Tax Issues Associated with Reporting Fellowships

|

|

|

- Myron Curtis

- 6 years ago

- Views:

Transcription

1 Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst February 16,

2 Scope This presentation applies to UC postdoctoral fellows and paid directs, and graduate students There is tuition associated with graduate students Assumption is that there are no services being performed by the Fellows and Paid Directs or graduate students This is not intended to provide tax advice; it is informational only and points to published resources such as the IRS and Franchise Tax Board. Please consult your personal tax advisor for more information 2

3 The Life Lessons of Tax Returns Through the Works of Homer Forgetting a Deadline Consequences What are the life lessons? 3

4 Tax Filing Question What is the deadline for filing your 2016 Income Tax Return? April 18, 2017 (15 th is Saturday and 17 th is Emancipation Day in D.C.) Usually April 15 4

5 National Research Service Award (NRSA) How does the IRS treat NRSA grants and fellowship grants "modeled" on the NRSA program? These are bona fide "fellowships" and not compensation for services rendered. Therefore, these are not wage income subject to OASDI and Medicare. However, these are still taxable income you need to report on your tax return because they are nonqualified fellowship, as explained in later slides. 5

6 Fellowship Grants Not Modeled on the NRSA Program But what about fellowship grants not modeled on the NRSA program? Non-NRSA grant programs may be classified as either fellowship or compensation, based on the facts and circumstances of the particular program * A requirement that a recipient furnish periodic reports to the grantor for the purpose of keeping the grantor informed with respect to the general progress of the individual, however, is not considered the performance of services. 6

7 Fellowship Grants Not Modeled on the NRSA Program A grant represents compensation for services if either of the following apply: There is a requirement for past, present, or future teaching, research, or other employment services by the recipient; or The grant payment enables the recipient to "pursue studies or research primarily for the benefit of the grantor. Therefore, the compensation received by the recipients- are the recipients gross income, and must be reported as gross taxable income on the recipients income tax returns. 7

8 Example Fellowship vs. Compensation Determination (see checklist) 8

9 **EXHIBIT G Fellowship vs. Compensation Determination Campus: Date: Program or Type of Award: PI: Dept 1. Does the focus of the program relate primarily to (a) the performance of research services for the University, or (b) the development of the research fellow s training skills? 2. Does the research fellow serve as a replacement or substitute for an employee, such as a medical resident or laboratory technician? 3. Do the activities of the research fellow during his/her training program materially benefit the University? 4. Are the research fellow s projects determined by the research fellow in conjunction with his/her training supervisor and/or faculty mentor? 5. Is the research fellow required to perform past or future services for the University as a condition to receiving the research fellowship grant? 6. Are the research activities conducted by the research fellow substantially the same as those research activities conducted by NIH National Research Service Award grantees? 7. Does the research fellow receive substantially the same training and mentoring as a NIH National Fellowship Compensation (b) No No Yes No Yes (a) Yes Yes No Yes No Research Service Award grantee? Yes No If all of the Fellowship boxes are marked, the individual will be treated as a fellowship recipient for federal tax purposes. If all Fellowship boxes are marked, then treated as a Fellowship 9

10 EXHIBIT G (Cont.) Fellowship vs. Compensation Determination If all of the Fellowship boxes were not marked, then please make the fellowship/compensation determination by responding to the following questions: 1. Are the research fellow s projects directly related to the fulfillment of a sponsored research agreement or other University contractual obligation? 2. Is the research fellow required to perform his/her research activities according to certain planned time schedules, e.g., a specified number of hours a day or week and a specified number of weeks during the year? 3. Is the research fellow subject to the same level and type of supervision over the conduct of his/her research activities as a University research assistant employee? 4. Is the research fellow classified as an employee for University payroll tax purposes? No No No No Yes Yes Yes Yes If 4 or more Fellowship boxes are marked, then treated as a Fellowship 5. Does the research fellow receive health and other employee benefits that would be provided to career faculty and staff employees? No Yes 6. Does the research fellow receive any faculty privileges? No Yes If four or more of the Fellowship boxes are marked, the individual will be treated as a fellowship recipient for federal tax purposes. If fewer than four Fellowship boxes are marked, please submit this checklist to [insert name of applicable office] who will make the fellowship/compensation determination. 10

11 Examples of Fellowships Fellowship funds paid directly by the University to the Postdoc Fellow Fellowship funds provided by a third party on behalf of the Postdoc Fellow (Paid Directs) Example : Award intended to pay recipient s expenses are paid directly by a third party to UC and credited to a recipient s University account Payment is treated the same for tax purposes as having been paid to the recipient 11

12 Taxable versus Nontaxable Scholarships and Fellowships Scholarships and Fellowships are Nontaxable if they are used for required: tuition and fees required for the enrollment or attendance of the University books, supplies, and equipment required for courses of instruction at the University These Nontaxable Scholarships and Fellowships are referred to as qualified 12

13 FORM 1098-T The Form 1098-T reports qualified tuition and related expenses, scholarships, fellowships, and grants administered by the University without regard for its possible taxability The Form 1098-T is generally only provided to U.S. citizens and resident aliens 13

14 Example of Form 1098-T $25,000 $10,000 X X Adjusted qualified education expenses = $25,000 - $10,000 Adjusted qualified education expenses = $15,000 Report the Adjusted qualified education expenses to reduce your income taxes 14

15 Taxable versus Nontaxable Scholarships and Fellowships Taxable if used to pay for expenses other than required tuition, fees, books, supplies and equipment. These Taxable Scholarships and Fellowships are referred to as nonqualified Example of Taxable Scholarship & Fellowship Payments: Room and Board Travel Health Insurance Premiums Other Living Expenses 15

16 Health Benefits The taxability of health benefits provided by the University to a postdoctoral scholar depends on whether the recipient of the benefits is a Postdoc Employee, or a Postdoc Fellow and/or a Postdoc Paid Direct. 16

17 Health Benefits-Postdoc Fellows and Pay Directs Health benefits provided by the University to Postdoctoral Fellows (TC 3253) and Paid Directs (TC 3254) {i.e., non-employees} and their dependents are subject to U.S. income tax with respect to the premiums that are paid by the University, less any amounts paid by the recipient. (imputed income) Benefits provided to the domestic partner of a Postdoctoral Fellow or Paid Direct also are taxable (for federal purposes) whether or not the domestic partner qualifies as a dependent. State tax treatment may differ. These benefits are not subject to FICA taxes. 17

18 Health Benefits-Postdoc Employees Health benefits provided by the University are not taxable (both U.S. and California income taxes) if they are provided to the following: Postdoc Employees {TC 3252} (includes U.S. citizens, U.S. resident aliens, and nonresident aliens) Dependents of Postdoc Employees The presence of a 3252 appointment of 50% or more along with a 3253 or 3254 will make the benefit treatment not taxable Health benefits provided by the University to the domestic partner of a postdoctoral employee, less any amount paid by the employee, will be taxable income to the postdoctoral employee for federal purposes (unless the domestic partner is a dependent of the postdoc employee) 18

19 Reporting of Nonqualified Scholarship and Fellowship Payments The University is not required to report these payments to the IRS or withhold tax on the payments. Exception: The University does have to report and withhold Nonqualified Scholarship and Fellowship Payments made to nonresident aliens on IRS Form 1042-S Graduate Students, Postdoctoral Fellows and Paid Directs who are U.S. citizens or resident aliens are required to self-report the total annual value of their fellowships, including benefits for themselves and their dependents, when they prepare their U.S. and California income tax returns. 19

20 Income Taxation of Nonqualified Scholarships and Fellowship Grants Federal Income Taxes Who are required to pay? U.S. citizens Resident Aliens Nonresident Aliens (it depends) 20

21 Federal Income Taxes U.S. Citizens and Resident Aliens* Subject to regular graduated income tax rates on income received from all sources. The income received from all sources include income from both within and outside the United States. When reporting on tax return, the student or fellow may claim appropriate marital status and exemptions. * Every non-u.s. citizen who will be receiving a fellowship grant or other type of payment must complete the UC W-8BEN, Certificate of Foreign Status for Federal Tax Withholding form. In most cases, residency status will be determined based on the information provided on this form. The UC W-8BEN is available on the UCOP Financial Accounting web site, located at 21

22 Federal Income Taxes Nonresident Aliens These Nonqualified Scholarships and Fellowships are reported on an IRS Form 1042-S Generally, the University has to withhold 30 percent of Nonqualified Scholarship and Fellowship payments under I.R.C. Section 1441(a). For Nonresident Aliens with an F, J, M, or Q visa, the University has to withhold 14 percent of Nonqualified Scholarship and Fellowship payments under I.R.C. Section 1441(a)-(b). 22

23 Federal Income Taxes Nonresident Aliens Exceptions to Nonresident Alien Withholding Laws: Foreign Source Fellowship Income Tax Treaties that reduce or eliminate U.S. withholding taxes* Grant that is a qualified scholarship or fellowship and not subject to tax withholding * For a list of income tax treaties, please visit the IRS website ( and type in "United States Income Tax Treaties - A to Z" 23

24 Example of Form 1042-S 24

25 Tax Treaty Exemption A Nonqualified Scholarship or Fellowship paid to a nonresident alien (NRA) may be treated as tax exempt for federal tax purposes if the NRA is from a country that has a tax treaty with the United States. If the Nonqualified Scholarship or Fellowship is deemed to be exempt the NRA would need to complete additional forms: PostDoc Employee - Form 8233 (Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual and a Tax Treaty Statement. Nonqualified Scholarship or Non-employee Fellowships Form W- 8BEN (Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding) 25

26 Tax Treaty Exemption IRS Publications 519 and 901 contain information on tax treaties. Contact your campus International Office to obtain access to the GLACIER Nonresident Alien Tax Compliance Software which will determine treaty eligibility and assist with completing the necessary forms. 26

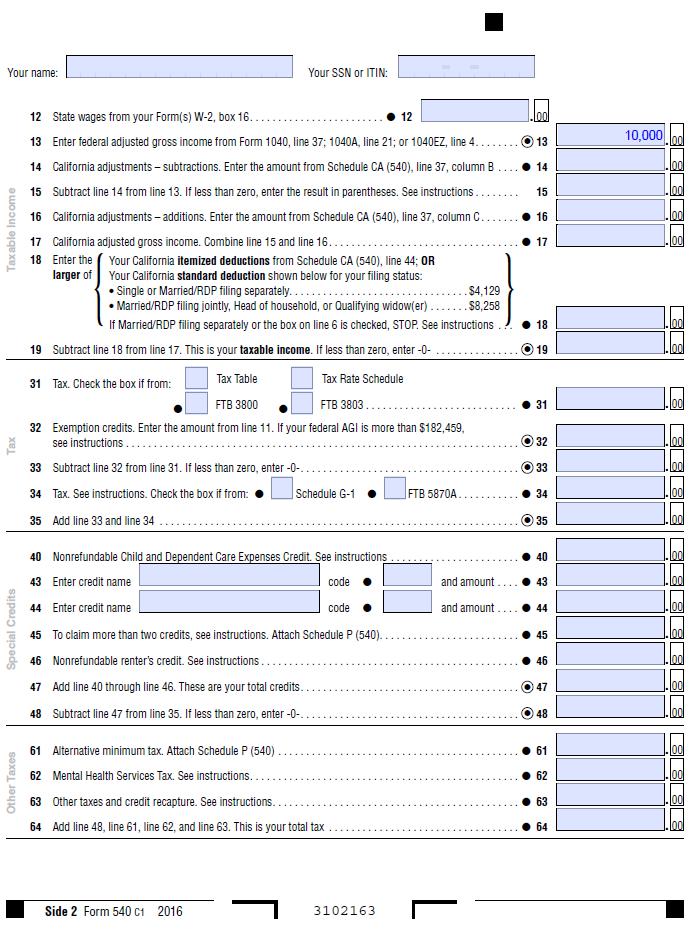

27 Dual Status Aliens If you feel you may be a dual status alien for the tax year, please refer to IRS Publication 519. You may also contact the campus International Office for access to the Glacier Nonresident Alien Tax Software system which will help guide you through the residency determination process. 27

28 How Does the Fellow Report Taxable Fellowships? Federal Income Tax Reporting: U.S. Citizens and U.S. Resident Aliens report their Fellowship Grants and Estimated Tax Payments on IRS Form 1040 (Line 7), Form 1040A (Line 7), or Form 1040EZ (Line 1). Since the Lines for these IRS Forms are only for amounts specified on Form W-2, the instructions indicate to write SCH and the fellowship amount on the following : On the dotted line next to Line 7 of IRS Form 1040 In the space to the left of Line 7 of IRS Form 1040A In the space to the left of Line 1 of IRS Form 1040EZ Nonresident Aliens report their Fellowship Grants on IRS Form 1040NR (Line 12) or Form 1040NR-EZ (Line 5) 28

