The Relocation Appraisal Training Program

|

|

|

- Damon Pearson

- 6 years ago

- Views:

Transcription

1 The Relocation Appraisal Training Program Module 3 Developing the Market Change and Forecasting Adjustments in a Relocation Appraisal

2 Today s Instructor Arnold M. Schwartz, SCRP, SRA, Arnold M. Schwartz & Associates, Atlanta Georgia Welcome and Introduction

3 Course Objectives Understand normal marketing time and how it is calculated Understand the market change adjustment and how it is calculated Understand the forecasting adjustment and how it is calculated Apply the market change and forecasting adjustments in the relocation appraisal The Relocation Appraisal Training Program Module 1 Concepts in Relocation Appraising Module 2 The Worldwide ERC Summary Appraisal Report: An Overview Module 3 Developing the Market Change and Forecasting Adjustments in a Relocation Appraisal

4 Development of Estimated Normal Marketing Time for Subject Property and Market Segment Determining Market Segment Normal Marketing Time Two Step Process Step 1: Investigate the actual marketing time (days on market) of sold properties (both closed and under contract), as well as the current days on market of available competitive listings. (Marketing time is measured from listing date to contract date.) Step 2: Consider any transitional or developing market trends and their anticipated impact on this projection of normal marketing time.

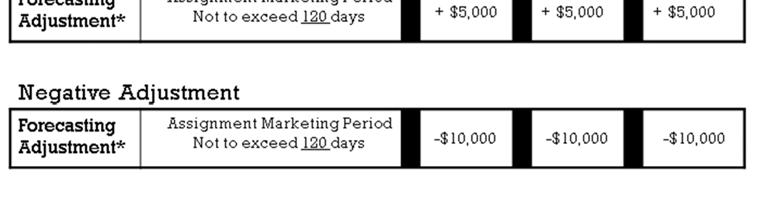

5 Marketing Time Market Trends Analysis

6 Market Trends Analysis Market Trends Analysis

7 Market Trends Analysis Market Trends Analysis

8 Market Trends Analysis Market Trends Analysis Estimated Normal Marketing Time for Subject Property and Market Segment 180 Days

9 Marketing Time Market Change Overview

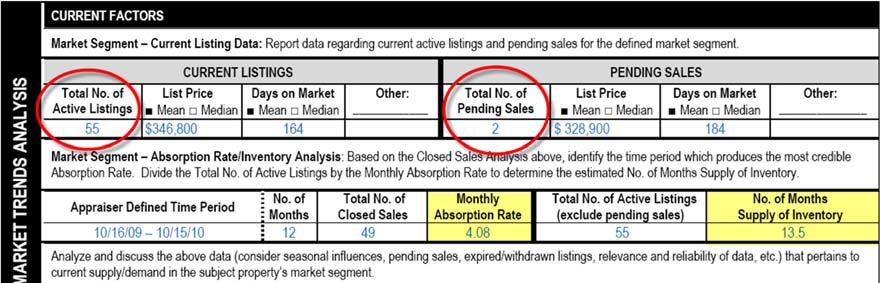

10 Price Change Analysis Price Change Analysis Prior 12 months 17.4% decline = 1.45% per month price decline Most Recent 12 months 18.7% decline = 1.56% per month price decline Overall price change analysis: 1.5% per month price decline

11 Sales Price Trend Sales Price Trend Comparable Sale # 1: $365,000 sale price / contract date 04/10/2010 Comparable Sale # 2: $348,500 sale price / contract date 07/20/2010 Difference - $16,500 3 months Calculate percentage difference: $16,500 $365,000 = 4.5% Price change: 4.5% 3 months = 1.5% per month price decline

12 Sales Price Trend Comparable Sale # 1: $365,000 sale price / contract date 04/10/2010 Comparable Sale # 3: $338,000 sale price / contract date 09/12/2010 Difference - $27,000 5 months Calculate percentage difference: $27,000 $365,000 = 7.4% Price change: 7.4% 5 months = 1.5% per month price decline Sales Price Trend Comparable Sale # 2: $348,500 sale price / contract date 07/20/2010 Comparable Sale # 3: $338,000 sale price / contract date 09/12/2010 Difference - $10,500 2 months Calculate percentage difference: $10,500 $348,500 = 3.0% Price change: 3.0% 2 months = 1.5% per month price decline

13 Sale/Resale Analysis Sale/Resale Analysis Comparable Sale # 1: Last sale date: 04/10/2008, Last sale price: $570,000 Closing date: 05/02/2010, Sales price: $365,000 Difference: 2 years -$205,000 Calculate percentage difference: $205,000 $570,000 = 36.0% (rounded) Price change: 36.0% 2 years = 18.0% per year or 1.5% per month price decline

14 Sale/Resale Analysis Comparable Sale # 2: Last sale date: 06/16/2008, Last sale price: $544,500 Closing date: 08/20/2010, Sales price: $348,500 Difference: 2 years -$196,000 Calculate percentage difference: $196,000 $544,500 = 36.0% (rounded) Price change: 36.0% 2 years = 18.0% per year or 1.5% per month price decline Sale/Resale Analysis Comparable Sale # 3: Last sale date: 08/01/2009, Last sale price: $412,000 Closing date: 10/10/2010, Sales price: $338,000 Difference: 1 year -$74,000 Calculate percentage difference: $74,000 $412,000 = 18.0% (rounded) Price change: 18.0% 1year = 18.0% per year or 1.5% per month price decline

15 Market Change Adjustment 1.5% per month price decline Market Trends Analysis

Contract Date for Comparable Sale #2: 07/20/2010 3 months at -1.5% per month = -4.")

16 Market Change Adjustment Date of Value Opinion 10/15/2010 Contract Date for Comparable Sale #1: 04/10/ months at -1.5% per month = -9% X $365,000 sales price = -$33,000 (rounded) Contract Date for Comparable Sale #2: 07/20/ months at -1.5% per month = -4.5% X $348,500 sales price = -$16,000 (rounded) Contract Date for Comparable Sale #3: 09/12/ month at -1.5% per month = -1.5% X $338,000 sales price = -$5,000 (rounded) Forecasting Adjustment

17 Forecasting Overview Forecasting Adjustment

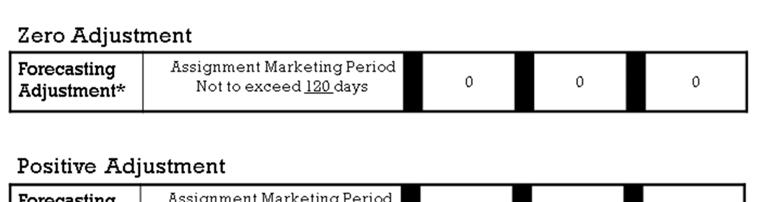

18 Forecasting Adjustment Consists of Two Components: Component One: Reflects the change in market conditions and prices anticipated between date of value opinion and end of subject property s estimated normal marketing time. Component Two: Applied to reflect any price reduction necessary to achieve sale within assignment marketing period. Forecasting Adjustment Component One Appraiser must develop the subject property s estimated normal marketing time that is presumed to being on the date of value opinion.

