Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development

|

|

|

- Byron Paul

- 6 years ago

- Views:

Transcription

1 For Official Use STD/NA(2002)27 Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development English - Or. English STATISTICS DIRECTORATE STD/NA(2002)27 For Official Use National Accounts SOURCES OF DATA FOR INTERNATIONAL COMPARISONS OF COMPANY PROFITABILITY (METHODOLOGY) Paper prepared by Richard Walton - Bank of England (United Kingdom) OECD MEETING OF NATIONAL ACCOUNTS EXPERTS Château de la Muette, Paris 8-11 October 2002 Beginning at 9:30 a.m. on the first day English - Or. English Richard.Walton@bankofengland.co.uk Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format

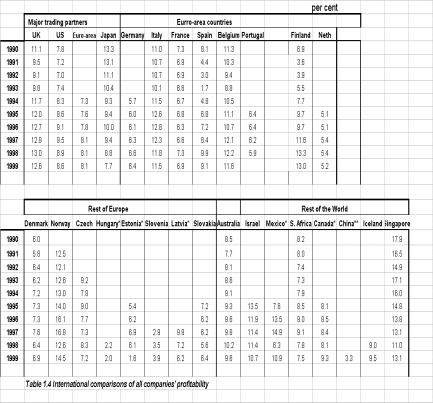

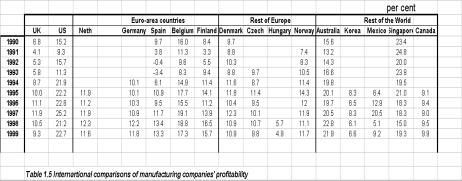

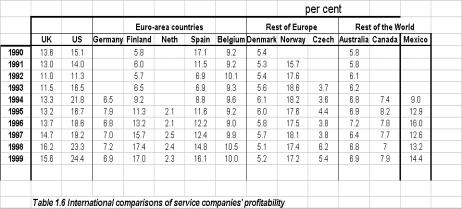

2 SOURCES OF DATA FOR INTERNATIONAL COMPARISONS OF COMPANY PROFITABILITY (METHODOLOGY) 1. The rates of return to be presented in the article, International comparisons of company profitability (UK Economic Trends, 15 October 2002) are ratios of the operating surpluses of non-financial companies compared with capital employed, expressed as percentages. Tables 1.4, 1.5 and 1.6 provide data on international comparisons of all companies, manufacturing and services companies. Data for 2000 an 2001 will be released on 15 October. The rate of return can be calculated in many ways 1, but this is considered the most important measure of profitability because it expresses the return on invested capital. The net rate of return uses capital estimates which are net of capital consumption and is more widely used than the gross rate of return. The sources of data are national accounts in most countries. In a few countries, financial indicators of business activity have been used which draw on data from balance sheets and the profit and loss accounts of surveys of enterprises. 2. The use of national accounts data has distinct advantages over company accounting: National accounts definitions and concepts for operating surplus net of depreciation in ESA95/SNA93 are consistent across all firms and over time. When conventions have changed, historic as well as current data are revised. National accounts data are gross of corporate taxes. Accounting conventions differ across countries and even within countries in the measurement of profits in company accounts 2. Accounting in Europe is geared rather more towards creditor protection than are US accounting policies. There are differences in the capitalisation of intangible assets related to computer software and in running costs which in Europe have to be included directly in the profit and loss account. In the US, operating earnings exclude items that firms choose to describe as extraordinary. Profits may also be distorted in company accounts because of inflation. Company accounts are often published with a huge time lag. There are differences also in accounting for capital: the list of items which can and cannot be capitalised, service lives, the rate and method of depreciation, how to deal with write-offs from bankruptcies and closures and different valuation rules for fixed and intangible assets. Capital is measured at current replacement cost, rather than at the prices at which the assets were purchased. Comparison of current income streams achieves consistency and coherence. 1 2 The numerator could be defined exclusive of net interest. Profits could be after tax or based on financial accounting standards. Similarly, capital could be measured at historical cost rather than at current cost and could include goodwill and intellectual property. Or, the denominator could be equity or sales. All publicly traded European companies will have to conform with International Accounting Standards by 2005 and apply a single set of internationally agreed standards (fair value, accruals basis) for the preparation of consolidated financial statements. 2

3 National accounts cover the earnings of the resident corporate sector, not just publicly quoted companies. Data in the non-financial sector of the national accounts are consistent with those for other sectors of the economy. 3. This paper sets out an inventory of present methodology. This is the third international survey and the author has noted that most countries have introduced concepts and classifications to produce comparable figures. There are now 34 countries contributing to this survey compared to 17 in the second and 11 in the first survey. Rates of return published in the third survey will be available on October The author recognises that even with comparable data care must be taken in analysis, given different structures and capital intensity of economies, institutional differences in corporate financing, the tax burden and different business cycles and rate of technological change. It follows that differences between countries can reflect a mixture of real differences in profitability and the results of differences in calculations. In this third world survey, these differences in calculation have continued to be minimised as a result of the use of national accounts data sources. In virtually every case, countries will, however, have calculated profitability consistently over time. Rises and falls will reflect real changes in their economies. I. How profits are calculated 5. In the United Kingdom, gross operating surplus consists of gross trading profits, plus income from rental of buildings less inventory holding gains. Gross trading profits include only that part of a company s income which arises from trading activities in the UK. It does not include income from investments. Nor does it include earnings from subsidiaries or branches located outside the United Kingdom. Gross trading profits are calculated before payments of dividends, interest and tax. Any change in the book value of inventories is subtracted from profits, because revaluations are not considered to be part of economic activity (as defined for National Accounts purposes). Net operating surplus is net of depreciation (capital consumption). Capital consumption is derived from capital stock and covers the depreciation of fixed assets over their service lives. The main difference between UK commercial accounting and national accounting is in the treatment of net interest. Commercial accounting show net interest received as profit. National accounts treat interest flows as property income. 6. Other countries follow the international guidelines outlined above. There are differences of detail, but they are not significant in terms of the impact on the data. European Union 7. The measure of profits for Austria is the operating surplus of non-financial corporations (S.11). Data are available for data would not be available until late December 2002 with the sectoral accounts within the national accounts (except financial accounts). 8. The measure of profits in Belgium is calculated indirectly from the value added, less compensation of employees and other operating expenses. It is equivalent to earnings before taxes, depreciation and amortisation. The manufacturing sector includes from 1997 oil refining companies. 3

4 9. For Denmark, net rates of return are calculated using profits measured as the gross operating surplus after deduction of depreciation (consumption of fixed capital). Data are available for the non-financial sectors and subdivided into industries, manufacturing and services. 10. Statistics Finland do not currently publish data for Finland on net rates of return, but have produced data for this world survey and will be considering their future publication. The data for profitability are the current price net operating surplus per average net capital stock and average inventories. Data are available for non-financial corporations, manufacturing and services which include some household sector net operating surplus/mixed income which cause some upward bias. Revised data back to 1975 on the ESA95 basis are available, including the capital stock data. 11. In France, INSEE has completed the calculations of the French national accounts including nonfinancial balance sheets according to SNA93 from To calculate profitability ratios, the net operating surplus is calculated from the gross operating surplus of non-financial companies (S11) less capital consumption. Operating surplus is available quarterly. 12. In Germany, the use of national account data enables profits to be calculated in this third survey from the net operating surplus of non-financial corporations. Use of net operating surplus by industry has one disadvantage: data are available only at t+18 months. The Bundesbank publish annual profitability ratios for the corporate sector (ratios of income/turnover) and in the latest review on German enterprises profitability and financing in 2000 do have data for 2000 (Bundesbank Monthly report April 2002). The Bundesbank use current balance sheets and profit and loss accounts submitted by companies, but acknowledge that there is a statistical bias with weaker companies and the services sector less well represented. Before taxes, profits as a percentage of turnover are reported as 3.5% in , figures which were in line with data in the first two surveys and in line with data produced by the Cologne Research Institute on post-tax rates of return on sales earned by German international companies. 13. Data on sales and profits before taxes in Greece are collected (Financial accounts section, Statistics Department, Bank of Greece) using a sample of 342 enterprises across the manufacturing and trade sectors. 14. Ireland calculates operating surplus in the framework of annual National Accounts, but it does not compile capital and, thus, cannot estimate rates of return. Nor, at the present time, does Ireland estimate quarterly profits. Ireland has, however, provided internationally comparable data for the net operating surplus of all non-financial companies, for manufacturing companies and for service companies. Data provided for 1990 to 2000 (estimates) are based on the 2000 National Income and Expenditure publication, released in July Ireland has deducted stock appreciation from gross operating surplus to be consistent with the ESA95 definition of net operating surplus. This ensures that the effects of price changes on the level of stocks are eliminated. 15. Alternative sources of profitability for this article have been considered. For example, those published by the United States Bureau of Economic Analysis, in articles in the Survey of Current Business on the operations of US companies abroad. This source has consistently shown high rates of return in Ireland and these figures should not be taken as representative of all companies in Ireland. 16. Italy uses national accounts data for profits based on the net operating surplus of non-financial companies. Data are calculated by imputing to the self-employed the labour cost per full-time equivalent worker. 4

5 17. Netherlands break down net operating surplus into public (i.e. owned/controlled by government) and private corporations (i.e. including non-public, non-profit institutions with market production and foreign-controlled, non-financial corporations) separately. But, the breakdown by manufacturing and services is for private and public corporations, together. Separate information for operations on the Continental Shelf is not available: data on mining and quarrying as a total only are available. 18. The net operating surplus of non-financial companies in Portugal is available only for 1995 to The data for profits of non-financial corporations in Spain are collected in an annual survey by the Banco de Espana. 10 years data has been collected from 1991 to The ratio which has been used is the ordinary return on equity which represents the ordinary profit net of depreciation and operating provisions as a ratio of equity. These ratios are available also for the manufacturing and services sectors. These ratios follow trends of earnings before taxes, interest, depreciation and amortisation which are used by stock market analysts in Spain. Quarterly data are provided, in articles on the Results of non-financial corporations which also gives annual data, calculated as the weighted average of the quarterly data. For Q4 2001, 758 corporations reported data relating to the four quarters of 2001 to the Central Balance Sheet Office. The gross value added of these corporations accounted for 14% of the total for non-financial corporations. From 1998, the surveys of the Bank of Spain are consistent with those used in the Spanish national accounts. 21. Data for companies in Sweden are regarded as less reliable for analytical purposes than in other countries. First, because the net operating surplus for the corporation sector is residually calculated from total GDP compiled from the expenditure side. Second, because in 2000 and in 2001, financial companies are included in the total. United States 22. The US Bureau of Economic Analysis 2 calculates annual profitability ratios for the United States as the ratio of property income before tax to produced assets. Property income for domestic nonfinancial corporations is the sum of profits and net interest. 23. Corporate profits before taxes are the main component and incorporate adjustments for the appreciation of inventories and capital consumption, plus net interest. In the UN System of National Accounts, the sum of profits and net interest is termed net operating surplus. Corporate profits and net interest are based on company data. As a result, property income for domestic nonfinancial corporations includes income earned by financial establishments of those corporations and it excludes income earned by nonfinancial units of financial establishments. In the United States, the share of property income in domestic income fell from 15.4 per cent in 2000 to 14.5 per cent in 2001, the lowest share in more than 40 years. 24. Profits of manufacturing and service sector (retail trade and wholesale trade companies) companies in the United States are calculated quarterly on a different basis. The U.S. Census Bureau publishes the Quarterly Financial Report for Manufacturing, Mining and Trade Corporations and the Quarterly Financial Report for Retail Trade Corporations These advance data provide income and retained earnings from statements of income and retained earnings, balance sheets and related 2 U.S. Bureau of Economic Analysis. Note on Profitability of domestic nonfinancial corporations, September Survey of Current Business. 5

6 financial and operating ratios, based on quarterly financial reports from a sample of about 8,200 manufacturing, mining and wholesale trade corporations and from 465 large retail trade corporations. US profits are, therefore, based on financial accounting standards, not profits from current production as in national accounts. Quarterly rates of return are calculated and published as the annual rate of profit before taxes and dividing by stockholders equity at the end of the quarter. Industries are defined according to the North American Industry Classification System (NAICS): the change from the Standard Industrial Classification (SIC) took place in the fourth quarter of Manufacturing corporations with assets over $250,000 and retail trade companies (as a proxy for service sector companies) with assets of $50 million and over report data. These data are used by the Bureau of Economic Analysis to extrapolate tax-return based estimates which are available with a two-year lag. 25. The Internal Revenue Service of the Department of the United States Treasury also presents United States corporate profits based on tax accounting standards. The balance sheets are based on financial accounting standards. Data are available by industries including manufacturing and services, but rates of return are not calculated. Data are also available for the corporate profits of transportation and public utilities and the wholesale and retail trades. These data are produced in the context of US national accounts, with a two-year time lag. Canada 26. In Canada, the profitability calculations are based on Financial Performance Indicators for Canadian, Volume 1 (Statistics Canada). Financial ratios are available for 144 industries for 1998, 1999 and Volumes 2-3 for the same years and approximately 800 industries will be available in autumn, Data for these years are based on the North American Industrial Classification 3 (NAICS Canada 1997). 27. Data for were based on the 1980 Standard Industrial Classification for Companies and Enterprises (SIC-C 1980). 28. Profitability ratios are the average return on capital for all firms with more than C$5 million in annual revenues. Profits are calculated before interest expenses, taxes and dividends. The number of firms in the survey of non-financial industries (business enterprises controlled by the Government and non-profit enterprises are excluded) was 6,773 in The same survey has been used to report profitability of manufacturing (1,945 companies) and retail trade (939 companies) in Canada. The publication Quarterly Survey of Financial Statistics for Enterprises, releasedbystatisticscanada are now also presented on the basis of NAICS Canada Prior to Q1 1999, the SIC-C 1980 was used. These data form a critical input into the measure of corporate profits and capital consumption allowances in the Canadian System of National Accounts (CSNA) and provide quarterly data on operating profits for all industries. 3 NAICS is a product-oriented industry classification that standardises the way businesses are classified across Canada, Mexico and the United States. NAICS was primarily designed to classify economic production performed at the establishment level. 6

7 Japan 29. Profits data for companies in Japan are the net operating surplus, before receipt and payment of property income and rental income received according to national accounts, based on SNA1993 (Source: Annual report 2001, SNA93). Data for 2001 will be available at the end of Rest of Europe 30. The net rate of return for the Czech Republic is the ratio of net operating surplus compared to capital employed. Net operating surplus is calculated as the difference between output and their operating costs. Capital employed is the net book value of tangible assets, intangible assets and inventories. 31. In Estonia, non-financial company data from the national accounts are used. Profits are before taxes and interest. The return on capital is calculated as the median computed on the basis of data of nonfinancial companies with 20 or more employees for The source of data is the yearbook, Financial Key Ratios 2000 available from the website of the Statistical Office of Estonia. 32. The rates of return for Hungary cover non-financial corporations with double bookkeeping. Profits are calculated after tax. 33. Profitability data in Latvia is drawn from financial indicators of business activity. A statistical bulletin on the website of the Central Statistical Bureau of Latvia presents the analysis of financial reports (balance sheets and the profit and loss accounts of enterprises) of business companies. Profits are defined as profits or loss before taxes. 34. Structural Business Statistics survey in Lithuania includes data on balance sheet and profit/loss accounts of enterprises. Financial ratios are available by NACE activities from For Norway, the net operating surplus of private non-financial corporations is calculated residually, from supply and uses tables. The net operating surplus is published as value added less depreciation and after taxes. 36. National Accounts data have recently been revised. Data prior to 1991 supplied for the 1999 world survey cannot be compared with data supplied for this third survey. This is because of changes to some of the definitions in the national accounts and some reclassifications in other products and services. Norway has also changed the calculation of capital formation for government services. 37. Poland is not yet able to supply data. The current calculation is of gross operating surplus. The calculation of consumption of fixed assets is underway and net operating surplus should be possible by the end of Russia has provided data on the level of profitability of products, by industry. Data were supplied by Goskomstat ( The rates of return are available for 1990, 1995 and Returns are available for all industry products and a ten-industry breakdown. Profits are described as the amount of profit received from the sale of the product less than the cost of the sold product. 39. Profits data for Slovakia are based on the net operating surplus of non-financial corporations (S.11), in accordance with ESA95. 7

8 40. Slovenia has provided profitability ratios based on the net operating surplus for non-financial companies as a ratio of the stock of non-financial assets. Although officially-published data does not presently exist, the Statistical Office of the Republic of Slovenia has made preliminary estimates available. These estimates indicate that the share of GDP contributed by the non-financial sector has risen from 5% in 1994 to 15% in Data for the GDP of the NFC sector includes production and the shares of the NFC sector in taxes on products minus subsidies on products (D21 minus D.31) and in FISIM (for the estimate of NFC sector intermediate consumption). The net operating surplus of the NFC sector is estimates of SNA/ESA B.2n for the NFC sector, using a valuation of gross value added. Rest of World 41. Australia has introduced SNA93 and has calculated gross operating surplus, consumption of fixed capital and net operating surplus by non-financial corporations. The Australian Bureau of Statistics (ABS) has also produced gross operating surplus and gross mixed income and consumption of fixed capital by industry. Manufacturing and services sector profitability can be calculated as a result. Data are consistent with the latest published annual data for The ABS calculates industry value estimates in current prices which have allowed the calculation of sector shares of GDP. The sector property and business services is at 11 per cent of GDP, now equally as large as manufacturing in Australia. 42. Ecuador has provided information for the first time. The Central Bank calculates a quarterly Competitive Trend Index (ICT), data for which are available from January The objective of the ICT is to evaluate performance of the country s levels of competitiveness and to suggest actions for economic policy. 43. The ICT is constructed on the basis of indicators in four areas: Macro-economic environment. Physical, human and technological infrastructure. Political and legal stability. Entrepreneurial costs. 44. Entrepreneurial costs include financial, labour and electricity all of which contribute directly to a company s profitability. The macroeconomic indicators of the availability of bank credit, the openness of the economy and the spread of bank interest rates contribute indirectly. 45. The net operating surplus in Israel was calculated by deducting compensation of employees and an imputation for compensation of self-employed from GDP at basic prices. The rate of return published is for the business sector which is the whole economy less the Government, local authorities and non-profit institutions. 46. Profitability of the manufacturing sector in Korea is defined as the ratio of ordinary income to sales. Manufacturing companies are required to compile quarterly financial statements: companies that compile quarterly financial statements of income and costs account for approximately 70% of total assets of companies in the sector. They include listed countries, enterprises registered at the Korea Securities Dealers Association and the Financial Supervisory Commission. 8

9 47. The Banco de Mexico has provided profitability data for companies in Mexico, from information supplied by the Mexican Stock Exchange. Information on profitability ratios included the return on equity which was used in the article. This ratio is net earnings over net worth minus net earnings. The Stock Exchange also provided data on the return on investment, measured as earnings before taxes and interest over assets. These rates of return were calculated by sampling companies whose stock was listed in the Exchange. Sampling was across the sectors of mining, construction, retail (used as a proxy for the service sector) and communications and transport. 48. Profits of the non-financial corporate sector in South Africa are measured as the net operating surplus (gross operating surplus less consumption of fixed capital). 49. Returns (pre-tax profits) on average equity (1/2 [equity in the current year + equity in previous year]) for companies in Singapore are available from (1999 is the latest available). There is a further breakdown of the company sector into local-controlled and foreign-controlled companies. 50. Profitability ratios for industrial enterprises in China are taken from the ratio of gross profits to sale. Data are published by China Statistics Press in the 2002 China industry economy statistical yearbook. An alternative source with similar results is taking the ratio of profits to industrial costs of all state-owned and non-state-owned industrial enterprises. Data are published in the statistical yearbook published annually by the National Bureau of Statistics. 51. For companies in Iceland, data on income, profits and balance sheets are derived from tax reports. Data covers 98% of all private companies in Iceland. Statistics Iceland has provided comparable data for 1998 through 2000, based on a sample of companies annual data will be ready at the end of 2002; the six-monthly results from listed companies would be available in August Profitability ratios have been calculated as the ratio of profits before tax to equity capital. Profitability ratios of profits as a ratio of operating revenues (turnover) were also available by industries. II. How capital is employed 52. Estimates of capital are the measure of fixed assets and the value of inventories. This includes the value at replacement cost of all fixed assets at the end of a calendar year. The coverage is all tangible assets and intangible assets which have been produced and are themselves repeatedly or continuously used in the processes of production for more than a year. Tangible assets include buildings, plant and machinery. Intangible assets include computer software and mineral exploration costs. For UK Continental Shelf companies, capital assets include mineral exploration costs and oil rigs, but not the oil and gas reserves which are classified as non-produced assets. Inventories include raw materials and fuel which are used up in production. Levels are calculated at book values. Estimates of net capital are net of accumulated capital consumption; i.e. they are a measure of the written down replacement costs of fixed assets. 53. Capital consumption is derived from capital and covers the depreciation of fixed assets over their service lives. Rates of return are sensitive to asset lives, but the effect is less than one might intuitively expect. For example, a shorter asset life reduces capital stock. However, capital consumption also falls and offsets some of this. Past sensitivity analyses showed that fairly large differences in asset lives are needed to make a significant difference. 54. The ONS estimates capital stock and capital consumption for the UK using the Perpetual Inventory Method. A review of the coverage and methodology is given in the March 1999 Economic Trends, 9

10 pages The principles behind the methodology in this model-based approach can be summarised as long back series of capital formation by asset, accumulating capital expenditures year by year, deflators by asset and deducting assets when they are deemed to have completed their expected lives. The Office for National Statistics (ONS) produces gross and net measures of capital. The first values the replacement cost of the stock of capital as if new. The second, net stock also measures the wealth of capital, but taking into account the loss of value due to depreciation. 55. The ONS is currently working on an UK index of capital services, to provide a measure of capital input from the capital stock into production and to complement the current wealth measures. The raw data for this remains, however, identical to UK capital stock measures. This heightened interest in capital measurement has particularly focused on the role of investment in information and communication technology (ICT) goods and services. ICT assets have shorter life-lengths than any of the other main asset types (in the UK, computers last about 5 years) and they have large annual falls in prices due largely to improvements in quality. 56. The variables used for service lives by capital type will vary country by country. They will be influenced by the business cycle and by technological change and by environmental conditions (for example, cars may be more prone to rust in some countries). European Union 57. Capital data are not available in Austria. 58. Capital in Belgium is the acquisition value of fixed tangible and intangible assets, before amortisation and an estimate of inventories of raw materials and merchandise. Fixed assets include plant, machinery and equipment, furniture and vehicles, leased goods and grounds and real estate. Intangible assets include computer software and research and development costs, patents and licenses, but not goodwill. Net capital is the net book value (i.e. without the amortisation in the current and previous year) of tangible and intangible assets. 59. Capital in Denmark is the net stock of capital at the beginning of each year. 60. Finland has used the Perpetual Inventory Method for compiling capital stock data and straight-line depreciation. Data for the stock of inventories are only available from Capital in France is the average of the two end-of-year non-financial assets. 62. In Germany, net capital is derived from net investment in buildings and machinery. Net capital is derived from the accumulation of investments, after allowing for the cumulated consumption of fixed capital. In the first and second surveys, the capital of all sectors of the economy was used in the calculation of profitability of non-financial corporations. There is no differentiation between non-financial (S.11) and private (S.14) sectors in the calculations of fixed assets/capital stock. The traditional German corporation sectors are S.11, S12 and S.14 together. This accounted for the low profitability ratios in Germany. In the current third survey, the Federal Statistical Office made available net figures for fixed assets and capital stock for industries (A60) with reference to NACE rev.1. This gave net capital data for industries less the financial sector and separate data for manufacturing and services industries. Comparable data for net operating surplus (including mixed income) were also available and new rates of return calculated (approximately 2.5%-3.0% higher than the previous estimates) in the period since

11 63. In Italy, net capital stock of the private sector (less the financial intermediation sector) is at replacement prices and is excluding dwellings (national accounts) and net of depreciation. The method of calculation uses national accounts and the institutional sector accounts. 64. Netherlands does have data on capital for non-financial corporations, but the data have not been sub-divided by the institutional sectors of private non-financial and public corporations. The main difficulties in classification are in transport and in financial and other services. Data for net capital are derived from totals for all industries less the Government sector. This breakdown enables the net capital to be calculated for manufacturing and services sectors. 65. In Portugal, gross capital stock data are available only from 1995 to 1998 and represents nonfinancial assets broken down by industry. 66. Capital data are not available in Sweden. United States 67. In the United States, capital is represented by produced assets : the current-cost value at the end of the year for domestic non-financial corporations of the net stock of equipment and software and of structures and the replacement cost value of inventories. Capital is measured less accumulated depreciation. Canada 68. Capital represents total funds provided by the owners and creditors. It includes borrowings, plus loans from affiliates and total equity. Japan 69. In Japan, the value of net fixed capital and inventories are recorded at replacement cost. Capital consumption is valued at book value. Capital includes intangible assets such as software. Capital and capital consumption data are not available by industry. Rest of Europe 70. In Estonia, capital is defined as equity and debt obligations and long-term liabilities. 71. In Hungary and Latvia, capital is defined as owners equity. 72. In Norway, capital includes only fixed assets. The value of inventories has not yet been estimated. Service lives are assumed to be years for buildings and years for machinery and equipment. Net capital stock is published. 73. In Slovakia, capital is measured by tangible and intangible fixed assets valued in acquisition prices (i.e., historic cost). 74. The stock of non-financial assets for the non-financial sector in Slovenia is averages from end-year and beginning of the year data. Source for these data is Bank of Slovenia reporting to Eurostat. 11

12 Rest of World 75. Australia has introduced SNA93 and has calculated capital stock (excluding ownership transfer costs) by industry. Gross fixed capital formation (chain volume measures and at current prices) and end-year net capital stock (chain volume measures and at current prices) by non-financial corporations are now available. The Australian Bureau of Statistics has also produced the end-year average age of gross stock and an experimental capital services index. The references for the index of the flow of capital services is = The index has a wider scope than the capital stock estimates which are restricted to produced assets. 76. In Israel, data on capital stock do not include inventories. 77. Capital stock in South Africa is measured at replacement value and includes inventories at book value. 12

13 13 STD/NA(2002)27

14 14

DG TAXUD. STAT/11/100 1 July 2011

DG TAXUD STAT/11/100 1 July 2011 Taxation trends in the European Union Recession drove EU27 overall tax revenue down to 38.4% of GDP in 2009 Half of the Member States hiked the standard rate of VAT since

DG TAXUD STAT/11/100 1 July 2011 Taxation trends in the European Union Recession drove EU27 overall tax revenue down to 38.4% of GDP in 2009 Half of the Member States hiked the standard rate of VAT since

Second estimate for the first quarter of 2010 EU27 current account deficit 34.8 bn euro 10.8 bn euro surplus on trade in services

109/2010-22 July 2010 Second estimate for the first quarter of 2010 EU27 current account deficit 34.8 bn euro 10.8 bn euro surplus on trade in According to the latest revisions 1, the EU27 2 external current

109/2010-22 July 2010 Second estimate for the first quarter of 2010 EU27 current account deficit 34.8 bn euro 10.8 bn euro surplus on trade in According to the latest revisions 1, the EU27 2 external current

EUROPA - Press Releases - Taxation trends in the European Union EU27 tax...of GDP in 2008 Steady decline in top corporate income tax rate since 2000

DG TAXUD STAT/10/95 28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio1

DG TAXUD STAT/10/95 28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio1

Gross domestic product of Montenegro in 2011

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 257 Podgorica, 28 September 2012 When using the data please name the source Gross domestic product of Montenegro in 2011 Real growth rate of gross domestic

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 257 Podgorica, 28 September 2012 When using the data please name the source Gross domestic product of Montenegro in 2011 Real growth rate of gross domestic

Gross domestic product of Montenegro for period

MONTENEGRO STATISTICAL OFFICE RELEASE No: 211 Podgorica, 30. September 2015 When using these data, please name the source Gross domestic product of Montenegro for period 2010-2014 Real growth rate of gross

MONTENEGRO STATISTICAL OFFICE RELEASE No: 211 Podgorica, 30. September 2015 When using these data, please name the source Gross domestic product of Montenegro for period 2010-2014 Real growth rate of gross

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

OECD Health Policy Unit. 10 June, 2001

The State of Implementation of the OECD Manual: A System of Health Accounts (SHA) in OECD Member Countries, 2001 OECD Health Policy Unit 10 June, 2001 TABLE OF CONTENTS Summary...3 Introduction...4 Background

The State of Implementation of the OECD Manual: A System of Health Accounts (SHA) in OECD Member Countries, 2001 OECD Health Policy Unit 10 June, 2001 TABLE OF CONTENTS Summary...3 Introduction...4 Background

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

CANADA EUROPEAN UNION

THE EUROPEAN UNION S PROFILE Economic Indicators Gross domestic product (GDP) at purchasing power parity (PPP): US$20.3 trillion (2016) GDP per capita at PPP: US$39,600 (2016) Population: 511.5 million

THE EUROPEAN UNION S PROFILE Economic Indicators Gross domestic product (GDP) at purchasing power parity (PPP): US$20.3 trillion (2016) GDP per capita at PPP: US$39,600 (2016) Population: 511.5 million

Taxation trends in the European Union Further increase in VAT rates in 2012 Corporate and top personal income tax rates inch up after long decline

STAT/12/77 21 May 2012 Taxation trends in the European Union Further increase in VAT rates in 2012 Corporate and top personal income tax rates inch up after long decline The average standard VAT rate 1

STAT/12/77 21 May 2012 Taxation trends in the European Union Further increase in VAT rates in 2012 Corporate and top personal income tax rates inch up after long decline The average standard VAT rate 1

GENERAL GOVERNMENT DATA

GENERAL GOVERNMENT DATA General Government Revenue, Expenditure, Balances and Gross Debt PART I: Tables by country AUTUMN 2013 Economic and Financial Affairs EUROPEAN COMMISSION DIRECTORATE GENERAL ECFIN

GENERAL GOVERNMENT DATA General Government Revenue, Expenditure, Balances and Gross Debt PART I: Tables by country AUTUMN 2013 Economic and Financial Affairs EUROPEAN COMMISSION DIRECTORATE GENERAL ECFIN

Gross domestic product of Montenegro in 2016

MONTENEGRO STATISTICAL OFFICE R E L E A S E No:174 Podgorica 29 September 2017 When using the data pleaase name the source Gross domestic product of Montenegro in 2016 Real growth rate of gross domestic

MONTENEGRO STATISTICAL OFFICE R E L E A S E No:174 Podgorica 29 September 2017 When using the data pleaase name the source Gross domestic product of Montenegro in 2016 Real growth rate of gross domestic

Growth in OECD Unit Labour Costs slows to 0.4% in the third quarter of 2016

Growth in OECD Unit Labour Costs slows to.4% in the third quarter of 26 Growth in unit labour costs (ULCs) in the OECD area slowed to.4% in the third quarter of 26 (compared with.6% in the previous quarter)

Growth in OECD Unit Labour Costs slows to.4% in the third quarter of 26 Growth in unit labour costs (ULCs) in the OECD area slowed to.4% in the third quarter of 26 (compared with.6% in the previous quarter)

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

Quarterly Gross Domestic Product of Montenegro 2st quarter 2016

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro 2st quarter 2016 The release presents the preliminary data for quarterly gross domestic product

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro 2st quarter 2016 The release presents the preliminary data for quarterly gross domestic product

Each month, the Office for National

Economic & Labour Market Review Vol 3 No 7 July 2009 FEATURE Jim O Donoghue The public sector balance sheet SUMMARY This article addresses the issues raised by banking groups, including Northern Rock,

Economic & Labour Market Review Vol 3 No 7 July 2009 FEATURE Jim O Donoghue The public sector balance sheet SUMMARY This article addresses the issues raised by banking groups, including Northern Rock,

Burden of Taxation: International Comparisons

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Updates and revisions of national SUTs for the November 2013 release of the WIOD

Updates and revisions of national SUTs for the November 2013 release of the WIOD Edited by Marcel Timmer (University of Groningen) With contributions from: Abdul A. Erumban, Reitze Gouma and Gaaitzen J.

Updates and revisions of national SUTs for the November 2013 release of the WIOD Edited by Marcel Timmer (University of Groningen) With contributions from: Abdul A. Erumban, Reitze Gouma and Gaaitzen J.

Lowest implicit tax rates on labour in Malta, on consumption in Spain and on capital in Lithuania

STAT/13/68 29 April 2013 Taxation trends in the European Union The overall tax-to-gdp ratio in the EU27 up to 38.8% of GDP in 2011 Labour taxes remain major source of tax revenue The overall tax-to-gdp

STAT/13/68 29 April 2013 Taxation trends in the European Union The overall tax-to-gdp ratio in the EU27 up to 38.8% of GDP in 2011 Labour taxes remain major source of tax revenue The overall tax-to-gdp

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Statistical annex. Sources and definitions

Statistical annex Sources and definitions Most of the statistics shown in these tables can be found as well in several other (paper or electronic) publications or references, as follows: the annual edition

Statistical annex Sources and definitions Most of the statistics shown in these tables can be found as well in several other (paper or electronic) publications or references, as follows: the annual edition

Sources of Government Revenue in the OECD, 2016

FISCAL FACT No. 517 July, 2016 Sources of Government Revenue in the OECD, 2016 By Kyle Pomerleau Director of Federal Projects Kevin Adams Research Assistant Key Findings OECD countries rely heavily on

FISCAL FACT No. 517 July, 2016 Sources of Government Revenue in the OECD, 2016 By Kyle Pomerleau Director of Federal Projects Kevin Adams Research Assistant Key Findings OECD countries rely heavily on

Integrated Compilation of Financial and Non-financial Accounts: The Chilean Experience

Integrated Compilation of Financial and Non-financial Accounts: The Chilean Experience Pérez, Josué Central Bank of Chile, National Accounts Department Morandé 115, piso 1 Santiago, Chile E-mail: jnperezt@bcentral.cl

Integrated Compilation of Financial and Non-financial Accounts: The Chilean Experience Pérez, Josué Central Bank of Chile, National Accounts Department Morandé 115, piso 1 Santiago, Chile E-mail: jnperezt@bcentral.cl

Sources of Government Revenue in the OECD, 2018

FISCAL FACT No. 581 Mar. 2018 Sources of Government Revenue in the OECD, 2018 Amir El-Sibaie Analyst Key Findings In 2015, OECD countries relied heavily on consumption taxes, such as the value-added tax,

FISCAL FACT No. 581 Mar. 2018 Sources of Government Revenue in the OECD, 2018 Amir El-Sibaie Analyst Key Findings In 2015, OECD countries relied heavily on consumption taxes, such as the value-added tax,

Sources of Government Revenue in the OECD, 2017

FISCAL FACT No. 558 Aug. 2017 Sources of Government Revenue in the OECD, 2017 Amir El-Sibaie Analyst Key Findings: OECD countries rely heavily on consumption taxes, such as the value-added tax, and social

FISCAL FACT No. 558 Aug. 2017 Sources of Government Revenue in the OECD, 2017 Amir El-Sibaie Analyst Key Findings: OECD countries rely heavily on consumption taxes, such as the value-added tax, and social

Quarterly Financial Accounts Household net worth reaches new peak in Q Irish Household Net Worth

Quarterly Financial Accounts Q4 2017 4 May 2018 Quarterly Financial Accounts Household net worth reaches new peak in Q4 2017 Household net worth rose by 2.1 per cent in Q4 2017. It now exceeds its pre-crisis

Quarterly Financial Accounts Q4 2017 4 May 2018 Quarterly Financial Accounts Household net worth reaches new peak in Q4 2017 Household net worth rose by 2.1 per cent in Q4 2017. It now exceeds its pre-crisis

ICT, knowledge and the economy 2012 Statistical annex

ICT, knowledge and the economy 2012 Statistical annex This annex includes some tables with supplementary figures to the publication ICT, knowledge and the economy 2012. The tables are arranged by chapter.

ICT, knowledge and the economy 2012 Statistical annex This annex includes some tables with supplementary figures to the publication ICT, knowledge and the economy 2012. The tables are arranged by chapter.

Second estimate for the fourth quarter of 2011 EU27 current account surplus 13.1 bn euro 32.3 bn euro surplus on trade in services

59/2012-18 April 2012 Second estimate for the fourth quarter of EU27 current account surplus 13.1 bn euro 32.3 bn euro surplus on trade in According to the latest available data, the EU27 1 external current

59/2012-18 April 2012 Second estimate for the fourth quarter of EU27 current account surplus 13.1 bn euro 32.3 bn euro surplus on trade in According to the latest available data, the EU27 1 external current

Courthouse News Service

14/2009-30 January 2009 Sector Accounts: Third quarter of 2008 Household saving rate at 14.4% in the euro area and 10.7% in the EU27 Business investment rate at 23.5% in the euro area and 23.6% in the

14/2009-30 January 2009 Sector Accounts: Third quarter of 2008 Household saving rate at 14.4% in the euro area and 10.7% in the EU27 Business investment rate at 23.5% in the euro area and 23.6% in the

An implicit tax rate for non-financial corporations: Macro vs micro approach

An implicit tax rate for non-financial corporations: Macro vs micro approach OECD Workshop on Effective Corporate Taxation Paris, 4 July 2006 Claudius Schmidt-Faber Emanuela Tassa An ITR for non-financial

An implicit tax rate for non-financial corporations: Macro vs micro approach OECD Workshop on Effective Corporate Taxation Paris, 4 July 2006 Claudius Schmidt-Faber Emanuela Tassa An ITR for non-financial

Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p)

") MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 46 Podgorica, 22 March 2019 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p) The release

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 46 Podgorica, 22 March 2019 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p) The release

Recommendation of the Council on Tax Avoidance and Evasion

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 224 Podgorica, 22 December 2017 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017 The release

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 224 Podgorica, 22 December 2017 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017 The release

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets

Derivatives Markets") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

PENSIONS IN OECD COUNTRIES: INDICATORS AND DEVELOPMENTS

PENSIONS IN OECD COUNTRIES: INDICATORS AND DEVELOPMENTS Marius Lüske Directorate for Employment, Labour and Social Affairs, OECD Lisbon, 28.09.2018 Marius.LUSKE@oecd.org www.oecd.org/els OUTLINE Talk based

PENSIONS IN OECD COUNTRIES: INDICATORS AND DEVELOPMENTS Marius Lüske Directorate for Employment, Labour and Social Affairs, OECD Lisbon, 28.09.2018 Marius.LUSKE@oecd.org www.oecd.org/els OUTLINE Talk based

DANMARKS NATIONALBANK

DANMARKS NATIONALBANK WEALTH, DEBT AND MACROECONOMIC STABILITY Niels Lynggård Hansen, Head of Economics and Monetary Policy. IARIW, Copenhagen, 21 August 2018 Agenda Descriptive evidence on household debt

DANMARKS NATIONALBANK WEALTH, DEBT AND MACROECONOMIC STABILITY Niels Lynggård Hansen, Head of Economics and Monetary Policy. IARIW, Copenhagen, 21 August 2018 Agenda Descriptive evidence on household debt

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts

Derivatives Markets Turnover for April, 2007 and Amounts") Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

Taxation trends in the European Union EU27 tax ratio at 39.8% of GDP in 2007 Steady decline in top personal and corporate income tax rates since 2000

DG TAXUD STAT/09/92 22 June 2009 Taxation trends in the European Union EU27 tax ratio at 39.8% of GDP in 2007 Steady decline in top personal and corporate income tax rates since 2000 The overall tax-to-gdp

DG TAXUD STAT/09/92 22 June 2009 Taxation trends in the European Union EU27 tax ratio at 39.8% of GDP in 2007 Steady decline in top personal and corporate income tax rates since 2000 The overall tax-to-gdp

THE COMPILATION OF HOUSEHOLD SECTOR ACCOUNTS IN KOREA

For Official Use STD/NA()18 Organisation de Coopération et de Développement Economiques OLIS : 26-Aug-1 Organisation for Economic Co-operation and Development Dist. : 27-Aug-1 Or. Eng. STATISTICS DIRECTORATE

For Official Use STD/NA()18 Organisation de Coopération et de Développement Economiques OLIS : 26-Aug-1 Organisation for Economic Co-operation and Development Dist. : 27-Aug-1 Or. Eng. STATISTICS DIRECTORATE

Stronger growth, but risks loom large

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

PUBLIC PROCUREMENT INDICATORS 2011, Brussels, 5 December 2012

PUBLIC PROCUREMENT INDICATORS 2011, Brussels, 5 December 2012 1. INTRODUCTION This document provides estimates of three indicators of performance in public procurement within the EU. The indicators are

PUBLIC PROCUREMENT INDICATORS 2011, Brussels, 5 December 2012 1. INTRODUCTION This document provides estimates of three indicators of performance in public procurement within the EU. The indicators are

May 2012 Euro area international trade in goods surplus of 6.9 bn euro 3.8 bn euro deficit for EU27

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

First estimate for 2011 Euro area external trade deficit 7.7 bn euro bn euro deficit for EU27

27/2012-15 February 2012 First estimate for 2011 Euro area external trade deficit 7.7 152.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

27/2012-15 February 2012 First estimate for 2011 Euro area external trade deficit 7.7 152.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28

127/2014-18 August 2014 June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

127/2014-18 August 2014 June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

The Architectural Profession in Europe 2012

The Architectural Profession in Europe 2012 - A Sector Study Commissioned by the Architects Council of Europe Chapter 2: Architecture the Market December 2012 2 Architecture - the Market The Construction

The Architectural Profession in Europe 2012 - A Sector Study Commissioned by the Architects Council of Europe Chapter 2: Architecture the Market December 2012 2 Architecture - the Market The Construction

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

June 2012 Euro area international trade in goods surplus of 14.9 bn euro 0.4 bn euro surplus for EU27

121/2012-17 August 2012 June 2012 Euro area international trade in goods surplus of 14.9 0.4 surplus for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

121/2012-17 August 2012 June 2012 Euro area international trade in goods surplus of 14.9 0.4 surplus for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

August 2012 Euro area international trade in goods surplus of 6.6 bn euro 12.6 bn euro deficit for EU27

146/2012-16 October 2012 August 2012 Euro area international trade in goods surplus of 6.6 12.6 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the

146/2012-16 October 2012 August 2012 Euro area international trade in goods surplus of 6.6 12.6 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the

ANNUAL HOURS WORKED Lithuania Austria, Estonia, Greece, Ireland, Latvia, Lithuania, Portugal and the Slovak Republic Australia: Austria: Belgium:

ANNUAL HOURS WORKED The series on annual hours actually worked per person in total employment presented in this table for 35 OECD countries are, in principle, consistent with the series retained for the

ANNUAL HOURS WORKED The series on annual hours actually worked per person in total employment presented in this table for 35 OECD countries are, in principle, consistent with the series retained for the

Sources of Government Revenue in the OECD, 2014

FISCAL FACT Nov. 2014 No. 443 Sources of Government Revenue in the OECD, 2014 By Kyle Pomerleau Economist Key Findings OECD countries rely heavily on consumption taxes, such as the value added tax, and

FISCAL FACT Nov. 2014 No. 443 Sources of Government Revenue in the OECD, 2014 By Kyle Pomerleau Economist Key Findings OECD countries rely heavily on consumption taxes, such as the value added tax, and

Measuring National Output and National Income. Gross Domestic Product. National Income and Product Accounts

C H A P T E R 18 Measuring National Output and National Income Prepared by: Fernando Quijano and Yvonn Quijano Gross Domestic Product Gross domestic product (GDP) is the total market value of all final

C H A P T E R 18 Measuring National Output and National Income Prepared by: Fernando Quijano and Yvonn Quijano Gross Domestic Product Gross domestic product (GDP) is the total market value of all final

STAT/12/ October Household saving rate fell in the euro area and remained stable in the EU27. Household saving rate (seasonally adjusted)

") STAT/12/152 30 October 2012 Quarterly Sector Accounts: second quarter of 2012 Household saving rate down to 12.9% in the euro area and stable at 11. in the EU27 Household real income per capita fell by

STAT/12/152 30 October 2012 Quarterly Sector Accounts: second quarter of 2012 Household saving rate down to 12.9% in the euro area and stable at 11. in the EU27 Household real income per capita fell by

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars. Number of business days

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Guidance on Transfer Pricing Documentation and Country-by-Country Reporting

OECD/G20 Base Erosion and Profit Shifting Project Guidance on Transfer Pricing Documentation and Country-by-Country Reporting ACTION 13: 2014 Deliverable ANNEX III TO CHAPTER V. A MODEL TEMPLATE FOR THE

OECD/G20 Base Erosion and Profit Shifting Project Guidance on Transfer Pricing Documentation and Country-by-Country Reporting ACTION 13: 2014 Deliverable ANNEX III TO CHAPTER V. A MODEL TEMPLATE FOR THE

Budget repair and the changing size of Australia s government. Crawford Australian Leadership Forum John Daley, Grattan Institute June 2016

Budget repair and the changing size of Australia s government Crawford Australian Leadership Forum John Daley, Grattan Institute June 2016 Commonwealth expenditure is high relative to history; revenue

Budget repair and the changing size of Australia s government Crawford Australian Leadership Forum John Daley, Grattan Institute June 2016 Commonwealth expenditure is high relative to history; revenue

Statistical Annex ANNEX

ISBN 92-64-02384-4 OECD Employment Outlook Boosting Jobs and Incomes OECD 2006 ANNEX Statistical Annex Sources and definitions Most of the statistics shown in these tables can be found as well in three

ISBN 92-64-02384-4 OECD Employment Outlook Boosting Jobs and Incomes OECD 2006 ANNEX Statistical Annex Sources and definitions Most of the statistics shown in these tables can be found as well in three

EVCA Mid-Year Survey 2000 January-June

EVCA Mid-Year Survey 2000 January-June 13.5bn invested by 613 private equity houses 57% of respondents confirm a positive growth Venture Capital represented 55% of total investment 50% of investee companies

EVCA Mid-Year Survey 2000 January-June 13.5bn invested by 613 private equity houses 57% of respondents confirm a positive growth Venture Capital represented 55% of total investment 50% of investee companies

Calculation of consolidated core original own funds Overview of the national rules. method

Calculation of consolidated core original own funds Overview of the national rules Annex 7 Country Minority interest Consolidated reserves (negative items) First Translation Differences arising from the

Calculation of consolidated core original own funds Overview of the national rules Annex 7 Country Minority interest Consolidated reserves (negative items) First Translation Differences arising from the

Chart 1. Percent change in manufacturing output per hour,

For release 10:00 a.m. (EDT) Thursday, October 22, 2009 Technical Information: (202) 691-5654 ilchelp@bls.gov www.bls.gov/ilc Media Contact: (202) 691-5902 PressOffice@bls.gov USDL-09-1271 INTERNATIONAL

For release 10:00 a.m. (EDT) Thursday, October 22, 2009 Technical Information: (202) 691-5654 ilchelp@bls.gov www.bls.gov/ilc Media Contact: (202) 691-5902 PressOffice@bls.gov USDL-09-1271 INTERNATIONAL

Non-financial corporations - statistics on profits and investment

Non-financial corporations - statistics on profits and investment Statistics Explained Data extracted in May 2018. Planned article update: May 2019. This article focuses on investment and the distribution

Non-financial corporations - statistics on profits and investment Statistics Explained Data extracted in May 2018. Planned article update: May 2019. This article focuses on investment and the distribution

Working Party on Private Pensions

For Official Use DAFFE/AS/PEN/WD(2000)13/REV2 DAFFE/AS/PEN/WD(2000)13/REV2 For Official Use Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development

For Official Use DAFFE/AS/PEN/WD(2000)13/REV2 DAFFE/AS/PEN/WD(2000)13/REV2 For Official Use Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development

Recommendation of the Council on the Implementation of the Polluter-Pays Principle

Recommendation of the Council on the Implementation of the Polluter-Pays Principle OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces

Recommendation of the Council on the Implementation of the Polluter-Pays Principle OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces

Overview of the deductions from original own funds across Europe

Overview of the deductions from original own funds across Europe Annex 6 Country Own shares Intangible assets Material losses of the current year The net loss as well as substantial negative results. Austria

Overview of the deductions from original own funds across Europe Annex 6 Country Own shares Intangible assets Material losses of the current year The net loss as well as substantial negative results. Austria

ANNEX 3.A1. Description of indicators and method

ANNEX 3.A1 Description of indicators and method The first graph for each country the radar graph illustrates the position of the country against the OECD average performance on a set of common indicators.

ANNEX 3.A1 Description of indicators and method The first graph for each country the radar graph illustrates the position of the country against the OECD average performance on a set of common indicators.

EU BUDGET AND NATIONAL BUDGETS

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT ON BUDGETARY AFFAIRS EU BUDGET AND NATIONAL BUDGETS 1999-2009 October 2010 INDEX Foreward 3 Table 1. EU and National budgets 1999-2009; EU-27

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT ON BUDGETARY AFFAIRS EU BUDGET AND NATIONAL BUDGETS 1999-2009 October 2010 INDEX Foreward 3 Table 1. EU and National budgets 1999-2009; EU-27

Statistical Annex. Sources and definitions

Statistical Annex Sources and definitions Most of the statistics shown in these tables can also be found in two other (paper or electronic) publication and data repository, as follows: The annual edition

Statistical Annex Sources and definitions Most of the statistics shown in these tables can also be found in two other (paper or electronic) publication and data repository, as follows: The annual edition

Working Party on International Trade in Goods and Trade in Services Statistics

Unclassified STD/TBS/WPTGS(2012)32 Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 03-Oct-2012 English - Or. English STATISTICS DIRECTORATE

Unclassified STD/TBS/WPTGS(2012)32 Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 03-Oct-2012 English - Or. English STATISTICS DIRECTORATE

Lithuania: in a wind of change. Robertas Dargis President of the Lithuanian Confederation of Industrialists

Lithuania: in a wind of change Robertas Dargis President of the Lithuanian Confederation of Industrialists 2017 06 15 Lithuanian Confederation of Industrialists - the largest business organisation in Lithuania

Lithuania: in a wind of change Robertas Dargis President of the Lithuanian Confederation of Industrialists 2017 06 15 Lithuanian Confederation of Industrialists - the largest business organisation in Lithuania

REFORMING PENSION SYSTEMS: THE OECD EXPERIENCE

REFORMING PENSION SYSTEMS: THE OECD EXPERIENCE IX Forum Nacional de Seguro de Vida e Previdencia Privada 12 June 2018, São Paulo Jessica Mosher, Policy Analyst, Private Pensions Unit of the Financial Affairs

REFORMING PENSION SYSTEMS: THE OECD EXPERIENCE IX Forum Nacional de Seguro de Vida e Previdencia Privada 12 June 2018, São Paulo Jessica Mosher, Policy Analyst, Private Pensions Unit of the Financial Affairs

January 2014 Euro area international trade in goods surplus 0.9 bn euro 13.0 bn euro deficit for EU28

STAT/14/41 18 March 2014 January 2014 Euro area international trade in goods surplus 0.9 13.0 deficit for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

STAT/14/41 18 March 2014 January 2014 Euro area international trade in goods surplus 0.9 13.0 deficit for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

Second estimate for the third quarter of 2008 EU27 current account deficit 39.5 bn euro 19.3 bn euro surplus on trade in services

STAT/09/12 22 January 2009 Second estimate for the third quarter of 20 EU27 current account deficit 39.5 bn euro 19.3 bn euro surplus on trade in According to the latest revisions1, the EU272 external

STAT/09/12 22 January 2009 Second estimate for the third quarter of 20 EU27 current account deficit 39.5 bn euro 19.3 bn euro surplus on trade in According to the latest revisions1, the EU272 external

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

Capital Cost Recovery across the OECD, 2018

FISCAL FACT No. 590 May 2018 Capital Cost Recovery across the OECD, 2018 Amir El-Sibaie Economist Key Findings A capital allowance is the percentage of total investment that a business can recover through

FISCAL FACT No. 590 May 2018 Capital Cost Recovery across the OECD, 2018 Amir El-Sibaie Economist Key Findings A capital allowance is the percentage of total investment that a business can recover through

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

2015 GNI Questionnaire - Part A Summary Quality Report

Eurostat/C3/GNIC/308A Rev.2 31 ST MEETING OF THE GNI COMMITTEE 21 ST - 22 ND OCTOBER 2015 LUXEMBOURG, BECH BUILDING, ROOM QUETELET 2015 GNI Questionnaire - Part A Summary Quality Report Point IV.1 on the

Eurostat/C3/GNIC/308A Rev.2 31 ST MEETING OF THE GNI COMMITTEE 21 ST - 22 ND OCTOBER 2015 LUXEMBOURG, BECH BUILDING, ROOM QUETELET 2015 GNI Questionnaire - Part A Summary Quality Report Point IV.1 on the

Quarterly Gross Domestic Product of Montenegro for period 1 st quarter rd quarter 2016

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro for period 1 st quarter 015 - rd quarter 016 The release presents the final results of quarterly

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro for period 1 st quarter 015 - rd quarter 016 The release presents the final results of quarterly

Methodology Calculating the insurance gap

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

1 People in Paid Work

1 People in Paid Work Indicator 1.1a Indicator 1.1b Indicator 1.2a Indicator 1.2b Indicator 1.3 Indicator 1.4 Indicator 1.5a Indicator 1.5b Indicator 1.6 Employment and Unemployment Trends (Republic of

1 People in Paid Work Indicator 1.1a Indicator 1.1b Indicator 1.2a Indicator 1.2b Indicator 1.3 Indicator 1.4 Indicator 1.5a Indicator 1.5b Indicator 1.6 Employment and Unemployment Trends (Republic of

Online appendix to Chapter 2: Growth, tangible and intangible investment in the EU and US before and since the Great Recession 1

Online appendix to Chapter 2: Growth, tangible and intangible investment in the EU and before and since the Great Recession 1 Measuring Intangible Investments: the INTAN-Invest database The INTAN-Invest

Online appendix to Chapter 2: Growth, tangible and intangible investment in the EU and before and since the Great Recession 1 Measuring Intangible Investments: the INTAN-Invest database The INTAN-Invest

STATISTICS. Taxing Wages DIS P O NIB LE E N SPECIAL FEATURE: PART-TIME WORK AND TAXING WAGES

AVAILABLE ON LINE DIS P O NIB LE LIG NE www.sourceoecd.org E N STATISTICS Taxing Wages «SPECIAL FEATURE: PART-TIME WORK AND TAXING WAGES 2004-2005 2005 Taxing Wages SPECIAL FEATURE: PART-TIME WORK AND

AVAILABLE ON LINE DIS P O NIB LE LIG NE www.sourceoecd.org E N STATISTICS Taxing Wages «SPECIAL FEATURE: PART-TIME WORK AND TAXING WAGES 2004-2005 2005 Taxing Wages SPECIAL FEATURE: PART-TIME WORK AND

Composition of capital IT044 IT044 POWSZECHNAIT044 UNIONE DI BANCHE ITALIANE SCPA (UBI BANCA)

") Composition of capital POWSZECHNA (in million Euro) Capital position CRD3 rules A) Common equity before deductions (Original own funds without hybrid instruments and government support measures other than

Composition of capital POWSZECHNA (in million Euro) Capital position CRD3 rules A) Common equity before deductions (Original own funds without hybrid instruments and government support measures other than

Statistics Brief. OECD Countries Spend 1% of GDP on Road and Rail Infrastructure on Average. Infrastructure Investment. June

Statistics Brief Infrastructure Investment June 212 OECD Countries Spend 1% of GDP on Road and Rail Infrastructure on Average The latest update of annual transport infrastructure investment and maintenance

Statistics Brief Infrastructure Investment June 212 OECD Countries Spend 1% of GDP on Road and Rail Infrastructure on Average The latest update of annual transport infrastructure investment and maintenance

Seventeenth Meeting of the IMF Committee on Balance of Payments Statistics Pretoria, October 26 29, 2004

BOPCOM-04/13 Seventeenth Meeting of the IMF Committee on Balance of Payments Statistics Pretoria, October 26 29, 2004 International Trade in Services Statistics Monitoring Progress on Implementation of

BOPCOM-04/13 Seventeenth Meeting of the IMF Committee on Balance of Payments Statistics Pretoria, October 26 29, 2004 International Trade in Services Statistics Monitoring Progress on Implementation of

Revenue Statistics Tax revenue trends in the OECD

Revenue Statistics 2017 Tax revenue trends in the OECD OECD 2017 The OECD freely authorises the use of this material for non-commercial purposes, provided that suitable acknowledgment of the source and

Revenue Statistics 2017 Tax revenue trends in the OECD OECD 2017 The OECD freely authorises the use of this material for non-commercial purposes, provided that suitable acknowledgment of the source and

1 People in Paid Work

1 People in Paid Work Indicator 1.1a Indicator 1.1b Indicator 1.2a Indicator 1.2b Indicator 1.3 Indicator 1.4 Indicator 1.5a Indicator 1.5b Indicator 1.6 Employment and Unemployment Trends (Republic of

1 People in Paid Work Indicator 1.1a Indicator 1.1b Indicator 1.2a Indicator 1.2b Indicator 1.3 Indicator 1.4 Indicator 1.5a Indicator 1.5b Indicator 1.6 Employment and Unemployment Trends (Republic of

Measuring International Investment by Multinational Enterprises

Measuring International Investment by Multinational Enterprises Implementation of the OECD s Benchmark Definition of Foreign Direct Investment, 4th edition 5 The 4 th edition of the OECD s Benchmark Definition

Measuring International Investment by Multinational Enterprises Implementation of the OECD s Benchmark Definition of Foreign Direct Investment, 4th edition 5 The 4 th edition of the OECD s Benchmark Definition

MODULE 9. Guidance to completing the Maturity Analysis module of BSL/2

MODULE 9 Guidance to completing the Maturity Analysis module of BSL/2 MATURITY ANALYSIS Overview The Commission recognises that banks may not measure their liquidity using the particular maturity ladder

MODULE 9 Guidance to completing the Maturity Analysis module of BSL/2 MATURITY ANALYSIS Overview The Commission recognises that banks may not measure their liquidity using the particular maturity ladder

139/ October 2006

139/2006-23 October 2006 Provision of deficit and debt data for 2005 Euro area and EU25 government deficit at 2.4% and 2.3% of GDP respectively Government debt at 70.8% and 63.2% In 2005 the government

139/2006-23 October 2006 Provision of deficit and debt data for 2005 Euro area and EU25 government deficit at 2.4% and 2.3% of GDP respectively Government debt at 70.8% and 63.2% In 2005 the government

OECD Report Shows Tax Burdens Falling in Many OECD Countries

OECD Centres Germany Berlin (49-30) 288 8353 Japan Tokyo (81-3) 5532-0021 Mexico Mexico (52-55) 5281 3810 United States Washington (1-202) 785 6323 AUSTRALIA AUSTRIA BELGIUM CANADA CZECH REPUBLIC DENMARK