9th Financial Risks International Forum

|

|

|

- Cameron Lucas

- 5 years ago

- Views:

Transcription

1 Calvet L., Czellar V.and C. Gouriéroux (2015) Structural Dynamic Analysis of Systematic Risk Duarte D., Lee K. and Scwenkler G. (2015) The Systemic E ects of Benchmarking University of Orléans March 21, 2016

2 Comments on Structural Dynamic Analysis of Systematic Risk Calvet L., Czellar V.and C. Gouriéroux (2015)

3 Summary This paper introduces an original structural dynamic factor model (SDFM) for stock returns Nonlinear impact of the common factor and stochastic volatilities on returns, that depends on the distance-to-default. Estimation: Indirect Inference (Gouriéroux, Monfort and Renault, 1993) Filtering: Approximate Bayesian Computation algorithm (Calvet and Czellar, 2011)

4 Fact The structural dynamic factor model (SDFM) is a (structural) nonlinear state space model Engle, R., and E. Siriwardane (2015). Structural GARCH: The Volatility-Leverage Connection. Harvard Business School Working Paper

5

6

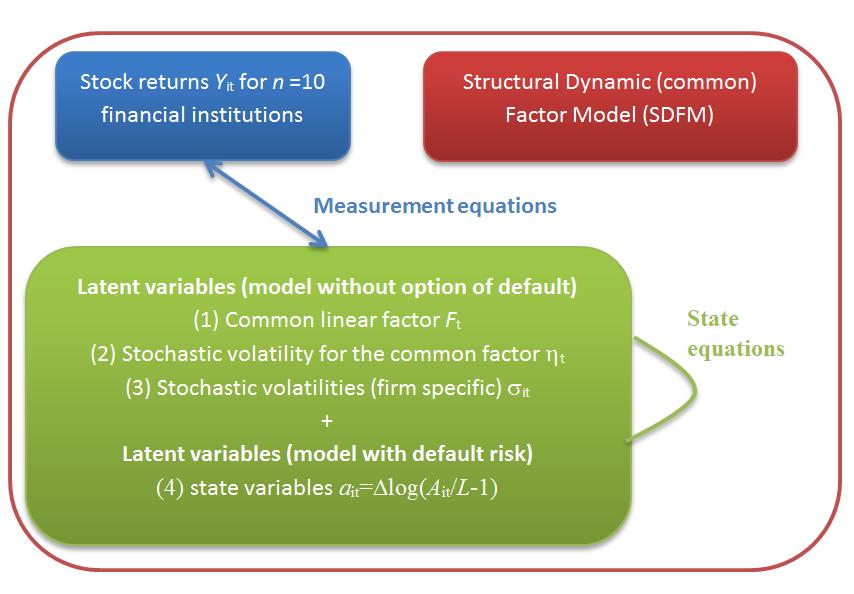

7 from a Dynamic Factor Model (DFM)... Y it = α i + β i F t + σ it ɛ it F t = γf t 1 + η t u t η 2 t ARG δ, ρ, (1 ρ) 1 γ2 /δ σ 2 it ARG e δ, eρ, ec ARG: AutoRegressive Gamma (ARG): exact time discretized Cox-Ingersoll-Ross process State variables: F t : common unobservable linear factor η t : factor stochastic volatility σ it : rm-speci c stochastic volatilities (i = 1,.., n)

8 to a Structural Dynamic Factor Model (SDFM)... a it = α i + β i F t + σ it ɛ it F t = γf t 1 + η t u t η 2 t ARG δ, ρ, (1 ρ) 1 γ2 /δ σ 2 it ARG e δ, eρ, ec Y it = h (log (A it /L 1)) h (log (A i,t 1 /L 1)) a it = log (A it /L 1) where A i,0 /L is xed and the asset value A it and the liabilities L (?) are unobservable.

9 This model is structural since it is based on an economic de nition of the default from the balance sheet information (Value-of-the Firm model). When the asset/liability ratio is large ( rm is far from the default): Y it ' a it But, in the general case, the stock returns depend not only on the changes a it, but also on the leverage A i,t 1 /L 1 The leverage e ect increases with the proximity to default, as measured by the excess asset/liability ratio.

10 Comment 1 In the paper, the authors derive three risk measures: 1 the implied nancial leverage AL it = ba it /L 1 2 the distance-to-default DD it = bh i log(ba it /L 1) log(ba it /L 1) 3 a measure of the magnitude of speculation ( DD) 2 Why not consider the SRISK index as in Engle and Siriwardane (2015)?

11 De nition (SRISK, Brownlees and Engle, 2015) The SRISK corresponds to the expected capital shortfall of a given rm i, conditional on a crisis a ecting the whole nancial system. SRISK it = W it (k LVG it (1 k) MES it 1) MES it (α) = E(Y it jy mt VaR mt (α); Ω t 1 ) with D it the book value of debt, W it the market value of equity and LVG it = D it / (D it + W it ).

12 Toward a structural-based SRISK

13 Source: Engle and Siriwardane (2015), page 30

14 Comment 2: Indirect inference and validation of the SRISK.. It could be interesting to compare 1 the structural-based SRISK and the "naive" SRISK for di erent rms (time-series analysis), 2 the systemic risk rankings implied by the two SRISKs at a given date (Spearman rank correlation). "Structural" validation test of the SRISK 1 Include SRISK-based statistics (rank correlation, etc.) in the auxiliary model (indirect inference) 2 Compare the estimated parameters with and without these additional statistics

15 Comment 3: The sample includes only 10 nancial institutions. Is it possible to consider a sample with a large n dimension? Comment 4: In the SDFM, the leverage has an impact on the return s volatility, as soon as the rm is close to the default => kind of switching regime model. What is the estimated e ect of the leverage on the volatility for the considered nancial institutions?

16 Systemic E ect of Benchmarking Comments on The Systemic E ects of Benchmarking Duarte D., Lee K. and Scwenkler G. (2015)

17 Systemic E ects of Benchmarking Summary Original theoretical model designed to study the systemic e ects of benchmarking Competitive pressure to beat a benchmark may induce institutional trading behavior ( re sales) that exposes retail investors to tail risk The model is (relatively) simple and elegant, and it can be solved in semi-closed form. So, the model allows to run: 1 a comparative analysis with di erent benchmarking incentives 2 a survival analysis and a welfare analysis.

18 Systemic E ects of Benchmarking Model Pure-exchange economy with two types of investors: retail and institutional Two assets: a benchmark and a non-benchmark stock Retail investors are mean-variance investors The utility of institutional investors increases in the states in which the benchmark stock outperforms. Main result If bad news about the benchmark arrives (jump), the institutional investors iniate re sales. These re sales increase the tail risk exposure of the retail investors.

19 Systemic E ects of Benchmarking Comment 1: The authors assume that the two sources of risk (for the dividends D 1t and D 2t ) are independent. Under this assumption, the systemic e ects of the benchmarking are maximum. If the systemic e ects decrease with the correlation of the two assets, it could be interesting to discuss this point.

20 Systemic E ects of Benchmarking Comment 2: The authors measure the systemic e ects of the benchmarking through the VaR of the nancial system. If we decompose the aggregate VaR between the institutional and retail investors, who have the largest contribution? Assumption: the retail investors have the largest risk contribution when the benchmark importance parameters are large and s 0 is small This is puzzle for the regulator since the largest risk contributors are not at the source of the systemic risk What are the best regulatory tools for the asset management industry within this framework?

A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR

A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR Sylvain Benoit, Gilbert Colletaz, Christophe Hurlin and Christophe Pérignon June 2012. Benoit, G.Colletaz, C. Hurlin,

A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR Sylvain Benoit, Gilbert Colletaz, Christophe Hurlin and Christophe Pérignon June 2012. Benoit, G.Colletaz, C. Hurlin,

GRANULARITY ADJUSTMENT FOR DYNAMIC MULTIPLE FACTOR MODELS : SYSTEMATIC VS UNSYSTEMATIC RISKS

GRANULARITY ADJUSTMENT FOR DYNAMIC MULTIPLE FACTOR MODELS : SYSTEMATIC VS UNSYSTEMATIC RISKS Patrick GAGLIARDINI and Christian GOURIÉROUX INTRODUCTION Risk measures such as Value-at-Risk (VaR) Expected

GRANULARITY ADJUSTMENT FOR DYNAMIC MULTIPLE FACTOR MODELS : SYSTEMATIC VS UNSYSTEMATIC RISKS Patrick GAGLIARDINI and Christian GOURIÉROUX INTRODUCTION Risk measures such as Value-at-Risk (VaR) Expected

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

Credit and Systemic Risks in the Financial Services Sector

Credit and Systemic Risks in the Financial Services Sector Measurement and Control of Systemic Risk Workshop Montréal Jean-François Bégin (Stat & Actuarial Sciences, Simon Fraser) Mathieu Boudreault (

Credit and Systemic Risks in the Financial Services Sector Measurement and Control of Systemic Risk Workshop Montréal Jean-François Bégin (Stat & Actuarial Sciences, Simon Fraser) Mathieu Boudreault (

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Bayesian Analysis of Systemic Risk Distributions

Bayesian Analysis of Systemic Risk Distributions Elena Goldman Department of Finance and Economics Lubin School of Business, Pace University New York, NY 10038 E-mail: egoldman@pace.edu Draft: 2016 Abstract

Bayesian Analysis of Systemic Risk Distributions Elena Goldman Department of Finance and Economics Lubin School of Business, Pace University New York, NY 10038 E-mail: egoldman@pace.edu Draft: 2016 Abstract

Bilateral Exposures and Systemic Solvency Risk

Bilateral Exposures and Systemic Solvency Risk C., GOURIEROUX (1), J.C., HEAM (2), and A., MONFORT (3) (1) CREST, and University of Toronto (2) CREST, and Autorité de Contrôle Prudentiel et de Résolution

Bilateral Exposures and Systemic Solvency Risk C., GOURIEROUX (1), J.C., HEAM (2), and A., MONFORT (3) (1) CREST, and University of Toronto (2) CREST, and Autorité de Contrôle Prudentiel et de Résolution

The Systemic Effects of Benchmarking

1 The Systemic Effects of Benchmarking Boston University Joint work with: Diogo Duarte, Boston University Keith Lee, Boston University Securities Markets: Trends, Risks and Policies Conference February

1 The Systemic Effects of Benchmarking Boston University Joint work with: Diogo Duarte, Boston University Keith Lee, Boston University Securities Markets: Trends, Risks and Policies Conference February

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market Liran Einav 1 Amy Finkelstein 2 Paul Schrimpf 3 1 Stanford and NBER 2 MIT and NBER 3 MIT Cowles 75th Anniversary Conference

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market Liran Einav 1 Amy Finkelstein 2 Paul Schrimpf 3 1 Stanford and NBER 2 MIT and NBER 3 MIT Cowles 75th Anniversary Conference

Housing Prices and Growth

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Estimating a Dynamic Oligopolistic Game with Serially Correlated Unobserved Production Costs. SS223B-Empirical IO

Estimating a Dynamic Oligopolistic Game with Serially Correlated Unobserved Production Costs SS223B-Empirical IO Motivation There have been substantial recent developments in the empirical literature on

Estimating a Dynamic Oligopolistic Game with Serially Correlated Unobserved Production Costs SS223B-Empirical IO Motivation There have been substantial recent developments in the empirical literature on

FE570 Financial Markets and Trading. Stevens Institute of Technology

FE570 Financial Markets and Trading Lecture 6. Volatility Models and (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 10/02/2012 Outline 1 Volatility

FE570 Financial Markets and Trading Lecture 6. Volatility Models and (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 10/02/2012 Outline 1 Volatility

Investment is one of the most important and volatile components of macroeconomic activity. In the short-run, the relationship between uncertainty and

Investment is one of the most important and volatile components of macroeconomic activity. In the short-run, the relationship between uncertainty and investment is central to understanding the business

Investment is one of the most important and volatile components of macroeconomic activity. In the short-run, the relationship between uncertainty and investment is central to understanding the business

A potentially useful approach to model nonlinearities in time series is to assume different behavior (structural break) in different subsamples

in different subsamples") 1.3 Regime switching models A potentially useful approach to model nonlinearities in time series is to assume different behavior (structural break) in different subsamples (or regimes). If the dates, the

1.3 Regime switching models A potentially useful approach to model nonlinearities in time series is to assume different behavior (structural break) in different subsamples (or regimes). If the dates, the

Stock Price, Risk-free Rate and Learning

Stock Price, Risk-free Rate and Learning Tongbin Zhang Univeristat Autonoma de Barcelona and Barcelona GSE April 2016 Tongbin Zhang (Institute) Stock Price, Risk-free Rate and Learning April 2016 1 / 31

Stock Price, Risk-free Rate and Learning Tongbin Zhang Univeristat Autonoma de Barcelona and Barcelona GSE April 2016 Tongbin Zhang (Institute) Stock Price, Risk-free Rate and Learning April 2016 1 / 31

Forecasting jumps in conditional volatility The GARCH-IE model

Forecasting jumps in conditional volatility The GARCH-IE model Philip Hans Franses and Marco van der Leij Econometric Institute Erasmus University Rotterdam e-mail: franses@few.eur.nl 1 Outline of presentation

Forecasting jumps in conditional volatility The GARCH-IE model Philip Hans Franses and Marco van der Leij Econometric Institute Erasmus University Rotterdam e-mail: franses@few.eur.nl 1 Outline of presentation

Robert Engle and Emil Siriwardane Volatility Institute of NYU Stern 6/24/2014 STRUCTURAL GARCH AND A RISK BASED TOTAL LEVERAGE CAPITAL REQUIREMENT

Robert Engle and Emil Siriwardane Volatility Institute of NYU Stern 6/24/2014 STRUCTURAL GARCH AND A RISK BASED TOTAL LEVERAGE CAPITAL REQUIREMENT SRISK How much additional capital would a firm expect

Robert Engle and Emil Siriwardane Volatility Institute of NYU Stern 6/24/2014 STRUCTURAL GARCH AND A RISK BASED TOTAL LEVERAGE CAPITAL REQUIREMENT SRISK How much additional capital would a firm expect

Empirical Evidence. r Mt r ft e i. now do second-pass regression (cross-sectional with N 100): r i r f γ 0 γ 1 b i u i

: r i r f γ 0 γ 1 b i u i") Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

The Transmission of Monetary Policy through Redistributions and Durable Purchases

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

Earnings Inequality and the Minimum Wage: Evidence from Brazil

Earnings Inequality and the Minimum Wage: Evidence from Brazil Niklas Engbom June 16, 2016 Christian Moser World Bank-Bank of Spain Conference This project Shed light on drivers of earnings inequality

Earnings Inequality and the Minimum Wage: Evidence from Brazil Niklas Engbom June 16, 2016 Christian Moser World Bank-Bank of Spain Conference This project Shed light on drivers of earnings inequality

Discussion: Bank Risk Dynamics and Distance to Default

Discussion: Bank Risk Dynamics and Distance to Default Andrea L. Eisfeldt UCLA Anderson BFI Conference on Financial Regulation October 3, 2015 Main Idea: Bank Assets 1 1 0.9 0.9 0.8 Bank assets 0.8 0.7

Discussion: Bank Risk Dynamics and Distance to Default Andrea L. Eisfeldt UCLA Anderson BFI Conference on Financial Regulation October 3, 2015 Main Idea: Bank Assets 1 1 0.9 0.9 0.8 Bank assets 0.8 0.7

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations?

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations? Bernard Dumas INSEAD, Wharton, CEPR, NBER Alexander Kurshev London Business School Raman Uppal London Business School,

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations? Bernard Dumas INSEAD, Wharton, CEPR, NBER Alexander Kurshev London Business School Raman Uppal London Business School,

Modelling the stochastic behaviour of short-term interest rates: A survey

Modelling the stochastic behaviour of short-term interest rates: A survey 4 5 6 7 8 9 10 SAMBA/21/04 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 Kjersti Aas September 23, 2004 NR Norwegian Computing

Modelling the stochastic behaviour of short-term interest rates: A survey 4 5 6 7 8 9 10 SAMBA/21/04 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 Kjersti Aas September 23, 2004 NR Norwegian Computing

Monetary Economics. Financial Markets and the Business Cycle: The Bernanke and Gertler Model. Nicola Viegi. September 2010

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Dependence Structure and Extreme Comovements in International Equity and Bond Markets

Dependence Structure and Extreme Comovements in International Equity and Bond Markets René Garcia Edhec Business School, Université de Montréal, CIRANO and CIREQ Georges Tsafack Suffolk University Measuring

Dependence Structure and Extreme Comovements in International Equity and Bond Markets René Garcia Edhec Business School, Université de Montréal, CIRANO and CIREQ Georges Tsafack Suffolk University Measuring

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business MFM Macroeconomic Fragility Fall 2013 Meeting Leverage and Equity Volatility I Crisis

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business MFM Macroeconomic Fragility Fall 2013 Meeting Leverage and Equity Volatility I Crisis

Survival of Hedge Funds : Frailty vs Contagion

Survival of Hedge Funds : Frailty vs Contagion February, 2015 1. Economic motivation Financial entities exposed to liquidity risk(s)... on the asset component of the balance sheet (market liquidity) on

Survival of Hedge Funds : Frailty vs Contagion February, 2015 1. Economic motivation Financial entities exposed to liquidity risk(s)... on the asset component of the balance sheet (market liquidity) on

Crises and Prices: Information Aggregation, Multiplicity and Volatility

: Information Aggregation, Multiplicity and Volatility Reading Group UC3M G.M. Angeletos and I. Werning November 09 Motivation Modelling Crises I There is a wide literature analyzing crises (currency attacks,

: Information Aggregation, Multiplicity and Volatility Reading Group UC3M G.M. Angeletos and I. Werning November 09 Motivation Modelling Crises I There is a wide literature analyzing crises (currency attacks,

Short-selling constraints and stock-return volatility: empirical evidence from the German stock market

Short-selling constraints and stock-return volatility: empirical evidence from the German stock market Martin Bohl, Gerrit Reher, Bernd Wilfling Westfälische Wilhelms-Universität Münster Contents 1. Introduction

Short-selling constraints and stock-return volatility: empirical evidence from the German stock market Martin Bohl, Gerrit Reher, Bernd Wilfling Westfälische Wilhelms-Universität Münster Contents 1. Introduction

Modeling Daily Oil Price Data Using Auto-regressive Jump Intensity GARCH Models

Modeling Daily Oil Price Data Using Auto-regressive Jump Intensity GARCH Models ifo Institute for Economic Research 22 June 2009 32nd IAEE International Conference San Francisco 1 Motivation 2 Descriptive

Modeling Daily Oil Price Data Using Auto-regressive Jump Intensity GARCH Models ifo Institute for Economic Research 22 June 2009 32nd IAEE International Conference San Francisco 1 Motivation 2 Descriptive

Bond Spreads, Market Integration and Contagion in the Crisis

Bond Spreads, Market Integration and Contagion in the 78 Crisis JaeYoung Kim, DongHyun Ahn and EunYoung Ko Yield spreads on sovereign bonds represent market expectations for the economic performance of

Bond Spreads, Market Integration and Contagion in the 78 Crisis JaeYoung Kim, DongHyun Ahn and EunYoung Ko Yield spreads on sovereign bonds represent market expectations for the economic performance of

Implied Systemic Risk Index (work in progress, still at an early stage)

") Implied Systemic Risk Index (work in progress, still at an early stage) Carole Bernard, joint work with O. Bondarenko and S. Vanduffel IPAM, March 23-27, 2015: Workshop I: Systemic risk and financial networks

Implied Systemic Risk Index (work in progress, still at an early stage) Carole Bernard, joint work with O. Bondarenko and S. Vanduffel IPAM, March 23-27, 2015: Workshop I: Systemic risk and financial networks

Stochastic Volatility Models. Hedibert Freitas Lopes

Stochastic Volatility Models Hedibert Freitas Lopes SV-AR(1) model Nonlinear dynamic model Normal approximation R package stochvol Other SV models STAR-SVAR(1) model MSSV-SVAR(1) model Volume-volatility

Stochastic Volatility Models Hedibert Freitas Lopes SV-AR(1) model Nonlinear dynamic model Normal approximation R package stochvol Other SV models STAR-SVAR(1) model MSSV-SVAR(1) model Volume-volatility

A Unified Theory of Bond and Currency Markets

A Unified Theory of Bond and Currency Markets Andrey Ermolov Columbia Business School April 24, 2014 1 / 41 Stylized Facts about Bond Markets US Fact 1: Upward Sloping Real Yield Curve In US, real long

A Unified Theory of Bond and Currency Markets Andrey Ermolov Columbia Business School April 24, 2014 1 / 41 Stylized Facts about Bond Markets US Fact 1: Upward Sloping Real Yield Curve In US, real long

Exchange Rates and Fundamentals: A General Equilibrium Exploration

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Return Decomposition over the Business Cycle

Return Decomposition over the Business Cycle Tolga Cenesizoglu March 1, 2016 Cenesizoglu Return Decomposition & the Business Cycle March 1, 2016 1 / 54 Introduction Stock prices depend on investors expectations

Return Decomposition over the Business Cycle Tolga Cenesizoglu March 1, 2016 Cenesizoglu Return Decomposition & the Business Cycle March 1, 2016 1 / 54 Introduction Stock prices depend on investors expectations

Portfolio selection with multiple risk measures

Portfolio selection with multiple risk measures Garud Iyengar Columbia University Industrial Engineering and Operations Research Joint work with Carlos Abad Outline Portfolio selection and risk measures

Portfolio selection with multiple risk measures Garud Iyengar Columbia University Industrial Engineering and Operations Research Joint work with Carlos Abad Outline Portfolio selection and risk measures

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

ARCH and GARCH models

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Systemic Risk of Dual Banking Systems

Systemic Risk of Dual Banking Systems S. Q. Hashem 1 P. Giudici 2 P. Abedifar 3 1&2 Faculty of Economics University of Pavia 3 Faculty of Management University of St Andrews September 216 Summary Context

Systemic Risk of Dual Banking Systems S. Q. Hashem 1 P. Giudici 2 P. Abedifar 3 1&2 Faculty of Economics University of Pavia 3 Faculty of Management University of St Andrews September 216 Summary Context

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space Tak Kuen Siu Department of Applied Finance and Actuarial Studies, Faculty of Business and Economics, Macquarie University,

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space Tak Kuen Siu Department of Applied Finance and Actuarial Studies, Faculty of Business and Economics, Macquarie University,

Implied Volatility Correlations

Implied Volatility Correlations Robert Engle, Stephen Figlewski and Amrut Nashikkar Date: May 18, 2007 Derivatives Research Conference, NYU IMPLIED VOLATILITY Implied volatilities from market traded options

Implied Volatility Correlations Robert Engle, Stephen Figlewski and Amrut Nashikkar Date: May 18, 2007 Derivatives Research Conference, NYU IMPLIED VOLATILITY Implied volatilities from market traded options

Bank Risk Dynamics and Distance to Default

Stefan Nagel 1 Amiyatosh Purnanandam 2 1 University of Michigan, NBER & CEPR 2 University of Michigan October 2015 Introduction Financial crisis highlighted need to understand bank default risk and bank

Stefan Nagel 1 Amiyatosh Purnanandam 2 1 University of Michigan, NBER & CEPR 2 University of Michigan October 2015 Introduction Financial crisis highlighted need to understand bank default risk and bank

Model Estimation. Liuren Wu. Fall, Zicklin School of Business, Baruch College. Liuren Wu Model Estimation Option Pricing, Fall, / 16

Model Estimation Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 Liuren Wu Model Estimation Option Pricing, Fall, 2007 1 / 16 Outline 1 Statistical dynamics 2 Risk-neutral dynamics 3 Joint

Model Estimation Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 Liuren Wu Model Estimation Option Pricing, Fall, 2007 1 / 16 Outline 1 Statistical dynamics 2 Risk-neutral dynamics 3 Joint

Prospect Theory and Asset Prices

Prospect Theory and Asset Prices Presenting Barberies - Huang - Santos s paper Attila Lindner January 2009 Attila Lindner (CEU) Prospect Theory and Asset Prices January 2009 1 / 17 Presentation Outline

Prospect Theory and Asset Prices Presenting Barberies - Huang - Santos s paper Attila Lindner January 2009 Attila Lindner (CEU) Prospect Theory and Asset Prices January 2009 1 / 17 Presentation Outline

Investors Attention and Stock Market Volatility

Investors Attention and Stock Market Volatility Daniel Andrei Michael Hasler Princeton Workshop, Lausanne 2011 Attention and Volatility Andrei and Hasler Princeton Workshop 2011 0 / 15 Prerequisites Attention

Investors Attention and Stock Market Volatility Daniel Andrei Michael Hasler Princeton Workshop, Lausanne 2011 Attention and Volatility Andrei and Hasler Princeton Workshop 2011 0 / 15 Prerequisites Attention

What Can a Life-Cycle Model Tell Us About Household Responses to the Financial Crisis?

What Can a Life-Cycle Model Tell Us About Household Responses to the Financial Crisis? Sule Alan 1 Thomas Crossley 1 Hamish Low 1 1 University of Cambridge and Institute for Fiscal Studies March 2010 Data:

What Can a Life-Cycle Model Tell Us About Household Responses to the Financial Crisis? Sule Alan 1 Thomas Crossley 1 Hamish Low 1 1 University of Cambridge and Institute for Fiscal Studies March 2010 Data:

The Complexity of GARCH Option Pricing Models

JOURNAL OF INFORMATION SCIENCE AND ENGINEERING 8, 689-704 (01) The Complexity of GARCH Option Pricing Models YING-CHIE CHEN +, YUH-DAUH LYUU AND KUO-WEI WEN + Department of Finance Department of Computer

JOURNAL OF INFORMATION SCIENCE AND ENGINEERING 8, 689-704 (01) The Complexity of GARCH Option Pricing Models YING-CHIE CHEN +, YUH-DAUH LYUU AND KUO-WEI WEN + Department of Finance Department of Computer

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

Discussion of Lumpy investment in general equilibrium by Bachman, Caballero, and Engel

Discussion of Lumpy investment in general equilibrium by Bachman, Caballero, and Engel Julia K. Thomas Federal Reserve Bank of Philadelphia 9 February 2007 Julia Thomas () Discussion of Bachman, Caballero,

Discussion of Lumpy investment in general equilibrium by Bachman, Caballero, and Engel Julia K. Thomas Federal Reserve Bank of Philadelphia 9 February 2007 Julia Thomas () Discussion of Bachman, Caballero,

Market Risk Analysis Volume IV. Value-at-Risk Models

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

2008 North American Summer Meeting. June 19, Information and High Frequency Trading. E. Pagnotta Norhwestern University.

2008 North American Summer Meeting Emiliano S. Pagnotta June 19, 2008 The UHF Revolution Fact (The UHF Revolution) Financial markets data sets at the transaction level available to scholars (TAQ, TORQ,

2008 North American Summer Meeting Emiliano S. Pagnotta June 19, 2008 The UHF Revolution Fact (The UHF Revolution) Financial markets data sets at the transaction level available to scholars (TAQ, TORQ,

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil. International Monetary Fund

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil International Monetary Fund September, 2008 Motivation Goal of the Paper Outline Systemic

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil International Monetary Fund September, 2008 Motivation Goal of the Paper Outline Systemic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

The Macroeconomics of Universal Health Insurance Vouchers

The Macroeconomics of Universal Health Insurance Vouchers Juergen Jung Towson University Chung Tran University of New South Wales Jul-Aug 2009 Jung and Tran (TU and UNSW) Health Vouchers 2009 1 / 29 Dysfunctional

The Macroeconomics of Universal Health Insurance Vouchers Juergen Jung Towson University Chung Tran University of New South Wales Jul-Aug 2009 Jung and Tran (TU and UNSW) Health Vouchers 2009 1 / 29 Dysfunctional

Course information FN3142 Quantitative finance

Course information 015 16 FN314 Quantitative finance This course is aimed at students interested in obtaining a thorough grounding in market finance and related empirical methods. Prerequisite If taken

Course information 015 16 FN314 Quantitative finance This course is aimed at students interested in obtaining a thorough grounding in market finance and related empirical methods. Prerequisite If taken

Financial Econometrics Jeffrey R. Russell. Midterm 2014 Suggested Solutions. TA: B. B. Deng

Financial Econometrics Jeffrey R. Russell Midterm 2014 Suggested Solutions TA: B. B. Deng Unless otherwise stated, e t is iid N(0,s 2 ) 1. (12 points) Consider the three series y1, y2, y3, and y4. Match

Financial Econometrics Jeffrey R. Russell Midterm 2014 Suggested Solutions TA: B. B. Deng Unless otherwise stated, e t is iid N(0,s 2 ) 1. (12 points) Consider the three series y1, y2, y3, and y4. Match

Rare Disasters, Credit and Option Market Puzzles. Online Appendix

Rare Disasters, Credit and Option Market Puzzles. Online Appendix Peter Christo ersen Du Du Redouane Elkamhi Rotman School, City University Rotman School, CBS and CREATES of Hong Kong University of Toronto

Rare Disasters, Credit and Option Market Puzzles. Online Appendix Peter Christo ersen Du Du Redouane Elkamhi Rotman School, City University Rotman School, CBS and CREATES of Hong Kong University of Toronto

Monetary Economics Basic Flexible Price Models

Monetary Economics Basic Flexible Price Models Nicola Viegi July 26, 207 Modelling Money I Cagan Model - The Price of Money I A Modern Classical Model (Without Money) I Money in Utility Function Approach

Monetary Economics Basic Flexible Price Models Nicola Viegi July 26, 207 Modelling Money I Cagan Model - The Price of Money I A Modern Classical Model (Without Money) I Money in Utility Function Approach

Likelihood Estimation of Jump-Diffusions

Likelihood Estimation of Jump-Diffusions Extensions from Diffusions to Jump-Diffusions, Implementation with Automatic Differentiation, and Applications Berent Ånund Strømnes Lunde DEPARTMENT OF MATHEMATICS

Likelihood Estimation of Jump-Diffusions Extensions from Diffusions to Jump-Diffusions, Implementation with Automatic Differentiation, and Applications Berent Ånund Strømnes Lunde DEPARTMENT OF MATHEMATICS

Is the Potential for International Diversification Disappearing? A Dynamic Copula Approach

Is the Potential for International Diversification Disappearing? A Dynamic Copula Approach Peter Christoffersen University of Toronto Vihang Errunza McGill University Kris Jacobs University of Houston

Is the Potential for International Diversification Disappearing? A Dynamic Copula Approach Peter Christoffersen University of Toronto Vihang Errunza McGill University Kris Jacobs University of Houston

Stochastic Volatility (SV) Models Lecture 9. Morettin & Toloi, 2006, Section 14.6 Tsay, 2010, Section 3.12 Tsay, 2013, Section 4.

Models Lecture 9. Morettin & Toloi, 2006, Section 14.6 Tsay, 2010, Section 3.12 Tsay, 2013, Section 4.") Stochastic Volatility (SV) Models Lecture 9 Morettin & Toloi, 2006, Section 14.6 Tsay, 2010, Section 3.12 Tsay, 2013, Section 4.13 Stochastic volatility model The canonical stochastic volatility model

Stochastic Volatility (SV) Models Lecture 9 Morettin & Toloi, 2006, Section 14.6 Tsay, 2010, Section 3.12 Tsay, 2013, Section 4.13 Stochastic volatility model The canonical stochastic volatility model

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

Country Spreads as Credit Constraints in Emerging Economy Business Cycles

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

University of Toronto Financial Econometrics, ECO2411. Course Outline

University of Toronto Financial Econometrics, ECO2411 Course Outline John M. Maheu 2006 Office: 5024 (100 St. George St.), K244 (UTM) Office Hours: T2-4, or by appointment Phone: 416-978-1495 (100 St.

University of Toronto Financial Econometrics, ECO2411 Course Outline John M. Maheu 2006 Office: 5024 (100 St. George St.), K244 (UTM) Office Hours: T2-4, or by appointment Phone: 416-978-1495 (100 St.

Risk Parity-based Smart Beta ETFs and Estimation Risk

Risk Parity-based Smart Beta ETFs and Estimation Risk Olessia Caillé, Christophe Hurlin and Daria Onori This version: March 2016. Preliminary version. Please do not cite. Abstract The aim of this paper

Risk Parity-based Smart Beta ETFs and Estimation Risk Olessia Caillé, Christophe Hurlin and Daria Onori This version: March 2016. Preliminary version. Please do not cite. Abstract The aim of this paper

Uninsured Unemployment Risk and Optimal Monetary Policy

Uninsured Unemployment Risk and Optimal Monetary Policy Edouard Challe CREST & Ecole Polytechnique ASSA 2018 Strong precautionary motive Low consumption Bad aggregate shock High unemployment Low output

Uninsured Unemployment Risk and Optimal Monetary Policy Edouard Challe CREST & Ecole Polytechnique ASSA 2018 Strong precautionary motive Low consumption Bad aggregate shock High unemployment Low output

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Modelling volatility - ARCH and GARCH models

Modelling volatility - ARCH and GARCH models Beáta Stehlíková Time series analysis Modelling volatility- ARCH and GARCH models p.1/33 Stock prices Weekly stock prices (library quantmod) Continuous returns:

Modelling volatility - ARCH and GARCH models Beáta Stehlíková Time series analysis Modelling volatility- ARCH and GARCH models p.1/33 Stock prices Weekly stock prices (library quantmod) Continuous returns:

A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite)

") A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite) Edward Kung UCLA March 1, 2013 OBJECTIVES The goal of this paper is to assess the potential impact of introducing alternative

A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite) Edward Kung UCLA March 1, 2013 OBJECTIVES The goal of this paper is to assess the potential impact of introducing alternative

Option Pricing Modeling Overview

Option Pricing Modeling Overview Liuren Wu Zicklin School of Business, Baruch College Options Markets Liuren Wu (Baruch) Stochastic time changes Options Markets 1 / 11 What is the purpose of building a

Option Pricing Modeling Overview Liuren Wu Zicklin School of Business, Baruch College Options Markets Liuren Wu (Baruch) Stochastic time changes Options Markets 1 / 11 What is the purpose of building a

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay. Solutions to Final Exam

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (30 pts) Answer briefly the following questions. 1. Suppose that

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (30 pts) Answer briefly the following questions. 1. Suppose that

Lecture Note 9 of Bus 41914, Spring Multivariate Volatility Models ChicagoBooth

Lecture Note 9 of Bus 41914, Spring 2017. Multivariate Volatility Models ChicagoBooth Reference: Chapter 7 of the textbook Estimation: use the MTS package with commands: EWMAvol, marchtest, BEKK11, dccpre,

Lecture Note 9 of Bus 41914, Spring 2017. Multivariate Volatility Models ChicagoBooth Reference: Chapter 7 of the textbook Estimation: use the MTS package with commands: EWMAvol, marchtest, BEKK11, dccpre,

Asymptotic Risk Factor Model with Volatility Factors

Asymptotic Risk Factor Model with Volatility Factors Abdoul Aziz Bah 1 Christian Gourieroux 2 André Tiomo 1 1 Credit Agricole Group 2 CREST and University of Toronto March 27, 2017 The views expressed

Asymptotic Risk Factor Model with Volatility Factors Abdoul Aziz Bah 1 Christian Gourieroux 2 André Tiomo 1 1 Credit Agricole Group 2 CREST and University of Toronto March 27, 2017 The views expressed

Menu Costs and Phillips Curve by Mikhail Golosov and Robert Lucas. JPE (2007)

") Menu Costs and Phillips Curve by Mikhail Golosov and Robert Lucas. JPE (2007) Virginia Olivella and Jose Ignacio Lopez October 2008 Motivation Menu costs and repricing decisions Micro foundation of sticky

Menu Costs and Phillips Curve by Mikhail Golosov and Robert Lucas. JPE (2007) Virginia Olivella and Jose Ignacio Lopez October 2008 Motivation Menu costs and repricing decisions Micro foundation of sticky

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business University of Chicago: 11/25/2013 Leverage and Equity Volatility I Crisis highlighted

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business University of Chicago: 11/25/2013 Leverage and Equity Volatility I Crisis highlighted

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1,2 1 NYU Stern School of Business 2 U.S. Treasury, Office of Financial Research (OFR) WFA Annual Meeting: 6/16/2014

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1,2 1 NYU Stern School of Business 2 U.S. Treasury, Office of Financial Research (OFR) WFA Annual Meeting: 6/16/2014

Preference-Free Option Pricing with Path-Dependent Volatility: A Closed-Form Approach

Preference-Free Option Pricing with Path-Dependent Volatility: A Closed-Form Approach Steven L. Heston and Saikat Nandi Federal Reserve Bank of Atlanta Working Paper 98-20 December 1998 Abstract: This

Preference-Free Option Pricing with Path-Dependent Volatility: A Closed-Form Approach Steven L. Heston and Saikat Nandi Federal Reserve Bank of Atlanta Working Paper 98-20 December 1998 Abstract: This

Money and monetary policy in Israel during the last decade

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Algorithmic and High-Frequency Trading

LOBSTER June 2 nd 2016 Algorithmic and High-Frequency Trading Julia Schmidt Overview Introduction Market Making Grossman-Miller Market Making Model Trading Costs Measuring Liquidity Market Making using

LOBSTER June 2 nd 2016 Algorithmic and High-Frequency Trading Julia Schmidt Overview Introduction Market Making Grossman-Miller Market Making Model Trading Costs Measuring Liquidity Market Making using

Empirical Test of Affine Stochastic Discount Factor Model of Currency Pricing. Abstract

Empirical Test of Affine Stochastic Discount Factor Model of Currency Pricing Alex Lebedinsky Western Kentucky University Abstract In this note, I conduct an empirical investigation of the affine stochastic

Empirical Test of Affine Stochastic Discount Factor Model of Currency Pricing Alex Lebedinsky Western Kentucky University Abstract In this note, I conduct an empirical investigation of the affine stochastic

Estimation of the Markov-switching GARCH model by a Monte Carlo EM algorithm

Estimation of the Markov-switching GARCH model by a Monte Carlo EM algorithm Maciej Augustyniak Fields Institute February 3, 0 Stylized facts of financial data GARCH Regime-switching MS-GARCH Agenda Available

Estimation of the Markov-switching GARCH model by a Monte Carlo EM algorithm Maciej Augustyniak Fields Institute February 3, 0 Stylized facts of financial data GARCH Regime-switching MS-GARCH Agenda Available

Oil and macroeconomic (in)stability

stability") Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

Market Risk Analysis Volume II. Practical Financial Econometrics

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

A Multivariate Analysis of Intercompany Loss Triangles

A Multivariate Analysis of Intercompany Loss Triangles Peng Shi School of Business University of Wisconsin-Madison ASTIN Colloquium May 21-24, 2013 Peng Shi (Wisconsin School of Business) Intercompany

A Multivariate Analysis of Intercompany Loss Triangles Peng Shi School of Business University of Wisconsin-Madison ASTIN Colloquium May 21-24, 2013 Peng Shi (Wisconsin School of Business) Intercompany

A market risk model for asymmetric distributed series of return

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

Financial Times Series. Lecture 6

Financial Times Series Lecture 6 Extensions of the GARCH There are numerous extensions of the GARCH Among the more well known are EGARCH (Nelson 1991) and GJR (Glosten et al 1993) Both models allow for

Financial Times Series Lecture 6 Extensions of the GARCH There are numerous extensions of the GARCH Among the more well known are EGARCH (Nelson 1991) and GJR (Glosten et al 1993) Both models allow for

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

Market MicroStructure Models. Research Papers

Market MicroStructure Models Jonathan Kinlay Summary This note summarizes some of the key research in the field of market microstructure and considers some of the models proposed by the researchers. Many

Market MicroStructure Models Jonathan Kinlay Summary This note summarizes some of the key research in the field of market microstructure and considers some of the models proposed by the researchers. Many

Application of Conditional Autoregressive Value at Risk Model to Kenyan Stocks: A Comparative Study

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Leverage Effect, Volatility Feedback, and Self-Exciting MarketAFA, Disruptions 1/7/ / 14

Leverage Effect, Volatility Feedback, and Self-Exciting Market Disruptions Liuren Wu, Baruch College Joint work with Peter Carr, New York University The American Finance Association meetings January 7,

Leverage Effect, Volatility Feedback, and Self-Exciting Market Disruptions Liuren Wu, Baruch College Joint work with Peter Carr, New York University The American Finance Association meetings January 7,

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

Aggregate Implications of Lumpy Adjustment

Aggregate Implications of Lumpy Adjustment Eduardo Engel Cowles Lunch. March 3rd, 2010 Eduardo Engel 1 1. Motivation Micro adjustment is lumpy for many aggregates of interest: stock of durable good nominal

Aggregate Implications of Lumpy Adjustment Eduardo Engel Cowles Lunch. March 3rd, 2010 Eduardo Engel 1 1. Motivation Micro adjustment is lumpy for many aggregates of interest: stock of durable good nominal

Market Efficiency, Asset Returns, and the Size of the Risk Premium in Global Equity Markets

Market Efficiency, Asset Returns, and the Size of the Risk Premium in Global Equity Markets Ravi Bansal and Christian Lundblad January 2002 Abstract An important economic insight is that observed equity

Market Efficiency, Asset Returns, and the Size of the Risk Premium in Global Equity Markets Ravi Bansal and Christian Lundblad January 2002 Abstract An important economic insight is that observed equity

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS001) p approach

p approach") Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS001) p.5901 What drives short rate dynamics? approach A functional gradient descent Audrino, Francesco University

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS001) p.5901 What drives short rate dynamics? approach A functional gradient descent Audrino, Francesco University

Booms and Busts in Asset Prices. May 2010

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of