19 Forecasting Adjustment Component Two Applied when the subject property s estimated normal marketing time exceeds assignment marketing period and a price reduction is required to provide the incentive for a sale of the subject property within this shorter than normal marketing period. Factors to Consider When Estimating Amount of Forecasting Adjustment New construction competition Distressed property competition Interest rate trends Mood of the market Seasonal market trends Economic trends Employment Shifts Withdrawn listings Expired listings Demographic trends Buyer profile trends Subject property listing history

20 Forecasting Analysis Forecasting Analysis

>> Date of Value")

Price Reduction << (Component 2) 120 Days (Assignment")

21 Forecasting Analysis Forecasting Adjustment Contract Date of Comparable Sale Market Change Adjustment (Historical) >> Date of Value Opinion Forecasting Adjustment >> 180 Days (Normal Marketing Time) (Component 1) Price Reduction << (Component 2) 120 Days (Assignment Marketing Period)

22 Forecasting Adjustment Forecasting Adjustment

23 Forecasting Adjustment Adjusted Sales Price before Forecasting: $332,500 Subject Property s Competitive List Price: $304,900 Forecasting Adjustment Forecasting Adjustment: Component 1 Normal Marketing Time: 180 days (6 months) Component 2 Price Reduction: 60 days (2 months) Total Monthly Adjustment: 8 months X -1.5% per month = -12% Adjusted Sales Price before Forecasting = $332,500 $332,500 X -12% = -$40,000 (rounded)

24 Forecasting Adjustment Forecasting Adjustment

25 Forecasting Adjustment Forecasting Adjustment Adjusted Sales Price before Forecasting: $332,500 Subject Property s Competitive List Price: $304,900

Anticipated")

26 Forecasting Adjustment Market Segment Sales Price / List Price Ratio = 96% Subject Property / Competitive List Price: $304,900 X 96% = $292, 500 (rounded) Anticipated Sales Price

27 The Relocation Appraisal Training Program Module 1 Concepts in Relocation Appraising Module 2 The Worldwide ERC Summary Appraisal Report: An Overview Module 3 Developing the Market Change and Forecasting Adjustments in a Relocation Appraisal The Relocation Appraisal Guide

Proactive Mobility Solutions For A Reactive Real Estate Market. Worldwide ERC would like to thank today s sponsor:

Proactive Mobility Solutions For A Reactive Real Estate Market Worldwide ERC would like to thank today s sponsor: Date: Tuesday, July 24 2012 Worldwide ERC Welcome and Learning Zone Instructions Technical

Proactive Mobility Solutions For A Reactive Real Estate Market Worldwide ERC would like to thank today s sponsor: Date: Tuesday, July 24 2012 Worldwide ERC Welcome and Learning Zone Instructions Technical

May 31, 2018 Our thanks to today s sponsor:

May 31, 2018 Our thanks to today s sponsor: Top Real Estate Trends and their Impact to Your Relocation Program WORLDWIDE ERC WEBINAR DISCLAIMER The views, opinions, and information expressed during this

May 31, 2018 Our thanks to today s sponsor: Top Real Estate Trends and their Impact to Your Relocation Program WORLDWIDE ERC WEBINAR DISCLAIMER The views, opinions, and information expressed during this

Absorption Rate Pricing

Absorption Rate Pricing By Zan Monroe The Monroe Company, Inc. PO Box 58241 Fayetteville NC, 28305 1-910-860-4200 Zan@ZanMonroe.com Absorption Rate Pricing and Positioning Calculating Absorption Rate If

Absorption Rate Pricing By Zan Monroe The Monroe Company, Inc. PO Box 58241 Fayetteville NC, 28305 1-910-860-4200 Zan@ZanMonroe.com Absorption Rate Pricing and Positioning Calculating Absorption Rate If

Decision Power Express SM Training Module I. Accessing eport

Decision Power Express SM Training Module I Accessing eport Confidentiality / Non-Disclosure Confidentiality, non-disclosure, and legal disclaimer information The contents of this Decision Power Express

Decision Power Express SM Training Module I Accessing eport Confidentiality / Non-Disclosure Confidentiality, non-disclosure, and legal disclaimer information The contents of this Decision Power Express

May 8, :00 am EST Our thanks to today s sponsor:

May 8, 2018 11:00 am EST Our thanks to today s sponsor: 2018 Worldwide ERC Here Comes Moving Season: What You Need to Know to Prepare and Manage Your Move WORLDWIDE ERC WEBINAR DISCLAIMER The views, opinions,

May 8, 2018 11:00 am EST Our thanks to today s sponsor: 2018 Worldwide ERC Here Comes Moving Season: What You Need to Know to Prepare and Manage Your Move WORLDWIDE ERC WEBINAR DISCLAIMER The views, opinions,

I N V E S T M E N T S We have the resources to fund the largest transactions and we look at situations and opportunities that others might overlook. I

Accounts Receivable Purchasing, Appraisals, and Consulting I N V E S T M E N T S Unlocking THE VALUE IN YOUR RECEIVABLES I N V E S T M E N T S We have the resources to fund the largest transactions and

Accounts Receivable Purchasing, Appraisals, and Consulting I N V E S T M E N T S Unlocking THE VALUE IN YOUR RECEIVABLES I N V E S T M E N T S We have the resources to fund the largest transactions and

DU 9.1 Revisions and Other Agency Enhancements

Bankruptcies Products (non AUS & DU) If a public record does not indicate a bankruptcy, but an individual tradeline does, the borrower must meet these bankruptcy guidelines. Generally, bankruptcies (except

Bankruptcies Products (non AUS & DU) If a public record does not indicate a bankruptcy, but an individual tradeline does, the borrower must meet these bankruptcy guidelines. Generally, bankruptcies (except

All Reinsured Companies All Risk Management Agency Field Offices All Other Interested Parties Administrator

United States Department of Agriculture Risk Management Agency 1400 Independence Avenue, SW Stop 0801 Washington, DC 20250-0801 BULLETIN NO.: MGR-05-014 TO: All Reinsured Companies All Risk Management

United States Department of Agriculture Risk Management Agency 1400 Independence Avenue, SW Stop 0801 Washington, DC 20250-0801 BULLETIN NO.: MGR-05-014 TO: All Reinsured Companies All Risk Management

2018 Worldwide ERC. June 19, :00 am (ET)

") June 19, 2018 11:00 am (ET) Worldwide ERC Government Affairs Update WORLDWIDE ERC WEBINAR DISCLAIMER The views, opinions, and information expressed during this webinar are those of the presenter and are

June 19, 2018 11:00 am (ET) Worldwide ERC Government Affairs Update WORLDWIDE ERC WEBINAR DISCLAIMER The views, opinions, and information expressed during this webinar are those of the presenter and are

June 29, 2pm EST. Worldwide ERC would like to thank today s sponsor: MSI Global Talent Solutions Worldwide ERC

June 29, 2pm EST Worldwide ERC would like to thank today s sponsor: MSI Global Talent Solutions 2017 Worldwide ERC Business Travel Tracking Knowing Where Your Mobile Employees Are is Now a C-suite Issue

June 29, 2pm EST Worldwide ERC would like to thank today s sponsor: MSI Global Talent Solutions 2017 Worldwide ERC Business Travel Tracking Knowing Where Your Mobile Employees Are is Now a C-suite Issue

