Taxable Income Elasticities. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

|

|

|

- Samuel Hunter

- 5 years ago

- Views:

Transcription

1 Taxable Income Elasticities 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1

2 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation elasticities Two main reasons: 1) What matters for policy is the total behavioral response to tax rates (not only hours of work but also occupational choices, avoidance, etc.) 2) Data availability: taxable income is precisely measured in tax return data Recent overview of this literature: Saez-Slemrod-Giertz JEL 12 2

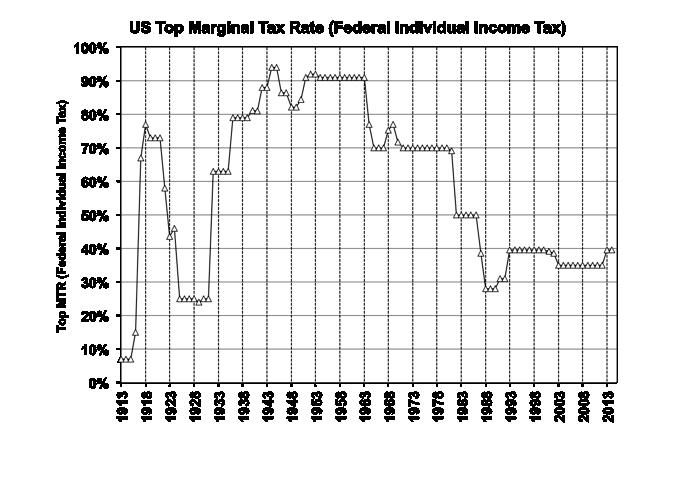

3 FEDERAL INCOME TAX CHANGES Tax rates change frequently over time Biggest tax rate changes have happened at the top Key recent reforms: Reagan I: ERTA 81: top rate 70% to 50% ( ) Reagan II: TRA 86: top rate 50% to 28% ( ) Clinton: OBRA 93: top rate 31% to 39.6% ( ) Bush: EGTRRA 01: top rate 39.6% to 35% ( ) Taxable Income = Ordinary Income + Realized Capital Gains - Deductions Each component can respond to MT Rs 3

4

5 LONG-RUN EVIDENCE IN THE Goal: evaluate whether top pre-tax incomes respond to changes in one minus the marginal tax rate (=net-of-tax rate) Focus is on pre-tax income before deductions and excluding realized capital gains (because they are taxed at lower separate rate) Piketty-Saez QJE 03 estimate top income shares since 1913 [IRS tabulations for , IRS micro-files since 1960] Piketty-Saez-Stantcheva AEJ 13 estimate the effect of top MTR on top income shares in the since

6 Top 1% Income Shares (%) Top 1% Income Share and Top MTR Top 1% (excluding Capital Gains) Top MTR Marginal Tax Rates (%) Year

7 INCOME SHARE BASED ELASTICITY ESTIMATION 1) Tax Reform Episode: Compare top pre-tax income shares at t 0 (before reform) and t 1 (after reform) e = log sh t1 log sh t0 log(1 τ t1 ) log(1 τ t0 ) where sh t is top income share and τ t is the average MTR for top group in year t Identification assumption: absent tax change, sh t0 = sh t1 2) Full Time Series: Run regression: log sh t = α + e log(1 τ t ) + ε t and adding time controls to capture non-tax related top income share trends ID assumption: non-tax related changes in sh t τ t 7

8 LONG-RUN EVIDENCE IN THE 1) Clear correlation between top incomes and top income rates both in several short-run tax reform episodes and in the longrun [but hard to assess long-run tax causality] 2) Correlation largely absent below the top 1% (such as the next 9%) 3) Top income shares sometimes do not respond to large tax rate cuts [e.g., Kennedy Tax Cuts of early 1960s] 4) Top income shares can change substantially for non-tax related reasons: (a) Great Depression (MTR stable and top income shares, (b) 1990s: MTR and top income shares 8

9 FISCAL EXTERNALITIES A Fiscal externality is a change in tax revenue that occurs in any tax base z B other than z due to the behavioral response to the tax change in the initial base z (1) z B can be a different tax base in the same time period (such as corporate income tax base) Income shifting (2) z B can be the same tax base in a different time period (such as future income) Inter-temporal Substitution Efficiency and optimal tax analysis depend on effect on total tax revenue 9

10 Inter-Temporal Substitution: Realized Capital Gains Realized capital gains occur when individual sells asset at a higher price than buying price Individuals have flexibility in the timing of asset sales and capital gains realizations TRA 86 lowered the top tax rate on ordinary income from 50% to 28% but increased the top tax rate on realized capital gains from 20% to 28% Surge in capital gains realizations in 1986 [and depressed capital gains in 1987] to take advantage of low 20% rate before 28% tax rate applies Short-term elasticity is very large but long-term elasticity is certainly much smaller 10

11 100% Top MTR ordinary income vs. capital gains 100% Top MTR (Federal Individual Income Tax) 90% 80% 70% 60% 50% 40% 30% 20% 10% Top MTR 0% Top MTR (capital gains) 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Source: statistics computed by the author

12 Top 0.1% Pre- Tax Income Share and Composi:on 12% 10% 8% Capital Gains Capital Income Business Income Salaries 6% 4% 2% 0% Source: Piketty and Saez, 2003 updated to Series based on pre-tax cash market income including or excluding realized capital gains, and always excluding government transfers

13 Inter-Temporal Substitution: Stock-Options Goolsbee JPE 00 analyzes CEO pay around the 1993 Clinton top tax rate increase [from 31% in 1992 to 39.6% in 1993 announced in late 1992] on executive pay Finds a strong re-timing response through stock-option exercise (executive can choose the timing of their stock-option exercises) Large short-term response due to re-timing, small long-term response 13

14 Source: Goolsbee (2000), p. 365

15 STOCK OPTIONS Major form of compensation of top executives. Theoretical goal is to motivate executives to increase the value of the company (stock price P (t)) Stock-option is granted at date t 0 allow executives to buy N company shares at price P (t 0 ) on or after t 1 (in general t 1 t years = vesting period) Executive exercise option at (chosen) time t 2 t 1 : pays N P (t 0 ) to get shares valued N P (t 2 ). Exercise profit N[P (t 2 ) P (t 0 )] (considered and taxed as wage income in the ) After t 2, executive owns N shares, eventually sold at time t 3 t 2 : realized capital gain N[P (t 3 ) P (t 2 )] (taxed as capital gains) 15

16 Income Shifting: Corporate And Individual Tax Base Businesses can be organized as corporations or unincorporated businesses [also called pass-through entities] Corporate profits are first taxed by corporate income tax [rate τ c ] Net-of-tax profits are taxed again when finally distributed to shareholders. 2 distribution options: a) dividends [tax rate τ d ] b) retained profits increase stock price: shareholders realize capital gains when finally selling the stock [tax rate τ cg ] For unincorporated businesses (sole proprietorships, partnerships, S-corporations) profits are taxed directly and solely as individual income (rate τ i ) 16

17 CORPORATE AND INDIVIDUAL TAX BASE Corporate form best if (1 τ c )(1 τ cg ) > 1 τ i fed taxes in 2013: τ c = 35%, τ cg = 20% (less because of deferral value), τ d = 20% τ i = 39.6%, (top rate) Today, individual form is best Before TRA 86 (and especially before ERTA 81), top individual rate τ i was much higher so corporate form was best Shifts from corporate to individual base increases business profits at the expense of dividends and realized capital gains Large part of TRA 86 response is due to such shifting 17

