in France, 1910-2010 Share of top decile in total (incomes or wages) 45% 4 35% 3 25% Share of top income

2 National tax systems: Structure and recent developments

Ireland Structure and development of tax revenues Table IE.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Ranking Revenue (billion euros) A. Structure by type of

Ireland Structure and development of tax revenues Table IE.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Ranking Revenue (billion euros) A. Structure by type of

The Distribution of Federal Taxes, Jeffrey Rohaly

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

Swiss Lump Sum Taxation

Geneva, December 1 st, 2016 Swiss Lump Sum Taxation Ali Kanani Tax Partner MBL & LL.M. in International Taxation 1 INTRODUCTION 1. History 2. Current situation in Switzerland 3. Numbers 4. How does it

Geneva, December 1 st, 2016 Swiss Lump Sum Taxation Ali Kanani Tax Partner MBL & LL.M. in International Taxation 1 INTRODUCTION 1. History 2. Current situation in Switzerland 3. Numbers 4. How does it

Income Inequality in France, : Evidence from Distributional National Accounts (DINA)

") WID.world WORKING PAPER SERIES N 2017/4 Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti, Jonathan Goupille-Lebret and Thomas Piketty April

WID.world WORKING PAPER SERIES N 2017/4 Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti, Jonathan Goupille-Lebret and Thomas Piketty April

Non-French tax residents are subject

FRENCH CONNECTIONS Using a trust to own French real estate does not particularly change the ownership situation in France regarding wealth tax and inheritance tax, and may bring potential drawbacks in

FRENCH CONNECTIONS Using a trust to own French real estate does not particularly change the ownership situation in France regarding wealth tax and inheritance tax, and may bring potential drawbacks in

Effective Tax Rates on Employee Stock Options in the European Union and the USA

Brussels, May 23 Ref. Ares(214)75853-15/1/214 Effective Tax Rates on Employee Stock Options in the European Union and the USA Table of Contents INTRODUCTION...2 RESULTS...3 Normal taxation (no special

Brussels, May 23 Ref. Ares(214)75853-15/1/214 Effective Tax Rates on Employee Stock Options in the European Union and the USA Table of Contents INTRODUCTION...2 RESULTS...3 Normal taxation (no special

Optimal Labor Income Taxation (follows loosely Chapters of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

131 Undergraduate Public Economics Emmanuel Saez UC Berkeley") Optimal Labor Income Taxation (follows loosely Chapters 20-21 of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Should government reduce

Optimal Labor Income Taxation (follows loosely Chapters 20-21 of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Should government reduce

Please note that we do not update this information in real time, so you should confirm that the laws or procedures have not changed recently.

FRANCE TAX CONSIDERATIONS ON LETTING PROPERTY The following information is a guide to help you get started in learning about some of the tax requirements that are likely to apply to you when providing

FRANCE TAX CONSIDERATIONS ON LETTING PROPERTY The following information is a guide to help you get started in learning about some of the tax requirements that are likely to apply to you when providing

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

Tax Burden, Tax Mix and Economic Growth in OECD Countries

Tax Burden, Tax Mix and Economic Growth in OECD Countries PAOLA PROFETA RICCARDO PUGLISI SIMONA SCABROSETTI June 30, 2015 FIRST DRAFT, PLEASE DO NOT QUOTE WITHOUT THE AUTHORS PERMISSION Abstract Focusing

Tax Burden, Tax Mix and Economic Growth in OECD Countries PAOLA PROFETA RICCARDO PUGLISI SIMONA SCABROSETTI June 30, 2015 FIRST DRAFT, PLEASE DO NOT QUOTE WITHOUT THE AUTHORS PERMISSION Abstract Focusing

Income Inequality in Korea,

Income Inequality in Korea, 1958-2013. Minki Hong Korea Labor Institute 1. Introduction This paper studies the top income shares from 1958 to 2013 in Korea using tax return. 2. Data and Methodology In

Income Inequality in Korea, 1958-2013. Minki Hong Korea Labor Institute 1. Introduction This paper studies the top income shares from 1958 to 2013 in Korea using tax return. 2. Data and Methodology In

Microeconomics. The Design of the Tax System. Introduction. In this chapter, look for the answers to these questions: N.

C H A P T E R 12 The Design of the Tax System P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

C H A P T E R 12 The Design of the Tax System P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

Roche & Cie. Chartered Accountants Since 1948 Specialists in Property for Non-Residents INVESTING IN FRANCE PROPERTY TAXATION 2018

ENGLISH Chartered Accountants Since 1948 Specialists in Property for Non-Residents INVESTING IN FRANCE PROPERTY TAXATION 2018 Specialists in property for non-residents, will assist you in the purchase/resale

ENGLISH Chartered Accountants Since 1948 Specialists in Property for Non-Residents INVESTING IN FRANCE PROPERTY TAXATION 2018 Specialists in property for non-residents, will assist you in the purchase/resale

Intermediate Macroeconomic Theory. Costas Azariadis. Costas Azariadis. Lecture 3: Productivity and Labor

Lecture 3: Productivity and Labor 1. THE ISSUES a)productivity most important determinant of living standards in the long run 2008 U.S. GDP per worker employed (current $) $100,000 per worker per year

Lecture 3: Productivity and Labor 1. THE ISSUES a)productivity most important determinant of living standards in the long run 2008 U.S. GDP per worker employed (current $) $100,000 per worker per year

Measuring Unemployment Economic Growth and Productivity. unemployed. News

Economic Growth and Productivity News Unemployment Redux Nations Have Experienced a Substantial Rise in Living Standards Over the Last 150 Years. Labor Productivity Accounts for a Great Deal of the Observed

Economic Growth and Productivity News Unemployment Redux Nations Have Experienced a Substantial Rise in Living Standards Over the Last 150 Years. Labor Productivity Accounts for a Great Deal of the Observed

Morocco Tax Guide 2012

Tax Guide 2012 structure of country descriptions a. taxes payable FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER

Tax Guide 2012 structure of country descriptions a. taxes payable FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER

Wealth Inequality Reading Summary by Danqing Yin, Oct 8, 2018

Summary of Keister & Moller 2000 This review summarized wealth inequality in the form of net worth. Authors examined empirical evidence of wealth accumulation and distribution, presented estimates of trends

Summary of Keister & Moller 2000 This review summarized wealth inequality in the form of net worth. Authors examined empirical evidence of wealth accumulation and distribution, presented estimates of trends

Lecture 6: Money, finance and crisis in historical perspective

Economic History (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2015-2016 Lecture 6: Money, finance and crisis in historical perspective (check on line for updated versions)

Economic History (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2015-2016 Lecture 6: Money, finance and crisis in historical perspective (check on line for updated versions)

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2017 preliminary estimates)

") Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2017 preliminary estimates) Emmanuel Saez, UC Berkeley October 13, 2018 What s new for recent years? 2016-2017: Robust

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2017 preliminary estimates) Emmanuel Saez, UC Berkeley October 13, 2018 What s new for recent years? 2016-2017: Robust

Income Inequality in France, : Evidence from Distributional National Accounts (DINA)

") WID.world WORKING PAPER SERIES N 2017/4 Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti, Jonathan Goupille-Lebret and Thomas Piketty April

WID.world WORKING PAPER SERIES N 2017/4 Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti, Jonathan Goupille-Lebret and Thomas Piketty April

ECONOMIC COMMENTARY. Income Inequality Matters, but Mobility Is Just as Important. Daniel R. Carroll and Anne Chen

ECONOMIC COMMENTARY Number 2016-06 June 20, 2016 Income Inequality Matters, but Mobility Is Just as Important Daniel R. Carroll and Anne Chen Concerns about rising income inequality are based on comparing

ECONOMIC COMMENTARY Number 2016-06 June 20, 2016 Income Inequality Matters, but Mobility Is Just as Important Daniel R. Carroll and Anne Chen Concerns about rising income inequality are based on comparing

Optimal Labor Income Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Optimal Labor Income Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Do/should government reduce inequality using taxes and transfers?

