Monetary and Macro-Prudential Policies

|

|

|

- Lily Norton

- 6 years ago

- Views:

Transcription

and is intended for use in IMF Institute courses.")

1 Monetary and Macro-Prudential Policies Jorge Roldos IMF-CEMLA Course Central Bank of Brazil, Brasilia October 213 This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute courses. Any reuse requires the permission of the IMF Institute.

2 There is a danger that the macroeconomic models now in use in central banks have been constructed in the past as part of the war against inflation. The central banks are prepared to fight the last war. But are they prepared to fight the new one against financial upheavals and recession? The macroeconomic models they have today certainly do not provide them with the right tools to be successful. Paul de Grauwe, 28

3 Contents Monetary Policy in Inflation Targeting Regimes Case Study 1: Inflation Targeting and Financial Instability Monetary Models and Financial Intermediation Monetary and Macro-Prudential Policies Monetary versus Macro-Prudential Rules Assessing the Macro Impact of Basel III

4 I. Monetary Policy and Inflation Targeting Central banks have three main objectives: Price Stability Output/ Employment Stability Financial Stability Monetary Policy J.Roldos 4

5 I. Monetary Policy and Inflation Targeting Financial Stability has always been an objective for central banks Lender of last resort (LOLR) function Main reason for their creation in many cases After WWII, output and price stability became the main objectives In the 199 s, monetary dominance overtakes fiscal dominance in macro policies

6 Convergence in Macroeconomics Since the mid-198 s we saw Great Moderation A new macroeconomic synthesis emerged Macro analysis should use models with consistent intertemporal general equilibrium foundation (DSGE) Econometrically validated/calibrated Endogenous expectations Monetary policy should use interest rate to manage aggregate demand New Keynesian model used by many central banks

7 The New Keynesian DSGE Model Aggregate demand, IS equation x = Ex [ r Eπ r ], where x = y y * * t t t+ 1 t t t+ 1 t t t t is the output gap Expectations-augmented Phillips curve πt = βetπt+ 1 + κxt, where πt is inflation Policy (Taylor) rule rt = αrt 1 + (1 α)[ φπ π t + φxxt], where rt is the interest rate

8 The New Keynesian DSGE Model It is basically the IS-LM model with a Monetary Policy (MP) rule instead of LM (MM equilibrium) Macroeconomic equilibrium shown in next charts (for given inflation expectations) This three-equation NK model (Clarida-Gertler- Gali) became the backbone of central banks inflation targeting (IT) regimes

9 The NK-DSGE is an IS-MP Model

10 Case Study 1: Inflation Targeting May Lead to Financial Instability Based on Christiano et al. (27) There is empirical evidence that episodes of low goods price inflation are associated with high asset price inflation (stock price booms) Boom may reflect inefficiently loose monetary policy in an IT regime, when optimism about the future requires high real interest rates Problem of misusing the NK model

11 Periods of low inflation coincide with stock price and credit booms (U.S )

12 Periods of low inflation coincide with stock price and credit booms (U.S )

13 Summary Statistical Evidence

14 Case Study 1: Inflation Targeting May Lead to Financial Instability Boom-bust can be rationalized with NK model Problem is that model is a gap model: all variables as deviations from steady state And steady-state is not constant, should reflect the evolution of natural output, rates Moreover, news or signals of better future times could be an important driver of natural GDP, interest rates

15 The missing part of the 3-equation NK-model Natural or equilibrium output responds to productivity ( supply ) and leisure/labor ( demand ) shocks: * 1 yt = at τ t, where at is the productivity shock ϕ r = E ( y y ) = E ( a a ), and a evolves as: * * * t t t+ 1 t t t+ 1 t t a = ρa + u ; u = ξ + ξ ; ξ is "news shock" 1 1 t t 1 t t t t 1 t 1 The news shock is signal of future productivity

16 The missing part of the 3-equation NK-model Replacing evolution of technology into equilibrium interest rate: r = ( 1) a + * ρ ξ 1 t t t small large News of future technology improvement requires higher current real interest rate

17 The missing part of the 3-equation NK-model But in the NK model higher future productivity means lower future marginal costs and inflation mc π π r e e t+ j t+ j t t (Taylor Rule) and Taylor rule leads central bank to lower current nominal interest rate, inflating asset prices and creating a boom

18 Case Study 1: Inflation Targeting May Lead to Financial Instability Bottom line: ignoring the underlying structural economy, and/or relevant shocks, could lead to mistakes in model use CIMR (27) show that including a response to credit growth in the monetary policy rule improves welfare by avoiding boom-bust Why? : Credit growth responds to signal of higher future productivity, push rates higher Go back to themes of L-3, credit boom-bust

19 II. Monetary Policy Models and Financial Intermediation (FI) Early attempts to add FI to macro models: Two interest rates Rationale for FI IS curve flatter (FA) Shocks to credit supply important for business cycles (shifts to IS curve)

20 A Disruption to Credit Supply

21

22 II. Monetary Policy Models and Financial Intermediation Main challenge to NK DSGE (or any) model is that FI requires two types of agents: borrower (impatient) and lender (patient) Another challenge is the behavior of the FI, and the resource cost for the economy And a final one is keeping track of the dynamics of borrowing (credit) Some classes of models that have made progress on these are reviewed in what follows

23 Curdia-Woodford (29) Simple NK model with two additions 1. Heterogeneous households (borrower&lender) 2. Costly FI: resource cost and NPL Two factors affect the three equations: λ λ =Ω = s + δeω, where Ω is mg utility gap b s t t t t t t+ 1 t r r = s b =Ξ b + χ b b s ' ' t t t( t) t( ) t( ), spread = mg cost of lending, where Ξ ( b) is resource cost of lending and χ ( b) are NPLs t t

24 Curdia-Woodford (29) A fourth equation would have to be added: s bt = δ[1 + αsst + αbξ t] bt 1(1 + rt 1) / πt αbξ t( bt) + other b s (1 + r ) b = (1 + r ) d, is FI balance sheet t t t t cost of borrow The three-equation model suffices only in special case where credit spread evolves exogenously and FI uses no resources (spread is just a mark-up)

25 Curdia-Woodford (29) Even under such strict conditions, response to financial shock is equivalent to simultaneous shocks to: Natural interest rate Cost-push inflation Monetary policy shock Result: Monetary Policy Rule that incorporates credit spread is better (more on this below), but weight depends on persistence of the financial shock

26 Christiano, Motto and Rostagno (29) Model combines NK DSGE with capital accumulation, and financial accelerator (FA) Savings done by household, and risk neutral entrepreneur borrows to invest Need to add three new equations: 1. Optimal lending contract (menu) 2. Bank s zero profit condition 3. Law of motion for entrepreneur net worth

27 Christiano, Motto and Rostagno (29) Optimal contract where marginal revenue equals marginal cost of internal funds times external finance premium (EFP): αr QK = ρω ( ) R Q, where ρω ( ) is the EFP and R k it, + 1 k α 1 t+ 1 t t+ 1 t+ 1 t ω = [ MPK + (1 δ) Q ] it, + 1 t+ 1 t+ 1 Q t is the return on capital Individual, idioscincratic shocks averaged out

28 Christiano, Motto and Rostagno (29) Bank monitors borrower at default such that expected return equals cost of funds: [ ( ) ( )] k α Γ ω µ Gω Rt Qt 1Kt = RB t t, where µ is monitoring cost expected proj. success Combining both expressions we get credit spread as a function of leverage: R R QK = S = N k t+ 1 t t+ 1 t+ 1 t+ 1 SL [ ( ω)]

29 Christiano, Motto and Rostagno (29) The evolution of entrepreneur net worth is: N = R Q K RB = k t+ 1 t t 1 t t t N = ( R Q R ) K + R N k t 1 t t+ 1 t t t t Nt Asset Returns-Debt Payout Entrepreneur s net worth grows with leverage Incentive to max leverage, mitigated by increasing spread

30 Christiano, Motto and Rostagno (29) Log-linearizing the two equations we get: fi fi s = χ( q + k n ) + ε, where ε is shock to FI t t t t t t n = Lr ( L 1)( s + r π ) + θn + ε, k nw t t 1 t 1 t 1 t t 1 t where ε nw t is shock to net worth The financial shock could also be an increase in the volatility of the firm s profitability A (tail) risk shock, on real sector This type of shock sacounts for a large share of business cycles in US and EU

31

32

33 Christiano, Motto and Rostagno (29) First shock to entrepreneurial risk leads to: Increase in spreads from 22 to 24 bps Reduction in D/N from.92 to.8, 13% fall in loans Second shock, Δ in monitoring/bankruptcy cost: Spread or EFP falls 64 bps (demand dominates) Similar reduction in D/N or lending Monetary Policy tightening of 25 percent: Spread rises by 34 bps Lending falls 1 percent

34 Christiano, Motto and Rostagno (29) Model with micro-founded FI shows how moves in spread may be small compared to those in lending (if dem&supply move same direction) Models with spread only (or without explicit contract for lending could be misleading) Again, adding credit growth to Monetary Policy rule improves welfare One draw back of CMR: intermediary has no capital; no bank failure or runs

35 Gilchrist and Zakrjsek (211) Similar NK with FA, but shock to FI (not real project) χ QK t t+ 1 exp( σ t), and the shock to FI follows: Nt St = σ = (1 ρ) σ + ρσ + ε t t 1 t An Δσ increases cost of FI for given leverage Model matches the recent U.S. crisis, and spread-augmented MP rule stabilizes GDP (with a bit of Δ inflation)

36 Gilchrist and Zakrjsek (211)

37 Gilchrist and Zakrjsek (211)

38 Gilchrist and Zakrjsek (211)

39 II. Monetary Policy Models and Financial Intermediation (FI) cont. Taking stock: NK DSGE + FA provides a good degree of amplification Dynamics of non-financial sector balance sheet and leverage micro-founded; spreads are counter-cyclical, good data fit But no meaningful FI, same with collateral constraints framework (see next table) Next class of models explicitly introduce a costly banking sector

40 Source: IMF/WP/

41 Gerali et al. (21) A NK DSGE model with an explicit banking sector and collateral constraints Emphasis on supply-side of credit markets Entrepreneurs and impatient households (HHs) borrow, patient HHs lend deposits to banks Banks are monopolistically competitive, setting sticky loan and deposit rates; bank capital One wholesale branch, two retail branches

42 Gerali et al. (21) Motivation: Interest rate spreads affected by degree of competition and bank capital costs

43 Gerali et al. (21) Entrepreneurs and impatient HHs borrow subject to collateral (LTV) constraints: Rb( i) me[ q k( i) π ], where m is the LTV b k t t t t t+ 1 t t+ 1 t Banks lending and deposit rates are set taking into account future values of the policy rate R > R > R b d t t t 5.3>3.6>2.4 (percent) ; lending, policy and deposit rates

44 Gerali et al. (21) Bank capital is accumulated out of retained earnings π K = (1 δ ) K + j ; where j are retained earnings b b b b b t t t 1 t t Banks max profits, and is costly to adjust banks capital ratio (inverse to leverage L) 2 b b d κ K b t b b max RB t t RD t t υ Kt ; υ is targeted CAR 2 B t

45 Gerali et al. (21) Wholesale bank lending rates then depend on: R 2 b b b d Kt b K t t = Rt κ υ Bt Bt Bank spread depends on bank leverage in contrast to CMR (on firm s leverage) 2 b b w b d Kt b K t t = t t = κ υ Bt Bt S R R,

46 Gerali et al. (21) Macroeconomic shocks affect banks profits and capital, with feedback to the real economy Banks affect monetary transmission, attenuating effects on real economy (sticky interest rates) Banks also are subject to financial shocks (spreads, collateral and capital) that affect the economy Financial shocks explain large share of GDP fluctuations in (next)

47

48 Gerali et al. (21) Model suited to study effects of bank capital loss (crisis) as well as recapitalization efforts After capital loss, banks attempt to rebuild balance sheet: cut lending and increase spread Firms reduce investment, but increase capacity utilization and labor demand Inflation lead central bank to tighten marginally Stress scenario with added ΔCAR (regulation)

49 Gerali et al.: Loss of Bank Capital

50 Gerali et al.: Loss of Bank Capital

51 III. Monetary and Macro-Prudential Policies The models sketched before allow for a number of applications In particular, analysis of monetary and macroprudential policies Next, three applications Monetary versus Macro-Prudential Rules Impact of Basel III on GDP Counter-cyclical capital adequacy ratios

52 Monetary versus Macro-Prudential Rules Based on Kannan, Rabanal and Scott (29) Key question: should central bank willing to mitigate boom-bust cycles move policy rate in response to credit or asset prices/spreads? Answer is YES, but for purely financial shock the macro-prudential instrument has comparative advantage over MP rate Discretion needed since is hard to know the source of shocks

53 Kannan, Rabanal and Scott (29) Model has non-durable and durable good (housing), only real asset Patient (lender) and impatient (borrower) HHs FI set lending rate as function of LTV, s.t. financial shock and macro-prudential instrument: b b h R = ν RF( B / QK ) τ ; where F (.) >, F (.) > ; t t t t t t t ν, τ, are financial shock and macroprudential instrument t t

54 Kannan, Rabanal and Scott (29) Compare four policy regimes: Taylor Rule Augmented Taylor Rule (with credit growth) Augmented Taylor Rule + Macro-prudential Optimization [Augm.TR + Macro-prudential] The augmented TR and macro-prudential are: Rt = γrrt 1+ (1 γr)[ γπ π t 1+ γ yxt 1+ γbbt 1], augm. TR τ = τ( B ), macroprudential instrument t t 1

55

56 Effect of a Financial Shock

57

58 Effect of a Productivity Shock

59 Kannan, Rabanal and Scott (29) Bottom line: comparative advantage dictates that macro-prudential (M Policy) instrument should be used against financial (technology) shock Critical to be able to isolate shocks The higher the incidence of financial shocks in an economy, the more important the relative use of the macro-prudential instrument (LTV, RR)

60

61 Case Study 2: Shocks to World Interest Rates and Capital Flows In the aftermath of Lehman Bros. collapse, most countries cut interest rates sharply Same in major EM countries, but some of them cut Reserve Requirements even more (and earlier); especially Brazil and Peru (chart) What is the best response to this shock (and associated fluctuations in capital flows)? What if rates go back up (Fed normalization )?

62 MP Rate and Reserve Requirements

63 Shock to the World Interest Rate

64 Case Study 2: Shocks to Global Interest Rates and Capital Flows In Christiano et al, future (positive) productivity shocks increase the natural rate of interest But their was closed-economy model: for shock to global rates we want an open-economy model A few available, focus on other shocks or on response with capital controls An exception is Medina and Roldos (forthcoming IMF/WP), next

65 Overview of the Model Small open economy Two differentiated tradable goods: Home and Foreign Nominal friction: price rigidity a-la-calvo (1983) Financial friction: financial accelerator plus a firesales amplification mechanism Solvency: loans default (Bernanke, Gertler and Gilchrist, BGG, 1999) Liquidity: real and financial resources are needed to liquidate distressed assets (extension of Choi-Cook, 212)

66 Firms Labor Market Capital Producers Entrepreneurs l R K R Households D R Liquidity Intermediaries IB R Lending Intermediaries K l IB D R > R > R > R

67 Figure 2 Timing of events Period t Period t+1 Using net worth and loans Entrepreneur buys new eop capital K t + 1 from capital goods producers B ω + 1 t After realization of shock t Entrepreneur supplies capital services Entrepreneur sell undepreciated (1 δ ) Kt+ 1 to capital producers, repays loan to lend-intermediary Production and Consumption Capital producers buy new, undepreciated and restructured capital Liquid-intermediary takes deposits, lends to interbank market and CB; Provides liquidity services Lend-intermediary sells defaulted capital to liquidintermediary; lends to finance next period capital

68 Financial Intermediaries and Spreads The two financial intermediaries summarize the main functions of a financial system: Provision of credit services Provision of liquidity services Both functions contribute to a wedge between deposit and lending rates: Endogenous spreads will interact with monetary policy rate and macro-prudential instrument

69 Credit Intermediary (1) Provides loans to entrepreneurs under a BGG contract that solves the agency problem The average return to capital for the entrepreneurs is capital is: R = VMPK + (1 δ ) Q ; where VMPK is the rental rate K t+ 1 t+ 1 t+ 1 t+ 1 Qt and Q t the price of capital

70 Credit Intermediary (2) Threshold condition for lending rate: R ϖ K Q = R B, where R is loan rate and k l l t+ 1 t+ 1 t+ 1 t t+ 1 t t+ 1 is the loan Zero profit condition for credit intermediary: B t ϖ t+ 1 IB ( VMPK ) [1 Φ ( ϖφ( )]; R B) +, + (1 δ) FS k ωd ω σ ω = R B l t+ 1 t+ 1 t t+ 1 t+ 1 t+ 1 t+ 1 t Revenue if loan repaid Revenue if default Cost of Funds where Φ( ϖ ) is the probability of default and FS t + 1 t+ 1 is the fire-sale price of the defaulted capital

71 Credit Intermediary (3) Define: µ t+ 1 = ( Qt+ 1 FSt+ 1)(1 δ ), VMPK + (1 δ ) Q t+ 1 t+ 1 Then, zero profit condition for credit intermediary is: l k IB [1 Φ Φ( ( ϖ t+ 1; )] Rt+ ) 1Bt + ( 1 µ t+ 1) Rt+ 1Qk t t+ 1 ωd ω σ ω = R t + 1Bt, Revenue if loan repaid Revenue if default Cost of Funds In contrast to BGG, cost of default is endogenous (and countercyclical); in recession: Prob (Default) increases Recovery rates fall (cost of default increases) ϖ

72 Liquidity Intermediary (1) Demand for liquidity services: lqt =υkdt,, where lqt are liquidity services To provide liquidity services, LI requires real and financial ( excess reserves ) resources 1 αlq 1 α t = t t xr lq min[ n ; xr ], where n is in units of final goods, and xr is "excess reserves"

73 Liquidity Intermediary (2) Maximize benefits derived from the use of deposits: IB MA RE D Dt max (1 s ) R + s R R Pn D,,( / ) R t t t t t t t ns DP t Allocation of funds: MA s t s t 1 Reserve Requirement Exc. Reserves Lending to Interbank Market

74 Liquidity Intermediary (3) Optimal condition for liquidity intermediary: (1 α ) lq lq IB t R = g R xr D t t t t IB MA 1 D MA t = (1 t ) [ t t ] R s R s Fire sale (or cash-in-the-market ) price: ( ) (1 )(1 ) [ ] FSt = ηkqt υ ft + gt + ηk δ Et sdt+ FSt+ Equilibrium in the interbank market: B = (1 s ) D t t t 1 1

75 Nominal friction Wholesale producers sell differentiated goods, a composite of domestic and imported goods Set sticky prices a-la-calvo Phillips curve: β χ log(1 + π ) = E [log(1 + π )] + log(1 + π ) p t t t+ 1 t 1 1+ βχ p 1+ βχ p marginal cost is: mgcr (1 ) (1 φp)(1 βφp) mgcr t + log, where φp (1 + βχ p ) mgcss 1 θ d * Pyt, ep t t t = αd + αd Pt Pt 1 1 θ d 1 θ d

76 Aggregate Equilibrium Aggregate (domestic) demand is given by da = c + c + inv + n t t kt, t t And is equal to the supply of final goods (adjusted by the price distortion or nominal friction disp ) da = ( disp ) y 1 t t st,

77 Summary of Spread Determinants The spread between the lending rate and the deposit rate is determined by leverage and liquidity conditions; policy instruments: l d MA R = R f QK / N, µ Q FS ; s macro leverage liquidity pru policy instr.

78 Calibration Macro-parameters: standard Financial system parameters: (i) annual default rate of 3 percent (in line with BGG); (ii) a leverage ratio of 4 percent (mid-point between BGG and estimate from Gonzalez-Miranda (212) ); (iii) an average cost of liquidation of 6 percent These parameter values imply: R K = 13.7% > R l = 6.6%, R IB = 4.5%, R D = 4% (in annual basis) a recovery rate of around 36 percent entrepreneurs debt/credit is 55 percent of annual GDP deposits, as percentage of annual GDP, is 61 percent Excess reserves as percentage of annual GDP of.15 percent

79 Alternative Policies We consider four alternative regimes 1. Standard Taylor rule and constant reserve requirement (RR) 2. Inflation Targeting and constant RR 3. Augmented Taylor rule and constant RR IB R t log = ψπ log(1 + πt) + ψ ylog( yt) + ψblog( bt) 1+ r 4. Inflation Targeting and countercyclical RR MA s t xr t log φxr log MA = s xr

80 Natural Price rigidities, financial frictions+it regime Price rigidities, financial frictions+augmented Taylor rule forces and more debt/credit 1.5 GDP 8 Investment 2 Real exchange rate 1 interbank rate Dev. from SS aggregate demand 4 default rate inflation rate 4 Tobin Q Dev. from SS fire sale price 4 deposits (% SS GDP) 4 ent. debt (% SS GDP) 1 deposit rate Dev. from SS excess of reserves (% SS GDP) 1 Foreign debt (% SS GDP) 3 networth (% SS GDP) 2 Loan rate Dev. from SS Quarters Quarters Quarters Quarters

81 Alternative policies (w/o MaPP) 1 Reserve requirement (% Deposits) 2 Cost of Liquidation 3 Recovery Rate Dev. from SS Quarters Quarters Quarters Policy Framework Welfare Losses (+)/ gains (-) expressed relative to the deterministic SS welfare in terms of SS consumption Standard Taylor rule % IT regime % Augmented Taylor rule %

82 Natural Price rigidities, financial frictions+it regime Price rigidities, financial frictions+augmented Taylor rule Price rigidities, financial frictions+it regime & countercyclical res. req. 1.5 GDP 8 Investment 2 Real exchange rate 1 interbank rate Dev. from SS aggregate demand 4 default rate inflation rate 4 Tobin Q Dev. from SS fire sale price 4 deposits (% SS GDP) 4 ent. debt (% SS GDP) 1 deposit rate Dev. from SS excess of reserves (% SS GDP) 1 Foreign debt (% SS GDP) 3 networth (% SS GDP) 2 Loan rate Dev. from SS Quarters Quarters Quarters Quarters

83 Higher Welfare with Countercyclical RR Policy Framework Welfare Losses (+)/ gains (-) expressed relative to the deterministic SS welfare in terms of SS consumption 3 Augmented Taylor type rule % 4 IT regime and Countercyclical RR % 3 Reserve requirement (% Deposits) 2 Cost of Liquidation 3 Recovery Rate Dev. from SS Quarters Quarters Quarters

84 MP rate: coordinate with Macroprudential tool Tinbergen, Mundell principles MP rate has to follow the natural rate and be adjusted by the RR 1 interbank rate

85 Robustness: Dollarization (1) Include foreign debt (denominated in dollars) for entrepreneurs and credit intermediaries More financial volatility, but same policy ranking Policy Framework Welfare Losses (+)/ gains (-) expressed relative to the deterministic SS welfare in terms of SS consumption 1 Standard Taylor rule % 2 IT Regime % 3 Augmented Taylor rule % 4 IT regime and Countercyclical RR %

86 Robustness: Dollarization (2) Loans to entrepreneurs are denominated in dollars. This also rises the volatility Taylor rules dominate IT, MaPP improves the welfare even more. Policy Framework Welfare Losses (+)/ gains (-) expressed relative to the deterministic SS welfare in terms of SS consumption 1 Standard Taylor type rule % 2 IT Regime % 3 Augmented Taylor type rule % 4 IT regime and Countercyclical RR %

87 Dollarization (2) Natural Price rigidities, financial frictions+it regime Price rigidities, financial frictions+augmented Taylor rule Price rigidities, financial frictions+it regime & countercyclical res. req. 1.5 GDP 1 Investment 2 Real exchange rate 1 interbank rate Dev. from SS aggregate demand 1 default rate inflation rate 1 Tobin Q Dev. from SS fire sale price 6 deposits (% SS GDP) 6 ent. debt (% SS GDP) 1 deposit rate Dev. from SS excess of reserves (% SS GDP) 1 Foreign debt (% SS GDP) 4 networth (% SS GDP) 1 Loan rate Dev. from SS Quarters Quarters Quarters Quarters

88 Robustness: Wage rigidities Only a fraction of workers adjust their wages to labor market condition every period (Blanchard- Galí, 27) This increases the responses of asset prices and defaults. Distortions reinforce each other and MaPP delivers more welfare benefits Losses (+)/ gains (-) expressed Policy Framework Welfare relative to the deterministic SS welfare in terms of SS consumption 1 Standard Taylor type rule % 2 IT Regime % 3 Augmented Taylor type rule % 4 IT regime and Countercyclical RR %

89 Case Study 2: Conclusion A countercyclical macroprudential policy is better suited to manage the volatility of world interest rates and associated capital flows Conclusion is robust to different combinations of nominal and financial frictions (other MaPP instruments? Probably, see next) Inflation Targeting continues to be the main monetary policy objective, but MP rate must accommodate moves in the natural interest rate and reserve requirements

90 Bianchi: Equivalence Between Reserve and Capital Adequacy Requirements

91 Bianchi s Equivalence Result

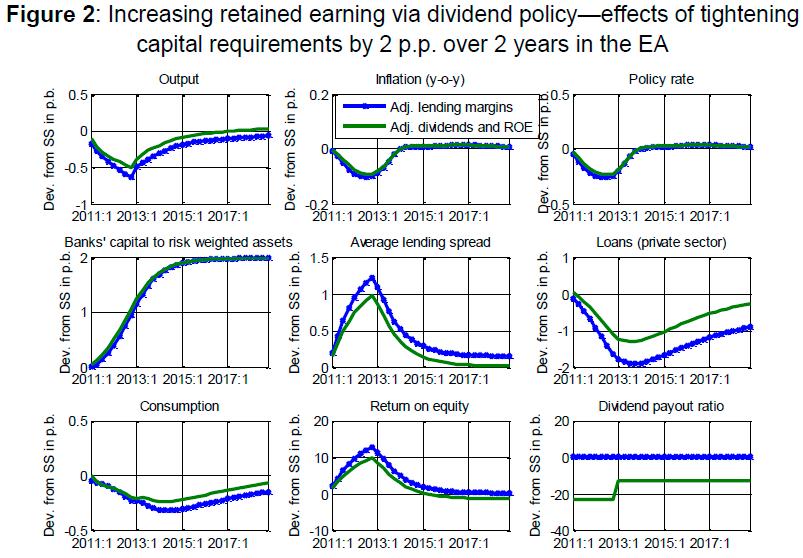

92 Macroeconomic Costs of Higher CAR Based on Rogers and Vlcek (IMF WP/11/13) Model similar to Gerali et al The macroeconomic impact of a 2% increase in CAR depends on: Banks optimal response: increase spreads, reduce dividends or lending Monetary policy response Implementation period

93 Macroeconomic Costs of Higher CAR The increase in CAR happens gradually over two years The least costly option is to reduce distribution of bank dividends But is not enough: next comes an increase in spreads Finally, last resort is a reduction in lending (with maximum negative impact on GDP)

94

95

96

97 Macroeconomic Costs of Higher Two effects: Liquidity Requirements Lower bank revenues, thus higher spreads Lower risky assets, thus less capital needed The last effect means that liquidity and CAR become complements; interaction effects are very important For a 25% increase in liquid assets, spreads increase only about 5 bps

98

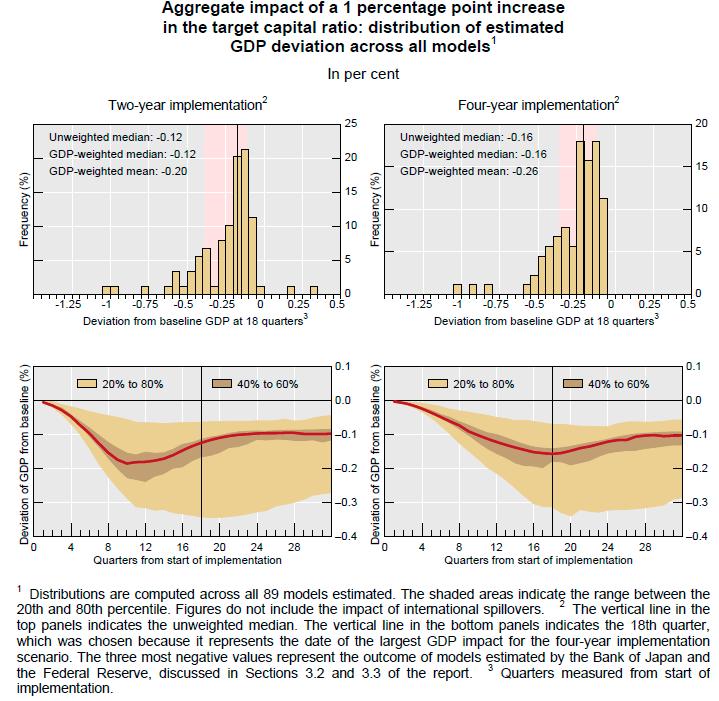

99 BIS Assessment of Δ CAR Conducted with a battery of models, across several countries Results are similar to those just shown with IMF model Typically, output reduction is rather small Contrast with industry estimates

100

101 Counter-cyclical Capital Buffers Using models similar to above examples, IMF (GFSR September 211) estimates role of counter-cyclical capital buffers on financial and macro-economic stability Baseline is an asset price bubble that builds up financial imbalances Volatility of GDP and trade balance are much lower with counter-cyclical buffer (next)

102

103 Credit Boom in Open Economy Model with simple FA (Unsal, IMF WP/11/189) where an improvement in external conditions leads to capital inflow Imposing regulatory premium complements monetary policy (theme of afternoon workshop)

104 Final Thoughts on Model Use Models reviewed (and others) are showing promising results for a number of macroprudential policy analyses The sources of shocks hitting the economy are critical Models could be used to deliver implications for other variables, to help decide whether an increase in credit growth is an imbalance (say, bubble) or genuine (due to productivity)

105

106 Final Thoughts on Model Use Successful use of models require deep understanding of transmission mechanisms, relation to data, and above all judgment However, some models ignore a number of important issues, many raised by recent crisis In particular, increased risk-taking, bank runs and asset price bubbles Need to be complemented with indicators of build-up of imbalances and financial intelligence

107 Final Thoughts Monetary and Macro-Prudential Policies are broadly complementary Models are useful, if used with judgment Financial Stability is a central bank objective, to be achieved with appropriate weight to monetary and macro-prudential tools It is critical to identify the source of shocks: financial or others; models and indicators useful for this as well

108 Thank You!

Capital Flows, Financial Intermediation and Macroprudential Policies

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Credit Frictions and Optimal Monetary Policy. Vasco Curdia (FRB New York) Michael Woodford (Columbia University)

Michael Woodford (Columbia University)") MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

Concerted Efforts? Monetary Policy and Macro-Prudential Tools

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

A Model with Costly-State Verification

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

A Policy Model for Analyzing Macroprudential and Monetary Policies

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

Lecture 4. Extensions to the Open Economy. and. Emerging Market Crises

Lecture 4 Extensions to the Open Economy and Emerging Market Crises Mark Gertler NYU June 2009 0 Objectives Develop micro-founded open-economy quantitative macro model with real/financial interactions

Lecture 4 Extensions to the Open Economy and Emerging Market Crises Mark Gertler NYU June 2009 0 Objectives Develop micro-founded open-economy quantitative macro model with real/financial interactions

Credit Frictions and Optimal Monetary Policy

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Asset Price Bubbles and Monetary Policy in a Small Open Economy

Asset Price Bubbles and Monetary Policy in a Small Open Economy Martha López Central Bank of Colombia Sixth BIS CCA Research Conference 13 April 2015 López (Central Bank of Colombia) (Central A. P. Bubbles

Asset Price Bubbles and Monetary Policy in a Small Open Economy Martha López Central Bank of Colombia Sixth BIS CCA Research Conference 13 April 2015 López (Central Bank of Colombia) (Central A. P. Bubbles

Asset Prices, Collateral and Unconventional Monetary Policy in a DSGE model

Asset Prices, Collateral and Unconventional Monetary Policy in a DSGE model Bundesbank and Goethe-University Frankfurt Department of Money and Macroeconomics January 24th, 212 Bank of England Motivation

Asset Prices, Collateral and Unconventional Monetary Policy in a DSGE model Bundesbank and Goethe-University Frankfurt Department of Money and Macroeconomics January 24th, 212 Bank of England Motivation

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Credit Frictions and Optimal Monetary Policy

Vasco Cúrdia FRB of New York 1 Michael Woodford Columbia University National Bank of Belgium, October 28 1 The views expressed in this paper are those of the author and do not necessarily re ect the position

Vasco Cúrdia FRB of New York 1 Michael Woodford Columbia University National Bank of Belgium, October 28 1 The views expressed in this paper are those of the author and do not necessarily re ect the position

Capital Controls and Optimal Chinese Monetary Policy 1

Capital Controls and Optimal Chinese Monetary Policy 1 Chun Chang a Zheng Liu b Mark Spiegel b a Shanghai Advanced Institute of Finance b Federal Reserve Bank of San Francisco International Monetary Fund

Capital Controls and Optimal Chinese Monetary Policy 1 Chun Chang a Zheng Liu b Mark Spiegel b a Shanghai Advanced Institute of Finance b Federal Reserve Bank of San Francisco International Monetary Fund

CAPITAL FLOWS AND FINANCIAL FRAGILITY IN EMERGING ASIAN ECONOMIES: A DSGE APPROACH α. Nur M. Adhi Purwanto

CAPITAL FLOWS AND FINANCIAL FRAGILITY IN EMERGING ASIAN ECONOMIES: A DSGE APPROACH α Nur M. Adhi Purwanto Abstract The objective of this paper is to study the interaction of monetary, macroprudential and

CAPITAL FLOWS AND FINANCIAL FRAGILITY IN EMERGING ASIAN ECONOMIES: A DSGE APPROACH α Nur M. Adhi Purwanto Abstract The objective of this paper is to study the interaction of monetary, macroprudential and

Reforms in a Debt Overhang

Structural Javier Andrés, Óscar Arce and Carlos Thomas 3 National Bank of Belgium, June 8 4 Universidad de Valencia, Banco de España Banco de España 3 Banco de España National Bank of Belgium, June 8 4

Structural Javier Andrés, Óscar Arce and Carlos Thomas 3 National Bank of Belgium, June 8 4 Universidad de Valencia, Banco de España Banco de España 3 Banco de España National Bank of Belgium, June 8 4

Fiscal Multipliers in Recessions

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

House Prices, Credit Growth, and Excess Volatility:

House Prices, Credit Growth, and Excess Volatility: Implications for Monetary and Macroprudential Policy Paolo Gelain Kevin J. Lansing 2 Caterina Mendicino 3 4th Annual IJCB Fall Conference New Frameworks

House Prices, Credit Growth, and Excess Volatility: Implications for Monetary and Macroprudential Policy Paolo Gelain Kevin J. Lansing 2 Caterina Mendicino 3 4th Annual IJCB Fall Conference New Frameworks

Optimal Monetary Policy Rules and House Prices: The Role of Financial Frictions

Optimal Monetary Policy Rules and House Prices: The Role of Financial Frictions A. Notarpietro S. Siviero Banca d Italia 1 Housing, Stability and the Macroeconomy: International Perspectives Dallas Fed

Optimal Monetary Policy Rules and House Prices: The Role of Financial Frictions A. Notarpietro S. Siviero Banca d Italia 1 Housing, Stability and the Macroeconomy: International Perspectives Dallas Fed

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

Monetary Economics. Financial Markets and the Business Cycle: The Bernanke and Gertler Model. Nicola Viegi. September 2010

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Output Gap, Monetary Policy Trade-Offs and Financial Frictions

Output Gap, Monetary Policy Trade-Offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank Marzie Taheri Sanjani International Monetary Fund Seminar at Narodowy Bank Polski

Output Gap, Monetary Policy Trade-Offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank Marzie Taheri Sanjani International Monetary Fund Seminar at Narodowy Bank Polski

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

DSGE Models with Financial Frictions

DSGE Models with Financial Frictions Simon Gilchrist 1 1 Boston University and NBER September 2014 Overview OLG Model New Keynesian Model with Capital New Keynesian Model with Financial Accelerator Introduction

DSGE Models with Financial Frictions Simon Gilchrist 1 1 Boston University and NBER September 2014 Overview OLG Model New Keynesian Model with Capital New Keynesian Model with Financial Accelerator Introduction

Fiscal Multipliers in Recessions. M. Canzoneri, F. Collard, H. Dellas and B. Diba

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

Fiscal Multipliers and Financial Crises

Fiscal Multipliers and Financial Crises Miguel Faria-e-Castro New York University June 20, 2017 1 st Research Conference of the CEPR Network on Macroeconomic Modelling and Model Comparison 0 / 12 Fiscal

Fiscal Multipliers and Financial Crises Miguel Faria-e-Castro New York University June 20, 2017 1 st Research Conference of the CEPR Network on Macroeconomic Modelling and Model Comparison 0 / 12 Fiscal

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

A Model of Financial Intermediation

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

Financial intermediaries in an estimated DSGE model for the UK

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

On the Merits of Conventional vs Unconventional Fiscal Policy

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Optimal Monetary Policy in a Sudden Stop

... Optimal Monetary Policy in a Sudden Stop with Jorge Roldos (IMF) and Fabio Braggion (Northwestern, Tilburg) 1 Modeling Issues/Tools Small, Open Economy Model Interaction Between Asset Markets and Monetary

... Optimal Monetary Policy in a Sudden Stop with Jorge Roldos (IMF) and Fabio Braggion (Northwestern, Tilburg) 1 Modeling Issues/Tools Small, Open Economy Model Interaction Between Asset Markets and Monetary

Leverage Restrictions in a Business Cycle Model. Lawrence J. Christiano Daisuke Ikeda

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Bank Capital, Agency Costs, and Monetary Policy. Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Risky Mortgages in a DSGE Model

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

Coordinating Monetary and Financial Regulatory Policies

Coordinating Monetary and Financial Regulatory Policies Alejandro Van der Ghote European Central Bank May 2018 The views expressed on this discussion are my own and do not necessarily re ect those of the

Coordinating Monetary and Financial Regulatory Policies Alejandro Van der Ghote European Central Bank May 2018 The views expressed on this discussion are my own and do not necessarily re ect those of the

Financial Factors in Business Cycles

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Interest-rate pegs and central bank asset purchases: Perfect foresight and the reversal puzzle

Interest-rate pegs and central bank asset purchases: Perfect foresight and the reversal puzzle Rafael Gerke Sebastian Giesen Daniel Kienzler Jörn Tenhofen Deutsche Bundesbank Swiss National Bank The views

Interest-rate pegs and central bank asset purchases: Perfect foresight and the reversal puzzle Rafael Gerke Sebastian Giesen Daniel Kienzler Jörn Tenhofen Deutsche Bundesbank Swiss National Bank The views

Inflation Dynamics During the Financial Crisis

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 R. Schoenle 2 J. W. Sim 3 E. Zakrajšek 3 1 Boston University and NBER 2 Brandeis University 3 Federal Reserve Board Theory and Methods in Macroeconomics

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 R. Schoenle 2 J. W. Sim 3 E. Zakrajšek 3 1 Boston University and NBER 2 Brandeis University 3 Federal Reserve Board Theory and Methods in Macroeconomics

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Macro-prudential Policies in a Commodity Exporting Economy

Macro-prudential Policies in a Commodity Exporting Economy Andrés González 1 Franz Hamann 2 Diego Rodríguez 2 1 Department of Economics Universidad de los Andes 2 Gerencia Técnica Banco de la República

Macro-prudential Policies in a Commodity Exporting Economy Andrés González 1 Franz Hamann 2 Diego Rodríguez 2 1 Department of Economics Universidad de los Andes 2 Gerencia Técnica Banco de la República

Estimating Output Gap in the Czech Republic: DSGE Approach

Estimating Output Gap in the Czech Republic: DSGE Approach Pavel Herber 1 and Daniel Němec 2 1 Masaryk University, Faculty of Economics and Administrations Department of Economics Lipová 41a, 602 00 Brno,

Estimating Output Gap in the Czech Republic: DSGE Approach Pavel Herber 1 and Daniel Němec 2 1 Masaryk University, Faculty of Economics and Administrations Department of Economics Lipová 41a, 602 00 Brno,

Monetary and Macroprudential Policies to Manage Capital Flows

Monetary and Macroprudential Policies to Manage Capital Flows Juan Pablo Medina a and Jorge Roldós b a Universidad Adolfo Ibáñez b International Monetary Fund We study interactions between monetary and

Monetary and Macroprudential Policies to Manage Capital Flows Juan Pablo Medina a and Jorge Roldós b a Universidad Adolfo Ibáñez b International Monetary Fund We study interactions between monetary and

Reserve Requirements and Optimal Chinese Stabilization Policy 1

Reserve Requirements and Optimal Chinese Stabilization Policy 1 Chun Chang 1 Zheng Liu 2 Mark M. Spiegel 2 Jingyi Zhang 1 1 Shanghai Jiao Tong University, 2 FRB San Francisco ABFER Conference, Singapore

Reserve Requirements and Optimal Chinese Stabilization Policy 1 Chun Chang 1 Zheng Liu 2 Mark M. Spiegel 2 Jingyi Zhang 1 1 Shanghai Jiao Tong University, 2 FRB San Francisco ABFER Conference, Singapore

State-Dependent Pricing and the Paradox of Flexibility

State-Dependent Pricing and the Paradox of Flexibility Luca Dedola and Anton Nakov ECB and CEPR May 24 Dedola and Nakov (ECB and CEPR) SDP and the Paradox of Flexibility 5/4 / 28 Policy rates in major

State-Dependent Pricing and the Paradox of Flexibility Luca Dedola and Anton Nakov ECB and CEPR May 24 Dedola and Nakov (ECB and CEPR) SDP and the Paradox of Flexibility 5/4 / 28 Policy rates in major

Credit Risk and the Macroeconomy

and the Macroeconomy Evidence From an Estimated Simon Gilchrist 1 Alberto Ortiz 2 Egon Zakrajšek 3 1 Boston University and NBER 2 Oberlin College 3 Federal Reserve Board XXVII Encuentro de Economistas

and the Macroeconomy Evidence From an Estimated Simon Gilchrist 1 Alberto Ortiz 2 Egon Zakrajšek 3 1 Boston University and NBER 2 Oberlin College 3 Federal Reserve Board XXVII Encuentro de Economistas

Lecture 23 The New Keynesian Model Labor Flows and Unemployment. Noah Williams

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Spillovers: The Role of Prudential Regulation and Monetary Policy in Small Open Economies

Spillovers: The Role of Prudential Regulation and Monetary Policy in Small Open Economies Paul Castillo, César Carrera, Marco Ortiz & Hugo Vega Presented by: Marco Ortiz Closing Conference of the BIS CCA

Spillovers: The Role of Prudential Regulation and Monetary Policy in Small Open Economies Paul Castillo, César Carrera, Marco Ortiz & Hugo Vega Presented by: Marco Ortiz Closing Conference of the BIS CCA

The science of monetary policy

Macroeconomic dynamics PhD School of Economics, Lectures 2018/19 The science of monetary policy Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Doctoral School of Economics Sapienza University

Macroeconomic dynamics PhD School of Economics, Lectures 2018/19 The science of monetary policy Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Doctoral School of Economics Sapienza University

Financial Frictions Under Asymmetric Information and Costly State Verification

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Probably Too Little, Certainly Too Late. An Assessment of the Juncker Investment Plan

Probably Too Little, Certainly Too Late. An Assessment of the Juncker Investment Plan Mathilde Le Moigne 1 Francesco Saraceno 2,3 Sébastien Villemot 2 1 École Normale Supérieure 2 OFCE Sciences Po 3 LUISS-SEP

Probably Too Little, Certainly Too Late. An Assessment of the Juncker Investment Plan Mathilde Le Moigne 1 Francesco Saraceno 2,3 Sébastien Villemot 2 1 École Normale Supérieure 2 OFCE Sciences Po 3 LUISS-SEP

The Risky Steady State and the Interest Rate Lower Bound

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

Credit Spreads and the Macroeconomy

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

Macroeconomic Models. with Financial Frictions

Macroeconomic Models with Financial Frictions Jesús Fernández-Villaverde University of Pennsylvania May 31, 2010 Jesús Fernández-Villaverde (PENN) Macro-Finance May 31, 2010 1 / 69 Motivation I Traditional

Macroeconomic Models with Financial Frictions Jesús Fernández-Villaverde University of Pennsylvania May 31, 2010 Jesús Fernández-Villaverde (PENN) Macro-Finance May 31, 2010 1 / 69 Motivation I Traditional

Quantitative Easing and Financial Stability

Quantitative Easing and Financial Stability Michael Woodford Columbia University Nineteenth Annual Conference Central Bank of Chile November 19-20, 2015 Michael Woodford (Columbia) Financial Stability

Quantitative Easing and Financial Stability Michael Woodford Columbia University Nineteenth Annual Conference Central Bank of Chile November 19-20, 2015 Michael Woodford (Columbia) Financial Stability

Macroprudential Policy Implementation in a Heterogeneous Monetary Union

Macroprudential Policy Implementation in a Heterogeneous Monetary Union Margarita Rubio University of Nottingham ECB conference on "Heterogenity in currency areas and macroeconomic policies" - 28-29 November

Macroprudential Policy Implementation in a Heterogeneous Monetary Union Margarita Rubio University of Nottingham ECB conference on "Heterogenity in currency areas and macroeconomic policies" - 28-29 November

The Dire Effects of the Lack of Monetary and Fiscal Coordination 1

The Dire Effects of the Lack of Monetary and Fiscal Coordination 1 Francesco Bianchi and Leonardo Melosi Duke University and FRB of Chicago The views in this paper are solely the responsibility of the

The Dire Effects of the Lack of Monetary and Fiscal Coordination 1 Francesco Bianchi and Leonardo Melosi Duke University and FRB of Chicago The views in this paper are solely the responsibility of the

Simple Analytics of the Government Expenditure Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Unemployment Fluctuations and Nominal GDP Targeting

Unemployment Fluctuations and Nominal GDP Targeting Roberto M. Billi Sveriges Riksbank 3 January 219 Abstract I evaluate the welfare performance of a target for the level of nominal GDP in the context

Unemployment Fluctuations and Nominal GDP Targeting Roberto M. Billi Sveriges Riksbank 3 January 219 Abstract I evaluate the welfare performance of a target for the level of nominal GDP in the context

Microfoundations of DSGE Models: III Lecture

Microfoundations of DSGE Models: III Lecture Barbara Annicchiarico BBLM del Dipartimento del Tesoro 2 Giugno 2. Annicchiarico (Università di Tor Vergata) (Institute) Microfoundations of DSGE Models 2 Giugno

Microfoundations of DSGE Models: III Lecture Barbara Annicchiarico BBLM del Dipartimento del Tesoro 2 Giugno 2. Annicchiarico (Università di Tor Vergata) (Institute) Microfoundations of DSGE Models 2 Giugno

2. Preceded (followed) by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,

by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,") Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Unconventional Monetary Policy

Unconventional Monetary Policy Mark Gertler (based on joint work with Peter Karadi) NYU October 29 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes pre versus post August 27 Post August

Unconventional Monetary Policy Mark Gertler (based on joint work with Peter Karadi) NYU October 29 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes pre versus post August 27 Post August

Debt Covenants and the Macroeconomy: The Interest Coverage Channel

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

Notes for a Model With Banks and Net Worth Constraints

Notes for a Model With Banks and Net Worth Constraints 1 (Revised) Joint work with Roberto Motto and Massimo Rostagno Combines Previous Model with Banking Model of Chari, Christiano, Eichenbaum (JMCB,

Notes for a Model With Banks and Net Worth Constraints 1 (Revised) Joint work with Roberto Motto and Massimo Rostagno Combines Previous Model with Banking Model of Chari, Christiano, Eichenbaum (JMCB,

Monetary Macroeconomics & Central Banking Lecture /

Monetary Macroeconomics & Central Banking Lecture 4 03.05.2013 / 10.05.2013 Outline 1 IS LM with banks 2 Bernanke Blinder (1988): CC LM Model 3 Woodford (2010):IS MP w. Credit Frictions Literature For

Monetary Macroeconomics & Central Banking Lecture 4 03.05.2013 / 10.05.2013 Outline 1 IS LM with banks 2 Bernanke Blinder (1988): CC LM Model 3 Woodford (2010):IS MP w. Credit Frictions Literature For

Overborrowing, Financial Crises and Macro-prudential Policy. Macro Financial Modelling Meeting, Chicago May 2-3, 2013

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Self-fulfilling Recessions at the ZLB

Self-fulfilling Recessions at the ZLB Charles Brendon (Cambridge) Matthias Paustian (Board of Governors) Tony Yates (Birmingham) August 2016 Introduction This paper is about recession dynamics at the ZLB

Self-fulfilling Recessions at the ZLB Charles Brendon (Cambridge) Matthias Paustian (Board of Governors) Tony Yates (Birmingham) August 2016 Introduction This paper is about recession dynamics at the ZLB

On the new Keynesian model

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Consumption Dynamics, Housing Collateral and Stabilisation Policy

Consumption Dynamics, Housing Collateral and Stabilisation Policy A Way Forward for Macro-Prudential Instruments? Effective Macroprudential Instruments - CFCM-MMF-MMPM Conference Jagjit S. Chadha University

Consumption Dynamics, Housing Collateral and Stabilisation Policy A Way Forward for Macro-Prudential Instruments? Effective Macroprudential Instruments - CFCM-MMF-MMPM Conference Jagjit S. Chadha University

Banking Crises and Real Activity: Identifying the Linkages

Banking Crises and Real Activity: Identifying the Linkages Mark Gertler New York University I interpret some key aspects of the recent crisis through the lens of macroeconomic modeling of financial factors.

Banking Crises and Real Activity: Identifying the Linkages Mark Gertler New York University I interpret some key aspects of the recent crisis through the lens of macroeconomic modeling of financial factors.

Spillovers, Capital Flows and Prudential Regulation in Small Open Economies

Spillovers, Capital Flows and Prudential Regulation in Small Open Economies Paul Castillo, César Carrera, Marco Ortiz & Hugo Vega Presented by: Hugo Vega BIS CCA Research Network Conference Incorporating

Spillovers, Capital Flows and Prudential Regulation in Small Open Economies Paul Castillo, César Carrera, Marco Ortiz & Hugo Vega Presented by: Hugo Vega BIS CCA Research Network Conference Incorporating

The Basic New Keynesian Model

Jordi Gali Monetary Policy, inflation, and the business cycle Lian Allub 15/12/2009 In The Classical Monetary economy we have perfect competition and fully flexible prices in all markets. Here there is

Jordi Gali Monetary Policy, inflation, and the business cycle Lian Allub 15/12/2009 In The Classical Monetary economy we have perfect competition and fully flexible prices in all markets. Here there is

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Default Risk and Aggregate Fluctuations in an Economy with Production Heterogeneity

Default Risk and Aggregate Fluctuations in an Economy with Production Heterogeneity Aubhik Khan The Ohio State University Tatsuro Senga The Ohio State University and Bank of Japan Julia K. Thomas The Ohio

Default Risk and Aggregate Fluctuations in an Economy with Production Heterogeneity Aubhik Khan The Ohio State University Tatsuro Senga The Ohio State University and Bank of Japan Julia K. Thomas The Ohio

Alternative theories of the business cycle

Alternative theories of the business cycle Lecture 14, ECON 4310 Tord Krogh October 19, 2012 Tord Krogh () ECON 4310 October 19, 2012 1 / 44 So far So far: Only looked at one business cycle model (the

Alternative theories of the business cycle Lecture 14, ECON 4310 Tord Krogh October 19, 2012 Tord Krogh () ECON 4310 October 19, 2012 1 / 44 So far So far: Only looked at one business cycle model (the

Monetary Policy in a New Keyneisan Model Walsh Chapter 8 (cont)

") Monetary Policy in a New Keyneisan Model Walsh Chapter 8 (cont) 1 New Keynesian Model Demand is an Euler equation x t = E t x t+1 ( ) 1 σ (i t E t π t+1 ) + u t Supply is New Keynesian Phillips Curve π

Monetary Policy in a New Keyneisan Model Walsh Chapter 8 (cont) 1 New Keynesian Model Demand is an Euler equation x t = E t x t+1 ( ) 1 σ (i t E t π t+1 ) + u t Supply is New Keynesian Phillips Curve π

Asset purchase policy at the effective lower bound for interest rates

at the effective lower bound for interest rates Bank of England 12 March 2010 Plan Introduction The model The policy problem Results Summary & conclusions Plan Introduction Motivation Aims and scope The

at the effective lower bound for interest rates Bank of England 12 March 2010 Plan Introduction The model The policy problem Results Summary & conclusions Plan Introduction Motivation Aims and scope The

Multi-Dimensional Monetary Policy

Multi-Dimensional Monetary Policy Michael Woodford Columbia University John Kuszczak Memorial Lecture Bank of Canada Annual Research Conference November 3, 2016 Michael Woodford (Columbia) Multi-Dimensional

Multi-Dimensional Monetary Policy Michael Woodford Columbia University John Kuszczak Memorial Lecture Bank of Canada Annual Research Conference November 3, 2016 Michael Woodford (Columbia) Multi-Dimensional

What is Cyclical in Credit Cycles?

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

The New Keynesian Approach to Monetary Policy Analysis: Lessons and New Directions

The to Monetary Policy Analysis: Lessons and New Directions Jordi Galí CREI and U. Pompeu Fabra ice of Monetary Policy Today" October 4, 2007 The New Keynesian Paradigm: Key Elements Dynamic stochastic

The to Monetary Policy Analysis: Lessons and New Directions Jordi Galí CREI and U. Pompeu Fabra ice of Monetary Policy Today" October 4, 2007 The New Keynesian Paradigm: Key Elements Dynamic stochastic

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Concerted Efforts? Monetary Policy and Macro-Prudential Tools

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Centre for Macroeconomics 2 nd Annual European Central

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Centre for Macroeconomics 2 nd Annual European Central

Inflation in the Great Recession and New Keynesian Models

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

The new Kenesian model

The new Kenesian model Michaª Brzoza-Brzezina Warsaw School of Economics 1 / 4 Flexible vs. sticky prices Central assumption in the (neo)classical economics: Prices (of goods and factor services) are fully

The new Kenesian model Michaª Brzoza-Brzezina Warsaw School of Economics 1 / 4 Flexible vs. sticky prices Central assumption in the (neo)classical economics: Prices (of goods and factor services) are fully

Structural Reforms in a Debt Overhang

in a Debt Overhang Javier Andrés, Óscar Arce and Carlos Thomas 3 9/5/5 - Birkbeck Center for Applied Macroeconomics Universidad de Valencia, Banco de España Banco de España 3 Banco de España 9/5/5 - Birkbeck

in a Debt Overhang Javier Andrés, Óscar Arce and Carlos Thomas 3 9/5/5 - Birkbeck Center for Applied Macroeconomics Universidad de Valencia, Banco de España Banco de España 3 Banco de España 9/5/5 - Birkbeck

Uninsured Unemployment Risk and Optimal Monetary Policy

Uninsured Unemployment Risk and Optimal Monetary Policy Edouard Challe CREST & Ecole Polytechnique ASSA 2018 Strong precautionary motive Low consumption Bad aggregate shock High unemployment Low output

Uninsured Unemployment Risk and Optimal Monetary Policy Edouard Challe CREST & Ecole Polytechnique ASSA 2018 Strong precautionary motive Low consumption Bad aggregate shock High unemployment Low output

... The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno

The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno Background Want to Construct a Dynamic Economic Model Useful for the Analysis of Monetary

The Great Depression and the Friedman-Schwartz Hypothesis Lawrence J. Christiano, Roberto Motto and Massimo Rostagno Background Want to Construct a Dynamic Economic Model Useful for the Analysis of Monetary

Incorporate Financial Frictions into a

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Technology shocks and Monetary Policy: Assessing the Fed s performance

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe