U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

|

|

|

- Annabel Dorsey

- 5 years ago

- Views:

Transcription

1 U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

2 Workshop Objectives To review U.S. tax filing requirements for international students and scholars Determination of residency status Filing required Form 8843 Statement for Exempt Individuals Tax treatment of scholarships, fellowships, stipends, and other income Filing Form 1040NR U.S. Nonresident Alien Income Tax Return Effect of tax treaties

3 Target Audience Students with F-1 or J-1 visas who have been in the U.S. for five years or less Scholars with J-1 visas who have been in the U.S. for two years or less

4 Internal Revenue Service Agency of the United States Department of Treasury Enforcement of Internal Revenue Code Nation s tax collection agency Process income tax and other information returns

5

6 U.S. Tax Overview United States taxes individuals based on their residency status U.S. Citizens and Resident Aliens Taxed on worldwide income Nonresident Aliens Taxed only on U.S. source income Individuals report income earned on calendar year basis (January through December)

Individuals who fail to meet the above")

7 Determination of Residency Status Resident Aliens Substantial Presence Test Green Card Test First-Year Choice Election Nonresident Aliens ( NRA ) Individuals who fail to meet the above residency standards

8 Substantial Presence Test Days physically present in the U.S. 31 days during the year (2016); and At least 183 days during the last three years (2016, 2015, and 2014) Counting number of days for 2016: all days in /3 of your days in /6 of your days in 2014 Example: Jane spent 100 days in the US in 2016, 180 days in the US in 2015, and 180 days in the US in Jane s number of days in the US for the substantial presence test is 100 days for days for 2015 (180 days x 1/3) + 30 days for 2014 (180 days x 1/6) for a total of 190 days. Does Jane meet the substantial presence test for 2016?

9 Substantial Presence Test Exception for students, scholars, teachers, and trainees considered exempt individuals Days are not counted toward the 183 days when present in the U.S. while under an F, J, M, or Q visa Exception discussed in detail later

issues an alien registration card Resident status continues until you")

10 Green Card Test Lawful Permanent Resident U.S. Citizenship and Immigration Service (USCIS) issues an alien registration card Resident status continues until you voluntarily abandon this status or if a federal court terminates your status

11 First-Year Choice Election Must be present for at least 31 consecutive days in 2016 and be present for at least 75% of the number of days beginning with the first day you re in the U.S. and ending with December 31st Election can be made by attaching a statement to your tax return Once you make this election, it cannot be revoked

12 Form 8843: Statement for Exempt Individuals and Individuals with a Medical Condition Explains basis for claim of excluding days of presence in the U.S. for purposes of the substantial presence test Must be filed annually with the IRS Filed with income tax return (Form 1040NR or 1040NR-EZ) If not filing a return, Form 8843 must be filed separately Failure to file could result in being considered a U.S. resident under the substantial presence test

13 Exempt Individuals Students and scholars Individual who is temporarily present in the U.S. under an F, J, M, or Q visa Must also substantially comply with the requirements of the visa Generally, cannot claim the exception if you were previously exempt as a student, teacher, or trainee for more than five years

14 Exempt Individuals Teachers, trainees, and researchers Individual who is temporarily present in the U.S. under a J or Q visa (other than as a student) Must also substantially comply with the requirements of the visa Generally, cannot exclude days if you were exempt as a teacher, trainee, or student for any part of two of the six prior years

15 Exempt Individuals and Form 8843 Students and scholars Part I General Information Part III Student Information If you have a Q visa, complete Part I and ONLY lines of Part III Teachers, trainees, and researchers Part I General Information Part II Teacher/Trainee/Researcher Information If you have a Q visa, complete Part I and ONLY lines 6-8 of Part II

16 Spouse & Dependent Form 8843 Filing Requirements Spouses and dependents with F-2 visas must file their own Form Spouses and dependents with J-2 visas must file their own Form 8843 and either Form 1040NR or Form 1040NR-EZ.

17 Form 8843, Part I: General Information

18 Form 8843, Part II: Teachers and Trainees

19 Form 8843, Part III: Students

20 Form 8843, Signature Line You must sign and date Form 8843 if submitting this form alone (i.e. without your tax return). Without your signature, the form is considered incomplete.

21 U.S. Income: Scholarships and Fellowships Generally, no work is required Nontaxable ( tuition waiver ) The student is pursuing a degree AND Used for tuition, fees, books, supplies and equipment required for courses No longer required to be reported on Form 1042-S (issued by University)

22 U.S. Income: Scholarships and Fellowships Generally, no work is required Taxable ( room and board waiver ) Used for room & board In exchange for teaching or research Can be exempted by tax treaty Reported on Form 1042-S (issued by University)

23 Form 1042-S: Foreign Person s U.S. Source Income Subject to Withholding

24 U.S. Income: Stipend Generally, recipient performs work Taxable ( Teaching or Research Assistant Stipend) May be eligible for treaty benefits Reported on Form W-2

25 U.S. Income: Other Compensation Work outside the University Taxable wages performance of services as an employee Reported on Form W-2 Subject to U.S. tax withholding May have exemption from withholding under a tax treaty (discussed in detail later)

26 Form W-2: Wage and Tax Statement

27 Form 1099-MISC: Miscellaneous Income

28 Form 1098-T: Tuition Statement

29 Form 1095-B: Health Coverage -Informational form issued by insurance provider that shows the IRS a person has health insurance -Health insurance is not a requirement for nonresident taxpayers

30 Form 1095-C: Employer-Provided Health Insurance Offer & Coverage -Informational form issued by employer that shows the IRS a person has health insurance -Health insurance is not a requirement for nonresident taxpayers

31 Filing Requirement Individual Tax Returns Only required if you have U.S. Source Income that was more than $4,050 in 2016 and/or You would like to claim a refund of over-withheld taxes Now able to submit 1040NR electronically ( e-file ) Form 1040NR paper file or e-file Due date for filing is April 18, 2017 Form 1040NR-EZ paper file Due date for filing is April 18, 2017

32 Individual Tax Returns If you are paper filing, attach Form W-2 and/or Form 1042-S to your tax return. You must sign and date your tax return. Without your signature, your return is considered incomplete. Below is the signature line on Form 1040NR.

33 Form 1040NR-EZ: U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Who can file Form 1040NR-EZ? Do not claim any dependents Taxable income is less than $100,000 Do not claim any itemized deductions Except state and local income taxes Receive only wages, tips and scholarship or fellowship grants Other reasons (see Publication 519 or Form 1040NR-EZ instructions)

34 Form 1040NR: U.S. Nonresident Alien Income Tax Return Who should file Form 1040NR? Nonresident aliens who do not qualify to file Form 1040NR-EZ Spousal/dependency exemptions Generally cannot be claimed by nonresident aliens

35 Form 1040NR: U.S. Nonresident Alien Income Tax Return Exceptions Available spousal exemptions Married individuals from Canada, Mexico or South Korea Married individuals who are students and are from India Exceptions Available dependency exemptions Individuals from Canada, Mexico or South Korea can claim children who live with them as dependents Individuals from Canada and Mexico can also claim children who do not live with them as dependents Students from India may be able to claim exemptions for children born in the U.S.

36 Form 1040NR: U.S. Nonresident Alien Income Tax Return What if you are married and you don t qualify for any spousal exemptions? Check the applicable box below on the tax return you qualify to file. Form 1040NR-EZ or Form 1040NR

37 Updates to Form 1040NR You can now file Form 1040NR electronically (e-file) beginning with 2016 (unable to e-file 2015 and earlier). There is a new option for taxpayers whose only option is to pay their taxes in cash. Visit for more information.

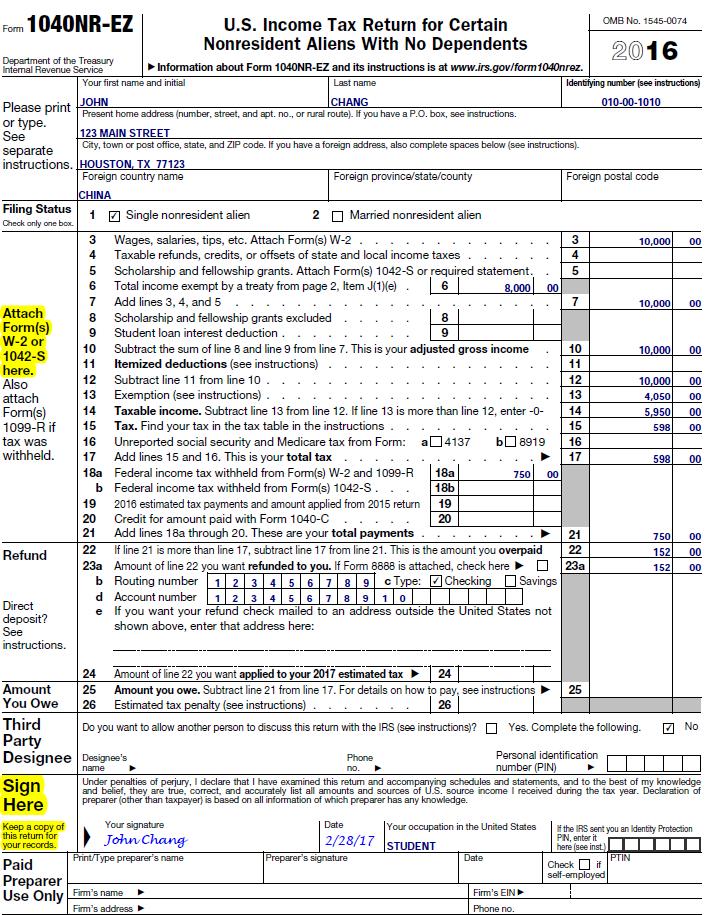

38 Form 1040NR-EZ

39 Form 1040NR (page 1)

40 Form 1040NR (page 2)

41 Form 1040 NR (Itemized Deductions)

42 Form 1040 NR (Schedule NEC)

43 Form 1040NR (Schedule OI)

44 Tax Treaties Under tax treaties, residents of foreign countries are taxed at a reduced rate or are exempt from U.S. income taxes on certain types of U.S. sourced income. There are over 60 tax treaties in place. See IRS Publication 901: U.S. Tax Treaties Relevant forms Form 8233: Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual Form W-8BEN: Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting

45 Form 8233 (page 1)

46 Form 8233 (page 2)

47 Form W-8BEN

48 U.S.-People s Republic of China ARTICLE 20 Students and Trainees Income Tax Treaty A student, business apprentice or trainee who is, or was immediately before visiting a Contracting State ( U.S. ), a resident of the other Contracting State ( China ) and who is present in the first-mentioned Contracting State ( U.S. ) solely for the purpose of his education, training or obtaining special technical experience shall be exempt from tax in that Contracting State ( U.S. ) with respect to: a) payments received from abroad for the purposes of his maintenance, education, study, research or training; b) grants or awards from a government, scientific, educational or other tax-exempt organization; and c) income from personal services performed in that Contracting State (U.S) in an amount not in excess of 5,000 United States dollars or its equivalent in Chinese Yuan for any taxable year. The benefits provided under this Article shall extend only for such period of time as is reasonably necessary to complete the education or training. Note: This is only an excerpt of the U.S.-China tax treaty.

49 Social Security & Medicare Taxes Generally, services performed by a nonresident alien temporarily in the U.S. as a nonimmigrant in F, J, M, or Q immigration status are not covered under the social security program if the services are performed to carry out the purpose for which you were admitted to the U.S. This means that there will be no withholding of Social Security or Medicare taxes from the pay you receive for these services Exemption from FICA (Social Security and Medicare taxes) If resident for tax purposes, usually subject to FICA taxes

50 Social Security & Medicare Taxes Form 843 Form 843: Claim for Refund and Request for Abatement When withheld in error: Ask the employer to refund If not refunded, use IRS Form 843 to request a refund Required attachments: Copy of W-2 and a letter from employer stating refund will not be issued

51 Form 843 SEE UPDATED FORM!

52 Example of 1040NR-EZ John Chang, a Chinese student, has the following items to report on his 1040NR-EZ: Works on campus at a restaurant and receives Form W-2 for $10,000 compensation earned Receives Form W-2 for a stipend in the amount of $5,000 as a research assistant Receives Form 1042-S for a teaching scholarship in the amount of $3,000

53 Form W-2: Compensation

54 Form W-2: Stipend

55 Form 1042-S: Taxable Scholarship

56

57

58 Tax Tables are included in the instructions for Form 1040NR & Form 1040NR-EZ Tax Table

59 Key Points Form 8843 must be filed regardless if an individual income tax return is filed. If you are required to file Form 1040NR/NR-EZ, attach Form 8843 to return and file by April 18, If filing Form 8843 on its own, the due date is April 18, Mailing/filing address for Form 8843: Department of the Treasury Internal Revenue Service Center Austin, TX Make sure to sign and date Form 8843 and/or Form 1040NR, or else the form is considered incomplete. Attach Form W-2 and/or Form 1042-S to your tax return.

60 Key Points Form 1040NR/1040NR-EZ is due April 18, Mailing/filing address for returns with no tax due or overpayment: Department of the Treasury Internal Revenue Service Austin, TX Mailing/filing address for returns with tax due: Internal Revenue Service P.O. Box 1303 Charlotte, NC Retain a copy of your tax return Now able to submit 1040NR electronically ( e-file )

61 Reference Guide: Common Forms Form 8843: Statement for Exempt Individuals and Individuals With a Medical Condition Form 1042-S: Foreign Person s U.S. Source Income Subject to Withholding Form W-2: Wage and Tax Statement Form 1098-T: Tuition Statement Form 1040NR-EZ: U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Form 1040NR: U.S. Nonresident Alien Income Tax Return Form 8233: Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual Form W-8BEN: Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting Form 843: Claim for Refund and Request for Abatement

62 Reference Guide: Definitions and Terminology Nonresident Alien: Generally, any person who is not a U.S. citizen or resident alien Student: Person temporarily in the U.S. on an F, J, M, or Q visa Teacher/trainee: Person who is not a student & who is temporarily in the U.S. on a J or Q visa Compensation/Earnings: Wages, salaries, tips Income: Wages, salaries, tips, interest, dividends, some scholarship/fellowship grants IRS: Internal Revenue Service Income Tax Return: Statement filed (submitted) by individual taxpayer to the IRS reporting taxable income

63 Reference Guide: Definitions and Terminology Withholding: U.S. income tax automatically taken from your paycheck U.S. Source Income: All income, gain or loss from U.S. sources Standard Deduction: Standard amount that individuals may subtract from income before calculating taxes owed Itemized Deductions: Allowable amounts that individuals may subtract from income before calculating taxes owed Examples: charitable contributions, state & local taxes withheld, etc. Note: No one can have both a standard deduction and itemized deductions. Itemized deductions are only taken if the total exceeds the standard deduction. Personal Exemption: Amount deducted from income for yourself and/or spouse/dependent (generally nonresidents cannot claim spouse/dependent) For 2016, exemption amount is $4,050.

64 Reference Guide Helpful sites and contact information Internal Revenue Service ( Forms and Instructions available IRS Toll Free Number 1-(800) IRS International Taxpayer Service Call Center (267) Useful resources Publication 519 U.S. Tax Guide for Aliens Publication 901 U.S. Tax Treaties

65 Thank you for attending!

66 Briggs & Veselka Co. Crystal C. Gates, CPA Crystal works closely with multinational companies and their owners in providing both domestic and international tax planning, consulting and compliances services. Her broad experience enables her to provide comprehensive value-added services with an emphasis on efficient tax structure, risk management and facilitating successful growth for a client s business at home and abroad. Crystal has worked with firms throughout the world through her global network of professional services firms. She focuses on building a team of quality in-country advisors and specialists to collaborate in providing the best strategies for her clients in navigating the global marketplace. In her 15 year career, she has focused her practice on middle market entrepreneurial companies working side by side with business owners in growing their businesses both domestically and abroad. Crystal s experiences include: Developing and managing a substantial international tax practice for a top 10 local accounting practice in Denver, Colorado, serving domestic and multinational middle-market and large companies. Collaborating with in-country tax advisors in all the major global regions (North and South America, Asia, Europe, Australia and Africa) to enable global U.S. business owners to effectively manage domestic and international tax positions. Advising clients on the growth of their businesses through sophisticated tax planning including operations, mergers and acquisitions, and business succession. Working efficiently with various types of business structures from start-up companies to large multinational enterprises, consolidated groups, U.S. flow through entities and high net-worth individuals. Crystal received a B.A. in Accounting from University of Colorado and a Masters of Taxation from the University of Denver. She is member of the AICPA and Colorado Society of CPAs. Crystal has authored and presented at various tax seminars providing continuing professional education on topics ranging from federal tax updates, IRS controversy and civil procedure and international taxation.

67 Briggs & Veselka Co. Kelley C. Heng, CPA Kelley started her public accounting career with Briggs & Veselka in 2009, and she works with high net worth clients in the tax department. She has experience with federal and state tax returns for individuals, trusts, partnerships, S corporations, and private foundations. She was born and raised in Houston. Her prior work experience consists of working in retail and working in the accounting and finance department of a financial services firm. Kelley received a B.B.A. in Accounting from the University of Houston in December Kelley is a Texas licensed Certified Public Accountant (CPA). She is a member of the American Institute of CPAs and the Texas Society of CPAs. Kelley is a member of the CPAs Helping Schools committee and the Accounting Career Education committee with the Houston CPA Society.

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Foreign Student and Scholar Volunteer Tax Return Preparation. VITA Training 1

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

2012 Non-Resident Alien Tax Filings

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

INTERNATIONAL STUDENTS TAX WORKSHOP 2018

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

TAX FILING FOR STUDENTS AND SCHOLARS 101. Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Frequently Asked Tax Questions 2018 Tax Returns

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room Presented by:

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

International Students and Scholars Nonresident Tax Orientation. February 14, 2018

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR

Session 2017 Tax Year Georgia Form 500 with Form 1040NR") Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500

Session 2015 Tax Year GA Form 500") Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS COMMON VISA TYPES AND THEIR TREATMENTS

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

Your Federal Income Tax Responsibilities as an Au Pair

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

2016 Publication 4011

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

Instructions for Form 1040NR-EZ

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

International Student Taxes. Information compiled by International Student Services

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

University of Utah Payments to Non Resident Aliens

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

Basic Tax Information for F and J Immigration Status

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

International Student Taxes

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

Office of International Services TAX WORKSHOP. Tax preparation for International Students and Scholars Tax Year 2018

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

Office of International Services TAX WORKSHOP Tax preparation for International Students and Scholars Tax Year 2018 Office of International Services OVERVIEW Introductions What are Taxes? Tax Forms Sprintax

SUBJECT: Payments to Nonresident Aliens

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

U.S. Nonresident Alien Income Tax Return

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes. Download Slides here: https://goo.gl/q1tigg

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

U.S. Nonresident Alien Income Tax Return

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

Subject: IMPORTANT TAX INFO FOR INTERNATIONAL STUDENTS FOR TAX YEAR 2018

Subject: IMPORTANT TAX INFO FOR INTERNATIONAL STUDENTS FOR TAX YEAR 2018 WHAT: Mandatory International Student Tax Requirements WHO: All international students and dependents WHEN: Tax Forms for Year 2018

Subject: IMPORTANT TAX INFO FOR INTERNATIONAL STUDENTS FOR TAX YEAR 2018 WHAT: Mandatory International Student Tax Requirements WHO: All international students and dependents WHEN: Tax Forms for Year 2018

U.S. Nonresident Alien Income Tax Return

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

U.S. Nonresident Alien Income Tax Return. Of what country were you a citizen or national during the tax year?

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6, 2019 1 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Wednesday March 6, 2019 1 Presenters Present Information: Chris Durham Assistant Director of HR/Payroll & Merchant Services Jodi Kessler

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

DISTRIBUTION OPTIONS GENERAL INFORMATION ABOUT ROLLOVERS

PLUMBERS LOCAL UNION NO. 68 PLAN OF DEFINED CONTRIBUTION BENEFITS P.O. Box 8726 Houston, Texas 77249 713.869.2592 Fax: 713.862.4877 Toll Free: 800.833.2980 DISTRIBUTION OPTIONS You are receiving this notice

PLUMBERS LOCAL UNION NO. 68 PLAN OF DEFINED CONTRIBUTION BENEFITS P.O. Box 8726 Houston, Texas 77249 713.869.2592 Fax: 713.862.4877 Toll Free: 800.833.2980 DISTRIBUTION OPTIONS You are receiving this notice

MICHIGAN DEPARTMENT OF TREASURY

MICHIGAN DEPARTMENT OF TREASURY 2015 To explain Michigan filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other

MICHIGAN DEPARTMENT OF TREASURY 2015 To explain Michigan filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other

Federal Tax Information Session For International Scholars

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

~E~ E-3 visa, 103 Earnings statement, 100, 131, 135, 136,

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Tax information. International Students in the United States

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

Tax Reporting for Inbound Students

Tax Reporting for Inbound Students March 9, 2018 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Taxation Resident vs. Nonresident Resident - Taxed on worldwide income - Allowed worldwide deductions

Tax Reporting for Inbound Students March 9, 2018 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Taxation Resident vs. Nonresident Resident - Taxed on worldwide income - Allowed worldwide deductions

Nonresident Aliens. Resident Alien. Are you a resident alien? Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns

Nonresident Aliens Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns Resident Alien Are you a resident alien? A resident alien is generally taxed in the same way as U.S. citizens You

Nonresident Aliens Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns Resident Alien Are you a resident alien? A resident alien is generally taxed in the same way as U.S. citizens You

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Form 1040NR Filing Challenges and Effective Approaches

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

RUTGERS POLICY. Responsible Executive: Senior Vice President for Finance and Administration

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

West Chester University. Taxation Issues Nonresident Aliens

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

Nonresident Alien Tax Compliance

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

OFFICIAL POLICY. Policy Statement

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax ComplianceAnalyst

2017 Tax Return Overview for International Students

2017 Tax Return Overview for International Students This quick guide is provided for international students to become familiar with U.S. Tax return filings. Tax returns are due April 17, 2018 for students

2017 Tax Return Overview for International Students This quick guide is provided for international students to become familiar with U.S. Tax return filings. Tax returns are due April 17, 2018 for students

Tax Reporting for Inbound Students

Tax Reporting for Inbound Students March 10, 2017 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Tax Residence 101 Defined in Internal Revenue Code (IRC) Section 7701(b) - Determined based on

Tax Reporting for Inbound Students March 10, 2017 www.moorestephensdm.com PRECISE. PROVEN. PERFORMANCE. US Tax Residence 101 Defined in Internal Revenue Code (IRC) Section 7701(b) - Determined based on

AMHERST COLLEGE Office of Financial Aid

AMHERST COLLEGE Office of Financial Aid B-5 Converse Hall P.O. Box 5000 Telephone (413) 542-2296 Amherst, Massachusetts 01002-5000 Facsimile (413) 542-2628 M E M O R A N D U M DATE: February 2009 TO: International

AMHERST COLLEGE Office of Financial Aid B-5 Converse Hall P.O. Box 5000 Telephone (413) 542-2296 Amherst, Massachusetts 01002-5000 Facsimile (413) 542-2628 M E M O R A N D U M DATE: February 2009 TO: International

DO NOT FILE THIS FORM IN 2019 WITH YOUR TAX RETURN

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

MICHIGAN DEPARTMENT OF TREASURY

MICHIGAN DEPARTMENT OF TREASURY 2013 To explain the filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other Michigan

MICHIGAN DEPARTMENT OF TREASURY 2013 To explain the filing requirements Who must file a Michigan Income Tax Return (MI-1040) Give instructions and guidelines on how to complete the MI-1040 and other Michigan

State Tax Issues for Non - Resident Scholars and Researchers

State Tax Issues for Non - Resident Scholars and Researchers Agenda 2 California Residency Laws Items taxed by California Taxation of fellowships, stipends and scholarships State & Federal Differences

State Tax Issues for Non - Resident Scholars and Researchers Agenda 2 California Residency Laws Items taxed by California Taxation of fellowships, stipends and scholarships State & Federal Differences

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Taxability of Prizes and Awards President s Engagement Prizes. December 9, Office of the Comptroller

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

Overview of Taxation for Students

Overview of Taxation for Students Disclaimer This session has been created under the premises of the Volunteer Income Tax Assistance Program (VITA), a program of the Internal Revenue Service. In offering

Overview of Taxation for Students Disclaimer This session has been created under the premises of the Volunteer Income Tax Assistance Program (VITA), a program of the Internal Revenue Service. In offering

Nonresident Alien Federal Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien State of Hawaii Tax Workshop

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Princeton University International Undergraduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 2, 2011

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

A Guide to US Federal Income Tax for F & J Visa Holders: Part Two

A Guide to US Federal Income Tax for F & J Visa Holders: Part Two Introduc?on The University of Michigan provides its F & J visa holders with free access to the user- friendly tax form comple>on so?ware,

A Guide to US Federal Income Tax for F & J Visa Holders: Part Two Introduc?on The University of Michigan provides its F & J visa holders with free access to the user- friendly tax form comple>on so?ware,

Completing IRS Form 1040NR-EZ for 2015

Completing IRS Form 1040NR-EZ for 2015 Note: If you had income other than wages and taxable scholarship (e.g., interest, dividends, capital gains), you must complete Form 1040NR, rather than Form 1040NR-EZ.

Completing IRS Form 1040NR-EZ for 2015 Note: If you had income other than wages and taxable scholarship (e.g., interest, dividends, capital gains), you must complete Form 1040NR, rather than Form 1040NR-EZ.

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

U.S. Taxation for International Students. by Sau-Wing Lam

U.S. Taxation for International Students by Sau-Wing Lam January 2018 Resident Alien or Non-Resident Alien? In American taxation there is a difference between a resident alien and a non-resident alien.

U.S. Taxation for International Students by Sau-Wing Lam January 2018 Resident Alien or Non-Resident Alien? In American taxation there is a difference between a resident alien and a non-resident alien.

IRS Federal Income Tax Publications provided by efile.com

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM. Glacier Guide for Departments

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

INTERNATIONAL TAX. Presented by Fiscal Services

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

Domestic Tax Issues for Non-resident Aliens

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

Paying Your Income Taxes. Advanced Level

Paying Your Income Taxes Advanced Level What are taxes? A sum of money demanded by a government for support of itself and specific programs and services; paid by taxpayers Take Charge Today February 2017

Paying Your Income Taxes Advanced Level What are taxes? A sum of money demanded by a government for support of itself and specific programs and services; paid by taxpayers Take Charge Today February 2017

Webinar Tax Treatment for Scholarships and Fellowships

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return LEE F DUT X. MN Foreign province/county

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

Date: March 24, A.P.EX. ProAuPair's US Based Professional Au Pairs. From: Tim Johnson, CPA JLK Rosenberger, LLP

Date: March 24, 2018 To: A.P.EX. ProAuPair's US Based Professional Au Pairs From: Tim Johnson, CPA JLK Rosenberger, LLP Re: Basic US Tax Treatment of Au Pairs The below information is meant to be general

Date: March 24, 2018 To: A.P.EX. ProAuPair's US Based Professional Au Pairs From: Tim Johnson, CPA JLK Rosenberger, LLP Re: Basic US Tax Treatment of Au Pairs The below information is meant to be general

Foreign Tax Issues REBECCA DONEHEW

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Equivalent Appendix How To Get Tax Help... 27

Department of the Treasury Internal Revenue Service Contents Reminder... 1 Introduction... 1 Publication 915 Are Any of Your Benefits Taxable?... 2 Cat. No. 15320P How To Report Your Benefits... 5 Social

Department of the Treasury Internal Revenue Service Contents Reminder... 1 Introduction... 1 Publication 915 Are Any of Your Benefits Taxable?... 2 Cat. No. 15320P How To Report Your Benefits... 5 Social

Princeton University International Graduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 9, 2011

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid