UCSF Postdoc Scholars. Revised March 20, 2013

|

|

|

- Myron Rich

- 5 years ago

- Views:

Transcription

1 UCSF Postdoc Scholars Revised March 20, 2013

2 Agenda Introduction Hiring Checklist Required Keying Practices Dues/Fees Taxation Financials Appendix: Taxation 2

3 Hiring Checklist Postdoc Scholars 3

4 Postdoc Hiring Checklist 1. Notice of Appointment (offer letter) signed by PI 2. UCSF Postdoc Acknowledgement of Receipt of Information Form (revised October, 2010). (All Postdocs) 3. Employment Eligibility Verification I-9 Form (All Postdocs) 4. Patent Acknowledgement and State Oath of Allegiance UPAY 585 Form (All Postdocs sign Patent section; only US citizens sign Oath) 5. Withholding Allowance Certificate (UC W-4/DE 4) (US Citizens) 6. Out-of State Withholding Form (UPAY 830) (All Postdocs) 4

5 Postdoc Hiring Checklist (p. 2) 7. State of Citizenship and Federal Tax Status (Non US Citizens) 8. Withholding Allowance Certificate-Non-Resident (UC W-4 NR/DE 4) (Non US Citizens) 9. Benefits Eligibility Level Indicator and Status Qualifier Code (UPAY 726) (All Postdocs) 10. Demographic Transmittal UPAY 5605 Form (All Postdocs) sent to payroll. 11. Deduction Authorization Form for Union Dues/Fees 5

6 Required Keying Practices Postdoc Scholars 6

7 Payments to Postdocs-OLD Payroll/Personnel System Postdoc Employees (TC 3252) Student Financial Aid Postdoc Fellows (TC 3253) External Source Postdoc Paid Directs (TC 3254) Inconsistent treatment/processes Difficult to do reporting Additional administrative effort 7

8 Payments to Postdocs-NEW Payroll/Personnel System Postdoc Employees (TC 3252) Postdoc Fellows (TC3253) External Source Postdoc Paid Directs (TC 3254) Consistency Consolidated payment source Decreased administrative effort 8

9 Payments to Fellows from PPS Employee Wages Does paying a postdoc fellow through PPS make him/her an employee? 9 Scholarship and fellowship grants given to an individual for study, training or research and which does not constitute compensation for personal services

10 Postdoc Titles & DOS Codes Payroll Title Title Code DOS Description Income Type Postdoc Employee 3252 REG Regular Pay Wages Postdoc Fellow 3253 FEN FEL Postdoc Paid Direct 3254 PDW PDE US Citizen & Permanent Resident Alien Nonresident Alien Postdoc without salary Monthly external pay Stipend: Scholarship Fellowship Training grant Paid by external source NO personal funds allowed 10

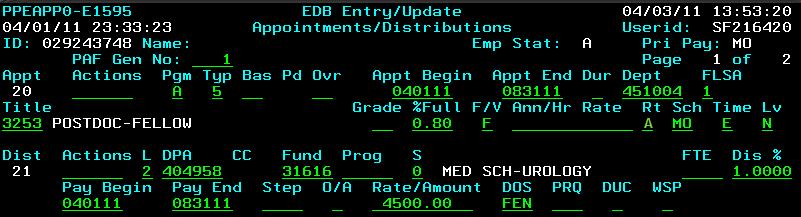

Setup: Typ: 5 F/V: F RT: A Sch: MO Time: E LV: N DOS: REG")

11 Postdoc Employee Funds are distributed via the payroll system (no change) Setup: Typ: 5 F/V: F RT: A Sch: MO Time: E LV: N DOS: REG 11

12 Postdoc Fellow Funds are now distributed via the payroll system Setup: Typ: 5 F/V: F RT: A Sch: MO Time: E LV: N Rate/Amt Dist %: Blank DOS: FEN: For Citizens and Resident Aliens 12 FEL: For Nonresident Aliens

13 Postdoc Fellow Benefits If the Fellow s benefits are to be paid from a funding source other than that designated for their stipend, a PDW distribution will need to be added. A PDW distribution is ONLY needed when you want to designate a different fund source to pay benefit expenses then what is being used to pay the stipend on FEN/FEL Only one PDW distribution line is permitted You will need to change the appointment rate code to A in order to add the PDW distribution Workers Compensation will still be assessed to the FEN/FEL distribution 13

14 Postdoc Fellow Benefits 14

15 Postdoc Scholar Paid Direct Employee receives their funding directly from an external source. No pay generated via the payroll system. Setup of their appointment includes a distribution to record the monthlyequivalent pay amount from an external source using DOS PDE and a distribution to fund their associated benefits on DOS PDW One appointment Typ: 5 F/V: F RT: A Sch: MO Time: E LV: N Two distributions L/A/C/F/P/S = Appropriate FAU Dist % = Blank Rate/Amt = PDW: Blank PDE: Monthly equivalent amount DOS = PDW and PDE 15

16 Postdoc Scholar Paid Direct 16

17 Postdoc Supplement Some Postdocs receive a supplement from University funds. The supplement is treated as wages Use REG when the supplement is required to meet the minimum base salary Use PDS when the supplement is above the minimum Appointment percentage should reflect percentage of total pay coming from each source (not to exceed 100%). Setup: 17 Appt 1-Postdoc Fellow or Paid Direct appointment Appt 2-Separate Postdoc Employee appointment to pay the supplement

18 Postdoc Supplement Example Appt 2 Appt 1 18

19 Transition for Postdoc Fellows Activity Date Fellow s last payment from stipend desk: April 1, 2011 Begin using FEN/FEL for Fellows April 6, 2011 New appointments for current Fellows must be setup in PPS by: April 25, :00PM Notice to Fellows mailed: April 15, 2011 Fellow s first payment from PPS : April 29, 2011 Discontinue sending hire documents to Student Accounts Determine if benefits will be paid from the same fund source as the stipend End current appointment/distributions for current Fellows effective 03/31/11 Create new appointment/distributions for current and new Fellows effective 04/01/11 Failure to setup a Fellow with a FEN/FEL distribution will result in the Fellow receiving no stipend payment 19

20 Dues & Agency Fees Postdoc Scholars 20

21 Dues/Fees Process Union dues and agency fees are deducted automatically for Postdoc Employees and Fellows Dues and fees are calculated based on the combined gross earnings from all pay sources Postdoc Paid Directs with a combo 3252 or 3253 appointment will have dues/fees deducted Postdoc Paid Directs with only a 3254 appointment will pay dues fees directly to the union Fellows are required to submit a written authorization form for dues/fees deduction 21

22 Benefits & Taxes Postdoc Scholars 22

23 Postdoc Benefits Benefits paid for by the University that are provided to Postdoc Fellows and Paid Directs and their dependents are subject to income tax. 23 Citizen & Resident Benefits are taxable and must be self reported to IRS and CA FTB The University is not required to report these payments to the IRS or withhold tax on the payments. Nonresident Alien The imputed income for benefits is reported on the Form 1042-S as non-qualified fellowship/scholarship The University is required to report these payments to the IRS and under some circumstances to withhold tax on the payments. Fellows will no longer be billed for required tax withholdings, deductions will be taken from the stipend payment.

24 Tax Treatment of Fellowship Stipend -Nonresident Aliens Federal tax withheld is based on the Postdoc s citizenship status and visa type as set up in PPS Nonresident aliens (NRA) paid on FEL Title Code Citizenship Code Visa Type Federal Tax Withholding Postdoc-Fellow (TC 3253) Nonresident Alien (N) J1 14% Postdoc-Fellow (TC 3253) Nonresident Alien (N) F1 14% Postdoc-Fellow (TC 3253) Nonresident Alien (N) All others 30% Postdoc-Fellow (TC 3253) Nonresident Alien (N) None 30% 24

25 Financials Postdoc Scholars 25

PSBP Life/AD&D 26")

26 Month End Reporting Postdoc Fellow s stipend payments and deductions are part of the normal month end processing and will appear on the Distribution of Payroll Expense (DPE) FEN/FEL gross earnings = stipend payment Benefits will include: PSBP Medical, Dental, Vision Worker s Comp, Unemployment Insurance and Broker/Admin Fees (where applicable) PSBP Life/AD&D 26

27 Expense Transfers Fellowship stipends will need to be transferred via the completion of a Payroll Expenditure Transfer (PET) Simplified - TS (UP773) In circumstances in which the benefit expenses cannot be transferred because there is no associated gross salary, expenses may be relocated by financial journal 27

28 The End Whom to contact: Payroll (keying questions): Tracy Lee, Postdoc Benefits Coordinator Postdoc Affairs (policy/contract questions): Christine Des Jarlais, Postdoc Affairs 28

29 Appendix: Taxation Postdoc Scholars 29

30 Withholding and Reporting Responsibility Two opportunities for taxation Tax treatment of fellowship stipend Tax treatment of postdoc health benefits Different rules for Employees, Fellows and Paid Directs Different rules for U.S. Citizen/Resident vs. Nonresident Alien and Resident of CA vs. Nonresident of CA 30

31 Tax Treatment of Fellowship Stipend The entire portion of the fellowship stipend for Postdoc Fellows is considered nonqualified Not required for either enrollment or attendance in a course of instruction Therefore, not excludable from gross income What does this mean to the Fellow? Must be reported by the recipient on his/her tax return The entire amount of the stipend is taxable 31

32 Tax Treatment of Fellowship Stipend -Citizens & Residents For the Postdoc Fellow, who is a citizen, pending permanent resident or resident alien, the University is not required to report or withhold tax on the fellowship stipend Citizenship codes: C Citizen R & F Resident Alien P Pending Permanent Resident Alien 32

33 Tax Treatment of Fellowship Stipend -Nonresident Aliens For the Postdoc Fellow who is a nonresident alien, the University must report fellowship payments on Form 1042-S, Foreign Person s U.S. Source Income Subject to Withholding The University must also withhold taxes unless the payment is excluded under one of the following exemptions: 33 The income is not U.S. source income The individual is covered by a tax treaty exemption

34 Tax Treatment of Fellowship Stipend -Nonresident Aliens Federal tax withheld is based on the Postdoc s citizenship status and visa type as set up in PPS Nonresident aliens (NRA) paid on FEL Title Code Citizenship Code Visa Type Federal Tax Withholding Postdoc-Fellow (TC 3253) Nonresident Alien (N) J1 14% Postdoc-Fellow (TC 3253) Nonresident Alien (N) F1 14% Postdoc-Fellow (TC 3253) Nonresident Alien (N) All others 30% Postdoc-Fellow (TC 3253) Nonresident Alien (N) None 30% 34

35 Tax Treatment of Fellowship Stipend -Resident/Nonresident of CA California does not distinguish between U.S. Citizens, Resident Aliens and Nonresident Aliens Nonresident of CA first year Subject withholding at 7%, reported on Form 592-B Resident of CA after first year No withholding, No reporting Recipient is required to self report 35

36 Postdoc Benefits Benefits paid for by the University that are provided to Postdoc Fellows and Paid Directs and their dependents are subject to income tax. Citizen & Resident Benefits are taxable and must be self reported to IRS and CA FTB The University is not required to report these payments to the IRS or withhold tax on the payments. Nonresident Alien The imputed income for benefits is reported on the Form 1042-S as non-qualified fellowship/scholarship 36

37 Imputed Income for Benefits (cont) Nonresident Alien The University must also withhold taxes unless the payment is excluded under a tax treaty exemption If no tax treaty exemption is provided: PPS calculates the imputed income related to the medical, dental, and vision contributions paid by the University. The Payroll office will withhold tax on the imputed income and report the income and withholding on a Form 1042-S. Such withholding will be taken from the stipend payments made to the Postdoc Fellow. Postdoc Paid Directs will be billed for this withholding, since their stipends are not paid by the University 37

38 Imputed Income for Benefits (cont) State taxes No state withholding is required The value of the benefits is reportable on a Form 592-B for any nonresident of California Withholding and Reporting Summary Postdoc Subject to Deductions for: Benefits Paid by the University Reported on: Federal State Federal State Postdoc-Pay Direct-Citizen/PR No No Postdoc-Pay Direct -NRA Yes No 1042-S 592-B Postdoc-Fellow-Citizen/PR No No Postdoc-Fellow-NRA Yes No 1042-S 592-B Postdoc-Employee-Citizen/PR No No Postdoc-Employee-NRA No No

Non-Resident Alien Fellowship/Scholarship Payments and Taxes Monthly Reporting Process. Service Request 16938

Non-Resident Alien Fellowship/Scholarship Payments and Taxes Monthly Reporting Process Service Request 16938 University of California Office of the President Payroll Coordination and Tax Services Revised

Non-Resident Alien Fellowship/Scholarship Payments and Taxes Monthly Reporting Process Service Request 16938 University of California Office of the President Payroll Coordination and Tax Services Revised

Postdoctoral Scholar Follow-up Issues Service Request 16976

Postdoctoral Scholar Follow-up Issues Service Request 16976 University of California Financial Management Payroll Coordination September 14, 2005 Postdoctoral Scholar Follow-up Issues Table of Contents

Postdoctoral Scholar Follow-up Issues Service Request 16976 University of California Financial Management Payroll Coordination September 14, 2005 Postdoctoral Scholar Follow-up Issues Table of Contents

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

West Chester University. Taxation Issues Nonresident Aliens

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM. Glacier Guide for Departments

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Webinar Tax Treatment for Scholarships and Fellowships

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

Business Requirements Document

Business Requirements Document SR101131 - Update Tax Treaty Income Code (EDB1170) and Tax Treaty Income Code Alternate (EDB1171) in PPS with New IRS Values Document Information Document Attributes ID Owner

Business Requirements Document SR101131 - Update Tax Treaty Income Code (EDB1170) and Tax Treaty Income Code Alternate (EDB1171) in PPS with New IRS Values Document Information Document Attributes ID Owner

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Vendor Set-Up Process

Vendor Set-Up Process Office of the Controller April 26, 2018 Karen Kittredge, Manager, Policy and Business Process Teri DeLeon, Procure to Pay Manager Sharon Henry-Bell, Accounts Payable Operations Supervisor

Vendor Set-Up Process Office of the Controller April 26, 2018 Karen Kittredge, Manager, Policy and Business Process Teri DeLeon, Procure to Pay Manager Sharon Henry-Bell, Accounts Payable Operations Supervisor

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

If you have additional questions on this, please call Payroll & Records Management at 831-

February 2013 Recipients of Graduate Fellowship Awards: The University of Delaware is not required to report to the Federal Government or to withhold taxes on fellowship awards to U.S. citizens and resident

February 2013 Recipients of Graduate Fellowship Awards: The University of Delaware is not required to report to the Federal Government or to withhold taxes on fellowship awards to U.S. citizens and resident

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

FOREIGN NATIONAL PAYMENT GUIDE

FOREIGN NATIONAL FOREIGN NATIONAL PAYMENT GUIDE PAYMENT GUIDE May-2018 UNIVERSITY OF PENNSYLVANIA Contents Chapter 1: Foreign National Payment Guide... 3 1.1 Visa Matrix... 3 Chapter 2: Nonresident New

FOREIGN NATIONAL FOREIGN NATIONAL PAYMENT GUIDE PAYMENT GUIDE May-2018 UNIVERSITY OF PENNSYLVANIA Contents Chapter 1: Foreign National Payment Guide... 3 1.1 Visa Matrix... 3 Chapter 2: Nonresident New

State Tax Issues for Non - Resident Scholars and Researchers

State Tax Issues for Non - Resident Scholars and Researchers Agenda 2 California Residency Laws Items taxed by California Taxation of fellowships, stipends and scholarships State & Federal Differences

State Tax Issues for Non - Resident Scholars and Researchers Agenda 2 California Residency Laws Items taxed by California Taxation of fellowships, stipends and scholarships State & Federal Differences

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes. Download Slides here: https://goo.gl/q1tigg

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

To-Be Process Review Workshop

1 To-Be Process Review Workshop Human Resources Taxes Location: ROSS Building Room: 130 Time: 8:00 am - 12:00 pm Date: 9/19/05 2 Workshop Logistics Tent Cards Rest Rooms Break Parking Lot 3 Workshop Agenda

1 To-Be Process Review Workshop Human Resources Taxes Location: ROSS Building Room: 130 Time: 8:00 am - 12:00 pm Date: 9/19/05 2 Workshop Logistics Tent Cards Rest Rooms Break Parking Lot 3 Workshop Agenda

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

SUBJECT: Payments to Nonresident Aliens

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6, 2019 1 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6, 2019 1 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler

CAMP IPPS August 21, 2018

CAMP IPPS 2018 August 21, 2018 WELCOME CAMPERS A few things to remember West Ballroom Stop by the ballroom to ask us questions after the class! Meet Connexxus travel vendors in honor of the Connexxus 10

CAMP IPPS 2018 August 21, 2018 WELCOME CAMPERS A few things to remember West Ballroom Stop by the ballroom to ask us questions after the class! Meet Connexxus travel vendors in honor of the Connexxus 10

Princeton University International Undergraduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 2, 2011

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Disbursements: State Tax Withholding from Nonwage Payments to Nonresidents of California

Disbursements: State Tax Withholding from Nonwage Payments to Nonresidents of California Responsible Officer: EVP - Chief Financial Officer Responsible Office: FO - Financial Operations Issuance Date:

Disbursements: State Tax Withholding from Nonwage Payments to Nonresidents of California Responsible Officer: EVP - Chief Financial Officer Responsible Office: FO - Financial Operations Issuance Date:

Nonresident Alien Federal Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Payments to Foreign Nationals. March 11, 2013

Payments to Foreign Nationals March 11, 2013 Workshop Presenters Denise Esworthy University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Payments to Foreign Nationals March 11, 2013 Workshop Presenters Denise Esworthy University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room Presented by:

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

PAYROLL SERVICES Presents: OVERVIEW OF RESIDENCY FOR TAX PURPOSES

PAYROLL SERVICES Presents: OVERVIEW OF RESIDENCY FOR TAX PURPOSES Is Residency for tax purposes a choice? NO We do not get to choose residency for tax purposes 6/11/2009 2 Objectives Understand the rules

PAYROLL SERVICES Presents: OVERVIEW OF RESIDENCY FOR TAX PURPOSES Is Residency for tax purposes a choice? NO We do not get to choose residency for tax purposes 6/11/2009 2 Objectives Understand the rules

Receiving payments in the U.S. Angela Gwinn

Receiving payments in the U.S. Angela Gwinn Payroll Payroll Department is part of the Office of Human Resources. 720 University Place, 2 nd floor in Evanston Abbott Hall, 8 th floor in Chicago 1071532

Receiving payments in the U.S. Angela Gwinn Payroll Payroll Department is part of the Office of Human Resources. 720 University Place, 2 nd floor in Evanston Abbott Hall, 8 th floor in Chicago 1071532

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

Nonresident Alien Tax Compliance

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

Payments to Foreign Nationals. March 9, 2015

Payments to Foreign Nationals March 9, 2015 Workshop Presenters Kelly Sellers University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Payments to Foreign Nationals March 9, 2015 Workshop Presenters Kelly Sellers University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Taxability of Prizes and Awards President s Engagement Prizes. December 9, Office of the Comptroller

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

PLEASE PRESS *6 ON YOUR PHONE TO MUTE

Immigration Services Year End Tax Presentation December, 2013 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following Keep your phone-line muted throughout the session to minimize background noise

Immigration Services Year End Tax Presentation December, 2013 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following Keep your phone-line muted throughout the session to minimize background noise

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Research Administration Forum August 9th, Yoon Lee Director, Extramural Fund Management

1 Research Administration Forum August 9th, 2018 Yoon Lee Director, Extramural Fund Management Meeting Agenda 2 Welcome and Announcements Yoon Lee Welcome! Research Administration Forum August 9th, 2018-10:00

1 Research Administration Forum August 9th, 2018 Yoon Lee Director, Extramural Fund Management Meeting Agenda 2 Welcome and Announcements Yoon Lee Welcome! Research Administration Forum August 9th, 2018-10:00

Requirements Definitions Form 1042-S 2001 Service Request 14859

Requirements Definitions Form 1042-S 2001 Service Request 14859 University of California Payroll Coordination Final -January 14, 2002 Requirements for Forms 1042-S Table of Contents Section Page I. Overview

Requirements Definitions Form 1042-S 2001 Service Request 14859 University of California Payroll Coordination Final -January 14, 2002 Requirements for Forms 1042-S Table of Contents Section Page I. Overview

Understanding Your W-2

Understanding Your W-2 The following information is intended to answer the most frequently asked questions regarding the content and distribution of your W-2, which is needed to file income tax returns.

Understanding Your W-2 The following information is intended to answer the most frequently asked questions regarding the content and distribution of your W-2, which is needed to file income tax returns.

PPS & Glacier Training. Desiree Hennon Nonresident Alien Tax Analyst Glacier Administrator UCSD Payroll Division November 28, 2017

PPS & Glacier Training for UCSD Administrative Personnel Desiree Hennon Nonresident Alien Tax Analyst Glacier Administrator UCSD Payroll Division November 28, 2017 Section 1: Introduction Who are we talking

PPS & Glacier Training for UCSD Administrative Personnel Desiree Hennon Nonresident Alien Tax Analyst Glacier Administrator UCSD Payroll Division November 28, 2017 Section 1: Introduction Who are we talking

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Prize, Grant, Award or Fellowship Policy Review Session

Prize, Grant, Award or Fellowship Policy Review Session Office of the Controller Karen Kittredge, OC, Manager Policy and Business Process Natasha Rivera, OC, Nonresident Alien Compliance Manager 1 Financial

Prize, Grant, Award or Fellowship Policy Review Session Office of the Controller Karen Kittredge, OC, Manager Policy and Business Process Natasha Rivera, OC, Nonresident Alien Compliance Manager 1 Financial

Princeton University International Graduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 9, 2011

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

Tax Information for US Resident Students and Scholars. Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP

Tax Information for US Resident Students and Scholars Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP 1 Fellowship Stipends (Not Earned Income) Regarding Students: Fellowship stipends

Tax Information for US Resident Students and Scholars Nabih Daaboul Carol McNeil Rich Wagman PricewaterhouseCoopers LLP 1 Fellowship Stipends (Not Earned Income) Regarding Students: Fellowship stipends

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR

Session 2017 Tax Year Georgia Form 500 with Form 1040NR") Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Federal Income Tax and Railroad Retirement Benefits

FROM THE DESK OF Walter A. BARROWS LABOR MEMBER U.S. RAILROAD RETIREMENT BOARD For Publication For Publication February 2012 Federal Income Tax and Railroad Retirement Benefits The following questions

FROM THE DESK OF Walter A. BARROWS LABOR MEMBER U.S. RAILROAD RETIREMENT BOARD For Publication For Publication February 2012 Federal Income Tax and Railroad Retirement Benefits The following questions

SCHEDULE OF EMPLOYER MATCHING CONTRIBUTION RATES (REVISED 1/1/2015)

") Section: 395-10 Supplement I Page 1 I RETIREMENT UCRP (1976 Tier) 668600 7/1/2014 14.00% of covered wages (1) 8.00% less $19.00/mo (6,7) UCRP Supplemental Assessment 668630 7/1/2014 0.50% of covered wages

Section: 395-10 Supplement I Page 1 I RETIREMENT UCRP (1976 Tier) 668600 7/1/2014 14.00% of covered wages (1) 8.00% less $19.00/mo (6,7) UCRP Supplemental Assessment 668630 7/1/2014 0.50% of covered wages

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

University of Utah Payments to Non Resident Aliens

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

OUTDATED. Back to Index. Policy 3-22 Rev. Date: April 30, Subject: STIPENDS AND TAX EXEMPT PAYMENTS PURPOSE

Policy 3-22 Rev. Date: April 30, 1976 Back to Index Subject: STIPENDS AND TAX EXEMPT PAYMENTS I. II. PURPOSE To establish a policy and related procedures for administering stipends for scholarships and

Policy 3-22 Rev. Date: April 30, 1976 Back to Index Subject: STIPENDS AND TAX EXEMPT PAYMENTS I. II. PURPOSE To establish a policy and related procedures for administering stipends for scholarships and

RELEASE New Federal Tax Withholding Rules for Nonresident Aliens Service Request Detail Design Document for Phase 1.

RELEASE 1721 New Federal Tax Withholding Rules for Nonresident Aliens Service Request 81561 Detail for Phase 1 Application Technology Services Information Resources & Communications Office of the President

RELEASE 1721 New Federal Tax Withholding Rules for Nonresident Aliens Service Request 81561 Detail for Phase 1 Application Technology Services Information Resources & Communications Office of the President

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

RUTGERS POLICY. Responsible Executive: Senior Vice President for Finance and Administration

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

HCM Specialists User Group. May 10, 2018

HCM Specialists User Group May 10, 2018 Agenda Resource updates Hiring Payroll Transfers Terminations Payments to International Students/Scholars 2 3 Resource Updates Updated Resources Available 4 www.vanderbilt.edu

HCM Specialists User Group May 10, 2018 Agenda Resource updates Hiring Payroll Transfers Terminations Payments to International Students/Scholars 2 3 Resource Updates Updated Resources Available 4 www.vanderbilt.edu

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Office of International Services TAX WORKSHOP. Tax preparation for International Students and Scholars Tax Year 2018

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

INTERNATIONAL TAX. Presented by Fiscal Services

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

Employees: Employees may only access and complete Glacier after their arrival in the US.

Administrator 3 View General Information and Getting Started Administrator is the term Glacier uses to describe departmental level access. The Payroll Office will provide Administrator 3 access to the

Administrator 3 View General Information and Getting Started Administrator is the term Glacier uses to describe departmental level access. The Payroll Office will provide Administrator 3 access to the

SCHEDULE OF EMPLOYER MATCHING CONTRIBUTION RATES (REVISED 7/1/2013)

") Section: 395-10 Supplement I Page 1 I RETIREMENT UCRP (1976 Tier) UCRP Supplemental Assessment 668600 668630 12.00% of covered wages (1) 0.66% of covered wages (1) 6.50% less $19.00/mo (6,7) Safety Class

Section: 395-10 Supplement I Page 1 I RETIREMENT UCRP (1976 Tier) UCRP Supplemental Assessment 668600 668630 12.00% of covered wages (1) 0.66% of covered wages (1) 6.50% less $19.00/mo (6,7) Safety Class

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS COMMON VISA TYPES AND THEIR TREATMENTS

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

SECTION C: Tax Manual I MISC

SECTION C: Tax Manual I. 1099-MISC The Internal Revenue Service requires a 1099-MISC form be issued to independent contractors, other individuals, LLCs, and unincorporated businesses that have received

SECTION C: Tax Manual I. 1099-MISC The Internal Revenue Service requires a 1099-MISC form be issued to independent contractors, other individuals, LLCs, and unincorporated businesses that have received

2012 Non-Resident Alien Tax Filings

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

International Students and Scholars Nonresident Tax Orientation. February 14, 2018

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

FOREIGN VISITOR TAX GUIDE

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

SCHEDULE OF EMPLOYER MATCHING CONTRIBUTION RATES (REVISED 1/1/2011)

") Section: 395-10 Supplement I Page 1 I RETIREMENT DCP-FICA 668600 5/1/2010 4.00% of covered wages (1) 2.00% of first 106,800 4.00% Thereafter less $19.00 a month. DCP-Summer Salary 668650 7/1/2010 3.50

Section: 395-10 Supplement I Page 1 I RETIREMENT DCP-FICA 668600 5/1/2010 4.00% of covered wages (1) 2.00% of first 106,800 4.00% Thereafter less $19.00 a month. DCP-Summer Salary 668650 7/1/2010 3.50

3. On the login screen, click the Login Now link or the system logo.

Overview For payments made to a foreign national, Harvard University utilizes a third-party system, called GLACIER Online Tax Compliance System, to calculate the tax withholding. This document provides

Overview For payments made to a foreign national, Harvard University utilizes a third-party system, called GLACIER Online Tax Compliance System, to calculate the tax withholding. This document provides

This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures.

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

INTERNATIONAL STUDENTS TAX WORKSHOP 2018

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Fellowships Toolkit:

Fellowships Toolkit: A Reference Guide to Fellowships, Reimbursements and Other Payments to U.S. Citizens and Non-Resident Aliens Office of the Controller January 1, 2015 Table of Contents INTRODUCTION:

Fellowships Toolkit: A Reference Guide to Fellowships, Reimbursements and Other Payments to U.S. Citizens and Non-Resident Aliens Office of the Controller January 1, 2015 Table of Contents INTRODUCTION:

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks Director, University Tax Services Financial Management Services Participant Outcomes Recognize when payment situations have

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks Director, University Tax Services Financial Management Services Participant Outcomes Recognize when payment situations have

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

F-1 or J-1 Student ITIN Applications. International Student & Scholar Services (ISSS)

") F-1 or J-1 tudent ITIN Applications International tudent & cholar ervices (I) In This Presentation ITIN Eligibility Application Process Contacts ITIN Eligibility What is an ITIN? ITIN = Individual Taxpayer

F-1 or J-1 tudent ITIN Applications International tudent & cholar ervices (I) In This Presentation ITIN Eligibility Application Process Contacts ITIN Eligibility What is an ITIN? ITIN = Individual Taxpayer

Education, Taxes, & Benefits. Duke University August 22, 2017

Education, Taxes, & Benefits Duke University August 22, 2017 Megan Hutchinson, CPA Senior Manager - Tax Raleigh Office DISCUSSION POINTS TYPES OF INCOME TAXABLE v NON-TAXABLE QUALIFIED v NON-QUALIFIED

Education, Taxes, & Benefits Duke University August 22, 2017 Megan Hutchinson, CPA Senior Manager - Tax Raleigh Office DISCUSSION POINTS TYPES OF INCOME TAXABLE v NON-TAXABLE QUALIFIED v NON-QUALIFIED

Service Request Update Tax Treaty Income Code and Tax treaty Income Code-Alternate. Technical Specification

Service Request 101131 Update Tax Treaty Income Code and Tax treaty Income Code-Alternate Prepared by Mary Meyer Information Technology Services Office of the President University of California Version

Service Request 101131 Update Tax Treaty Income Code and Tax treaty Income Code-Alternate Prepared by Mary Meyer Information Technology Services Office of the President University of California Version

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

Supplier Information Form Instructions

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

INDEPENDENT CONTRACTORS

Responsible University Administrator: Vice President for Finance and Administration Responsible Officer: Director of the Office of Budget and Tax Compliance Origination Date: N/A Current Revision Date:

Responsible University Administrator: Vice President for Finance and Administration Responsible Officer: Director of the Office of Budget and Tax Compliance Origination Date: N/A Current Revision Date:

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

PLEASE PRESS *6 ON YOUR PHONE TO MUTE

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

AMHERST COLLEGE Office of Financial Aid

AMHERST COLLEGE Office of Financial Aid B-5 Converse Hall P.O. Box 5000 Telephone (413) 542-2296 Amherst, Massachusetts 01002-5000 Facsimile (413) 542-2628 M E M O R A N D U M DATE: February 2009 TO: International

AMHERST COLLEGE Office of Financial Aid B-5 Converse Hall P.O. Box 5000 Telephone (413) 542-2296 Amherst, Massachusetts 01002-5000 Facsimile (413) 542-2628 M E M O R A N D U M DATE: February 2009 TO: International

I. Policy: All other University Finance policies and procedures apply in addition to those stated in this document.

Page 1 of 5 Subject: Applies to: Payments to Foreign Nationals (except salary/wage payments) For information regarding Employment of Foreign Nationals please see Personnel Policy 124: http://www.rochester.edu/working/hr/policies/pdfpolicies/124.pdf.

Page 1 of 5 Subject: Applies to: Payments to Foreign Nationals (except salary/wage payments) For information regarding Employment of Foreign Nationals please see Personnel Policy 124: http://www.rochester.edu/working/hr/policies/pdfpolicies/124.pdf.

1 Introduction Work Authorization Taxpayer Identification Numbers... 2

1 Introduction... 1 1.1 Work Authorization... 1 1.2 Taxpayer Identification Numbers... 2 2 U.S. Tax Residency Rules... 3 2.1 Residency Status Based on U.S. Presence... 3 2.2 U.S. Days That Do Not Count...

1 Introduction... 1 1.1 Work Authorization... 1 1.2 Taxpayer Identification Numbers... 2 2 U.S. Tax Residency Rules... 3 2.1 Residency Status Based on U.S. Presence... 3 2.2 U.S. Days That Do Not Count...

Global Mobility of Employees: Practical Strategies

Global Mobility of Employees: Practical Strategies Tax Executives Institute Carolinas Chapter Charlotte, NC Jodi Epstein (202) 662-3468 JEpstein@ipbtax.com Douglas Andre (202) 662-3471 DAndre@ipbtax.com

Global Mobility of Employees: Practical Strategies Tax Executives Institute Carolinas Chapter Charlotte, NC Jodi Epstein (202) 662-3468 JEpstein@ipbtax.com Douglas Andre (202) 662-3471 DAndre@ipbtax.com

Table of Contents. Table of Contents 1. AP Information 2. Foreign Nationals Definitions 3-4. Policy Overview 5. What to Ask 6 10

Table of Contents Table of Contents 1 AP Information 2 Foreign Nationals Definitions 3-4 Policy Overview 5 What to Ask 6 10 Example Documents 11 14 Papers, Papers, and More Papers 15 Payment Information

Table of Contents Table of Contents 1 AP Information 2 Foreign Nationals Definitions 3-4 Policy Overview 5 What to Ask 6 10 Example Documents 11 14 Papers, Papers, and More Papers 15 Payment Information

Garnett-Powers & Associates, Inc. University of Southern California Postdoctoral Scholar Benefit Program

Garnett-Powers & Associates, Inc. University of Southern California Postdoctoral Scholar Benefit Program Frequently Asked Questions (FAQ) Garnett-Powers & Associates, Inc. California Insurance License:

Garnett-Powers & Associates, Inc. University of Southern California Postdoctoral Scholar Benefit Program Frequently Asked Questions (FAQ) Garnett-Powers & Associates, Inc. California Insurance License:

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

15. Special Rules for Various Types of Services and Payments

15. Special Rules for Various Types of Services and Payments Section references are to the Internal Revenue Code unless otherwise noted. Special Classes of Employment and Income Tax ing Aliens, nonresident.

15. Special Rules for Various Types of Services and Payments Section references are to the Internal Revenue Code unless otherwise noted. Special Classes of Employment and Income Tax ing Aliens, nonresident.

Disbursement Services Guide

Disbursement Services Guide This document is intended to guide the campus community in understanding the protocol and services provided within the Disbursements department for the Office of Accounting

Disbursement Services Guide This document is intended to guide the campus community in understanding the protocol and services provided within the Disbursements department for the Office of Accounting

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

LESSON Recording A Payroll. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

LESSON 13-1 Recording A Payroll 2 PAYROLL REGISTER page 369 Use the payroll register to record the payment of the payroll. The payment of the payroll is recorded in the cash payments journal. LESSON 13-1

LESSON 13-1 Recording A Payroll 2 PAYROLL REGISTER page 369 Use the payroll register to record the payment of the payroll. The payment of the payroll is recorded in the cash payments journal. LESSON 13-1

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Withholding Requirements. Foreign Citizen / Residents Who Sell US / California Property By: Michael W. Brooks, Esq.

Tax Withholding Requirements for Foreign Citizen / Residents Who Sell US / California Property By: Michael W. Brooks, Esq. DI R E C T S Domestic and International Real Estate Closing Tax Services local:

Tax Withholding Requirements for Foreign Citizen / Residents Who Sell US / California Property By: Michael W. Brooks, Esq. DI R E C T S Domestic and International Real Estate Closing Tax Services local:

NEW VENDOR REQUEST NEW VENDOR INFORMATION INTERNATIONAL VENDOR REQUEST INDIVIDUAL

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

Personal Demographic Information

New Revised Office of Human Resources Personal Demographic Information (to be completed by employee) Your name as it should appear in the OSU directory: * Last Name First Name MI (optional) Your name as

New Revised Office of Human Resources Personal Demographic Information (to be completed by employee) Your name as it should appear in the OSU directory: * Last Name First Name MI (optional) Your name as

Addendum: An addition to an existing document, such as additional terms or a modification of terms.

Research Corporation of the University of Hawai i 2.002 Definitions Accountable Plan: A business reimbursement expense plan for the payment of business expenses incurred by a service provider (such as

Research Corporation of the University of Hawai i 2.002 Definitions Accountable Plan: A business reimbursement expense plan for the payment of business expenses incurred by a service provider (such as