Lecture 23 The New Keynesian Model Labor Flows and Unemployment. Noah Williams

|

|

|

- Alexis McGee

- 5 years ago

- Views:

Transcription

1 Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702

2 Basic New Keynesian Model of Transmission Can be derived from primitives: household consumption decisions, firm pricing decisions. Assumes monopolistic competition, sticky prices. Only labor input, C t = Y t. Unlike old Keynesian literature, assumes rational expectations. When firms set prices, forecast future demand and policy. Households also forecast future conditions when choosing consumption. Basic model has 2 key equations: a Euler equation which gives an IS relation between output and interest rates, and a Phillips curve which results from price setting decisions. Gives a relation between output and inflation. Along with a specification of monetary policy, these determine the evolution of output, inflation, and interest rates.

3 Basic Model Clarida-Gali-Gertler (1999), Woodford (2003). Let π t be inflation, E t π t+1 expected inflation, x t = y t y p t the output gap (deviation of output from potential ), R t the nominal interest rate. First equation relates output gap to real interest rate: x t = φ(r t E t π t+1 ) + E t x t+1 + g t Linearized consumption Euler equation/is curve. Second equation is the New Keynesian Phillips curve relating inflation and real activity: π t = κx t + βe t π t+1 + u t Linearized pricing decisions of firms with staggered price setting.

4 g t and u t are exogenous shocks. Demand (such as government spending) and cost-push (such as wage or markup fluctuations) Assume they re serially correlated: g t = ρ g g t 1 + ɛ g t u t = ρ u u t 1 + ɛ u t Note that timing of Phillips curve is different from previous expectations-augmented (Lucas suprise model): here inflation is fully forward looking. Can close model via an LM curve once we specify money demand. But since we ll analyze policy via setting interest rate R t, this will only pin down the stock of money.

5 Policy Implication of Forward-Looking Models The basic new Keynesian inflation adjustment equation without cost shocks is: π t = κx t + βe t π t+1 We can solve this equation forward to get an expression for inflation: π t = κ β i E t x t+i i=0 Inflation is a function of the present discounted value of current and future output gaps. The absence of a stochastic disturbance implies there is no conflict between a policy designed to maintain inflation at zero and a policy designed to keep the output gap equal to zero. Just set x t+i = 0 for all i; keeps inflation equal to zero.

6 Optimal Policy Thus, the key implication of the basic new Keynesian model is that price stability is the appropriate objective of monetary policy. No policy conflicts. When prices are sticky but wages are flexible, the nominal wage can adjust to ensure labor market equilibrium is maintained in the face of productivity shocks. Optimal policy should then aim to keep the price level stable.

7 Policy Implications of Price Stickiness Models that combine optimizing agents and sticky prices have very strong policy implications. When the price level fluctuates, and not all firms are able to adjust, price dispersion results. This causes the relative prices of the different goods to vary. If the price level rises, for example, two things happen. 1 The relative price of firms who have not set their prices for a while falls. They experience in increase in demand and raise output, while firms who have just reset their prices reduce output. This production dispersion is inefficient. 2 Consumers increase their consumption of the goods whose relative price has fallen and reduce consumption of those goods whose relative price has risen. This dispersion in consumption reduces welfare.

8 Optimal Policy The solution is to prevent price dispersion by stabilizing the price level. What is critical for this result is that nominal wages are assumed to be completely flexible. But the same argument would apply if wages are sticky and prices flexible. With sticky wages and flexible prices, monetary policy should stabilizes the nominal wage.

9 Woodford versus Friedman The basic new Keynesian model suggests price stability (i.e., zero inflation) is optimal. Zero inflation eliminates inefficient price dispersion. Friedman rule: zero nominal rate of interest is optimal. Zero nominal rate eliminates inefficiency in money holdings. Optimal inflation is negative (deflation) at rate equal to real rate of interest. Khan, King, and Wolman (2000) analysis model with both distortions. The conclude optimal inflation is closer to zero than to the Friedman rule.

10 Cost Shocks Now assume π t = κx t + βe t π t+1 + u t where u t represents an inflation or cost shock, which is serially correlated: Then u t = ρ u u t 1 + ɛ u t π t = κ β i E t x t+i + β i E t u t+i i=0 i=0 Cannot keep both x and π equal to zero. Trade-offs must be made.

11 Objective of Policy Policy objective in general is to maximize welfare of agents. In this model, can derive approximation of welfare giving loss function: L t = 1 ( ) ωxt 2 + π 2 t 2 Penalizes deviations of output relative potential, deviation of inflation from target (zero): Price stability and Full Employment goals. In deriving this expression, weight on output ω can be related to underlying parameters. If there are distortions in the economy (such as monopoly power), optimal level of output gap is positive so loss is: L t = 1 2 ( ) ω(x t x) 2 + π 2 t

12 Policy Problem Suppose central bank targets positive output gap x > 0. Chooses interest rate policy each period to minimize loss, taking as given private expectations. Easiest here to suppose central bank directly controls inflation and output gap, then use IS to back out optimal interest rate choice. Suppose also β = 1. Represent the central bank s problem as a Lagrangian: L = 1 2 ( ) λ(x t x) 2 + π 2 t + µ (κx t + βe t π t+1 + u t π t ) The first order conditions are: λ(x t x) + µκ = 0 and π t = µ or x t = κ λ π t + x

13 x t = κ λ π t + x Substitute back into Phillips: π t = κx t + βe t π t+1 + u t (1 + κ 2 /λ)π t = κ x + βe t π t+1 + u t Guess π t = k 0 + k 1 u t. Then E t π t+1 = k 0 + k 1 E t u t+1 = k 0 + k 1 ρu t. Substitute and use β = 1: λ π t = κ 2 + ω(1 ρ) u t + λ κ x Then from optimality get: x t = κ λ π t + x = κ κ 2 + λ(1 ρ) u t

14 Inflation Bias and Time Consistency Note Eπ t = λ κ x but Ex t = 0. Target gap x only affects mean inflation rate. If β < 1 then targeting x > 0 will result in x > Ex t > 0.) Government tries to push output above potential, in equilibrium only leads to higher inflation. This is just as in the earlier analysis, but more direct/explicit. Policymakers have an incentive to announce they will be tough on inflation to affect people s expectations, then actually to pursue loose policy. In equilibrium, people will come to expect this. With rational expectations (as we ve used), this only leads to higher inflation.

15 Optimal Discretionary Policy With x = 0 (for any β): π t = λ κ 2 + λ(1 βρ) u t, x t = κ κ 2 + λ(1 βρ) u t Can then get optimal interest rate response from IS: x t = φ(r t E t π t+1 ) + E t x t+1 + g t R t = E t π t+1 + (1/φ) (E t x t+1 x t + g t ) = γe t π t+1 + (1/φ)g t, where γ > 1. (i) Cost push shocks u t imply inflation/ouput tradeoff. (ii) If expected inflation rises, nominal interest rates should rise by more (γ > 1) so real rates increase. (iii) Policy should offset demand shocks g t, accommodate movements in potential output (say productivity shocks).

16 Commitment When forward-looking expectations play a role, discretion leads to a stabilization bias even though there is no average inflation bias. Under optimal commitment, central bank at time t chooses both current and expected future values of inflation and the output gap. Minimize [ ΩE t β i π 2 t+i + λ (x t+i x ) 2] i=0 subject to π t = βe t π t+1 + κx t + u t. Notice the IS imposes no constraint use it to solve for i t once optimal π t and x t have been determined.

17 Optimal Commitment The central bank s problem is to pick π t+i and x t+i to minimize E t i=0 [ ] β i π 2 t+i + λxt+i 2 + ψ t+i (π t+i βπ t+i+1 κx t+i u t+i ). The first order conditions can be written as π t + ψ t = 0 (1) E t ( πt+i + ψ t+i ψ t+i 1 ) = 0 i 1 (2) E t ( λxt+i κψ t+i ) = 0 i 0. (3) Dynamic inconsistency at time t, the central bank sets π t = ψ t and promises to set π t+1 = ( E t ψ t+1 ψ t ). When t + 1 arrives, a central bank that reoptimizes will again obtains π t+1 = ψ t+1 the first order condition (1) updated to t + 1 will reappear.

18 Discretion vs Commitment Responses of to a 1% inflation shock under the optimal commitment (solid) and discretion (dashed) policies.

19 Improved trade-off under commitment The difference in the stabilization response under commitment and discretion is the stabilization bias due to discretion. Consider a positive inflation shock, u > 0. A given change in current inflation can be achieved with a smaller fall in x if expected future inflation can be reduced: π t = βe t π t+1 + κx t + u t Requires a commitment to future deflation. By keeping output below potential (a negative output gap) for several periods into the future after a positive cost shock, the central bank is able to lower expectations of future inflation. A fall in E t π t+1 at the time of the positive inflation shock improves the trade-off between inflation and output gap stabilization faced by the central bank.

20 Gains from Commitment

21 Contemporary New Keynesian Models To capture the dynamics and persistence in the data, modern NK models add many real and nominal frictions Smets and Wouters (2003) model has the following features: - Sticky prices - Habit formation - Sticky wages - Variable capacity utilization - Price & wage indexation - Investment adjustment costs There are 10 structural shocks: - Productivity - Goods markup - Labor supply - Labor markup - Preference - Equity premium - Adjustment cost - Policy instrument - Government spending - Policy objective Later models add explicit financial sector

22 Estimation and Use Most of the literature uses Bayesian methods. Simulation based approach (MCMC) which allows to calculate posterior distribution of parameters. Use observations on (Y t, C t, I t, π t, w t, N t, R t ). Can be difficult to estimate: 7 time series, 32 parameters 16 structural parameters, 10 shock standard deviations, 6 autocorrelations. Standard of fit is a vector autorgregression (VAR): atheoretical, empirical model. Most modern NK models are comparable in fit. But unlike VAR, NK model can be used for policy analysis. Models of this type used by most central banks and policy institutions: Fed, ECB, Bank of England, IMF, etc.

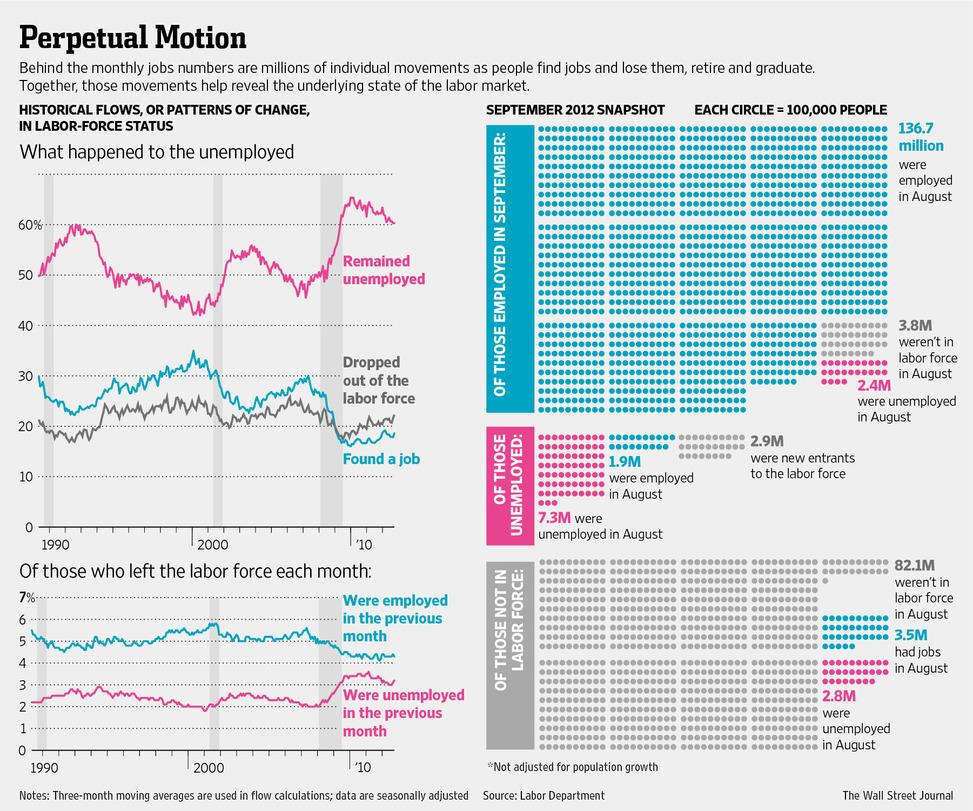

23 Basic Facts About the Labor Market US Labor Force in Sept. 2012: 142 million people US working age population in 2012: million people Labor force participation rate of about 63.6%. Employment-population ratio of 58.7% Between 1967 and 1993 the average job loss rate was 2.7% per month, average job finding rate was 43%, and average unemployment rate 6.2%. In September 2012 job loss rate was 1.3% per month (with 2.5% going out of labor force), finding rate was 19%, and unemployment rate was 9.1%. Large differences in employment, unemployment, and their evolution in US and Europe.

24 Employment/Population and Participation Rates 67.5 Civilian Labor Force Participation Rate Civilian Employment-Population Ratio (Percent) research.stlouisfed.org

25 Separations and Hires Total Separations: Total Nonfarm (left) Quits: Total Nonfarm (left) Civilian Unemployment Rate (right) Hires: Total Nonfarm (right) Layoffs and Discharges: Total Nonfarm (right) (Rate) (Percent), (Rate) research.stlouisfed.org

26

27

28

29

30

31

32 Length of Unemployment Spells Unemployment Spell 8/89 10/92 10/06 3/11 < 5 weeks 48% 35% 38% 18% 5-14 weeks 31% 28% 31% 22% weeks 11% 14% 14% 15% > 26 weeks 9% 23% 16% 46% Other countries: in Germany, France or the Netherlands about two thirds of all unemployed workers in 1989 were unemployed for longer than six months.

33

34

35 Median Duration of Unemployment 30 Median Duration of Unemployment (Weeks) Source: US. Bureau of Labor Statistics research.stlouisfed.org

36 Distribution of Unemployment Duration 70 Of Total Unemployed, Percent Unemployed Less than 5 Weeks Of Total Unemployed, Percent Unemployed 5 to 14 Weeks Of Total Unemployed, Percent Unemployed 15 to 26 Weeks Of Total Unemployed, Percent Unemployed 27 Weeks and over (Percent) research.stlouisfed.org

Monetary Policy in a New Keyneisan Model Walsh Chapter 8 (cont)

") Monetary Policy in a New Keyneisan Model Walsh Chapter 8 (cont) 1 New Keynesian Model Demand is an Euler equation x t = E t x t+1 ( ) 1 σ (i t E t π t+1 ) + u t Supply is New Keynesian Phillips Curve π

Monetary Policy in a New Keyneisan Model Walsh Chapter 8 (cont) 1 New Keynesian Model Demand is an Euler equation x t = E t x t+1 ( ) 1 σ (i t E t π t+1 ) + u t Supply is New Keynesian Phillips Curve π

ECON 815. A Basic New Keynesian Model II

ECON 815 A Basic New Keynesian Model II Winter 2015 Queen s University ECON 815 1 Unemployment vs. Inflation 12 10 Unemployment 8 6 4 2 0 1 1.5 2 2.5 3 3.5 4 4.5 5 Core Inflation 14 12 10 Unemployment

ECON 815 A Basic New Keynesian Model II Winter 2015 Queen s University ECON 815 1 Unemployment vs. Inflation 12 10 Unemployment 8 6 4 2 0 1 1.5 2 2.5 3 3.5 4 4.5 5 Core Inflation 14 12 10 Unemployment

The New Keynesian Model

The New Keynesian Model Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) New Keynesian model 1 / 37 Research strategy policy as systematic and predictable...the central bank s stabilization

The New Keynesian Model Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) New Keynesian model 1 / 37 Research strategy policy as systematic and predictable...the central bank s stabilization

MA Advanced Macroeconomics: 11. The Smets-Wouters Model

MA Advanced Macroeconomics: 11. The Smets-Wouters Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) The Smets-Wouters Model Spring 2016 1 / 23 A Popular DSGE Model Now we will discuss

MA Advanced Macroeconomics: 11. The Smets-Wouters Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) The Smets-Wouters Model Spring 2016 1 / 23 A Popular DSGE Model Now we will discuss

The science of monetary policy

Macroeconomic dynamics PhD School of Economics, Lectures 2018/19 The science of monetary policy Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Doctoral School of Economics Sapienza University

Macroeconomic dynamics PhD School of Economics, Lectures 2018/19 The science of monetary policy Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Doctoral School of Economics Sapienza University

Discussion of Limitations on the Effectiveness of Forward Guidance at the Zero Lower Bound

Discussion of Limitations on the Effectiveness of Forward Guidance at the Zero Lower Bound Robert G. King Boston University and NBER 1. Introduction What should the monetary authority do when prices are

Discussion of Limitations on the Effectiveness of Forward Guidance at the Zero Lower Bound Robert G. King Boston University and NBER 1. Introduction What should the monetary authority do when prices are

Technology shocks and Monetary Policy: Assessing the Fed s performance

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Science of Monetary Policy: CGG (1999)

") Science of Monetary Policy: CGG (1999) Satya P. Das @ NIPFP Satya P. Das (@ NIPFP) Science of Monetary Policy: CGG (1999) 1 / 14 1 Model Structure 2 Time Inconsistency and Commitment 3 Discretion Satya

Science of Monetary Policy: CGG (1999) Satya P. Das @ NIPFP Satya P. Das (@ NIPFP) Science of Monetary Policy: CGG (1999) 1 / 14 1 Model Structure 2 Time Inconsistency and Commitment 3 Discretion Satya

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

TFP Persistence and Monetary Policy. NBS, April 27, / 44

TFP Persistence and Monetary Policy Roberto Pancrazi Toulouse School of Economics Marija Vukotić Banque de France NBS, April 27, 2012 NBS, April 27, 2012 1 / 44 Motivation 1 Well Known Facts about the

TFP Persistence and Monetary Policy Roberto Pancrazi Toulouse School of Economics Marija Vukotić Banque de France NBS, April 27, 2012 NBS, April 27, 2012 1 / 44 Motivation 1 Well Known Facts about the

State-Dependent Pricing and the Paradox of Flexibility

State-Dependent Pricing and the Paradox of Flexibility Luca Dedola and Anton Nakov ECB and CEPR May 24 Dedola and Nakov (ECB and CEPR) SDP and the Paradox of Flexibility 5/4 / 28 Policy rates in major

State-Dependent Pricing and the Paradox of Flexibility Luca Dedola and Anton Nakov ECB and CEPR May 24 Dedola and Nakov (ECB and CEPR) SDP and the Paradox of Flexibility 5/4 / 28 Policy rates in major

On the new Keynesian model

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Unemployment Persistence, Inflation and Monetary Policy in A Dynamic Stochastic Model of the Phillips Curve

Unemployment Persistence, Inflation and Monetary Policy in A Dynamic Stochastic Model of the Phillips Curve by George Alogoskoufis* March 2016 Abstract This paper puts forward an alternative new Keynesian

Unemployment Persistence, Inflation and Monetary Policy in A Dynamic Stochastic Model of the Phillips Curve by George Alogoskoufis* March 2016 Abstract This paper puts forward an alternative new Keynesian

The Zero Lower Bound

The Zero Lower Bound Eric Sims University of Notre Dame Spring 4 Introduction In the standard New Keynesian model, monetary policy is often described by an interest rate rule (e.g. a Taylor rule) that

The Zero Lower Bound Eric Sims University of Notre Dame Spring 4 Introduction In the standard New Keynesian model, monetary policy is often described by an interest rate rule (e.g. a Taylor rule) that

Credit Frictions and Optimal Monetary Policy

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Concerted Efforts? Monetary Policy and Macro-Prudential Tools

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

Unemployment Fluctuations and Nominal GDP Targeting

Unemployment Fluctuations and Nominal GDP Targeting Roberto M. Billi Sveriges Riksbank 3 January 219 Abstract I evaluate the welfare performance of a target for the level of nominal GDP in the context

Unemployment Fluctuations and Nominal GDP Targeting Roberto M. Billi Sveriges Riksbank 3 January 219 Abstract I evaluate the welfare performance of a target for the level of nominal GDP in the context

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

Credit Frictions and Optimal Monetary Policy. Vasco Curdia (FRB New York) Michael Woodford (Columbia University)

Michael Woodford (Columbia University)") MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

Is the New Keynesian Phillips Curve Flat?

Is the New Keynesian Phillips Curve Flat? Keith Kuester Federal Reserve Bank of Philadelphia Gernot J. Müller University of Bonn Sarah Stölting European University Institute, Florence January 14, 2009

Is the New Keynesian Phillips Curve Flat? Keith Kuester Federal Reserve Bank of Philadelphia Gernot J. Müller University of Bonn Sarah Stölting European University Institute, Florence January 14, 2009

Was The New Deal Contractionary? Appendix C:Proofs of Propositions (not intended for publication)

") Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

The Basic New Keynesian Model

Jordi Gali Monetary Policy, inflation, and the business cycle Lian Allub 15/12/2009 In The Classical Monetary economy we have perfect competition and fully flexible prices in all markets. Here there is

Jordi Gali Monetary Policy, inflation, and the business cycle Lian Allub 15/12/2009 In The Classical Monetary economy we have perfect competition and fully flexible prices in all markets. Here there is

Monetary Economics Final Exam

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

Sharing the Burden: Monetary and Fiscal Responses to a World Liquidity Trap David Cook and Michael B. Devereux

Sharing the Burden: Monetary and Fiscal Responses to a World Liquidity Trap David Cook and Michael B. Devereux Online Appendix: Non-cooperative Loss Function Section 7 of the text reports the results for

Sharing the Burden: Monetary and Fiscal Responses to a World Liquidity Trap David Cook and Michael B. Devereux Online Appendix: Non-cooperative Loss Function Section 7 of the text reports the results for

NBER WORKING PAPER SERIES OPTIMAL MONETARY STABILIZATION POLICY. Michael Woodford. Working Paper

NBER WORKING PAPER SERIES OPTIMAL MONETARY STABILIZATION POLICY Michael Woodford Working Paper 16095 http://www.nber.org/papers/w16095 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES OPTIMAL MONETARY STABILIZATION POLICY Michael Woodford Working Paper 16095 http://www.nber.org/papers/w16095 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

Notes on Estimating the Closed Form of the Hybrid New Phillips Curve

Notes on Estimating the Closed Form of the Hybrid New Phillips Curve Jordi Galí, Mark Gertler and J. David López-Salido Preliminary draft, June 2001 Abstract Galí and Gertler (1999) developed a hybrid

Notes on Estimating the Closed Form of the Hybrid New Phillips Curve Jordi Galí, Mark Gertler and J. David López-Salido Preliminary draft, June 2001 Abstract Galí and Gertler (1999) developed a hybrid

Output Gaps and Robust Monetary Policy Rules

Output Gaps and Robust Monetary Policy Rules Roberto M. Billi Sveriges Riksbank Conference on Monetary Policy Challenges from a Small Country Perspective, National Bank of Slovakia Bratislava, 23-24 November

Output Gaps and Robust Monetary Policy Rules Roberto M. Billi Sveriges Riksbank Conference on Monetary Policy Challenges from a Small Country Perspective, National Bank of Slovakia Bratislava, 23-24 November

Microeconomic Foundations of Incomplete Price Adjustment

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Lecture 23 Monetary Policy. Noah Williams

Lecture 23 Monetary Policy Noah Williams University of Wisconsin - Madison Economics 702 Fed Policy Instrument Main instrument of conventional policy is the Federal Funds rate. An extremely short-term

Lecture 23 Monetary Policy Noah Williams University of Wisconsin - Madison Economics 702 Fed Policy Instrument Main instrument of conventional policy is the Federal Funds rate. An extremely short-term

Money in a Neoclassical Framework

Money in a Neoclassical Framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 21 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why

Money in a Neoclassical Framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 21 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why

Dual Wage Rigidities: Theory and Some Evidence

MPRA Munich Personal RePEc Archive Dual Wage Rigidities: Theory and Some Evidence Insu Kim University of California, Riverside October 29 Online at http://mpra.ub.uni-muenchen.de/18345/ MPRA Paper No.

MPRA Munich Personal RePEc Archive Dual Wage Rigidities: Theory and Some Evidence Insu Kim University of California, Riverside October 29 Online at http://mpra.ub.uni-muenchen.de/18345/ MPRA Paper No.

The Optimal Perception of Inflation Persistence is Zero

The Optimal Perception of Inflation Persistence is Zero Kai Leitemo The Norwegian School of Management (BI) and Bank of Finland March 2006 Abstract This paper shows that in an economy with inflation persistence,

The Optimal Perception of Inflation Persistence is Zero Kai Leitemo The Norwegian School of Management (BI) and Bank of Finland March 2006 Abstract This paper shows that in an economy with inflation persistence,

Gali Chapter 6 Sticky wages and prices

Gali Chapter 6 Sticky wages and prices Up till now: o Wages taken as given by households and firms o Wages flexible so as to clear labor market o Marginal product of labor = disutility of labor (i.e. employment

Gali Chapter 6 Sticky wages and prices Up till now: o Wages taken as given by households and firms o Wages flexible so as to clear labor market o Marginal product of labor = disutility of labor (i.e. employment

Lecture 24 Unemployment. Noah Williams

Lecture 24 Unemployment Noah Williams University of Wisconsin - Madison Economics 702 Basic Facts About the Labor Market US Labor Force in March 2018: 161.8 million people US working age population on

Lecture 24 Unemployment Noah Williams University of Wisconsin - Madison Economics 702 Basic Facts About the Labor Market US Labor Force in March 2018: 161.8 million people US working age population on

Monetary Theory and Policy. Fourth Edition. Carl E. Walsh. The MIT Press Cambridge, Massachusetts London, England

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Money and monetary policy in the Eurozone: an empirical analysis during crises

Money and monetary policy in the Eurozone: an empirical analysis during crises Money Macro and Finance Research Group 46 th Annual Conference Jonathan Benchimol 1 and André Fourçans 2 This presentation

Money and monetary policy in the Eurozone: an empirical analysis during crises Money Macro and Finance Research Group 46 th Annual Conference Jonathan Benchimol 1 and André Fourçans 2 This presentation

Money in an RBC framework

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Shocks, frictions and monetary policy Frank Smets

Shocks, frictions and monetary policy Frank Smets OECD Workshop Paris, 14 June 2007 Outline Two results from the Inflation Persistence Network (IPN) and their monetary policy implications Based on Altissimo,

Shocks, frictions and monetary policy Frank Smets OECD Workshop Paris, 14 June 2007 Outline Two results from the Inflation Persistence Network (IPN) and their monetary policy implications Based on Altissimo,

Inflation s Role in Optimal Monetary-Fiscal Policy

Inflation s Role in Optimal Monetary-Fiscal Policy Eric M. Leeper & Xuan Zhou Indiana University 5 August 2013 KDI Journal of Economic Policy Conference Policy Institution Arrangements Advanced economies

Inflation s Role in Optimal Monetary-Fiscal Policy Eric M. Leeper & Xuan Zhou Indiana University 5 August 2013 KDI Journal of Economic Policy Conference Policy Institution Arrangements Advanced economies

Principles of Banking (III): Macroeconomics of Banking (1) Introduction

: Macroeconomics of Banking (1) Introduction") Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Simple Analytics of the Government Expenditure Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Simple Analytics of the Government Expenditure Multiplier Michael Woodford Columbia University New Approaches to Fiscal Policy FRB Atlanta, January 8-9, 2010 Woodford (Columbia) Analytics of Multiplier

Nobel Symposium Money and Banking

Nobel Symposium Money and Banking https://www.houseoffinance.se/nobel-symposium May 26-28, 2018 Clarion Hotel Sign, Stockholm Money and Banking: Some DSGE Challenges Nobel Symposium on Money and Banking

Nobel Symposium Money and Banking https://www.houseoffinance.se/nobel-symposium May 26-28, 2018 Clarion Hotel Sign, Stockholm Money and Banking: Some DSGE Challenges Nobel Symposium on Money and Banking

Macroeconomics. Basic New Keynesian Model. Nicola Viegi. April 29, 2014

Macroeconomics Basic New Keynesian Model Nicola Viegi April 29, 2014 The Problem I Short run E ects of Monetary Policy Shocks I I I persistent e ects on real variables slow adjustment of aggregate price

Macroeconomics Basic New Keynesian Model Nicola Viegi April 29, 2014 The Problem I Short run E ects of Monetary Policy Shocks I I I persistent e ects on real variables slow adjustment of aggregate price

Chapter 22. Modern Business Cycle Theory

Chapter 22 Modern Business Cycle Theory Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models

Chapter 22 Modern Business Cycle Theory Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models

EC3115 Monetary Economics

EC3115 :: L.12 : Time inconsistency and inflation bias Almaty, KZ :: 20 January 2016 EC3115 Monetary Economics Lecture 12: Time inconsistency and inflation bias Anuar D. Ushbayev International School of

EC3115 :: L.12 : Time inconsistency and inflation bias Almaty, KZ :: 20 January 2016 EC3115 Monetary Economics Lecture 12: Time inconsistency and inflation bias Anuar D. Ushbayev International School of

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program. Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

Satya P. Das NIPFP) Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18

Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18") Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model Satya P. Das @ NIPFP Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18 1 CGG (2001) 2 CGG (2002)

Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model Satya P. Das @ NIPFP Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18 1 CGG (2001) 2 CGG (2002)

Comment. The New Keynesian Model and Excess Inflation Volatility

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Macro II. John Hassler. Spring John Hassler () New Keynesian Model:1 04/17 1 / 10

New Keynesian Model:1 04/17 1 / 10") Macro II John Hassler Spring 27 John Hassler () New Keynesian Model: 4/7 / New Keynesian Model The RBC model worked (perhaps surprisingly) well. But there are problems in generating enough variation in

Macro II John Hassler Spring 27 John Hassler () New Keynesian Model: 4/7 / New Keynesian Model The RBC model worked (perhaps surprisingly) well. But there are problems in generating enough variation in

Central bank losses and monetary policy rules: a DSGE investigation

Central bank losses and monetary policy rules: a DSGE investigation Western Economic Association International Keio University, Tokyo, 21-24 March 219. Jonathan Benchimol 1 and André Fourçans 2 This presentation

Central bank losses and monetary policy rules: a DSGE investigation Western Economic Association International Keio University, Tokyo, 21-24 March 219. Jonathan Benchimol 1 and André Fourçans 2 This presentation

Risk shocks and monetary policy in the new normal

Risk shocks and monetary policy in the new normal Martin Seneca Bank of England Workshop of ESCB Research Cluster on Monetary Economics Banco de España 9 October 17 Views expressed are solely those of

Risk shocks and monetary policy in the new normal Martin Seneca Bank of England Workshop of ESCB Research Cluster on Monetary Economics Banco de España 9 October 17 Views expressed are solely those of

Phillips Curve Instability and Optimal Monetary Policy

issn 1936-5330 Phillips Curve Instability and Optimal Monetary Policy Troy Davig* July 25, 2007 RWP 07-04 Abstract: This paper assesses the implications for optimal discretionary monetary policy if the

issn 1936-5330 Phillips Curve Instability and Optimal Monetary Policy Troy Davig* July 25, 2007 RWP 07-04 Abstract: This paper assesses the implications for optimal discretionary monetary policy if the

Dynamic Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Monetary policy regime formalization: instrumental rules

Monetary policy regime formalization: instrumental rules PhD program in economics 2009/10 University of Rome La Sapienza Course in monetary policy (with G. Ciccarone) University of Teramo The monetary

Monetary policy regime formalization: instrumental rules PhD program in economics 2009/10 University of Rome La Sapienza Course in monetary policy (with G. Ciccarone) University of Teramo The monetary

Optimality of Inflation and Nominal Output Targeting

Optimality of Inflation and Nominal Output Targeting Julio Garín Department of Economics University of Georgia Robert Lester Department of Economics University of Notre Dame First Draft: January 7, 15

Optimality of Inflation and Nominal Output Targeting Julio Garín Department of Economics University of Georgia Robert Lester Department of Economics University of Notre Dame First Draft: January 7, 15

Inflation in the Great Recession and New Keynesian Models

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

1 Explaining Labor Market Volatility

Christiano Economics 416 Advanced Macroeconomics Take home midterm exam. 1 Explaining Labor Market Volatility The purpose of this question is to explore a labor market puzzle that has bedeviled business

Christiano Economics 416 Advanced Macroeconomics Take home midterm exam. 1 Explaining Labor Market Volatility The purpose of this question is to explore a labor market puzzle that has bedeviled business

Macroeconomics 2. Lecture 5 - Money February. Sciences Po

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

New Keynesian Model. Prof. Eric Sims. Fall University of Notre Dame. Sims (ND) New Keynesian Model Fall / 20

New Keynesian Model Fall / 20") New Keynesian Model Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) New Keynesian Model Fall 2012 1 / 20 New Keynesian Economics New Keynesian (NK) model: leading alternative to RBC model

New Keynesian Model Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) New Keynesian Model Fall 2012 1 / 20 New Keynesian Economics New Keynesian (NK) model: leading alternative to RBC model

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg *

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

Involuntary (Unlucky) Unemployment and the Business Cycle. Lawrence Christiano Mathias Trabandt Karl Walentin

Unemployment and the Business Cycle. Lawrence Christiano Mathias Trabandt Karl Walentin") Involuntary (Unlucky) Unemployment and the Business Cycle Lawrence Christiano Mathias Trabandt Karl Walentin Background New Keynesian (NK) models receive lots of attention ti in central lbanks. People

Involuntary (Unlucky) Unemployment and the Business Cycle Lawrence Christiano Mathias Trabandt Karl Walentin Background New Keynesian (NK) models receive lots of attention ti in central lbanks. People

Estimating Output Gap in the Czech Republic: DSGE Approach

Estimating Output Gap in the Czech Republic: DSGE Approach Pavel Herber 1 and Daniel Němec 2 1 Masaryk University, Faculty of Economics and Administrations Department of Economics Lipová 41a, 602 00 Brno,

Estimating Output Gap in the Czech Republic: DSGE Approach Pavel Herber 1 and Daniel Němec 2 1 Masaryk University, Faculty of Economics and Administrations Department of Economics Lipová 41a, 602 00 Brno,

Inflation Target Uncertainty and Monetary Policy

Inflation Target Uncertainty and Monetary Policy Job Market Paper Yevgeniy Teryoshin Stanford University http://www.stanford.edu/~yteryosh This version: January 4, 208 Latest version: http://www.stanford.edu/~yteryosh/yevgeniy_teryoshin_jmp.pdf

Inflation Target Uncertainty and Monetary Policy Job Market Paper Yevgeniy Teryoshin Stanford University http://www.stanford.edu/~yteryosh This version: January 4, 208 Latest version: http://www.stanford.edu/~yteryosh/yevgeniy_teryoshin_jmp.pdf

Monetary policy and the asset risk-taking channel

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

The Impact of Model Periodicity on Inflation Persistence in Sticky Price and Sticky Information Models

The Impact of Model Periodicity on Inflation Persistence in Sticky Price and Sticky Information Models By Mohamed Safouane Ben Aïssa CEDERS & GREQAM, Université de la Méditerranée & Université Paris X-anterre

The Impact of Model Periodicity on Inflation Persistence in Sticky Price and Sticky Information Models By Mohamed Safouane Ben Aïssa CEDERS & GREQAM, Université de la Méditerranée & Université Paris X-anterre

Advanced Topics in Monetary Economics II 1

Advanced Topics in Monetary Economics II 1 Carl E. Walsh UC Santa Cruz August 18-22, 2014 1 c Carl E. Walsh, 2014. Carl E. Walsh (UC Santa Cruz) Gerzensee Study Center August 18-22, 2014 1 / 38 Uncertainty

Advanced Topics in Monetary Economics II 1 Carl E. Walsh UC Santa Cruz August 18-22, 2014 1 c Carl E. Walsh, 2014. Carl E. Walsh (UC Santa Cruz) Gerzensee Study Center August 18-22, 2014 1 / 38 Uncertainty

Money and monetary policy in Israel during the last decade

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

The New Keynesian Approach to Monetary Policy Analysis: Lessons and New Directions

The to Monetary Policy Analysis: Lessons and New Directions Jordi Galí CREI and U. Pompeu Fabra ice of Monetary Policy Today" October 4, 2007 The New Keynesian Paradigm: Key Elements Dynamic stochastic

The to Monetary Policy Analysis: Lessons and New Directions Jordi Galí CREI and U. Pompeu Fabra ice of Monetary Policy Today" October 4, 2007 The New Keynesian Paradigm: Key Elements Dynamic stochastic

Comment on The Central Bank Balance Sheet as a Commitment Device By Gauti Eggertsson and Kevin Proulx

Comment on The Central Bank Balance Sheet as a Commitment Device By Gauti Eggertsson and Kevin Proulx Luca Dedola (ECB and CEPR) Banco Central de Chile XIX Annual Conference, 19-20 November 2015 Disclaimer:

Comment on The Central Bank Balance Sheet as a Commitment Device By Gauti Eggertsson and Kevin Proulx Luca Dedola (ECB and CEPR) Banco Central de Chile XIX Annual Conference, 19-20 November 2015 Disclaimer:

Conditional versus Unconditional Utility as Welfare Criterion: Two Examples

Conditional versus Unconditional Utility as Welfare Criterion: Two Examples Jinill Kim, Korea University Sunghyun Kim, Sungkyunkwan University March 015 Abstract This paper provides two illustrative examples

Conditional versus Unconditional Utility as Welfare Criterion: Two Examples Jinill Kim, Korea University Sunghyun Kim, Sungkyunkwan University March 015 Abstract This paper provides two illustrative examples

Monetary Policy Trade-offs in the Open Economy

Monetary Policy Trade-offs in the Open Economy Carl E. Walsh 1 This draft: November 1999 1 University of California, Santa Cruz and Federal Reserve Bank of San Francisco. Any opinions expressed are those

Monetary Policy Trade-offs in the Open Economy Carl E. Walsh 1 This draft: November 1999 1 University of California, Santa Cruz and Federal Reserve Bank of San Francisco. Any opinions expressed are those

Optimal Monetary Policy in the new Keynesian model. The two equations for the AD curve and the Phillips curve are

Economics 05 K. Kletzer Spring 05 Optimal Monetary Policy in the new Keynesian model The two equations for the AD curve and the Phillips curve are y t E t y t+ σ (i t E t π t+ δ)+g t (AD) and π t E t π

Economics 05 K. Kletzer Spring 05 Optimal Monetary Policy in the new Keynesian model The two equations for the AD curve and the Phillips curve are y t E t y t+ σ (i t E t π t+ δ)+g t (AD) and π t E t π

Endogenous Money or Sticky Wages: A Bayesian Approach

Endogenous Money or Sticky Wages: A Bayesian Approach Guangling Dave Liu 1 Working Paper Number 17 1 Contact Details: Department of Economics, University of Stellenbosch, Stellenbosch, 762, South Africa.

Endogenous Money or Sticky Wages: A Bayesian Approach Guangling Dave Liu 1 Working Paper Number 17 1 Contact Details: Department of Economics, University of Stellenbosch, Stellenbosch, 762, South Africa.

Optimal Monetary Policy Rule under the Non-Negativity Constraint on Nominal Interest Rates

Bank of Japan Working Paper Series Optimal Monetary Policy Rule under the Non-Negativity Constraint on Nominal Interest Rates Tomohiro Sugo * sugo@troi.cc.rochester.edu Yuki Teranishi ** yuuki.teranishi

Bank of Japan Working Paper Series Optimal Monetary Policy Rule under the Non-Negativity Constraint on Nominal Interest Rates Tomohiro Sugo * sugo@troi.cc.rochester.edu Yuki Teranishi ** yuuki.teranishi

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Real Business Cycle Model

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Central Bankers Preferences and Attitudes Towards Uncertainty: Identification by Means of Asset Prices

Central Bankers Preferences and Attitudes Towards Uncertainty: Identification by Means of Asset Prices Anna Orlik February 1, 2018 Abstract Can we identify preferences of a central bank and her attitude

Central Bankers Preferences and Attitudes Towards Uncertainty: Identification by Means of Asset Prices Anna Orlik February 1, 2018 Abstract Can we identify preferences of a central bank and her attitude

The Role of Firm-Level Productivity Growth for the Optimal Rate of Inflation

The Role of Firm-Level Productivity Growth for the Optimal Rate of Inflation Henning Weber Kiel Institute for the World Economy Seminar at the Economic Institute of the National Bank of Poland November

The Role of Firm-Level Productivity Growth for the Optimal Rate of Inflation Henning Weber Kiel Institute for the World Economy Seminar at the Economic Institute of the National Bank of Poland November

Monetary Policy and Resource Mobility

Monetary Policy and Resource Mobility 2th Anniversary of the Bank of Finland Carl E. Walsh University of California, Santa Cruz May 5-6, 211 C. E. Walsh (UCSC) Bank of Finland 2th Anniversary May 5-6,

Monetary Policy and Resource Mobility 2th Anniversary of the Bank of Finland Carl E. Walsh University of California, Santa Cruz May 5-6, 211 C. E. Walsh (UCSC) Bank of Finland 2th Anniversary May 5-6,

Monetary Policy and Resource Mobility

Monetary Policy and Resource Mobility 2th Anniversary of the Bank of Finland Carl E. Walsh University of California, Santa Cruz May 5-6, 211 C. E. Walsh (UCSC) Bank of Finland 2th Anniversary May 5-6,

Monetary Policy and Resource Mobility 2th Anniversary of the Bank of Finland Carl E. Walsh University of California, Santa Cruz May 5-6, 211 C. E. Walsh (UCSC) Bank of Finland 2th Anniversary May 5-6,

Optimal Interest-Rate Rules: I. General Theory

Optimal Interest-Rate Rules: I. General Theory Marc P. Giannoni Columbia University Michael Woodford Princeton University September 9, 2002 Abstract This paper proposes a general method for deriving an

Optimal Interest-Rate Rules: I. General Theory Marc P. Giannoni Columbia University Michael Woodford Princeton University September 9, 2002 Abstract This paper proposes a general method for deriving an

The new Kenesian model

The new Kenesian model Michaª Brzoza-Brzezina Warsaw School of Economics 1 / 4 Flexible vs. sticky prices Central assumption in the (neo)classical economics: Prices (of goods and factor services) are fully

The new Kenesian model Michaª Brzoza-Brzezina Warsaw School of Economics 1 / 4 Flexible vs. sticky prices Central assumption in the (neo)classical economics: Prices (of goods and factor services) are fully

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

On Quality Bias and Inflation Targets: Supplementary Material

On Quality Bias and Inflation Targets: Supplementary Material Stephanie Schmitt-Grohé Martín Uribe August 2 211 This document contains supplementary material to Schmitt-Grohé and Uribe (211). 1 A Two Sector

On Quality Bias and Inflation Targets: Supplementary Material Stephanie Schmitt-Grohé Martín Uribe August 2 211 This document contains supplementary material to Schmitt-Grohé and Uribe (211). 1 A Two Sector

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

On the Design of an European Unemployment Insurance Mechanism

On the Design of an European Unemployment Insurance Mechanism Árpád Ábrahám João Brogueira de Sousa Ramon Marimon Lukas Mayr European University Institute Lisbon Conference on Structural Reforms, 6 July

On the Design of an European Unemployment Insurance Mechanism Árpád Ábrahám João Brogueira de Sousa Ramon Marimon Lukas Mayr European University Institute Lisbon Conference on Structural Reforms, 6 July

Macroeconomics 2. Lecture 6 - New Keynesian Business Cycles March. Sciences Po

Macroeconomics 2 Lecture 6 - New Keynesian Business Cycles 2. Zsófia L. Bárány Sciences Po 2014 March Main idea: introduce nominal rigidities Why? in classical monetary models the price level ensures money

Macroeconomics 2 Lecture 6 - New Keynesian Business Cycles 2. Zsófia L. Bárány Sciences Po 2014 March Main idea: introduce nominal rigidities Why? in classical monetary models the price level ensures money

Teaching Inflation Targeting: An Analysis for Intermediate Macro. Carl E. Walsh * First draft: September 2000 This draft: July 2001

Teaching Inflation Targeting: An Analysis for Intermediate Macro Carl E. Walsh * First draft: September 2000 This draft: July 2001 * Professor of Economics, University of California, Santa Cruz, and Visiting

Teaching Inflation Targeting: An Analysis for Intermediate Macro Carl E. Walsh * First draft: September 2000 This draft: July 2001 * Professor of Economics, University of California, Santa Cruz, and Visiting

Credit Frictions and Optimal Monetary Policy

Vasco Cúrdia FRB of New York 1 Michael Woodford Columbia University National Bank of Belgium, October 28 1 The views expressed in this paper are those of the author and do not necessarily re ect the position

Vasco Cúrdia FRB of New York 1 Michael Woodford Columbia University National Bank of Belgium, October 28 1 The views expressed in this paper are those of the author and do not necessarily re ect the position

The Transmission of Monetary Policy through Redistributions and Durable Purchases

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

Monetary Policy and Stock Market Boom-Bust Cycles by L. Christiano, C. Ilut, R. Motto, and M. Rostagno

Comments on Monetary Policy and Stock Market Boom-Bust Cycles by L. Christiano, C. Ilut, R. Motto, and M. Rostagno Andrew Levin Federal Reserve Board May 8 The views expressed are solely the responsibility

Comments on Monetary Policy and Stock Market Boom-Bust Cycles by L. Christiano, C. Ilut, R. Motto, and M. Rostagno Andrew Levin Federal Reserve Board May 8 The views expressed are solely the responsibility

Robust Discretionary Monetary Policy under Cost- Push Shock Uncertainty of Iran s Economy

Iran. Econ. Rev. Vol. 22, No. 2, 218. pp. 53-526 Robust Discretionary Monetary Policy under Cost- Push Shock Uncertainty of Iran s Economy Fatemeh Labafi Feriz 1, Saeed Samadi *2 Khadijeh Nasrullahi 3,

Iran. Econ. Rev. Vol. 22, No. 2, 218. pp. 53-526 Robust Discretionary Monetary Policy under Cost- Push Shock Uncertainty of Iran s Economy Fatemeh Labafi Feriz 1, Saeed Samadi *2 Khadijeh Nasrullahi 3,

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Macroeconomics and finance

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Oil and macroeconomic (in)stability

stability") Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

GHG Emissions Control and Monetary Policy

GHG Emissions Control and Monetary Policy Barbara Annicchiarico* Fabio Di Dio** *Department of Economics and Finance University of Rome Tor Vergata **IT Economia - SOGEI S.P.A Workshop on Central Banking,

GHG Emissions Control and Monetary Policy Barbara Annicchiarico* Fabio Di Dio** *Department of Economics and Finance University of Rome Tor Vergata **IT Economia - SOGEI S.P.A Workshop on Central Banking,

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

Fiscal and Monetary Policies: Background

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Optimal Perception of Inflation Persistence at an Inflation-Targeting Central Bank

Optimal Perception of Inflation Persistence at an Inflation-Targeting Central Bank Kai Leitemo The Norwegian School of Management BI and Norges Bank March 2003 Abstract Delegating monetary policy to a

Optimal Perception of Inflation Persistence at an Inflation-Targeting Central Bank Kai Leitemo The Norwegian School of Management BI and Norges Bank March 2003 Abstract Delegating monetary policy to a

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy Mitsuru Katagiri International Monetary Fund October 24, 2017 @Keio University 1 / 42 Disclaimer The views expressed here are those of

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy Mitsuru Katagiri International Monetary Fund October 24, 2017 @Keio University 1 / 42 Disclaimer The views expressed here are those of