18 3.5% The Top 0.01% Income Share, Composition, and MTR 90% Top 0.01% share and composition 3.0% 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% Wages Partnership Dividends Other S-Corp. Sole Prop. Interest MTR 80% 70% 60% 50% 40% 30% 20% 10% 0% Marginal Tax Rate for the top 0.01% Source: Saez et al. (2010)

19 Bottom Line on Behavioral Responses to Taxes 1) Clear evidence of strong responses to tax changes due to re-timing or income shifting 2) Heterogeneity in tax responses due to heterogeneity in shifting opportunities [e.g., Kennedy tax cuts of 61 vs. TRA 86] 3) Top income shares can change drastically without changes in tax rates [e.g., ] 4) Difficult to know from single country time series the role played by top tax rate cuts in the surge of top incomes International evidence can cast further useful evidence 19

20 TOP RATES AND TOP INCOMES INTERNATIONAL EVIDENCE 1) Use pre-tax top 1% income share data from 18 OECD countries since 1960 using the World Top Incomes Database 2) Compute top (statutory) individual income tax rates using OECD data [including both central and local income taxes]. Plot top 1% pre-tax income share against top MTR in , in , and vs

21 Elasticity=.07 (.15) Top 1% Income Share (%) Top Marginal Tax Rate (%) A. Top 1% Share and Top Marginal Tax Rate in

22 Elasticity= 1.90 (.43) Top 1% Income Share (%) Top Marginal Tax Rate (%) B. Top 1% Share and Top Marginal Tax Rate in

23 Elasticity=.47 (.11) Change in Top 1% Income Share (points) Change in Top Marginal Tax Rate (points) Change in Top Tax Rate and Top 1% Share, to

24 TOP RATES AND TOP INCOMES EVIDENCE 1) Pre-tax Top income shares have increased significantly in some but not all countries [Atkinson-Piketty-Saez JEL 11] 2) Top tax rates have come down significantly in a number of countries since 1960s 3) Correlation between 1) and 2) is strong but not perfect: lower top tax rates are a necessary but not sufficient condition for surge in top incomes 22

25 ECONOMIC EFFECTS OF TAXING THE TOP 1% Strong empirical evidence that pre-tax top incomes are affected by top tax rates 3 potential scenarios with very different policy consequences 1) Supply-Side: Top earners work less and earn less when top tax rate increases Top tax rates should not be too high 2) Tax Avoidance/Evasion: Top earners avoid/evade more when top tax rate increases a) Eliminate loopholes, b) Then increase top tax rates 3) Rent-seeking: Top earners extract more pay (at the expense of the 99%) when top tax rates are low High top tax rates are desirable 23

26 Real changes vs. tax Avoidance? (Piketty-Saez-Stantcheva AEJ 13) Correlation between pre-tax top incomes and top tax rates If this is due to tax avoidance, real top income shares were as high as today in the 1960s-70s but top earners reported a smaller fraction of their incomes [draw graph] correlation should be much stronger when using narrow taxable income definition than when using comprehensive income definition (including realized capital gains) Empirical correlation is very similar ruling out the pure tax avoidance scenario 24

27 Top 1% Income Shares (%) Tax Avoidance: Top 1% Income Shares and Top MTR Top 1% Share Top 1% (excl. KG) Top MTR MTR K gains Marginal Tax Rates (%) Year

28 Supply-Side or Rent-Seeking? (Piketty-Saez-Stantcheva AEJ 13) Correlation between pre-tax top incomes and top tax rates If rent-seeking: growth in top 1% incomes should come at the expense of bottom 99% (and conversely) Two macro-preliminary tests: 1) In the, top 1% incomes grow slowly from 1933 to 1975 and fast afterwards. Bottom 99% incomes grow fast from 1933 to 1975 and slowly afterwards Consistent with rentseeking effects 2) Look at cross-country correlation between economic growth and top tax rate cuts No correlation supports rent-seeking One micro-test using CEO pay data 26

29 Real Income per adult (1913=100) Top 1% and Bottom 99% Income Growth Top 1% Top MTR Bottom 99% Marginal Tax Rate (%) Year

30 Top tax rates and average growth GDP per capita real annual growth (%) Change in Top Marginal Tax Rate (points) A. Growth and Change in Top Marginal Tax Rate Piketty, Saez & Stantcheva () Three Elasticities November / 62

31 Top tax rates and average growth GDP per capita real annual growth (%) Change in Top Marginal Tax Rate (points) B. Growth (adjusted for initial 1960 GDP) Piketty, Saez & Stantcheva () Three Elasticities November / 62

32 INTERNATIONAL CEO PAY EVIDENCE Recent micro-data for 2006 gathered by Fernandes, Ferreira, Matos, Murphy RFS 12. 1) CEO pay across countries strongly negatively correlated with top tax rates 2) Correlation remains as strong even when controlling for firms characteristics and performance Consistent with rent-seeking effects 29

33 CEO pay($ million, log scale) A. Average CEO compensation United States Elasticity= 1.97 (.27) United Kingdom Belgium Top Income Marginal Tax Rate Piketty, Saez & Stantcheva () Three Elasticities November / 62

34 CEO pay($ million, log scale) with controls B. Average CEO compensation with controls Elasticity= 1.90 (.29) United States United Kingdom Belgium Top Income Marginal Tax Rate Piketty, Saez & Stantcheva () Three Elasticities November / 62

35 Tax Induced International Migration Public debate concern that top skilled individuals move to low tax countries (e.g., in EU context) or low tax states (within Federation) Migration concern bigger in public debate than supply-side within a country debate Little work on tax induced international migration of top skilled workers Hard to get data but interesting variation due to proliferation of special low tax schemes for highly paid foreigners in Europe Kleven-Landais-Saez AER 13 look at football players in Europe (highly mobile group, many tax reforms) Find significant migration responses to taxes after football market was de-regulated in 95 31

36 KLEVEN-LANDAIS-SAEZ-SCHULTZ 13 Exploit the 1991 tax scheme in : high earnings immigrants ( 103, 000 Euros/year) taxed at flat 25% rate (instead of regular tax with top 59% rate) for 3 years Use population wide Danish tax data and DD strategy: compare immigrants above eligibility earnings threshold (treatment) to immigrants below threshold (control) Key Finding: Scheme doubles the number of highly paid foreigners in relative to controls Elasticity of migration with respect to the net-of-tax rate above one (much larger than the within country elasticity of earnings) Tax coordination will be key to preserve progressive taxation in the European Union 32

37 Figure 3: Total number of foreigners in different income groups # of foreigners Control 1 Control 2 Treatment Control 1= annualized income between.8 and.9 of threshold Control 2= annualized income between.9 and.995 of threshold. Source: Diamond and Saez JEP'11

38 REFERENCES Atkinson, A., F. Alvaredo, T. Piketty and E. Saez The World Top Incomes Database, (web) Atkinson, A., T. Piketty and E. Saez Top Incomes in the Long Run of History, Journal of Economic Literature, 49(1), 2011, (web) Goolsbee, A. What Happens When You Tax the Rich? Evidence from Executive Compensation, Journal of Political Economy, Vol. 108, 2000, (web) Gordon, R.H. and J. Slemrod Are Real Responses to Taxes Simply Income Shifting Between Corporate and Personal Tax Bases?, NBER Working Paper No. 6576, (web) Kleven, Henrik, Camille Landais, and Emmanuel Saez Taxation and International Mobility of Superstars: Evidence from the European Football Market, NBER Working Paper No , November 2010, revised June (web) Kleven, Henrik, Camille Landais, Emmanuel Saez, and Esben Schultz Taxation and International Migration of Top Earners: Evidence from the Foreigner Tax Scheme in, preliminary draft, November (web) 34

39 Piketty, T. and E. Saez Income Inequality in the United States, , Quarterly Journal of Economics, Vol. 116, 2003, (web) Piketty, Thomas, Emmanuel Saez, and Stefanie Stantcheva Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities, NBER Working Paper No , November (web) Saez, E., J. Slemrod, and S. Giertz (2012) The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review, Journal of Economic Literature (web)

Lecture 6: Taxable Income Elasticities

1 40 Lecture 6: Taxable Income Elasticities Stefanie Stantcheva Fall 2017 40 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation

1 40 Lecture 6: Taxable Income Elasticities Stefanie Stantcheva Fall 2017 40 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation

230B: Public Economics Taxable Income Elasticities

230B: Public Economics Taxable Income Elasticities Emmanuel Saez Berkeley 1 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation

230B: Public Economics Taxable Income Elasticities Emmanuel Saez Berkeley 1 TAXABLE INCOME ELASTICITIES Modern public finance literature focuses on taxable income elasticities instead of hours/participation

Taxing the Rich More: Evidence from the 2013 Tax Increase

Taxing the Rich More: Evidence from the 2013 Tax Increase Emmanuel Saez, UC Berkeley and NBER October 2016 Tax Policy and the Economy 1 MOTIVATION Controversial debate on the proper taxation of top incomes

Taxing the Rich More: Evidence from the 2013 Tax Increase Emmanuel Saez, UC Berkeley and NBER October 2016 Tax Policy and the Economy 1 MOTIVATION Controversial debate on the proper taxation of top incomes

Optimal Labor Income Taxation. Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011

Optimal Labor Income Taxation Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011 MODERN ECONOMIES DO SIGNIFICANT REDISTRIBUTION 1) Taxes:

Optimal Labor Income Taxation Thomas Piketty, Paris School of Economics Emmanuel Saez, UC Berkeley PE Handbook Conference, Berkeley December 2011 MODERN ECONOMIES DO SIGNIFICANT REDISTRIBUTION 1) Taxes:

TAXABLE INCOME RESPONSES. Henrik Jacobsen Kleven London School of Economics. Lecture Notes for MSc Public Economics (EC426): Lent Term 2014

: Lent Term 2014") TAXABLE INCOME RESPONSES Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Economics (EC426): Lent Term 2014 AGENDA The Elasticity of Taxable Income (ETI): concept and policy

TAXABLE INCOME RESPONSES Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Economics (EC426): Lent Term 2014 AGENDA The Elasticity of Taxable Income (ETI): concept and policy

Taxation and International Migration of Superstars: Evidence from the European Football Market

Taxation and International Migration of Superstars: Evidence from the European Football Market Henrik Kleven (London School of Economics) Camille Landais (Stanford University) Emmanuel Saez (UC Berkeley)

Taxation and International Migration of Superstars: Evidence from the European Football Market Henrik Kleven (London School of Economics) Camille Landais (Stanford University) Emmanuel Saez (UC Berkeley)

Hilary Hoynes UC Davis EC230. Taxes and the High Income Population

Hilary Hoynes UC Davis EC230 Taxes and the High Income Population New Tax Responsiveness Literature Started by Feldstein [JPE The Effect of MTR on Taxable Income: A Panel Study of 1986 TRA ]. Hugely important

Hilary Hoynes UC Davis EC230 Taxes and the High Income Population New Tax Responsiveness Literature Started by Feldstein [JPE The Effect of MTR on Taxable Income: A Panel Study of 1986 TRA ]. Hugely important

Top Marginal Tax Rates and Within-Firm Income Inequality

. Top Marginal Tax Rates and Within-Firm Income Inequality Extended abstract. Not for quotation. Comments welcome. Max Risch University of Michigan May 12, 2017 Extended Abstract Behavioral responses to

. Top Marginal Tax Rates and Within-Firm Income Inequality Extended abstract. Not for quotation. Comments welcome. Max Risch University of Michigan May 12, 2017 Extended Abstract Behavioral responses to

Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities

Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities Thomas Piketty (PSE) Emmanuel Saez (Berkeley and NBER) Stefanie Stantcheva (MIT) November 2012 Piketty, Saez & Stantcheva () Three Elasticities

Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticities Thomas Piketty (PSE) Emmanuel Saez (Berkeley and NBER) Stefanie Stantcheva (MIT) November 2012 Piketty, Saez & Stantcheva () Three Elasticities

Taxation, Migration, and Innovation: The Effect of Taxes on the Location of Star Scientists?

: The Effect of Taxes on the Location of Star Scientists? Enrico Moretti (UC Berkeley) Daniel Wilson (Federal Reserve Bank of San Francisco) Preliminary IZA, 31 May 2014 *The views expressed in this paper

: The Effect of Taxes on the Location of Star Scientists? Enrico Moretti (UC Berkeley) Daniel Wilson (Federal Reserve Bank of San Francisco) Preliminary IZA, 31 May 2014 *The views expressed in this paper

Sarah K. Burns James P. Ziliak. November 2013

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Lecture on Taxable Income Elasticities PhD Course in Uppsala

Lecture on Taxable Income Elasticities PhD Course in Uppsala Håkan Selin Institute for Evaluation of Labour Market and Education Policy Uppsala, May 15, 2014 1 TAXABLE INCOME ELASTICITIES Modern public

Lecture on Taxable Income Elasticities PhD Course in Uppsala Håkan Selin Institute for Evaluation of Labour Market and Education Policy Uppsala, May 15, 2014 1 TAXABLE INCOME ELASTICITIES Modern public

Top MTR. Threshold/Averag e Income. US Top Marginal Tax Rate and Top Bracket Threshold. Top MTR (Federal Individual Income Tax)

") Source: IRS, Statistics of Income Division, Historical Table 23 Top Marginal Tax Rate and Top Bracket Threshold Top MTR (Federal Individual Income Tax) 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% Top MTR

Source: IRS, Statistics of Income Division, Historical Table 23 Top Marginal Tax Rate and Top Bracket Threshold Top MTR (Federal Individual Income Tax) 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% Top MTR

THE ELASTICITY OF TAXABLE INCOME Fall 2012

THE ELASTICITY OF TAXABLE INCOME 14.471 - Fall 2012 1 Why Focus on "Elasticity of Taxable Income" (ETI)? i) Captures Not Just Hours of Work but Other Changes (Effort, Structure of Compensation, Occupation/Career

THE ELASTICITY OF TAXABLE INCOME 14.471 - Fall 2012 1 Why Focus on "Elasticity of Taxable Income" (ETI)? i) Captures Not Just Hours of Work but Other Changes (Effort, Structure of Compensation, Occupation/Career

INCOME AND WEALTH INEQUALITY: EVIDENCE AND POLICY IMPLICATIONS*

INCOME AND WEALTH INEQUALITY: EVIDENCE AND POLICY IMPLICATIONS* EMMANUEL SAEZ (with an introduction by David Card) Drawing on the author s work, this lecture presents evidence on U.S. income and wealth

INCOME AND WEALTH INEQUALITY: EVIDENCE AND POLICY IMPLICATIONS* EMMANUEL SAEZ (with an introduction by David Card) Drawing on the author s work, this lecture presents evidence on U.S. income and wealth

Reported Incomes and Marginal Tax Rates, : Evidence and Policy Implications

Very Preliminary - Comments Welcome Reported Incomes and Marginal Tax Rates, 1960-2000: Evidence and Policy Implications Emmanuel Saez, UC Berkeley and NBER August 23, 2003 Abstract This paper use income