Optimal Labor Income Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Do/should government reduce inequality using taxes and transfers?

Introduction of World Wealth and Income Database

Introduction The World Wealth and Income Database (WID.world) aims to provide open and convenient access to the historical evolution of the world distribution of income and wealth, both within countries

Introduction The World Wealth and Income Database (WID.world) aims to provide open and convenient access to the historical evolution of the world distribution of income and wealth, both within countries

6 Critical SOCIAL SECURITY Facts Retirees Must Know

6 Critical SOCIAL SECURITY Facts Retirees Must Know Updated as of May 18, 2016 Introduction Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming

6 Critical SOCIAL SECURITY Facts Retirees Must Know Updated as of May 18, 2016 Introduction Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming

THE STATISTICS OF INCOME (SOI) DIVISION OF THE

DIVISION OF THE") 104 TH ANNUAL CONFERENCE ON TAXATION A NEW LOOK AT THE RELATIONSHIP BETWEEN REALIZED INCOME AND WEALTH Barry Johnson, Brian Raub, and Joseph Newcomb, Statistics of Income, Internal Revenue Service THE

104 TH ANNUAL CONFERENCE ON TAXATION A NEW LOOK AT THE RELATIONSHIP BETWEEN REALIZED INCOME AND WEALTH Barry Johnson, Brian Raub, and Joseph Newcomb, Statistics of Income, Internal Revenue Service THE

Rent-seeking elites, integration, and the coevolution of political institutions

Rent-seeking elites, integration, and the coevolution of political institutions Arthur Silve Paris School of Economics Sciences Po November 20th, 2014 Taxing the moveables: an old problem 1225 Magna Carta:

Rent-seeking elites, integration, and the coevolution of political institutions Arthur Silve Paris School of Economics Sciences Po November 20th, 2014 Taxing the moveables: an old problem 1225 Magna Carta:

TAX REFORM, DEMOGRAPHIC CHANGE AND RISING INEQUALITY

TAX REFORM, DEMOGRAPHIC CHANGE AND RISING INEQUALITY Asia and the Pacific Policy Society Conference 2014: G20 s policy Challenges for ASIA and the Pacific 11-12 March 2014 Crawford School of Public Policy

TAX REFORM, DEMOGRAPHIC CHANGE AND RISING INEQUALITY Asia and the Pacific Policy Society Conference 2014: G20 s policy Challenges for ASIA and the Pacific 11-12 March 2014 Crawford School of Public Policy

UK and Ireland impose highest taxes on inheritance of all major economies

Prague, 25 April 2014 Press release UK and Ireland impose highest taxes on inheritance of all major economies Old world economies charge higher inheritance and estate taxes than the new world Stealth taxes

Prague, 25 April 2014 Press release UK and Ireland impose highest taxes on inheritance of all major economies Old world economies charge higher inheritance and estate taxes than the new world Stealth taxes

The figures in this factsheet are correct for the 2010/11 tax year, which runs from 6 April 2010 to 5 April 2011.

Factsheet 15 April 2010 Income Tax About this factsheet This factsheet gives basic information about Income Tax for older people. It explains tax rates, the main types of income that are not taxable and

Factsheet 15 April 2010 Income Tax About this factsheet This factsheet gives basic information about Income Tax for older people. It explains tax rates, the main types of income that are not taxable and

During fiscal year 2004, the federal government

Preview Objectives After studying this section you will be able to: 1. Describe the process of paying individual income. 2. Explain the basic characteristics of corporate income. 3. Understand the purpose

Preview Objectives After studying this section you will be able to: 1. Describe the process of paying individual income. 2. Explain the basic characteristics of corporate income. 3. Understand the purpose