29 U.S. Citizens and Resident Aliens Nonresident Aliens 29

30 Federal Tax Resources Publication 515: Withholding of Tax on Nonresident Aliens and Foreign Entities Publication 519: U.S. Tax Guide for Aliens Publication 901: U.S. Tax Treaties Publication 970: Tax Benefits for Education IRS Notice 87-31: Taxation of Grants IRS Notice 96-68: Educational Assistance Programs IRS Website: United States Income Tax Treaties - A to Z National Taxpayer Advocate Service: Internal Revenue Service (IRS) Website: Individuals :

31 Federal Tax Resources Federal E-Filing Information: Franchise Tax Board: Other Online Filing Options WT.svl=HEf2 IRS Form Instructions: A 1040EZ 1040NR 1040NR-EZ 1040-ES 31

32 California State Income Taxes Who are required to pay? U.S. citizens Resident Aliens Nonresident Aliens California does not generally conform to Federal tax treaties. Residents of foreign countries who perform services in California or who receive income from California sources are usually subject to State income tax withholding. 32

33 California State Income Taxes Residents of California Generally, a resident of California for income tax purposes is someone who lives in California for more than 9 months in a tax year, files a resident tax return, registered to vote, etc. Please refer to FTB Publication 1031 for guidelines on California residency status Nonresidents of California California does not require reporting or withholding on fellowship grant payments, except for the portion that represents payment for services Fellow should review requirements for self reporting items subject to California income taxes 33

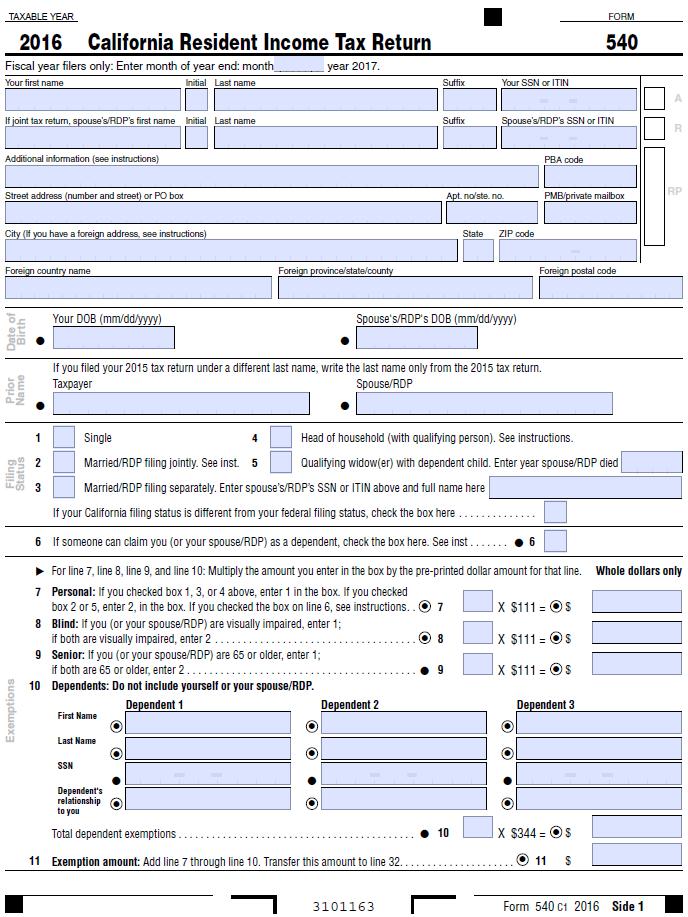

34 How Does the Fellow Report Taxable Fellowships? California State Income Tax Reporting: California Residents report their Federal Adjusted Gross Income on Line 13 of FTB Form 540 California Nonresidents and Part-Year Residents report their Federal Adjusted Gross Income on Line 13 of FTB Form 540NR (Long) or FTB Form 540NR (Short) Caution: If Federal Adjusted Gross Income is more than $100,000, use Form 540NR (Long) 34

35 California Residents 35

36 California Nonresident 36

37 California Tax Resources FTB Publication 1031: Guidelines for Determining Resident Status FTB Publication 1017: Resident and Nonresident Withholding Guidelines Franchise Tax Board (FTB) Website: Individuals : x.shtml?wt.mc_id=global_individuals _Tab 37

38 California Tax Resources FTB s Online Filing Options: allsoftware.shtml?wt.mc_id=hp_ban ner_allsoftware&wt.svl=hef1 FTB Form Instructions: NR (Long) 540NR (Short) 38

39 University Resources UC Website: See Tax forms and information for Employee s Federal-State Withholding Allowance Certificate (UC W-4/DE 4) Taxation of nonresident aliens Glacier Nonresident Alien Tax Preparation Software 39

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Princeton University International Undergraduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 2, 2011

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Webinar Tax Treatment for Scholarships and Fellowships

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

West Chester University. Taxation Issues Nonresident Aliens

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

UCSF Postdoc Scholars. Revised March 20, 2013

UCSF Postdoc Scholars Revised March 20, 2013 Agenda Introduction Hiring Checklist Required Keying Practices Dues/Fees Taxation Financials Appendix: Taxation 2 Hiring Checklist Postdoc Scholars 3 Postdoc

UCSF Postdoc Scholars Revised March 20, 2013 Agenda Introduction Hiring Checklist Required Keying Practices Dues/Fees Taxation Financials Appendix: Taxation 2 Hiring Checklist Postdoc Scholars 3 Postdoc

Princeton University International Graduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 9, 2011

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

SUBJECT: Payments to Nonresident Aliens

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Disbursements: State Tax Withholding from Nonwage Payments to Nonresidents of California

Disbursements: State Tax Withholding from Nonwage Payments to Nonresidents of California Responsible Officer: EVP - Chief Financial Officer Responsible Office: FO - Financial Operations Issuance Date:

Disbursements: State Tax Withholding from Nonwage Payments to Nonresidents of California Responsible Officer: EVP - Chief Financial Officer Responsible Office: FO - Financial Operations Issuance Date:

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS COMMON VISA TYPES AND THEIR TREATMENTS

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

Tax Information for US Resident Students and Scholars. Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP

Tax Information for US Resident Students and Scholars Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP 1 Fellowship Stipends (Not Earned Income) Regarding Students: Fellowship stipends

Tax Information for US Resident Students and Scholars Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP 1 Fellowship Stipends (Not Earned Income) Regarding Students: Fellowship stipends

Postdoctoral Scholar Follow-up Issues Service Request 16976

Postdoctoral Scholar Follow-up Issues Service Request 16976 University of California Financial Management Payroll Coordination September 14, 2005 Postdoctoral Scholar Follow-up Issues Table of Contents

Postdoctoral Scholar Follow-up Issues Service Request 16976 University of California Financial Management Payroll Coordination September 14, 2005 Postdoctoral Scholar Follow-up Issues Table of Contents

Foreign Student and Scholar Volunteer Tax Return Preparation. VITA Training 1

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes. Download Slides here: https://goo.gl/q1tigg

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

International Students and Scholars Nonresident Tax Orientation. February 14, 2018

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6, 2019 1 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6, 2019 1 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

2012 Non-Resident Alien Tax Filings

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

Taxability of Prizes and Awards President s Engagement Prizes. December 9, Office of the Comptroller

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

University of Utah Payments to Non Resident Aliens

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

FOREIGN VISITOR TAX GUIDE

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

Welcome to Tax Filing Information for International Students and Scholars

Welcome to Tax Filing Information for International Students and Scholars Presented by Office of International Student & Scholar Services Florida Institute of Technology DISCLAIMER ISSS staff are not licensed

Welcome to Tax Filing Information for International Students and Scholars Presented by Office of International Student & Scholar Services Florida Institute of Technology DISCLAIMER ISSS staff are not licensed

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room Presented by:

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

OUTDATED. Back to Index. Policy 3-22 Rev. Date: April 30, Subject: STIPENDS AND TAX EXEMPT PAYMENTS PURPOSE

Policy 3-22 Rev. Date: April 30, 1976 Back to Index Subject: STIPENDS AND TAX EXEMPT PAYMENTS I. II. PURPOSE To establish a policy and related procedures for administering stipends for scholarships and

Policy 3-22 Rev. Date: April 30, 1976 Back to Index Subject: STIPENDS AND TAX EXEMPT PAYMENTS I. II. PURPOSE To establish a policy and related procedures for administering stipends for scholarships and

Frequently Asked Tax Questions 2018 Tax Returns

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

MICHIGAN DEPARTMENT OF TREASURY

MICHIGAN DEPARTMENT OF TREASURY 2013 To explain the filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other Michigan

MICHIGAN DEPARTMENT OF TREASURY 2013 To explain the filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other Michigan

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

Basic Tax Information for F and J Immigration Status

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

MICHIGAN DEPARTMENT OF TREASURY

MICHIGAN DEPARTMENT OF TREASURY 2015 To explain Michigan filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other

MICHIGAN DEPARTMENT OF TREASURY 2015 To explain Michigan filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

TAX FILING FOR STUDENTS AND SCHOLARS 101. Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

Prize, Grant, Award or Fellowship Policy Review Session

Prize, Grant, Award or Fellowship Policy Review Session Office of the Controller Karen Kittredge, OC, Manager Policy and Business Process Natasha Rivera, OC, Nonresident Alien Compliance Manager 1 Financial

Prize, Grant, Award or Fellowship Policy Review Session Office of the Controller Karen Kittredge, OC, Manager Policy and Business Process Natasha Rivera, OC, Nonresident Alien Compliance Manager 1 Financial

Non-Resident Alien Fellowship/Scholarship Payments and Taxes Monthly Reporting Process. Service Request 16938

Non-Resident Alien Fellowship/Scholarship Payments and Taxes Monthly Reporting Process Service Request 16938 University of California Office of the President Payroll Coordination and Tax Services Revised

Non-Resident Alien Fellowship/Scholarship Payments and Taxes Monthly Reporting Process Service Request 16938 University of California Office of the President Payroll Coordination and Tax Services Revised

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

CAMP PAYING: INNOVATIVE SOLUTIONS

CAMP IPPS 2016 CAMP PAYING: INNOVATIVE SOLUTIONS Spelunking in the Cave of Tax Topics Presented by Heather Vinograd PC West: Eleanor Roosevelt College Room 2:30 3:15 TAX TOPICS Non-payroll Payments SALES

CAMP IPPS 2016 CAMP PAYING: INNOVATIVE SOLUTIONS Spelunking in the Cave of Tax Topics Presented by Heather Vinograd PC West: Eleanor Roosevelt College Room 2:30 3:15 TAX TOPICS Non-payroll Payments SALES

INTERNATIONAL TAX. Presented by Fiscal Services

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

Tax Reporting for Inbound Students

Tax Reporting for Inbound Students March 10, 2017 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Tax Residence 101 Defined in Internal Revenue Code (IRC) Section 7701(b) - Determined based on

Tax Reporting for Inbound Students March 10, 2017 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Tax Residence 101 Defined in Internal Revenue Code (IRC) Section 7701(b) - Determined based on

International Student Taxes

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

International Student Taxes. Information compiled by International Student Services

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

RUTGERS POLICY. Responsible Executive: Senior Vice President for Finance and Administration

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Business Requirements Document

Business Requirements Document SR101131 - Update Tax Treaty Income Code (EDB1170) and Tax Treaty Income Code Alternate (EDB1171) in PPS with New IRS Values Document Information Document Attributes ID Owner

Business Requirements Document SR101131 - Update Tax Treaty Income Code (EDB1170) and Tax Treaty Income Code Alternate (EDB1171) in PPS with New IRS Values Document Information Document Attributes ID Owner

Nonresident Alien Tax Compliance

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

Vendor Set-Up Process

Vendor Set-Up Process Office of the Controller April 26, 2018 Karen Kittredge, Manager, Policy and Business Process Teri DeLeon, Procure to Pay Manager Sharon Henry-Bell, Accounts Payable Operations Supervisor

Vendor Set-Up Process Office of the Controller April 26, 2018 Karen Kittredge, Manager, Policy and Business Process Teri DeLeon, Procure to Pay Manager Sharon Henry-Bell, Accounts Payable Operations Supervisor

Nonresident Alien Federal Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

Office of International Services TAX WORKSHOP. Tax preparation for International Students and Scholars Tax Year 2018

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

Tax Reporting for Inbound Students

Tax Reporting for Inbound Students March 9, 2018 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Taxation Resident vs. Nonresident Resident - Taxed on worldwide income - Allowed worldwide deductions

Tax Reporting for Inbound Students March 9, 2018 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Taxation Resident vs. Nonresident Resident - Taxed on worldwide income - Allowed worldwide deductions

1 Introduction Work Authorization Taxpayer Identification Numbers... 2

1 Introduction... 1 1.1 Work Authorization... 1 1.2 Taxpayer Identification Numbers... 2 2 U.S. Tax Residency Rules... 3 2.1 Residency Status Based on U.S. Presence... 3 2.2 U.S. Days That Do Not Count...

1 Introduction... 1 1.1 Work Authorization... 1 1.2 Taxpayer Identification Numbers... 2 2 U.S. Tax Residency Rules... 3 2.1 Residency Status Based on U.S. Presence... 3 2.2 U.S. Days That Do Not Count...

Payments to Foreign Nationals. March 9, 2015

Payments to Foreign Nationals March 9, 2015 Workshop Presenters Kelly Sellers University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Payments to Foreign Nationals March 9, 2015 Workshop Presenters Kelly Sellers University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

NOTE: In August 2011, you will receive a pro-rated stipend amount of $2,101.45, as your August start date is 8/4.

August 31, 2011 Dear Combined Degree Students, There is some confusion regarding the years of the program in which you have no taxes withheld from your stipend check, and need to file estimated taxes and

August 31, 2011 Dear Combined Degree Students, There is some confusion regarding the years of the program in which you have no taxes withheld from your stipend check, and need to file estimated taxes and

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures.

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

If you have additional questions on this, please call Payroll & Records Management at 831-

February 2013 Recipients of Graduate Fellowship Awards: The University of Delaware is not required to report to the Federal Government or to withhold taxes on fellowship awards to U.S. citizens and resident

February 2013 Recipients of Graduate Fellowship Awards: The University of Delaware is not required to report to the Federal Government or to withhold taxes on fellowship awards to U.S. citizens and resident

PLEASE PRESS *6 ON YOUR PHONE TO MUTE

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM. Glacier Guide for Departments

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

CSU 101 Tax Discussion Monterey 2011

CSU 101 Tax Discussion Monterey 2011 Marc F. Benadiba Assistant Director Fiscal Services Cal Poly San Luis Obispo CSU Tax Discussion Contrary to popular belief, there are significant tax issues on CSU

CSU 101 Tax Discussion Monterey 2011 Marc F. Benadiba Assistant Director Fiscal Services Cal Poly San Luis Obispo CSU Tax Discussion Contrary to popular belief, there are significant tax issues on CSU

Tax information. International Students in the United States

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

PAYROLL SERVICES Presents: OVERVIEW OF RESIDENCY FOR TAX PURPOSES

PAYROLL SERVICES Presents: OVERVIEW OF RESIDENCY FOR TAX PURPOSES Is Residency for tax purposes a choice? NO We do not get to choose residency for tax purposes 6/11/2009 2 Objectives Understand the rules

PAYROLL SERVICES Presents: OVERVIEW OF RESIDENCY FOR TAX PURPOSES Is Residency for tax purposes a choice? NO We do not get to choose residency for tax purposes 6/11/2009 2 Objectives Understand the rules

INTERNATIONAL STUDENTS TAX WORKSHOP 2018

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

In year 1 you may be supported in one of the following ways:

October 1 st 2015 Dear BGS Students, There is some confusion regarding the years of the program in which you get no taxes withheld from your stipend check, and need to file estimated taxes and the years

October 1 st 2015 Dear BGS Students, There is some confusion regarding the years of the program in which you get no taxes withheld from your stipend check, and need to file estimated taxes and the years

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

THE BOTTOM LINE. Did You Know.

THE BOTTOM LINE Volume 11, Issue 1 Spring 2009 Dear Colleagues, The winter seems to be dragging on and I m definitely ready for some warm weather. The budget process and cycle changed this year. First

THE BOTTOM LINE Volume 11, Issue 1 Spring 2009 Dear Colleagues, The winter seems to be dragging on and I m definitely ready for some warm weather. The budget process and cycle changed this year. First

Independent Contractor Guidelines for Federal Tax Purposes. UC Independent Contractor Guidelines for Federal Tax Purposes

Guidance on Related Policy: N/A Effective Date: 1/17/2018 Independent Contractor Guidelines for Federal Tax Purposes Contact: John Barrett Email: John.Barrett@ucop.edu Phone #: (510) 987-0903 UC Independent

Guidance on Related Policy: N/A Effective Date: 1/17/2018 Independent Contractor Guidelines for Federal Tax Purposes Contact: John Barrett Email: John.Barrett@ucop.edu Phone #: (510) 987-0903 UC Independent

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

Payments to Foreign Nationals. March 11, 2013

Payments to Foreign Nationals March 11, 2013 Workshop Presenters Denise Esworthy University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Payments to Foreign Nationals March 11, 2013 Workshop Presenters Denise Esworthy University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Overview of Taxation for Students

Overview of Taxation for Students Disclaimer This session has been created under the premises of the Volunteer Income Tax Assistance Program (VITA), a program of the Internal Revenue Service. In offering

Overview of Taxation for Students Disclaimer This session has been created under the premises of the Volunteer Income Tax Assistance Program (VITA), a program of the Internal Revenue Service. In offering

Fellowships Toolkit:

Fellowships Toolkit: A Reference Guide to Fellowships, Reimbursements and Other Payments to U.S. Citizens and Non-Resident Aliens Office of the Controller January 1, 2015 Table of Contents INTRODUCTION:

Fellowships Toolkit: A Reference Guide to Fellowships, Reimbursements and Other Payments to U.S. Citizens and Non-Resident Aliens Office of the Controller January 1, 2015 Table of Contents INTRODUCTION:

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

OFFICIAL POLICY. Policy Statement

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

Education, Taxes, & Benefits. Duke University August 22, 2017

Education, Taxes, & Benefits Duke University August 22, 2017 Megan Hutchinson, CPA Senior Manager - Tax Raleigh Office DISCUSSION POINTS TYPES OF INCOME TAXABLE v NON-TAXABLE QUALIFIED v NON-QUALIFIED

Education, Taxes, & Benefits Duke University August 22, 2017 Megan Hutchinson, CPA Senior Manager - Tax Raleigh Office DISCUSSION POINTS TYPES OF INCOME TAXABLE v NON-TAXABLE QUALIFIED v NON-QUALIFIED

Filing your 2015 North Carolina State Income Tax Return. International Employment and Taxation

Filing your 2015 North Carolina State Income Tax Return International Employment and Taxation To Begin You will need your W-2 and 1042-S to complete your North Carolina Tax Return. (Form 1042-S is only

Filing your 2015 North Carolina State Income Tax Return International Employment and Taxation To Begin You will need your W-2 and 1042-S to complete your North Carolina Tax Return. (Form 1042-S is only

CAMP IPPS August 21, 2018

CAMP IPPS 2018 August 21, 2018 WELCOME CAMPERS A few things to remember West Ballroom Stop by the ballroom to ask us questions after the class! Meet Connexxus travel vendors in honor of the Connexxus 10

CAMP IPPS 2018 August 21, 2018 WELCOME CAMPERS A few things to remember West Ballroom Stop by the ballroom to ask us questions after the class! Meet Connexxus travel vendors in honor of the Connexxus 10

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR

Session 2017 Tax Year Georgia Form 500 with Form 1040NR") Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

Business Requirements Document. SR IRS Employer Reporting Requirements under the Affordable Care Act (ACA), Phase I

, Phase I") Business Requirements Document SR100508 IRS Employer Reporting Requirements under the Affordable Care Act (ACA), Phase I 1 Document Information Document Attributes ID Owner Author(s) Contributor(s) Revision

Business Requirements Document SR100508 IRS Employer Reporting Requirements under the Affordable Care Act (ACA), Phase I 1 Document Information Document Attributes ID Owner Author(s) Contributor(s) Revision

Tax Treatment of Incentive Payments

Tax Treatment of Incentive Payments By Brad Caftel bcaftel@insightcced.org August 2001 Through a new program, government and private funders will assist at least 200 low-income families to gain self-sufficiency.

Tax Treatment of Incentive Payments By Brad Caftel bcaftel@insightcced.org August 2001 Through a new program, government and private funders will assist at least 200 low-income families to gain self-sufficiency.

NEW VENDOR REQUEST NEW VENDOR INFORMATION INTERNATIONAL VENDOR REQUEST INDIVIDUAL

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500

Session 2015 Tax Year GA Form 500") Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law