Applications of Quantum Annealing in Computational Finance. Dr. Phil Goddard Head of Research, 1QBit D-Wave User Conference, Santa Fe, Sept.

|

|

|

- Mitchell Casey

- 5 years ago

- Views:

Transcription

1 Applications of Quantum Annealing in Computational Finance Dr. Phil Goddard Head of Research, 1QBit D-Wave User Conference, Santa Fe, Sept. 2016

2 Outline Where s my Babel Fish? Quantum-Ready Applications for Computational Finance Tools and Resources 2

3 Where s my Babel Fish?

4 Where s my Babel Fish? k-coloring Connected Dominating Set Job Shop Scheduling Portfolio Optimization Expected Return Mean-Variance-Efficient Frontier Job 1 Job 2 Job Risk (Standard Deviation) Asset Allocation Risk Management time Graph Similarity Graph Partitioning Option Pricing 4

5 Is that a QUBO? min - x. Qx x 0,1 & Q R & & x R & Q R & & Weight of assets in portfolio Covariance matrix 5

6 Quantum-Ready Applications for Computational Finance

7 Applications for Computational Finance A Multi-Period Optimal Trading Strategy Quantum-Ready Hierarchical Risk Parity (QHRP) Real-Time Optimization Framework Tax Loss Harvesting 7

8 8 Optimal Trading Trajectories

9 A Multi-Period Optimal Trading Strategy The optimal trading trajectory problem The mathematical formulation Considerations in using the quantum annealer Experimental Results 9

10 The Optimal Trading Trajectory Problem Managers of large portfolios typically need to optimize their portfolios over a multiple period horizon. A sequence of single-period optimal positons is rarely multi-period optimal. Rebalancing the portfolio to align with each single period optimal weight is typically prohibitively expensive t h0.6 ig e a l W 0.5 tim p O Time of Rebalance Single-period Optimal Weight --- Multi-period Optimal Weight 10

11 Practical Considerations Friction: Transaction costs prevent portfolio managers from monetizing much of their forecasting power Basic Constraints Trading Constraints Efficient Frontier Market Impact: The sale or purchase of large blocks of a given asset may result in temporary and/or permanent price movements Constraints: Some positions can only be traded in blocks (e.g. real-estate, private offerings, fixed lot sizes, ), thus requiring integer solutions Return Risk 11

12 Mathematical Formulation The multi-period integer optimization problem may be written as 12 w = argmax 5 6 μ 8. w 8 s.t.: mean-variance portfolio optimization. 8PQ 9:;<9=> γ 2 w 8. Σ 8 w 8 9C>D To solve, the problem must be converted to standard QUBO form: & t: 6 w U,8 K UPQ Δw 8. Λ 8 Δw 8 GC9:H; HJ>;>, ;:KL.CKLNH; ; t, n: w U,8 K O min - x. Qx x 0,1 &, Q R & & Δw 8. Λ 8 O Δw 8 L:9K.CKLNH; transaction cost and market impacts

13 Bit Encoding The integer variables of the optimization problem w Z annealer x Z. must be recast to the binary variables used by the 13

14 Experimental Procedure and Results Generate a random problem: number of assets; time horizon; and total investable assets Solve using quantum annealer Find exact minimum solution using an exhaustive search Evaluate performance by how far the quantum solution is from the exact solution The annealer solution is typically within a small and acceptable margin of error of the exact globally minimal solution. 14

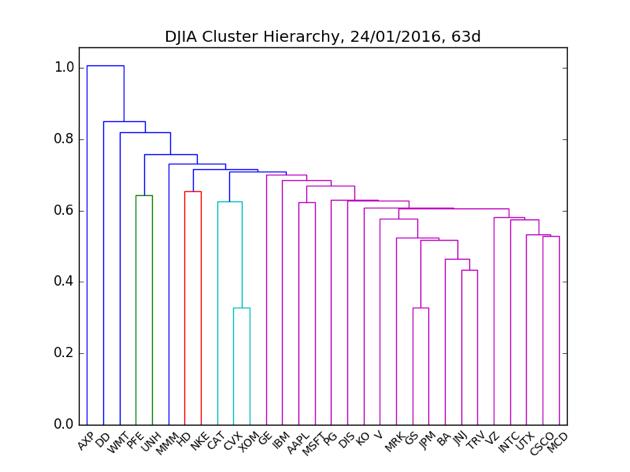

15 Quantum-Ready Hierarchical Risk Parity

16 16 Quantum-Ready Hierarchical Risk Parity

17 The Approach Use tree structure to reduce connections between assets as well as estimation error Instead of minimizing variance via all correlations using all assets at once, solve the minimum variance problem at each node of the tree w = arg min w w. Σ^w s. t. 6 w Z = 1 Z Classical Build the final weight vector by recursively minimizing variance from the bottom of the tree to the top w 1,1 = arg min w w. Σ d Q,Qw QHRP Ignore correlations in determining weights, use only in calculating variance of sub-trees Effect: Improve out-of-sample realized volatility Can also be applied to linear regression w 2,1 = arg min w w. Σ d c,qw w 2,2 = arg min w w. Σ d c,cw 17

18 (Out-of-Sample) Minimum Risk Portfolios Classical algorithm minimizes in-sample risk, but sometimes missed the point In this example, it invests over 50% of the portfolio in just McDonalds, Coca-Cola and Johnson & Johnson QHRP provides more diversification 18

19 20 % Risk Improvement in Simulations Out-of-sample volatility is reduced by 20% in simulated examples using 10 assets with 10% volatility each, random shocks, random correlations. 19

20 Real-Time Optimization Framework

21 Real-Time Optimization Framework Stream Analytics Real-Time data signals Quantum powered analytics GOOG AAPL MSFT SBUX TSLA Correlation Graph Generator 1QBit SDK D-Wave 2X Processor Post Processing Stock Market Time Trading Signals 21

22 Real-Time Optimization Framework Stream Analytics Real-Time data signals Quantum powered analytics GOOG AAPL MSFT SBUX TSLA Correlation Graph Generator 1QBit SDK D-Wave 2X Processor Post Processing Stock Market Time Trading Signals 22

23 Real-Time Optimization Framework Stream Analytics Real-Time data signals Quantum powered analytics GOOG AAPL MSFT SBUX TSLA Correlation Graph Generator 1QBit SDK D-Wave 2X Processor Post Processing Stock Market Time Trading Signals 23

24 Tax Loss Harvesting

Offset gains and income; carry losses forward; create a tax buffer Quantum annealer used to find the optimal share quantities to buy and sell to generate the")

25 Tax Loss Harvesting Track an index using a subset of the components of the index while selling losses and moving into unowned components Integer Quadratic Programming: sell quantities from owned lots; buy new lots (avoiding wash sales) Offset gains and income; carry losses forward; create a tax buffer Quantum annealer used to find the optimal share quantities to buy and sell to generate the greatest tax benefit while staying within a specified tracking error. 25

26 Tools and Resources

27 Tools 1QBit s quantum-ready Software Development Kit: Explore: 1qbit.com Register for Beta Release: qdk.1qbit.com 27

28 28 Resources:

29 Phil Goddard QB Information Technologies. All rights reserved.

Finding optimal arbitrage opportunities using a quantum annealer

Finding optimal arbitrage opportunities using a quantum annealer White Paper Finding optimal arbitrage opportunities using a quantum annealer Gili Rosenberg Abstract We present two formulations for finding

Finding optimal arbitrage opportunities using a quantum annealer White Paper Finding optimal arbitrage opportunities using a quantum annealer Gili Rosenberg Abstract We present two formulations for finding

The Optimization Process: An example of portfolio optimization

ISyE 6669: Deterministic Optimization The Optimization Process: An example of portfolio optimization Shabbir Ahmed Fall 2002 1 Introduction Optimization can be roughly defined as a quantitative approach

ISyE 6669: Deterministic Optimization The Optimization Process: An example of portfolio optimization Shabbir Ahmed Fall 2002 1 Introduction Optimization can be roughly defined as a quantitative approach

Risk-Based Investing & Asset Management Final Examination

Risk-Based Investing & Asset Management Final Examination Thierry Roncalli February 6 th 2015 Contents 1 Risk-based portfolios 2 2 Regularizing portfolio optimization 3 3 Smart beta 5 4 Factor investing

Risk-Based Investing & Asset Management Final Examination Thierry Roncalli February 6 th 2015 Contents 1 Risk-based portfolios 2 2 Regularizing portfolio optimization 3 3 Smart beta 5 4 Factor investing

SciBeta CoreShares South-Africa Multi-Beta Multi-Strategy Six-Factor EW

SciBeta CoreShares South-Africa Multi-Beta Multi-Strategy Six-Factor EW Table of Contents Introduction Methodological Terms Geographic Universe Definition: Emerging EMEA Construction: Multi-Beta Multi-Strategy

SciBeta CoreShares South-Africa Multi-Beta Multi-Strategy Six-Factor EW Table of Contents Introduction Methodological Terms Geographic Universe Definition: Emerging EMEA Construction: Multi-Beta Multi-Strategy

Applications of Linear Programming

Applications of Linear Programming lecturer: András London University of Szeged Institute of Informatics Department of Computational Optimization Lecture 8 The portfolio selection problem The portfolio

Applications of Linear Programming lecturer: András London University of Szeged Institute of Informatics Department of Computational Optimization Lecture 8 The portfolio selection problem The portfolio

Mean Variance Portfolio Theory

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

THE CHINESE UNIVERSITY OF HONG KONG Department of Mathematics MMAT5250 Financial Mathematics Homework 2 Due Date: March 24, 2018

THE CHINESE UNIVERSITY OF HONG KONG Department of Mathematics MMAT5250 Financial Mathematics Homework 2 Due Date: March 24, 2018 Name: Student ID.: I declare that the assignment here submitted is original

THE CHINESE UNIVERSITY OF HONG KONG Department of Mathematics MMAT5250 Financial Mathematics Homework 2 Due Date: March 24, 2018 Name: Student ID.: I declare that the assignment here submitted is original

Quantum-inspired hierarchical risk parity

Quantum-inspired hierarchical risk parity White Paper Quantum-inspired hierarchical risk parity Elham Alipour, Clemens Adolphs, Arman Zaribafiyan, and Maxwell Rounds Abstract We present a quantum-inspired

Quantum-inspired hierarchical risk parity White Paper Quantum-inspired hierarchical risk parity Elham Alipour, Clemens Adolphs, Arman Zaribafiyan, and Maxwell Rounds Abstract We present a quantum-inspired

P s =(0,W 0 R) safe; P r =(W 0 σ,w 0 µ) risky; Beyond P r possible if leveraged borrowing OK Objective function Mean a (Std.Dev.

safe; P r =(W 0 σ,w 0 µ) risky; Beyond P r possible if leveraged borrowing OK Objective function Mean a (Std.Dev.") ECO 305 FALL 2003 December 2 ORTFOLIO CHOICE One Riskless, One Risky Asset Safe asset: gross return rate R (1 plus interest rate) Risky asset: random gross return rate r Mean µ = E[r] >R,Varianceσ 2 =

ECO 305 FALL 2003 December 2 ORTFOLIO CHOICE One Riskless, One Risky Asset Safe asset: gross return rate R (1 plus interest rate) Risky asset: random gross return rate r Mean µ = E[r] >R,Varianceσ 2 =

An Exact Solution Approach for Portfolio Optimization Problems under Stochastic and Integer Constraints

An Exact Solution Approach for Portfolio Optimization Problems under Stochastic and Integer Constraints P. Bonami, M.A. Lejeune Abstract In this paper, we study extensions of the classical Markowitz mean-variance

An Exact Solution Approach for Portfolio Optimization Problems under Stochastic and Integer Constraints P. Bonami, M.A. Lejeune Abstract In this paper, we study extensions of the classical Markowitz mean-variance

Lecture outline W.B.Powell 1

Lecture outline What is a policy? Policy function approximations (PFAs) Cost function approximations (CFAs) alue function approximations (FAs) Lookahead policies Finding good policies Optimizing continuous

Lecture outline What is a policy? Policy function approximations (PFAs) Cost function approximations (CFAs) alue function approximations (FAs) Lookahead policies Finding good policies Optimizing continuous

International Finance. Estimation Error. Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc.

International Finance Estimation Error Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 17, 2017 Motivation The Markowitz Mean Variance Efficiency is the

International Finance Estimation Error Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 17, 2017 Motivation The Markowitz Mean Variance Efficiency is the

FE670 Algorithmic Trading Strategies. Stevens Institute of Technology

FE670 Algorithmic Trading Strategies Lecture 4. Cross-Sectional Models and Trading Strategies Steve Yang Stevens Institute of Technology 09/26/2013 Outline 1 Cross-Sectional Methods for Evaluation of Factor

FE670 Algorithmic Trading Strategies Lecture 4. Cross-Sectional Models and Trading Strategies Steve Yang Stevens Institute of Technology 09/26/2013 Outline 1 Cross-Sectional Methods for Evaluation of Factor

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall Financial mathematics

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Lecture 17: More on Markov Decision Processes. Reinforcement learning

Lecture 17: More on Markov Decision Processes. Reinforcement learning Learning a model: maximum likelihood Learning a value function directly Monte Carlo Temporal-difference (TD) learning COMP-424, Lecture

Lecture 17: More on Markov Decision Processes. Reinforcement learning Learning a model: maximum likelihood Learning a value function directly Monte Carlo Temporal-difference (TD) learning COMP-424, Lecture

6.231 DYNAMIC PROGRAMMING LECTURE 10 LECTURE OUTLINE

6.231 DYNAMIC PROGRAMMING LECTURE 10 LECTURE OUTLINE Rollout algorithms Cost improvement property Discrete deterministic problems Approximations of rollout algorithms Discretization of continuous time

6.231 DYNAMIC PROGRAMMING LECTURE 10 LECTURE OUTLINE Rollout algorithms Cost improvement property Discrete deterministic problems Approximations of rollout algorithms Discretization of continuous time

Log-Robust Portfolio Management

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

RiskTorrent: Using Portfolio Optimisation for Media Streaming

RiskTorrent: Using Portfolio Optimisation for Media Streaming Raul Landa, Miguel Rio Communications and Information Systems Research Group Department of Electronic and Electrical Engineering University

RiskTorrent: Using Portfolio Optimisation for Media Streaming Raul Landa, Miguel Rio Communications and Information Systems Research Group Department of Electronic and Electrical Engineering University

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Optimal Portfolios and Random Matrices

Optimal Portfolios and Random Matrices Javier Acosta Nai Li Andres Soto Shen Wang Ziran Yang University of Minnesota, Twin Cities Mentor: Chris Bemis, Whitebox Advisors January 17, 2015 Javier Acosta Nai

Optimal Portfolios and Random Matrices Javier Acosta Nai Li Andres Soto Shen Wang Ziran Yang University of Minnesota, Twin Cities Mentor: Chris Bemis, Whitebox Advisors January 17, 2015 Javier Acosta Nai

In terms of covariance the Markowitz portfolio optimisation problem is:

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Energy Systems under Uncertainty: Modeling and Computations

Energy Systems under Uncertainty: Modeling and Computations W. Römisch Humboldt-University Berlin Department of Mathematics www.math.hu-berlin.de/~romisch Systems Analysis 2015, November 11 13, IIASA (Laxenburg,

Energy Systems under Uncertainty: Modeling and Computations W. Römisch Humboldt-University Berlin Department of Mathematics www.math.hu-berlin.de/~romisch Systems Analysis 2015, November 11 13, IIASA (Laxenburg,

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

Stochastic Programming in Gas Storage and Gas Portfolio Management. ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier

Stochastic Programming in Gas Storage and Gas Portfolio Management ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier Agenda Optimization tasks in gas storage and gas portfolio management Scenario

Stochastic Programming in Gas Storage and Gas Portfolio Management ÖGOR-Workshop, September 23rd, 2010 Dr. Georg Ostermaier Agenda Optimization tasks in gas storage and gas portfolio management Scenario

Price Impact and Optimal Execution Strategy

OXFORD MAN INSTITUE, UNIVERSITY OF OXFORD SUMMER RESEARCH PROJECT Price Impact and Optimal Execution Strategy Bingqing Liu Supervised by Stephen Roberts and Dieter Hendricks Abstract Price impact refers

OXFORD MAN INSTITUE, UNIVERSITY OF OXFORD SUMMER RESEARCH PROJECT Price Impact and Optimal Execution Strategy Bingqing Liu Supervised by Stephen Roberts and Dieter Hendricks Abstract Price impact refers

Robust Portfolio Construction

Robust Portfolio Construction Presentation to Workshop on Mixed Integer Programming University of Miami June 5-8, 2006 Sebastian Ceria Chief Executive Officer Axioma, Inc sceria@axiomainc.com Copyright

Robust Portfolio Construction Presentation to Workshop on Mixed Integer Programming University of Miami June 5-8, 2006 Sebastian Ceria Chief Executive Officer Axioma, Inc sceria@axiomainc.com Copyright

PORTFOLIO OPTIMIZATION: ANALYTICAL TECHNIQUES

PORTFOLIO OPTIMIZATION: ANALYTICAL TECHNIQUES Keith Brown, Ph.D., CFA November 22 nd, 2007 Overview of the Portfolio Optimization Process The preceding analysis demonstrates that it is possible for investors

PORTFOLIO OPTIMIZATION: ANALYTICAL TECHNIQUES Keith Brown, Ph.D., CFA November 22 nd, 2007 Overview of the Portfolio Optimization Process The preceding analysis demonstrates that it is possible for investors

29 Week 10. Portfolio theory Overheads

29 Week 1. Portfolio theory Overheads 1. Outline (a) Mean-variance (b) Multifactor portfolios (value etc.) (c) Outside income, labor income. (d) Taking advantage of predictability. (e) Options (f) Doubts

29 Week 1. Portfolio theory Overheads 1. Outline (a) Mean-variance (b) Multifactor portfolios (value etc.) (c) Outside income, labor income. (d) Taking advantage of predictability. (e) Options (f) Doubts

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Budget Management In GSP (2018)

") Budget Management In GSP (2018) Yahoo! March 18, 2018 Miguel March 18, 2018 1 / 26 Today s Presentation: Budget Management Strategies in Repeated auctions, Balseiro, Kim, and Mahdian, WWW2017 Learning

Budget Management In GSP (2018) Yahoo! March 18, 2018 Miguel March 18, 2018 1 / 26 Today s Presentation: Budget Management Strategies in Repeated auctions, Balseiro, Kim, and Mahdian, WWW2017 Learning

Optimal Portfolio Selection Under the Estimation Risk in Mean Return

Optimal Portfolio Selection Under the Estimation Risk in Mean Return by Lei Zhu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree of Master of Mathematics

Optimal Portfolio Selection Under the Estimation Risk in Mean Return by Lei Zhu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree of Master of Mathematics

Financial Giffen Goods: Examples and Counterexamples

Financial Giffen Goods: Examples and Counterexamples RolfPoulsen and Kourosh Marjani Rasmussen Abstract In the basic Markowitz and Merton models, a stock s weight in efficient portfolios goes up if its

Financial Giffen Goods: Examples and Counterexamples RolfPoulsen and Kourosh Marjani Rasmussen Abstract In the basic Markowitz and Merton models, a stock s weight in efficient portfolios goes up if its

Economics 483. Midterm Exam. 1. Consider the following monthly data for Microsoft stock over the period December 1995 through December 1996:

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

Integer Programming. Review Paper (Fall 2001) Muthiah Prabhakar Ponnambalam (University of Texas Austin)

Muthiah Prabhakar Ponnambalam (University of Texas Austin)") Integer Programming Review Paper (Fall 2001) Muthiah Prabhakar Ponnambalam (University of Texas Austin) Portfolio Construction Through Mixed Integer Programming at Grantham, Mayo, Van Otterloo and Company

Integer Programming Review Paper (Fall 2001) Muthiah Prabhakar Ponnambalam (University of Texas Austin) Portfolio Construction Through Mixed Integer Programming at Grantham, Mayo, Van Otterloo and Company

Risk Aggregation with Dependence Uncertainty

Risk Aggregation with Dependence Uncertainty Carole Bernard GEM and VUB Risk: Modelling, Optimization and Inference with Applications in Finance, Insurance and Superannuation Sydney December 7-8, 2017

Risk Aggregation with Dependence Uncertainty Carole Bernard GEM and VUB Risk: Modelling, Optimization and Inference with Applications in Finance, Insurance and Superannuation Sydney December 7-8, 2017

Multistage risk-averse asset allocation with transaction costs

Multistage risk-averse asset allocation with transaction costs 1 Introduction Václav Kozmík 1 Abstract. This paper deals with asset allocation problems formulated as multistage stochastic programming models.

Multistage risk-averse asset allocation with transaction costs 1 Introduction Václav Kozmík 1 Abstract. This paper deals with asset allocation problems formulated as multistage stochastic programming models.

Comparison of Static and Dynamic Asset Allocation Models

Comparison of Static and Dynamic Asset Allocation Models John R. Birge University of Michigan University of Michigan 1 Outline Basic Models Static Markowitz mean-variance Dynamic stochastic programming

Comparison of Static and Dynamic Asset Allocation Models John R. Birge University of Michigan University of Michigan 1 Outline Basic Models Static Markowitz mean-variance Dynamic stochastic programming

Macroeconomics Sequence, Block I. Introduction to Consumption Asset Pricing

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Risk Aggregation with Dependence Uncertainty

Risk Aggregation with Dependence Uncertainty Carole Bernard (Grenoble Ecole de Management) Hannover, Current challenges in Actuarial Mathematics November 2015 Carole Bernard Risk Aggregation with Dependence

Risk Aggregation with Dependence Uncertainty Carole Bernard (Grenoble Ecole de Management) Hannover, Current challenges in Actuarial Mathematics November 2015 Carole Bernard Risk Aggregation with Dependence

IEOR E4004: Introduction to OR: Deterministic Models

IEOR E4004: Introduction to OR: Deterministic Models 1 Dynamic Programming Following is a summary of the problems we discussed in class. (We do not include the discussion on the container problem or the

IEOR E4004: Introduction to OR: Deterministic Models 1 Dynamic Programming Following is a summary of the problems we discussed in class. (We do not include the discussion on the container problem or the

Risk Reward Optimisation for Long-Run Investors: an Empirical Analysis

GoBack Risk Reward Optimisation for Long-Run Investors: an Empirical Analysis M. Gilli University of Geneva and Swiss Finance Institute E. Schumann University of Geneva AFIR / LIFE Colloquium 2009 München,

GoBack Risk Reward Optimisation for Long-Run Investors: an Empirical Analysis M. Gilli University of Geneva and Swiss Finance Institute E. Schumann University of Geneva AFIR / LIFE Colloquium 2009 München,

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Robust Portfolio Optimization SOCP Formulations

1 Robust Portfolio Optimization SOCP Formulations There has been a wealth of literature published in the last 1 years explaining and elaborating on what has become known as Robust portfolio optimization.

1 Robust Portfolio Optimization SOCP Formulations There has been a wealth of literature published in the last 1 years explaining and elaborating on what has become known as Robust portfolio optimization.

Is Greedy Coordinate Descent a Terrible Algorithm?

Is Greedy Coordinate Descent a Terrible Algorithm? Julie Nutini, Mark Schmidt, Issam Laradji, Michael Friedlander, Hoyt Koepke University of British Columbia Optimization and Big Data, 2015 Context: Random

Is Greedy Coordinate Descent a Terrible Algorithm? Julie Nutini, Mark Schmidt, Issam Laradji, Michael Friedlander, Hoyt Koepke University of British Columbia Optimization and Big Data, 2015 Context: Random

Session 8: The Markowitz problem p. 1

Session 8: The Markowitz problem Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 8: The Markowitz problem p. 1 Portfolio optimisation Session 8: The Markowitz problem

Session 8: The Markowitz problem Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 8: The Markowitz problem p. 1 Portfolio optimisation Session 8: The Markowitz problem

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Implementing Momentum Strategy with Options: Dynamic Scaling and Optimization

Implementing Momentum Strategy with Options: Dynamic Scaling and Optimization Abstract: Momentum strategy and its option implementation are studied in this paper. Four basic strategies are constructed

Implementing Momentum Strategy with Options: Dynamic Scaling and Optimization Abstract: Momentum strategy and its option implementation are studied in this paper. Four basic strategies are constructed

Portfolio Management and Optimal Execution via Convex Optimization

Portfolio Management and Optimal Execution via Convex Optimization Enzo Busseti Stanford University April 9th, 2018 Problems portfolio management choose trades with optimization minimize risk, maximize

Portfolio Management and Optimal Execution via Convex Optimization Enzo Busseti Stanford University April 9th, 2018 Problems portfolio management choose trades with optimization minimize risk, maximize

Simulating the loss distribution of a corporate bond portfolio

Simulating the loss distribution of a corporate bond portfolio Srichander Ramaswamy Head of Investment Analysis Beatenberg, 2 September 2003 Summary of presentation Why do a simulation? On the computational

Simulating the loss distribution of a corporate bond portfolio Srichander Ramaswamy Head of Investment Analysis Beatenberg, 2 September 2003 Summary of presentation Why do a simulation? On the computational

Multi-Period Trading via Convex Optimization

Multi-Period Trading via Convex Optimization Stephen Boyd Enzo Busseti Steven Diamond Ronald Kahn Kwangmoo Koh Peter Nystrup Jan Speth Stanford University & Blackrock City University of Hong Kong September

Multi-Period Trading via Convex Optimization Stephen Boyd Enzo Busseti Steven Diamond Ronald Kahn Kwangmoo Koh Peter Nystrup Jan Speth Stanford University & Blackrock City University of Hong Kong September

EC316a: Advanced Scientific Computation, Fall Discrete time, continuous state dynamic models: solution methods

EC316a: Advanced Scientific Computation, Fall 2003 Notes Section 4 Discrete time, continuous state dynamic models: solution methods We consider now solution methods for discrete time models in which decisions

EC316a: Advanced Scientific Computation, Fall 2003 Notes Section 4 Discrete time, continuous state dynamic models: solution methods We consider now solution methods for discrete time models in which decisions

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

Chapter 10 Inventory Theory

Chapter 10 Inventory Theory 10.1. (a) Find the smallest n such that g(n) 0. g(1) = 3 g(2) =2 n = 2 (b) Find the smallest n such that g(n) 0. g(1) = 1 25 1 64 g(2) = 1 4 1 25 g(3) =1 1 4 g(4) = 1 16 1

Chapter 10 Inventory Theory 10.1. (a) Find the smallest n such that g(n) 0. g(1) = 3 g(2) =2 n = 2 (b) Find the smallest n such that g(n) 0. g(1) = 1 25 1 64 g(2) = 1 4 1 25 g(3) =1 1 4 g(4) = 1 16 1

Algorithmic Trading using Reinforcement Learning augmented with Hidden Markov Model

Algorithmic Trading using Reinforcement Learning augmented with Hidden Markov Model Simerjot Kaur (sk3391) Stanford University Abstract This work presents a novel algorithmic trading system based on reinforcement

Algorithmic Trading using Reinforcement Learning augmented with Hidden Markov Model Simerjot Kaur (sk3391) Stanford University Abstract This work presents a novel algorithmic trading system based on reinforcement

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Portfolio theory and risk management Homework set 2

Portfolio theory and risk management Homework set Filip Lindskog General information The homework set gives at most 3 points which are added to your result on the exam. You may work individually or in

Portfolio theory and risk management Homework set Filip Lindskog General information The homework set gives at most 3 points which are added to your result on the exam. You may work individually or in

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Handout 8: Introduction to Stochastic Dynamic Programming. 2 Examples of Stochastic Dynamic Programming Problems

SEEM 3470: Dynamic Optimization and Applications 2013 14 Second Term Handout 8: Introduction to Stochastic Dynamic Programming Instructor: Shiqian Ma March 10, 2014 Suggested Reading: Chapter 1 of Bertsekas,

SEEM 3470: Dynamic Optimization and Applications 2013 14 Second Term Handout 8: Introduction to Stochastic Dynamic Programming Instructor: Shiqian Ma March 10, 2014 Suggested Reading: Chapter 1 of Bertsekas,

Minimum Risk vs. Capital and Risk Diversification strategies for portfolio construction

Minimum Risk vs. Capital and Risk Diversification strategies for portfolio construction F. Cesarone 1 S. Colucci 2 1 Università degli Studi Roma Tre francesco.cesarone@uniroma3.it 2 Symphonia Sgr - Torino

Minimum Risk vs. Capital and Risk Diversification strategies for portfolio construction F. Cesarone 1 S. Colucci 2 1 Università degli Studi Roma Tre francesco.cesarone@uniroma3.it 2 Symphonia Sgr - Torino

Smart Beta: Managing Diversification of Minimum Variance Portfolios

Smart Beta: Managing Diversification of Minimum Variance Portfolios Jean-Charles Richard and Thierry Roncalli Lyxor Asset Management 1, France University of Évry, France Risk Based and Factor Investing

Smart Beta: Managing Diversification of Minimum Variance Portfolios Jean-Charles Richard and Thierry Roncalli Lyxor Asset Management 1, France University of Évry, France Risk Based and Factor Investing

Optimal Portfolio Liquidation and Macro Hedging

Bloomberg Quant Seminar, October 15, 2015 Optimal Portfolio Liquidation and Macro Hedging Marco Avellaneda Courant Institute, YU Joint work with Yilun Dong and Benjamin Valkai Liquidity Risk Measures Liquidity

Bloomberg Quant Seminar, October 15, 2015 Optimal Portfolio Liquidation and Macro Hedging Marco Avellaneda Courant Institute, YU Joint work with Yilun Dong and Benjamin Valkai Liquidity Risk Measures Liquidity

Dynamic Portfolio Choice II

Dynamic Portfolio Choice II Dynamic Programming Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Dynamic Portfolio Choice II 15.450, Fall 2010 1 / 35 Outline 1 Introduction to Dynamic

Dynamic Portfolio Choice II Dynamic Programming Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Dynamic Portfolio Choice II 15.450, Fall 2010 1 / 35 Outline 1 Introduction to Dynamic

Chapter 5 Portfolio. O. Afonso, P. B. Vasconcelos. Computational Economics: a concise introduction

Chapter 5 Portfolio O. Afonso, P. B. Vasconcelos Computational Economics: a concise introduction O. Afonso, P. B. Vasconcelos Computational Economics 1 / 22 Overview 1 Introduction 2 Economic model 3 Numerical

Chapter 5 Portfolio O. Afonso, P. B. Vasconcelos Computational Economics: a concise introduction O. Afonso, P. B. Vasconcelos Computational Economics 1 / 22 Overview 1 Introduction 2 Economic model 3 Numerical

Approximations of Stochastic Programs. Scenario Tree Reduction and Construction

Approximations of Stochastic Programs. Scenario Tree Reduction and Construction W. Römisch Humboldt-University Berlin Institute of Mathematics 10099 Berlin, Germany www.mathematik.hu-berlin.de/~romisch

Approximations of Stochastic Programs. Scenario Tree Reduction and Construction W. Römisch Humboldt-University Berlin Institute of Mathematics 10099 Berlin, Germany www.mathematik.hu-berlin.de/~romisch

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Resource Dedication Problem in a Multi-Project Environment*

1 Resource Dedication Problem in a Multi-Project Environment* Umut Be³ikci 1, Ümit Bilge 1 and Gündüz Ulusoy 2 1 Bogaziçi University, Turkey umut.besikci, bilge@boun.edu.tr 2 Sabanc University, Turkey

1 Resource Dedication Problem in a Multi-Project Environment* Umut Be³ikci 1, Ümit Bilge 1 and Gündüz Ulusoy 2 1 Bogaziçi University, Turkey umut.besikci, bilge@boun.edu.tr 2 Sabanc University, Turkey

9.1 Principal Component Analysis for Portfolios

Chapter 9 Alpha Trading By the name of the strategies, an alpha trading strategy is to select and trade portfolios so the alpha is maximized. Two important mathematical objects are factor analysis and

Chapter 9 Alpha Trading By the name of the strategies, an alpha trading strategy is to select and trade portfolios so the alpha is maximized. Two important mathematical objects are factor analysis and

Dynamic Asset and Liability Management Models for Pension Systems

Dynamic Asset and Liability Management Models for Pension Systems The Comparison between Multi-period Stochastic Programming Model and Stochastic Control Model Muneki Kawaguchi and Norio Hibiki June 1,

Dynamic Asset and Liability Management Models for Pension Systems The Comparison between Multi-period Stochastic Programming Model and Stochastic Control Model Muneki Kawaguchi and Norio Hibiki June 1,

Comparative analysis and estimation of mathematical methods of market risk valuation in application to Russian stock market.

Comparative analysis and estimation of mathematical methods of market risk valuation in application to Russian stock market. Andrey M. Boyarshinov Rapid development of risk management as a new kind of

Comparative analysis and estimation of mathematical methods of market risk valuation in application to Russian stock market. Andrey M. Boyarshinov Rapid development of risk management as a new kind of

SOLVING ROBUST SUPPLY CHAIN PROBLEMS

SOLVING ROBUST SUPPLY CHAIN PROBLEMS Daniel Bienstock Nuri Sercan Özbay Columbia University, New York November 13, 2005 Project with Lucent Technologies Optimize the inventory buffer levels in a complicated

SOLVING ROBUST SUPPLY CHAIN PROBLEMS Daniel Bienstock Nuri Sercan Özbay Columbia University, New York November 13, 2005 Project with Lucent Technologies Optimize the inventory buffer levels in a complicated

2016 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC 3: BUSINESS MATHEMATICS & STATISTICS

EXAMINATION NO. 16 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC : BUSINESS MATHEMATICS & STATISTICS WEDNESDAY 0 NOVEMBER 16 TIME ALLOWED : HOURS 9.00 AM - 12.00 NOON INSTRUCTIONS 1. You are allowed

EXAMINATION NO. 16 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC : BUSINESS MATHEMATICS & STATISTICS WEDNESDAY 0 NOVEMBER 16 TIME ALLOWED : HOURS 9.00 AM - 12.00 NOON INSTRUCTIONS 1. You are allowed

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Quantitative Measure. February Axioma Research Team

February 2018 How When It Comes to Momentum, Evaluate Don t Cramp My Style a Risk Model Quantitative Measure Risk model providers often commonly report the average value of the asset returns model. Some

February 2018 How When It Comes to Momentum, Evaluate Don t Cramp My Style a Risk Model Quantitative Measure Risk model providers often commonly report the average value of the asset returns model. Some

MS Project 2007 Page 1 of 18

MS Project 2007 Page 1 of 18 PROJECT MANAGEMENT (PM):- There are powerful environment forces contributed to the rapid expansion of the projects and project management approaches to the business problems

MS Project 2007 Page 1 of 18 PROJECT MANAGEMENT (PM):- There are powerful environment forces contributed to the rapid expansion of the projects and project management approaches to the business problems

P2.T8. Risk Management & Investment Management. Grinold, Chapter 14: Portfolio Construction

P2.T8. Risk Management & Investment Management Grinold, Chapter 14: Portfolio Construction Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Grinold, Chapter 14: Portfolio

P2.T8. Risk Management & Investment Management Grinold, Chapter 14: Portfolio Construction Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Grinold, Chapter 14: Portfolio

Predicting Foreign Exchange Arbitrage

Predicting Foreign Exchange Arbitrage Stefan Huber & Amy Wang 1 Introduction and Related Work The Covered Interest Parity condition ( CIP ) should dictate prices on the trillion-dollar foreign exchange

Predicting Foreign Exchange Arbitrage Stefan Huber & Amy Wang 1 Introduction and Related Work The Covered Interest Parity condition ( CIP ) should dictate prices on the trillion-dollar foreign exchange

The risk/return trade-off has been a

Efficient Risk/Return Frontiers for Credit Risk HELMUT MAUSSER AND DAN ROSEN HELMUT MAUSSER is a mathematician at Algorithmics Inc. in Toronto, Canada. DAN ROSEN is the director of research at Algorithmics

Efficient Risk/Return Frontiers for Credit Risk HELMUT MAUSSER AND DAN ROSEN HELMUT MAUSSER is a mathematician at Algorithmics Inc. in Toronto, Canada. DAN ROSEN is the director of research at Algorithmics

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

Optimal liquidation with market parameter shift: a forward approach

Optimal liquidation with market parameter shift: a forward approach (with S. Nadtochiy and T. Zariphopoulou) Haoran Wang Ph.D. candidate University of Texas at Austin ICERM June, 2017 Problem Setup and

Optimal liquidation with market parameter shift: a forward approach (with S. Nadtochiy and T. Zariphopoulou) Haoran Wang Ph.D. candidate University of Texas at Austin ICERM June, 2017 Problem Setup and

Edinburgh Research Explorer

Edinburgh Research Explorer A Global Chance-Constraint for Stochastic Inventory Systems Under Service Level Constraints Citation for published version: Rossi, R, Tarim, SA, Hnich, B & Pestwich, S 2008,

Edinburgh Research Explorer A Global Chance-Constraint for Stochastic Inventory Systems Under Service Level Constraints Citation for published version: Rossi, R, Tarim, SA, Hnich, B & Pestwich, S 2008,

Port(A,B) is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.

is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.") Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Portfolio Sharpening

Portfolio Sharpening Patrick Burns 21st September 2003 Abstract We explore the effective gain or loss in alpha from the point of view of the investor due to the volatility of a fund and its correlations

Portfolio Sharpening Patrick Burns 21st September 2003 Abstract We explore the effective gain or loss in alpha from the point of view of the investor due to the volatility of a fund and its correlations

Stochastic Portfolio Theory Optimization and the Origin of Rule-Based Investing.

Stochastic Portfolio Theory Optimization and the Origin of Rule-Based Investing. Gianluca Oderda, Ph.D., CFA London Quant Group Autumn Seminar 7-10 September 2014, Oxford Modern Portfolio Theory (MPT)

Stochastic Portfolio Theory Optimization and the Origin of Rule-Based Investing. Gianluca Oderda, Ph.D., CFA London Quant Group Autumn Seminar 7-10 September 2014, Oxford Modern Portfolio Theory (MPT)

Approximate methods for dynamic portfolio allocation under transaction costs

Western University Scholarship@Western Electronic Thesis and Dissertation Repository November 2012 Approximate methods for dynamic portfolio allocation under transaction costs Nabeel Butt The University

Western University Scholarship@Western Electronic Thesis and Dissertation Repository November 2012 Approximate methods for dynamic portfolio allocation under transaction costs Nabeel Butt The University

Portfolio Optimization

Portfolio Optimization Stephen Boyd EE103 Stanford University December 8, 2017 Outline Return and risk Portfolio investment Portfolio optimization Return and risk 2 Return of an asset over one period asset

Portfolio Optimization Stephen Boyd EE103 Stanford University December 8, 2017 Outline Return and risk Portfolio investment Portfolio optimization Return and risk 2 Return of an asset over one period asset

Regularizing Bayesian Predictive Regressions. Guanhao Feng

Regularizing Bayesian Predictive Regressions Guanhao Feng Booth School of Business, University of Chicago R/Finance 2017 (Joint work with Nicholas Polson) What do we study? A Bayesian predictive regression

Regularizing Bayesian Predictive Regressions Guanhao Feng Booth School of Business, University of Chicago R/Finance 2017 (Joint work with Nicholas Polson) What do we study? A Bayesian predictive regression

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

IMPA Commodities Course : Forward Price Models

IMPA Commodities Course : Forward Price Models Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Department of Statistics and Mathematical Finance Program, University of Toronto, Toronto, Canada http://www.utstat.utoronto.ca/sjaimung

IMPA Commodities Course : Forward Price Models Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Department of Statistics and Mathematical Finance Program, University of Toronto, Toronto, Canada http://www.utstat.utoronto.ca/sjaimung

Sensitivity Analysis with Data Tables. 10% annual interest now =$110 one year later. 10% annual interest now =$121 one year later

Sensitivity Analysis with Data Tables Time Value of Money: A Special kind of Trade-Off: $100 @ 10% annual interest now =$110 one year later $110 @ 10% annual interest now =$121 one year later $100 @ 10%

Sensitivity Analysis with Data Tables Time Value of Money: A Special kind of Trade-Off: $100 @ 10% annual interest now =$110 one year later $110 @ 10% annual interest now =$121 one year later $100 @ 10%

HOW TO HARNESS VOLATILITY TO UNLOCK ALPHA

HOW TO HARNESS VOLATILITY TO UNLOCK ALPHA The Excess Growth Rate: The Best-Kept Secret in Investing June 2017 UNCORRELATED ANSWERS TM Executive Summary Volatility is traditionally viewed exclusively as

HOW TO HARNESS VOLATILITY TO UNLOCK ALPHA The Excess Growth Rate: The Best-Kept Secret in Investing June 2017 UNCORRELATED ANSWERS TM Executive Summary Volatility is traditionally viewed exclusively as

6.231 DYNAMIC PROGRAMMING LECTURE 8 LECTURE OUTLINE

6.231 DYNAMIC PROGRAMMING LECTURE 8 LECTURE OUTLINE Suboptimal control Cost approximation methods: Classification Certainty equivalent control: An example Limited lookahead policies Performance bounds

6.231 DYNAMIC PROGRAMMING LECTURE 8 LECTURE OUTLINE Suboptimal control Cost approximation methods: Classification Certainty equivalent control: An example Limited lookahead policies Performance bounds

Session 5. Predictive Modeling in Life Insurance

SOA Predictive Analytics Seminar Hong Kong 29 Aug. 2018 Hong Kong Session 5 Predictive Modeling in Life Insurance Jingyi Zhang, Ph.D Predictive Modeling in Life Insurance JINGYI ZHANG PhD Scientist Global

SOA Predictive Analytics Seminar Hong Kong 29 Aug. 2018 Hong Kong Session 5 Predictive Modeling in Life Insurance Jingyi Zhang, Ph.D Predictive Modeling in Life Insurance JINGYI ZHANG PhD Scientist Global