Robert Engle and Emil Siriwardane Volatility Institute of NYU Stern 6/24/2014 STRUCTURAL GARCH AND A RISK BASED TOTAL LEVERAGE CAPITAL REQUIREMENT

|

|

|

- Agatha Lamb

- 5 years ago

- Views:

Transcription

1 Robert Engle and Emil Siriwardane Volatility Institute of NYU Stern 6/24/2014 STRUCTURAL GARCH AND A RISK BASED TOTAL LEVERAGE CAPITAL REQUIREMENT

2 SRISK How much additional capital would a firm expect to need in order to function normally if we have another financial crisis? Functioning normally means a capital ratio of k. We estimate this econometrically weekly and post it on: VLAB.stern.nyu.edu It is a useful measure of systemic risk that is showing improvement today in US and much of Europe.

3 THE MODEL Simulate crisis paths for the global stock market with six month decline of 40%. For each path simulate market cap for each firm using dynamic conditional beta and bootstrapped residuals. Measure capital shortfall relative to book value of liabilities and average across crisis paths. Take stressed normal capital ratio to be 8% for GAAP and 5.5% for IFRS firms. Some approximations are made.

4 AMERICAS SINCE 2000

5 ASIA SINCE 2000

6 EUROPE SINCE 2000

7 WHERE IS THE RISK TODAY?

8 THE FINANCIAL CRISIS: WERE WE PREPARED?

9 PRECAUTIONARY CAPITAL: A NEW QUESTION How much additional capital should a firm have today so that with probability l its capital ratio will fall below k if we have another financial crisis? The parameters lambda and kappa define the capital ratio but it must be assessed with a probability model.

10 k When capital ratios become too low, financial firms cease to function effectively and ultimately fail. We sometimes call these zombie banks. Measure with market value of equity over book value of liabilities plus equity. Lehman failed with a capital ratio of 2% in Aug 08. FNMA and FMAC were less than 1% and WAMU was 2.5%. BSC was 2.5% in Feb 08 before it failed. Subsequently, big US banks and insurers had capital ratios even lower but by this time they were under Treasury protection.

11 DIFFERENCES BETWEEN PRECAUTIONARY CAPITAL AND SRISK Precautionary capital is needed today vs. bailout capital needed later Tail probability of low capital ratios vs. expected capital needs Precautionary capital corresponds better to the goals of a risk manager as well as to a prudential supervisor.

12 A CAPITAL CRITERION Why does this give a sensible capital criterion? Conditional on a crisis, the probability of firm undercapitalization is less than or equal to lambda. Conditional on a crisis, firm outcomes will be approximately independent, hence the expected failure rate is lambda and the probability of much higher rates is very small. The tolerance for financial firm failure in a crisis is a reasonable criterion for requiring capital. It does not however assess the cost of excess capital.

13 COUNTER CYCLICAL IMPLEMENTATION It would be desirable to implement any capital requirement so that it is countercyclical. Capital requirements would be raised in good times and reduced in bad times. Timing is complicated and optimality is very difficult to achieve in light of the Lucas critique. Should capital ratios ever be reduced below the minimum viewed as sustainable?

14 ECONOMETRICS Estimate the fall in market capitalization of a firm in a financial crisis. Calculate the distribution of capital ratios that result. If losses are unaffected by the initial capital of the firm, then it is easy to compute both SRISK and Precautionary Capital. However, it is likely that a well capitalized firm will have lower volatility and suffer less in a crisis. How can we estimate this effect? STRUCTURAL GARCH

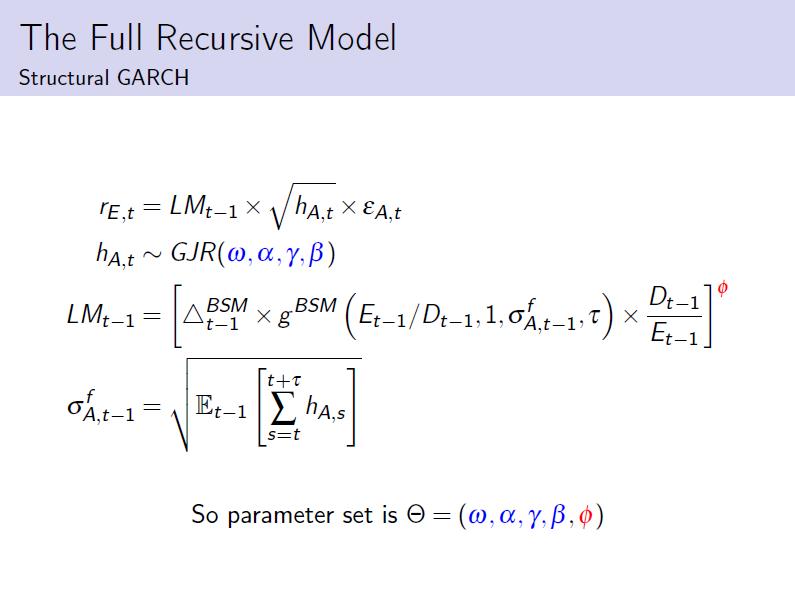

15 STRUCTURAL GARCH Engle and Siriwardane (2014) Recognizing that equity is a call option on the asset value of a firm, the moneyness of this option will affect its volatility. The moneyness of the equity option is a monotonic function of the debt to equity ratio. We estimate a model of equity prices by inferring a GJR-GARCH for asset values and a leverage multiplier.

16 THEORETICAL ANALYSIS

17

18

19

20

21

22 EMPIRICAL RESULTS

23

24

25

26

27 COMPUTE PRECAUTIONARY CAPITAL

28 BAC ON OCTOBER 1, 2008 How much capital is needed today to be 90% certain that capital will not fall below 2% if the global market falls by 40%?

29

30 WHAT THIS SHOWS Standard volatility models do not have a channel for leverage and therefore adding capital today does not reduce the volatility or beta. With Structural Garch, reducing leverage by increasing capital today will reduce risk in the future.

31

Rethinking Economics after the Crisis. Robert Engle, NYU Stern Policy Panel at ECB June 24,2014

Rethinking Economics after the Crisis Robert Engle, NYU Stern Policy Panel at ECB June 24,2014 HAS MACROECONOMICS CHANGED? I taught macroeconomics long ago. I taught IS- LM, Phillips curve and the FRB-MIT-Penn

Rethinking Economics after the Crisis Robert Engle, NYU Stern Policy Panel at ECB June 24,2014 HAS MACROECONOMICS CHANGED? I taught macroeconomics long ago. I taught IS- LM, Phillips curve and the FRB-MIT-Penn

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1,2 1 NYU Stern School of Business 2 U.S. Treasury, Office of Financial Research (OFR) WFA Annual Meeting: 6/16/2014

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1,2 1 NYU Stern School of Business 2 U.S. Treasury, Office of Financial Research (OFR) WFA Annual Meeting: 6/16/2014

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business University of Chicago: 11/25/2013 Leverage and Equity Volatility I Crisis highlighted

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business University of Chicago: 11/25/2013 Leverage and Equity Volatility I Crisis highlighted

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business MFM Macroeconomic Fragility Fall 2013 Meeting Leverage and Equity Volatility I Crisis

Structural GARCH: The Volatility-Leverage Connection Robert Engle 1 Emil Siriwardane 1 1 NYU Stern School of Business MFM Macroeconomic Fragility Fall 2013 Meeting Leverage and Equity Volatility I Crisis

Session 28 Systemic Risk of Banks & Insurance. Richard Nesbitt, CEO Global Risk Institute in Financial Services

Session 28 Systemic Risk of Banks & Insurance Richard Nesbitt, CEO Global Risk Institute in Financial Services Our Mission GRI is the premier risk management institute, that defines thought leadership

Session 28 Systemic Risk of Banks & Insurance Richard Nesbitt, CEO Global Risk Institute in Financial Services Our Mission GRI is the premier risk management institute, that defines thought leadership

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004 WHAT IS ARCH? Autoregressive Conditional Heteroskedasticity Predictive (conditional)

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004 WHAT IS ARCH? Autoregressive Conditional Heteroskedasticity Predictive (conditional)

V Time Varying Covariance and Correlation. Covariances and Correlations

V Time Varying Covariance and Correlation DEFINITION OF CORRELATIONS ARE THEY TIME VARYING? WHY DO WE NEED THEM? ONE FACTOR ARCH MODEL DYNAMIC CONDITIONAL CORRELATIONS ASSET ALLOCATION THE VALUE OF CORRELATION

V Time Varying Covariance and Correlation DEFINITION OF CORRELATIONS ARE THEY TIME VARYING? WHY DO WE NEED THEM? ONE FACTOR ARCH MODEL DYNAMIC CONDITIONAL CORRELATIONS ASSET ALLOCATION THE VALUE OF CORRELATION

9th Financial Risks International Forum

Calvet L., Czellar V.and C. Gouriéroux (2015) Structural Dynamic Analysis of Systematic Risk Duarte D., Lee K. and Scwenkler G. (2015) The Systemic E ects of Benchmarking University of Orléans March 21,

Calvet L., Czellar V.and C. Gouriéroux (2015) Structural Dynamic Analysis of Systematic Risk Duarte D., Lee K. and Scwenkler G. (2015) The Systemic E ects of Benchmarking University of Orléans March 21,

Capital Shortfall: A New Approach to Ranking and Regulating Systemic Risks

American Economic Review: Papers & Proceedings 2012, 102(3): 59 64 http://dx.doi.org/10.1257/aer.102.3.59 Capital Shortfall: A New Approach to Ranking and Regulating Systemic Risks By Viral Acharya, Robert

American Economic Review: Papers & Proceedings 2012, 102(3): 59 64 http://dx.doi.org/10.1257/aer.102.3.59 Capital Shortfall: A New Approach to Ranking and Regulating Systemic Risks By Viral Acharya, Robert

Towards a Financial Statement Based Approach to Modeling Systemic Risk in Insurance and Banking

Towards a Financial Statement Based Approach to Modeling Systemic Risk in Insurance and Banking Iyengar, Luo, Rajgopal*, Srinivasan, Venkatasubramanian, Wu and Zhang October 28, 2016 Workshop on Systemic

Towards a Financial Statement Based Approach to Modeling Systemic Risk in Insurance and Banking Iyengar, Luo, Rajgopal*, Srinivasan, Venkatasubramanian, Wu and Zhang October 28, 2016 Workshop on Systemic

Bank Rescues and Bailout Expectations: The Erosion of Market Discipline During the Financial Crisis

Bank Rescues and Bailout Expectations: The Erosion of Market Discipline During the Financial Crisis Florian Hett Goethe University Frankfurt Alexander Schmidt Deutsche Bundesbank & Goethe University Frankfurt

Bank Rescues and Bailout Expectations: The Erosion of Market Discipline During the Financial Crisis Florian Hett Goethe University Frankfurt Alexander Schmidt Deutsche Bundesbank & Goethe University Frankfurt

Risk Modeling: Lecture outline and projects. (updated Mar5-2012)

") Risk Modeling: Lecture outline and projects (updated Mar5-2012) Lecture 1 outline Intro to risk measures economic and regulatory capital what risk measurement is done and how is it used concept and role

Risk Modeling: Lecture outline and projects (updated Mar5-2012) Lecture 1 outline Intro to risk measures economic and regulatory capital what risk measurement is done and how is it used concept and role

Online Appendix: Structural GARCH: The Volatility-Leverage Connection

Online Appendix: Structural GARCH: The Volatility-Leverage Connection Robert Engle Emil Siriwardane Abstract In this appendix, we: (i) show that total equity volatility is well approximated by the leverage

Online Appendix: Structural GARCH: The Volatility-Leverage Connection Robert Engle Emil Siriwardane Abstract In this appendix, we: (i) show that total equity volatility is well approximated by the leverage

Systemic Risk: What is it? Are Insurance Firms Systemically Important?

Systemic Risk: What is it? Are Insurance Firms Systemically Important? Viral V Acharya (NYU-Stern, CEPR and NBER) What is systemic risk? Micro-prudential view: Contagion Failure of an entity leads to distress

Systemic Risk: What is it? Are Insurance Firms Systemically Important? Viral V Acharya (NYU-Stern, CEPR and NBER) What is systemic risk? Micro-prudential view: Contagion Failure of an entity leads to distress

EU fiscal rules, real-time uncertainty, and stabilization

EU fiscal rules, real-time uncertainty, and stabilization Tero Kuusi, ETLA Firstrun project meeting, Helsinki October 3, 2017 Real-time uncertainty affects the EU s key fiscal policy indicators EC s real-time

EU fiscal rules, real-time uncertainty, and stabilization Tero Kuusi, ETLA Firstrun project meeting, Helsinki October 3, 2017 Real-time uncertainty affects the EU s key fiscal policy indicators EC s real-time

Financial Times Series. Lecture 6

Financial Times Series Lecture 6 Extensions of the GARCH There are numerous extensions of the GARCH Among the more well known are EGARCH (Nelson 1991) and GJR (Glosten et al 1993) Both models allow for

Financial Times Series Lecture 6 Extensions of the GARCH There are numerous extensions of the GARCH Among the more well known are EGARCH (Nelson 1991) and GJR (Glosten et al 1993) Both models allow for

Market Risk Analysis Volume II. Practical Financial Econometrics

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Quantitative Investing with a Focus on Low-Risk Stocks

Topic 1: Quantitative Investing with a Focus on Low-Risk Stocks Jan Bauer According to Schmielewski and Stoyanov (2017), there are at least two ways how low-volatility portfolios can be constructed: The

Topic 1: Quantitative Investing with a Focus on Low-Risk Stocks Jan Bauer According to Schmielewski and Stoyanov (2017), there are at least two ways how low-volatility portfolios can be constructed: The

Bayesian Analysis of Systemic Risk Distributions

Bayesian Analysis of Systemic Risk Distributions Elena Goldman Department of Finance and Economics Lubin School of Business, Pace University New York, NY 10038 E-mail: egoldman@pace.edu Draft: 2016 Abstract

Bayesian Analysis of Systemic Risk Distributions Elena Goldman Department of Finance and Economics Lubin School of Business, Pace University New York, NY 10038 E-mail: egoldman@pace.edu Draft: 2016 Abstract

The VaR Measure. Chapter 8. Risk Management and Financial Institutions, Chapter 8, Copyright John C. Hull

The VaR Measure Chapter 8 Risk Management and Financial Institutions, Chapter 8, Copyright John C. Hull 2006 8.1 The Question Being Asked in VaR What loss level is such that we are X% confident it will

The VaR Measure Chapter 8 Risk Management and Financial Institutions, Chapter 8, Copyright John C. Hull 2006 8.1 The Question Being Asked in VaR What loss level is such that we are X% confident it will

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Lucas s Investment Tax Credit Example

Lucas s Investment Tax Credit Example The key idea: It is 1975 and you have just been hired by the Council of Economic Adviser s to estimate the effects of an investment tax credit. This policy is being

Lucas s Investment Tax Credit Example The key idea: It is 1975 and you have just been hired by the Council of Economic Adviser s to estimate the effects of an investment tax credit. This policy is being

22 nd Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank

Experience Next Generation Banking To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank

FRBSF Economic Letter

FRBSF Economic Letter 2019-06 February 19, 2019 Research from the Federal Reserve Bank of San Francisco Measuring Connectedness between the Largest Banks Galina Hale, Jose A. Lopez, and Shannon Sledz The

FRBSF Economic Letter 2019-06 February 19, 2019 Research from the Federal Reserve Bank of San Francisco Measuring Connectedness between the Largest Banks Galina Hale, Jose A. Lopez, and Shannon Sledz The

Markus K. Brunnermeier (joint with Tobias Adrian) Princeton University

Princeton University") Markus K. Brunnermeier (joint with Tobias Adrian) Princeton University 1 Current bank regulation 1. Risk of each bank in isolation Value at Risk 1% 2. Procyclical capital requirements 3. Focus on asset

Markus K. Brunnermeier (joint with Tobias Adrian) Princeton University 1 Current bank regulation 1. Risk of each bank in isolation Value at Risk 1% 2. Procyclical capital requirements 3. Focus on asset

Falling Short of Expectations? Stress-Testing the European Banking System

Falling Short of Expectations? Stress-Testing the European Banking System Viral V. Acharya (NYU Stern, CEPR and NBER) and Sascha Steffen (ESMT) January 2014 1 Falling Short of Expectations? Stress-Testing

Falling Short of Expectations? Stress-Testing the European Banking System Viral V. Acharya (NYU Stern, CEPR and NBER) and Sascha Steffen (ESMT) January 2014 1 Falling Short of Expectations? Stress-Testing

Does my beta look big in this?

Does my beta look big in this? Patrick Burns 15th July 2003 Abstract Simulations are performed which show the difficulty of actually achieving realized market neutrality. Results suggest that restrictions

Does my beta look big in this? Patrick Burns 15th July 2003 Abstract Simulations are performed which show the difficulty of actually achieving realized market neutrality. Results suggest that restrictions

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2012 Morningstar. All Rights Reserved. These materials are for information and/or illustration

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2012 Morningstar. All Rights Reserved. These materials are for information and/or illustration

Financial Econometrics Notes. Kevin Sheppard University of Oxford

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

The Capital and Loss Assessment Under Stress Scenarios (CLASS) Model

Model") The Capital and Loss Assessment Under Stress Scenarios (CLASS) Model Beverly Hirtle, Federal Reserve Bank of New York (joint work with James Vickery, Anna Kovner and Meru Bhanot) Federal Reserve in the

The Capital and Loss Assessment Under Stress Scenarios (CLASS) Model Beverly Hirtle, Federal Reserve Bank of New York (joint work with James Vickery, Anna Kovner and Meru Bhanot) Federal Reserve in the

A Practical Guide to Volatility Forecasting in a Crisis

A Practical Guide to Volatility Forecasting in a Crisis Christian Brownlees Robert Engle Bryan Kelly Volatility Institute @ NYU Stern Volatilities and Correlations in Stressed Markets April 3, 2009 BEK

A Practical Guide to Volatility Forecasting in a Crisis Christian Brownlees Robert Engle Bryan Kelly Volatility Institute @ NYU Stern Volatilities and Correlations in Stressed Markets April 3, 2009 BEK

Financial Times Series. Lecture 8

Financial Times Series Lecture 8 Nobel Prize Robert Engle got the Nobel Prize in Economics in 2003 for the ARCH model which he introduced in 1982 It turns out that in many applications there will be many

Financial Times Series Lecture 8 Nobel Prize Robert Engle got the Nobel Prize in Economics in 2003 for the ARCH model which he introduced in 1982 It turns out that in many applications there will be many

Structural GARCH: The Volatility-Leverage Connection

Structural GARCH: The Volatility-Leverage Connection The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters. Citation Accessed Citable

Structural GARCH: The Volatility-Leverage Connection The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters. Citation Accessed Citable

GARCH vs. Traditional Methods of Estimating Value-at-Risk (VaR) of the Philippine Bond Market

of the Philippine Bond Market") GARCH vs. Traditional Methods of Estimating Value-at-Risk (VaR) of the Philippine Bond Market INTRODUCTION Value-at-Risk (VaR) Value-at-Risk (VaR) summarizes the worst loss over a target horizon that

GARCH vs. Traditional Methods of Estimating Value-at-Risk (VaR) of the Philippine Bond Market INTRODUCTION Value-at-Risk (VaR) Value-at-Risk (VaR) summarizes the worst loss over a target horizon that

Portfolio Management

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

Investment Opportunity in BSE-SENSEX: A study based on asymmetric GARCH model

Investment Opportunity in BSE-SENSEX: A study based on asymmetric GARCH model Jatin Trivedi Associate Professor, Ph.D AMITY UNIVERSITY, Mumbai contact.tjatin@gmail.com Abstract This article aims to focus

Investment Opportunity in BSE-SENSEX: A study based on asymmetric GARCH model Jatin Trivedi Associate Professor, Ph.D AMITY UNIVERSITY, Mumbai contact.tjatin@gmail.com Abstract This article aims to focus

Measurement of Market Risk

Measurement of Market Risk Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements scenario analysis statistical analysis Scenario Analysis A scenario analysis measures

Measurement of Market Risk Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements scenario analysis statistical analysis Scenario Analysis A scenario analysis measures

Recent analysis of the leverage effect for the main index on the Warsaw Stock Exchange

Recent analysis of the leverage effect for the main index on the Warsaw Stock Exchange Krzysztof Drachal Abstract In this paper we examine four asymmetric GARCH type models and one (basic) symmetric GARCH

Recent analysis of the leverage effect for the main index on the Warsaw Stock Exchange Krzysztof Drachal Abstract In this paper we examine four asymmetric GARCH type models and one (basic) symmetric GARCH

Consultancy LLP. General Insurance Actuaries & Consultants

Consultancy LLP General Insurance Actuaries & Consultants Capital Allocation and Risk Measures in Practice Peter England, PhD GIRO 2005, Blackpool So you ve got an ICA model Group ICA Financial Statements

Consultancy LLP General Insurance Actuaries & Consultants Capital Allocation and Risk Measures in Practice Peter England, PhD GIRO 2005, Blackpool So you ve got an ICA model Group ICA Financial Statements

Structural GARCH: The Volatility-Leverage. Connection

Structural GARCH: The Volatility-Leverage Connection Robert Engle Emil Siriwardane August 5, 014 Abstract We propose a new model of volatility where financial leverage amplifies equity volatility by what

Structural GARCH: The Volatility-Leverage Connection Robert Engle Emil Siriwardane August 5, 014 Abstract We propose a new model of volatility where financial leverage amplifies equity volatility by what

Taxation and the Financial Sector (by Shackelford, Shaviro, and Slemrod) Daniel Shaviro NYU Law School

Daniel Shaviro NYU Law School") Taxation and the Financial Sector (by Shackelford, Shaviro, and Slemrod) Daniel Shaviro NYU Law School 1 Background A looming global catastrophe Can we measure marginal social harm? Is international cooperation

Taxation and the Financial Sector (by Shackelford, Shaviro, and Slemrod) Daniel Shaviro NYU Law School 1 Background A looming global catastrophe Can we measure marginal social harm? Is international cooperation

Investment & Actuarial Consulting, Controlling and Research.

Investment & Actuarial Consulting, Controlling and Research. www.ppcmetrics.ch Investment Consulting The Illiquidity Premium Revisited Can Pension Funds Access this? EPFIF PPCmetrics AG Dr. Diego Liechti,

Investment & Actuarial Consulting, Controlling and Research. www.ppcmetrics.ch Investment Consulting The Illiquidity Premium Revisited Can Pension Funds Access this? EPFIF PPCmetrics AG Dr. Diego Liechti,

A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR

A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR Sylvain Benoit, Gilbert Colletaz, Christophe Hurlin and Christophe Pérignon June 2012. Benoit, G.Colletaz, C. Hurlin,

A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR Sylvain Benoit, Gilbert Colletaz, Christophe Hurlin and Christophe Pérignon June 2012. Benoit, G.Colletaz, C. Hurlin,

Capital Management in commercial and investment banking Back to the drawing board? Rolf van den Heever. ABSA Capital

Capital Management in commercial and investment banking Back to the drawing board? Rolf van den Heever ABSA Capital Contents Objectives Background Existing regulatory and internal dispensation to meet

Capital Management in commercial and investment banking Back to the drawing board? Rolf van den Heever ABSA Capital Contents Objectives Background Existing regulatory and internal dispensation to meet

Analysis of the SRISK Measure and Its Application to the Canadian Banking and Insurance Industries

Analysis of the SRISK Measure and Its Application to the Canadian Banking and Insurance Industries Authors Thomas F. Coleman, University of Waterloo, Global Risk Institute Alex LaPlante, Global Risk Institute

Analysis of the SRISK Measure and Its Application to the Canadian Banking and Insurance Industries Authors Thomas F. Coleman, University of Waterloo, Global Risk Institute Alex LaPlante, Global Risk Institute

Modeling Exchange Rate Volatility using APARCH Models

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

Intraday Volatility Forecast in Australian Equity Market

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Intraday Volatility Forecast in Australian Equity Market Abhay K Singh, David

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Intraday Volatility Forecast in Australian Equity Market Abhay K Singh, David

IMPROVING the CAPITAL ADEQUACY

IMPROVING the MEASUREMENT OF CAPITAL ADEQUACY The future of economic capital and stress testing 1 Daniel Cope Andy McGee Over the better part of the last 20 years, banks have been developing credit risk

IMPROVING the MEASUREMENT OF CAPITAL ADEQUACY The future of economic capital and stress testing 1 Daniel Cope Andy McGee Over the better part of the last 20 years, banks have been developing credit risk

1. Introduction. 2. The Nature of the Insurance Business. Insurance Business Model Supports Long-term Investment

1. Introduction With almost 90 per cent, or $540 billion of their $615 billion Canadian assets, held in long-term investments, life and health insurers are one of the largest long-term institutional investors

1. Introduction With almost 90 per cent, or $540 billion of their $615 billion Canadian assets, held in long-term investments, life and health insurers are one of the largest long-term institutional investors

WORKING MACROPRUDENTIAL TOOLS

WORKING MACROPRUDENTIAL TOOLS Jesús Saurina Director. Financial Stability Department Banco de España Macro-prudential Regulatory Policies: The New Road to Financial Stability? Thirteenth Annual International

WORKING MACROPRUDENTIAL TOOLS Jesús Saurina Director. Financial Stability Department Banco de España Macro-prudential Regulatory Policies: The New Road to Financial Stability? Thirteenth Annual International

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation. March 28, 2014

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation Michael T. Kiley Jae W. Sim March 28, 2014 THEORETICAL FRAMEWORK Financial intermediation sector in

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation Michael T. Kiley Jae W. Sim March 28, 2014 THEORETICAL FRAMEWORK Financial intermediation sector in

Lecture 9: Markov and Regime

Lecture 9: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2017 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Lecture 9: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2017 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Robert Engle and Robert Ferstenberg Microstructure in Paris December 8, 2014

Robert Engle and Robert Ferstenberg Microstructure in Paris December 8, 2014 Is varying over time and over assets Is a powerful input to many financial decisions such as portfolio construction and trading

Robert Engle and Robert Ferstenberg Microstructure in Paris December 8, 2014 Is varying over time and over assets Is a powerful input to many financial decisions such as portfolio construction and trading

VOLATILITY. Time Varying Volatility

VOLATILITY Time Varying Volatility CONDITIONAL VOLATILITY IS THE STANDARD DEVIATION OF the unpredictable part of the series. We define the conditional variance as: 2 2 2 t E yt E yt Ft Ft E t Ft surprise

VOLATILITY Time Varying Volatility CONDITIONAL VOLATILITY IS THE STANDARD DEVIATION OF the unpredictable part of the series. We define the conditional variance as: 2 2 2 t E yt E yt Ft Ft E t Ft surprise

Commission Services Staff Working Document - possible further changes to the Capital Requirements Directive

Our Ref GTI/AW/NJJ/0809 Your Ref markt-h1 By email 4 September 2009 7th Floor, 338 Euston Road Regents Place London NW1 3BG T +44 207 391 9500 F +44 207 391 9501 www.gti.org Dear Sirs Commission Services

Our Ref GTI/AW/NJJ/0809 Your Ref markt-h1 By email 4 September 2009 7th Floor, 338 Euston Road Regents Place London NW1 3BG T +44 207 391 9500 F +44 207 391 9501 www.gti.org Dear Sirs Commission Services

Smile in the low moments

Smile in the low moments L. De Leo, T.-L. Dao, V. Vargas, S. Ciliberti, J.-P. Bouchaud 10 jan 2014 Outline 1 The Option Smile: statics A trading style The cumulant expansion A low-moment formula: the moneyness

Smile in the low moments L. De Leo, T.-L. Dao, V. Vargas, S. Ciliberti, J.-P. Bouchaud 10 jan 2014 Outline 1 The Option Smile: statics A trading style The cumulant expansion A low-moment formula: the moneyness

Viral V. Acharya (NYU Stern, NBER, CEPR) Sascha Steffen (ESMT)

Sascha Steffen (ESMT)") Benchmarking the European Central Bank's Asset Quality Review and Stress Test A Tale of Two Leverage Ratios Viral V. Acharya (NYU Stern, NBER, CEPR) Sascha Steffen (ESMT) November 214 Motivation In an

Benchmarking the European Central Bank's Asset Quality Review and Stress Test A Tale of Two Leverage Ratios Viral V. Acharya (NYU Stern, NBER, CEPR) Sascha Steffen (ESMT) November 214 Motivation In an

IFRS Seminar Series for Regulators GDLN 15 December 2010

REPARIS A REGIONAL PROGRAM Technical Update for Banking and Insurance Regulators Overview on Institutional Developments IFRS Seminar Series for Regulators GDLN 15 December 2010 THE ROAD TO EUROPE: PROGRAM

REPARIS A REGIONAL PROGRAM Technical Update for Banking and Insurance Regulators Overview on Institutional Developments IFRS Seminar Series for Regulators GDLN 15 December 2010 THE ROAD TO EUROPE: PROGRAM

Economic Scenario Generators

Economic Scenario Generators A regulator s perspective Falk Tschirschnitz, FINMA Bahnhofskolloquium Motivation FINMA has observed: Calibrating the interest rate model of choice has become increasingly

Economic Scenario Generators A regulator s perspective Falk Tschirschnitz, FINMA Bahnhofskolloquium Motivation FINMA has observed: Calibrating the interest rate model of choice has become increasingly

Distributed Computing in Finance: Case Model Calibration

Distributed Computing in Finance: Case Model Calibration Global Derivatives Trading & Risk Management 19 May 2010 Techila Technologies, Tampere University of Technology juho.kanniainen@techila.fi juho.kanniainen@tut.fi

Distributed Computing in Finance: Case Model Calibration Global Derivatives Trading & Risk Management 19 May 2010 Techila Technologies, Tampere University of Technology juho.kanniainen@techila.fi juho.kanniainen@tut.fi

International Finance. Investment Styles. Campbell R. Harvey. Duke University, NBER and Investment Strategy Advisor, Man Group, plc.

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period

Cahier de recherche/working Paper 13-13 Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period 2000-2012 David Ardia Lennart F. Hoogerheide Mai/May

Cahier de recherche/working Paper 13-13 Cross-Sectional Distribution of GARCH Coefficients across S&P 500 Constituents : Time-Variation over the Period 2000-2012 David Ardia Lennart F. Hoogerheide Mai/May

Tuomo Lampinen Silicon Cloud Technologies LLC

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Lecture 6: Non Normal Distributions

Lecture 6: Non Normal Distributions and their Uses in GARCH Modelling Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2015 Overview Non-normalities in (standardized) residuals from asset return

Lecture 6: Non Normal Distributions and their Uses in GARCH Modelling Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2015 Overview Non-normalities in (standardized) residuals from asset return

Lecture 8: Markov and Regime

Lecture 8: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2016 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Lecture 8: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2016 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Risk & Capital Management Under Basel III and IFRS 9 This course is presented in London on: May 2018

Risk & Capital Management Under Basel III and IFRS 9 This course is presented in London on: 14-17 May 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants Will: Understand

Risk & Capital Management Under Basel III and IFRS 9 This course is presented in London on: 14-17 May 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants Will: Understand

Web Appendix. Are the effects of monetary policy shocks big or small? Olivier Coibion

Web Appendix Are the effects of monetary policy shocks big or small? Olivier Coibion Appendix 1: Description of the Model-Averaging Procedure This section describes the model-averaging procedure used in

Web Appendix Are the effects of monetary policy shocks big or small? Olivier Coibion Appendix 1: Description of the Model-Averaging Procedure This section describes the model-averaging procedure used in

Financial Risk Management and Governance Beyond VaR. Prof. Hugues Pirotte

Financial Risk Management and Governance Beyond VaR Prof. Hugues Pirotte 2 VaR Attempt to provide a single number that summarizes the total risk in a portfolio. What loss level is such that we are X% confident

Financial Risk Management and Governance Beyond VaR Prof. Hugues Pirotte 2 VaR Attempt to provide a single number that summarizes the total risk in a portfolio. What loss level is such that we are X% confident

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

Compromise proposal on Omnibus II

Compromise proposal on Omnibus II On 25 November 2013 a compromise proposal on the Omnibus II Directive was published. This was based on a provisional agreement from the European Parliament, the European

Compromise proposal on Omnibus II On 25 November 2013 a compromise proposal on the Omnibus II Directive was published. This was based on a provisional agreement from the European Parliament, the European

SYSTEMATIC GLOBAL MACRO ( CTAs ):

:") G R A H M C A P I T A L M A N G E M N T G R A H A M C A P I T A L M A N A G E M E N T GC SYSTEMATIC GLOBAL MACRO ( CTAs ): PERFORMANCE, RISK, AND CORRELATION CHARACTERISTICS ROBERT E. MURRAY, CHIEF OPERATING

G R A H M C A P I T A L M A N G E M N T G R A H A M C A P I T A L M A N A G E M E N T GC SYSTEMATIC GLOBAL MACRO ( CTAs ): PERFORMANCE, RISK, AND CORRELATION CHARACTERISTICS ROBERT E. MURRAY, CHIEF OPERATING

An Empirical Study Regards the Bank Level Systemic Risk and Wealth Management Products in China. Tiange Ye

An Empirical Study Regards the Bank Level Systemic Risk and Wealth Management Products in China by Tiange Ye An honors thesis submitted in partial fulfillment of the requirements for the degree of Bachelor

An Empirical Study Regards the Bank Level Systemic Risk and Wealth Management Products in China by Tiange Ye An honors thesis submitted in partial fulfillment of the requirements for the degree of Bachelor

Financial Frictions and Employment during the Great Depression

Financial Frictions and Employment during the Great Depression Efraim Benmelech, Carola Frydman, and Dimitris Papanikolaou discussion by Toni Whited 216 NBER Summer Institute We learn two things. Firms

Financial Frictions and Employment during the Great Depression Efraim Benmelech, Carola Frydman, and Dimitris Papanikolaou discussion by Toni Whited 216 NBER Summer Institute We learn two things. Firms

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Financial Stress and Equilibrium Dynamics in Term Interbank Funding Markets

Financial Stress and Equilibrium Dynamics in Term Interbank Funding Markets Emre Yoldas a Zeynep Senyuz a a Federal Reserve Board June 17, 2017 North American Summer Meeting of the Econometric Society

Financial Stress and Equilibrium Dynamics in Term Interbank Funding Markets Emre Yoldas a Zeynep Senyuz a a Federal Reserve Board June 17, 2017 North American Summer Meeting of the Econometric Society

Rationale for keeping the cap on the substitutability category for the G-SIB scoring methodology

Rationale for keeping the cap on the substitutability category for the G-SIB scoring methodology November 2017 Francisco Covas +1.202.649.4605 francisco.covas@theclearinghouse.org I. Summary This memo

Rationale for keeping the cap on the substitutability category for the G-SIB scoring methodology November 2017 Francisco Covas +1.202.649.4605 francisco.covas@theclearinghouse.org I. Summary This memo

Valuing the GSEs Government Support

Valuing the GSEs Government Support Deborah Lucas, Sloan Distinguished Professor of Finance, Director MIT Golub Center for Finance and Policy and Shadow Open Market Committee Shadow Open Market Committee

Valuing the GSEs Government Support Deborah Lucas, Sloan Distinguished Professor of Finance, Director MIT Golub Center for Finance and Policy and Shadow Open Market Committee Shadow Open Market Committee

Assessing the Systemic Risk Contributions of Large and Complex Financial Institutions

Assessing the Systemic Risk Contributions of Large and Complex Financial Institutions Xin Huang, Hao Zhou and Haibin Zhu IMF Conference on Operationalizing Systemic Risk Monitoring May 27, 2010, Washington

Assessing the Systemic Risk Contributions of Large and Complex Financial Institutions Xin Huang, Hao Zhou and Haibin Zhu IMF Conference on Operationalizing Systemic Risk Monitoring May 27, 2010, Washington

Markus K. Brunnermeier

Markus K. Brunnermeier 1 Overview Two world views 1. No financial frictions sticky price 2. Financial sector + bubbles Role of the financial sector Leverage Maturity mismatch maturity rat race linkage

Markus K. Brunnermeier 1 Overview Two world views 1. No financial frictions sticky price 2. Financial sector + bubbles Role of the financial sector Leverage Maturity mismatch maturity rat race linkage

Traded Risk & Regulation

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

ARCH and GARCH models

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

Trend-following strategies for tail-risk hedging and alpha generation

Trend-following strategies for tail-risk hedging and alpha generation Artur Sepp FXCM Algo Summit 15 June 2018 Disclaimer I Trading forex/cfds on margin carries a high level of risk and may not be suitable

Trend-following strategies for tail-risk hedging and alpha generation Artur Sepp FXCM Algo Summit 15 June 2018 Disclaimer I Trading forex/cfds on margin carries a high level of risk and may not be suitable

Systemic Risk Measures

Econometric of in the Finance and Insurance Sectors Monica Billio, Mila Getmansky, Andrew W. Lo, Loriana Pelizzon Scuola Normale di Pisa March 29, 2011 Motivation Increased interconnectednessof financial

Econometric of in the Finance and Insurance Sectors Monica Billio, Mila Getmansky, Andrew W. Lo, Loriana Pelizzon Scuola Normale di Pisa March 29, 2011 Motivation Increased interconnectednessof financial

All Bank Risks are Idiosyncratic, Until They are Not: The Case of Operational Risk

All Bank Risks are Idiosyncratic, Until They are Not: The Case of Operational Risk 2018 Operational Risk Research Conference Allen N. Berger a, Filippo Curti b, Atanas Mihov b, and John Sedunov c a University

All Bank Risks are Idiosyncratic, Until They are Not: The Case of Operational Risk 2018 Operational Risk Research Conference Allen N. Berger a, Filippo Curti b, Atanas Mihov b, and John Sedunov c a University

FII Flows in Indian Equity Markets: Boon or Curse?

1 FII Flows in Indian Equity Markets: Boon or Curse? Viral V. Acharya, V. Ravi Anshuman, and K. Kiran Kumar 1 The principal risk facing India remains the inward spillover from global financial market volatility,

1 FII Flows in Indian Equity Markets: Boon or Curse? Viral V. Acharya, V. Ravi Anshuman, and K. Kiran Kumar 1 The principal risk facing India remains the inward spillover from global financial market volatility,

, SIFIs. ( Systemically Important Financial Institutions, SIFIs) Bernanke. (too interconnected to fail), Rajan (2009) (too systemic to fail),

Bernanke. (too interconnected to fail), Rajan (2009) (too systemic to fail),") : SIFIs SIFIs FSB : : F831 : A (IMF) (FSB) (BIS) ; ( Systemically Important Financial Institutions SIFIs) Bernanke (2009) (too interconnected to fail) Rajan (2009) (too systemic to fail) SIFIs : /2011.11

: SIFIs SIFIs FSB : : F831 : A (IMF) (FSB) (BIS) ; ( Systemically Important Financial Institutions SIFIs) Bernanke (2009) (too interconnected to fail) Rajan (2009) (too systemic to fail) SIFIs : /2011.11

Operationalizing the Selection and Application of Macroprudential Instruments

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

MFM Practitioner Module: Quantitative Risk Management. John Dodson. September 6, 2017

MFM Practitioner Module: Quantitative September 6, 2017 Course Fall sequence modules quantitative risk management Gary Hatfield fixed income securities Jason Vinar mortgage securities introductions Chong

MFM Practitioner Module: Quantitative September 6, 2017 Course Fall sequence modules quantitative risk management Gary Hatfield fixed income securities Jason Vinar mortgage securities introductions Chong

Graduated from Glasgow University in 2009: BSc with Honours in Mathematics and Statistics.

The statistical dilemma: Forecasting future losses for IFRS 9 under a benign economic environment, a trade off between statistical robustness and business need. Katie Cleary Introduction Presenter: Katie

The statistical dilemma: Forecasting future losses for IFRS 9 under a benign economic environment, a trade off between statistical robustness and business need. Katie Cleary Introduction Presenter: Katie

SYSTEMIC RISK AND THE PROSPECT FOR GLOBAL FINANCIAL TABILITY BY ROBERT F. ENGLE AND MATTHEW RICHARDSON NYU STERN SCHOOL OF BUSINESS

SYSTEMIC RISK AND THE PROSPECT FOR GLOBAL FINANCIAL TABILITY BY ROBERT F. ENGLE AND MATTHEW RICHARDSON NYU STERN SCHOOL OF BUSINESS HHOW DO WE IDENTIFY which countries and firms currently pose the greatest

SYSTEMIC RISK AND THE PROSPECT FOR GLOBAL FINANCIAL TABILITY BY ROBERT F. ENGLE AND MATTHEW RICHARDSON NYU STERN SCHOOL OF BUSINESS HHOW DO WE IDENTIFY which countries and firms currently pose the greatest

Structural credit risk models and systemic capital

Structural credit risk models and systemic capital Somnath Chatterjee CCBS, Bank of England November 7, 2013 Structural credit risk model Structural credit risk models are based on the notion that both

Structural credit risk models and systemic capital Somnath Chatterjee CCBS, Bank of England November 7, 2013 Structural credit risk model Structural credit risk models are based on the notion that both

Thoughts on Asset Allocation Global China Roundtable (GCR) Beijing CITICS CITADEL Asset Management.

Beijing CITICS CITADEL Asset Management.") Thoughts on Asset Allocation Global China Roundtable (GCR) Beijing CITICS CITADEL Asset Management www.bschool.nus.edu.sg/camri 1. The difficulty in predictions A real world example 2. Dynamic asset allocation

Thoughts on Asset Allocation Global China Roundtable (GCR) Beijing CITICS CITADEL Asset Management www.bschool.nus.edu.sg/camri 1. The difficulty in predictions A real world example 2. Dynamic asset allocation

Some lessons from six years of practical inflation targeting

Some lessons from six years of practical inflation targeting Lars E.O. Svensson Web: larseosvensson.se May 21, 2014 1 Some of my lessons for Sweden and the Riksbank: Outline 1. How should the mandate should

Some lessons from six years of practical inflation targeting Lars E.O. Svensson Web: larseosvensson.se May 21, 2014 1 Some of my lessons for Sweden and the Riksbank: Outline 1. How should the mandate should

Would Conventional Regulatory requirements be. Maher Hasan

Capital Management in Islamic Finance: Would Conventional Regulatory requirements be Appropriate for Islamic Finance? Maher Hasan IMF Global Islamic Finance Forum, Regulators Forum, KL October 26, 2010

Capital Management in Islamic Finance: Would Conventional Regulatory requirements be Appropriate for Islamic Finance? Maher Hasan IMF Global Islamic Finance Forum, Regulators Forum, KL October 26, 2010

Bank Capital Adequacy Standards: CRD IV & Europe s transition to Basel III

Professor CHRISTOS HADJIEMMANUIL University of Piraeus & London School of Economics Bank Capital Adequacy Standards: CRD IV & Europe s transition to Basel III Annual Conference of the Greek Society of

Professor CHRISTOS HADJIEMMANUIL University of Piraeus & London School of Economics Bank Capital Adequacy Standards: CRD IV & Europe s transition to Basel III Annual Conference of the Greek Society of

Risk & Capital Management Under Basel III and IFRS 9 This course can also be presented in-house for your company or via live on-line webinar

Risk & Capital Management Under Basel III and IFRS 9 This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course

Risk & Capital Management Under Basel III and IFRS 9 This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course

Are BRIC countries currencies to play. a dominant role in the system? A Brazilian perception

Are BRIC countries currencies to play The Policy of International Reserves a dominant role in the system? Accumulation: Lessons from the A Brazilian perception Crisis (Brazil s Perspective) Carlos Hamilton

Are BRIC countries currencies to play The Policy of International Reserves a dominant role in the system? Accumulation: Lessons from the A Brazilian perception Crisis (Brazil s Perspective) Carlos Hamilton

Liquidity Risk Management for Portfolios

Liquidity Risk Management for Portfolios IPARM China Summit 2011 Shanghai, China November 30, 2011 Joseph Cherian Professor of Finance (Practice) Director, Centre for Asset Management Research & Investments

Liquidity Risk Management for Portfolios IPARM China Summit 2011 Shanghai, China November 30, 2011 Joseph Cherian Professor of Finance (Practice) Director, Centre for Asset Management Research & Investments

UNDERSTANDING THE MARKET UNCERTAINTIES. Andrea Loddo Associate Director, Financial Risk Advisory

UNDERSTANDING THE MARKET UNCERTAINTIES Andrea Loddo Associate Director, Financial Risk Advisory Executive Summary Markets are unpredictable: the implications on risk management Rethinking risk management:

UNDERSTANDING THE MARKET UNCERTAINTIES Andrea Loddo Associate Director, Financial Risk Advisory Executive Summary Markets are unpredictable: the implications on risk management Rethinking risk management: