Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes

|

|

|

- Giles Harmon

- 5 years ago

- Views:

Transcription

1 Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6,

2 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler Senior Manager of Tax, VPF Tax and Global Operations Questions and Answers: PwC Carol McNeil, William Fleming and Mark Sampson 2

3 Agenda Residency Status Filing Requirements Reportable Income Tax Forms Tax Treaty Benefits Q&A 3

4 Residency Status Resident for U.S. income tax purposes is determined by 2 tests: 1. Green Card Test 2. Substantial Presence Test Present in the U.S. for at least 183 days in a calendar year (or combination of 31 days in current and 183 total in past 3 years) Scholars exemption from counting days for teachers and trainers on a J or Q visa for 2 calendar years Students exemption from counting days for students on a F, J, M or Q visa for 5 years Note: Prior visa and U.S. visit history must be taken into account Tax residency is separate from immigration residency 4

5 Substantial Presence Student vs. Scholar Student enrolled in an MIT Degree Program; Non-Degree students (Visiting, Special or Exchange) Scholar Post Docs, Lecturers, Visiting Professors, Scientists, Scholars and Engineers, and others that have graduated and are now working at MIT Student 5 year exemption and Scholar 2 year exemption: The exemption allows students and scholars to remain nonresident aliens for this period of years, thus exempt from the substantial presence test Exemption period is by calendar year even if only in U.S. 1 day during a calendar year, it counts towards total years exempt 5

6 Residency Start Date The residency start date is the earlier of the dates determined below: Substantial Presence Test the first day you are present in the U.S. during the calendar year (usually January 1) Green Card Test the date you become a lawful permanent resident Example: A student on a J-1 visa since September calendar years have passed (2013, 2014, 2015, 2016, 2017) that are exempt from substantial presence test. Year 2018 is not exempt. On the 183 day of 2018, the student has met the substantial presence test. Under the substantial presence test the residency start date is the first date the student was in the U.S. Residency start date = January 1,

7 Dual Status Residency In rare circumstances an individual can claim dual-status residency, meaning they were a U.S. tax resident for part of the year, and a nonresident alien for the other part of the year. This is typically only possible when: Entering the U.S later than January 1 during year that substantial presence is met. Since the start date of residency status is the first day of the calendar year a person is present in the U.S., that person can claim to be a non-resident for the days before they enter the U.S. and a resident for the period after. Any individual who becomes a lawful permanent resident during the year may be able to claim to be a nonresident prior to that date. Why claim dual-status? U.S. residents are taxed on worldwide income, nonresidents are only taxed on U.S. sourced income. 7

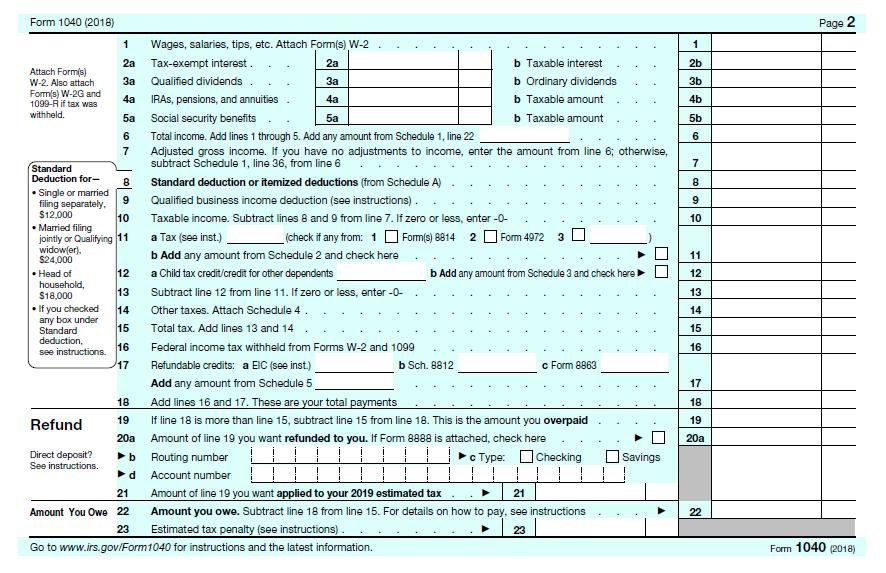

8 Filing Requirements Who is Required to File: IRS Interactive Tax Assistant: Refund withheld taxes if overpaid Claim refundable tax credits (e.g. earned income credit, additional child tax credit, American opportunity credit) 8

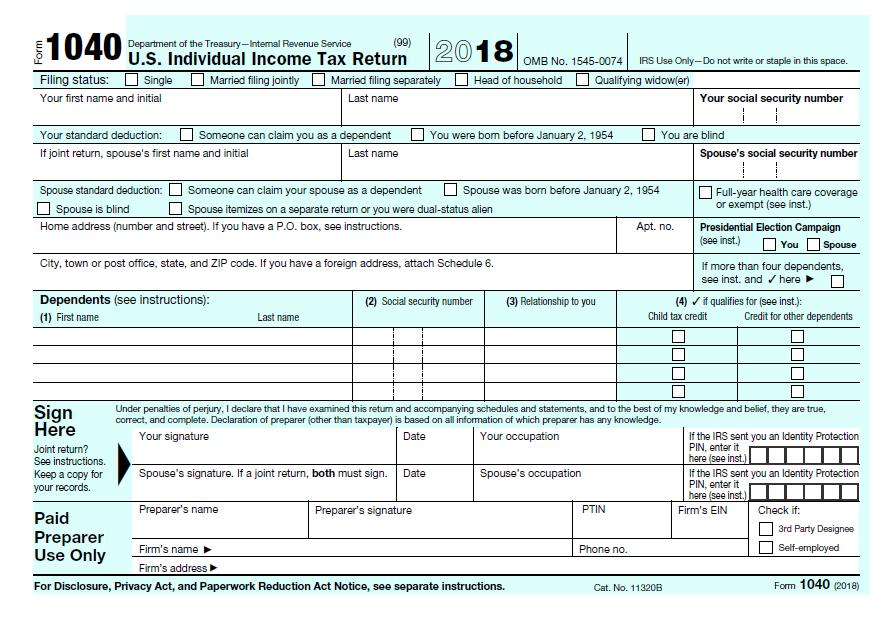

9 Filing Requirements, Cont. Forms , 1040A, 1040EZ Software will determine appropriate form, if unsure use 1040, which includes all deductions and credits. Filing Options: Residents can electronically or paper file tax forms. Free tax filing options at Free if below $66,000 in taxable income, otherwise pay a fee. Due Dates: Federal (IRS) and Massachusetts Wednesday, April 17, 2019 California Monday, April 15, 2019 Other states check on state tax website 9

10 10

11 11

12 Reportable Income Residents are taxed on worldwide income Report all income from any source U.S. AND Foreign: Salaries (W-2) Taxable fellowships, scholarships and grants (1042-S or none) Bank interest and dividends (1099) Investment income (1099) Royalties, prizes and awards (1099) Real estate rentals and sale proceeds (none) Gifts and any money received (none/other) 12

13 Fellowships, Scholarships and Grants Money received for the purpose of study or research: Non-Taxable Qualified Fellowship and Scholarship Amounts: Degree candidate, and Amounts received are used to pay tuition and fees for enrollment, Taxable: or for books, supplies and equipment required for courses. All other amounts, such as amounts used for room and board, travel, equipment not required for a course. Amounts received for services that are required as a condition of receiving the otherwise qualified amount (e.g. Research Assistant stipend amount, postdoctoral fellowship). 13

14 Determine Amount of Taxable Scholarships & Fellowships Methods to Assist in Determining Amount of Taxable Scholarships & Fellowships: 1. IRS Interactive Tax Assistant online interview to determine how much of your scholarship, fellowship, or education grant to include as income: 2. IRS Publication 970, Worksheet 1-1: 14

15 Reporting Taxable Fellowships & Scholarships Amount to Report: W-2 (only for services in relation to fellowship/scholarship), Grant/Fellowship/Scholarship Letter, or Personal Bank Account or Student Account Where to Report: Form 1040, Line 1 include the taxable portion in the Wages, salaries, tips line of the return. If not included on a W-2 or 1042-S enter SCH along the line. SCH 10, Form 1040NR, 1040NR-EZ report on Scholarship and fellowship grants line 15

16 Foreign Income Resident taxpayers are subject to income from all sources, even income fully earned and sourced to another country, including Investment Income royalties, interest, etc. Real Estate Income, including: o o Rental income from non-u.s. property Capital gains from sale of property inside or outside of the U.S. Foreign Tax Credit/Deduction IRS Topic Number

17 Foreign Assets/Accounts Additional Forms required if you have foreign assets or bank accounts that exceed certain thresholds: Foreign Assets Form 8938, Statement of Specified Foreign Financial Assets Threshold - $50,000 or more depending on filing status Forms and instructions - statement-of-foreign-financial-assets Foreign Bank Accounts FinCEN Form 114 ( FBAR ) Threshold - $10,000 in an account over which you have signature or other authority File electronically through BSA E-FilingSystem website at bsaefiling.fincen.treas.gov/noregfbarfiler.html 17

18 Estimated Tax Payments If you expect to owe taxes on income received that was not subject to tax withholding you should pay quarterly estimated taxes with the IRS and any state in which you are required to file to avoid any penalties. Examples of when you want to pay estimated taxes: Received taxable scholarship/fellowship income (U.S. or Foreign) Significant foreign sourced income In business for yourself How to make estimated tax payments: IRS Form 1040-ES provides a worksheet to estimate taxes and instructions on how to pay (check, by phone or electronically) 18

19 Tax Treaties Typically a resident does not receive the benefit of a tax treaty because the treaty only covers a number of years, which is the same as the substantial presence visa exemption period. Treaty Saving Clause allows country to tax income when an individual meets residency status in that country. Exceptions to Saving Clauses allow continuation of treaty benefits for the period specified in the treaty for that type of income, for example: Example - UK treaty allows treaty for students without limit Exception clause is in all but 2 treaties (Greece and Pakistan) Contact VPF Payroll (payroll@mit.edu) for how to utilize a treaty savings clause. 19

20 Tax Treaties Example of Savings Clause and Exception may be hard to locate in treaty, check the miscellaneous provisions. U.S. UK Tax Treaty Article 1, General Scope 4. Notwithstanding any provision of this Convention except paragraph 5 of this Article, the [U.S] may tax its residents and its citizens, as if the Convention had not come into effect. 5. The provisions of paragraph 4 of this Article shall not affect: (b) The benefits conferred under paragraph 20 (Students), 20A (Teachers), 21 (Students and Trainees) upon individuals who are neither citizens of, nor have been admitted for permanent residence in, [the U.S.]. 20

21 How to Claim Tax Treaty on Form 1040 Include the treaty-exempt income in the wages, tips, salaries, etc. line of the tax return. Take the treaty-exempt income out as a negative amount on the other income line and handwrite See Attached 8833 on the dotted line next to the income. Complete Form 8833, Treaty-Based Return Position Disclosure: Check the box to indicate you are a U.S. citizen or resident Supply the appropriate treaty info in Section 1 In narrative section include brief immigration history and substantiation for treaty claim. Mail return, forms and schedules to IRS Philadelphia Service Center, regardless of how instructions say how and where to file. 21

22 How to Claim Tax Treaty on Form 1040 Example Assuming $10,000 of treaty exempt income Form 1040, Line 1 SCH 10, Form 1040, Schedule 1, Line 21 22

23 Tax Treaties Following are Examples of Common Tax Forms you may receive: W S 1098-T 23

24 Form W-2 24

25 Form 1042-S 25

26 Form 1098-T Due to an IRS change in reporting requirements, MIT will be reporting amounts paid for qualified tuition and related expenses (QTRE) in Box 1 on the 2018 Forms 1098-T. In prior years, MIT reported only amounts billed for QTRE in Box 2. Depending on a student s income (or family s income, if a dependent), enrollment status (full-time or half-time), and/or the amount of your qualified educational expenses for the year, students may be eligible for a federal education tax credit. Please consult your tax advisor for further tax questions or advice. 26

27 Form 1098-T continued MIT provides Form 1098-T to all MIT students: Box 1: Tuition + Student Fee paid during Calendar Year 2018 (Spring Semester 2018, Summer Semester 2018 and Fall Semester 2018). Student may prepare Form 8863 Education Credits Report qualifying expenses from Form 1098-T Box 1 to claim credits. Note that students may choose to report calendar year 2018 expenses + first semester expenses for 2019 however, you may NOT double-count the first semester 2019 expenses when preparing your 2019 individual income tax return. 27

28 Form 1098-T continued MIT provides Form 1098-T to all MIT students: Box 5: Scholarships and/or grants paid during Calendar Year 2018 (Spring Semester 2018, Summer Semester 2018 and Fall Semester 2018). Scholarships and grants generally include: All payments designated as grants or scholarships that are administered and processed by MIT SFS All payments by third parties, including governmental and private entities, civic and religious organizations and nonprofit entities, to offset the cost of attendance Student may prepare Form 8863 Education Credits Scholarships and grants paid during Calendar Year 2018 may reduce the amount of qualified educational expenses used in calculating education credits on Form

29 Massachusetts Tax Filings For Massachusetts state income tax, you are deemed a full year resident if you maintain a permanent place of abode in MA & you spend more than 183 days of the taxable year in MA Above tests not met, generally a nonresident for MA income tax. Earn more than $8,000 & the income is not exempt from taxation under a treaty, file MAForm 1-NR, if you are a nonresident alien. (Federal tax return may still be required) o Income less than $8,000 May want to file MA Form 1-NR to claim refund of any tax withheld Resident, file MA Form 1. Need to prove you have health insurance Form MA 1099-HC, Individual Mandate Massachusetts Health Care Coverage 29

30 Massachusetts Tax Filings Permanent place of abode depends on the type of housing. Off campus & not affiliated with MIT, you may be deemed to have a permanent place of abode in MA. If non-u.s. citizen U.S. citizen still financially supported by parents are generally deemed to be residents of the state of parents residency o Unless U.S. citizen student provides more than one-half of his or her own financial support, likely supported by parents 1099-HC form Not attached to MA return, need its information to complete the Massachusetts return o Informational Form Only No Tax Penalty assessed up to 50% of minimum monthly insurance premium qualified through MA Health Connector 30

31 Other States If you worked or were a student in more than one state, (CA and MA for example), in the same year because you moved from one state to another, you may be required to file tax forms in each state. Which form to use? Non-resident/Part-year resident Generally less than 183 days present in a state or no place of abode, (rental apartment, home, or similar dwelling) o Taxed on only income earned in the state and/or all income received or earned during part-year residency Resident Living in a state, or more than 183 days presence, with place of abode o Taxed on income from all sources Tax credits may be available on income taxed by both states 31

32 Healthcare Health Care Forms1095B or 1095C o o o Forms are not required to file returns and very possible they will not be received before individuals file 2017 tax returns. (If received keep in your records) Health insurance coverage from foreign employer generally satisfies the minimum essential coverage required Health Insurance purchased directly from a foreign insurance issuer or provided by a foreign government must be recognized by the US Department of Health & Human Services: Insurance-Market-Reforms/minimum-essential-coverage.html 32

33 Changes in U.S. taxes for 2018 Tax Law signed in late 2017 changes the federal income tax rates beginning in 2018: o o Changes include removing individual deductions and replacing with an increased standard deduction If employed, update W-4 once released by IRS (end of Feb.) o MIT Employees Go to Atlas, About Me and choose Tax Withholding from the menu on the left o IRS webpage

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes. Download Slides here: https://goo.gl/q1tigg

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

Tax Information for US Resident Students and Scholars. Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP

Tax Information for US Resident Students and Scholars Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP 1 Fellowship Stipends (Not Earned Income) Regarding Students: Fellowship stipends

Tax Information for US Resident Students and Scholars Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP 1 Fellowship Stipends (Not Earned Income) Regarding Students: Fellowship stipends

West Chester University. Taxation Issues Nonresident Aliens

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Foreign Student and Scholar Volunteer Tax Return Preparation. VITA Training 1

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

SUBJECT: Payments to Nonresident Aliens

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

OFFICIAL POLICY. Policy Statement

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

2012 Non-Resident Alien Tax Filings

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

If you have additional questions on this, please call Payroll & Records Management at 831-

February 2013 Recipients of Graduate Fellowship Awards: The University of Delaware is not required to report to the Federal Government or to withhold taxes on fellowship awards to U.S. citizens and resident

February 2013 Recipients of Graduate Fellowship Awards: The University of Delaware is not required to report to the Federal Government or to withhold taxes on fellowship awards to U.S. citizens and resident

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

PwC Boston Bill Fleming Carol McNeil William Reynolds March 2016

www.pwc.com U.S. Income Tax Presentation MIT International Scholars U.S. Residents for Tax Purposes Boston Bill Fleming Carol McNeil William Reynolds Agenda Filing Requirements & Residency Status Wages,

www.pwc.com U.S. Income Tax Presentation MIT International Scholars U.S. Residents for Tax Purposes Boston Bill Fleming Carol McNeil William Reynolds Agenda Filing Requirements & Residency Status Wages,

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS COMMON VISA TYPES AND THEIR TREATMENTS

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Frequently Asked Tax Questions 2018 Tax Returns

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks Director, University Tax Services Financial Management Services Participant Outcomes Recognize when payment situations have

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks Director, University Tax Services Financial Management Services Participant Outcomes Recognize when payment situations have

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Nonresident Alien Tax Compliance Workshop Comprehensive Overview and Update of the Issues

Day One: Monday October 17, 2016 Comprehensive Overview and Update of the Issues 8:00 8:30 Registration 8:30 8:45 Welcome, Introduction and Workshop Goals 8:45 10:30 Getting Started: An Overview of the

Day One: Monday October 17, 2016 Comprehensive Overview and Update of the Issues 8:00 8:30 Registration 8:30 8:45 Welcome, Introduction and Workshop Goals 8:45 10:30 Getting Started: An Overview of the

Tax Reporting for Inbound Students

Tax Reporting for Inbound Students March 9, 2018 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Taxation Resident vs. Nonresident Resident - Taxed on worldwide income - Allowed worldwide deductions

Tax Reporting for Inbound Students March 9, 2018 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Taxation Resident vs. Nonresident Resident - Taxed on worldwide income - Allowed worldwide deductions

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

Tax Reporting for Inbound Students

Tax Reporting for Inbound Students March 10, 2017 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Tax Residence 101 Defined in Internal Revenue Code (IRC) Section 7701(b) - Determined based on

Tax Reporting for Inbound Students March 10, 2017 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Tax Residence 101 Defined in Internal Revenue Code (IRC) Section 7701(b) - Determined based on

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

RUTGERS POLICY. Responsible Executive: Senior Vice President for Finance and Administration

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

TAX FILING FOR STUDENTS AND SCHOLARS 101. Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

Princeton University International Undergraduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 2, 2011

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

INTERNATIONAL TAX. Presented by Fiscal Services

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Basic Tax Information for F and J Immigration Status

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

Princeton University International Graduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 9, 2011

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

International Student Taxes

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room Presented by:

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

U.S. Nonresident Alien Income Tax Return

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Webinar Tax Treatment for Scholarships and Fellowships

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

PLEASE PRESS *6 ON YOUR PHONE TO MUTE

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

Tax information. International Students in the United States

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

Overview of Taxation for Students

Overview of Taxation for Students Disclaimer This session has been created under the premises of the Volunteer Income Tax Assistance Program (VITA), a program of the Internal Revenue Service. In offering

Overview of Taxation for Students Disclaimer This session has been created under the premises of the Volunteer Income Tax Assistance Program (VITA), a program of the Internal Revenue Service. In offering

U.S. Nonresident Alien Income Tax Return

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

State Tax Issues for Non - Resident Scholars and Researchers

State Tax Issues for Non - Resident Scholars and Researchers Agenda 2 California Residency Laws Items taxed by California Taxation of fellowships, stipends and scholarships State & Federal Differences

State Tax Issues for Non - Resident Scholars and Researchers Agenda 2 California Residency Laws Items taxed by California Taxation of fellowships, stipends and scholarships State & Federal Differences

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

Feeley & Driscoll, P.C. 200 Portland Street Boston, MA

Feeley & Driscoll, P.C. 200 Portland Street Boston, MA 02114 www.fdcpa.com U.S. Tax Resident vs. Non-Resident 2 1. Residents a. Report worldwide income b. File form 1040, form 114 (FBAR) form 8938 (FATCA)

Feeley & Driscoll, P.C. 200 Portland Street Boston, MA 02114 www.fdcpa.com U.S. Tax Resident vs. Non-Resident 2 1. Residents a. Report worldwide income b. File form 1040, form 114 (FBAR) form 8938 (FATCA)

Subject: IMPORTANT TAX INFO FOR INTERNATIONAL STUDENTS FOR TAX YEAR 2018

Subject: IMPORTANT TAX INFO FOR INTERNATIONAL STUDENTS FOR TAX YEAR 2018 WHAT: Mandatory International Student Tax Requirements WHO: All international students and dependents WHEN: Tax Forms for Year 2018

Subject: IMPORTANT TAX INFO FOR INTERNATIONAL STUDENTS FOR TAX YEAR 2018 WHAT: Mandatory International Student Tax Requirements WHO: All international students and dependents WHEN: Tax Forms for Year 2018

U.S. Nonresident Alien Income Tax Return

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

~E~ E-3 visa, 103 Earnings statement, 100, 131, 135, 136,

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Sponsored by University Student Financial Services PERSONAL TAXES. Jodi R. Kessler, LLM Tax Manager Harvard University

Sponsored by University Student Financial Services PERSONAL TAXES Jodi R. Kessler, LLM Tax Manager Harvard University 1 DISCLAIMER Federal income tax; states may differ Information is specific to US citizens

Sponsored by University Student Financial Services PERSONAL TAXES Jodi R. Kessler, LLM Tax Manager Harvard University 1 DISCLAIMER Federal income tax; states may differ Information is specific to US citizens

Taxability of Prizes and Awards President s Engagement Prizes. December 9, Office of the Comptroller

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

U.S. Nonresident Alien Income Tax Return. Of what country were you a citizen or national during the tax year?

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

International Student Taxes. Information compiled by International Student Services

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR

Session 2017 Tax Year Georgia Form 500 with Form 1040NR") Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Nonresident Alien Tax Compliance

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

Your Federal Income Tax Responsibilities as an Au Pair

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

Instructions for Form 1040NR-EZ

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

University of Utah Payments to Non Resident Aliens

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

Education, Taxes, & Benefits. Duke University August 22, 2017

Education, Taxes, & Benefits Duke University August 22, 2017 Megan Hutchinson, CPA Senior Manager - Tax Raleigh Office DISCUSSION POINTS TYPES OF INCOME TAXABLE v NON-TAXABLE QUALIFIED v NON-QUALIFIED

Education, Taxes, & Benefits Duke University August 22, 2017 Megan Hutchinson, CPA Senior Manager - Tax Raleigh Office DISCUSSION POINTS TYPES OF INCOME TAXABLE v NON-TAXABLE QUALIFIED v NON-QUALIFIED

Receiving payments in the U.S. Angela Gwinn

Receiving payments in the U.S. Angela Gwinn Payroll Payroll Department is part of the Office of Human Resources. 720 University Place, 2 nd floor in Evanston Abbott Hall, 8 th floor in Chicago 1071532

Receiving payments in the U.S. Angela Gwinn Payroll Payroll Department is part of the Office of Human Resources. 720 University Place, 2 nd floor in Evanston Abbott Hall, 8 th floor in Chicago 1071532

Nonresident Aliens. Resident Alien. Are you a resident alien? Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns

Nonresident Aliens Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns Resident Alien Are you a resident alien? A resident alien is generally taxed in the same way as U.S. citizens You

Nonresident Aliens Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns Resident Alien Are you a resident alien? A resident alien is generally taxed in the same way as U.S. citizens You

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

INTERNATIONAL STUDENTS TAX WORKSHOP 2018

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

Nonresident Alien Federal Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500

Session 2015 Tax Year GA Form 500") Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

International Students and Scholars Nonresident Tax Orientation. February 14, 2018

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

NEW VENDOR REQUEST NEW VENDOR INFORMATION INTERNATIONAL VENDOR REQUEST INDIVIDUAL

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

Tax Information for Employees of the British Embassy & Consulate

Tax Information for Employees of the British & Consulate Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared for employees of the British by LLC. The information in this presentation

Tax Information for Employees of the British & Consulate Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared for employees of the British by LLC. The information in this presentation

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Non-Resident Aliens. Filing a Minnesota Return

Non-Resident Aliens Filing a Minnesota Return Minnesota Residency for tax purposes 183 day rule - in Minnesota must establish a tax home - visa s are a temporary status any day or part of a day qualifies

Non-Resident Aliens Filing a Minnesota Return Minnesota Residency for tax purposes 183 day rule - in Minnesota must establish a tax home - visa s are a temporary status any day or part of a day qualifies

FOREIGN VISITOR TAX GUIDE

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

Office of International Services TAX WORKSHOP. Tax preparation for International Students and Scholars Tax Year 2018

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

Welcome to Tax Filing Information for International Students and Scholars

Welcome to Tax Filing Information for International Students and Scholars Presented by Office of International Student & Scholar Services Florida Institute of Technology DISCLAIMER ISSS staff are not licensed

Welcome to Tax Filing Information for International Students and Scholars Presented by Office of International Student & Scholar Services Florida Institute of Technology DISCLAIMER ISSS staff are not licensed

Foreign Tax Issues REBECCA DONEHEW

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Nonresident Alien State of Hawaii Tax Workshop

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

DO NOT FILE THIS FORM IN 2019 WITH YOUR TAX RETURN

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

Student's Guide to Federal Income Tax

Publication 4 Cat. No. 46073X Department of the Treasury Internal Revenue Service Student's Guide to Federal Income Tax For use in preparing 1998 Returns Contents Introduction... 2 Where Do My Tax Dollars

Publication 4 Cat. No. 46073X Department of the Treasury Internal Revenue Service Student's Guide to Federal Income Tax For use in preparing 1998 Returns Contents Introduction... 2 Where Do My Tax Dollars

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

In year 1 you may be supported in one of the following ways:

October 1 st 2015 Dear BGS Students, There is some confusion regarding the years of the program in which you get no taxes withheld from your stipend check, and need to file estimated taxes and the years

October 1 st 2015 Dear BGS Students, There is some confusion regarding the years of the program in which you get no taxes withheld from your stipend check, and need to file estimated taxes and the years

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

Form 1040NR Filing Challenges and Effective Approaches

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

Navigator. U.S. residency Canadians travelling to the U.S. beware. The. U.S. income tax residency rules could affect you

The Navigator RBC Wealth Management Services U.S. residency Canadians travelling to the U.S. beware U.S. income tax residency rules could affect you If you are a Canadian resident who spends extended time

The Navigator RBC Wealth Management Services U.S. residency Canadians travelling to the U.S. beware U.S. income tax residency rules could affect you If you are a Canadian resident who spends extended time

Tax Basics Workshop, for Professional Degree Students at UCSF

Tax Basics Workshop, for Professional Degree Students at UCSF Tuesday 2/12/19 in S-214 Wednesday 2/20/19 in CL 221-222 and Monday 2/25/19 in N-225 Zoom: https://ucsf.zoom.us/j/8531229278 Daniel Roddick

Tax Basics Workshop, for Professional Degree Students at UCSF Tuesday 2/12/19 in S-214 Wednesday 2/20/19 in CL 221-222 and Monday 2/25/19 in N-225 Zoom: https://ucsf.zoom.us/j/8531229278 Daniel Roddick

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

MIT U.S. Income Tax Presenta3on Interna3onal Scholars, Nonresidents for Tax Purposes

MIT U.S. Income Tax Presenta3on Interna3onal Scholars, Nonresidents for Tax Purposes PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Who are Scholars Postdoctoral Associates and Fellows Lecturers Visi3ng

MIT U.S. Income Tax Presenta3on Interna3onal Scholars, Nonresidents for Tax Purposes PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Who are Scholars Postdoctoral Associates and Fellows Lecturers Visi3ng

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

Federal Tax Information Session For International Scholars

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

NOTE: In August 2011, you will receive a pro-rated stipend amount of $2,101.45, as your August start date is 8/4.

August 31, 2011 Dear Combined Degree Students, There is some confusion regarding the years of the program in which you have no taxes withheld from your stipend check, and need to file estimated taxes and

August 31, 2011 Dear Combined Degree Students, There is some confusion regarding the years of the program in which you have no taxes withheld from your stipend check, and need to file estimated taxes and

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January