Balance Sheet and Income Statement of a Commercial Bank

|

|

|

- Roger Holmes

- 6 years ago

- Views:

Transcription

1 Balance Sheet and Income Statement of a Commercial Bank Economics of Financial Intermediation March 7, 2017

2 Financial information on commercial banks is reported in two basic documents: The report of condition (or balance sheet) presents financial information on a banks assets, liabilities, and equity capital. The balance sheet reports a banks condition at a single point in time. The report of income (or the income statement) presents the major categories of revenues and expenses (or costs) and the net profit or loss for a bank over a period of time. (off balance activities produce income or losses)

3 Assets Liabilities Capital Off-Balance-Sheet assets and liabilities Perfomance Analysis

4 Assets A banks assets are grouped into four major subcategories: 1 cash and due from depository institutions, 2 investment securities, 3 loans and leases, 4 other assets (i.e., intangible assets, goodwill, badwill). Investment securities and loans and leases are the banks earning assets.

5 Investment securities: Federal Funds and repos (repurchase agreements) U.S. Treasury and agency securities MBS/ABS Debt/Equity securities Investment securities are highly liquid, have low default risk and are usually traded in secondary markets. The Investment securities may have different maturity: Short-maturity < 1 year Long-maturity > 1 year

6 Loans and leases: Commercial and Industrial loans, Loans secured by real estate (maturity more than 20 years), Individual or consumer loans, Other loans, Leases (if the bank is owner of a physical asset, it allows to a customer to use the asset in return the bank receives a periodic lease payment).

7 Liabilities A banks liabilities consist of various types of deposit accounts and other borrowings used to fund the investments and loans on the asset side of the balance sheet. Deposits: Demand Deposit or Transaction deposit (no bear interest) NOW accounts: Negotiable order of withdrawal accounts are like demand deposits but pay interest when a minimum balance is maintained. MMDAs (Money market deposit account): similar to NOW accounts but negotiable in a secondary markets or interbank markets. MMDAs pay higher interest rate with respect to the NOW accounts. Other savings deposits: All savings account with respect to MMDAs.

8 The major class of time deposits are: Retail CDs: Time deposits with a face value below 100,000. Wholesale CDs: Time deposits with a face value of 100,000 or more. The CDs are negotiable instruments. Others source of funds: Borrowed Funds, Other liabilities.

9 Some banks separate core deposits from purchased funds on their balance sheets. The stable deposits of the bank are referred to as core deposits. These deposits are not expected to be withdrawn over short periods of time and are therefore a more permanent source of funding for the bank. Core deposits are also the cheapest funds banks can use to finance their assets. Because they are both a stable and low-cost source of funding, core deposits are the most frequently used source of funding by commercial banks. Core deposits generally are defined as demand deposits, NOW accounts, MMDAs, other savings accounts, and retail CDs.

10 Purchased funds are more expensive and/or volatile sources of funds because they are highly rate sensitive, these funds are more likely to beimmediately withdrawn or replaced as rates on competitive instruments change. Further, interest rates on these funds, at any point in time, are generally higher than rates on core deposits. Purchased funds are generally defined as brokered deposits, wholesale CDs, deposits at foreign offices, fed funds purchased, RPs.

11 Equity Capital The banks equity capital (item 45) consists mainly of preferred (item 41) and common (item 42) stock (listed at par value), surplus or additional paid-in capital (item 43), and retained earnings (item 44). Regulations require banks to hold a minimum level of equity capital to act as a buffer against losses from their on- and off-balance-sheet assets.

12

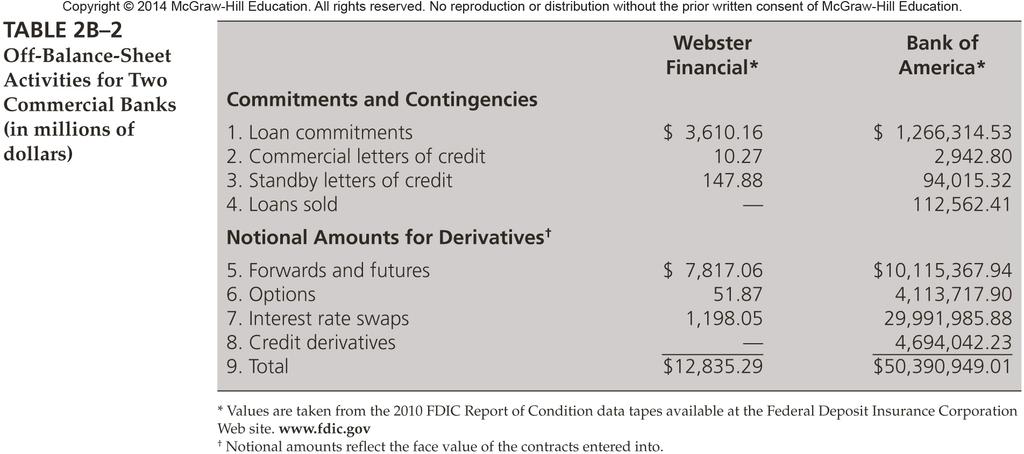

13 Off-Balance-Sheet assets and liabilities Loan commitments: Contractual commitment to loan to a firm a certain maximum amount at given interest rate terms. (it is possible that the bank foresees a (provision) commitment fee: it charged on the unused component of a loan commitment.) Commercial Letters of Credit and Standby Letters of Credit: - Commercial Letters of Credit (LCs): Contingent guarantees sold by an FI to underwrite the trade or commercial performance of the buyers of the guarantees. - Standby Letters of Credit (SLCs): Guarantees issued to cover contingencies that are potentially more severe and less predictable than contingencies covered under trade-related or commercial letters of credit (credit enhancements facilities the borrowing in the commercial paper markets).

14 Off-Balance-Sheet assets and liabilities Con t In economic terms, the depository institution that sells LCs and SLCs is selling insurance against the frequency or severity of some future event occurring. Further, like the different lines of insurance sold by property casualty insurers, LC (low-medium risk) and SLC (high risk) contracts differ as to the severity and frequency of their risk exposures.

15 Off-Balance-Sheet assets and liabilities Con t Loan sold: Loans originated by the bank and then sold to other investors that can be returned to the originating institution (i.e. MBS, ABS). Derivative securities: Futures, forward, swap, and option positions taken by the FI for hedging or other purposes.

16 Assets Liabilities Capital Off-Balance-Sheet assets and liabilities Perfomance Analysis

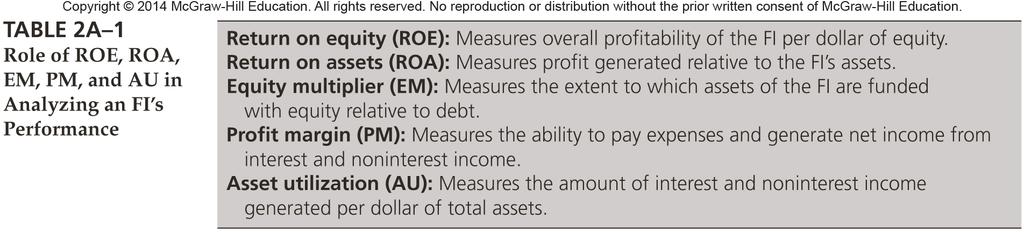

17 RATIO = DUPONT ANALYSIS ROE (Return on Equity) = Net Income Total equity capital Total assets EM (Equity Multiplier) = Total equity capital measures the dollar value of assets funded with each dollar of equity capital ROA (Return on Assets) = ROE = Net Income Total assets ROE = ROA*EM Net Income Total Assets Total assets Total equity capital

18 RETURN ON ASSETS COMPONENTS PM (Profit Margin) = (banks ability to control expenses) Net Income Total Operating Income Total Operating Income AU (Asset Utilization) = Total Assets (banks ability to generate income from its assets) ROA = Net Income Total Operating Income Total Operating Income Total Assets ROA = PM*AU

19

20 PROFIT MARGIN COMPONENTS INTEREST EXPENSE RATIO = NONINTEREST EXPENSE RATIO = Interest expense Total operating income Noninterest expense Total operating income NON PERFORMING LOANS RATIO = Non performing loans Total loans PROVISION FOR LOAN LOSS RATIO = Provision for loan losses Total operating income Income taxes TAX RATIO = Total operating income These ratios measure the proportion of total operating income that

21 ASSET UTILIZATION COMPONETS ASSET UTILIZATION RATIO = Total operating income Total assets = Interest income ratio + noninterest income ratio INTEREST INCOME RATIO = Interest Income Total assets NONINTEREST INCOME RATIO = Noninterest Income Total assets

22 The interest income and noninterest income ratios are not necessarily independent. For example, the banks ability to generate loans affects both interest income and, through fees and service charges, noninterest income. High values for these ratios signify the efficient use of bank resources to generate income and are thus generally positive for the bank. But some problematic situations that result in high ratio values could exist.

23 For example, a bank that replaces low-risk, low-return loans with high-risk, high-return loans will experience an increase in its interest income ratio. However, high-risk loans have a higher default probability, which could result in the ultimate loss of both interest and principal payments. Further breakdown of these ratios is therefore a valuable tool in the financial performance evaluation process.

24 Some Balance sheet indicators Loans to Total Assets = Deposits to Total Assets = Loans to Deposits = Loans Total Assets Deposits Total Assets Loans Deposit

25 OTHERS RATIO NET INTEREST MARGIN = Net interest income Earning assets = (Interest Income - Interest expenses) (Investments securities + Net loans and leases) Generally, the higher this ratio, the better. Suppose, however, that the preceding scenario (replacement of low-risk, low-return loans with high-risk, high-return loans) is the reason for the increase. This situation can increase risk for the bank. It highlights the fact that looking at returns without looking at risk can be misleading and potentially dangerous in terms of bank solvency and long-run profitability.

26 OTHERS RATIO SPREAD = Interest income Earning assets Interest expense Interest-bearing liabilities The higher the spread, the more profitable the bank, but again, the source of a high spread and the potential risk implications should be considered.

27 OTHERS RATIO OVERHEAD EFFICIENCY = Noninterest income Noninterest expenses In general, the higher this ratio, the better. However, because of the high levels of noninterest expense relative to noninterest income, overhead efficiency is rarely higher than 1 (or in percentage terms, 100 percent). Further, low operating expenses (and thus low noninterest expenses) can also indicate increased risk if the institution is not investing in the most efficient technology or its back office systems are poorly supported.

Bank Financial Statements

5-1 Bank Financial Statements Report of Condition Balance Sheet Report of Income Income Statement Key Items on Bank Financial Statements 5-3 Report of Condition The Balance Sheet of a Bank Showing its

5-1 Bank Financial Statements Report of Condition Balance Sheet Report of Income Income Statement Key Items on Bank Financial Statements 5-3 Report of Condition The Balance Sheet of a Bank Showing its

ANALYZING BANK PERFORMANCE

ANALYZING BANK PERFORMANCE Key Topics An Overview of the Balance Sheets and Income Statements of Banks The Balance Sheet or Report of Condition Asset Items Liability Items Components of the Income Statement:

ANALYZING BANK PERFORMANCE Key Topics An Overview of the Balance Sheets and Income Statements of Banks The Balance Sheet or Report of Condition Asset Items Liability Items Components of the Income Statement:

Chapter 2 Analyzing Bank Performance

Chapter 2 Analyzing Bank Performance Balance Sheet It is a statement of financial position listing assets owned, liabilities owed, and owner s equity as of a specific date. Assets = Liabilities + Equity.

Chapter 2 Analyzing Bank Performance Balance Sheet It is a statement of financial position listing assets owned, liabilities owed, and owner s equity as of a specific date. Assets = Liabilities + Equity.

Bank Financial Analysis. Georgia Bankers Association

Bank Financial Analysis Georgia Bankers Association Learning Objectives Recognize the basic balance sheet accounts and income statement components and understand their relationship Grasp the ROE model

Bank Financial Analysis Georgia Bankers Association Learning Objectives Recognize the basic balance sheet accounts and income statement components and understand their relationship Grasp the ROE model

2. If a bank meets a net deposit drain by borrowing money in the fed funds market it is using purchased liquidity.

Chapter 21: Managing Liquidity Risk on the Balance Sheet True/False 1. Large banks tend to rely more on purchased liquidity and small banks tend to rely more on stored liquidity. 2. If a bank meets a net

Chapter 21: Managing Liquidity Risk on the Balance Sheet True/False 1. Large banks tend to rely more on purchased liquidity and small banks tend to rely more on stored liquidity. 2. If a bank meets a net

Chapter 9. Banks and Bank Management. Depository Institutions: The Big Questions

Chapter 9 Banks and Bank Management Depository Institutions: The Big Questions Where do commercial banks get their funds and what do they do with them? How do commercial banks manage their balance sheets?

Chapter 9 Banks and Bank Management Depository Institutions: The Big Questions Where do commercial banks get their funds and what do they do with them? How do commercial banks manage their balance sheets?

Bank Assets BANK FINANCIAL STATEMENTS. The Balance Sheet Conceptually. Bank Securities. Types of Loans. Balance Sheet Deposits. Cash & Due from Banks

BANK FINANCIAL STEMENTS Bank Assets Cash and due from banks Vault cash, deposits held at the Fed and other financial institutions, and cash items in the process of collection Investment Securities Bonds,

BANK FINANCIAL STEMENTS Bank Assets Cash and due from banks Vault cash, deposits held at the Fed and other financial institutions, and cash items in the process of collection Investment Securities Bonds,

The Du Pont System of the Analysis of Return Ratios Applied to Sears, Roebuck & Co.

The Du Pont System of the Analysis of Return Ratios Applied to Sears, Roebuck & Co. Return on Assets (ROA) 1 Return on Equity (ROE) 2 Calculation for fiscal year 2003 Calculation for fiscal year 2003 (

The Du Pont System of the Analysis of Return Ratios Applied to Sears, Roebuck & Co. Return on Assets (ROA) 1 Return on Equity (ROE) 2 Calculation for fiscal year 2003 Calculation for fiscal year 2003 (

Bank Management, 6th edition. Timothy W. Koch and S. Scott MacDonald Copyright 2006 by South-Western, a division of Thomson Learning

Bank Management, 6th edition. Timothy W. Koch and S. Scott MacDonald Copyright 2006 by South-Western, a division of Thomson Learning ANALYZING BANK PERFORMANCE: USING THE UBPR Chapter 2 William Chittenden

Bank Management, 6th edition. Timothy W. Koch and S. Scott MacDonald Copyright 2006 by South-Western, a division of Thomson Learning ANALYZING BANK PERFORMANCE: USING THE UBPR Chapter 2 William Chittenden

Managing Risk off the Balance Sheet with Derivative Securities

Managing Risk off the Balance Sheet Managing Risk off the Balance Sheet with Derivative Securities Managers are increasingly turning to off-balance-sheet (OBS) instruments such as forwards, futures, options,

Managing Risk off the Balance Sheet Managing Risk off the Balance Sheet with Derivative Securities Managers are increasingly turning to off-balance-sheet (OBS) instruments such as forwards, futures, options,

Ch 13 Off-balance sheet risk Overview

Ch 13 Off-balance sheet risk Overview This chapter discusses the risks associated with offbalance-sheet activities. OBS activities are often designed to reduce risks through hedging with derivative securities

Ch 13 Off-balance sheet risk Overview This chapter discusses the risks associated with offbalance-sheet activities. OBS activities are often designed to reduce risks through hedging with derivative securities

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended June 30, 2016

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2016 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy... 2

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2016 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy... 2

This lecture examines how banking is conducted to earn the highest possible profit.

Banking and the Management of Financial Institutions This lecture examines how banking is conducted to earn the highest possible profit. The Bank Balance Sheet A. The basic bank balance sheet B. Assets

Banking and the Management of Financial Institutions This lecture examines how banking is conducted to earn the highest possible profit. The Bank Balance Sheet A. The basic bank balance sheet B. Assets

Temporary Liquidity Guarantee Program Frequently Asked Questions

FDIC: Temporary Liquidity Guarantee Program Frequently Asked Questions 1 of 22 3/9/2009 10:56 AM Home > Regulation & Examinations > Resources for Bank Officers & Directors > Temporary Liquidity Guarantee

FDIC: Temporary Liquidity Guarantee Program Frequently Asked Questions 1 of 22 3/9/2009 10:56 AM Home > Regulation & Examinations > Resources for Bank Officers & Directors > Temporary Liquidity Guarantee

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended June 30, 2017

Basel III Pillar 3 Disclosures Report For the Quarterly Period Ended June 30, 2017 BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2017 Table of Contents Page 1 Morgan Stanley

Basel III Pillar 3 Disclosures Report For the Quarterly Period Ended June 30, 2017 BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2017 Table of Contents Page 1 Morgan Stanley

E RNIN I GS G S R EL E EA E SE S E F IN I ANCIA I L S U S PP P L P EM E E M N E T FIRST QUARTER

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2011 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Statements of Income 4 Consolidated Balance Sheets 5 Condensed

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2011 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Statements of Income 4 Consolidated Balance Sheets 5 Condensed

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended September 30, 2016

Basel III Pillar 3 Disclosures Report For the Quarterly Period Ended September 30, 2016 BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended September 30, 2016 Table of Contents Page 1

Basel III Pillar 3 Disclosures Report For the Quarterly Period Ended September 30, 2016 BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended September 30, 2016 Table of Contents Page 1

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

Mc Graw Hill Education

Financial Institutions Management A Risk Management Approach Ninth Edition Anthony Saunders John M. Schiff Professor of Finance Solomon Center Stern School of Business New York University Marcia Millon

Financial Institutions Management A Risk Management Approach Ninth Edition Anthony Saunders John M. Schiff Professor of Finance Solomon Center Stern School of Business New York University Marcia Millon

Chapter 10. Banking and the Management of Financial Institutions

Chapter 10 Banking and the Management of Financial Institutions The Bank Balance Sheet Liabilities Checkable deposits Nontransaction deposits Borrowings Bank capital 10-2 The Bank Balance Sheet (cont d)

Chapter 10 Banking and the Management of Financial Institutions The Bank Balance Sheet Liabilities Checkable deposits Nontransaction deposits Borrowings Bank capital 10-2 The Bank Balance Sheet (cont d)

Economics 435 The Financial System (10/25/2017) Instructor: Prof. Menzie Chinn UW Madison Fall 2017

Instructor: Prof. Menzie Chinn UW Madison Fall 2017") Economics 435 The Financial System (10/25/2017) Instructor: Prof. Menzie Chinn UW Madison Fall 2017 Introduction Most people use the word bank to describe a depository institution. There are depository

Economics 435 The Financial System (10/25/2017) Instructor: Prof. Menzie Chinn UW Madison Fall 2017 Introduction Most people use the word bank to describe a depository institution. There are depository

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended December 31, 2015

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

Chapter 6. Managing Liabilities

Chapter 6 Managing Liabilities Composition of Bank Liabilities Different types of liabilities Interest-bearing and non-interest-bearing Transaction accounts: Low explicit interest rates High non-interest

Chapter 6 Managing Liabilities Composition of Bank Liabilities Different types of liabilities Interest-bearing and non-interest-bearing Transaction accounts: Low explicit interest rates High non-interest

The Financial System. Instructor: Prof. Menzie Chinn UW Madison

Economics 435 The Financial System (10/23/12) Instructor: Prof. Menzie Chinn UW Madison Fall 2012 Introduction Most people p use the word bank to describe a depository institution. There are depository

Economics 435 The Financial System (10/23/12) Instructor: Prof. Menzie Chinn UW Madison Fall 2012 Introduction Most people p use the word bank to describe a depository institution. There are depository

CHAPTER 5 MEASURING AND EVALUATING THE PERFORMANCE OF BANKS AND THEIR PRINCIPAL COMPETITORS

CHAPTER 5 MEASURING AND EVALUATING THE PERFORMANCE OF BANKS AND THEIR PRINCIPAL COMPETITORS Goal of This Chapter: The purpose of this chapter is to discover what analytical tools can be applied to a bank

CHAPTER 5 MEASURING AND EVALUATING THE PERFORMANCE OF BANKS AND THEIR PRINCIPAL COMPETITORS Goal of This Chapter: The purpose of this chapter is to discover what analytical tools can be applied to a bank

Depository Institutions

Economics of Financial Intermediation March 2, 2017 Historical trends Historically, Commericial banks have operated as more diversified institutions, having a large concentration of residental mortgage

Economics of Financial Intermediation March 2, 2017 Historical trends Historically, Commericial banks have operated as more diversified institutions, having a large concentration of residental mortgage

PRO FORMA COMBINED FINANCIAL SUPPLEMENT FIRST QUARTER 2005

PRO FORMA COMBINED FINANCIAL SUPPLEMENT FIRST QUARTER 2005 TABLE OF CONTENTS Page Consolidated Results Financial Highlights 3 Statements of Income - Reported Basis 4 Consolidated Balance Sheets 5 Condensed

PRO FORMA COMBINED FINANCIAL SUPPLEMENT FIRST QUARTER 2005 TABLE OF CONTENTS Page Consolidated Results Financial Highlights 3 Statements of Income - Reported Basis 4 Consolidated Balance Sheets 5 Condensed

Chapter 9. Banking and the Management of Financial Institutions

Chapter 9 Banking and the Management of Financial Institutions Copyright 2007 Pearson Addison-Wesley. All rights reserved. 9-2 Basic Banking Cash Deposit First National Bank First National Bank Assets

Chapter 9 Banking and the Management of Financial Institutions Copyright 2007 Pearson Addison-Wesley. All rights reserved. 9-2 Basic Banking Cash Deposit First National Bank First National Bank Assets

Georgia Banking School

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

PA Policy Responses to the Great Recession Lecture 6 (9/22/09) Instructor: Menzie Chinn Fall 2009

Instructor: Menzie Chinn Fall 2009") PA974-001 Policy Responses to the Great Recession Lecture 6 (9/22/09) Instructor: Menzie Chinn Fall 2009 Outline Interpreting balance sheets, and Managing liquidity risk, Asset Management, Capital Adequacy

PA974-001 Policy Responses to the Great Recession Lecture 6 (9/22/09) Instructor: Menzie Chinn Fall 2009 Outline Interpreting balance sheets, and Managing liquidity risk, Asset Management, Capital Adequacy

BBI2353 Commercial Bank Management Prepared by Dr Khairul Anuar

1 BBI2353 Commercial Bank Management Prepared by Dr Khairul Anuar L3: Liquidity and Reserves Management: Strategies and Policies www.lecturenotes.wordpress.com 11-2 2 Key Topics Sources of Demand for and

1 BBI2353 Commercial Bank Management Prepared by Dr Khairul Anuar L3: Liquidity and Reserves Management: Strategies and Policies www.lecturenotes.wordpress.com 11-2 2 Key Topics Sources of Demand for and

Chapter 6 : Money Markets

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

EARNINGS RELEASE FINANCIAL SUPPLEMENT THIRD QUARTER 2010

EARNINGS RELEASE FINANCIAL SUPPLEMENT THIRD QUARTER 2010 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Statements of Income 4 Consolidated Balance Sheets 5 Condensed

EARNINGS RELEASE FINANCIAL SUPPLEMENT THIRD QUARTER 2010 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Statements of Income 4 Consolidated Balance Sheets 5 Condensed

Basel III Standardized Approach Disclosures

Disclosures September 30, 2016 Table of Contents Introduction 1 Background 1 Overview 1 Disclosure Matrix 3 Components of Capital 10 Capital Adequacy 10 Standardized Risk-Weighted Assets 11 Capital Ratios

Disclosures September 30, 2016 Table of Contents Introduction 1 Background 1 Overview 1 Disclosure Matrix 3 Components of Capital 10 Capital Adequacy 10 Standardized Risk-Weighted Assets 11 Capital Ratios

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2009

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2009 TABLE OF CONTENTS Page Consolidated Results Consolidated Financial Highlights 2 Statements of Income 3 Consolidated Balance Sheets 4 Condensed Average

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2009 TABLE OF CONTENTS Page Consolidated Results Consolidated Financial Highlights 2 Statements of Income 3 Consolidated Balance Sheets 4 Condensed Average

Topics in Banking: Theory and Practice Lecture Notes 1

Topics in Banking: Theory and Practice Lecture Notes 1 Academic Program: Master in Financial Economics (Research track) Semester: Spring 2010/11 Instructor: Dr. Nikolaos I. Papanikolaou The financial system

Topics in Banking: Theory and Practice Lecture Notes 1 Academic Program: Master in Financial Economics (Research track) Semester: Spring 2010/11 Instructor: Dr. Nikolaos I. Papanikolaou The financial system

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN. Money, Banking, and the Financial System Pearson Education, Inc. Publishing as Prentice Hall

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Money, Banking, and the Financial System 2012 Pearson Education, Inc. Publishing as Prentice Hall C H A P T E R 10 The Economics of Banking LEARNING OBJECTIVES

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Money, Banking, and the Financial System 2012 Pearson Education, Inc. Publishing as Prentice Hall C H A P T E R 10 The Economics of Banking LEARNING OBJECTIVES

EARNINGS RELEASE FINANCIAL SUPPLEMENT SECOND QUARTER 2010

EARNINGS RELEASE FINANCIAL SUPPLEMENT SECOND QUARTER 2010 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Statements of Income 4 Consolidated Balance Sheets 5 Condensed

EARNINGS RELEASE FINANCIAL SUPPLEMENT SECOND QUARTER 2010 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Statements of Income 4 Consolidated Balance Sheets 5 Condensed

Financial Data KEY FINANCIAL INDICATORS. Key Financial Indicators

Financial Data KEY FINANCIAL INDICATORS Key Financial Indicators Ordinary income 1,897,281 1,968,987 Operating profit (before provision for general reserve for possible loan losses) 354,087 385,897 Net

Financial Data KEY FINANCIAL INDICATORS Key Financial Indicators Ordinary income 1,897,281 1,968,987 Operating profit (before provision for general reserve for possible loan losses) 354,087 385,897 Net

Measuring and Evaluating Bank Performance

Measuring and Evaluating Bank Performance The purpose of this session is to discover what analytical tools can be applied to a bank s financial statements so that management and the public can identify

Measuring and Evaluating Bank Performance The purpose of this session is to discover what analytical tools can be applied to a bank s financial statements so that management and the public can identify

Supplementary Financial Information Q For the period ended January 31, 2011 (UNAUDITED) For further information, please contact:

For further information, please contact:") Supplementary Financial Information Q 0 For the period ended January, 0 (UNAUDITED) For further information, please contact: Josie Merenda Vice-President & Head, Investor Relations (46) 955-780 josie.merenda@rbc.com

Supplementary Financial Information Q 0 For the period ended January, 0 (UNAUDITED) For further information, please contact: Josie Merenda Vice-President & Head, Investor Relations (46) 955-780 josie.merenda@rbc.com

McGraw-Hill/Irwin Bank Management and Financial Services, 7/e 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Funding the Bank Key Issues Depository Institutions Are Faced With: 12-2 1. Where can funds be raised at lowest possible cost? 2. How can management ensure that there are enough deposits to support lending

Funding the Bank Key Issues Depository Institutions Are Faced With: 12-2 1. Where can funds be raised at lowest possible cost? 2. How can management ensure that there are enough deposits to support lending

Henry Castillo Alex Santana Rich Molloy Patricia Maone Mike Tursi

Henry Castillo Alex Santana Rich Molloy Patricia Maone Mike Tursi August 2, 2001 Purpose and General Instructions Henry Castillo Purpose of the Call Report The FFIEC 002 is used to: Provide information

Henry Castillo Alex Santana Rich Molloy Patricia Maone Mike Tursi August 2, 2001 Purpose and General Instructions Henry Castillo Purpose of the Call Report The FFIEC 002 is used to: Provide information

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

4Q15 Quarterly Supplement

4Q15 Quarterly Supplement January 15, 2016 These results do not reflect the impact of the agreement in principle Wells Fargo & Company reached with the United States government on February 1, 2016 to pay

4Q15 Quarterly Supplement January 15, 2016 These results do not reflect the impact of the agreement in principle Wells Fargo & Company reached with the United States government on February 1, 2016 to pay

01jul jan jul jan jul jan2010. Panel B. Small Banks. 01jul jan jul jan jul jan2010

ONLINE APPENDIX Figure A1. Cumulative Growth of Non-deposit Liabilities These two figures plot the cumulative growth of key balance sheet non-deposit liabilities at the weekly frequency from July 2007

ONLINE APPENDIX Figure A1. Cumulative Growth of Non-deposit Liabilities These two figures plot the cumulative growth of key balance sheet non-deposit liabilities at the weekly frequency from July 2007

McGraw-Hill/Irwin Bank Management and Financial Services, 7/e 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Bank Reserves Management Legal Reserves Legal Reserves Those assets that law and central bank regulation say must be held during a particular time period The current system of accounting for legal reserves

Bank Reserves Management Legal Reserves Legal Reserves Those assets that law and central bank regulation say must be held during a particular time period The current system of accounting for legal reserves

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Commercial paper collateralized by a pool of loans, leases, receivables, or structured credit products.

Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset guarantee Asset Protection Scheme Asset purchase Assets under management (AUM) Bad bank Basel II Break-even inflation rate Buyback

Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset guarantee Asset Protection Scheme Asset purchase Assets under management (AUM) Bad bank Basel II Break-even inflation rate Buyback

Financial Statements Danske Bank Group

58 Danske bank / ANNUAL REPORT 2011 Financial Statements Danske Bank Group FINANCIAL STATEMENTS 60 Income statement 61 Statement of comprehensive income 62 Balance sheet 63 Statement of capital 66 Cash

58 Danske bank / ANNUAL REPORT 2011 Financial Statements Danske Bank Group FINANCIAL STATEMENTS 60 Income statement 61 Statement of comprehensive income 62 Balance sheet 63 Statement of capital 66 Cash

UNION HAMILTON REINSURANCE, LTD. (A wholly-owned subsidiary of Wells Fargo & Company) FINANCIAL STATEMENTS

FINANCIAL STATEMENTS") FINANCIAL STATEMENTS As of, and for the Years then Ended (With Independent Auditors Report Thereon) NOT FOR DISCLOSURE Independent Auditors Report The Board of Directors Union Hamilton Reinsurance, Ltd.:

FINANCIAL STATEMENTS As of, and for the Years then Ended (With Independent Auditors Report Thereon) NOT FOR DISCLOSURE Independent Auditors Report The Board of Directors Union Hamilton Reinsurance, Ltd.:

2Q15 Quarterly Supplement

2Q15 Quarterly Supplement July 14, 2015 2015 Wells Fargo & Company. All rights reserved. Table of contents 2Q15 Results - 2Q15 Highlights Page 2 - Year-over-year results 3 - Balance Sheet and credit overview

2Q15 Quarterly Supplement July 14, 2015 2015 Wells Fargo & Company. All rights reserved. Table of contents 2Q15 Results - 2Q15 Highlights Page 2 - Year-over-year results 3 - Balance Sheet and credit overview

UNION HAMILTON REINSURANCE, LTD. (A wholly-owned subsidiary of Wells Fargo & Company) FINANCIAL STATEMENTS

FINANCIAL STATEMENTS") FINANCIAL STATEMENTS As of, and for the Years then Ended (With Independent Auditors Report Thereon) NOT FOR DISCLOSURE BALANCE SHEETS ($ in thousands, except par value and shares) 2017 2016 ASSETS Investment

FINANCIAL STATEMENTS As of, and for the Years then Ended (With Independent Auditors Report Thereon) NOT FOR DISCLOSURE BALANCE SHEETS ($ in thousands, except par value and shares) 2017 2016 ASSETS Investment

Basel III Standardized Approach Disclosures

Disclosures September 30, 2017 Table of Contents Page No. Introduction 1 Background 1 Overview 1 Disclosure Matrix 3 Components of Capital 10 Capital Adequacy Standardized Risk-Weighted Assets 10 Capital

Disclosures September 30, 2017 Table of Contents Page No. Introduction 1 Background 1 Overview 1 Disclosure Matrix 3 Components of Capital 10 Capital Adequacy Standardized Risk-Weighted Assets 10 Capital

GENERAL DISCUSSION OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

GENERAL DISCUSSION OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS About the Company NLV Financial Corporation ( NLVF ) through its subsidiaries (collectively, the Company, we, our ) offers life insurance

GENERAL DISCUSSION OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS About the Company NLV Financial Corporation ( NLVF ) through its subsidiaries (collectively, the Company, we, our ) offers life insurance

SUMITOMO MITSUI BANKING CORPORATION MALAYSIA BERHAD (Company No U) (Incorporated in Malaysia)

(Incorporated in Malaysia)") UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS 30 JUNE UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE Note RM 000 31 March RM 000 Assets Cash and short-term

UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS 30 JUNE UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE Note RM 000 31 March RM 000 Assets Cash and short-term

CHAPTER 09 (Part B) Banking and Bank Management

Banking and Bank Management") CHAPTER 09 (Part B) Banking and Bank Management Financial Environment: A Policy Perspective S.C. Savvides Learning Outcomes Upon completion of this chapter, you will be able to: Discuss the developments

CHAPTER 09 (Part B) Banking and Bank Management Financial Environment: A Policy Perspective S.C. Savvides Learning Outcomes Upon completion of this chapter, you will be able to: Discuss the developments

LIQUIDITY COVERAGE RATIO DISCLOSURE

LIQUIDITY COVERAGE RATIO DISCLOSURE For the quarterly period ended December 31, 2018 Table of Contents Liquidity Coverage Ratio 1 High Quality Liquid Assets and other liquidity sources 3 Net Cash Outflows

LIQUIDITY COVERAGE RATIO DISCLOSURE For the quarterly period ended December 31, 2018 Table of Contents Liquidity Coverage Ratio 1 High Quality Liquid Assets and other liquidity sources 3 Net Cash Outflows

For the 52 weeks ended 2 May 2010

36 Greene King plc Annual Report 2010 1 Accounting policies Corporate information The consolidated financial statements of Greene King plc for the 52 weeks ended 2 May 2010 were authorised for issue by

36 Greene King plc Annual Report 2010 1 Accounting policies Corporate information The consolidated financial statements of Greene King plc for the 52 weeks ended 2 May 2010 were authorised for issue by

GlobalCurrencySM Disclosure Statement

OCTOBER 2015 GlobalCurrencySM Disclosure Statement Introduction............................................. 2 Your Relationship With Morgan Stanley. and the Bank..........................................

OCTOBER 2015 GlobalCurrencySM Disclosure Statement Introduction............................................. 2 Your Relationship With Morgan Stanley. and the Bank..........................................

Consolidated Balance Sheet - 1/2

Consolidated Balance Sheet March 31, 212 ASSETS CURRENT ASSETS: Cash and cash equivalents (Notes 8 and 19) Time deposits over three months (Note 19) Receivables (Note 19): Trade notes (Note 11) Trade accounts

Consolidated Balance Sheet March 31, 212 ASSETS CURRENT ASSETS: Cash and cash equivalents (Notes 8 and 19) Time deposits over three months (Note 19) Receivables (Note 19): Trade notes (Note 11) Trade accounts

EARNINGS RELEASE FINANCIAL SUPPLEMENT (REVISED AS OF AUGUST 9, 2012) FIRST QUARTER 2012

FIRST QUARTER 2012") EARNINGS RELEASE FINANCIAL SUPPLEMENT (REVISED AS OF AUGUST 9, 2012) FIRST QUARTER 2012 On August 9, 2012, JPMorgan Chase & Co. ( the Firm ) restated its previously-filed interim financial statements for

EARNINGS RELEASE FINANCIAL SUPPLEMENT (REVISED AS OF AUGUST 9, 2012) FIRST QUARTER 2012 On August 9, 2012, JPMorgan Chase & Co. ( the Firm ) restated its previously-filed interim financial statements for

E RNIN I GS G S R EL E EA E SE S E F IN I ANCIA I L S U S PP P L P EM E EN E T THIRD QUARTER

EARNINGS RELEASE FINANCIAL SUPPLEMENT THIRD QUARTER 2012 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Consolidated Statements of Income 4 Consolidated Balance Sheets

EARNINGS RELEASE FINANCIAL SUPPLEMENT THIRD QUARTER 2012 TABLE OF CONTENTS Page(s) Consolidated Results Consolidated Financial Highlights 2-3 Consolidated Statements of Income 4 Consolidated Balance Sheets

FI3300: CORPORATE FINANCE. Problem Set 1 Chapters 1-5

FI3300: CORPORATE FINANCE Problem Set 1 Chapters 1-5 1. The goal of the firm is to. a. maximize profit b. minimize risk c. promote social good d. maximize shareholder wealth 2. Which of the following would

FI3300: CORPORATE FINANCE Problem Set 1 Chapters 1-5 1. The goal of the firm is to. a. maximize profit b. minimize risk c. promote social good d. maximize shareholder wealth 2. Which of the following would

FirstCaribbean International Bank (Bahamas) Limited

Limited") FirstCaribbean International Bank (Bahamas) Limited Financial Statements 2003 PricewaterhouseCoopers Providence House East Hill Street P.O. Box N-3910 Nassau, Bahamas Website: www.pwcglobal.com E-mail:

FirstCaribbean International Bank (Bahamas) Limited Financial Statements 2003 PricewaterhouseCoopers Providence House East Hill Street P.O. Box N-3910 Nassau, Bahamas Website: www.pwcglobal.com E-mail:

Financial Institutions, Markets, and Money, 9 th Edition

Power Point Slides for: Financial Institutions, Markets, and Money, 9 th Edition Authors: Kidwell, Blackwell, Whidbee & Peterson Prepared by: Babu G. Baradwaj, Towson University And Lanny R. Martindale,

Power Point Slides for: Financial Institutions, Markets, and Money, 9 th Edition Authors: Kidwell, Blackwell, Whidbee & Peterson Prepared by: Babu G. Baradwaj, Towson University And Lanny R. Martindale,

McGraw-Hill/Irwin Bank Management and Financial Services, 7/e 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Bank Capital Management 15-2 Key Topics The Many Tasks of Capital Capital and Risk Exposures Types of Capital In Use Capital as the Centerpiece of Regulation Basel I and Basel II Introduction What is capital?

Bank Capital Management 15-2 Key Topics The Many Tasks of Capital Capital and Risk Exposures Types of Capital In Use Capital as the Centerpiece of Regulation Basel I and Basel II Introduction What is capital?

Supplementary Financial Information Q For the period ended April 30, 2011 (UNAUDITED) For further information, please contact:

For further information, please contact:") Supplementary Financial Information Q 0 For the period ended April 0, 0 (UNAUDITED) For further information, please contact: Josie Merenda Vice-President & Head, Investor Relations (46) 955-780 josie.merenda@rbc.com

Supplementary Financial Information Q 0 For the period ended April 0, 0 (UNAUDITED) For further information, please contact: Josie Merenda Vice-President & Head, Investor Relations (46) 955-780 josie.merenda@rbc.com

Liquidity CAPITAL ASSET QUALITY MANAGEMENT EARNINGS LIQUIDITY SENSITIVITY TO MARKET RISK

represents a financial institution s ability to accommodate expected and unexpected withdrawals in deposits, decreases in other liabilities, and increases in assets. The stronger an institution s liquidity,

represents a financial institution s ability to accommodate expected and unexpected withdrawals in deposits, decreases in other liabilities, and increases in assets. The stronger an institution s liquidity,

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch. President\CEO FARIN & Associates, Inc.

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

HSBC Bank USA, N.A. HSBC Bank USA, National Association

HSBC Bank USA, N.A. HSBC Bank USA, National Association Fixed to Floating Rate Interest Certificates of Deposit Trading & Sales Desk: (212) 525-8010 452 Fifth Ave., New York, NY 10018 Indicative Terms

HSBC Bank USA, N.A. HSBC Bank USA, National Association Fixed to Floating Rate Interest Certificates of Deposit Trading & Sales Desk: (212) 525-8010 452 Fifth Ave., New York, NY 10018 Indicative Terms

Liquidity & Capital Management

Liquidity & Capital Management David Hart SunTrust Bank May 5, 2016 Unprecedented Times Current Events 2007-2010: A difficult period marked by bank failures and challenging economic conditions 2012 2014:

Liquidity & Capital Management David Hart SunTrust Bank May 5, 2016 Unprecedented Times Current Events 2007-2010: A difficult period marked by bank failures and challenging economic conditions 2012 2014:

Review Material for Exam I

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

Bank Management, 6th edition. Timothy W. Koch and S. Scott MacDonald Copyright 2006 by South-Western, a division of Thomson Learning

Bank Management, 6th edition. Timothy W. Koch and S. Scott MacDonald Copyright 2006 by South-Western, a division of Thomson Learning Funding the Bank and Managing Liquidity Chapter 8 William Chittenden

Bank Management, 6th edition. Timothy W. Koch and S. Scott MacDonald Copyright 2006 by South-Western, a division of Thomson Learning Funding the Bank and Managing Liquidity Chapter 8 William Chittenden

Explanation on reconciliation between balance sheet items and regulatory capital elements as of September 30, 2016

Explanation on reconciliation between balance sheet items and regulatory capital elements as of September 30, 2016 [Consolidated] (Millions of yen) Items Consolidated

Explanation on reconciliation between balance sheet items and regulatory capital elements as of September 30, 2016 [Consolidated] (Millions of yen) Items Consolidated

FIN 4140 Financial Markets & Institutions

FIN 4140 Financial Markets & Institutions Lecture 9-10 Money Market Money Market Securities Securities with maturities within one year are referred to as money market securities. They are issued by corporations

FIN 4140 Financial Markets & Institutions Lecture 9-10 Money Market Money Market Securities Securities with maturities within one year are referred to as money market securities. They are issued by corporations

NEWS RELEASE. Great American Bancorp, Inc. Announces Earnings - Third Quarter 2016

NEWS RELEASE FOR IMMEDIATE RELEASE October 18, 2016 Contact: Ms. Jane F. Adams Chief Financial Officer and Investor Relations (217) 356-2265 Great American Bancorp, Inc. Announces Earnings - Third Quarter

NEWS RELEASE FOR IMMEDIATE RELEASE October 18, 2016 Contact: Ms. Jane F. Adams Chief Financial Officer and Investor Relations (217) 356-2265 Great American Bancorp, Inc. Announces Earnings - Third Quarter

from 2001:Q1 to 2014:Q1 BHCAP859 for advanced approach banks and Tier 1 Common Equity from 2014:Q1 to 2014:Q4. BHCAP859 after 2014:Q4

Appendix: Data Sources and Definitions This appendix contains the details concerning the construction of all the variables used in the construction of TCH Bank Conditions Index. The aggregate index synthesizes

Appendix: Data Sources and Definitions This appendix contains the details concerning the construction of all the variables used in the construction of TCH Bank Conditions Index. The aggregate index synthesizes

ΑΣΚΗΣΕΙΣ Κεφάλαιο 6 (Κεφαλαιακή Επάρκεια)

") ΑΣΚΗΣΕΙΣ Κεφάλαιο 6 (Κεφαλαιακή Επάρκεια) 6.5, 6.16, 6.18, 6.21, 6.23, 6.25, 6.26, 6.27, 6.28, 6.29, 6.32 6.5. State Bank has the following year-end balance sheet (in millions): Cash $10 Deposits $90 Loans

ΑΣΚΗΣΕΙΣ Κεφάλαιο 6 (Κεφαλαιακή Επάρκεια) 6.5, 6.16, 6.18, 6.21, 6.23, 6.25, 6.26, 6.27, 6.28, 6.29, 6.32 6.5. State Bank has the following year-end balance sheet (in millions): Cash $10 Deposits $90 Loans

Liquidity Risk Basics Measuring and Managing Liquidity. Dad, What is Liquidity & Where Does it Come From?

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

JPMorgan Chase Bank, National Association $1,200,000 Upside Knock-Out Certificates of Deposit Linked to the S&P 500 Index due October 11, 2019

Disclosure supplement To disclosure statement dated September 21, 2012 and underlying supplement no. CD-5-I dated August 3, 2012 JPMorgan Chase Bank, National Association $1,200,000 due October 11, 2019

Disclosure supplement To disclosure statement dated September 21, 2012 and underlying supplement no. CD-5-I dated August 3, 2012 JPMorgan Chase Bank, National Association $1,200,000 due October 11, 2019

Lecture Materials BANK PERFORMANCE ANALYSIS AND CAPITAL PLANNING

Lecture Materials BANK PERFORMANCE ANALYSIS AND CAPITAL PLANNING David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 11, 2017 BANK PERFORMANCE

Lecture Materials BANK PERFORMANCE ANALYSIS AND CAPITAL PLANNING David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 11, 2017 BANK PERFORMANCE

Managing Interest Rate Risk (I): GAP and Earnings Sensitivity

: GAP and Earnings Sensitivity") Managing Interest Rate Risk (I): GAP and Earnings Sensitivity Interest Rate Risk Interest Rate Risk The potential loss from unexpected changes in interest rates which can significantly alter a bank s profitability

Managing Interest Rate Risk (I): GAP and Earnings Sensitivity Interest Rate Risk Interest Rate Risk The potential loss from unexpected changes in interest rates which can significantly alter a bank s profitability

PT BANK CENTRAL ASIA Tbk & Subsidiaries STATEMENTS OF FINANCIAL POSITION As of September 30, 2017 and December 31, 2016 (In millions of Rupiah)

") No. ACCOUNTS PT BANK CENTRAL ASIA Tbk & Subsidiaries STATEMENTS OF FINANCIAL POSITION As of September 30, 2017 and December 31, 2016 CONSOLIDATED Unaudited Audited Unaudited Audited Sep 30, 2017 Dec 31,

No. ACCOUNTS PT BANK CENTRAL ASIA Tbk & Subsidiaries STATEMENTS OF FINANCIAL POSITION As of September 30, 2017 and December 31, 2016 CONSOLIDATED Unaudited Audited Unaudited Audited Sep 30, 2017 Dec 31,

FINALTERM EXAMINATION Fall 2009 MGT411- Money & Banking (Session - 3) Time: 120 min Marks: 87

Time: 120 min Marks: 87") FINALTERM EXAMINATION Fall 2009 MGT411- Money & Banking (Session - 3) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one If more students didn't pay back their student loans then which

FINALTERM EXAMINATION Fall 2009 MGT411- Money & Banking (Session - 3) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one If more students didn't pay back their student loans then which

Explanation on reconciliation between balance sheet items and regulatory capital elements as of June 30, 2017

Explanation on reconciliation between balance sheet items and regulatory capital elements as of June 30, 2017 [Consolidated] (Millions of yen) Items Consolidated

Explanation on reconciliation between balance sheet items and regulatory capital elements as of June 30, 2017 [Consolidated] (Millions of yen) Items Consolidated

Polk County Wisconsin. Policy 913 Effective Date: Revision Date: , ,

Polk County Wisconsin INVESTMENT POLICY Policy 913 Effective Date: 06-19-2000 Revision Date: 5-20-2003, 7-18-2006, 01-16-07 POLK COUNTY INVESTMENT POLICY 1.0 Policy: The County Board Chairperson, Polk

Polk County Wisconsin INVESTMENT POLICY Policy 913 Effective Date: 06-19-2000 Revision Date: 5-20-2003, 7-18-2006, 01-16-07 POLK COUNTY INVESTMENT POLICY 1.0 Policy: The County Board Chairperson, Polk

Consolidated Balance Sheet - 1/2

Consolidated Balance Sheet March 31, ASSETS CURRENT ASSETS (Note 3): Cash and cash equivalents (Notes 9 and 21) Time deposits over three months (Note 21) Receivables (Note 21): Trade notes (Note 13) Trade

Consolidated Balance Sheet March 31, ASSETS CURRENT ASSETS (Note 3): Cash and cash equivalents (Notes 9 and 21) Time deposits over three months (Note 21) Receivables (Note 21): Trade notes (Note 13) Trade

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 5 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 5 3. Supplementary

Officer's Questionnaire. My Bank Corporation September 30, 2003

Officer's Questionnaire My Bank Corporation September 30, 2003 (Name of Holding Company) (As of Close of Business) Any Where, Any Country (Location) Jeff R. Brownie (Examiner-In-Charge) In order to expedite

Officer's Questionnaire My Bank Corporation September 30, 2003 (Name of Holding Company) (As of Close of Business) Any Where, Any Country (Location) Jeff R. Brownie (Examiner-In-Charge) In order to expedite

Significant accounting policies and estimates. Significant accounting changes No significant accounting changes were effective for us in 2011.

Note 1 Significant accounting policies and estimates The accompanying Consolidated Financial Statements have been prepared in accordance with Subsection 308 of the Bank Act (Canada) (the Act), which states

Note 1 Significant accounting policies and estimates The accompanying Consolidated Financial Statements have been prepared in accordance with Subsection 308 of the Bank Act (Canada) (the Act), which states

Financial Results for the Nine Months Ended December 31, 2012

February 14, 2013 Financial Results for the Nine Months Ended December 31, 2012 Nippon Life Insurance Company (the Company or the Parent Company ; President: Yoshinobu Tsutsui) announces financial results

February 14, 2013 Financial Results for the Nine Months Ended December 31, 2012 Nippon Life Insurance Company (the Company or the Parent Company ; President: Yoshinobu Tsutsui) announces financial results

PT BANK CENTRAL ASIA Tbk & Subsidiaries STATEMENTS OF FINANCIAL POSITION As of March 31, 2017 and December 31, 2016 (In millions of Rupiah)

") No. ACCOUNTS PT BANK CENTRAL ASIA Tbk & Subsidiaries STATEMENTS OF FINANCIAL POSITION As of March 31, 2017 and December 31, 2016 CONSOLIDATED Unaudited Audited Unaudited Audited Mar 31, 2017 Dec 31, 2016

No. ACCOUNTS PT BANK CENTRAL ASIA Tbk & Subsidiaries STATEMENTS OF FINANCIAL POSITION As of March 31, 2017 and December 31, 2016 CONSOLIDATED Unaudited Audited Unaudited Audited Mar 31, 2017 Dec 31, 2016

Sainsbury s Bank plc. Pillar 3 Disclosures for the year ended 31 December 2008

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2006

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2006 TABLE OF CONTENTS Page Consolidated Results Consolidated Financial Highlights 2 Statements of Income 3 Consolidated Balance Sheets 4 Condensed Average

EARNINGS RELEASE FINANCIAL SUPPLEMENT FIRST QUARTER 2006 TABLE OF CONTENTS Page Consolidated Results Consolidated Financial Highlights 2 Statements of Income 3 Consolidated Balance Sheets 4 Condensed Average

Supplemental Financial Information

Supplemental Financial Information For the Fourth Quarter Ended October, 06 For further information, please contact: Investor Relations Department Gillian Manning 46-08-900 www.td.com/investor Basis of

Supplemental Financial Information For the Fourth Quarter Ended October, 06 For further information, please contact: Investor Relations Department Gillian Manning 46-08-900 www.td.com/investor Basis of

SUMITOMO MITSUI BANKING CORPORATION MALAYSIA BERHAD (Company No U) (Incorporated in Malaysia)

(Incorporated in Malaysia)") UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS SEPTEMBER UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT SEPTEMBER Note 31 March Assets Cash and short-term funds

UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS SEPTEMBER UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT SEPTEMBER Note 31 March Assets Cash and short-term funds

KeyCorp. Third Quarter 2017 Earnings Review. Don Kimble Chief Financial Officer. Beth E. Mooney Chairman and Chief Executive Officer.

KeyCorp Third Quarter 2017 Earnings Review October 19, 2017 Beth E. Mooney Chairman and Chief Executive Officer Don Kimble Chief Financial Officer FORWARD-LOOKING STATEMENTS AND ADDITIONAL INFORMATION

KeyCorp Third Quarter 2017 Earnings Review October 19, 2017 Beth E. Mooney Chairman and Chief Executive Officer Don Kimble Chief Financial Officer FORWARD-LOOKING STATEMENTS AND ADDITIONAL INFORMATION