Very Preliminary - Comments Welcome Reported Incomes and Marginal Tax Rates, 1960-2000: Evidence and Policy Implications Emmanuel Saez, UC Berkeley and NBER August 23, 2003 Abstract This paper use income

Lecture 4: Taxation and income distribution

Lecture 4: Taxation and income distribution Public Economics 336/337 University of Toronto Public Economics 336/337 (Toronto) Lecture 4: Income distribution 1 / 33 Introduction In recent years we have

Lecture 4: Taxation and income distribution Public Economics 336/337 University of Toronto Public Economics 336/337 (Toronto) Lecture 4: Income distribution 1 / 33 Introduction In recent years we have

Part 1: Welfare Analysis and Optimal Taxation (Hendren) Basics of Welfare Estimation. Hendren, N (2014). The Policy Elasticity, NBER Working Paper

Basics of Welfare Estimation. Hendren, N (2014). The Policy Elasticity, NBER Working Paper") 2450B Reading List Part 1: Welfare Analysis and Optimal Taxation (Hendren) Basics of Welfare Estimation Saez, Slemrod and Giertz (2012). The Elasticity of Taxable Income with Respect to Marginal Tax Rates:

2450B Reading List Part 1: Welfare Analysis and Optimal Taxation (Hendren) Basics of Welfare Estimation Saez, Slemrod and Giertz (2012). The Elasticity of Taxable Income with Respect to Marginal Tax Rates:

Econ 551 Government Finance: Revenues Winter 2018

Econ 551 Government Finance: Revenues Winter 2018 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture 8c: Taxing High Income Workers ECON 551: Lecture 8c 1 of 34

Econ 551 Government Finance: Revenues Winter 2018 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture 8c: Taxing High Income Workers ECON 551: Lecture 8c 1 of 34

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2017 preliminary estimates)

") Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2017 preliminary estimates) Emmanuel Saez, UC Berkeley October 13, 2018 What s new for recent years? 2016-2017: Robust

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2017 preliminary estimates) Emmanuel Saez, UC Berkeley October 13, 2018 What s new for recent years? 2016-2017: Robust

131: Public Economics Taxes on Capital and Savings

131: Public Economics Taxes on Capital and Savings Emmanuel Saez Berkeley 1 MOTIVATION 1) Capital income is about 25% of national income (labor income is 75%) but distribution of capital income is much

131: Public Economics Taxes on Capital and Savings Emmanuel Saez Berkeley 1 MOTIVATION 1) Capital income is about 25% of national income (labor income is 75%) but distribution of capital income is much

Wealth Taxation and Wealth Inequality: Evidence from Denmark,

Wealth Taxation and Wealth Inequality: Evidence from Denmark, 1980-2014 Katrine Jakobsen (University of Copenhagen) Kristian Jakobsen (Kraka) Henrik Kleven (London School of Economics) Gabriel Zucman (UC

Wealth Taxation and Wealth Inequality: Evidence from Denmark, 1980-2014 Katrine Jakobsen (University of Copenhagen) Kristian Jakobsen (Kraka) Henrik Kleven (London School of Economics) Gabriel Zucman (UC

Taxation of labor income

Lund University Department of Economics NEKH01 Tutor: Alessandro Martinello Taxation of labor income A choice between efficiency and inequality? Ane Margrete Tømmerås Abstract This thesis applies a model

Lund University Department of Economics NEKH01 Tutor: Alessandro Martinello Taxation of labor income A choice between efficiency and inequality? Ane Margrete Tømmerås Abstract This thesis applies a model

Class 13 Question 2 Estimating Taxable Income Responses Using Danish Tax Reforms Kleven and Schultz (2014)

") Class 13 Question 2 Estimating Taxable Income Responses Using Danish Tax Reforms Kleven and Schultz (2014) Outline: 1) Background Information 2) Advantages of Danish Data 3) Empirical Strategy 4) Key Findings

Class 13 Question 2 Estimating Taxable Income Responses Using Danish Tax Reforms Kleven and Schultz (2014) Outline: 1) Background Information 2) Advantages of Danish Data 3) Empirical Strategy 4) Key Findings

TOP INCOMES IN THE UNITED STATES AND CANADA OVER THE TWENTIETH CENTURY

TOP INCOMES IN THE UNITED STATES AND CANADA OVER THE TWENTIETH CENTURY Emmanuel Saez University of California, Berkeley Abstract This paper presents top income shares series for the United States and Canada

TOP INCOMES IN THE UNITED STATES AND CANADA OVER THE TWENTIETH CENTURY Emmanuel Saez University of California, Berkeley Abstract This paper presents top income shares series for the United States and Canada

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 REMINDER: Two General Rules for Government Intervention

Introduction to Taxes and Transfers: Income Distribution, Poverty, Taxes and Transfers 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 REMINDER: Two General Rules for Government Intervention

The Distribution of US Wealth, Capital Income and Returns since Emmanuel Saez (UC Berkeley) Gabriel Zucman (LSE and UC Berkeley)

Gabriel Zucman (LSE and UC Berkeley)") The Distribution of US Wealth, Capital Income and Returns since 1913 Emmanuel Saez (UC Berkeley) Gabriel Zucman (LSE and UC Berkeley) March 2014 Is rising inequality purely a labor income phenomenon? Income

The Distribution of US Wealth, Capital Income and Returns since 1913 Emmanuel Saez (UC Berkeley) Gabriel Zucman (LSE and UC Berkeley) March 2014 Is rising inequality purely a labor income phenomenon? Income

High incomes and personal taxation in Colombia

High incomes and personal taxation in Colombia 1993-2010 Facundo Alvaredo Nuffield College/EMod, Conicet & Paris School of Economics & Juliana Londoño Vélez UC Berkeley Commitment to Equity Conference

High incomes and personal taxation in Colombia 1993-2010 Facundo Alvaredo Nuffield College/EMod, Conicet & Paris School of Economics & Juliana Londoño Vélez UC Berkeley Commitment to Equity Conference

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates)

") Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates) Emmanuel Saez March 2, 2012 What s new for recent years? Great Recession 2007-2009 During the

Striking it Richer: The Evolution of Top Incomes in the United States (Updated with 2009 and 2010 estimates) Emmanuel Saez March 2, 2012 What s new for recent years? Great Recession 2007-2009 During the

Corporate Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 24 24.1 What Are Corporations and Why Do We Tax Them? 24.2 The Structure of the Corporate Tax 24.3 The

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 24 24.1 What Are Corporations and Why Do We Tax Them? 24.2 The Structure of the Corporate Tax 24.3 The

Income Inequality in France, : Evidence from Distributional National Accounts (DINA)

") Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest, and

Income Inequality in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest, and

Labour Supply, Taxes and Benefits

Labour Supply, Taxes and Benefits William Elming Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic

Labour Supply, Taxes and Benefits William Elming Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic

Lecture 4: Optimal Labor Income Taxation

78 Lecture 4: Optimal Labor Income Taxation Stefanie Stantcheva Fall 2017 78 TAXATION AND REDISTRIBUTION Key question: Should government reduce inequality using taxes and transfers? 1) Governments use

78 Lecture 4: Optimal Labor Income Taxation Stefanie Stantcheva Fall 2017 78 TAXATION AND REDISTRIBUTION Key question: Should government reduce inequality using taxes and transfers? 1) Governments use

TAX EXPENDITURES Fall 2012

TAX EXPENDITURES 14.471 - Fall 2012 1 Base-Broadening Strategies for Tax Reform: Eliminate Existing Deductions Retain but Scale Back Existing Deductions o Income-Related Clawbacks o Cap on Rate for Deductions

TAX EXPENDITURES 14.471 - Fall 2012 1 Base-Broadening Strategies for Tax Reform: Eliminate Existing Deductions Retain but Scale Back Existing Deductions o Income-Related Clawbacks o Cap on Rate for Deductions

Antoine Bozio. Master APE and PPD Paris October Paris School of Economics (PSE) École des hautes études en sciences sociales (EHESS)

École des hautes études en sciences sociales (EHESS)") Top Lecture 7: Labour Paris School of Economics (PSE) École des hautes études en sciences sociales (EHESS) Master APE and PPD Paris October 2017 1 / 141 Top Outline of the lecture 6 I. Labour : institutions

Top Lecture 7: Labour Paris School of Economics (PSE) École des hautes études en sciences sociales (EHESS) Master APE and PPD Paris October 2017 1 / 141 Top Outline of the lecture 6 I. Labour : institutions

Inequality Dynamics in France, : Evidence from Distributional National Accounts (DINA)

") Inequality Dynamics in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest,

Inequality Dynamics in France, 1900-2014: Evidence from Distributional National Accounts (DINA) Bertrand Garbinti 1, Jonathan Goupille-Lebret 2 and Thomas Piketty 2 1 Paris School of Economics, Crest,

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income Hilary Hoynes, UC Berkeley Ankur Patel US Treasury April 2015 Overview The U.S. social safety net for

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income Hilary Hoynes, UC Berkeley Ankur Patel US Treasury April 2015 Overview The U.S. social safety net for

Labour Supply and Taxes

Labour Supply and Taxes Barra Roantree Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic how should

Labour Supply and Taxes Barra Roantree Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic how should

Rethinking Wealth Taxation

Rethinking Wealth Taxation Thomas Piketty (Paris School of Economics Gabriel Zucman (London School of Economics) November 2014 This talk: two points Wealth is becoming increasingly important relative to

Rethinking Wealth Taxation Thomas Piketty (Paris School of Economics Gabriel Zucman (London School of Economics) November 2014 This talk: two points Wealth is becoming increasingly important relative to

Optimal Labor Income Taxation (follows loosely Chapters of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

131 Undergraduate Public Economics Emmanuel Saez UC Berkeley") Optimal Labor Income Taxation (follows loosely Chapters 20-21 of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Should government reduce

Optimal Labor Income Taxation (follows loosely Chapters 20-21 of Gruber) 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Should government reduce

Corporate Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 Basic Definitions Corporation is a for-profit business owned by shareholders with limited liability (if business goes bankrupt,

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 Basic Definitions Corporation is a for-profit business owned by shareholders with limited liability (if business goes bankrupt,

Fiscal Fact. Reversal of the Trend: Income Inequality Now Lower than It Was under Clinton. Introduction. By William McBride

Fiscal Fact January 30, 2012 No. 289 Reversal of the Trend: Income Inequality Now Lower than It Was under Clinton By William McBride Introduction Numerous academic studies have shown that income inequality

Fiscal Fact January 30, 2012 No. 289 Reversal of the Trend: Income Inequality Now Lower than It Was under Clinton By William McBride Introduction Numerous academic studies have shown that income inequality

Graduate Public Finance

Graduate Public Finance Measuring Income and Wealth Inequality Owen Zidar Princeton Fall 2018 Lecture 12 Thanks to Thomas Piketty, Emmanuel Saez, Gabriel Zucman, and Eric Zwick for sharing notes/slides,

Graduate Public Finance Measuring Income and Wealth Inequality Owen Zidar Princeton Fall 2018 Lecture 12 Thanks to Thomas Piketty, Emmanuel Saez, Gabriel Zucman, and Eric Zwick for sharing notes/slides,

Economic Policy Analysis: Lecture 4

Economic Policy Analysis: Lecture 4 Local Public Finance Camille Landais Stanford University February 10, 2010 Outline Background The Tiebout Conjecture Optimal Federalism Figure 1: Local vs Federal Spending

Economic Policy Analysis: Lecture 4 Local Public Finance Camille Landais Stanford University February 10, 2010 Outline Background The Tiebout Conjecture Optimal Federalism Figure 1: Local vs Federal Spending

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley ozidar@econ.berkeley.edu October 1, 2012 Owen Zidar (UC Berkeley) Tax

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley ozidar@econ.berkeley.edu October 1, 2012 Owen Zidar (UC Berkeley) Tax

Earnings Inequality and Taxes on the Rich

Earnings Inequality and Taxes on the Rich Dr. Fabian Kindermann * Institute for Macroeconomics and Econometrics University of Bonn Background on taxation and inequality in the US Income tax policy in the

Earnings Inequality and Taxes on the Rich Dr. Fabian Kindermann * Institute for Macroeconomics and Econometrics University of Bonn Background on taxation and inequality in the US Income tax policy in the

Distributional National Accounts DINA

Distributional National Accounts DINA Facundo Alvaredo Anthony B. Atkinson Thomas Piketty Emmanuel Saez Gabriel Zucman Meeting of Providers of OECD IDD Data OECD, Paris, February 18-19, 2016 Envision a

Distributional National Accounts DINA Facundo Alvaredo Anthony B. Atkinson Thomas Piketty Emmanuel Saez Gabriel Zucman Meeting of Providers of OECD IDD Data OECD, Paris, February 18-19, 2016 Envision a

FRBSF Joint Board of Directors Meeting Economic Research Seminar Session April 11, U.S. Income Inequality in Perspective

FRBSF Joint Board of Directors Meeting Economic Research Seminar Session April 11, 2012 U.S. Income Inequality in Perspective The Evolution of Top Incomes in the United States Bradley Heim School of Public

FRBSF Joint Board of Directors Meeting Economic Research Seminar Session April 11, 2012 U.S. Income Inequality in Perspective The Evolution of Top Incomes in the United States Bradley Heim School of Public

Working paper series. Simplified Distributional National Accounts. Thomas Piketty Emmanuel Saez Gabriel Zucman. January 2019

Washington Center Equitable Growth 1500 K Street NW, Suite 850 Washington, DC 20005 for Working paper series Simplified Distributional National Accounts Thomas Piketty Emmanuel Saez Gabriel Zucman January

Washington Center Equitable Growth 1500 K Street NW, Suite 850 Washington, DC 20005 for Working paper series Simplified Distributional National Accounts Thomas Piketty Emmanuel Saez Gabriel Zucman January

Why do we tax at all? It may first help to take a step back and think about why taxes exist and what it means to design and reform a tax system.

December, 2017 siepr.stanford.edu Policy Brief Tax Reform: An Optimal Equation By Stefanie Stantcheva Tax reform is poised for passage in Washington, D.C., at a time of high and increasing inequality between

December, 2017 siepr.stanford.edu Policy Brief Tax Reform: An Optimal Equation By Stefanie Stantcheva Tax reform is poised for passage in Washington, D.C., at a time of high and increasing inequality between

Taxation of Earnings and the Impact on Labor Supply and Human Capital. Discussion by Henrik Kleven (LSE)

") Taxation of Earnings and the Impact on Labor Supply and Human Capital Discussion by Henrik Kleven (LSE) The Empirical Foundations of Supply Side Economics The Becker Friedman Institute, September 2013

Taxation of Earnings and the Impact on Labor Supply and Human Capital Discussion by Henrik Kleven (LSE) The Empirical Foundations of Supply Side Economics The Becker Friedman Institute, September 2013

Online Appendix for Taxation and the International Mobility of Inventors

Online Appendix for Taxation and the International Mobility of Inventors Ufuk Akcigit, University of Chicago and NBER Salomé Baslandze, EIEF Stefanie Stantcheva, Harvard and NBER May 2016 A Data Construction

Online Appendix for Taxation and the International Mobility of Inventors Ufuk Akcigit, University of Chicago and NBER Salomé Baslandze, EIEF Stefanie Stantcheva, Harvard and NBER May 2016 A Data Construction

NBER WORKING PAPER SERIES TAXATION AND INTERNATIONAL MIGRATION OF SUPERSTARS: EVIDENCE FROM THE EUROPEAN FOOTBALL MARKET

NBER WORKING PAPER SERIES TAXATION AND INTERNATIONAL MIGRATION OF SUPERSTARS: EVIDENCE FROM THE EUROPEAN FOOTBALL MARKET Henrik Kleven Camille Landais Emmanuel Saez Working Paper 16545 http://www.nber.org/papers/w16545

NBER WORKING PAPER SERIES TAXATION AND INTERNATIONAL MIGRATION OF SUPERSTARS: EVIDENCE FROM THE EUROPEAN FOOTBALL MARKET Henrik Kleven Camille Landais Emmanuel Saez Working Paper 16545 http://www.nber.org/papers/w16545

The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review

The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review Emmanuel Saez, University of California Berkeley and NBER Joel Slemrod, University of Michigan and NBER Seth H. Giertz,

The Elasticity of Taxable Income with Respect to Marginal Tax Rates: A Critical Review Emmanuel Saez, University of California Berkeley and NBER Joel Slemrod, University of Michigan and NBER Seth H. Giertz,

Results are preliminary. Comments welcome.

Estimating high-income tax elasticities using sub-national variation in tax rates Kevin Milligan Vancouver School of Economics University of British Columbia Michael Smart Department of Economics University

Estimating high-income tax elasticities using sub-national variation in tax rates Kevin Milligan Vancouver School of Economics University of British Columbia Michael Smart Department of Economics University

Finance, an Inequality Factor

Finance, an Inequality Factor Olivier GODECHOT This study shows that, contrary to preconceptions, CEOs and stars of the sport and entertainment industry are not the first ones to blame for rising inequalities.

Finance, an Inequality Factor Olivier GODECHOT This study shows that, contrary to preconceptions, CEOs and stars of the sport and entertainment industry are not the first ones to blame for rising inequalities.

Provincial Taxation of High Incomes: What are the Impacts on Equity and Tax Revenue?

Provincial Taxation of High Incomes: What are the Impacts on Equity and Tax Revenue? Kevin Milligan Vancouver School of Economics University of British Columbia Michael Smart Department of Economics University

Provincial Taxation of High Incomes: What are the Impacts on Equity and Tax Revenue? Kevin Milligan Vancouver School of Economics University of British Columbia Michael Smart Department of Economics University

Income inequality has been widening in

Taxing the 1 Percent Raising taxes on top earners is often seen as a straightforward way to stem inequality. The trick is preserving efficient revenue generation and work incentives for the economy s most

Taxing the 1 Percent Raising taxes on top earners is often seen as a straightforward way to stem inequality. The trick is preserving efficient revenue generation and work incentives for the economy s most

Response by Thomas Piketty and Emmanuel Saez to: The Top 1%... of What? By ALAN REYNOLDS

Response by Thomas Piketty and Emmanuel Saez to: The Top 1%... of What? By ALAN REYNOLDS In his December 14 article, The Top 1% of What?, Alan Reynolds casts doubts on the interpretation of our results

Response by Thomas Piketty and Emmanuel Saez to: The Top 1%... of What? By ALAN REYNOLDS In his December 14 article, The Top 1% of What?, Alan Reynolds casts doubts on the interpretation of our results

WID.world/TECHNICAL/NOTE/SERIES/N /2015/7/

! WID.world/TECHNICAL/NOTE/SERIES/N /2015/7/! Frank&Sommeiller&Price/Series/for/Top/Income/Shares/ by/us/states/since/1917/ / / MarkFrank,EstelleSommeiller, MarkPriceandEmmanuelSaez July2015/ The World

! WID.world/TECHNICAL/NOTE/SERIES/N /2015/7/! Frank&Sommeiller&Price/Series/for/Top/Income/Shares/ by/us/states/since/1917/ / / MarkFrank,EstelleSommeiller, MarkPriceandEmmanuelSaez July2015/ The World

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

Lectures 9 and 10: Optimal Income Taxes and Transfers

Lectures 9 and 10: Optimal Income Taxes and Transfers Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 36 Agenda 1 Redistribution vs. Effi ciency 2 The Mirrlees optimal nonlinear

Lectures 9 and 10: Optimal Income Taxes and Transfers Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 36 Agenda 1 Redistribution vs. Effi ciency 2 The Mirrlees optimal nonlinear

NBER WORKING PAPER SERIES MIGRATION AND WAGE EFFECTS OF TAXING TOP EARNERS: EVIDENCE FROM THE FOREIGNERS' TAX SCHEME IN DENMARK

NBER WORKING PAPER SERIES MIGRATION AND WAGE EFFECTS OF TAXING TOP EARNERS: EVIDENCE FROM THE FOREIGNERS' TAX SCHEME IN DENMARK Henrik Jacobsen Kleven Camille Landais Emmanuel Saez Esben Anton Schultz

NBER WORKING PAPER SERIES MIGRATION AND WAGE EFFECTS OF TAXING TOP EARNERS: EVIDENCE FROM THE FOREIGNERS' TAX SCHEME IN DENMARK Henrik Jacobsen Kleven Camille Landais Emmanuel Saez Esben Anton Schultz

Over the last 40 years, the U.S. federal tax system has undergone three

Journal of Economic Perspectives Volume 21, Number 1 Winter 2006 Pages 000 000 How Progressive is the U.S. Federal Tax System? A Historical and International Perspective Thomas Piketty and Emmanuel Saez

Journal of Economic Perspectives Volume 21, Number 1 Winter 2006 Pages 000 000 How Progressive is the U.S. Federal Tax System? A Historical and International Perspective Thomas Piketty and Emmanuel Saez

Econ 230B Spring FINAL EXAM: Solutions

Econ 230B Spring 2017 FINAL EXAM: Solutions The average grade for the final exam is 45.82 (out of 60 points). The average grade including all assignments is 79.38. The distribution of course grades is:

Econ 230B Spring 2017 FINAL EXAM: Solutions The average grade for the final exam is 45.82 (out of 60 points). The average grade including all assignments is 79.38. The distribution of course grades is:

ECON 361: Income Distributions and Problems of Inequality

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 9, 2017 1/35 Last class... Top income share in Canada- Veall (2012( Income inequality in the U.S. - Piketty

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 9, 2017 1/35 Last class... Top income share in Canada- Veall (2012( Income inequality in the U.S. - Piketty

Real Median Family Income is Falling. Family incomes have stagnated since the mid-1980s. Income in 2012 ($51,017) is lower than in 1989 ($51,681).

is lower than in 1989 ($51,681).") U.S. Income 1 Real Median Family Income is Falling Family incomes have stagnated since the mid-1980s. Income in 2012 ($51,017) is lower than in 1989 ($51,681). 2 Labor Income Share Falls As Profits Rise

U.S. Income 1 Real Median Family Income is Falling Family incomes have stagnated since the mid-1980s. Income in 2012 ($51,017) is lower than in 1989 ($51,681). 2 Labor Income Share Falls As Profits Rise

ECON 361: Income Distributions and Problems of Inequality

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 7, 2018 1/1 Last class... Top income share in Canada- Veall (2012) Income inequality in the U.S. - Piketty

ECON 361: Income Distributions and Problems of Inequality David Rosé Queen s University February 7, 2018 1/1 Last class... Top income share in Canada- Veall (2012) Income inequality in the U.S. - Piketty

Voting over Selfishly Optimal Income Tax Schedules with Tax-Driven Migrations

Voting over Selfishly Optimal Income Tax Schedules ith Tax-Driven Migrations Darong Dai Department of Economics Texas A&M University Darong Dai (TAMU) Voting over Income Taxes 11/28/2017 1 / 27 Outline

Voting over Selfishly Optimal Income Tax Schedules ith Tax-Driven Migrations Darong Dai Department of Economics Texas A&M University Darong Dai (TAMU) Voting over Income Taxes 11/28/2017 1 / 27 Outline

Generalized Social Marginal Welfare Weights for Optimal Tax Theory

Generalized Social Marginal Welfare Weights for Optimal Tax Theory Emmanuel Saez, UC Berkeley Stefanie Stantcheva, MIT January 2013 AEA Meetings 1 MOTIVATION Welfarism is the dominant approach in optimal

Generalized Social Marginal Welfare Weights for Optimal Tax Theory Emmanuel Saez, UC Berkeley Stefanie Stantcheva, MIT January 2013 AEA Meetings 1 MOTIVATION Welfarism is the dominant approach in optimal

Tax Simplicity and Heterogeneous Learning

80 Tax Simplicity and Heterogeneous Learning Philippe Aghion (College de France) Ufuk Akcigit (Chicago) Matthieu Lequien (Banque de France) Stefanie Stantcheva (Harvard) 80 Motivation: The Value of Tax

80 Tax Simplicity and Heterogeneous Learning Philippe Aghion (College de France) Ufuk Akcigit (Chicago) Matthieu Lequien (Banque de France) Stefanie Stantcheva (Harvard) 80 Motivation: The Value of Tax

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics

Henrik Jacobsen Kleven London School of Economics") LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

Income and Wealth Concentration in Switzerland over the 20 th Century

September 2003 Income and Wealth Concentration in Switzerland over the 20 th Century Fabien Dell, INSEE Thomas Piketty, EHESS Emmanuel Saez, UC Berkeley and NBER Abstract: This paper presents homogeneous

September 2003 Income and Wealth Concentration in Switzerland over the 20 th Century Fabien Dell, INSEE Thomas Piketty, EHESS Emmanuel Saez, UC Berkeley and NBER Abstract: This paper presents homogeneous

Discussion Paper Series

Discussion Paper Series IZA DP No. 10667 Trends and Gradients in Top Tax Elasticities: Cross-Country Evidence, 1900 2014 Enrico Rubolino Daniel Waldenström march 2017 Discussion Paper Series IZA DP No.

Discussion Paper Series IZA DP No. 10667 Trends and Gradients in Top Tax Elasticities: Cross-Country Evidence, 1900 2014 Enrico Rubolino Daniel Waldenström march 2017 Discussion Paper Series IZA DP No.

Economics 230a, Fall 2014 Lecture Note 12: Introduction to International Taxation

Economics 230a, Fall 2014 Lecture Note 12: Introduction to International Taxation It is useful to begin a discussion of international taxation with a look at the evolution of corporate tax rates over the

Economics 230a, Fall 2014 Lecture Note 12: Introduction to International Taxation It is useful to begin a discussion of international taxation with a look at the evolution of corporate tax rates over the

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Taxation and Migration: Evidence and Policy Implications

Taxation and Migration: Evidence and Policy Implications Henrik Kleven, Princeton University and NBER Camille Landais, London School of Economics Mathilde Muñoz, Paris School of Economics Stefanie Stantcheva,

Taxation and Migration: Evidence and Policy Implications Henrik Kleven, Princeton University and NBER Camille Landais, London School of Economics Mathilde Muñoz, Paris School of Economics Stefanie Stantcheva,

Tax Reforms and Intertemporal Shifting of Wage Income: Evidence from Danish Monthly Payroll Records

Tax Reforms and Intertemporal Shifting of Wage Income: Evidence from Danish Monthly Payroll Records Claus Thustrup Kreiner University of Copenhagen, CESifo and CEPR Søren Leth-Petersen University of Copenhagen

Tax Reforms and Intertemporal Shifting of Wage Income: Evidence from Danish Monthly Payroll Records Claus Thustrup Kreiner University of Copenhagen, CESifo and CEPR Søren Leth-Petersen University of Copenhagen

NBER WORKING PAPER SERIES THE ELASTICITY OF TAXABLE INCOME WITH RESPECT TO MARGINAL TAX RATES: A CRITICAL REVIEW

NBER WORKING PAPER SERIES THE ELASTICITY OF TAXABLE INCOME WITH RESPECT TO MARGINAL TAX RATES: A CRITICAL REVIEW Emmanuel Saez Joel B. Slemrod Seth H. Giertz Working Paper 15012 http://www.nber.org/papers/w15012

NBER WORKING PAPER SERIES THE ELASTICITY OF TAXABLE INCOME WITH RESPECT TO MARGINAL TAX RATES: A CRITICAL REVIEW Emmanuel Saez Joel B. Slemrod Seth H. Giertz Working Paper 15012 http://www.nber.org/papers/w15012

Reflections on capital taxation

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Applying Generalized Pareto Curves to Inequality Analysis

Applying Generalized Pareto Curves to Inequality Analysis By THOMAS BLANCHET, BERTRAND GARBINTI, JONATHAN GOUPILLE-LEBRET AND CLARA MARTÍNEZ- TOLEDANO* *Blanchet: Paris School of Economics, 48 boulevard

Applying Generalized Pareto Curves to Inequality Analysis By THOMAS BLANCHET, BERTRAND GARBINTI, JONATHAN GOUPILLE-LEBRET AND CLARA MARTÍNEZ- TOLEDANO* *Blanchet: Paris School of Economics, 48 boulevard

How Progressive is the U.S. Federal Tax System? A Historical and International Perspective

Revised paper July 2006 How Progressive is the U.S. Federal Tax System? A Historical and International Perspective Thomas Piketty and Emmanuel Saez Abstract (NBER version only): This paper provides estimates

Revised paper July 2006 How Progressive is the U.S. Federal Tax System? A Historical and International Perspective Thomas Piketty and Emmanuel Saez Abstract (NBER version only): This paper provides estimates

Taxation and International Migration of Superstars: Evidence from the European Football Market

Taxation and International Migration of Superstars: Evidence from the European Football Market Henrik Jacobsen Kleven, London School of Economics Camille Landais, Stanford University Emmanuel Saez, UC

Taxation and International Migration of Superstars: Evidence from the European Football Market Henrik Jacobsen Kleven, London School of Economics Camille Landais, Stanford University Emmanuel Saez, UC

Learning Dynamics in Tax Bunching at the Kink: Evidence from Ecuador

Learning Dynamics in Tax Bunching at the Kink: Evidence from Ecuador Albrecht Bohne Jan Sebastian Nimczik University of Mannheim UNU-WIDER Public Economics for Development July 2017 Albrecht Bohne (U Mannheim)

Learning Dynamics in Tax Bunching at the Kink: Evidence from Ecuador Albrecht Bohne Jan Sebastian Nimczik University of Mannheim UNU-WIDER Public Economics for Development July 2017 Albrecht Bohne (U Mannheim)

Theoretical Tools of Public Finance. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Theoretical Tools of Public Finance 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 THEORETICAL AND EMPIRICAL TOOLS Theoretical tools: The set of tools designed to understand the mechanics

Theoretical Tools of Public Finance 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 THEORETICAL AND EMPIRICAL TOOLS Theoretical tools: The set of tools designed to understand the mechanics

Recent Development in Income Inequality in Thailand

Recent Development in Income Inequality in Thailand V.Vanitcharearnthum Chulalongkorn Business School vimut@cbs.chula.ac.th September 21, 2015 V.Vanitcharearnthum (CBS) Income Inequality Sep. 21, 2015

Recent Development in Income Inequality in Thailand V.Vanitcharearnthum Chulalongkorn Business School vimut@cbs.chula.ac.th September 21, 2015 V.Vanitcharearnthum (CBS) Income Inequality Sep. 21, 2015

Taxation and Development from the WIDER Perspective

Taxation and Development from the WIDER Perspective Jukka Pirttilä (UNU-WIDER) UNU-WIDER 30th Anniversary Conference 1 / 29 Outline Introduction Modern public economics approach to tax analysis Taxes in

Taxation and Development from the WIDER Perspective Jukka Pirttilä (UNU-WIDER) UNU-WIDER 30th Anniversary Conference 1 / 29 Outline Introduction Modern public economics approach to tax analysis Taxes in

DISCUSSION PAPER SERIES. No OPTIMAL TAXATION OF TOP LABOR INCOMES: A TALE OF THREE ELASTICITIES

DISCUSSION PAPER SERIES No. 8675 OPTIMAL TAXATION OF TOP LABOR INCOMES: A TALE OF THREE ELASTICITIES Thomas Piketty, Emmanuel Saez and Stefanie Stantcheva PUBLIC POLICY ABCD www.cepr.org Available online

DISCUSSION PAPER SERIES No. 8675 OPTIMAL TAXATION OF TOP LABOR INCOMES: A TALE OF THREE ELASTICITIES Thomas Piketty, Emmanuel Saez and Stefanie Stantcheva PUBLIC POLICY ABCD www.cepr.org Available online

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings Raj Chetty, Harvard and NBER John N. Friedman, Harvard and NBER Emmanuel Saez, UC Berkeley and NBER April

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings Raj Chetty, Harvard and NBER John N. Friedman, Harvard and NBER Emmanuel Saez, UC Berkeley and NBER April

Taxation and the International Mobility of Inventors

44 Taxation and the International Mobility of Inventors Ufuk Akcigit Salome Baslandze Stefanie Stantcheva Chicago Einaudi Harvard May 20, 2016 Alexander G. Bell Alexander G. Bell Inventor of the telephone

44 Taxation and the International Mobility of Inventors Ufuk Akcigit Salome Baslandze Stefanie Stantcheva Chicago Einaudi Harvard May 20, 2016 Alexander G. Bell Alexander G. Bell Inventor of the telephone

Lecture 4: Income Taxes Over Time & Across Countries

Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2014-2015 Lecture 4: Income Taxes Over Time & Across Countries (January 27 th 2015)

Public Economics: Tax & Transfer Policies (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2014-2015 Lecture 4: Income Taxes Over Time & Across Countries (January 27 th 2015)

Optimal Labor Income Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Optimal Labor Income Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Do/should government reduce inequality using taxes and transfers?

Optimal Labor Income Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 TAXATION AND REDISTRIBUTION Key question: Do/should government reduce inequality using taxes and transfers?

Econ 133 Global Inequality and Growth. What is Income? Gabriel Zucman

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign income 2. Income = labor income + capital income 3. Functional vs. personal

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign income 2. Income = labor income + capital income 3. Functional vs. personal

What can we learn about household consumption expenditure from data on income and assets?

What can we learn about household consumption expenditure from data on income and assets? Preliminary and incomplete version Lasse Eika Magne Mogstad Ola Vestad Statistics Norway U Chicago U Chicago NBER

What can we learn about household consumption expenditure from data on income and assets? Preliminary and incomplete version Lasse Eika Magne Mogstad Ola Vestad Statistics Norway U Chicago U Chicago NBER

Graduate Public Finance

Graduate Public Finance Taxing Top Earners Owen Zidar Princeton Fall 2017 Lecture 5 Thanks to Emmanuel Saez and David Card for sharing his slides/notes, many of which are reproduced here. Stephanie Kestelman

Graduate Public Finance Taxing Top Earners Owen Zidar Princeton Fall 2017 Lecture 5 Thanks to Emmanuel Saez and David Card for sharing his slides/notes, many of which are reproduced here. Stephanie Kestelman

NBER WORKING PAPER SERIES DOES TAX POLICY AFFECT EXECUTIVE COMPENSATION? EVIDENCE FROM POSTWAR TAX REFORMS. Carola Frydman Raven S.

NBER WORKING PAPER SERIES DOES TAX POLICY AFFECT EXECUTIVE COMPENSATION? EVIDENCE FROM POSTWAR TAX REFORMS Carola Frydman Raven S. Molloy Working Paper 16812 http://www.nber.org/papers/w16812 NATIONAL

NBER WORKING PAPER SERIES DOES TAX POLICY AFFECT EXECUTIVE COMPENSATION? EVIDENCE FROM POSTWAR TAX REFORMS Carola Frydman Raven S. Molloy Working Paper 16812 http://www.nber.org/papers/w16812 NATIONAL

State and Local Government Expenditures. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

State and Local Government Expenditures 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 FISCAL FEDERALISM optimal fiscal federalism: The question of which activities should take place at

State and Local Government Expenditures 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 FISCAL FEDERALISM optimal fiscal federalism: The question of which activities should take place at

TAXES, TRANSFERS, AND LABOR SUPPLY. Henrik Jacobsen Kleven London School of Economics. Lecture Notes for PhD Public Finance (EC426): Lent Term 2012

: Lent Term 2012") TAXES, TRANSFERS, AND LABOR SUPPLY Henrik Jacobsen Kleven London School of Economics Lecture Notes for PhD Public Finance (EC426): Lent Term 2012 AGENDA Why care about labor supply responses to taxes and

TAXES, TRANSFERS, AND LABOR SUPPLY Henrik Jacobsen Kleven London School of Economics Lecture Notes for PhD Public Finance (EC426): Lent Term 2012 AGENDA Why care about labor supply responses to taxes and

Karin Mayr Office room number 5.310, Oskar-Morgenstern-Platz 1 (OMP), 5th floor. Office hours: by appointment.

, 5th floor. Office hours: by appointment.") 040032 UK PUBLIC SPENDING AND TAXATION (MA) Summer Term 2014, 8 ECTS, in English. Lecturer Karin Mayr (karin.mayr@univie.ac.at). Office room number 5.310, Oskar-Morgenstern-Platz 1 (OMP), 5th floor. Office

040032 UK PUBLIC SPENDING AND TAXATION (MA) Summer Term 2014, 8 ECTS, in English. Lecturer Karin Mayr (karin.mayr@univie.ac.at). Office room number 5.310, Oskar-Morgenstern-Platz 1 (OMP), 5th floor. Office

131: Public Economics Taxes on Capital and Savings

131: Public Economics Taxes on Capital and Savings Emmanuel Saez Berkeley 1 MOTIVATION 1) Capital income is about 25-30% of national income (labor income is 70-75%) but distribution of capital income is

131: Public Economics Taxes on Capital and Savings Emmanuel Saez Berkeley 1 MOTIVATION 1) Capital income is about 25-30% of national income (labor income is 70-75%) but distribution of capital income is