Stochastic Programming in Gas Storage and Gas Portfolio Management. ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier

|

|

|

- Norman Ramsey

- 5 years ago

- Views:

Transcription

1 Stochastic Programming in Gas Storage and Gas Portfolio Management ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier

2 Agenda Optimization tasks in gas storage and gas portfolio management Scenario Tree based Stochastic Programming applied to Gas Portfolio Management Stochastic Processes and Scenario Tree generation Technical, contractual and gas market constraints in gas portfolio management Exemplary Results Conclusions 2

3 Optimization tasks in gas portfolio management Objectives: Cost minimal supply of retail demand by optimal utilizaiton of gas supply sources and storages Dimensioning of assets (gas storages, flexible contracts) Supply sources: Forward market products (Months, Quarters, Years) Spot market products (Daily) Balancing market Flexible supply contracts Gas storages Methods: Deterministic Optimization and Simulation Stochastic Optimization Challenges: Mathematical modelling of gas markets and assets with all contractual and technical constraints Future uncertainties of market prices and retail demand 3

4 Efficiency of gas procurement portfolios Forward market products + flexible supply contract : Uncetainty: future retail demand Structuring of procurement by monthly average of retail demand Structuring of procurement by mathematical optimiaztion of forward products Forward market products + flexible supply contract + spot market: Additional uncertainty: future uncertainty of spot market prices Determinsistic optimization with daily price forward curve of gas spot market prices and gas retail demand Stochastic optimizaiton with scenario tree of gas spot market prices and gas retail demand Forward market products + flexible supply contract + spot market + gas storage: Determinsistic optimization with daily price forward curve of gas spot market prices and gas retail demand Stochastic optimizaiton with scenario tree of gas spot market prices and gas retail demand Effici iency 4

5 Valuation and exercise of flexibilities in the energy industry Not path dependent: Today s exercise of an option has no impact on future optionality Examples: monthly strip of options, coal fired plant with unlimited fuel Adequate valuation technique: Monte-Carlo-Simulation (= one path scenario simulation ) Path dependent: Today s exercise of an option does have impact on future optionality Examples: Swing Options, Pumped storage, CCGT with limited fuel supply contract, Gas Storage Path dependency is: When I fill the storage today, I cannot inject tomorrow anymore. Adequate valuation technique: Tree based stochastic optimization, Least Square Monte Carlo methods 5

6 Comparison of valuation approaches Least Square Monte Carlo: Advantage: Generation of price scenarios can use a variety of price processes and can represent daily granularity Disadvantage: Technical and contractual constraints of the storage are difficult to implement because of the growth of the state space Tree based Stochastic Optimization: Advantage: Technical and contractual constraints can be modeled precisely Disadvantage: Scenario tree cannot branch on a daily basis, scenario generation is limited to scaled daily price forward curves in periods of the tree. 6

\ \MWh 7")

7 Discrepancy between forward and day ahead prices - daily price forward curves for TTF (every tenth day) - historic spot prices (red) \ \MWh 7

8 Example: Storage Operation under consideration of future spot price uncertainty Stochastic vs. Deterministic optimization stochastische Optimierungen deterministische Optimierungen

9 Storage volume trajectories 100% profit 73.85% profit 73.2% profit MWh 9

10 Concept of Simulation Analysis of profits / costs z s,n derived from decisions (u 1,..., u S ) for different price processes (p 1,..., p N ) Drawbacks: Different first stage decisions with different price processes p 1,..., p N Anticipativity of decision making t p 1 z s,1 p 2 z s,2 p 3 z s,3 p 4 z s,4 p 5 z s,5 p 6 z s,6... p N z s,n 10

11 Concept of Stochastic Optimization Unique optimal decision in every node with respect to all possible future developments (1,1) Scenario tree (binary process) (1) Non-anticipativity of the decisions (1,2) (2,1) (1,1,1) Szenario 1 (1,1,2) Szenario 2 (1,2,1) Szenario 3 (1,2,2) Szenario 4 (2,1,1) Szenario 5 (2) (2,2) (2,1,2) Szenario 6 (2,2,1) Szenario 7 t (2,2,2) Szenario 8 11

12 Storage balance equations in the scenario tree Shadow price of volume is derived from dual variable of volume balance equation of first node Storage Balance equation of period 1, scenario 1 V S1 1 + W S1 1 I S1 1 S1 = V Scenario tree Path dependent PnL P(Scenario1) P(Scenario 2) Storage Balance equation of period 0, scenario 1 V 0 + W 0 - I 0 = V -1 Value-at-Risk (10%) Constant! Initial Volume V -1 Storage Balance equation of period 1, scenario 2 V S2 1 + W S2 1 I S2 1 = V V. Volume W: Withdrawal I : Injection t 0 t 1 t 2 t 3 3 Min/max Volume constraints for each path of the tree 12

13 Storage balance equations in the scenario tree Shadow price of volume is derived from dual variable of volume balance equation of first node Storage Balance equation of period 1, scenario 1 V S1 1 + W S1 1 I S1 1 S1 = V 0 V 3 min <= V S1 3 <= V max 3 min <= V 3 min <= V S2 3 <= V max 3 min <= V 3 min <= V S3 3 <= V max 3 min <= Storage Balance equation of period 0, scenario 1 V 0 + W 0 - I 0 = V Constant! Initial Volume V -1 V. Volume W: Withdrawal I : Injection Storage Balance equation of period 1, scenario 2 V S2 1 + W S2 1 I S2 1 = V 0 t 0 t 1 t 2 t 3 V 3 min <= V S8 3 <= V max 3 min <= max 13

14 Multi-dimensional scenario tree generation Day Ahead price (Market 1) Gas demand Day Ahead price (Market 2) Storage outages FX rate Oil Price indices All trees share the same branching structure but hold different values, according to expectation, volatility, correlations and other parameters of the underlying stochastic processes 14

15 Structure of the overall mathematical model Shadow price of gas is derived from dual variable of gas balance equation of first node 15

Historic demand Estimation of volatility/mean")

Solving the math.")

16 Workflow for the valuation of gas storages / gas portfolios Stochastic impacts: Gas spot prices (i.e. TTF) Gas demand (optionally) Oil price index, FX-Rate (optionally) Historic demand Estimation of volatility/mean reversion (Demand) Stochastic optimization: 1) Scenario trees Historic TTF-spot price Estimation of volatility/mean reversion (Spot prices) (Spot prices and demand) 2) max Objective function Distributions Historc TTF- spot price Calculation of DPFC (Fleten s model) Actual price forward curve 3) Solving the math. model Solver (CPLEX ) Constraints Mean of P&L- Distribution = Value of the Storage 16

17 Structure of the mathematical optimization kernel Energy [ MWh / 2 weeks ] Scenario trees scen. tree lower appr. expected load real load scen. tree upper appr Analytical model formulation Periods Stochastic multistage (mixed integer) program Solver (CPLEX ) LP-Solver (Simplex, Barrier) MIP-Solver (Branch-and-Bound) Decisions and P&L Distribution 17

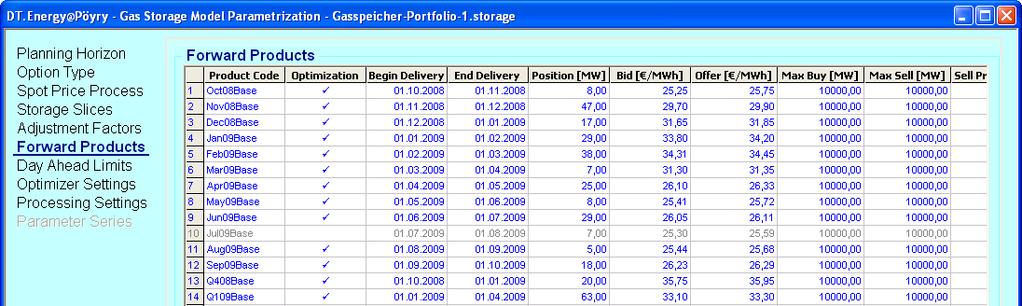

18 Spot price process: Pilipovic Spot price process for the gas day ahead market: Mean reversion Sigma Price Spot price process: Equilibrium price process: Uncorrelated Brownian motions Sigma Trend 18

19 Stochastic processes of multiple uncertainties Spot price processes for the Gas-Day-Ahead-Market, Gas Demand, oil price and FX rate: Spot price process: Long term price process: Gas demand: Oil price: FX rate: 19 Sigma long term price: Sigma short term price: Sigma demand: Sigma oil price: Alpha (Mean Reversion) short term price: Alpha (Mean Reversion) gas demand: Alpha (Mean Reversion) oil price: Correlation between gas demand and short term gas price: Uncorrelated Brownian Motions

20 Division of the planning horizon Problem: exponential growth of the problem with the number of stages in the tree ( curse of dimensionality) Solution: Division of the planning horizon into a limited number of periods at which the tree branches In each node of the tree, the DPFC is scaled to a certain scenario of the DPFC 12/5/ /22/ /02/ /4/ /25/ /19/ /11/ day 4 weeks 8 weeks 12 weeks 12 weeks 2 weks DPFC /MWh 20

21 Scenarios as deviations from DPFC 1. Scenarios of the logarithmic spot price x p for each period of the tree x 0 2. Scenarios of exp(x p 0.5 Var(x p )) exp (x ½ Var(x)) 1 3. Scenarios of DPFC t exp(x p 0.5 Var(x p )) DPFC exp (x ½ Var(x)) DPFC 21

22 Generation of scenario trees Estimation of stochastic process parameters Volatilities, Mean Reversions Correlations Analytic Integration of stochastic differencial equations in order to define the moments of the distributions (Var/Covar-Matrix) at every branching step of the scenario tree Approximation of the multidimensional standard normal distribution with multinomial distributions Transformation of the approximation of the standard normal distribution with the moments of the desired distribution at every step t of the scenario tree 22

23 Definition of the planning horizon Valuation date: Today Start/End Date: Defines the planning horizon The user can define the number and dates of the scenario tree branching steps 23

24 Definition of the stochastic spot price process The basis for the spot price scenario generation is a Daily price forward curvecurve) The parameters of volatility (standard deviation), mean reversion and correlation define the generation of the scenario tree 24

25 25 Set up of gas procurement portfolios (storages)

26 26 Set up of gas procurement portfolios (contracts)

27 27 Definition of min/max power of storages and contracts, min/max volume of storages

28 28 Definition of Forward-Portfolios (Prices, already closed positions)

29 29 Definition of liquidity and market depth of dayahead gas market

30 Modeling of gas storages Time series of min/max injection, withdrawal and volume Non linear constraints of maximum injection/withdrawal dependent on volume (piecewise linear approximations or stair curves ->integer modelling) Total depletion only at a maximum number of days Time series of injection/withdrawal costs Time series of injection/withdrawal losses Shrinkage of volume over time Stochastic outages / interruption of transport capacity 30

31 Modeling of gas markets / traded products Joint optimization of forward, spot (and balance market) products Maximum day ahead trading limits (market depth) Maximum forward trading limits Price influence of large traded positions (market elasticity) Lot size of traded products as integer numbers Availability of standard and non-standard products Representation of already closed positions 31

32 Representation of characteristics of flexible supply contracts Daily, monthly, quarterly, seasonal and yearly min/max quantities Discounts after withdrawal of specific quantities Oil price indexed and FX-rate dependent price Time lags in oil price indexation 32

33 Sensitivity of P&L distribution with different trading strategies Expected profits increase with high share of spot trading 33

34 Example of gas storage valuation results 34

")

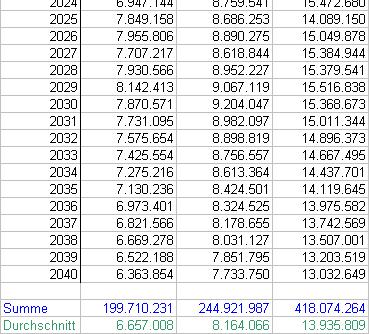

35 Gas Storage Valuation based on Least Square Monte Carlo (overall profit over 30 years) 35

36 Gas Storage Valuation based on Scenario Tree (overall profit over 30 years) 36

37 37 Sensitivities with short term spot price volatility

38 38 Sensitivities with short term spot price volatility

39 39 Sensitivities with long term spot price volatility

40 Conclusions Valuation of gas storages and gas procurement portfolios requires methods that consider path dependency in the decision process Tree based Stochastic Optimization is an approach to represent uncertainty and at the same time complex technical and contractual constraints in the portfolio Representation of uncertainty in the valuation and operation of gas procurement portfolios leads to lower expected procurement costs 40

Matlab Based Stochastic Processes in Stochastic Asset Portfolio Optimization

Matlab Based Stochastic Processes in Stochastic Asset Portfolio Optimization Workshop OR und Statistische Analyse mit Mathematischen Tools, May 13th, 2014 Dr. Georg Ostermaier, Ömer Kuzugüden Agenda Introduction

Matlab Based Stochastic Processes in Stochastic Asset Portfolio Optimization Workshop OR und Statistische Analyse mit Mathematischen Tools, May 13th, 2014 Dr. Georg Ostermaier, Ömer Kuzugüden Agenda Introduction

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

A Multi-Stage Stochastic Programming Model for Managing Risk-Optimal Electricity Portfolios. Stochastic Programming and Electricity Risk Management

A Multi-Stage Stochastic Programming Model for Managing Risk-Optimal Electricity Portfolios SLIDE 1 Outline Multi-stage stochastic programming modeling Setting - Electricity portfolio management Electricity

A Multi-Stage Stochastic Programming Model for Managing Risk-Optimal Electricity Portfolios SLIDE 1 Outline Multi-stage stochastic programming modeling Setting - Electricity portfolio management Electricity

STOCHASTIC PROGRAMMING FOR ASSET ALLOCATION IN PENSION FUNDS

STOCHASTIC PROGRAMMING FOR ASSET ALLOCATION IN PENSION FUNDS IEGOR RUDNYTSKYI JOINT WORK WITH JOËL WAGNER > city date

STOCHASTIC PROGRAMMING FOR ASSET ALLOCATION IN PENSION FUNDS IEGOR RUDNYTSKYI JOINT WORK WITH JOËL WAGNER > city date

Notes. Cases on Static Optimization. Chapter 6 Algorithms Comparison: The Swing Case

Notes Chapter 2 Optimization Methods 1. Stationary points are those points where the partial derivatives of are zero. Chapter 3 Cases on Static Optimization 1. For the interested reader, we used a multivariate

Notes Chapter 2 Optimization Methods 1. Stationary points are those points where the partial derivatives of are zero. Chapter 3 Cases on Static Optimization 1. For the interested reader, we used a multivariate

Contents Critique 26. portfolio optimization 32

Contents Preface vii 1 Financial problems and numerical methods 3 1.1 MATLAB environment 4 1.1.1 Why MATLAB? 5 1.2 Fixed-income securities: analysis and portfolio immunization 6 1.2.1 Basic valuation of

Contents Preface vii 1 Financial problems and numerical methods 3 1.1 MATLAB environment 4 1.1.1 Why MATLAB? 5 1.2 Fixed-income securities: analysis and portfolio immunization 6 1.2.1 Basic valuation of

Investigations on Factors Influencing the Operational Benefit of Stochastic Optimization in Generation and Trading Planning

Investigations on Factors Influencing the Operational Benefit of Stochastic Optimization in Generation and Trading Planning Introduction Stochastic Optimization Model Exemplary Investigations Summary Dipl.-Ing.

Investigations on Factors Influencing the Operational Benefit of Stochastic Optimization in Generation and Trading Planning Introduction Stochastic Optimization Model Exemplary Investigations Summary Dipl.-Ing.

Energy Systems under Uncertainty: Modeling and Computations

Energy Systems under Uncertainty: Modeling and Computations W. Römisch Humboldt-University Berlin Department of Mathematics www.math.hu-berlin.de/~romisch Systems Analysis 2015, November 11 13, IIASA (Laxenburg,

Energy Systems under Uncertainty: Modeling and Computations W. Römisch Humboldt-University Berlin Department of Mathematics www.math.hu-berlin.de/~romisch Systems Analysis 2015, November 11 13, IIASA (Laxenburg,

Implications of Spot Price Models on the Valuation of Gas Storages

Implications of Spot Price Models on the Valuation of Gas Storages LEF, Energy & Finance Dr. Sven-Olaf Stoll EnBW Trading GmbH Essen, 4th July 2012 Energie braucht Impulse Agenda Gas storage Valuation

Implications of Spot Price Models on the Valuation of Gas Storages LEF, Energy & Finance Dr. Sven-Olaf Stoll EnBW Trading GmbH Essen, 4th July 2012 Energie braucht Impulse Agenda Gas storage Valuation

Sensitivity Analysis for LPs - Webinar

Sensitivity Analysis for LPs - Webinar 25/01/2017 Arthur d Herbemont Agenda > I Introduction to Sensitivity Analysis > II Marginal values : Shadow prices and reduced costs > III Marginal ranges : RHS ranges

Sensitivity Analysis for LPs - Webinar 25/01/2017 Arthur d Herbemont Agenda > I Introduction to Sensitivity Analysis > II Marginal values : Shadow prices and reduced costs > III Marginal ranges : RHS ranges

Resource Planning with Uncertainty for NorthWestern Energy

Resource Planning with Uncertainty for NorthWestern Energy Selection of Optimal Resource Plan for 213 Resource Procurement Plan August 28, 213 Gary Dorris, Ph.D. Ascend Analytics, LLC gdorris@ascendanalytics.com

Resource Planning with Uncertainty for NorthWestern Energy Selection of Optimal Resource Plan for 213 Resource Procurement Plan August 28, 213 Gary Dorris, Ph.D. Ascend Analytics, LLC gdorris@ascendanalytics.com

The Value of Storage Forecasting storage flows and gas prices

Amsterdam, 9 May 2017 FLAME conference The Value of Storage Forecasting storage flows and gas prices www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS Energy Analytics Analytical solutions

Amsterdam, 9 May 2017 FLAME conference The Value of Storage Forecasting storage flows and gas prices www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS Energy Analytics Analytical solutions

Optimal Search for Parameters in Monte Carlo Simulation for Derivative Pricing

Optimal Search for Parameters in Monte Carlo Simulation for Derivative Pricing Prof. Chuan-Ju Wang Department of Computer Science University of Taipei Joint work with Prof. Ming-Yang Kao March 28, 2014

Optimal Search for Parameters in Monte Carlo Simulation for Derivative Pricing Prof. Chuan-Ju Wang Department of Computer Science University of Taipei Joint work with Prof. Ming-Yang Kao March 28, 2014

Dynamic Replication of Non-Maturing Assets and Liabilities

Dynamic Replication of Non-Maturing Assets and Liabilities Michael Schürle Institute for Operations Research and Computational Finance, University of St. Gallen, Bodanstr. 6, CH-9000 St. Gallen, Switzerland

Dynamic Replication of Non-Maturing Assets and Liabilities Michael Schürle Institute for Operations Research and Computational Finance, University of St. Gallen, Bodanstr. 6, CH-9000 St. Gallen, Switzerland

Introducing Uncertainty in Brazil's Oil Supply Chain

R&D Project IMPA-Petrobras Introducing Uncertainty in Brazil's Oil Supply Chain Juan Pablo Luna (UFRJ) Claudia Sagastizábal (IMPA visiting researcher) on behalf of OTIM-PBR team Workshop AASS, April 1st

R&D Project IMPA-Petrobras Introducing Uncertainty in Brazil's Oil Supply Chain Juan Pablo Luna (UFRJ) Claudia Sagastizábal (IMPA visiting researcher) on behalf of OTIM-PBR team Workshop AASS, April 1st

Market Risk Analysis Volume II. Practical Financial Econometrics

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Accelerated Option Pricing Multiple Scenarios

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

Multistage Stochastic Demand-side Management for Price-Making Major Consumers of Electricity in a Co-optimized Energy and Reserve Market

Multistage Stochastic Demand-side Management for Price-Making Major Consumers of Electricity in a Co-optimized Energy and Reserve Market Mahbubeh Habibian Anthony Downward Golbon Zakeri Abstract In this

Multistage Stochastic Demand-side Management for Price-Making Major Consumers of Electricity in a Co-optimized Energy and Reserve Market Mahbubeh Habibian Anthony Downward Golbon Zakeri Abstract In this

Brooks, Introductory Econometrics for Finance, 3rd Edition

P1.T2. Quantitative Analysis Brooks, Introductory Econometrics for Finance, 3rd Edition Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Chris Brooks,

P1.T2. Quantitative Analysis Brooks, Introductory Econometrics for Finance, 3rd Edition Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Chris Brooks,

Calculating VaR. There are several approaches for calculating the Value at Risk figure. The most popular are the

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

Sanjeev Chowdhri - Senior Product Manager, Analytics Lu Liu - Analytics Consultant SunGard Energy Solutions

Mr. Chowdhri is responsible for guiding the evolution of the risk management capabilities for SunGard s energy trading and risk software suite for Europe, and leads a team of analysts and designers in

Mr. Chowdhri is responsible for guiding the evolution of the risk management capabilities for SunGard s energy trading and risk software suite for Europe, and leads a team of analysts and designers in

Market interest-rate models

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Approximations of Stochastic Programs. Scenario Tree Reduction and Construction

Approximations of Stochastic Programs. Scenario Tree Reduction and Construction W. Römisch Humboldt-University Berlin Institute of Mathematics 10099 Berlin, Germany www.mathematik.hu-berlin.de/~romisch

Approximations of Stochastic Programs. Scenario Tree Reduction and Construction W. Römisch Humboldt-University Berlin Institute of Mathematics 10099 Berlin, Germany www.mathematik.hu-berlin.de/~romisch

Implementing Models in Quantitative Finance: Methods and Cases

Gianluca Fusai Andrea Roncoroni Implementing Models in Quantitative Finance: Methods and Cases vl Springer Contents Introduction xv Parti Methods 1 Static Monte Carlo 3 1.1 Motivation and Issues 3 1.1.1

Gianluca Fusai Andrea Roncoroni Implementing Models in Quantitative Finance: Methods and Cases vl Springer Contents Introduction xv Parti Methods 1 Static Monte Carlo 3 1.1 Motivation and Issues 3 1.1.1

UPDATED IAA EDUCATION SYLLABUS

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

Robust Optimization Applied to a Currency Portfolio

Robust Optimization Applied to a Currency Portfolio R. Fonseca, S. Zymler, W. Wiesemann, B. Rustem Workshop on Numerical Methods and Optimization in Finance June, 2009 OUTLINE Introduction Motivation &

Robust Optimization Applied to a Currency Portfolio R. Fonseca, S. Zymler, W. Wiesemann, B. Rustem Workshop on Numerical Methods and Optimization in Finance June, 2009 OUTLINE Introduction Motivation &

A Study on Optimal Limit Order Strategy using Multi-Period Stochastic Programming considering Nonexecution Risk

Proceedings of the Asia Pacific Industrial Engineering & Management Systems Conference 2018 A Study on Optimal Limit Order Strategy using Multi-Period Stochastic Programming considering Nonexecution Ris

Proceedings of the Asia Pacific Industrial Engineering & Management Systems Conference 2018 A Study on Optimal Limit Order Strategy using Multi-Period Stochastic Programming considering Nonexecution Ris

Multistage risk-averse asset allocation with transaction costs

Multistage risk-averse asset allocation with transaction costs 1 Introduction Václav Kozmík 1 Abstract. This paper deals with asset allocation problems formulated as multistage stochastic programming models.

Multistage risk-averse asset allocation with transaction costs 1 Introduction Václav Kozmík 1 Abstract. This paper deals with asset allocation problems formulated as multistage stochastic programming models.

Dynamic Asset and Liability Management Models for Pension Systems

Dynamic Asset and Liability Management Models for Pension Systems The Comparison between Multi-period Stochastic Programming Model and Stochastic Control Model Muneki Kawaguchi and Norio Hibiki June 1,

Dynamic Asset and Liability Management Models for Pension Systems The Comparison between Multi-period Stochastic Programming Model and Stochastic Control Model Muneki Kawaguchi and Norio Hibiki June 1,

Market Risk: FROM VALUE AT RISK TO STRESS TESTING. Agenda. Agenda (Cont.) Traditional Measures of Market Risk

Traditional Measures of Market Risk") Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

EC316a: Advanced Scientific Computation, Fall Discrete time, continuous state dynamic models: solution methods

EC316a: Advanced Scientific Computation, Fall 2003 Notes Section 4 Discrete time, continuous state dynamic models: solution methods We consider now solution methods for discrete time models in which decisions

EC316a: Advanced Scientific Computation, Fall 2003 Notes Section 4 Discrete time, continuous state dynamic models: solution methods We consider now solution methods for discrete time models in which decisions

Modeling Flexibilities in Power Purchase Agreements: a Real Option Approach

Modeling Flexibilities in Power Purchase Agreements: a Real Option Approach Rafael Igrejas a,*, Leonardo Lima Gomes a, Luiz E. Brandão a. Abstract Power purchase and sale contracts in Brazil, have been

Modeling Flexibilities in Power Purchase Agreements: a Real Option Approach Rafael Igrejas a,*, Leonardo Lima Gomes a, Luiz E. Brandão a. Abstract Power purchase and sale contracts in Brazil, have been

The Economics of Gas Storage Is there light at the end of the tunnel?

#1 in gas storage, swing & option valuation models The Economics of Gas Storage Is there light at the end of the tunnel? www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com Business case for

#1 in gas storage, swing & option valuation models The Economics of Gas Storage Is there light at the end of the tunnel? www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com Business case for

Gas storage: overview and static valuation

In this first article of the new gas storage segment of the Masterclass series, John Breslin, Les Clewlow, Tobias Elbert, Calvin Kwok and Chris Strickland provide an illustration of how the four most common

In this first article of the new gas storage segment of the Masterclass series, John Breslin, Les Clewlow, Tobias Elbert, Calvin Kwok and Chris Strickland provide an illustration of how the four most common

Robust Dual Dynamic Programming

1 / 18 Robust Dual Dynamic Programming Angelos Georghiou, Angelos Tsoukalas, Wolfram Wiesemann American University of Beirut Olayan School of Business 31 May 217 2 / 18 Inspired by SDDP Stochastic optimization

1 / 18 Robust Dual Dynamic Programming Angelos Georghiou, Angelos Tsoukalas, Wolfram Wiesemann American University of Beirut Olayan School of Business 31 May 217 2 / 18 Inspired by SDDP Stochastic optimization

Lattice Model of System Evolution. Outline

Lattice Model of System Evolution Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Massachusetts Institute of Technology Lattice Model Slide 1 of 48

Lattice Model of System Evolution Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Massachusetts Institute of Technology Lattice Model Slide 1 of 48

The Pennsylvania State University. The Graduate School. Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Neuro-Dynamic Programming for Fractionated Radiotherapy Planning

Neuro-Dynamic Programming for Fractionated Radiotherapy Planning Geng Deng Michael C. Ferris University of Wisconsin at Madison Conference on Optimization and Health Care, Feb, 2006 Background Optimal

Neuro-Dynamic Programming for Fractionated Radiotherapy Planning Geng Deng Michael C. Ferris University of Wisconsin at Madison Conference on Optimization and Health Care, Feb, 2006 Background Optimal

Scenario Construction and Reduction Applied to Stochastic Power Generation Expansion Planning

Industrial and Manufacturing Systems Engineering Publications Industrial and Manufacturing Systems Engineering 1-2013 Scenario Construction and Reduction Applied to Stochastic Power Generation Expansion

Industrial and Manufacturing Systems Engineering Publications Industrial and Manufacturing Systems Engineering 1-2013 Scenario Construction and Reduction Applied to Stochastic Power Generation Expansion

Scenario reduction and scenario tree construction for power management problems

Scenario reduction and scenario tree construction for power management problems N. Gröwe-Kuska, H. Heitsch and W. Römisch Humboldt-University Berlin Institute of Mathematics Page 1 of 20 IEEE Bologna POWER

Scenario reduction and scenario tree construction for power management problems N. Gröwe-Kuska, H. Heitsch and W. Römisch Humboldt-University Berlin Institute of Mathematics Page 1 of 20 IEEE Bologna POWER

Operational Risk Modeling

Operational Risk Modeling RMA Training (part 2) March 213 Presented by Nikolay Hovhannisyan Nikolay_hovhannisyan@mckinsey.com OH - 1 About the Speaker Senior Expert McKinsey & Co Implemented Operational

Operational Risk Modeling RMA Training (part 2) March 213 Presented by Nikolay Hovhannisyan Nikolay_hovhannisyan@mckinsey.com OH - 1 About the Speaker Senior Expert McKinsey & Co Implemented Operational

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

Computer Exercise 2 Simulation

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Fall 2017 Computer Exercise 2 Simulation This lab deals with pricing

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Fall 2017 Computer Exercise 2 Simulation This lab deals with pricing

Investigation of the and minimum storage energy target levels approach. Final Report

Investigation of the AV@R and minimum storage energy target levels approach Final Report First activity of the technical cooperation between Georgia Institute of Technology and ONS - Operador Nacional

Investigation of the AV@R and minimum storage energy target levels approach Final Report First activity of the technical cooperation between Georgia Institute of Technology and ONS - Operador Nacional

Option Pricing Using Monte Carlo Methods. A Directed Research Project. Submitted to the Faculty of the WORCESTER POLYTECHNIC INSTITUTE

Option Pricing Using Monte Carlo Methods A Directed Research Project Submitted to the Faculty of the WORCESTER POLYTECHNIC INSTITUTE in partial fulfillment of the requirements for the Professional Degree

Option Pricing Using Monte Carlo Methods A Directed Research Project Submitted to the Faculty of the WORCESTER POLYTECHNIC INSTITUTE in partial fulfillment of the requirements for the Professional Degree

ÖGOR - IHS Workshop und ÖGOR-Arbeitskreis

ÖGOR - IHS Workshop und ÖGOR-Arbeitskreis "MATHEMATISCHE ÖKONOMIE UND OPTIMIERUNG IN DER ENERGIEWIRTSCHAFT" 6TH "WORKSHOP ON STOCHASTIC AND DETERMINISTIC OPTIMISATION AND PRICE MODELLING IN POWER MARKETS

ÖGOR - IHS Workshop und ÖGOR-Arbeitskreis "MATHEMATISCHE ÖKONOMIE UND OPTIMIERUNG IN DER ENERGIEWIRTSCHAFT" 6TH "WORKSHOP ON STOCHASTIC AND DETERMINISTIC OPTIMISATION AND PRICE MODELLING IN POWER MARKETS

Practical example of an Economic Scenario Generator

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Risk Management for Chemical Supply Chain Planning under Uncertainty

for Chemical Supply Chain Planning under Uncertainty Fengqi You and Ignacio E. Grossmann Dept. of Chemical Engineering, Carnegie Mellon University John M. Wassick The Dow Chemical Company Introduction

for Chemical Supply Chain Planning under Uncertainty Fengqi You and Ignacio E. Grossmann Dept. of Chemical Engineering, Carnegie Mellon University John M. Wassick The Dow Chemical Company Introduction

Monte Carlo Methods in Structuring and Derivatives Pricing

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Numerical Methods in Option Pricing (Part III)

") Numerical Methods in Option Pricing (Part III) E. Explicit Finite Differences. Use of the Forward, Central, and Symmetric Central a. In order to obtain an explicit solution for the price of the derivative,

Numerical Methods in Option Pricing (Part III) E. Explicit Finite Differences. Use of the Forward, Central, and Symmetric Central a. In order to obtain an explicit solution for the price of the derivative,

STARRY GOLD ACADEMY , , Page 1

ICAN KNOWLEDGE LEVEL QUANTITATIVE TECHNIQUE IN BUSINESS MOCK EXAMINATION QUESTIONS FOR NOVEMBER 2016 DIET. INSTRUCTION: ATTEMPT ALL QUESTIONS IN THIS SECTION OBJECTIVE QUESTIONS Given the following sample

ICAN KNOWLEDGE LEVEL QUANTITATIVE TECHNIQUE IN BUSINESS MOCK EXAMINATION QUESTIONS FOR NOVEMBER 2016 DIET. INSTRUCTION: ATTEMPT ALL QUESTIONS IN THIS SECTION OBJECTIVE QUESTIONS Given the following sample

Cost Estimation as a Linear Programming Problem ISPA/SCEA Annual Conference St. Louis, Missouri

Cost Estimation as a Linear Programming Problem 2009 ISPA/SCEA Annual Conference St. Louis, Missouri Kevin Cincotta Andrew Busick Acknowledgments The author wishes to recognize and thank the following

Cost Estimation as a Linear Programming Problem 2009 ISPA/SCEA Annual Conference St. Louis, Missouri Kevin Cincotta Andrew Busick Acknowledgments The author wishes to recognize and thank the following

Bloomberg. Portfolio Value-at-Risk. Sridhar Gollamudi & Bryan Weber. September 22, Version 1.0

Portfolio Value-at-Risk Sridhar Gollamudi & Bryan Weber September 22, 2011 Version 1.0 Table of Contents 1 Portfolio Value-at-Risk 2 2 Fundamental Factor Models 3 3 Valuation methodology 5 3.1 Linear factor

Portfolio Value-at-Risk Sridhar Gollamudi & Bryan Weber September 22, 2011 Version 1.0 Table of Contents 1 Portfolio Value-at-Risk 2 2 Fundamental Factor Models 3 3 Valuation methodology 5 3.1 Linear factor

Martingale Pricing Theory in Discrete-Time and Discrete-Space Models

IEOR E4707: Foundations of Financial Engineering c 206 by Martin Haugh Martingale Pricing Theory in Discrete-Time and Discrete-Space Models These notes develop the theory of martingale pricing in a discrete-time,

IEOR E4707: Foundations of Financial Engineering c 206 by Martin Haugh Martingale Pricing Theory in Discrete-Time and Discrete-Space Models These notes develop the theory of martingale pricing in a discrete-time,

About the Risk Quantification of Technical Systems

About the Risk Quantification of Technical Systems Magda Schiegl ASTIN Colloquium 2013, The Hague Outline Introduction / Overview Fault Tree Analysis (FTA) Method of quantitative risk analysis Results

About the Risk Quantification of Technical Systems Magda Schiegl ASTIN Colloquium 2013, The Hague Outline Introduction / Overview Fault Tree Analysis (FTA) Method of quantitative risk analysis Results

Optimal Dam Management

Optimal Dam Management Michel De Lara et Vincent Leclère July 3, 2012 Contents 1 Problem statement 1 1.1 Dam dynamics.................................. 2 1.2 Intertemporal payoff criterion..........................

Optimal Dam Management Michel De Lara et Vincent Leclère July 3, 2012 Contents 1 Problem statement 1 1.1 Dam dynamics.................................. 2 1.2 Intertemporal payoff criterion..........................

Applications of Quantum Annealing in Computational Finance. Dr. Phil Goddard Head of Research, 1QBit D-Wave User Conference, Santa Fe, Sept.

Applications of Quantum Annealing in Computational Finance Dr. Phil Goddard Head of Research, 1QBit D-Wave User Conference, Santa Fe, Sept. 2016 Outline Where s my Babel Fish? Quantum-Ready Applications

Applications of Quantum Annealing in Computational Finance Dr. Phil Goddard Head of Research, 1QBit D-Wave User Conference, Santa Fe, Sept. 2016 Outline Where s my Babel Fish? Quantum-Ready Applications

DUALITY AND SENSITIVITY ANALYSIS

DUALITY AND SENSITIVITY ANALYSIS Understanding Duality No learning of Linear Programming is complete unless we learn the concept of Duality in linear programming. It is impossible to separate the linear

DUALITY AND SENSITIVITY ANALYSIS Understanding Duality No learning of Linear Programming is complete unless we learn the concept of Duality in linear programming. It is impossible to separate the linear

Simulation of delta hedging of an option with volume uncertainty. Marc LE DU, Clémence ALASSEUR EDF R&D - OSIRIS

Simulation of delta hedging of an option with volume uncertainty Marc LE DU, Clémence ALASSEUR EDF R&D - OSIRIS Agenda 1. Introduction : volume uncertainty 2. Test description: a simple option 3. Results

Simulation of delta hedging of an option with volume uncertainty Marc LE DU, Clémence ALASSEUR EDF R&D - OSIRIS Agenda 1. Introduction : volume uncertainty 2. Test description: a simple option 3. Results

Monte Carlo Simulations

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Puttable Bond and Vaulation

and Vaulation Dmitry Popov FinPricing http://www.finpricing.com Summary Puttable Bond Definition The Advantages of Puttable Bonds Puttable Bond Payoffs Valuation Model Selection Criteria LGM Model LGM

and Vaulation Dmitry Popov FinPricing http://www.finpricing.com Summary Puttable Bond Definition The Advantages of Puttable Bonds Puttable Bond Payoffs Valuation Model Selection Criteria LGM Model LGM

Monte Carlo Methods in Financial Engineering

Paul Glassennan Monte Carlo Methods in Financial Engineering With 99 Figures

Paul Glassennan Monte Carlo Methods in Financial Engineering With 99 Figures

Computer Exercise 2 Simulation

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Spring 2010 Computer Exercise 2 Simulation This lab deals with

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Spring 2010 Computer Exercise 2 Simulation This lab deals with

Parallel Multilevel Monte Carlo Simulation

Parallel Simulation Mathematisches Institut Goethe-Universität Frankfurt am Main Advances in Financial Mathematics Paris January 7-10, 2014 Simulation Outline 1 Monte Carlo 2 3 4 Algorithm Numerical Results

Parallel Simulation Mathematisches Institut Goethe-Universität Frankfurt am Main Advances in Financial Mathematics Paris January 7-10, 2014 Simulation Outline 1 Monte Carlo 2 3 4 Algorithm Numerical Results

4. Introduction to Prescriptive Analytics. BIA 674 Supply Chain Analytics

4. Introduction to Prescriptive Analytics BIA 674 Supply Chain Analytics Why is Decision Making difficult? The biggest sources of difficulty for decision making: Uncertainty Complexity of Environment or

4. Introduction to Prescriptive Analytics BIA 674 Supply Chain Analytics Why is Decision Making difficult? The biggest sources of difficulty for decision making: Uncertainty Complexity of Environment or

Computational Finance Least Squares Monte Carlo

Computational Finance Least Squares Monte Carlo School of Mathematics 2019 Monte Carlo and Binomial Methods In the last two lectures we discussed the binomial tree method and convergence problems. One

Computational Finance Least Squares Monte Carlo School of Mathematics 2019 Monte Carlo and Binomial Methods In the last two lectures we discussed the binomial tree method and convergence problems. One

Universitat Politècnica de Catalunya (UPC) - BarcelonaTech

- BarcelonaTech") Solving electricity market quadratic problems by Branch and Fix Coordination methods. F.-Javier Heredia 1,2, C. Corchero 1,2, Eugenio Mijangos 1,3 1 Group on Numerical Optimization and Modeling, Universitat

Solving electricity market quadratic problems by Branch and Fix Coordination methods. F.-Javier Heredia 1,2, C. Corchero 1,2, Eugenio Mijangos 1,3 1 Group on Numerical Optimization and Modeling, Universitat

RISK MANAGEMENT IN PUBLIC-PRIVATE PARTNERSHIP ROAD PROJECTS USING THE REAL OPTIONS THEORY

I International Symposium Engineering Management And Competitiveness 20 (EMC20) June 24-25, 20, Zrenjanin, Serbia RISK MANAGEMENT IN PUBLIC-PRIVATE PARTNERSHIP ROAD PROJECTS USING THE REAL OPTIONS THEORY

I International Symposium Engineering Management And Competitiveness 20 (EMC20) June 24-25, 20, Zrenjanin, Serbia RISK MANAGEMENT IN PUBLIC-PRIVATE PARTNERSHIP ROAD PROJECTS USING THE REAL OPTIONS THEORY

Markov Decision Processes

Markov Decision Processes Robert Platt Northeastern University Some images and slides are used from: 1. CS188 UC Berkeley 2. AIMA 3. Chris Amato Stochastic domains So far, we have studied search Can use

Markov Decision Processes Robert Platt Northeastern University Some images and slides are used from: 1. CS188 UC Berkeley 2. AIMA 3. Chris Amato Stochastic domains So far, we have studied search Can use

Combined Accumulation- and Decumulation-Plans with Risk-Controlled Capital Protection

Combined Accumulation- and Decumulation-Plans with Risk-Controlled Capital Protection Peter Albrecht and Carsten Weber University of Mannheim, Chair for Risk Theory, Portfolio Management and Insurance

Combined Accumulation- and Decumulation-Plans with Risk-Controlled Capital Protection Peter Albrecht and Carsten Weber University of Mannheim, Chair for Risk Theory, Portfolio Management and Insurance

Equity correlations implied by index options: estimation and model uncertainty analysis

1/18 : estimation and model analysis, EDHEC Business School (joint work with Rama COT) Modeling and managing financial risks Paris, 10 13 January 2011 2/18 Outline 1 2 of multi-asset models Solution to

1/18 : estimation and model analysis, EDHEC Business School (joint work with Rama COT) Modeling and managing financial risks Paris, 10 13 January 2011 2/18 Outline 1 2 of multi-asset models Solution to

Approximate Dynamic Programming for the Merchant Operations of Commodity and Energy Conversion Assets

Approximate Dynamic Programming for the Merchant Operations of Commodity and Energy Conversion Assets Selvaprabu (Selva) Nadarajah, (Joint work with François Margot and Nicola Secomandi) Tepper School

Approximate Dynamic Programming for the Merchant Operations of Commodity and Energy Conversion Assets Selvaprabu (Selva) Nadarajah, (Joint work with François Margot and Nicola Secomandi) Tepper School

Assessing dynamic hedging strategies

Düsseldorf, 5 April 2017 Energy portfolio optimisation and electricity price forecasting forum Assessing dynamic hedging strategies www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS

Düsseldorf, 5 April 2017 Energy portfolio optimisation and electricity price forecasting forum Assessing dynamic hedging strategies www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS

2.1 Mathematical Basis: Risk-Neutral Pricing

Chapter Monte-Carlo Simulation.1 Mathematical Basis: Risk-Neutral Pricing Suppose that F T is the payoff at T for a European-type derivative f. Then the price at times t before T is given by f t = e r(t

Chapter Monte-Carlo Simulation.1 Mathematical Basis: Risk-Neutral Pricing Suppose that F T is the payoff at T for a European-type derivative f. Then the price at times t before T is given by f t = e r(t

The Evaluation of Swing Contracts with Regime Switching. 6th World Congress of the Bachelier Finance Society Hilton, Toronto June

The Evaluation of Swing Contracts with Regime Switching Carl Chiarella, Les Clewlow and Boda Kang School of Finance and Economics University of Technology, Sydney Lacima Group, Sydney 6th World Congress

The Evaluation of Swing Contracts with Regime Switching Carl Chiarella, Les Clewlow and Boda Kang School of Finance and Economics University of Technology, Sydney Lacima Group, Sydney 6th World Congress

Numerical schemes for SDEs

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

SIMULATION OF ELECTRICITY MARKETS

SIMULATION OF ELECTRICITY MARKETS MONTE CARLO METHODS Lectures 15-18 in EG2050 System Planning Mikael Amelin 1 COURSE OBJECTIVES To pass the course, the students should show that they are able to - apply

SIMULATION OF ELECTRICITY MARKETS MONTE CARLO METHODS Lectures 15-18 in EG2050 System Planning Mikael Amelin 1 COURSE OBJECTIVES To pass the course, the students should show that they are able to - apply

Stochastic Dual Dynamic Programming

1 / 43 Stochastic Dual Dynamic Programming Operations Research Anthony Papavasiliou 2 / 43 Contents [ 10.4 of BL], [Pereira, 1991] 1 Recalling the Nested L-Shaped Decomposition 2 Drawbacks of Nested Decomposition

1 / 43 Stochastic Dual Dynamic Programming Operations Research Anthony Papavasiliou 2 / 43 Contents [ 10.4 of BL], [Pereira, 1991] 1 Recalling the Nested L-Shaped Decomposition 2 Drawbacks of Nested Decomposition

Valuation of Transmission Assets and Projects. Transmission Investment: Opportunities in Asset Sales, Recapitalization and Enhancements

Valuation of Transmission Assets and Projects Assef Zobian Cambridge Energy Solutions Alex Rudkevich Tabors Caramanis and Associates Transmission Investment: Opportunities in Asset Sales, Recapitalization

Valuation of Transmission Assets and Projects Assef Zobian Cambridge Energy Solutions Alex Rudkevich Tabors Caramanis and Associates Transmission Investment: Opportunities in Asset Sales, Recapitalization

Chapter 2 Linear programming... 2 Chapter 3 Simplex... 4 Chapter 4 Sensitivity Analysis and duality... 5 Chapter 5 Network... 8 Chapter 6 Integer

目录 Chapter 2 Linear programming... 2 Chapter 3 Simplex... 4 Chapter 4 Sensitivity Analysis and duality... 5 Chapter 5 Network... 8 Chapter 6 Integer Programming... 10 Chapter 7 Nonlinear Programming...

目录 Chapter 2 Linear programming... 2 Chapter 3 Simplex... 4 Chapter 4 Sensitivity Analysis and duality... 5 Chapter 5 Network... 8 Chapter 6 Integer Programming... 10 Chapter 7 Nonlinear Programming...

Stochastic Finance 2010 Summer School Ulm Lecture 1: Energy Derivatives

Stochastic Finance 2010 Summer School Ulm Lecture 1: Energy Derivatives Professor Dr. Rüdiger Kiesel 21. September 2010 1 / 62 1 Energy Markets Spot Market Futures Market 2 Typical models Schwartz Model

Stochastic Finance 2010 Summer School Ulm Lecture 1: Energy Derivatives Professor Dr. Rüdiger Kiesel 21. September 2010 1 / 62 1 Energy Markets Spot Market Futures Market 2 Typical models Schwartz Model

Fast Convergence of Regress-later Series Estimators

Fast Convergence of Regress-later Series Estimators New Thinking in Finance, London Eric Beutner, Antoon Pelsser, Janina Schweizer Maastricht University & Kleynen Consultants 12 February 2014 Beutner Pelsser

Fast Convergence of Regress-later Series Estimators New Thinking in Finance, London Eric Beutner, Antoon Pelsser, Janina Schweizer Maastricht University & Kleynen Consultants 12 February 2014 Beutner Pelsser

Financial Risk Modeling on Low-power Accelerators: Experimental Performance Evaluation of TK1 with FPGA

Financial Risk Modeling on Low-power Accelerators: Experimental Performance Evaluation of TK1 with FPGA Rajesh Bordawekar and Daniel Beece IBM T. J. Watson Research Center 3/17/2015 2014 IBM Corporation

Financial Risk Modeling on Low-power Accelerators: Experimental Performance Evaluation of TK1 with FPGA Rajesh Bordawekar and Daniel Beece IBM T. J. Watson Research Center 3/17/2015 2014 IBM Corporation

"Vibrato" Monte Carlo evaluation of Greeks

"Vibrato" Monte Carlo evaluation of Greeks (Smoking Adjoints: part 3) Mike Giles mike.giles@maths.ox.ac.uk Oxford University Mathematical Institute Oxford-Man Institute of Quantitative Finance MCQMC 2008,

"Vibrato" Monte Carlo evaluation of Greeks (Smoking Adjoints: part 3) Mike Giles mike.giles@maths.ox.ac.uk Oxford University Mathematical Institute Oxford-Man Institute of Quantitative Finance MCQMC 2008,

Computational Finance Binomial Trees Analysis

Computational Finance Binomial Trees Analysis School of Mathematics 2018 Review - Binomial Trees Developed a multistep binomial lattice which will approximate the value of a European option Extended the

Computational Finance Binomial Trees Analysis School of Mathematics 2018 Review - Binomial Trees Developed a multistep binomial lattice which will approximate the value of a European option Extended the

ANALYSIS OF THE BINOMIAL METHOD

ANALYSIS OF THE BINOMIAL METHOD School of Mathematics 2013 OUTLINE 1 CONVERGENCE AND ERRORS OUTLINE 1 CONVERGENCE AND ERRORS 2 EXOTIC OPTIONS American Options Computational Effort OUTLINE 1 CONVERGENCE

ANALYSIS OF THE BINOMIAL METHOD School of Mathematics 2013 OUTLINE 1 CONVERGENCE AND ERRORS OUTLINE 1 CONVERGENCE AND ERRORS 2 EXOTIC OPTIONS American Options Computational Effort OUTLINE 1 CONVERGENCE

Commodity and Energy Markets

Lecture 3 - Spread Options p. 1/19 Commodity and Energy Markets (Princeton RTG summer school in financial mathematics) Lecture 3 - Spread Option Pricing Michael Coulon and Glen Swindle June 17th - 28th,

Lecture 3 - Spread Options p. 1/19 Commodity and Energy Markets (Princeton RTG summer school in financial mathematics) Lecture 3 - Spread Option Pricing Michael Coulon and Glen Swindle June 17th - 28th,

IMPA Commodities Course: Introduction

IMPA Commodities Course: Introduction Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Department of Statistics and Mathematical Finance Program, University of Toronto, Toronto, Canada http://www.utstat.utoronto.ca/sjaimung

IMPA Commodities Course: Introduction Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Department of Statistics and Mathematical Finance Program, University of Toronto, Toronto, Canada http://www.utstat.utoronto.ca/sjaimung

Dynamic Portfolio Choice II

Dynamic Portfolio Choice II Dynamic Programming Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Dynamic Portfolio Choice II 15.450, Fall 2010 1 / 35 Outline 1 Introduction to Dynamic

Dynamic Portfolio Choice II Dynamic Programming Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Dynamic Portfolio Choice II 15.450, Fall 2010 1 / 35 Outline 1 Introduction to Dynamic

Monte Carlo Methods in Finance

Monte Carlo Methods in Finance Peter Jackel JOHN WILEY & SONS, LTD Preface Acknowledgements Mathematical Notation xi xiii xv 1 Introduction 1 2 The Mathematics Behind Monte Carlo Methods 5 2.1 A Few Basic

Monte Carlo Methods in Finance Peter Jackel JOHN WILEY & SONS, LTD Preface Acknowledgements Mathematical Notation xi xiii xv 1 Introduction 1 2 The Mathematics Behind Monte Carlo Methods 5 2.1 A Few Basic

Introductory Econometrics for Finance

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

ROBUST OPTIMIZATION OF MULTI-PERIOD PRODUCTION PLANNING UNDER DEMAND UNCERTAINTY. A. Ben-Tal, B. Golany and M. Rozenblit

ROBUST OPTIMIZATION OF MULTI-PERIOD PRODUCTION PLANNING UNDER DEMAND UNCERTAINTY A. Ben-Tal, B. Golany and M. Rozenblit Faculty of Industrial Engineering and Management, Technion, Haifa 32000, Israel ABSTRACT

ROBUST OPTIMIZATION OF MULTI-PERIOD PRODUCTION PLANNING UNDER DEMAND UNCERTAINTY A. Ben-Tal, B. Golany and M. Rozenblit Faculty of Industrial Engineering and Management, Technion, Haifa 32000, Israel ABSTRACT

MFE Course Details. Financial Mathematics & Statistics

MFE Course Details Financial Mathematics & Statistics FE8506 Calculus & Linear Algebra This course covers mathematical tools and concepts for solving problems in financial engineering. It will also help

MFE Course Details Financial Mathematics & Statistics FE8506 Calculus & Linear Algebra This course covers mathematical tools and concepts for solving problems in financial engineering. It will also help

To apply SP models we need to generate scenarios which represent the uncertainty IN A SENSIBLE WAY, taking into account

Scenario Generation To apply SP models we need to generate scenarios which represent the uncertainty IN A SENSIBLE WAY, taking into account the goal of the model and its structure, the available information,

Scenario Generation To apply SP models we need to generate scenarios which represent the uncertainty IN A SENSIBLE WAY, taking into account the goal of the model and its structure, the available information,

Oil prices and depletion path

Pierre-Noël GIRAUD (CERNA, Paris) Aline SUTTER Timothée DENIS (EDF R&D) timothee.denis@edf.fr Oil prices and depletion path Hubbert oil peak and Hotelling rent through a combined Simulation and Optimisation

Pierre-Noël GIRAUD (CERNA, Paris) Aline SUTTER Timothée DENIS (EDF R&D) timothee.denis@edf.fr Oil prices and depletion path Hubbert oil peak and Hotelling rent through a combined Simulation and Optimisation

Advanced Operations Research Prof. G. Srinivasan Dept of Management Studies Indian Institute of Technology, Madras

Advanced Operations Research Prof. G. Srinivasan Dept of Management Studies Indian Institute of Technology, Madras Lecture 23 Minimum Cost Flow Problem In this lecture, we will discuss the minimum cost

Advanced Operations Research Prof. G. Srinivasan Dept of Management Studies Indian Institute of Technology, Madras Lecture 23 Minimum Cost Flow Problem In this lecture, we will discuss the minimum cost

Gamma. The finite-difference formula for gamma is

Gamma The finite-difference formula for gamma is [ P (S + ɛ) 2 P (S) + P (S ɛ) e rτ E ɛ 2 ]. For a correlation option with multiple underlying assets, the finite-difference formula for the cross gammas

Gamma The finite-difference formula for gamma is [ P (S + ɛ) 2 P (S) + P (S ɛ) e rτ E ɛ 2 ]. For a correlation option with multiple underlying assets, the finite-difference formula for the cross gammas

APPROXIMATING FREE EXERCISE BOUNDARIES FOR AMERICAN-STYLE OPTIONS USING SIMULATION AND OPTIMIZATION. Barry R. Cobb John M. Charnes

Proceedings of the 2004 Winter Simulation Conference R. G. Ingalls, M. D. Rossetti, J. S. Smith, and B. A. Peters, eds. APPROXIMATING FREE EXERCISE BOUNDARIES FOR AMERICAN-STYLE OPTIONS USING SIMULATION

Proceedings of the 2004 Winter Simulation Conference R. G. Ingalls, M. D. Rossetti, J. S. Smith, and B. A. Peters, eds. APPROXIMATING FREE EXERCISE BOUNDARIES FOR AMERICAN-STYLE OPTIONS USING SIMULATION