Real Estate Investment Guidelines Overview Buy and Hold rules. David Wright

Real Estate Investment Guidelines Overview Buy and Hold rules Financing Fannie Mae Residential (traditional fixed Rate mortgages terms can be from 8-30 years) Commercial (terms vary) Bank Portfolio Residential

Real Estate Investment Guidelines Overview Buy and Hold rules Financing Fannie Mae Residential (traditional fixed Rate mortgages terms can be from 8-30 years) Commercial (terms vary) Bank Portfolio Residential

U.S. Transfer Activity, Policy & Cost Survey

U.S. Transfer Activity, Policy & Cost Survey 2016 About Worldwide ERC Since 1964 Worldwide ERC has been committed to connecting and educating workforce mobility professonals across the globe. A global

U.S. Transfer Activity, Policy & Cost Survey 2016 About Worldwide ERC Since 1964 Worldwide ERC has been committed to connecting and educating workforce mobility professonals across the globe. A global

Please complete credit card information below for your retainer and monthly fees to be deducted from. Credit Card Number: Expiration:

When We ll Do It This engagement will begin on (Date) and will continue on a regular scheduled basis or until either party terminates the agreement. This engagement is made on a time-and-materials, best-efforts

When We ll Do It This engagement will begin on (Date) and will continue on a regular scheduled basis or until either party terminates the agreement. This engagement is made on a time-and-materials, best-efforts

Prime / Credit Ascent

Prime / Credit Ascent REQUIRED APPRAISAL REPORTS Property Type FNMA Form 1 family properties & PUDs FNMA Form #1004 2-4 family properties FNMA Form #1025 Condominiums/PUDs FNMA Form #1073 Market conditions

Prime / Credit Ascent REQUIRED APPRAISAL REPORTS Property Type FNMA Form 1 family properties & PUDs FNMA Form #1004 2-4 family properties FNMA Form #1025 Condominiums/PUDs FNMA Form #1073 Market conditions

Confirmation of Coverage

Confirmation of Coverage HAREON SOLAR USA CORPORATION (and affiliates worldwide) 121 Metro Drive San Jose, CA 95110 USA Warranty Policy Effective September 1, 2014 to September 1, 2015 License 0H30199

Confirmation of Coverage HAREON SOLAR USA CORPORATION (and affiliates worldwide) 121 Metro Drive San Jose, CA 95110 USA Warranty Policy Effective September 1, 2014 to September 1, 2015 License 0H30199

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - March 214 Summary Statistics March 214 March 213 Paid in Cash 1,21 1,199.9% 59 491 3.7% New Pending Sales 1,995 1,897 5.2% 2,419 1,948 24.2% $268,5 $242,5 1.7% Average Sale Price $332,392

ly Market Detail - March 214 Summary Statistics March 214 March 213 Paid in Cash 1,21 1,199.9% 59 491 3.7% New Pending Sales 1,995 1,897 5.2% 2,419 1,948 24.2% $268,5 $242,5 1.7% Average Sale Price $332,392

Making the switch is easy. Welcome to Bank of Oklahoma.

Making the switch is easy. Have you thought about changing banks? If you re like most people, then the answer is yes. Maybe you recently relocated, switched jobs or perhaps your bank just isn t providing

Making the switch is easy. Have you thought about changing banks? If you re like most people, then the answer is yes. Maybe you recently relocated, switched jobs or perhaps your bank just isn t providing

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

Summary Statistics November 214 November 213 Paid in Cash 58 76-23.7% 38 57-33.3% New Pending Sales 68 66 3.% 17 113-5.3% $14, $12, 36.6% Average Sale Price $178,924 $13,748 36.8% Median Days on Market

Summary Statistics November 214 November 213 Paid in Cash 58 76-23.7% 38 57-33.3% New Pending Sales 68 66 3.% 17 113-5.3% $14, $12, 36.6% Average Sale Price $178,924 $13,748 36.8% Median Days on Market

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

Summary Statistics February 215 February 214 Paid in Cash 79 67 17.9% 36 36.% New Pending Sales 123 87 41.4% 171 148 15.5% $173,5 $165, 5.2% Average Sale Price $219,938 $197,353 11.4% Median Days on Market

Summary Statistics February 215 February 214 Paid in Cash 79 67 17.9% 36 36.% New Pending Sales 123 87 41.4% 171 148 15.5% $173,5 $165, 5.2% Average Sale Price $219,938 $197,353 11.4% Median Days on Market

KEY CONCEPTS. A shorter amortization period means larger payments but less total interest

KEY CONCEPTS A shorter amortization period means larger payments but less total interest There are a number of strategies for reducing the time needed to pay off a mortgage and for reducing the total interest

KEY CONCEPTS A shorter amortization period means larger payments but less total interest There are a number of strategies for reducing the time needed to pay off a mortgage and for reducing the total interest

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - December 214 Summary Statistics December 214 December 213 Paid in Cash 973 93 7.8% 754 73 7.3% New Pending Sales 889 88 1.% 1,112 1,327-16.2% $54, $49,9 8.2% Average Sale Price $64,27

ly Market Detail - December 214 Summary Statistics December 214 December 213 Paid in Cash 973 93 7.8% 754 73 7.3% New Pending Sales 889 88 1.% 1,112 1,327-16.2% $54, $49,9 8.2% Average Sale Price $64,27

How to Order an Employment Verification

How to Order an Employment Verification To order an Employment verification, do the following: Some employers require using an alternate Employee ID rather than using a SSN. If this is a requirement for

How to Order an Employment Verification To order an Employment verification, do the following: Some employers require using an alternate Employee ID rather than using a SSN. If this is a requirement for

ASSET FLOWS REPORT. First Quarter 2016

ASSET FLOWS REPORT First Quarter 2016 About the evestment Asset Flows Report Asset Flows Report This report is intended to show the flow of institutional funds across regions, universes and products. We

ASSET FLOWS REPORT First Quarter 2016 About the evestment Asset Flows Report Asset Flows Report This report is intended to show the flow of institutional funds across regions, universes and products. We

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - June 215 Summary Statistics June 215 June 214 Paid in Cash 75 74 1.4% 55 54 1.9% New Pending Sales 59 64-7.8% 72 65 1.8% $125, $112,25 11.4% Average Sale Price $147,14 $127,475 15.3%

ly Market Detail - June 215 Summary Statistics June 215 June 214 Paid in Cash 75 74 1.4% 55 54 1.9% New Pending Sales 59 64-7.8% 72 65 1.8% $125, $112,25 11.4% Average Sale Price $147,14 $127,475 15.3%

Course Syllabus. CMPS Certification Course (Online Self-Study)

") Course Syllabus CMPS Certification Course (Online Self-Study) Welcome! This Certified Mortgage Planning Specialist (CMPS ) Certification Course is designed to euip you with five skills: Mortgage & Real

Course Syllabus CMPS Certification Course (Online Self-Study) Welcome! This Certified Mortgage Planning Specialist (CMPS ) Certification Course is designed to euip you with five skills: Mortgage & Real

Pension Funding Framework Review. And other issues affecting pension plans

Pension Funding Framework Review And other issues affecting pension plans September 2017 Crown copyright, Province of Nova Scotia, 2017 Introduction Employer sponsored pension plans play a key role in

Pension Funding Framework Review And other issues affecting pension plans September 2017 Crown copyright, Province of Nova Scotia, 2017 Introduction Employer sponsored pension plans play a key role in

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - Q2 213 Summary Statistics Q2 213 Q2 212 Paid in Cash 11,981 1,522 13.9% 5,467 4,686 16.7% New Pending Sales 18,292 15,57 21.5% 18,353 16,486 11.3% $245, $25, 19.5% Average Sale Price

ly Market Detail - Q2 213 Summary Statistics Q2 213 Q2 212 Paid in Cash 11,981 1,522 13.9% 5,467 4,686 16.7% New Pending Sales 18,292 15,57 21.5% 18,353 16,486 11.3% $245, $25, 19.5% Average Sale Price

2012 Tax & Legal Update

2012 Tax & Legal Update This issue of Mobility Insights takes a look at the tax and legal landscape as it pertains to relocation in 2012, including issues that are not new, but are still relevant; issues

2012 Tax & Legal Update This issue of Mobility Insights takes a look at the tax and legal landscape as it pertains to relocation in 2012, including issues that are not new, but are still relevant; issues

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - December 213 Summary Statistics December 213 December 212 Paid in Cash 3,687 3,878-4.9% 2,649 3,37-12.8% New Pending Sales 4,81 4,738-13.9% 5,856 5,294 1.6% $14, $119,5 17.2% Average

ly Market Detail - December 213 Summary Statistics December 213 December 212 Paid in Cash 3,687 3,878-4.9% 2,649 3,37-12.8% New Pending Sales 4,81 4,738-13.9% 5,856 5,294 1.6% $14, $119,5 17.2% Average

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - April 213 Summary Statistics April 213 April 212 Paid in Cash 1,43 1,23 14.1% 729 69 19.7% New Pending Sales 2,34 1,414 65.5% 2,91 1,917 9.1% $265, $21, 26.2% Average Sale Price $468,37

ly Market Detail - April 213 Summary Statistics April 213 April 212 Paid in Cash 1,43 1,23 14.1% 729 69 19.7% New Pending Sales 2,34 1,414 65.5% 2,91 1,917 9.1% $265, $21, 26.2% Average Sale Price $468,37

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

Summary Statistics December 15 December 14 Paid in Cash 39 48-18.8% 21 26-19.2% New Pending Sales 3 33.3% 61 31.1% $2, $225, -2.% Average Sale Price $3,655 $285,919 5.2% Median Days on Market 123 111 1.8%

Summary Statistics December 15 December 14 Paid in Cash 39 48-18.8% 21 26-19.2% New Pending Sales 3 33.3% 61 31.1% $2, $225, -2.% Average Sale Price $3,655 $285,919 5.2% Median Days on Market 123 111 1.8%

Summary Statistics. Closed Sales. Paid in Cash. New Pending Sales. New Listings. Median Sale Price. Average Sale Price. Median Days on Market

ly Market Detail - December 215 Summary Statistics December 215 December 214 Paid in Cash 118 114 3.5% 43 5-14.% New Pending Sales 79 65 21.5% 13 13.% $212,5 $181, 17.4% Average Sale Price $294,36 $228,45

ly Market Detail - December 215 Summary Statistics December 215 December 214 Paid in Cash 118 114 3.5% 43 5-14.% New Pending Sales 79 65 21.5% 13 13.% $212,5 $181, 17.4% Average Sale Price $294,36 $228,45

Notes To Consolidated Financial Statements

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES As used herein, the terms Equifax, the Company, we, our and us refer to Equifax Inc., a Georgia corporation, and its consolidated subsidiaries as a combined

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES As used herein, the terms Equifax, the Company, we, our and us refer to Equifax Inc., a Georgia corporation, and its consolidated subsidiaries as a combined

(a) Conversion recorded at book value of the bonds:

Conversion recorded at book value of the bonds:") Accounting 472 Summer 2002 Chapter 17 Solutions EXERCISE 17-3 (10-20 minutes) (a) Conversion recorded at book value of the bonds: Bonds Payable... 500,000 Premium on Bonds Payable... 7,500 Preferred Stock...

Accounting 472 Summer 2002 Chapter 17 Solutions EXERCISE 17-3 (10-20 minutes) (a) Conversion recorded at book value of the bonds: Bonds Payable... 500,000 Premium on Bonds Payable... 7,500 Preferred Stock...

FREDERICK OWUSU PREMPEH

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 5 Advanced Investment Appraisal & Application of option pricing

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 5 Advanced Investment Appraisal & Application of option pricing

Long-Term Natural Gas Supply and Transportation Contracts. Dated: October 1, 2008 File No.: EB

Long-Term Natural Gas Supply and Transportation Contracts Dated: October 1, 2008 File No.: EB-2008-0280 Overview Purpose, Process and Timelines North American Background Jurisdictional Review Options &

Long-Term Natural Gas Supply and Transportation Contracts Dated: October 1, 2008 File No.: EB-2008-0280 Overview Purpose, Process and Timelines North American Background Jurisdictional Review Options &

Property Tax Solutions

Silver Oak Advisors LLC Financial Solutions that impact your bottom line Property Tax Solutions Silver Oak Advisors professionals have been providing corporate property tax services bringing a total of

Silver Oak Advisors LLC Financial Solutions that impact your bottom line Property Tax Solutions Silver Oak Advisors professionals have been providing corporate property tax services bringing a total of

Decision Power Insight TM. Training Module II. (TeleCheck Decisioning Only) Submitting Requests for Decisioning Consumer and Commercial

Submitting Requests for Decisioning Consumer and Commercial") Decision Power Insight TM (TeleCheck Decisioning Only) Training Module II Submitting Requests for Decisioning Consumer and Commercial Confidentiality / Non-Disclosure Confidentiality, non-disclosure, and

Decision Power Insight TM (TeleCheck Decisioning Only) Training Module II Submitting Requests for Decisioning Consumer and Commercial Confidentiality / Non-Disclosure Confidentiality, non-disclosure, and

Intermediary Buy to Let Mortgage Range for New Purchases

Intermediary Buy to Let Mortgage Range for New Purchases This guide gives you the specific rates, features and prices of our current Buy to Let range. checklist emortgage application and signed declaration

Intermediary Buy to Let Mortgage Range for New Purchases This guide gives you the specific rates, features and prices of our current Buy to Let range. checklist emortgage application and signed declaration

U.S. Transfer Volume & Cost

U.S. Transfer Volume & Cost Survey 2015 SPONSORED BY About Worldwide ERC Worldwide ERC has served 50 years as the membership association and foremost center for corporate and government mobility; educating

U.S. Transfer Volume & Cost Survey 2015 SPONSORED BY About Worldwide ERC Worldwide ERC has served 50 years as the membership association and foremost center for corporate and government mobility; educating

COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY

CCRSI RELEASE JULY 2013 (With data through May 2013) COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY STRONG ABSORPTION ACROSS ALLL SIZE AND QUALITY DIMENSIONS OF REAL ESTATEE SECTOR REFLECTED

CCRSI RELEASE JULY 2013 (With data through May 2013) COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY STRONG ABSORPTION ACROSS ALLL SIZE AND QUALITY DIMENSIONS OF REAL ESTATEE SECTOR REFLECTED

COMMERCIAL PRICING SURGE

CCRSI RELEASE MARCH 2013 (With data through JANUARY 2013) COMMERCIAL REAL ESTATE PRICING LEVELS OFF FOLLOWING YEAR-END SURGE IN JANUARY INCREASING LIQUIDITY AND DECLINING DISTRESSED IMPROVING INVESTOR

CCRSI RELEASE MARCH 2013 (With data through JANUARY 2013) COMMERCIAL REAL ESTATE PRICING LEVELS OFF FOLLOWING YEAR-END SURGE IN JANUARY INCREASING LIQUIDITY AND DECLINING DISTRESSED IMPROVING INVESTOR

Course Syllabus. CMPS Live Certification Course

Course Syllabus CMPS Live Certification Course Welcome! This Certified Mortgage Planning Specialist (CMPS ) Certification Course is designed to euip you with five skills: Mortgage & Real Estate Taxation

Course Syllabus CMPS Live Certification Course Welcome! This Certified Mortgage Planning Specialist (CMPS ) Certification Course is designed to euip you with five skills: Mortgage & Real Estate Taxation

Suntory Holdings Limited and its Subsidiaries

Suntory Holdings Limited and its Subsidiaries Consolidated Financial Statements for the Year Ended December 31, 2017, and Independent Auditor's Report Consolidated statement of financial position Suntory

Suntory Holdings Limited and its Subsidiaries Consolidated Financial Statements for the Year Ended December 31, 2017, and Independent Auditor's Report Consolidated statement of financial position Suntory

NIH Modular Budget Examples

NIH Modular Budget Examples Simple modular with NO consortium: - Recommend preparing tentative detailed budget to best determine module amount requested (modules of $25K up to a limit of $250K). - In this

NIH Modular Budget Examples Simple modular with NO consortium: - Recommend preparing tentative detailed budget to best determine module amount requested (modules of $25K up to a limit of $250K). - In this

EUROPEAN REPO COMMITTEE. European Central Bank Payment Systems and Market Infrastructure attn. Ms Daniela Russo

EUROPEAN REPO COMMITTEE European Central Bank Payment Systems and Market Infrastructure attn. Ms Daniela Russo POB 16 03 19 D-60066 Frankfurt am Main Germany Project Integration of s triparty collateral

EUROPEAN REPO COMMITTEE European Central Bank Payment Systems and Market Infrastructure attn. Ms Daniela Russo POB 16 03 19 D-60066 Frankfurt am Main Germany Project Integration of s triparty collateral

Relocation Assistance:

Relocation Assistance: U.S. Domestic Transferred Employees A comprehensive picture of the programs facilitating employee mobility in the United States. Sponsored By Copyright 2013 Worldwide ERC The Worldwide

Relocation Assistance: U.S. Domestic Transferred Employees A comprehensive picture of the programs facilitating employee mobility in the United States. Sponsored By Copyright 2013 Worldwide ERC The Worldwide

City of Carrollton, Carrollton Housing Authority Neighborhood Stabilization Program. Real Estate Services Sales + Purchases

City of Carrollton, Carrollton Housing Authority Neighborhood Stabilization Program Real Estate Services Sales + Purchases Purpose of the City of Carrollton NSP Program Purchase foreclosed and abandoned

City of Carrollton, Carrollton Housing Authority Neighborhood Stabilization Program Real Estate Services Sales + Purchases Purpose of the City of Carrollton NSP Program Purchase foreclosed and abandoned

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 20-F. (Mark One)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) Registration statement pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934 OR Annual Report

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) Registration statement pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934 OR Annual Report

Decision Power Express SM Training Module II

Please forward through the slides with a mouse click. If you need to move back you can do so using a right mouse click. A link to a PDF file intended for printing is on the final page. Decision Power Express

Please forward through the slides with a mouse click. If you need to move back you can do so using a right mouse click. A link to a PDF file intended for printing is on the final page. Decision Power Express

MARYLAND STATE TREASURER S OFFICE Louis L. Goldstein Treasury Building 80 Calvert Street, Room 109 Annapolis, Maryland 21401

MARYLAND STATE TREASURER S OFFICE Louis L. Goldstein Treasury Building 80 Calvert Street, Room 109 Annapolis, Maryland 21401 QUESTIONS AND ANSWERS FOR REQUEST FOR PROPOSALS FOR GLOBAL CUSTODY SERVICES

MARYLAND STATE TREASURER S OFFICE Louis L. Goldstein Treasury Building 80 Calvert Street, Room 109 Annapolis, Maryland 21401 QUESTIONS AND ANSWERS FOR REQUEST FOR PROPOSALS FOR GLOBAL CUSTODY SERVICES

Integrating Real Estate Market-Based Indicators into Fundamental Home Price Forecasting Systems

Integrating Real Estate Market-Based Indicators into Fundamental Home Price Forecasting Systems Western Economics Association 86 th Annual Conference 8:15 am 10:00 am, Saturday, July 2, 2011 Forecasting

Integrating Real Estate Market-Based Indicators into Fundamental Home Price Forecasting Systems Western Economics Association 86 th Annual Conference 8:15 am 10:00 am, Saturday, July 2, 2011 Forecasting

Managing Cash Flow Updated:

Managing Cash Flow Updated: 09-2016 Pre-Test Locate the Pre- and Post-Test Form at the back of your Participant Guide. Complete the BEFORE Training column to assess your knowledge on this topic before

Managing Cash Flow Updated: 09-2016 Pre-Test Locate the Pre- and Post-Test Form at the back of your Participant Guide. Complete the BEFORE Training column to assess your knowledge on this topic before

FINANCIAL STRATEGY Jul 2018, Dubai 21 Oct - 01 Nov 2018, Dubai

FINANCIAL STRATEGY & ACCOUNTING SKILLS 15-26 Jul 2018, Dubai 21 Oct - 01 Nov 2018, Dubai Approved Centre REP logo, PMI & PMP are registered trademarks of Project Management Institute, Inc. FINANCIAL STRATEGY

FINANCIAL STRATEGY & ACCOUNTING SKILLS 15-26 Jul 2018, Dubai 21 Oct - 01 Nov 2018, Dubai Approved Centre REP logo, PMI & PMP are registered trademarks of Project Management Institute, Inc. FINANCIAL STRATEGY

PAPER No. 16: Financial Markets and Institutions MODULE No. 18: Bank Credit: Working Capital & Bank Funds

Subject Paper No and Title Module No and Title Module Tag 16: Financial Markets and Institutions 18: Bank Credit: Working Capital & Bank Funds Com_P16_M18 TABLE OF CONTENTS 1) Learning Outcomes 2) Introduction-

Subject Paper No and Title Module No and Title Module Tag 16: Financial Markets and Institutions 18: Bank Credit: Working Capital & Bank Funds Com_P16_M18 TABLE OF CONTENTS 1) Learning Outcomes 2) Introduction-

Purchase, Rate and term refinance, Cash-out refinance. Finance Type. Owner-occupied primary residences only F15, F20, F25, F30, F15HB.

Finance Type Occupancy Product Codes Purchase, Rate and term refinance, Cash-out refinance Owner-occupied primary residences only F15, F20, F25, F30, F15HB. F30HB FHA Fixed Rate Type of Loan Maximum Mortgage

Finance Type Occupancy Product Codes Purchase, Rate and term refinance, Cash-out refinance Owner-occupied primary residences only F15, F20, F25, F30, F15HB. F30HB FHA Fixed Rate Type of Loan Maximum Mortgage

Lending TRAINING AND EVENTS. aba.com/lendingtraining

Lending TRAINING AND EVENTS aba.com/lendingtraining Enhance your lending expertise. Adapt to a dynamic economic landscape through sound lending practices, underwriting considerations and regulatory risk

Lending TRAINING AND EVENTS aba.com/lendingtraining Enhance your lending expertise. Adapt to a dynamic economic landscape through sound lending practices, underwriting considerations and regulatory risk

STEPS TO FINANCING YOUR FIRST VEHICLE Route 23, Butler, NJ PrecisionChrysler.com POWERHOUSE ROUTE

STEPS TO FINANCING YOUR FIRST VEHICLE ROUTE 1341 Route, Butler, NJ 07405 888-313-2410 PrecisionChrysler.com STEPS TO FINANCING YOUR FIRST VEHICLE Introduction Well, you finally did it. After hours of research

STEPS TO FINANCING YOUR FIRST VEHICLE ROUTE 1341 Route, Butler, NJ 07405 888-313-2410 PrecisionChrysler.com STEPS TO FINANCING YOUR FIRST VEHICLE Introduction Well, you finally did it. After hours of research

CREDIT UNION FE DERAL HO ME LO A N B A N K O F AT LA N TA

CREDIT UNION A P P L I C AT I O N F O R M E M B E R S H I P FE DERAL HO ME LO A N B A N K O F AT LA N TA CREDIT UNION APPLICATION FOR MEMBERSHIP IN THE FEDERAL HOME LOAN BANK OF ATLANTA GENERAL INSTRUCTIONS

CREDIT UNION A P P L I C AT I O N F O R M E M B E R S H I P FE DERAL HO ME LO A N B A N K O F AT LA N TA CREDIT UNION APPLICATION FOR MEMBERSHIP IN THE FEDERAL HOME LOAN BANK OF ATLANTA GENERAL INSTRUCTIONS

A GFE must be issued when the originator receives an application OR six minimum pieces of information sufficient to complete an application including:

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

BEPROTECTED SECURING GUARANTEED STABLE RETURNS

LIFE INSURANCE - SAVINGS BEPROTECTED SECURING GUARANTEED STABLE RETURNS Sun Phoenix Endowment Plan Sun Life Hong Kong Limited (Incorporated in Bermuda) LIMITED OFFER 1 Wouldn t it be great if you could

LIFE INSURANCE - SAVINGS BEPROTECTED SECURING GUARANTEED STABLE RETURNS Sun Phoenix Endowment Plan Sun Life Hong Kong Limited (Incorporated in Bermuda) LIMITED OFFER 1 Wouldn t it be great if you could

Goal Setting Form. Calculate Prospects Needed Per Week

Goal Setting Form Step 1: Set Your Goals Income Goal... A) Average Sales Price... B) Average Office Commission Rate Per Side (%)... C) Average Office Commission Per Side (B times C)... D) Average Office

Goal Setting Form Step 1: Set Your Goals Income Goal... A) Average Sales Price... B) Average Office Commission Rate Per Side (%)... C) Average Office Commission Per Side (B times C)... D) Average Office

NEW ATLANTA STADIUM RESERVE SEAT PSL MARKETING PLAN

RESERVE SEAT PSL MARKETING PLAN 6.2.15 CLUB SEAT SALES $77 million contracted revenue Tracking ahead of plan Over 54% sold through on club seats in just over 3 ½ months Based on previous projects at the

RESERVE SEAT PSL MARKETING PLAN 6.2.15 CLUB SEAT SALES $77 million contracted revenue Tracking ahead of plan Over 54% sold through on club seats in just over 3 ½ months Based on previous projects at the

Actual Cash Value and Depreciation

Developed with Xactware Data and Technology April 2015 Contents Introduction... 2 Actual Cash Value (ACV)... 2 Depreciation Based Upon... 2 Age and Condition of Structure Based... 3 Percentage Based...

Developed with Xactware Data and Technology April 2015 Contents Introduction... 2 Actual Cash Value (ACV)... 2 Depreciation Based Upon... 2 Age and Condition of Structure Based... 3 Percentage Based...

2012 Strategic Business Initiatives Cooperative Extension Service Environmental and Heritage Center Health and Human Services Parks and Recreation

2013 Business Plan 2012 Strategic Business Initiatives Cooperative Extension Service Environmental and Heritage Center Health and Human Services Parks and Recreation Operations Parks and Recreation Project

2013 Business Plan 2012 Strategic Business Initiatives Cooperative Extension Service Environmental and Heritage Center Health and Human Services Parks and Recreation Operations Parks and Recreation Project

Survey of Emerging Market Conditions Quarter

Survey of Emerging Market Conditions Quarter 4 2009 Published January 27, 2010 Lead Researcher Dr. Wayne R. Archer, Executive Director University of Florida Bergstrom Center for Real Estate Studies Professor

Survey of Emerging Market Conditions Quarter 4 2009 Published January 27, 2010 Lead Researcher Dr. Wayne R. Archer, Executive Director University of Florida Bergstrom Center for Real Estate Studies Professor

ADOPTED REGULATION OF THE REAL ESTATE COMMISSION. LCB File No. R Effective May 30, 2012

ADOPTED REGULATION OF THE REAL ESTATE COMMISSION LCB File No. R093-10 Effective May 30, 2012 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted. AUTHORITY:

ADOPTED REGULATION OF THE REAL ESTATE COMMISSION LCB File No. R093-10 Effective May 30, 2012 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted. AUTHORITY:

E-BOOK / PROPERTY CASUALTY STUDY MANUAL GA ARCHIVE

12 December, 2017 E-BOOK / PROPERTY CASUALTY STUDY MANUAL GA ARCHIVE Document Filetype: PDF 322.93 KB 0 E-BOOK / PROPERTY CASUALTY STUDY MANUAL GA ARCHIVE All property and casualty insurers licensed to

12 December, 2017 E-BOOK / PROPERTY CASUALTY STUDY MANUAL GA ARCHIVE Document Filetype: PDF 322.93 KB 0 E-BOOK / PROPERTY CASUALTY STUDY MANUAL GA ARCHIVE All property and casualty insurers licensed to

Relocation TAX. & the Mobile. Workforce

Relocation TAX & the Mobile Workforce Policy Components and Taxability Economic studies have repeatedly shown that a mobile workforce is a prerequisite for a strong, competitive economy. To maximize economic

Relocation TAX & the Mobile Workforce Policy Components and Taxability Economic studies have repeatedly shown that a mobile workforce is a prerequisite for a strong, competitive economy. To maximize economic

HSBC Channel Islands and Isle of Man Mortgage Rates

HSBC Channel Islands and Isle of Man Mortgage Rates The information in the tables and further information section does not contain all of the details you need to choose a mortgage. We ll provide you with

HSBC Channel Islands and Isle of Man Mortgage Rates The information in the tables and further information section does not contain all of the details you need to choose a mortgage. We ll provide you with

HSBC Channel Islands and Isle of Man Mortgage Rates

HSBC Channel Islands and Isle of Man Mortgage Rates The information in the tables and further information section does not contain all of the details you need to choose a mortgage. We ll provide you with

HSBC Channel Islands and Isle of Man Mortgage Rates The information in the tables and further information section does not contain all of the details you need to choose a mortgage. We ll provide you with

Suggested Answers to Discussion Questions

Suggested Answers to Discussion Questions 1. Premium Time Premium Break Even Dec put103 Strike 6.95 1.59 96.05 Dec call100strike 0.00 2.02 102.02 3. (a) The stock price is currently at $52.51. There is

Suggested Answers to Discussion Questions 1. Premium Time Premium Break Even Dec put103 Strike 6.95 1.59 96.05 Dec call100strike 0.00 2.02 102.02 3. (a) The stock price is currently at $52.51. There is

Client Services Procedure Manual

Procedure: 48.00 Subject: Return to Work and Labour Market Re-entry Expenses 48.00 Introduction While not all employers have a re-employment obligation and an obligation to pay for modifications and assistive

Procedure: 48.00 Subject: Return to Work and Labour Market Re-entry Expenses 48.00 Introduction While not all employers have a re-employment obligation and an obligation to pay for modifications and assistive

FisherBroyles A LIMITED LIABILITY PARTNERSHIP

Financial Institutions Update Happy 2015 (how is that possible) and welcome to the latest, LLP, Financial Institutions Update. In preparing this update for you, which is forward focused, we also looked

Financial Institutions Update Happy 2015 (how is that possible) and welcome to the latest, LLP, Financial Institutions Update. In preparing this update for you, which is forward focused, we also looked

Brandon s Cabinet Shop

Brandon s Cabinet Shop Adjusting Entries and Closing Entries for the Quarter Ended June 30 and the Final Evaluation Page 1 Adjusting Entries for the Period Using a copy of the June 30 Trial Balance (printed

Brandon s Cabinet Shop Adjusting Entries and Closing Entries for the Quarter Ended June 30 and the Final Evaluation Page 1 Adjusting Entries for the Period Using a copy of the June 30 Trial Balance (printed

Health Care Reform Update

Health Care Reform Update Issue 8-2013 March 13, 2013 Pay or Play Penalty Examples for Determining Full-time Status Under section 4980H of the Affordable Care Act (ACA), large employers may be subject

Health Care Reform Update Issue 8-2013 March 13, 2013 Pay or Play Penalty Examples for Determining Full-time Status Under section 4980H of the Affordable Care Act (ACA), large employers may be subject

n the Endo tate ankrupttp Court for the outhjetn Oitritt of dkoria

Case: 11-41963-LWD Doc#:392 Filed:01/09/13 Page:1 of 15 n the Endo tate ankrupttp Court for the outhjetn Oitritt of dkoria 'abannab ibiion In the matter of ) INVESTORS LENDING GROUP, LLC ) ) Chapter )

Case: 11-41963-LWD Doc#:392 Filed:01/09/13 Page:1 of 15 n the Endo tate ankrupttp Court for the outhjetn Oitritt of dkoria 'abannab ibiion In the matter of ) INVESTORS LENDING GROUP, LLC ) ) Chapter )

Bonds for Beginners. WELCOME!! Atlanta, April 3, National Association of Local Housing Finance Agencies. Gene Slater, CSG Advisors

Bonds for Beginners National Association of Local Housing Finance Agencies WELCOME!! Atlanta, April 3, 2014 Gene Slater, CSG Advisors 2 What You Will Learn 1. Bonds are Debt Instruments 3 2. Bonds are

Bonds for Beginners National Association of Local Housing Finance Agencies WELCOME!! Atlanta, April 3, 2014 Gene Slater, CSG Advisors 2 What You Will Learn 1. Bonds are Debt Instruments 3 2. Bonds are

HSBC Channel Islands and Isle of Man Mortgage Rates

HSBC Channel Islands and Isle of Man Mortgage Rates The information in the tables and further information section does not contain all of the details you need to choose a mortgage. We ll provide you with

HSBC Channel Islands and Isle of Man Mortgage Rates The information in the tables and further information section does not contain all of the details you need to choose a mortgage. We ll provide you with

YOUR HOMEBUYER S GUIDE

YOUR HOMEBUYER S GUIDE Contents: What Every Home Buyer Needs To Know: Outlines important information every homebuyer needs. Types of Loans: Provides a brief explanation of the different types of loan programs

YOUR HOMEBUYER S GUIDE Contents: What Every Home Buyer Needs To Know: Outlines important information every homebuyer needs. Types of Loans: Provides a brief explanation of the different types of loan programs

FORTIVE CORPORATION RECONCILIATION OF GAAP TO NON-GAAP FINANCIAL MEASURES

FORTIVE CORPORATION RECONCILIATION OF GAAP TO NON-GAAP FINANCIAL MEASURES Adjusted Net Earnings, Adjusted Diluted Net Earnings per Share, Adjusted Sales, and Adjusted Operating Profit We disclose the non-gaap

FORTIVE CORPORATION RECONCILIATION OF GAAP TO NON-GAAP FINANCIAL MEASURES Adjusted Net Earnings, Adjusted Diluted Net Earnings per Share, Adjusted Sales, and Adjusted Operating Profit We disclose the non-gaap

Deal Protections and Remedies

(Actual image used will be more applicable to the webinar subject matter) Deal Protections and Remedies April 12, 2014 Presenter: Stephen M. Kotran, Sullivan & Cromwell LLP 2 Study Overview Study of deal-protection

(Actual image used will be more applicable to the webinar subject matter) Deal Protections and Remedies April 12, 2014 Presenter: Stephen M. Kotran, Sullivan & Cromwell LLP 2 Study Overview Study of deal-protection

William J. Flynn President and CEO Spencer Schwartz Senior Vice President and CFO Spencer Schwartz Executive Vice President and CFO

Fourth-Quarter First-Quarter 2016 2012 Review February May 5, 13, 2016 2013 William J. Flynn President William and J. Flynn CEO President and CEO Spencer Schwartz Senior Vice President and CFO Spencer

Fourth-Quarter First-Quarter 2016 2012 Review February May 5, 13, 2016 2013 William J. Flynn President William and J. Flynn CEO President and CEO Spencer Schwartz Senior Vice President and CFO Spencer

Registering a Deal and Requesting Waivers

Registering a Deal and Requesting Waivers May 2010 2010 Fannie Mae 1 Welcome to Registering a Deal and Requesting Waivers, part of a six-module course on the processes and applications you use in completing

Registering a Deal and Requesting Waivers May 2010 2010 Fannie Mae 1 Welcome to Registering a Deal and Requesting Waivers, part of a six-module course on the processes and applications you use in completing

Module: Financials Topic: Budget Munis Budget Analysis Munis Version 11.2

Module: Financials Topic: Budget Munis Budget Analysis Munis Version 11.2 Overview This document is intended to give an overview of how certain programs in Munis can be utilized to enhance the way the

Module: Financials Topic: Budget Munis Budget Analysis Munis Version 11.2 Overview This document is intended to give an overview of how certain programs in Munis can be utilized to enhance the way the

Vol. 1, Chapter 8 Introduction to Managerial Accounting

Vol. 1, Chapter 8 Introduction to Managerial Accounting Problem 1: Solution 1. Account 2. Adjusting entry 3. Balance sheet 4. Trial balance; Debit/Credit; Debit/Credit 5. Fundamental accounting equation

Vol. 1, Chapter 8 Introduction to Managerial Accounting Problem 1: Solution 1. Account 2. Adjusting entry 3. Balance sheet 4. Trial balance; Debit/Credit; Debit/Credit 5. Fundamental accounting equation

Mortgage Cadence User Guide Reserving a VHDA Down Payment Assistance Grant

Purpose Mortgage Cadence User Guide Reserving a VHDA Down Payment Assistance Grant Link to Mortgage Cadence This quick reference guide provides a step-by-step list of actions to reserve a VHDA Down Payment

Purpose Mortgage Cadence User Guide Reserving a VHDA Down Payment Assistance Grant Link to Mortgage Cadence This quick reference guide provides a step-by-step list of actions to reserve a VHDA Down Payment

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS Financial instruments FRS 102 significantly changed the accounting for financial instruments in comparison to the requirements applicable to most UK and Ireland

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS Financial instruments FRS 102 significantly changed the accounting for financial instruments in comparison to the requirements applicable to most UK and Ireland

Buy-to-Let Product Guide

Buy-to-Let Product Guide Why choose Magellan Homeloans: No credit scoring - human decision making Variable rates with no ERCs 2 & rates CCJs, Defaults, Arrears, and historic DMPs considered Online case

Buy-to-Let Product Guide Why choose Magellan Homeloans: No credit scoring - human decision making Variable rates with no ERCs 2 & rates CCJs, Defaults, Arrears, and historic DMPs considered Online case

Multiple Award Task Order Contracts (MATOC) Staff Augmentation Re-Procurement

Staff Augmentation Re-Procurement") Multiple Award Task Order Contracts (MATOC) Staff Augmentation Re-Procurement David Salazar, Chief Facilities Executive, LACCD December 14, 2018 www.jacobs.com worldwide Agenda Welcome Program Vision Services

Multiple Award Task Order Contracts (MATOC) Staff Augmentation Re-Procurement David Salazar, Chief Facilities Executive, LACCD December 14, 2018 www.jacobs.com worldwide Agenda Welcome Program Vision Services

CHEROKEE COUNTY WATER AND SEWERAGE AUTHORITY CHEROKEE COUNTY, GEORGIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED AUGUST 31, 2017

CHEROKEE COUNTY WATER AND SEWERAGE AUTHORITY CHEROKEE COUNTY, GEORGIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED AUGUST 31, 2017 TOGETHER WITH INDEPENDENT AUDITORS REPORTS FINANCIAL STATEMENTS AUGUST

CHEROKEE COUNTY WATER AND SEWERAGE AUTHORITY CHEROKEE COUNTY, GEORGIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED AUGUST 31, 2017 TOGETHER WITH INDEPENDENT AUDITORS REPORTS FINANCIAL STATEMENTS AUGUST

Commercial Lending Underwriting Guide

Commercial Lending Underwriting Guide For bridging, buy to let and Commercial loans and mortgages June 2017 0.1 Welcome to Together Commercial Finance Limited s Underwriting Guide Acceptable Security Most

Commercial Lending Underwriting Guide For bridging, buy to let and Commercial loans and mortgages June 2017 0.1 Welcome to Together Commercial Finance Limited s Underwriting Guide Acceptable Security Most

PROCEDURE MANUAL FOR REPURCHASE (REPO) OPERATIONS BOLSA DE VALORES DE PANAMÁ, S.A.

OPERATIONS BOLSA DE VALORES DE PANAMÁ, S.A.") PROCEDURE MANUAL FOR REPURCHASE (REPO) OPERATIONS BOLSA DE VALORES DE PANAMÁ, S.A. Text modified pursuant to Resolution No. 6-2005 of the National Securities Commission, issued on January 14, 2005. I.

PROCEDURE MANUAL FOR REPURCHASE (REPO) OPERATIONS BOLSA DE VALORES DE PANAMÁ, S.A. Text modified pursuant to Resolution No. 6-2005 of the National Securities Commission, issued on January 14, 2005. I.

Buy-to-Let Product Guide

Buy-to-Let Product Guide Why choose Magellan Homeloans: No credit scoring - human decision making Variable rates with no ERCs 2 & rates CCJs, Defaults, Arrears, and historic DMPs considered Online case

Buy-to-Let Product Guide Why choose Magellan Homeloans: No credit scoring - human decision making Variable rates with no ERCs 2 & rates CCJs, Defaults, Arrears, and historic DMPs considered Online case

INS Mutual Funds and Individual Securities Exam Study Guide

INS Mutual Funds and Individual Securities Exam Study Guide This document contains the questions that will be on the exam. When you have studied the course materials, reviewed the questions in this document,

INS Mutual Funds and Individual Securities Exam Study Guide This document contains the questions that will be on the exam. When you have studied the course materials, reviewed the questions in this document,

GOV: HOW TO VIEW AND ENROLL IN BENEFITS

GOV: HOW TO VIEW AND ENROLL IN BENEFITS Summary In this module you will learn how to view and enroll in benefits. Steps 1. Welcome to the training module on How to View and Enroll in Benefits! 2. Once

GOV: HOW TO VIEW AND ENROLL IN BENEFITS Summary In this module you will learn how to view and enroll in benefits. Steps 1. Welcome to the training module on How to View and Enroll in Benefits! 2. Once

Interest (monthly) = Principal x Rate x Time

= Principal x Rate x Time") Lesson 3: Mortgages In this lesson you will take a look at mortgages and the monthly payments they require. More detailed calculations will be examined in Lesson 4. While home ownership can be a rewarding

Lesson 3: Mortgages In this lesson you will take a look at mortgages and the monthly payments they require. More detailed calculations will be examined in Lesson 4. While home ownership can be a rewarding

Masthaven Bank Buy to Let Mortgage Product Guide

Masthaven Bank Buy to Let Mortgage Product Guide First Charge This information is for intermediaries only. First Charge Buy to Let Product Guide Date of Issue: March 2019 Version: 5 Page 1 of 5 Buy to

Masthaven Bank Buy to Let Mortgage Product Guide First Charge This information is for intermediaries only. First Charge Buy to Let Product Guide Date of Issue: March 2019 Version: 5 Page 1 of 5 Buy to

Our Mortgage Rates and Features Guide for New Purchase Mortgages

Our Mortgage Rates and Features Guide New Purchase Mortgages This Mortgage Rates and Features Guide should be used in conjunction with our general Mortgage Guide which will give you more in depth inmation.

Our Mortgage Rates and Features Guide New Purchase Mortgages This Mortgage Rates and Features Guide should be used in conjunction with our general Mortgage Guide which will give you more in depth inmation.

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE

Rev. 10/11/07 (Correction 5/16/08) NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE Purpose: These underwriting standards are intended to be an internal

Rev. 10/11/07 (Correction 5/16/08) NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE Purpose: These underwriting standards are intended to be an internal