Dealing with Capital Flow Volatility: The Nigerian Experience

|

|

|

- Annice Jordan

- 6 years ago

- Views:

Transcription

1 Dealing with Capital Flow Volatility: The Nigerian Experience BY Moses K. TULE Director, Monetary Policy Department CENTRAL BANK OF NIGERIA Being a Paper Presented at the G-24 Technical Group Meeting (TGM), Colombo, Sri Lanka, February 27-28,

2 Introduction Stylized Facts on Capital Flows in Nigeria Outline Macroeconomic Policy Responses Fiscal and Monetary Policy Response Response by Types of Flow Unorthodox Policy Responses Summary and Conclusion 2

3 In Nigeria, capital importation is skewed in favour of FPI in equities, accounting for per cent of total, as against 6.12 and 6.88 per cent, invested in the bonds and money markets, respectively. INTRODUCTION Foreign capital flow is central to the development efforts of emerging market economies, as it helps to bridge the savings-investment gap These type of capital are however, volatile and large, relative to the size of the country s financial markets Major challenges confronting policymakers in recent time is to provide appropriate policy responses to tackle the impact of unexpected surge or reversal in capital flows on the financial markets and the macro-economy

4 INTRODUCTION Despite the benefits of openness, macroeconomic concerns exist with capital flows Capital flows tend to be pro-cyclical and could precipitate financial and macroeconomic instability Some of the many risks of surge or reversal in capital flows are: the possibility of rapid changes in exchange rate, external reserves and monetary policy, amongst others (Tule, 2013) The major challenge confronting policymakers therefore, is to provide appropriate policy responses to tackle the impact of unexpected surge in capital flows

5 STYLIZED FACTS Nigeria: Trend in Capital Flows

6 STYLIZED FACTS Demand and Supply of Foreign Exchange (US$ Billion) Sales Demand

7 STYLIZED FACTS External Reserves and Exchange rates Movements

Oil production improved to 1.")

8 STYLIZED FACTS Aggregate inflow to Nigeria has expanded phenomenally. Three important drivers are easily identified: Improvement in crude oil prices and domestic production Rise in Crude Oil Price by 22.01% to US$68.03pb (end-dec 2017) Oil production improved to 1.93 mbd in January 2018, from 1.86 mbd in December 2017 Relative calmness in the Niger Delta region Improved macroeconomic environment Foreign Reserve rose from US$26.99 billion (end-dec., 2016) to US$41.14 billion (end-jan., 2018) Deceleration in Inflation Rate from 18.55% in 2016 and to 15.13% in January 2018 Recovery from Recession to Growth by 1.40% in Q3, 2017 BOP surplus of US$2.3 billion or 2.4 per cent of GDP in Q3, 2017 Investment friendlier policy Expansionary Fiscal Policy Implementation of Economic Recovery and Growth Plan (ERGP) Expansionary Monetary Policy

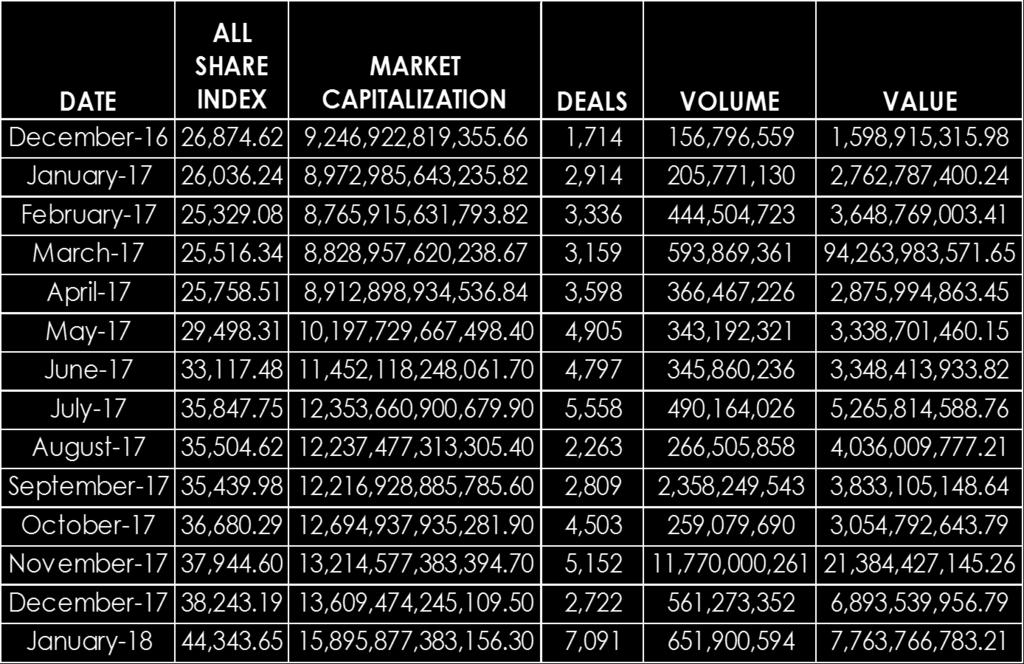

9 STYLIZED FACTS Transactions on the NSE

10 STYLIZED FACTS Domestic and Foreign Participation in Equities Trading on the NSE ( ) Domestic and Foreign Participation in Equity Trading in the NSE, Jan November 2017 Total Foreign Inflow in N'Billion Total Foreign Outflow in N'Billion Total Foreign Transactions N'Billion Total Domestic Transactions N'Billion Total Foreign Transactions as a per centage of Total Transactions (%) Total Domestic Transactions as a per centage of Total Transactions (%) Total Transactions Period N' Billion Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Jan Dec 2015(Aggregate) Jan Dec 2016 (Aggregate) Jan 2017-November 2017(Aggregate) Source: Nigerian Stock Exchange

11 STYLIZED FACTS Flow of Foreign Portfolio Investment (Equities) on the NSE) Total Foreign Outflow (N'Billion) Total Foreign Inflow (N'Billion)

12 STYLIZED FACTS Market Structure: Foreign VS Domestic Transactions (Equities)

13 Macroeconomic Policy Responses to Capital Flow Volatility The fluctuation in capital flows is quite obvious over the sample period, January 2013 to December 2017 Net capital flows decreased substantially from N20.46 billion at end of January 2013, to negative N0.4 billion in May 2013 before reversing shortly in June 2013 to N30.06 billion. There were signs of temporary recovery between June and September 2014, but slumped further into negative net flow of N49.16 billion and N70.51 billion in October 2014 and November It should be recalled that the year 2014 was quite turbulent, bearing in mind the pre-election uncertainties and the ravaging incursion of the terrorist group, Boko haram in the country. Net capital flows retracted into negative region through 2015, with exception of April and June when positive net flows of N4.45 billion and N15.69 billion, respectively.

14 Macroeconomic Policy Responses to Capital Flow Volatility As the recession deepened, the negative outflow continued until June 2016 when net capital flow moderated following the policy intervention by the central bank and a shift into a more flexible exchange rate regime. The impact of the intervention waned towards August 2016; and negative net capital flow persisted until March 2017 when there were strong signs of economic recovery

15 Macroeconomic Policy Responses to Capital Flow Volatility Foreign exchange intervention Foreign exchange intervention trailed the ebbs and tides of capital flows Positive net capital inflows are associated with reserve accumulation. On average, the central bank purchase about 5 percent of the inflows. The response is stronger when we segment capital flows into capital inflow and outflow. A large negative coefficient of (-0.51) in the correlation analysis was obtained for capital outflow, indicating that in the face of fleeing capital and to avoid the depreciation of the currency, the central bank sold foreign reserves.

16 MPC Decisions in 2017

17 Macroeconomic Policy Responses to Capital Flow Volatility Monetary policy The coefficient of correlation for the monetary policy rate shows that net capital flow tends to incite higher policy rates. An increase in net capital flows is associated with increase in the policy rate by almost 21 per cent. In other words, the decision to maintain high policy rate, or out-rightly raise the rate is often motivated by the desire to attract capital inflow into the economy. In deciding on the policy rate, the Monetary Policy Committee s (MPC) considerations often revolve around the possible exit of portfolio investments (CBN, 2017: MPC Communique No.114, July, 2017). Fiscal policy The coefficient of -0.01, obtained for the fiscal policy response, shows that fiscal policy is seldom deployed in dealing with capital flows. This is not surprising bearing in mind the long time lag it takes to pull through with fiscal policy.

18 Macroeconomic Policy Responses to Capital Flow Volatility Unorthodox Measures The cash reserve requirement (CRR) is the most prominent of the macroprudential measures. The correlation analysis indicates a positive coefficient of The positive association between this macroprudential measure and net capital flow implies that CRR reacts to capital flows. The increase in net flow elicited the likelihood of tightening macroprudential policy as hedge against financial vulnerability The likelihood of adopting macroprudential policy was more associated with capital outflows as indicated by the correlation coefficient of Intuitively, it is expected that policy makers would react more aggressively to portfolio inflows with macroprudential tools because of the financial stability risks often associated with portfolio investment.

19 Macroeconomic Policy Responses to Capital Flow Volatility Capital Controls Demand Side Capital flow management measures Supply Side Capital flow Management Measures In June 2015, the Bank excluded importers of some goods and services (initially 41 items) from accessing the official window of foreign exchange market in order to encourage local production of these items. The Bank s at the May 2016 MPC meeting introduced some flexibility in the foreign exchange market. Over The Counter (OTC) FX futures were introduced. In addition, non-oil exporters were allowed unfettered access to export proceeds and all these reduced pressure on the Bank to meet a predetermined rate and it also encourage a market-driven value for the Naira One covert measure taken by the government to stabilize and boost inward capital flow was the issuance of two executive orders in May, st : Promoting transparency and efficiency innigeria s business environment To improve ease of doing business Boost investor confidence 2 nd : Support for Local Content in public Procurement by MDAs. To moderate export demand and the capital outflow

20 Conclusion and Policy Implications The Bank, in the course of managing capital flow volatility, keeps its policy menu open and respond in a symmetrical manner. The Bank responds when there is need and effectively prepare buffers through reserves accumulation as a means to have a firm grip on the boom and bust inherent in capital mobility. Complementary reforms in key sectors of the economy also provide long-term benefits in sustaining capital flows and the effective management of associated volatility. It should be noted, however, that the issue of capital outflow in Nigeria was exaggerated and there was no fundamental reason for a panic. Overall, the outflow witnessed was in sync with the seasonal pattern that had been observed in the past. 20

21 Conclusion and Policy Implications Policy Implications Re-introduction of the one year cap on capital inflow Investors are allowed to bring in funds and exit any time they wish The issue of unremunerated reserve requirement The Cash Reserve Requirement (CRR) could be raised to manage short-term volatility in capital flow. Without banks having to increase their collateral in tight liquidity conditions, this could serve to insulate the banking sector from the large inflow and often outflow. The CRR could be reduced in periods of high liquidity needs. The flip side remains the liquidity implications of a CRR policy. Complement the CRR by introducing asymmetric interest rate corridor with a wider lower band to encourage banks to trade among themselves; overall, the option would help to guarantee banking system stability. The down side effect of this is that economic agent would direct their idle funds to the foreign exchange market. 21

22 Conclusion and Policy Implications Create a Market Support Instrument Introduce a Market Support Instrument (MSI) as applied in the case of India that could serve as a stabilization instrument to smoothen the up- and down-swings in capital flow; This can be achieved through the issuance of short-term instruments by the central bank a buy back scheme, where the bank can issue, redeem or buy back government bonds to stem the impact of capital inflows and shore up its reserves. The short-term nature offer opportunity for flexibility in managing short-term market liquidity conditions. Thus, by increasing the holdings of foreign currency assets, the Bank can manipulate these instruments to provide the desired market liquidity; Although, cost of issuance could be borne by government, it can be offset by the subsequent transfer of surplus income to government; Care must be taken not to overlap the maturity structure of these instruments with those arising from the domestic debt market; and to avoid possible market segmentation; and This option can enhance the Bank s potential to meet total demand for foreign exchange to assure investors that they will always get their money back. This will make some foreign investors to come back which will dampen foreign exchange demand pressure. 22

23 Thank you 23

Nigeria: Economic Outlook Top 10 themes for 2018

PwC Nigeria Economics Top 10 themes for 2018 February 2018 Disclaimer This document has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You

PwC Nigeria Economics Top 10 themes for 2018 February 2018 Disclaimer This document has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You

NIGERIA S ECONOMIC OVERVIEW

NIGERIA S ECONOMIC OVERVIEW Presented at the Plenary Session of UK-Nigeria Trade & Investment Forum By Senator Udoma Udo Udoma, CON Honourable Minister Ministry of Budget and National Planning 17 th April,2018

NIGERIA S ECONOMIC OVERVIEW Presented at the Plenary Session of UK-Nigeria Trade & Investment Forum By Senator Udoma Udo Udoma, CON Honourable Minister Ministry of Budget and National Planning 17 th April,2018

CBRT Policy Mix. Devrim Yavuz Central Bank of the Republic of Turkey. April Jakarta

CBRT Policy Mix Devrim Yavuz Central Bank of the Republic of Turkey April 2018 Jakarta Outline Global Financial Crises: The lessons taken, the challenges faced and the need for policy mix How the trade-offs

CBRT Policy Mix Devrim Yavuz Central Bank of the Republic of Turkey April 2018 Jakarta Outline Global Financial Crises: The lessons taken, the challenges faced and the need for policy mix How the trade-offs

Interest and Exchange Rates: Impact on the Economy

Interest and Exchange Rates: Impact on the Economy Economists Point of View Saman Kelegama Institute of Policy Studies of Sri Lanka (IPS) Increase in Credit Supply Government borrowing strategy was supported

Interest and Exchange Rates: Impact on the Economy Economists Point of View Saman Kelegama Institute of Policy Studies of Sri Lanka (IPS) Increase in Credit Supply Government borrowing strategy was supported

T R U S T F U N D P E N S I O N S P L C

MARKET AND ECONOMIC COMMENTARY NOVEMBER 31, 2014 T R U S T F U N D P E N S I O N S P L C Investment Research MACROS EQUITIES BONDS MONEY MARKET ALTERNATIVE INVESTMENTS Outline Key Macro Variables Growth

MARKET AND ECONOMIC COMMENTARY NOVEMBER 31, 2014 T R U S T F U N D P E N S I O N S P L C Investment Research MACROS EQUITIES BONDS MONEY MARKET ALTERNATIVE INVESTMENTS Outline Key Macro Variables Growth

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: December 20, 2017 Prepared by the UNL College of Business Administration, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident

Nebraska Monthly Economic Indicators: December 20, 2017 Prepared by the UNL College of Business Administration, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident

Development of Economy and Financial Markets of Kazakhstan

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

CENTRAL BANK OF NIGERIA COMMUNIQUÉ NO 116 OF THE MONETARY POLICY COMMITTEE MEETING OF MONDAY 20 th AND TUESDAY 21 st NOVEMBER, 2017

CENTRAL BANK OF NIGERIA COMMUNIQUÉ NO 116 OF THE MONETARY POLICY COMMITTEE MEETING OF MONDAY 20 th AND TUESDAY 21 st NOVEMBER, 2017 Background The Monetary Policy Committee met on the 20 th and 21 st of

CENTRAL BANK OF NIGERIA COMMUNIQUÉ NO 116 OF THE MONETARY POLICY COMMITTEE MEETING OF MONDAY 20 th AND TUESDAY 21 st NOVEMBER, 2017 Background The Monetary Policy Committee met on the 20 th and 21 st of

Figure 1: Change in LEI-N August 2018

Nebraska Monthly Economic Indicators: September 26, 2018 Prepared by the UNL College of Business, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident Economic

Nebraska Monthly Economic Indicators: September 26, 2018 Prepared by the UNL College of Business, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident Economic

Economic and Financial Markets Outlook ( ):

:") Economic and Financial Outlook: 2016-2020 Economic and Financial Markets Outlook (2018 2022): Strong Growth Prospect with Downside Risks February 09, 2018 1 Economic and Financial Outlook: 2016-2020 Contents

Economic and Financial Outlook: 2016-2020 Economic and Financial Markets Outlook (2018 2022): Strong Growth Prospect with Downside Risks February 09, 2018 1 Economic and Financial Outlook: 2016-2020 Contents

Nigeria's economic recovery Defining the path for economic growth

www.pwc.com/ng Nigeria's economic recovery Defining the path for economic growth Nigeria's economy has turned a corner The oil price shock, which started in mid-2014, severely affected the Nigerian economy.

www.pwc.com/ng Nigeria's economic recovery Defining the path for economic growth Nigeria's economy has turned a corner The oil price shock, which started in mid-2014, severely affected the Nigerian economy.

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Trustfund Pensions Plc

Trustfund Pensions Plc H1 Performance Report Update on the Economies, Markets and Portfolio Performance... Global Economy...Nigeria...Trustfund Pensions Plc Investment Department June 2016 Global Economy

Trustfund Pensions Plc H1 Performance Report Update on the Economies, Markets and Portfolio Performance... Global Economy...Nigeria...Trustfund Pensions Plc Investment Department June 2016 Global Economy

Facts Behind the Figures

Facts Behind the Figures PRESENTATION TO THE NIGERIA STOCK EXCHANGE May 2018 Outline 1 2 3 4 Operating Environment Our Journey Performance Highlights Milestones/Accomplishments Operating Environment %

Facts Behind the Figures PRESENTATION TO THE NIGERIA STOCK EXCHANGE May 2018 Outline 1 2 3 4 Operating Environment Our Journey Performance Highlights Milestones/Accomplishments Operating Environment %

Monetary Policy, Financial Regulation and Procyclicality of the Financial System - The Indian Experience

Monetary Policy, Financial Regulation and Procyclicality of the Financial System - The Indian Experience Mohua Roy Monetary Policy Department Reserve Bank of India Outline of the Presentation Monetary

Monetary Policy, Financial Regulation and Procyclicality of the Financial System - The Indian Experience Mohua Roy Monetary Policy Department Reserve Bank of India Outline of the Presentation Monetary

2017 FULL YEAR RESULTS PRESENTATION TO INVESTORS & ANALYSTS

2017 FULL YEAR RESULTS PRESENTATION TO INVESTORS & ANALYSTS OUTLINE Section Page 1. Africa Prudential Overview 02 2. Domestic Operating Environment 08 3. Financial Overview 11 4. 2018 Outlook 17 5. Appendix

2017 FULL YEAR RESULTS PRESENTATION TO INVESTORS & ANALYSTS OUTLINE Section Page 1. Africa Prudential Overview 02 2. Domestic Operating Environment 08 3. Financial Overview 11 4. 2018 Outlook 17 5. Appendix

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monetary Policy in India

Monetary Policy in India Deepak Mohanty Executive Director Reserve Bank of India September 16, 2013 1 I. Objective(s) An Outline II. III. IV. Policy Framework Operating Procedure Outcome V. Conclusion

Monetary Policy in India Deepak Mohanty Executive Director Reserve Bank of India September 16, 2013 1 I. Objective(s) An Outline II. III. IV. Policy Framework Operating Procedure Outcome V. Conclusion

Bank Indonesia s Experience on Policy Mix

Bank Indonesia s Experience on Policy Mix Sahminan Department of Economic and Monetary Policy Bank Indonesia Central Bank Policy Mix: Issues, Challenges and Policy Responses Jakarta, 9-13 April 2018 Outline

Bank Indonesia s Experience on Policy Mix Sahminan Department of Economic and Monetary Policy Bank Indonesia Central Bank Policy Mix: Issues, Challenges and Policy Responses Jakarta, 9-13 April 2018 Outline

Dynamic Change, Economic Fluctuations, and the AD-AS Model

Dynamic Change, Economic Fluctuations, and the AD-AS Model Full Length Text Part: Macro Only Text Part: 3 Chapter: 10 3 Chapter: 10 To Accompany Economics: Private and Public Choice 13th ed. James Gwartney,

Dynamic Change, Economic Fluctuations, and the AD-AS Model Full Length Text Part: Macro Only Text Part: 3 Chapter: 10 3 Chapter: 10 To Accompany Economics: Private and Public Choice 13th ed. James Gwartney,

Sterling Bank PLC H Investor/Creditor Presentation. July 2011

Sterling Bank PLC H1 2011 Investor/Creditor Presentation July 2011 Important Information Investor Relations This presentation has been prepared by Sterling Bank PLC. It is intended for an audience of professional

Sterling Bank PLC H1 2011 Investor/Creditor Presentation July 2011 Important Information Investor Relations This presentation has been prepared by Sterling Bank PLC. It is intended for an audience of professional

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: September 20, 2017 Prepared by the UNL College of Business Administration, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident

Nebraska Monthly Economic Indicators: September 20, 2017 Prepared by the UNL College of Business Administration, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident

Leading Economic Indicator Nebraska

Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Nebraska Monthly Economic Indicators: February 17, 2012 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric

Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Nebraska Monthly Economic Indicators: February 17, 2012 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric

Mongolia Selected Macroeconomic Indicators September 19, 2013

Mongolia Selected Macroeconomic Indicators September 19, 13 For further information, please contact: SSelenge@imf.org Jan-8 May-8 Sep-8 Jan-9 May-9 Sep-9 Jan-1 May-1 Sep-1 May-11 Sep-11 May-1 Sep-1 May-13

Mongolia Selected Macroeconomic Indicators September 19, 13 For further information, please contact: SSelenge@imf.org Jan-8 May-8 Sep-8 Jan-9 May-9 Sep-9 Jan-1 May-1 Sep-1 May-11 Sep-11 May-1 Sep-1 May-13

Russian Federation. Recent Economic Developments and Challenges. October 2015 IMF MOSCOW OFFICE

Russian Federation Recent Economic Developments and Challenges IMF MOSCOW OFFICE October 215 1 Outline Shocks affecting Russia s economy Policy Reaction: Monetary and Fiscal Policy Responses Current economic

Russian Federation Recent Economic Developments and Challenges IMF MOSCOW OFFICE October 215 1 Outline Shocks affecting Russia s economy Policy Reaction: Monetary and Fiscal Policy Responses Current economic

Government Cash Balances - Linkages with Liquidity

Amol Agrawal amol@stcipd.com +91-22-6622234 Government Cash Balances - Linkages with Liquidity We have been releasing reports in the nature of primers on RBI s operations and accounts (Refer Guide to Weekly

Amol Agrawal amol@stcipd.com +91-22-6622234 Government Cash Balances - Linkages with Liquidity We have been releasing reports in the nature of primers on RBI s operations and accounts (Refer Guide to Weekly

BANK OF UGANDA STATE OF THE UGANDAN ECONOMY DURING 2008/09. Research Function

BANK OF UGANDA STATE OF THE UGANDAN ECONOMY DURING 2008/09 Research Function Prepared for the meeting of the Board of Directors of the Bank of Uganda 0 Introduction This brief report reviews developments

BANK OF UGANDA STATE OF THE UGANDAN ECONOMY DURING 2008/09 Research Function Prepared for the meeting of the Board of Directors of the Bank of Uganda 0 Introduction This brief report reviews developments

CREDIT UNION TRENDS REPORT

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics May 21 (March 21 Data) Highlights During March, credit unions picked-up 423, in new memberships, and loan and savings balances grew at a.5% and 5.7%

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics May 21 (March 21 Data) Highlights During March, credit unions picked-up 423, in new memberships, and loan and savings balances grew at a.5% and 5.7%

Julio Velarde Governor Central Reserve Bank of Peru Kuala Lumpur, Malaysia October 2011

Monetary Policy Implementation: Lessons from the Crisis and Challenges for Coming Years Julio Velarde Governor Central Reserve Bank of Peru Kuala Lumpur, Malaysia October 2011 Content 1. Introductory remarks

Monetary Policy Implementation: Lessons from the Crisis and Challenges for Coming Years Julio Velarde Governor Central Reserve Bank of Peru Kuala Lumpur, Malaysia October 2011 Content 1. Introductory remarks

Viet Nam GDP growth by sector Crude oil output Million metric tons 20

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

7. Foreign Investments in India

81 7. 7.1 Introduction Since 1992, Foreign Institutional Investors (FIIs) have been allowed to invest in all traded securities on the primary and secondary markets, including shares, debentures and warrants

81 7. 7.1 Introduction Since 1992, Foreign Institutional Investors (FIIs) have been allowed to invest in all traded securities on the primary and secondary markets, including shares, debentures and warrants

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: June 21, 2017 Prepared by the UNL College of Business Administration, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident

Nebraska Monthly Economic Indicators: June 21, 2017 Prepared by the UNL College of Business Administration, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident

III. MONETARY AND LIQUIDITY CONDITIONS

III. MONETARY AND LIQUIDITY CONDITIONS Monetary and liquidity aggregates continued to expand at a strong pace during 2007-08, albeit with some moderation, reflecting large and persistent capital flows.

III. MONETARY AND LIQUIDITY CONDITIONS Monetary and liquidity aggregates continued to expand at a strong pace during 2007-08, albeit with some moderation, reflecting large and persistent capital flows.

Incorporating Macro-prudential Instruments into Monetary Policy: Thailand s experience

Incorporating Macro-prudential Instruments into Monetary Policy: Thailand s experience Dr. CHAYAWADEE CHAI-ANANT Division Executive, International Department Bank of Thailand Japan, 22 March 2012 Issues

Incorporating Macro-prudential Instruments into Monetary Policy: Thailand s experience Dr. CHAYAWADEE CHAI-ANANT Division Executive, International Department Bank of Thailand Japan, 22 March 2012 Issues

Spheria Australian Smaller Companies Fund

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: July 24, 2015 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Nebraska Monthly Economic Indicators: July 24, 2015 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Turkish Experience with Inflation Targeting

Turkish Experience with Inflation Targeting Hakan Kara Central Bank of Turkey International Financial Congress July 12 14, 2017 St. Petersburg Outline 1. Performance under inflation targeting 2. Operational

Turkish Experience with Inflation Targeting Hakan Kara Central Bank of Turkey International Financial Congress July 12 14, 2017 St. Petersburg Outline 1. Performance under inflation targeting 2. Operational

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: July 29, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Nebraska Monthly Economic Indicators: July 29, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: August 15, 2014 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Graduate Research Assistants:

Nebraska Monthly Economic Indicators: August 15, 2014 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Graduate Research Assistants:

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: October 24, 2018 Prepared by the UNL College of Business, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident Economic

Nebraska Monthly Economic Indicators: October 24, 2018 Prepared by the UNL College of Business, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident Economic

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: June 17, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Nebraska Monthly Economic Indicators: June 17, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Macroeconomic and Financial Development: Mongolia

Macroeconomic and Financial Development: Mongolia WORKSHOPS ON SUPPORTING ASIA PACIFIC LLDCs AND BHUTAN IN MOBILIZING RESOURCES FOR THE SDGs 14 December 201 Current state of macroeconomic and financial

Macroeconomic and Financial Development: Mongolia WORKSHOPS ON SUPPORTING ASIA PACIFIC LLDCs AND BHUTAN IN MOBILIZING RESOURCES FOR THE SDGs 14 December 201 Current state of macroeconomic and financial

1. Macroeconomic Highlights

1. Macroeconomic Highlights ht Macroeconomic Highlights Resilient growth over the last 2 years, despite the global economic slowdown Banking industry robust with high level of CAR and low NPLN. In 2008

1. Macroeconomic Highlights ht Macroeconomic Highlights Resilient growth over the last 2 years, despite the global economic slowdown Banking industry robust with high level of CAR and low NPLN. In 2008

Targeting the Cash Balance: the Cash Buffer

Targeting the Cash Balance: the Cash Buffer PEMPAL Treasury Community of Practice Cash Management Thematic Group Meeting 1 Ankara March 2016 Mike Williams mike.williams@mj-w.net Outline The Cash Buffer

Targeting the Cash Balance: the Cash Buffer PEMPAL Treasury Community of Practice Cash Management Thematic Group Meeting 1 Ankara March 2016 Mike Williams mike.williams@mj-w.net Outline The Cash Buffer

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: August 19, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Nebraska Monthly Economic Indicators: August 19, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Sterling Bank Plc. Analyst/Investor Presentation Q3 2017

Sterling Bank Plc Analyst/Investor Presentation Q3 2017 Important Information Notice This presentation has been prepared by Sterling Bank PLC. It is intended for an audience of professional and institutional

Sterling Bank Plc Analyst/Investor Presentation Q3 2017 Important Information Notice This presentation has been prepared by Sterling Bank PLC. It is intended for an audience of professional and institutional

Macroprudential Policy in Korea - An Introduction to BOK Framework -

II Meeting on Financial Stability Bogotá, Colombia (October 25, 2012) Macroprudential Policy in Korea - An Introduction to BOK Framework - Hyeonjin Cha Bank of Korea DISCLAIMER: This presentation represents

II Meeting on Financial Stability Bogotá, Colombia (October 25, 2012) Macroprudential Policy in Korea - An Introduction to BOK Framework - Hyeonjin Cha Bank of Korea DISCLAIMER: This presentation represents

Introduction to the UK Economy

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Perry Warjiyo: US monetary policy normalization and EME policy mix the Indonesian experience

Perry Warjiyo: US monetary policy normalization and EME policy mix the Indonesian experience Speech by Mr Perry Warjiyo, Deputy Governor of Bank Indonesia, at the NBER 25th Annual East Asian Seminar on

Perry Warjiyo: US monetary policy normalization and EME policy mix the Indonesian experience Speech by Mr Perry Warjiyo, Deputy Governor of Bank Indonesia, at the NBER 25th Annual East Asian Seminar on

AN EMPIRICAL ANALYSIS OF MACROPRUDENTIAL POLICIES IN PERU: The Case of Dynamic Provisioning and Conditional Reserve Requirements

AN EMPIRICAL ANALYSIS OF MACROPRUDENTIAL POLICIES IN PERU: The Case of Dynamic Provisioning and Conditional Reserve Requirements June 2016 Miguel Cabello, José Lupú and Elías Minaya Outline 2 1. Motivation

AN EMPIRICAL ANALYSIS OF MACROPRUDENTIAL POLICIES IN PERU: The Case of Dynamic Provisioning and Conditional Reserve Requirements June 2016 Miguel Cabello, José Lupú and Elías Minaya Outline 2 1. Motivation

PRESS RELEASE. Securities issued by Hungarian residents and breakdown by holding sectors. October 2018

PRESS RELEASE 10 December 2018 Securities issued by Hungarian residents and breakdown by holding sectors October 2018 According to securities statistics, the amount outstanding of equity securities and

PRESS RELEASE 10 December 2018 Securities issued by Hungarian residents and breakdown by holding sectors October 2018 According to securities statistics, the amount outstanding of equity securities and

The Malaysian Economy

The Malaysian Economy Prospects and critical issues in 2011-20122012 Presentation for ISIS PRAXIS Seminar Nor Zahidi Alias Chief Economist March 3 rd, 2011 In a nutshell US economy is emitting more positive

The Malaysian Economy Prospects and critical issues in 2011-20122012 Presentation for ISIS PRAXIS Seminar Nor Zahidi Alias Chief Economist March 3 rd, 2011 In a nutshell US economy is emitting more positive

MPC MARKET PERCEPTIONS SURVEY - MARCH

MPC MARKET PERCEPTIONS SURVEY - MARCH 2018 1 CONTENTS BACKGROUND......4 SURVEY METHODOLOGY......4 HIGHLIGHTS OF THE SURVEY.........4 INFLATION EXPECTATIONS....5 EXCHANGE RATE EXPECTATIONS...6 PRIVATE SECTOR

MPC MARKET PERCEPTIONS SURVEY - MARCH 2018 1 CONTENTS BACKGROUND......4 SURVEY METHODOLOGY......4 HIGHLIGHTS OF THE SURVEY.........4 INFLATION EXPECTATIONS....5 EXCHANGE RATE EXPECTATIONS...6 PRIVATE SECTOR

The new liquidity measurement model developed by the Hungarian Central Bank during the financial crisis

The new liquidity measurement model developed by the Júlia Király Deputy Governor 29 November 212 Content Liquidity and measurement prior to the crisis New measures and new data collection during the crisis

The new liquidity measurement model developed by the Júlia Király Deputy Governor 29 November 212 Content Liquidity and measurement prior to the crisis New measures and new data collection during the crisis

Debt Management and Sustainability: Strengthening Liability Management

Debt Management and Sustainability: Strengthening Liability Management Sri Lankan Perspective 27 February 2018 Colombo, Sri Lanka C J P Siriwardana Deputy Governor 2 Overview 1. Evolution of Public Debt

Debt Management and Sustainability: Strengthening Liability Management Sri Lankan Perspective 27 February 2018 Colombo, Sri Lanka C J P Siriwardana Deputy Governor 2 Overview 1. Evolution of Public Debt

Outlook for the Texas Economy. Luis Bernardo Torres Ruiz, Ph.D. June 29, 2016

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. June 29, 2016 Research Economist Texas Gas Association Contents 1. Economic Outlook 2. Housing Market 3. Challenges and Issues During the

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. June 29, 2016 Research Economist Texas Gas Association Contents 1. Economic Outlook 2. Housing Market 3. Challenges and Issues During the

TRENDS, DYNAMICS, AND CHALLENGES OF CAPITAL FLOWS TO FRONTIER MARKETS

HIGH-LEVEL CONFERENCE ON MANAGING CAPITAL FLOWS: LESSONS FROM EMERGING MARKETS FOR FRONTIER ECONOMIES MARCH 2, 2015, MAURITIUS TRENDS, DYNAMICS, AND CHALLENGES OF CAPITAL FLOWS TO FRONTIER MARKETS By Henry

HIGH-LEVEL CONFERENCE ON MANAGING CAPITAL FLOWS: LESSONS FROM EMERGING MARKETS FOR FRONTIER ECONOMIES MARCH 2, 2015, MAURITIUS TRENDS, DYNAMICS, AND CHALLENGES OF CAPITAL FLOWS TO FRONTIER MARKETS By Henry

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS Yiping Huang Seminar at the Crawford School of Economics and Government, ANU, March 1, 29 GLOBAL FINANCIAL CRISIS Three unique factors contributed to the current

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS Yiping Huang Seminar at the Crawford School of Economics and Government, ANU, March 1, 29 GLOBAL FINANCIAL CRISIS Three unique factors contributed to the current

XML Publisher Balance Sheet Vision Operations (USA) Feb-02

Feb-02") Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION JUNE 2018 RIYADH, SAUDI ARABIA JUNE 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION JUNE 2018 RIYADH, SAUDI ARABIA JUNE 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON

MAINTAIN BULLISHNESS; INCREASE EXPOSURE

First Capital Research MAINTAIN BULLISHNESS; INCREASE EXPOSURE First Capital Fixed Income Recommendation - 12 th OCT 18 Lead Analyst: Secondary Analyst: Atchuthan Srirangan Dimantha Mathew 1.0 New Recommendation

First Capital Research MAINTAIN BULLISHNESS; INCREASE EXPOSURE First Capital Fixed Income Recommendation - 12 th OCT 18 Lead Analyst: Secondary Analyst: Atchuthan Srirangan Dimantha Mathew 1.0 New Recommendation

Monetary Policy Review Premature end to the easing cycle?

The monetary policy committee (MPC) maintained status quo for the second policy review running, keeping Repo rate at 6.25%, contrary to market expectations of 25bps cut. Consequently, the reverse repo/msf

The monetary policy committee (MPC) maintained status quo for the second policy review running, keeping Repo rate at 6.25%, contrary to market expectations of 25bps cut. Consequently, the reverse repo/msf

State of the Turkish Economy. Emre Deliveli TOBB ETU, October

State of the Turkish Economy Emre Deliveli TOBB ETU, October 11 2005 State of the Turkish Economy Slide 2 Agenda Overview of the Turkish economy Risks and priorities New anchor: EU What are the policy

State of the Turkish Economy Emre Deliveli TOBB ETU, October 11 2005 State of the Turkish Economy Slide 2 Agenda Overview of the Turkish economy Risks and priorities New anchor: EU What are the policy

PRESENTATION BY PROF. E. TUMUSIIME-MUTEBILE, GOVERNOR, BANK OF UGANDA, TO THE NRM RETREAT, KYANKWANZI, JANUARY

BANK OF UGANDA PRESENTATION BY PROF. E. TUMUSIIME-MUTEBILE, GOVERNOR, BANK OF UGANDA, TO THE NRM RETREAT, KYANKWANZI, JANUARY 19, 2012 MACROECONOMIC MANAGEMENT IN TURBULENT TIMES Introduction I want to

BANK OF UGANDA PRESENTATION BY PROF. E. TUMUSIIME-MUTEBILE, GOVERNOR, BANK OF UGANDA, TO THE NRM RETREAT, KYANKWANZI, JANUARY 19, 2012 MACROECONOMIC MANAGEMENT IN TURBULENT TIMES Introduction I want to

Monthly Mutual Fund Report

July, Monthly Mutual Fund Report Statistics for May-June Sales and Redemptions Total assets for all funds increased in May by $9. billion, or., to $.7 trillion. Money market funds had a net cash outflow

July, Monthly Mutual Fund Report Statistics for May-June Sales and Redemptions Total assets for all funds increased in May by $9. billion, or., to $.7 trillion. Money market funds had a net cash outflow

Mongolia Selected Macroeconomic Indicators January 24, 2014

Mongolia Selected Macroeconomic Indicators January 2, 21 For further information, please contact: SSelenge@imf.org 2 2 27 2 29 21 211 212 213 213 Q1 Q2 Q3 Oct. Nov. Dec. Q Total US$-value 1,3 1,97 2,3

Mongolia Selected Macroeconomic Indicators January 2, 21 For further information, please contact: SSelenge@imf.org 2 2 27 2 29 21 211 212 213 213 Q1 Q2 Q3 Oct. Nov. Dec. Q Total US$-value 1,3 1,97 2,3

SRI LANKA. Highlights

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized SRI LANKA FINANCIAL SECTOR QUARTERLY UPDATE THIRD QUARTER 27 Highlights Financial Sector

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized SRI LANKA FINANCIAL SECTOR QUARTERLY UPDATE THIRD QUARTER 27 Highlights Financial Sector

Finally, A Global Tailwind for U.S. Manufacturing Growth

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Stylized Financial System

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Monetary Policy Workshop on Strengthening

Monetary Policy Workshop on Strengthening Macroprudential Framework held by IMF Regional Office for Asia and Pacific (March 22~23, 2012, Tokyo) Macroprudential Policy Framework: The Case of Korea Tae Soo

Monetary Policy Workshop on Strengthening Macroprudential Framework held by IMF Regional Office for Asia and Pacific (March 22~23, 2012, Tokyo) Macroprudential Policy Framework: The Case of Korea Tae Soo

3rd Bi-Monthly Monetary Policy Review, Kotak Mutual Fund Update as on 9 th August

3rd Bi-Monthly Monetary Policy Review, 2016-17 Kotak Mutual Fund Update as on 9 th August 2016 1 Monetary Measures: Key Rates Measures CRR Unchanged at 4.00% Reverse Repo rate Unchanged at 6.00% (affixed

3rd Bi-Monthly Monetary Policy Review, 2016-17 Kotak Mutual Fund Update as on 9 th August 2016 1 Monetary Measures: Key Rates Measures CRR Unchanged at 4.00% Reverse Repo rate Unchanged at 6.00% (affixed

FX Viewpoint. Wednesday, October 12, Asia Net portfolio capital inflow update

FX Viewpoint Wednesday, October 12, 216 Asia Net portfolio capital inflow update Corporate FX & Structured Products Tel: 69-1888 / 1881 Fixed Income & Structured Products Tel: 69-181 The net capital inflow

FX Viewpoint Wednesday, October 12, 216 Asia Net portfolio capital inflow update Corporate FX & Structured Products Tel: 69-1888 / 1881 Fixed Income & Structured Products Tel: 69-181 The net capital inflow

MFW4A: The impact of the global financial crisis on funding needs and borrowing strategies in Africa

MFW4A: The impact of the global financial crisis on funding needs and borrowing strategies in Africa Stefan Nalletamby, Coordinator This presentation covers four sections 1. Impact of the financial crisis

MFW4A: The impact of the global financial crisis on funding needs and borrowing strategies in Africa Stefan Nalletamby, Coordinator This presentation covers four sections 1. Impact of the financial crisis

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: January 17, 2014 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Graduate Research

Nebraska Monthly Economic Indicators: January 17, 2014 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Graduate Research

MonitorING Turkey ING BANK A.Ş. Further fiscal support in the Medium Term Plan. Emerging Markets 4 October 2017

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

MONETARY POLICY COMMITTEE STATEMENT FOR FIRST QUARTER Governor s Presentation to the Media. 16 th May, 2018

1 MONETARY POLICY COMMITTEE STATEMENT FOR FIRST QUARTER 2018 Governor s Presentation to the Media 16 th May, 2018 INTRODUCTION 2 The presentation is structured as follows: 1. Decision of the Monetary Policy

1 MONETARY POLICY COMMITTEE STATEMENT FOR FIRST QUARTER 2018 Governor s Presentation to the Media 16 th May, 2018 INTRODUCTION 2 The presentation is structured as follows: 1. Decision of the Monetary Policy

ARM Research. Economic Update July Economic Report Monthly Update. 9 August FMDQ ignites further FX liquidity flame.

ARM Research research@armsecurities.com.ng +234 1 270 1652 9 August 2017 Economic Report Monthly Update Economic Update July 2017 Economic Snapshot June 2017 Inflation Data/Indices MoM YoY Prev YoY Headline

ARM Research research@armsecurities.com.ng +234 1 270 1652 9 August 2017 Economic Report Monthly Update Economic Update July 2017 Economic Snapshot June 2017 Inflation Data/Indices MoM YoY Prev YoY Headline

AS Economics: ECON2 Economics: The National Economy 2009/10

2 weeks 1 st Sep - 11 th Sep Term 1 Introduction to the objectives and instruments of government This is an introduction to 3.2.3, 3.2.1 macroeconomic policy the Unit and most of the content Candidates

2 weeks 1 st Sep - 11 th Sep Term 1 Introduction to the objectives and instruments of government This is an introduction to 3.2.3, 3.2.1 macroeconomic policy the Unit and most of the content Candidates

Mexico s Economic Policy under External Constraints. Manuel Sánchez, Member of the Board

Manuel Sánchez, Member of the Board Adam Smith Seminar, Schloss Spiez, Switzerland, June 27, 2012 Contents 1 Monetary Policy and Capital Inflows 2 Implications of European Uncertainty 3 Economic Developments

Manuel Sánchez, Member of the Board Adam Smith Seminar, Schloss Spiez, Switzerland, June 27, 2012 Contents 1 Monetary Policy and Capital Inflows 2 Implications of European Uncertainty 3 Economic Developments

China Economic Update Q1 2015

Key Developments in Brief Economic development Growth drivers Risks GDP growth slows to 7. Slowdown challenging, but manageable More easing policies expected Reforms progressing slowly Services and retail

Key Developments in Brief Economic development Growth drivers Risks GDP growth slows to 7. Slowdown challenging, but manageable More easing policies expected Reforms progressing slowly Services and retail

Radu Mihai Balan, Edilberto L. Segura

April 15 GDP expanded by.9% yoy in 1, reaching EUR 15.7 billion. Industrial output expanded 1.% yoy in January, slowing down from 3.1% yoy in December. The consolidated budget deficit posted a.33% of GDP

April 15 GDP expanded by.9% yoy in 1, reaching EUR 15.7 billion. Industrial output expanded 1.% yoy in January, slowing down from 3.1% yoy in December. The consolidated budget deficit posted a.33% of GDP

Statistics for RMB OTC Closing Values in 2006

Bracing For More RMB Volatility Summary n Post IMF/G7 meetings, RMB continued to maintain a steady strengthening trend but in rising volatility, as talks of a one-off move gave way. We expect such RMB

Bracing For More RMB Volatility Summary n Post IMF/G7 meetings, RMB continued to maintain a steady strengthening trend but in rising volatility, as talks of a one-off move gave way. We expect such RMB

Mongolia Selected Macroeconomic Indicators December 18, 2013

Mongolia Selected Macroeconomic Indicators December 18, 213 For further information, please contact: SSelenge@imf.org 2 2 27 28 29 21 211 212 213 212 213 Q1 Q2 Q3 Oct. Nov. First 11 months Total US$-value

Mongolia Selected Macroeconomic Indicators December 18, 213 For further information, please contact: SSelenge@imf.org 2 2 27 28 29 21 211 212 213 212 213 Q1 Q2 Q3 Oct. Nov. First 11 months Total US$-value

SYSTEMATIC GLOBAL MACRO ( CTAs ):

:") G R A H M C A P I T A L M A N G E M N T G R A H A M C A P I T A L M A N A G E M E N T GC SYSTEMATIC GLOBAL MACRO ( CTAs ): PERFORMANCE, RISK, AND CORRELATION CHARACTERISTICS ROBERT E. MURRAY, CHIEF OPERATING

G R A H M C A P I T A L M A N G E M N T G R A H A M C A P I T A L M A N A G E M E N T GC SYSTEMATIC GLOBAL MACRO ( CTAs ): PERFORMANCE, RISK, AND CORRELATION CHARACTERISTICS ROBERT E. MURRAY, CHIEF OPERATING

Sri Lanka: Recent Economic Trends. January 2018

Sri Lanka: Recent Economic Trends January 2018 1 Agenda Summary Economic Growth Inflation and Monetary Policy External Account Fiscal Scenario of Government of Sri Lanka ICRA Lanka Limited 2 2 Agenda Summary

Sri Lanka: Recent Economic Trends January 2018 1 Agenda Summary Economic Growth Inflation and Monetary Policy External Account Fiscal Scenario of Government of Sri Lanka ICRA Lanka Limited 2 2 Agenda Summary

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Monetary Policy. Confidence in the kina exchange rate and management of the economy; A foundation for stable fiscal operations of the Government;

Bank of Papua New Guinea PRESENTATION - ON THE MARCH 2012 MONETARY POLICY STATEMENT BY MR. LOI M. BAKANI - GOVERNOR BANK OF PAPUA NEW GUINEA TUESDAY 3 RD APRIL 2012 LAE INTERNATIONAL HOTEL, LAE Monetary

Bank of Papua New Guinea PRESENTATION - ON THE MARCH 2012 MONETARY POLICY STATEMENT BY MR. LOI M. BAKANI - GOVERNOR BANK OF PAPUA NEW GUINEA TUESDAY 3 RD APRIL 2012 LAE INTERNATIONAL HOTEL, LAE Monetary

Nigeria Economy 2018 Economic Outlook TABLE OF CONTENTS

February 20, 2018 www.panafricancapitalplc.com TABLE OF CONTENTS EXECUTIVE SUMMARY 2 THE REVIEW OF THE 2017 ECONOMIC PERFORMANCE Real GDP Growth Rate 3 Foreign Exchange Policies and Foreign Reserves 9

February 20, 2018 www.panafricancapitalplc.com TABLE OF CONTENTS EXECUTIVE SUMMARY 2 THE REVIEW OF THE 2017 ECONOMIC PERFORMANCE Real GDP Growth Rate 3 Foreign Exchange Policies and Foreign Reserves 9

Banks have to necessarily use marginal cost of funds to calculate the change in the base rate

BFSI The impending change in banks base rate formula The RBI is shortly expected to announce the new base rate formula, linking banks base rates to their marginal cost of funds. This is notwithstanding

BFSI The impending change in banks base rate formula The RBI is shortly expected to announce the new base rate formula, linking banks base rates to their marginal cost of funds. This is notwithstanding

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Reviewing Macro-economic Developments and Understanding Macro-Economic Policy

MINISTRY OF FINANCE GOVERNMENT OF INDIA Reviewing Macro-economic Developments and Understanding Macro-Economic Policy Module 5 Contemporary Themes in India s Economic Development and the Economic Survey

MINISTRY OF FINANCE GOVERNMENT OF INDIA Reviewing Macro-economic Developments and Understanding Macro-Economic Policy Module 5 Contemporary Themes in India s Economic Development and the Economic Survey

PRESS RELEASE. Securities issued by Hungarian residents and breakdown by holding sectors. January 2019

7 March 2019 PRESS RELEASE Securities issued by Hungarian residents and breakdown by holding sectors January 2019 According to securities statistics, the amount outstanding of equity securities and debt

7 March 2019 PRESS RELEASE Securities issued by Hungarian residents and breakdown by holding sectors January 2019 According to securities statistics, the amount outstanding of equity securities and debt

Turkey s Experience with Macroprudential Policy

Turkey s Experience with Macroprudential Policy Hakan Kara* Central Bank of Turkey Macroprudential Policy: Effectiveness and Implementation Challenges CBRT-IMF-BIS Joint Conference October 26-27, 2015

Turkey s Experience with Macroprudential Policy Hakan Kara* Central Bank of Turkey Macroprudential Policy: Effectiveness and Implementation Challenges CBRT-IMF-BIS Joint Conference October 26-27, 2015

PN0807 Volatility of Stock Return in the Dhaka Stock Exchange

PN0807 Volatility of Stock Return in the Dhaka Stock Exchange Md. Habibour Rahman Md. Sakhawat Hossain Abstract This note examines the volatility in stock prices in the Dhaka Stock Exchange (DSE) during

PN0807 Volatility of Stock Return in the Dhaka Stock Exchange Md. Habibour Rahman Md. Sakhawat Hossain Abstract This note examines the volatility in stock prices in the Dhaka Stock Exchange (DSE) during

ACCESS BANK RIGHTS ISSUE

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Primary Market Watch Capitalising to push strategic growth plan Capital is key to achieving medium term strategic plan:

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Primary Market Watch Capitalising to push strategic growth plan Capital is key to achieving medium term strategic plan:

UNCTAD s Seventh Debt Management Conference. Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

Indian Economy. GDP growth slowed down but remained above the comfortable 7% Manufacturing GVAbp

Indian Economy Economic Growth GDP growth slowed down but remained above the comfortable 7% Domestic economy witnessed 7.1% GDP growth during the first quarter (Apr - Jun) of fiscal 2016-17 (Q1FY17) as

Indian Economy Economic Growth GDP growth slowed down but remained above the comfortable 7% Domestic economy witnessed 7.1% GDP growth during the first quarter (Apr - Jun) of fiscal 2016-17 (Q1FY17) as

RBI in Defence of INR

RBI in Defence of INR Jayesh Mehta Country Treasurer Bank of America September 2013 Real current account deficit 3.5% Current account deficit really ~3.5% of GDP Trade data overestimating oil imports Reduced

RBI in Defence of INR Jayesh Mehta Country Treasurer Bank of America September 2013 Real current account deficit 3.5% Current account deficit really ~3.5% of GDP Trade data overestimating oil imports Reduced

NOT JUST A BOND PROXY

GLOBAL LISTED INFRASTRUCTURE: NOT JUST A BOND PROXY This research paper will explore the often misunderstood impact of interest rates on Global Listed Infrastructure and differentiate between the short

GLOBAL LISTED INFRASTRUCTURE: NOT JUST A BOND PROXY This research paper will explore the often misunderstood impact of interest rates on Global Listed Infrastructure and differentiate between the short