Implications of Spot Price Models on the Valuation of Gas Storages

|

|

|

- Brianne Foster

- 5 years ago

- Views:

Transcription

1 Implications of Spot Price Models on the Valuation of Gas Storages LEF, Energy & Finance Dr. Sven-Olaf Stoll EnBW Trading GmbH Essen, 4th July 2012 Energie braucht Impulse

2 Agenda Gas storage Valuation of gas storages Spot price model Example: Valuation of gas storages Conclusions 2I

3 Gas storage Asset to inject or withdraw gas, e.g. depleted gas reservoir, salt cavern Source: NUON 3I

4 Gas storage Asset to inject or withdraw gas, e.g. depleted gas reservoir, salt cavern Natural gas is stored to structure delivery according to variations in demand seasonal load variations intraday load profile Physical storage capacities and virtual storage contracts are auctioned by several storage companies (e.g. E.On Gas Storage (D), Centrica Storage (UK)) Daily or hourly execution rights, but on the spot market natural gas is traded only on daily basis Source: NUON 4I

5 Gas storage 5I Asset to inject or withdraw gas, e.g. depleted gas reservoir, salt cavern Natural gas is stored to structure delivery according to variations in demand seasonal load variations intraday load profile Physical storage capacities and virtual storage contracts are auctioned by several storage companies (e.g. E.On Gas Storage (D), Centrica Storage (UK)) Daily or hourly execution rights, but on the spot market natural gas is traded only on daily basis Valuation is done via Least Squares Monte Carlo References: A. Boogert, C. de Jong: Gas Storage Valuation Using a Monte Carlo Method; Journal of Derivatives, Spring 2008

6 Agenda Gas storage Valuation of gas storages Spot price model Example: Valuation of gas storages Conclusions 6I

7 Technical Conditions for Gas Storages Storage volume: maximum working gas volume on day d minimum working gas volume on day d actual working gas volume content on day d (positive variable) Injection: maximum injection rate on day d as a function of the working gas volume level actual injection rate (positive variable) injection costs on day d as a function of the working gas volume level Withdrawal: maximum withdrawal rate on day d as a function of the working gas volume level actual withdrawal rate (positive variable) withdrawal costs on day d as a function of the working gas volume level Initial condition: Final condition: working gas volume at start of valuation period working gas volume at the end of the valuation period 7I

8 Valuation and Optimal Scheduling Problem Statement storage balance Constraints Value function Fair option value (risk neutral measure Q) at time : 8I

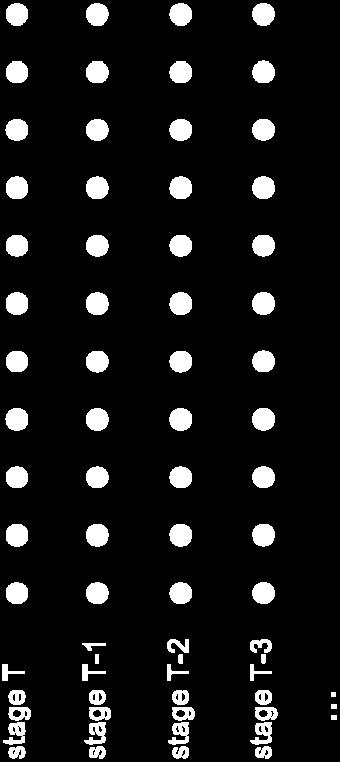

9 Dynamic Programming: Discretization (1) volume level in storage grid point 9I

10 Dynamic Programming: Discretization (2) volume level in storage grid point 10 I

11 Dynamic Programming: Interpolation If injection and withdrawal rates are not integer multiples of the grid distance: Interpolate between continuation values for adjoint grid points 11 I

12 Dynamic Program for Gas Storages Dynamic program: start with allowed grid points at time step T initialize continuation values with zeros (grid point, price scenario ) recursively step back in time 1. discount continuation value to actual time for allowed grid points 2. calculate reachable grid points and all allowed actions 3. maximise sum of immediate payoffs and future cashflows here h is the immediate payoff from injection ( ) or withdrawal ( ) Calculate option value as mean (starting volume ): What is the fair value? 12 I

13 Least Squares Monte Carlo Stochastic dynamic program (cf. Boogert and de Jong (2008)): start with allowed grid points at time step T initialize continuation values with zeros (grid point, price scenario ) recursively step back in time 1. discount continuation value to actual time for allowed grid points 2. calculate reachable grid points and all allowed actions 3. Approximate continuation value using a set of basis functions by regression 4. maximise sum of immediate payoffs and future cashflows here h is the immediate payoff from injection of withdrawal Calculate option value as scenario mean (starting volume ): 13 I

14 Agenda Gas storage Valuation of gas storages Spot price model Example: Valuation of gas storages Conclusions 14 I

15 Natural Gas Prices Properties of Spot Price Time Series beginning of financial crisis Gas price in EUR/MWh TTF Spot Prices 15 I

16 Natural Gas Prices Is there a naive seasonality? trigonometric fit does not lead to satisfying results trend is significant Gas price in EUR/MWh 16 I

17 Natural Gas Prices Are there any further influencing variables? Idea 1: In winter gas price is influenced by available storage volume. Storage volume data is not sufficient. Storage demand strongly depends on temperature. Longer periods of cold weather lead to low storage volume and increasing spot market prices. Idea 2: Gas is imported by long term contracts which are indexed on oil price by formulas. Typical formulas are 6-1-3, 6-3-3, or date of calculation Gas oil and fuel oil price formulas are widely used. 1 month delay 17 I 6 months average Valid for 3 months

18 Influencing Variables Heating Degree Days Heating Degree Days HDD = max(15-temperature;0) Cumulated Heating Degree Days (Winter) CHDD(t) = Sum of all HDDs in winter up to day t Cumulated Heating Degree Days for norm winter MCHDD(t) = Mean of CHDD(t) for all historic winters Deviation of CHDD from norm winter: DCHDD for Eindhoven DCHDD(t) = CHDD(t) MCHDD(t) In summer linear interpolation down to 0 18 I

19 Seasonality with DCHDD DCHDD can capture behaviour in warm and cold winters trend is still significant Gas price in EUR/MWh residuals are stationary 19 I

20 Seasonality with DCHDD What happened during the financial crisis? Gas price in EUR/MWh 20 I

21 Influencing Variables Oil price component Correlation between gas oil, fuel oil and Brent crude oil is 97% - 99%. Thus, choose Brent because of longer history and better quality of data. Use formulas to include smoothing and time lag. Formula R 2 of regression I

22 Seasonality with DCHDD and oil formula Fit until end of 2009 Gas price in EUR/MWh 22 I

23 Seasonality with DCHDD and oil formula Fit until end of 2008 Gas price in EUR/MWh 23 I

24 Residuals Stationary or not? modelled dependence on heating degree days modelled dependence on heating degree days and oil price component 24 I

25 Stochastic Model X t m s S a f g ( ) t t t 1 ( t ) a 2 t Y t m t s t linear trend weekly seasonality S t yearly seasonality f Y t ( t g ( t ) ) Normalised cumulative heating degree days with linear return to 0 during summer oil formula for Brent crude oil stochastic component: ARMA(2,1) process with variance gamma innovations 25 I

26 Simulation paths 26 I

27 Agenda Gas storage Valuation of gas storages Spot price model Example: Valuation of gas storages Conclusions 27 I

28 Examples: Gas storage valuation Storage 1 Storage 2 Start date End date Max. volume (MWh) Initial volume (MWh) Injection rate (MW) Withdrawal rate (MW) Injections costs ( /MWh) 0 0,30 Withdrawal costs ( /MWh) Valuation without oil component ( ) % difference in valuation! Valuation with oil component ( ) I

29 Agenda Gas storage Valuation of gas storages Spot price model Example: Valuation of gas storages Conclusions 29 I

30 Conclusion Significant parts of gas spot prices behaviour can be explained by using exogenous variables as regressors. Using NCHDD as fundamental component reduces volatility often overestimated by other models. The second fundamental component is oil which can explain behaviour during financial crisis Good models including fundamental components are important for valuation and trading decisions. References: A. Boogert, C. de Jong: Gas Storage Valuation Using a Monte Carlo Method; Journal of Derivatives, Spring 2008 S.O. Stoll, K. Wiebauer: A Spot Price Model for Natural Gas Considering Temperature as Exogenous Factor and Applications; Journal of Energy Markets, I J. Müller: Ein gekoppeltes Spotmarktmodell für Öl- und Gaspreise; Master Thesis, University of Siegen, 2010.

31 Thank you for your attention! EnBW Trading GmbH Sven-Olaf Stoll Durlacher Allee 93 D Karlsruhe tel Energie braucht Impulse

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

Stochastic Programming in Gas Storage and Gas Portfolio Management. ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier

Stochastic Programming in Gas Storage and Gas Portfolio Management ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier Agenda Optimization tasks in gas storage and gas portfolio management Scenario

Stochastic Programming in Gas Storage and Gas Portfolio Management ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier Agenda Optimization tasks in gas storage and gas portfolio management Scenario

Energy Systems under Uncertainty: Modeling and Computations

Energy Systems under Uncertainty: Modeling and Computations W. Römisch Humboldt-University Berlin Department of Mathematics www.math.hu-berlin.de/~romisch Systems Analysis 2015, November 11 13, IIASA (Laxenburg,

Energy Systems under Uncertainty: Modeling and Computations W. Römisch Humboldt-University Berlin Department of Mathematics www.math.hu-berlin.de/~romisch Systems Analysis 2015, November 11 13, IIASA (Laxenburg,

Assessing dynamic hedging strategies

Düsseldorf, 5 April 2017 Energy portfolio optimisation and electricity price forecasting forum Assessing dynamic hedging strategies www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS

Düsseldorf, 5 April 2017 Energy portfolio optimisation and electricity price forecasting forum Assessing dynamic hedging strategies www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS

The Value of Storage Forecasting storage flows and gas prices

Amsterdam, 9 May 2017 FLAME conference The Value of Storage Forecasting storage flows and gas prices www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS Energy Analytics Analytical solutions

Amsterdam, 9 May 2017 FLAME conference The Value of Storage Forecasting storage flows and gas prices www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS Energy Analytics Analytical solutions

Clearing Manager. Financial Transmission Rights. Prudential Security Assessment Methodology. 18 September with September 2015 variation

Clearing Manager Financial Transmission Rights Prudential Security Assessment Methodology with September 2015 variation 18 September 2015 To apply from 9 October 2015 Author: Warwick Small Document owner:

Clearing Manager Financial Transmission Rights Prudential Security Assessment Methodology with September 2015 variation 18 September 2015 To apply from 9 October 2015 Author: Warwick Small Document owner:

Notes. Cases on Static Optimization. Chapter 6 Algorithms Comparison: The Swing Case

Notes Chapter 2 Optimization Methods 1. Stationary points are those points where the partial derivatives of are zero. Chapter 3 Cases on Static Optimization 1. For the interested reader, we used a multivariate

Notes Chapter 2 Optimization Methods 1. Stationary points are those points where the partial derivatives of are zero. Chapter 3 Cases on Static Optimization 1. For the interested reader, we used a multivariate

Volatility, risk, and risk-premium in German and Continental power markets

Volatility, risk, and risk-premium in German and Continental power markets Stefan Judisch Supply & Trading GmbH RWE Supply & Trading PAGE 0 Agenda 1. What are the market fundamentals telling us? 2. What

Volatility, risk, and risk-premium in German and Continental power markets Stefan Judisch Supply & Trading GmbH RWE Supply & Trading PAGE 0 Agenda 1. What are the market fundamentals telling us? 2. What

Gas storage: overview and static valuation

In this first article of the new gas storage segment of the Masterclass series, John Breslin, Les Clewlow, Tobias Elbert, Calvin Kwok and Chris Strickland provide an illustration of how the four most common

In this first article of the new gas storage segment of the Masterclass series, John Breslin, Les Clewlow, Tobias Elbert, Calvin Kwok and Chris Strickland provide an illustration of how the four most common

Volatility, risk, and risk-premium in German and Continental power markets. Stefan Judisch Supply & Trading GmbH 3 rd April 2014

Volatility, risk, and risk-premium in German and Continental power markets Stefan Judisch Supply & Trading GmbH 3 rd April 2014 RWE Supply & Trading 01/04/2014 PAGE 0 Agenda 1. What are the market fundamentals

Volatility, risk, and risk-premium in German and Continental power markets Stefan Judisch Supply & Trading GmbH 3 rd April 2014 RWE Supply & Trading 01/04/2014 PAGE 0 Agenda 1. What are the market fundamentals

The Economics of Gas Storage Is there light at the end of the tunnel?

#1 in gas storage, swing & option valuation models The Economics of Gas Storage Is there light at the end of the tunnel? www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com Business case for

#1 in gas storage, swing & option valuation models The Economics of Gas Storage Is there light at the end of the tunnel? www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com Business case for

Berlin, 10 th February 2017

Forecasting the Distribution of Hourly Electricity Spot Prices - Accounting for Cross Correlation Patterns and Non-Normality of Price Distributions Arne Vogler Co-Authors: Christoph Weber, Christian Pape

Forecasting the Distribution of Hourly Electricity Spot Prices - Accounting for Cross Correlation Patterns and Non-Normality of Price Distributions Arne Vogler Co-Authors: Christoph Weber, Christian Pape

Investigations on Factors Influencing the Operational Benefit of Stochastic Optimization in Generation and Trading Planning

Investigations on Factors Influencing the Operational Benefit of Stochastic Optimization in Generation and Trading Planning Introduction Stochastic Optimization Model Exemplary Investigations Summary Dipl.-Ing.

Investigations on Factors Influencing the Operational Benefit of Stochastic Optimization in Generation and Trading Planning Introduction Stochastic Optimization Model Exemplary Investigations Summary Dipl.-Ing.

Simulation of delta hedging of an option with volume uncertainty. Marc LE DU, Clémence ALASSEUR EDF R&D - OSIRIS

Simulation of delta hedging of an option with volume uncertainty Marc LE DU, Clémence ALASSEUR EDF R&D - OSIRIS Agenda 1. Introduction : volume uncertainty 2. Test description: a simple option 3. Results

Simulation of delta hedging of an option with volume uncertainty Marc LE DU, Clémence ALASSEUR EDF R&D - OSIRIS Agenda 1. Introduction : volume uncertainty 2. Test description: a simple option 3. Results

Commodity and Energy Markets

Lecture 3 - Spread Options p. 1/19 Commodity and Energy Markets (Princeton RTG summer school in financial mathematics) Lecture 3 - Spread Option Pricing Michael Coulon and Glen Swindle June 17th - 28th,

Lecture 3 - Spread Options p. 1/19 Commodity and Energy Markets (Princeton RTG summer school in financial mathematics) Lecture 3 - Spread Option Pricing Michael Coulon and Glen Swindle June 17th - 28th,

HYDROPOWER OPERATION IN A CHANGING ENVIRONMENT

HYDROPOWER OPERATION IN A CHANGING ENVIRONMENT Moritz Schillinger 1, Hannes Weigt 1, Michael Barry 2, René Schumann 2 1 University of Basel, 2 HES-SO Valais IEWT 2017 - Session 1C: Erneuerbare Energien

HYDROPOWER OPERATION IN A CHANGING ENVIRONMENT Moritz Schillinger 1, Hannes Weigt 1, Michael Barry 2, René Schumann 2 1 University of Basel, 2 HES-SO Valais IEWT 2017 - Session 1C: Erneuerbare Energien

Analysis and Enhancement of Prac4ce- based Methods for the Real Op4on Management of Commodity Storage Assets

Analysis and Enhancement of Prac4ce- based Methods for the Real Op4on Management of Commodity Storage Assets Nicola Secomandi Carnegie Mellon Tepper School of Business ns7@andrew.cmu.edu Interna4onal Conference

Analysis and Enhancement of Prac4ce- based Methods for the Real Op4on Management of Commodity Storage Assets Nicola Secomandi Carnegie Mellon Tepper School of Business ns7@andrew.cmu.edu Interna4onal Conference

Resource Planning with Uncertainty for NorthWestern Energy

Resource Planning with Uncertainty for NorthWestern Energy Selection of Optimal Resource Plan for 213 Resource Procurement Plan August 28, 213 Gary Dorris, Ph.D. Ascend Analytics, LLC gdorris@ascendanalytics.com

Resource Planning with Uncertainty for NorthWestern Energy Selection of Optimal Resource Plan for 213 Resource Procurement Plan August 28, 213 Gary Dorris, Ph.D. Ascend Analytics, LLC gdorris@ascendanalytics.com

The histogram should resemble the uniform density, the mean should be close to 0.5, and the standard deviation should be close to 1/ 12 =

Chapter 19 Monte Carlo Valuation Question 19.1 The histogram should resemble the uniform density, the mean should be close to.5, and the standard deviation should be close to 1/ 1 =.887. Question 19. The

Chapter 19 Monte Carlo Valuation Question 19.1 The histogram should resemble the uniform density, the mean should be close to.5, and the standard deviation should be close to 1/ 1 =.887. Question 19. The

Managing your profits using temperature and commodity price protection

Managing your profits using temperature and commodity price protection What affects my business? Your earnings volatility Temperature Commodity Prices Dec13 Feb14-1981-2010 anomaly European Climate Assessment

Managing your profits using temperature and commodity price protection What affects my business? Your earnings volatility Temperature Commodity Prices Dec13 Feb14-1981-2010 anomaly European Climate Assessment

Jaime Frade Dr. Niu Interest rate modeling

Interest rate modeling Abstract In this paper, three models were used to forecast short term interest rates for the 3 month LIBOR. Each of the models, regression time series, GARCH, and Cox, Ingersoll,

Interest rate modeling Abstract In this paper, three models were used to forecast short term interest rates for the 3 month LIBOR. Each of the models, regression time series, GARCH, and Cox, Ingersoll,

Forecasting Design Day Demand Using Extremal Quantile Regression

Forecasting Design Day Demand Using Extremal Quantile Regression David J. Kaftan, Jarrett L. Smalley, George F. Corliss, Ronald H. Brown, and Richard J. Povinelli GasDay Project, Marquette University,

Forecasting Design Day Demand Using Extremal Quantile Regression David J. Kaftan, Jarrett L. Smalley, George F. Corliss, Ronald H. Brown, and Richard J. Povinelli GasDay Project, Marquette University,

Optimal Bidding Strategies in Electricity Markets*

Optimal Bidding Strategies in Electricity Markets* R. Rajaraman December 14, 2004 (*) New PSERC report co-authored with Prof. Fernando Alvarado slated for release in early 2005 PSERC December 2004 1 Opening

Optimal Bidding Strategies in Electricity Markets* R. Rajaraman December 14, 2004 (*) New PSERC report co-authored with Prof. Fernando Alvarado slated for release in early 2005 PSERC December 2004 1 Opening

Sanjeev Chowdhri - Senior Product Manager, Analytics Lu Liu - Analytics Consultant SunGard Energy Solutions

Mr. Chowdhri is responsible for guiding the evolution of the risk management capabilities for SunGard s energy trading and risk software suite for Europe, and leads a team of analysts and designers in

Mr. Chowdhri is responsible for guiding the evolution of the risk management capabilities for SunGard s energy trading and risk software suite for Europe, and leads a team of analysts and designers in

Financial Econometrics Notes. Kevin Sheppard University of Oxford

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Matlab Based Stochastic Processes in Stochastic Asset Portfolio Optimization

Matlab Based Stochastic Processes in Stochastic Asset Portfolio Optimization Workshop OR und Statistische Analyse mit Mathematischen Tools, May 13th, 2014 Dr. Georg Ostermaier, Ömer Kuzugüden Agenda Introduction

Matlab Based Stochastic Processes in Stochastic Asset Portfolio Optimization Workshop OR und Statistische Analyse mit Mathematischen Tools, May 13th, 2014 Dr. Georg Ostermaier, Ömer Kuzugüden Agenda Introduction

The pricing of temperature futures at the Chicago Mercantile Exchange

The pricing of temperature futures at the Chicago Mercantile Exchange Journal of Banking & Finance 34 (6), pp 1360 1370 Agenda 1 Index Modeling 2 Modeling market prices 3 Trading strategies 4 Conclusion

The pricing of temperature futures at the Chicago Mercantile Exchange Journal of Banking & Finance 34 (6), pp 1360 1370 Agenda 1 Index Modeling 2 Modeling market prices 3 Trading strategies 4 Conclusion

Value of Midstream Flexibility

Value of Midstream Flexibility Alexey Gnatyuk Head of Division of European Gas Market Monitoring Gazprom Export EU-RUSSIA ENERGY DIALOGUE Gas Advisory Council Markets Workshop Brussels - February 24, 2014

Value of Midstream Flexibility Alexey Gnatyuk Head of Division of European Gas Market Monitoring Gazprom Export EU-RUSSIA ENERGY DIALOGUE Gas Advisory Council Markets Workshop Brussels - February 24, 2014

Managing Temperature Driven Volume Risks

Managing Temperature Driven Volume Risks Pascal Heider (*) E.ON Global Commodities SE 21. January 2015 (*) joint work with Laura Cucu, Rainer Döttling, Samuel Maina Contents 1 Introduction 2 Model 3 Calibration

Managing Temperature Driven Volume Risks Pascal Heider (*) E.ON Global Commodities SE 21. January 2015 (*) joint work with Laura Cucu, Rainer Döttling, Samuel Maina Contents 1 Introduction 2 Model 3 Calibration

PHASE I.A. STOCHASTIC STUDY TESTIMONY OF DR. SHUCHENG LIU ON BEHALF OF THE CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION

Rulemaking No.: 13-12-010 Exhibit No.: Witness: Dr. Shucheng Liu Order Instituting Rulemaking to Integrate and Refine Procurement Policies and Consider Long-Term Procurement Plans. Rulemaking 13-12-010

Rulemaking No.: 13-12-010 Exhibit No.: Witness: Dr. Shucheng Liu Order Instituting Rulemaking to Integrate and Refine Procurement Policies and Consider Long-Term Procurement Plans. Rulemaking 13-12-010

(FRED ESPEN BENTH, JAN KALLSEN, AND THILO MEYER-BRANDIS) UFITIMANA Jacqueline. Lappeenranta University Of Technology.

UFITIMANA Jacqueline. Lappeenranta University Of Technology.") (FRED ESPEN BENTH, JAN KALLSEN, AND THILO MEYER-BRANDIS) UFITIMANA Jacqueline Lappeenranta University Of Technology. 16,April 2009 OUTLINE Introduction Definitions Aim Electricity price Modelling Approaches

(FRED ESPEN BENTH, JAN KALLSEN, AND THILO MEYER-BRANDIS) UFITIMANA Jacqueline Lappeenranta University Of Technology. 16,April 2009 OUTLINE Introduction Definitions Aim Electricity price Modelling Approaches

Pricing the purchase of gas losses on regional gas transport networks

Pricing the purchase of gas losses on regional gas transport networks Version: Final Date: 29/07/13 Version History Version Date Description Prepared by Approved by Final 29/07/2013 Sian Morgan Oliver

Pricing the purchase of gas losses on regional gas transport networks Version: Final Date: 29/07/13 Version History Version Date Description Prepared by Approved by Final 29/07/2013 Sian Morgan Oliver

Gas storage valuation using a multi-factor price process

Gas storage valuation using a multi-factor price process Alexander Boogert Cyriel de Jong September, 2 Abstract In this paper we discuss an extension to a popular gas storage valuation method called the

Gas storage valuation using a multi-factor price process Alexander Boogert Cyriel de Jong September, 2 Abstract In this paper we discuss an extension to a popular gas storage valuation method called the

Accelerated Option Pricing Multiple Scenarios

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

fast cycle gas storage Our services A Gasunie company

fast cycle gas storage Our services A Gasunie company Live volatility dashboard on our website The energy industry has entered a new era. Supply and demand are decentralizing at an accelerating pace. Traditional

fast cycle gas storage Our services A Gasunie company Live volatility dashboard on our website The energy industry has entered a new era. Supply and demand are decentralizing at an accelerating pace. Traditional

Monte Carlo Methods in Structuring and Derivatives Pricing

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

On modelling of electricity spot price

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

OPINION on position limits on Phelix DE/AT Base Power contract. I. Introduction and legal basis

Date: 24 September 2018 ESMA70-155-2931 OPINION on position limits on Phelix DE/AT Base Power contract I. Introduction and legal basis 1. On 20 October 2017, the European Securities and Markets Authority

Date: 24 September 2018 ESMA70-155-2931 OPINION on position limits on Phelix DE/AT Base Power contract I. Introduction and legal basis 1. On 20 October 2017, the European Securities and Markets Authority

Value of Price Dependent Bidding for Thermal Power Producers

Erik B. Rudlang Carl Fredrik Tjeransen Project work Value of Price Dependent Bidding for Thermal Power Producers Teaching supervisor: Stein-Erik Fleten NTNU Norwegian University of Science and Technology

Erik B. Rudlang Carl Fredrik Tjeransen Project work Value of Price Dependent Bidding for Thermal Power Producers Teaching supervisor: Stein-Erik Fleten NTNU Norwegian University of Science and Technology

Recent developments in. Portfolio Modelling

Recent developments in Portfolio Modelling Presentation RiskLab Madrid Agenda What is Portfolio Risk Tracker? Original Features Transparency Data Technical Specification 2 What is Portfolio Risk Tracker?

Recent developments in Portfolio Modelling Presentation RiskLab Madrid Agenda What is Portfolio Risk Tracker? Original Features Transparency Data Technical Specification 2 What is Portfolio Risk Tracker?

The power of flexibility

The power of flexibility new services included A Gasunie company The energy industry has entered a new era. Supply and demand are decentralizing at an accelerating pace. Traditional energy companies and

The power of flexibility new services included A Gasunie company The energy industry has entered a new era. Supply and demand are decentralizing at an accelerating pace. Traditional energy companies and

Numerical Methods for Pricing Energy Derivatives, including Swing Options, in the Presence of Jumps

Numerical Methods for Pricing Energy Derivatives, including Swing Options, in the Presence of Jumps, Senior Quantitative Analyst Motivation: Swing Options An electricity or gas SUPPLIER needs to be capable,

Numerical Methods for Pricing Energy Derivatives, including Swing Options, in the Presence of Jumps, Senior Quantitative Analyst Motivation: Swing Options An electricity or gas SUPPLIER needs to be capable,

This homework assignment uses the material on pages ( A moving average ).

.") Module 2: Time series concepts HW Homework assignment: equally weighted moving average This homework assignment uses the material on pages 14-15 ( A moving average ). 2 Let Y t = 1/5 ( t + t-1 + t-2 +

Module 2: Time series concepts HW Homework assignment: equally weighted moving average This homework assignment uses the material on pages 14-15 ( A moving average ). 2 Let Y t = 1/5 ( t + t-1 + t-2 +

WEEKLY MARKET UPDATE

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 206 Bcf. The withdrawal for the same week last year was 76 Bcf while

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 206 Bcf. The withdrawal for the same week last year was 76 Bcf while

Approximate Dynamic Programming for the Merchant Operations of Commodity and Energy Conversion Assets

Approximate Dynamic Programming for the Merchant Operations of Commodity and Energy Conversion Assets Selvaprabu (Selva) Nadarajah, (Joint work with François Margot and Nicola Secomandi) Tepper School

Approximate Dynamic Programming for the Merchant Operations of Commodity and Energy Conversion Assets Selvaprabu (Selva) Nadarajah, (Joint work with François Margot and Nicola Secomandi) Tepper School

Trading of Pumped Hydro Storages in ID Markets

Trading of Pumped Hydro Storages in ID Markets Continuous Optimization ID Price Forecasts Market Insights Strommarkttreffen Berlin,. Juni 28 Sebastian Braun, Senior Analyst Power Markets Introduction Education

Trading of Pumped Hydro Storages in ID Markets Continuous Optimization ID Price Forecasts Market Insights Strommarkttreffen Berlin,. Juni 28 Sebastian Braun, Senior Analyst Power Markets Introduction Education

Passing the repeal of the carbon tax back to wholesale electricity prices

University of Wollongong Research Online National Institute for Applied Statistics Research Australia Working Paper Series Faculty of Engineering and Information Sciences 2014 Passing the repeal of the

University of Wollongong Research Online National Institute for Applied Statistics Research Australia Working Paper Series Faculty of Engineering and Information Sciences 2014 Passing the repeal of the

Linz Kickoff workshop. September 8-12,

Linz Kickoff workshop September 8-12, 2008. 1 Power and Gas Markets Challenges for Pricing and Managing Derivatives Peter Leoni, Electrabel Linz Kickoff workshop September 8-12, 2008. 2 Outline Power Markets:

Linz Kickoff workshop September 8-12, 2008. 1 Power and Gas Markets Challenges for Pricing and Managing Derivatives Peter Leoni, Electrabel Linz Kickoff workshop September 8-12, 2008. 2 Outline Power Markets:

From default probabilities to credit spreads: Credit risk models do explain market prices

From default probabilities to credit spreads: Credit risk models do explain market prices Presented by Michel M Dacorogna (Joint work with Stefan Denzler, Alexander McNeil and Ulrich A. Müller) The 2007

From default probabilities to credit spreads: Credit risk models do explain market prices Presented by Michel M Dacorogna (Joint work with Stefan Denzler, Alexander McNeil and Ulrich A. Müller) The 2007

Scenario reduction and scenario tree construction for power management problems

Scenario reduction and scenario tree construction for power management problems N. Gröwe-Kuska, H. Heitsch and W. Römisch Humboldt-University Berlin Institute of Mathematics Page 1 of 20 IEEE Bologna POWER

Scenario reduction and scenario tree construction for power management problems N. Gröwe-Kuska, H. Heitsch and W. Römisch Humboldt-University Berlin Institute of Mathematics Page 1 of 20 IEEE Bologna POWER

BSc (Hons) Software Engineering BSc (Hons) Computer Science with Network Security

Software Engineering BSc (Hons) Computer Science with Network Security") BSc (Hons) Software Engineering BSc (Hons) Computer Science with Network Security Cohorts BCNS/ 06 / Full Time & BSE/ 06 / Full Time Resit Examinations for 2008-2009 / Semester 1 Examinations for 2008-2009

BSc (Hons) Software Engineering BSc (Hons) Computer Science with Network Security Cohorts BCNS/ 06 / Full Time & BSE/ 06 / Full Time Resit Examinations for 2008-2009 / Semester 1 Examinations for 2008-2009

Pacific Gas and Electric Company. Statement of Estimated Cash Flows April 20, 2001

Pacific Gas and Electric Company Statement of Estimated Cash Flows April 20, 2001 This document provides the latest forecast of cash flows for Pacific Gas and Electric Company (the Company ). The purpose

Pacific Gas and Electric Company Statement of Estimated Cash Flows April 20, 2001 This document provides the latest forecast of cash flows for Pacific Gas and Electric Company (the Company ). The purpose

Monte Carlo Methods for Uncertainty Quantification

Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Mike Giles (Oxford) Monte Carlo methods 2 1 / 24 Lecture outline

Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Mike Giles (Oxford) Monte Carlo methods 2 1 / 24 Lecture outline

Statistical Arbitrage in Balancing Markets

Statistical Arbitrage in Balancing Markets and the Impact of Time Delay Stefan Kermer, Derek Bunn 1 Agenda Introduction Austrian Imbalance Settlement Design Market Players Perspectives Predicting the Conditional

Statistical Arbitrage in Balancing Markets and the Impact of Time Delay Stefan Kermer, Derek Bunn 1 Agenda Introduction Austrian Imbalance Settlement Design Market Players Perspectives Predicting the Conditional

A random walk in the Bakken Oil prices, investment and energy policy

A random walk in the Bakken Oil prices, investment and energy policy Professor Gordon Hughes University of Edinburgh Scottish Oil Club 15 th January 2015 Introduction Forecasting future oil & gas prices

A random walk in the Bakken Oil prices, investment and energy policy Professor Gordon Hughes University of Edinburgh Scottish Oil Club 15 th January 2015 Introduction Forecasting future oil & gas prices

In April 2013, the UK government brought into force a tax on carbon

The UK carbon floor and power plant hedging Due to the carbon floor, the price of carbon emissions has become a highly significant part of the generation costs for UK power producers. Vytautas Jurenas

The UK carbon floor and power plant hedging Due to the carbon floor, the price of carbon emissions has become a highly significant part of the generation costs for UK power producers. Vytautas Jurenas

Properties of the estimated five-factor model

Informationin(andnotin)thetermstructure Appendix. Additional results Greg Duffee Johns Hopkins This draft: October 8, Properties of the estimated five-factor model No stationary term structure model is

Informationin(andnotin)thetermstructure Appendix. Additional results Greg Duffee Johns Hopkins This draft: October 8, Properties of the estimated five-factor model No stationary term structure model is

Statistical Models and Methods for Financial Markets

Tze Leung Lai/ Haipeng Xing Statistical Models and Methods for Financial Markets B 374756 4Q Springer Preface \ vii Part I Basic Statistical Methods and Financial Applications 1 Linear Regression Models

Tze Leung Lai/ Haipeng Xing Statistical Models and Methods for Financial Markets B 374756 4Q Springer Preface \ vii Part I Basic Statistical Methods and Financial Applications 1 Linear Regression Models

Energy Price Processes

Energy Processes Used for Derivatives Pricing & Risk Management In this first of three articles, we will describe the most commonly used process, Geometric Brownian Motion, and in the second and third

Energy Processes Used for Derivatives Pricing & Risk Management In this first of three articles, we will describe the most commonly used process, Geometric Brownian Motion, and in the second and third

Modeling and Accounting Methods for Estimating Unbilled Energy

Itron White Paper Energy Forecasting ing and Accounting Methods for Estimating Unbilled Energy J. Stuart McMenamin, Ph.D. Vice President, Itron Forecasting 2006, Itron Inc. All rights reserved. 1 Introduction

Itron White Paper Energy Forecasting ing and Accounting Methods for Estimating Unbilled Energy J. Stuart McMenamin, Ph.D. Vice President, Itron Forecasting 2006, Itron Inc. All rights reserved. 1 Introduction

Essen2013. Revisiting the relationship between spot and futures prices. in the Nord Pool electricity market

Revisiting the relationship between spot and futures prices in the Nord Pool electricity market Michał Zator Wrocław University of Technology Joint work with Rafał Weron Essen, 10.10.13 The relationship

Revisiting the relationship between spot and futures prices in the Nord Pool electricity market Michał Zator Wrocław University of Technology Joint work with Rafał Weron Essen, 10.10.13 The relationship

The Volatility of Temperature, Pricing of Weather Derivatives, and Hedging Spatial Temperature Risk

The Volatility of Temperature, Pricing of Weather Derivatives, and Hedging Spatial Temperature Risk Fred Espen Benth In collaboration with A. Barth, J. Saltyte Benth, S. Koekebakker and J. Potthoff Centre

The Volatility of Temperature, Pricing of Weather Derivatives, and Hedging Spatial Temperature Risk Fred Espen Benth In collaboration with A. Barth, J. Saltyte Benth, S. Koekebakker and J. Potthoff Centre

Monte Carlo Methods in Financial Engineering

Paul Glassennan Monte Carlo Methods in Financial Engineering With 99 Figures

Paul Glassennan Monte Carlo Methods in Financial Engineering With 99 Figures

Long-Term Trading Strategies

Long-Term Trading Strategies Alfred Hoffmann Bewag AG, Berlin 3th January 3, St. Veit, Austria 1 Structure Definition of the strategy Implementation of the strategy Case Study Conclusions Value chains

Long-Term Trading Strategies Alfred Hoffmann Bewag AG, Berlin 3th January 3, St. Veit, Austria 1 Structure Definition of the strategy Implementation of the strategy Case Study Conclusions Value chains

MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, Student Name (print):

:") MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

Valuing Energy Security Quantifying the Benefits of Operational and Strategic Flexibility Tom Parkinson 4 October 2013

Quantifying the Benefits of Operational and Strategic Flexibility Tom Parkinson 4 October 2013 We at The Lantau Group are experts in the economics of energy systems Seoul (TLG Korea) Asia Pacific Energy

Quantifying the Benefits of Operational and Strategic Flexibility Tom Parkinson 4 October 2013 We at The Lantau Group are experts in the economics of energy systems Seoul (TLG Korea) Asia Pacific Energy

Toward an ideal international gas market : the role of LNG destination clauses

Toward an ideal international gas market : the role of LNG destination clauses Amina BABA (University Paris Dauphine) Anna CRETI (University Paris Dauphine) Olivier MASSOL (IFP School) International Conference

Toward an ideal international gas market : the role of LNG destination clauses Amina BABA (University Paris Dauphine) Anna CRETI (University Paris Dauphine) Olivier MASSOL (IFP School) International Conference

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Report on the system balancing actions and related procurement activities in the GASPOOL market area in the gas year 2015/2016

Report on the system balancing actions and related procurement activities in the GASPOOL market area in the gas year 2015/2016 Current as at: 5 December 2016 Table of contents Introduction... 6 Internal

Report on the system balancing actions and related procurement activities in the GASPOOL market area in the gas year 2015/2016 Current as at: 5 December 2016 Table of contents Introduction... 6 Internal

The Volatility of Temperature and Pricing of Weather Derivatives

The Volatility of Temperature and Pricing of Weather Derivatives Fred Espen Benth Work in collaboration with J. Saltyte Benth and S. Koekebakker Centre of Mathematics for Applications (CMA) University

The Volatility of Temperature and Pricing of Weather Derivatives Fred Espen Benth Work in collaboration with J. Saltyte Benth and S. Koekebakker Centre of Mathematics for Applications (CMA) University

Practical example of an Economic Scenario Generator

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Valuation of Transmission Assets and Projects. Transmission Investment: Opportunities in Asset Sales, Recapitalization and Enhancements

Valuation of Transmission Assets and Projects Assef Zobian Cambridge Energy Solutions Alex Rudkevich Tabors Caramanis and Associates Transmission Investment: Opportunities in Asset Sales, Recapitalization

Valuation of Transmission Assets and Projects Assef Zobian Cambridge Energy Solutions Alex Rudkevich Tabors Caramanis and Associates Transmission Investment: Opportunities in Asset Sales, Recapitalization

hydro thermal portfolio management

hydro thermal portfolio management presentation @ Schloss Leopoldskron 8 Sep 004 contents. thesis initiation. context 3. problem definition 4. main milestones of the thesis 5. milestones presentation 6.

hydro thermal portfolio management presentation @ Schloss Leopoldskron 8 Sep 004 contents. thesis initiation. context 3. problem definition 4. main milestones of the thesis 5. milestones presentation 6.

List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Practical application of Liquidity Premium to the valuation of insurance liabilities and determination of capital requirements

28 April 2011 Practical application of Liquidity Premium to the valuation of insurance liabilities and determination of capital requirements 1. Introduction CRO Forum Position on Liquidity Premium The

28 April 2011 Practical application of Liquidity Premium to the valuation of insurance liabilities and determination of capital requirements 1. Introduction CRO Forum Position on Liquidity Premium The

INTRODUCTION - Price volatility is a measure of the dispersion in prices observed over a time period. - Price volatility in the electricity market is

Day-ahead market price volatility analysis in deregulated electricity markets. M.Benini, A. Venturini P. Pelacchi, Member, IEEE, M. Marracci CESI - T&D Network Milan, Italy Electric Systems and Automation

Day-ahead market price volatility analysis in deregulated electricity markets. M.Benini, A. Venturini P. Pelacchi, Member, IEEE, M. Marracci CESI - T&D Network Milan, Italy Electric Systems and Automation

APPENDIX B: WHOLESALE AND RETAIL PRICE FORECAST

Seventh Northwest Conservation and Electric Power Plan APPENDIX B: WHOLESALE AND RETAIL PRICE FORECAST Contents Introduction... 3 Key Findings... 3 Background... 5 Methodology... 7 Inputs and Assumptions...

Seventh Northwest Conservation and Electric Power Plan APPENDIX B: WHOLESALE AND RETAIL PRICE FORECAST Contents Introduction... 3 Key Findings... 3 Background... 5 Methodology... 7 Inputs and Assumptions...

The Pennsylvania State University. The Graduate School. Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

Policies to Cope with Volatility of Oil Prices: Oil Importing Countries. Oil Price Volatility is Everywhere and Everpresent

Policies to Cope with Volatility of Oil Prices: Oil Importing Countries Robert Bacon Oil, Gas and Mining Policy Division The World Bank 1 Oil Price Volatility is Everywhere and Everpresent SD of return

Policies to Cope with Volatility of Oil Prices: Oil Importing Countries Robert Bacon Oil, Gas and Mining Policy Division The World Bank 1 Oil Price Volatility is Everywhere and Everpresent SD of return

Fortum Corporation Interim report January-March April 2010

Fortum Corporation Interim report January-March 21 27 April 21 Disclaimer This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any Fortum

Fortum Corporation Interim report January-March 21 27 April 21 Disclaimer This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any Fortum

Introductory Econometrics for Finance

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

Lecture 13. Commodity Modeling. Alexander Eydeland. Morgan Stanley

Lecture 13 Commodity Modeling Alexander Eydeland Morgan Stanley 1 Commodity Modeling The views represented herein are the author s own views and do not necessarily represent the views of Morgan Stanley

Lecture 13 Commodity Modeling Alexander Eydeland Morgan Stanley 1 Commodity Modeling The views represented herein are the author s own views and do not necessarily represent the views of Morgan Stanley

Investments in Thermopower Generation: A Real Options Approach for the New Brazilian Electrical Power Regulation *

Investments in Thermopower Generation: A Real Options Approach for the New Brazilian Electrical Power Regulation * Katia Rocha IPEA 1 katia@ipea.gov.br Ajax Moreira IPEA ajax@ipea.gov.br Pedro David FURNAS

Investments in Thermopower Generation: A Real Options Approach for the New Brazilian Electrical Power Regulation * Katia Rocha IPEA 1 katia@ipea.gov.br Ajax Moreira IPEA ajax@ipea.gov.br Pedro David FURNAS

Net Benefits Test SPP EIS Market May 2012

Net Benefits Test SPP EIS Market May 2012 Topics Net Benefits Test Threshold Steps for Determining Net Benefits Test Threshold Results for May 2011 through May 2012 3 Net Benefits Threshold Price The Net

Net Benefits Test SPP EIS Market May 2012 Topics Net Benefits Test Threshold Steps for Determining Net Benefits Test Threshold Results for May 2011 through May 2012 3 Net Benefits Threshold Price The Net

Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options

for Measuring Counterparty Credit Exposure of American-style Options") Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options Kin Hung (Felix) Kan 1 Greg Frank 3 Victor Mozgin 3 Mark Reesor 2 1 Department of Applied

Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options Kin Hung (Felix) Kan 1 Greg Frank 3 Victor Mozgin 3 Mark Reesor 2 1 Department of Applied

Hedging Derivative Securities with VIX Derivatives: A Discrete-Time -Arbitrage Approach

Hedging Derivative Securities with VIX Derivatives: A Discrete-Time -Arbitrage Approach Nelson Kian Leong Yap a, Kian Guan Lim b, Yibao Zhao c,* a Department of Mathematics, National University of Singapore

Hedging Derivative Securities with VIX Derivatives: A Discrete-Time -Arbitrage Approach Nelson Kian Leong Yap a, Kian Guan Lim b, Yibao Zhao c,* a Department of Mathematics, National University of Singapore

Credit Exposure Measurement Fixed Income & FX Derivatives

1 Credit Exposure Measurement Fixed Income & FX Derivatives Dr Philip Symes 1. Introduction 2 Fixed Income Derivatives Exposure Simulation. This methodology may be used for fixed income and FX derivatives.

1 Credit Exposure Measurement Fixed Income & FX Derivatives Dr Philip Symes 1. Introduction 2 Fixed Income Derivatives Exposure Simulation. This methodology may be used for fixed income and FX derivatives.

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

OPINION on position limits on Swiss Power Base contracts. I. Introduction and legal basis

Date: 24 September 2018 ESMA70-155-2938 OPINION on position limits on Swiss Power Base contracts I. Introduction and legal basis 1. On 20 October 2017, the European Securities and Markets Authority ( ESMA

Date: 24 September 2018 ESMA70-155-2938 OPINION on position limits on Swiss Power Base contracts I. Introduction and legal basis 1. On 20 October 2017, the European Securities and Markets Authority ( ESMA

The Impact of Stochastic Volatility and Policyholder Behaviour on Guaranteed Lifetime Withdrawal Benefits

and Policyholder Guaranteed Lifetime 8th Conference in Actuarial Science & Finance on Samos 2014 Frankfurt School of Finance and Management June 1, 2014 1. Lifetime withdrawal guarantees in PLIs 2. policyholder

and Policyholder Guaranteed Lifetime 8th Conference in Actuarial Science & Finance on Samos 2014 Frankfurt School of Finance and Management June 1, 2014 1. Lifetime withdrawal guarantees in PLIs 2. policyholder

Spring 2015 NDM Analysis - Recommended Approach

Spring 2015 NDM Analysis - Recommended Approach Impacts of Industry change programme: Ahead of each annual NDM analysis, it is customary to prepare a note for Demand Estimation Sub Committee (DESC) setting

Spring 2015 NDM Analysis - Recommended Approach Impacts of Industry change programme: Ahead of each annual NDM analysis, it is customary to prepare a note for Demand Estimation Sub Committee (DESC) setting

The Value of Flexibility to Expand Production Capacity for Oil Projects: Is it Really Important in Practice?

SPE 139338-PP The Value of Flexibility to Expand Production Capacity for Oil Projects: Is it Really Important in Practice? G. A. Costa Lima; A. T. F. S. Gaspar Ravagnani; M. A. Sampaio Pinto and D. J.

SPE 139338-PP The Value of Flexibility to Expand Production Capacity for Oil Projects: Is it Really Important in Practice? G. A. Costa Lima; A. T. F. S. Gaspar Ravagnani; M. A. Sampaio Pinto and D. J.

How can renewables support Europe?

Florence School of Regulation, Annual Climate Conference 2016 How can renewables support Europe? Karsten Neuhoff German Institute for Economic Research (DIW Berlin) Technical University Berlin 1 Moving

Florence School of Regulation, Annual Climate Conference 2016 How can renewables support Europe? Karsten Neuhoff German Institute for Economic Research (DIW Berlin) Technical University Berlin 1 Moving

Valuation of a Spark Spread: an LM6000 Power Plant

Valuation of a Spark Spread: an LM6000 Power Plant Mark Cassano and Gordon Sick May 14, 2009 Respectively, Independent Consultant and Professor of Finance at the Haskayne School of Business, University

Valuation of a Spark Spread: an LM6000 Power Plant Mark Cassano and Gordon Sick May 14, 2009 Respectively, Independent Consultant and Professor of Finance at the Haskayne School of Business, University

Monte Carlo Introduction

Monte Carlo Introduction Probability Based Modeling Concepts moneytree.com Toll free 1.877.421.9815 1 What is Monte Carlo? Monte Carlo Simulation is the currently accepted term for a technique used by

Monte Carlo Introduction Probability Based Modeling Concepts moneytree.com Toll free 1.877.421.9815 1 What is Monte Carlo? Monte Carlo Simulation is the currently accepted term for a technique used by

Market Risk Analysis Volume IV. Value-at-Risk Models

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

Lévy processes and the financial crisis: can we design a more effective deposit protection?

30 th August 2011, Eindhoven Lévy processes and the financial crisis: can we design a more effective deposit protection? Maccaferri S., Cariboni J., Schoutens W. European Commission JRC, Ispra (VA), Italy

30 th August 2011, Eindhoven Lévy processes and the financial crisis: can we design a more effective deposit protection? Maccaferri S., Cariboni J., Schoutens W. European Commission JRC, Ispra (VA), Italy

Ex post payoffs of a tolling agreement for natural-gas-fired generation in Texas

Ex post payoffs of a tolling agreement for natural-gas-fired generation in Texas The 5th IAEE Asian Conference, University of Western Australia, Spring, 2016 Yun LIU, Ph.D. Candidate Department of Economics,

Ex post payoffs of a tolling agreement for natural-gas-fired generation in Texas The 5th IAEE Asian Conference, University of Western Australia, Spring, 2016 Yun LIU, Ph.D. Candidate Department of Economics,

Determinants of the Forward Premium in Electricity Markets

Determinants of the Forward Premium in Electricity Markets Álvaro Cartea, José S. Penalva, Eduardo Schwartz Universidad Carlos III, Universidad Carlos III, UCLA June, 2011 Electricity: a Special Kind of

Determinants of the Forward Premium in Electricity Markets Álvaro Cartea, José S. Penalva, Eduardo Schwartz Universidad Carlos III, Universidad Carlos III, UCLA June, 2011 Electricity: a Special Kind of

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch