Incremental Cash Flow: Example

|

|

|

- Ashley Potter

- 6 years ago

- Views:

Transcription

1 Note 8. Making Capital Investment Decisions To include or not to include? that is the question. General Milk Company is currently evaluating the NPV of establishing a line of chocolate milk. As part of the evaluation the company had paid a consulting firm $100,000 to perform a test-marketing analysis. The expenditure was made last year. Should you include this $100,000 as part of the relevant costs for the capital budgeting decision now confronting the management of General Milk Company? 1 2 I. Fundamental Principles of Project Evaluation A project evaluation is an application of one or more capital budgeting decision rules to estimated relevant project cash flows in order to make the investment decision. Then, what is relevant cash flow? Relevent cash flows are the incremental cash flows associated with the decision to invest in a project. The incremental cash flows for project evaluation consist of any and all changes in the firm s future cash flows that are a direct consequence of taking the project. Incremental Cash Flow: Example PharMed Co. is the producer of the best-seller toothpaste EVERSHINE. The company is now considering the introduction of a new formula toothpaste ultra-evershine. EVERSHINE ultra-evershine 3 4 1

2 EVERSHINE Before (Base Case) Revenues: $800M Expenses: $400M Net Cash Flow: $400M ultra-evershine New Product Revenues: $500M Expenses: $250M Net Cash Flow: $250M <Incremental Cash Flows> Every capital budgeting problem compares an investment alternative to a base case. Incremental cash flows in the investment alternative are those which differ from the base case (that is, the difference between the cash flows with a project and the cash flows without the project). Incremental = Cash flow Cash Flow Cash Flow with Project without Project In estimating relevant cash flows from a project, you should include only extra (that is, incremental ) cash flows that would result from the project! In the process, you need to apply the following general rules (in the next slide). 5 6 Sunk Costs: an Example 1 st Stage 2 nd Stage 3 rd Stage Initial test Test drilling Mass Production NPV drilling NPV NPV analysis analysis analysis -$30 million -$200 million -$2 billion 7 8 2

3 Example: Incremental Cash Flow Concept Suppose the Beta Trading Company has an empty warehouse that can be used to store a new line of products. Should the cost of warehouse and land be included in the costs associated with introducing the new line? Example: Incremental Cash Flow Concept General Milk Company is currently evaluating the NPV of establishing a line of chocolate milk. As part of the evaluation the company had paid a consulting firm $100,000 to perform a testmarketing analysis. The expenditure was made last year. Is this cost relevant for the capital budgeting decision now confronting the management of General Milk Company? 9 10 Example: Incremental Cash Flow In 1971, Lockheed sought a federal guarantee for a bank loan to continue development of the TriStar aero-plane. Lockheed and its supporters argued it would be foolish to abandon a project on which nearly $1 billion has already been spent. Some of Lockheed s critics countered that it would be equally foolish to continue with the project that offered no prospect of a satisfactory return on that $1 billion. Whose argument is correct? 11 Is Uber's Service Doomed To Get Worse? A car owner faces two sources of cost: variable use costs and fixed costs. Variable use costs happen with every mile of use, and include gas prices, maintenance, and labor, whereas fixed costs happen no matter what you do, like cost of capital and time depreciation. For someone deciding whether or not to become an Uber driver, the fixed costs are a sunk cost. In the future, when car purchase decisions are made entirely on the net present value of buying the asset and using it as an Uber vehicle, fixed costs won't be sunk costs, but will be part of the NPV consideration. 12 Oct. 31, 201 3

4 II. Cash Flow Revisited Now, once you have determined the incremental cash flows from undertaking a project, you can view the project as a "mini-firm" with its own future revenues and costs, its own assets, and its own cash flows and just focus on the cash flows. Recall how we calculated cash flows from assets. Cash Flow From Assets Cash Flow To Creditors Cash Flow To Equityholders

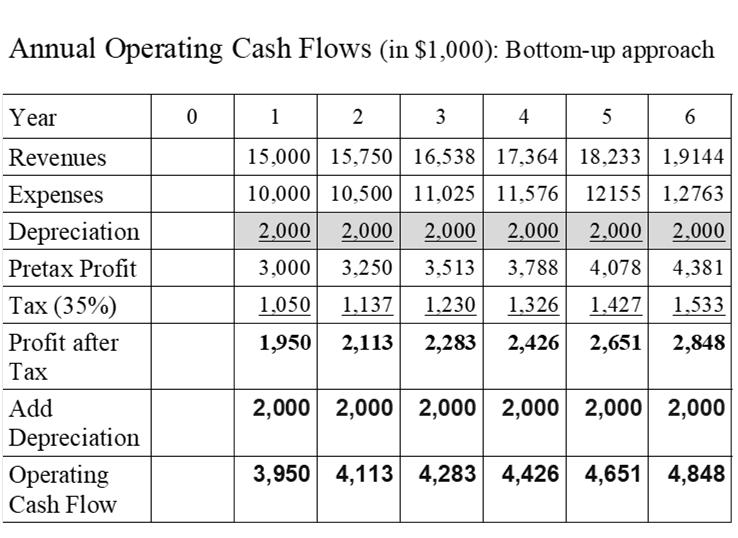

5 III. Example Cash Flow Analysis Using NPV: Nittany Mining As the financial manager of Nittany Mining, you are about to analyze a proposal for developing a new dollarmond mine in the Nittany Mountain area. The following is the summary of the information about the project. 1. Capital Spending: $12 million in mining machinery. After 6 years, the machinery has no further value on the book but can be sold at $5 million. 2. Working Capital: Increases in the initial years, but will be recovered (disinvestment) at the end of the project's life. The schedule for the working capital is as follows: Year Working Capital Sales Revenues: The company expects to sell 7,500 pounds of dollarmond a year at a price of $2,000 a pound in Year 1. That points to initial revenues of 7,500 $2,000 = $15,000,000. Inflation is expected at 5% a year Expenses (or costs): Initially $10 million (Year 1). Then, increases in line with inflation at 5% a year. 5. Depreciation: Straight-line over 6 years for the mining machinery. 6. Tax: 35% of pre-tax profits. 7. The company s capital consists of all equity (no debt). The company s beta is estimated at 0.9. The going risk-free rate is 3%. The market risk premium is estimated at 10%. We will apply NPV, IRR, and PI. We will go through the following steps. Step 1. Forecast the project cash flows based on a pro forma income statement. Step 2. Use the required return to discount the future cash flows. Step 3. Go ahead with the project if the present value of the payoff is greater than the investment (i.e., if NPV > 0)

6 Step 1. Cash Flow Projections We need to fill out the following table in three steps First Component - Capital Spending: First, we have to figure out the amount of capital spending. We know that the capital investment for the mining machine is $12 million at time 0. The machine will bear no book value but can be sold at $5 million in year 6. Taxes on capital gains from sales of fixed assets at project termination Any capital gains from selling fixed assets (i.e., market value less book value) are subject to taxes. Capital gain (from the sale of a fixed asset) = market value book value Tax = capital gain tax rate In our example, Tax = ($5M - $0)(0.35) = $1.75M Hence, after-tax salvage cash flow = $5M - $1.75 = $3.25M

tax rate For example, if you sold an asset worth $10M in the book at $5M, you are eligible for a tax credit of ($10M - $5M)*0.35 = $1.")

7 Taxes on capital losses from sales of fixed assets at project termination When the market value of a fixed asset is below the asset s book value, the gap is subject to a tax credit. Tax credit = (book value market value) tax rate For example, if you sold an asset worth $10M in the book at $5M, you are eligible for a tax credit of ($10M - $5M)*0.35 = $1.75M First Component - Capital Spending: In our case, the after-tax cash flow from the sale of the machine at project termination is $3.25M. (in $1,000) Second Component - Investment in Net Working Capital: Third Component - Operating Cash Flows: We first prepare a pro-forma income statement. Then, we calculate the projected cash flow based on the information provided by the income statement. In the process, we have to pay attention to non-cash items. We can use either the top-down or bottom-up approaches

8

9 Step 2. Use the required return to discount the projected annual cash flows. The company s capital consists of all equity (no debt). The compa ny s beta is estimated at 0.9. The going risk-free rate is 3%. The m arket risk premium is estimated at 10%. According to the CAPM, E(r) = Based on the above calculation, you decide to apply a 12% discount rate to discount your estimated project cash flows Step 3. Calculate the NPV. NPV = PV(CF 0 ) + PV(CF 1 ) + +PV(CF 6 ) = $5,666 (in 000) We accept the investment since its NPV is positive. Other Rules IRR = 22.29% (Using Excel) > 12% (Accept) Profitability Index = $19,166/$13,500 = 1.42 > 1 (Accept)

10 IV. Special Case: Evaluating Investment Options with Different Lives When two different equipment setups, systems, or procedures have different economic lives and when we will need whatever we buy more or less indefinitely, the typical NPV rule, which typically assumes one investment horizon, does not help. In this case, we have to use one of the following: 1.Replacement Chains 2.Equivalent Annual Cost (EAC) 1.Replacement Chains We assume for each of the alternative equipment setups that we purchase it as soon as its life is over until we find a matching cycle. Then, we calculate the present value for each equipment for this matching cycle. The project with the lower PV is chosen. Option A Option B 2 yrs. 2 yrs. 2 yrs. 3 yrs. 3 yrs Example: Replacement Chains You have to choose between two alternatives Life: 5 years Price: $140,000 Annual Maintenance Cost: $8,000 No salvage value after 5 years 5 yrs. 5 yrs. Solution: NPV = $140,000 + $140,000/(1.08) 5 + $8,000 x Annuity PVF( 10 yrs 8%) = $288,962 Life: 10 years Price: $245,000 Annual Maintenance Cost: $7,000 No salvage value after 10 years 10 yrs. Solution: NPV = $245,000 + $7,000 x Annuity PVF( 10 years 8%) = $291,

= $43,063.90 Solution: NPV = $245,000 + $7,000 x Annuity PVF( 10 yrs 8%) = $291,970.57 EAC = $291,970.")

11 If we apply EAC to the truck example. Solution: PV of Costs = $140,000 + $8,000 x Annuity PVF( 5 yrs 8%) =$171, EAC = $171,941.68/Annuity PVF( 5 yrs 8%) = $43, Solution: NPV = $245,000 + $7,000 x Annuity PVF( 10 yrs 8%) = $291, EAC = $291,970.57/Annuity PVF( 10 yrs 8%) = $43,

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

Exercises Corporate Finance

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Measuring Investment Returns

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle

CHAPTER 8 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 8 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concept Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a project. The relevant

CHAPTER 8 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concept Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a project. The relevant

INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS

CHAPTER8 INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS PROBABILISTIC APPROACH Question 1: A project under consideration is likely to cost `5 lakh by way of fixed assets and requires

CHAPTER8 INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS PROBABILISTIC APPROACH Question 1: A project under consideration is likely to cost `5 lakh by way of fixed assets and requires

1) Side effects such as erosion should be considered in a capital budgeting decision.

Side effects such as erosion should be considered in a capital budgeting decision.") Questions Chapter 10 1) Side effects such as erosion should be considered in a capital budgeting decision. [B] :A project s cash flows should include all changes in a firm s future cash flows. This includes

Questions Chapter 10 1) Side effects such as erosion should be considered in a capital budgeting decision. [B] :A project s cash flows should include all changes in a firm s future cash flows. This includes

Should there be a risk premium for foreign projects?

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

DISCOUNTED CASH-FLOW ANALYSIS

DISCOUNTED CASH-FLOW ANALYSIS Objectives: Study determinants of incremental cash flows Estimate incremental after-tax cash flows from accounting data and use them to estimate NPV Introduce salvage value

DISCOUNTED CASH-FLOW ANALYSIS Objectives: Study determinants of incremental cash flows Estimate incremental after-tax cash flows from accounting data and use them to estimate NPV Introduce salvage value

Note: it is your responsibility to verify that this examination has 16 pages.

UNIVERSITY OF MANITOBA Faculty of Management Department of Accounting and Finance 9.0 Corporation Finance Professors: A. Dua, J. Falk, and R. Scott February 8, 006; 6:30 p.m. - 8:30 p.m. Note: it is your

UNIVERSITY OF MANITOBA Faculty of Management Department of Accounting and Finance 9.0 Corporation Finance Professors: A. Dua, J. Falk, and R. Scott February 8, 006; 6:30 p.m. - 8:30 p.m. Note: it is your

AFM 271. Midterm Examination #2. Friday June 17, K. Vetzal. Answer Key

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Finance 100 Problem Set Capital Budgeting

Finance 100 Problem Set Capital Budgeting 1. Consider the following capital budgeting problem. The following two machines are mutually exclusive and the firm would keep reinvesting in whatever machine

Finance 100 Problem Set Capital Budgeting 1. Consider the following capital budgeting problem. The following two machines are mutually exclusive and the firm would keep reinvesting in whatever machine

Tables of discount factors and annuity factors are provided in the appendix at the end of the paper.

UNIVERSITY OF EAST ANGLIA Norwich Business School Main Series UG Examination 2016-17 BUSINESS FINANCE NBS-5008Y Time allowed: 3 hours Answer FOUR questions out of six ALL questions carry EQUAL marks Tables

UNIVERSITY OF EAST ANGLIA Norwich Business School Main Series UG Examination 2016-17 BUSINESS FINANCE NBS-5008Y Time allowed: 3 hours Answer FOUR questions out of six ALL questions carry EQUAL marks Tables

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

Time Value of Money. PV of Multiple Cash Flows. Present Value & Discounting. Future Value & Compounding. PV of Multiple Cash Flows

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting. Konan Chan Financial Management, Time Value of Money

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

PMBA 8135 Take Home Problem Set 3 Spring 2014

PMBA 8135 Take Home Problem Set 3 Spring 2014 Directions: Determine or compute an answer for each question/problem on this problem set. After you have computed an answer for every question, enter your

PMBA 8135 Take Home Problem Set 3 Spring 2014 Directions: Determine or compute an answer for each question/problem on this problem set. After you have computed an answer for every question, enter your

*Efficient markets assumed

LECTURE 1 Introduction To Corporate Projects, Investments, and Major Theories Corporate Finance It is about how corporations make financial decisions. It is about money and markets, but also about people.

LECTURE 1 Introduction To Corporate Projects, Investments, and Major Theories Corporate Finance It is about how corporations make financial decisions. It is about money and markets, but also about people.

Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

CAPITAL BUDGETING PRACTICE PROBLEMS. Self-Study Question

CAPITAL BUDGETING PRACTICE PROBLEMS Self-Study Question Nu-Concepts, Inc., a southeastern advertising agency, is considering the purchase of new computer equipment and software to enhance its graphics

CAPITAL BUDGETING PRACTICE PROBLEMS Self-Study Question Nu-Concepts, Inc., a southeastern advertising agency, is considering the purchase of new computer equipment and software to enhance its graphics

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Aswath Damodaran. Value Trade Off. Cash flow benefits - Tax benefits - Better project choices. What is the cost to the firm of hedging this risk?

Value Trade Off Negligible What is the cost to the firm of hedging this risk? High Cash flow benefits - Tax benefits - Better project choices Is there a significant benefit in terms of higher cash flows

Value Trade Off Negligible What is the cost to the firm of hedging this risk? High Cash flow benefits - Tax benefits - Better project choices Is there a significant benefit in terms of higher cash flows

Indian River Citrus Company (A)

") Case 12 Indian River Citrus Company (A) Capital Budgeting Directed Indian River Citrus Company is a leading producer of fresh, frozen, and made-from-concentrate citrus drinks. The firm was founded in 1929

Case 12 Indian River Citrus Company (A) Capital Budgeting Directed Indian River Citrus Company is a leading producer of fresh, frozen, and made-from-concentrate citrus drinks. The firm was founded in 1929

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

Analyzing Project Cash Flows. Chapter 12

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

COMM 298 INTRO TO FINANCE 2016 WINTER TERM2 [FINAL] BY LEAH ZHANG

![COMM 298 INTRO TO FINANCE 2016 WINTER TERM2 [FINAL] BY LEAH ZHANG](/thumbs/77/76249397.jpg "COMM 298 INTRO TO FINANCE 2016 WINTER TERM2 [FINAL] BY LEAH ZHANG") COMM 298 INTRO TO FINANCE 2016 WINTER TERM2 [FINAL] BY LEAH ZHANG TABLE OF CONTENT I. Introduction II. Summary III. Sample Questions IV. Past Exams V. Q&A VI. Feedback Form INTRODUCTION Tutor: - Leah Zhang

COMM 298 INTRO TO FINANCE 2016 WINTER TERM2 [FINAL] BY LEAH ZHANG TABLE OF CONTENT I. Introduction II. Summary III. Sample Questions IV. Past Exams V. Q&A VI. Feedback Form INTRODUCTION Tutor: - Leah Zhang

Chapter 4. Establishing the Planning Horizon & MARR. Principles of Engineering Economic Analysis, 5th edition

Chapter 4 Establishing the Planning Horizon & MARR Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate

Chapter 4 Establishing the Planning Horizon & MARR Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate

Chapter 11 Cash Flow Estimation and Risk Analysis ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 11 Cash Flow Estimation and Risk Analysis ANSWERS TO END-OF-CHAPTER QUESTIONS 11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the actual flow of cash,

Chapter 11 Cash Flow Estimation and Risk Analysis ANSWERS TO END-OF-CHAPTER QUESTIONS 11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the actual flow of cash,

Institute of Certified Management Accountants of Sri Lanka. Strategic Level May 2012 Examination. Financial Strategy and Policy (FSP / SL 3-403)

") Copyright Reserved Serial No Strategic Level May 2012 Examination Examination Date : 12 th May 2012 Number of Pages : 08 Examination Time: 9.30 a:m. 12.30 p:m. Number of Questions: 05 Instructions to Candidates

Copyright Reserved Serial No Strategic Level May 2012 Examination Examination Date : 12 th May 2012 Number of Pages : 08 Examination Time: 9.30 a:m. 12.30 p:m. Number of Questions: 05 Instructions to Candidates

3 Leasing Decisions. The Institute of Chartered Accountants of India

3 Leasing Decisions BASIC CONCEPTS AND FORMULAE 1. Introduction Lease can be defined as a right to use an equipment or capital goods on payment of periodical amount. Two principal parties to any lease

3 Leasing Decisions BASIC CONCEPTS AND FORMULAE 1. Introduction Lease can be defined as a right to use an equipment or capital goods on payment of periodical amount. Two principal parties to any lease

Chapter 10: Making Capital Investment Decisions. Faculty of Business Administration Lakehead University Spring 2003 May 21, 2003

Chapter 10: Making Capital Investment Decisions Faculty of Business Administration Lakehead University Spring 2003 May 21, 2003 Outline 10.1 Project Cash Flows: A First Look 10.2 Incremental Cash Flows

Chapter 10: Making Capital Investment Decisions Faculty of Business Administration Lakehead University Spring 2003 May 21, 2003 Outline 10.1 Project Cash Flows: A First Look 10.2 Incremental Cash Flows

What is it? Measure of from project. The Investment Rule: Accept projects with NPV and accept highest NPV first

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

b) What is sunk cost? Is it relevant when evaluating proposed capital budgeting project? Explain.

What is sunk cost? Is it relevant when evaluating proposed capital budgeting project? Explain.") KARACHI UNIVERSITY BUSINESS SCHOOL University of Karachi FINAL EXAMINATION, DECEMBER 2009; AFFILIATED COLLEGES Date: January 07, 2010 Max Marks: 60 Max Time: 3 Hours INSTRUCTION: Attempt Any FIVE Questions.

KARACHI UNIVERSITY BUSINESS SCHOOL University of Karachi FINAL EXAMINATION, DECEMBER 2009; AFFILIATED COLLEGES Date: January 07, 2010 Max Marks: 60 Max Time: 3 Hours INSTRUCTION: Attempt Any FIVE Questions.

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E

1 P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E 2 The objective of a manager is to maximize NPV of cash flows and is

1 P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E 2 The objective of a manager is to maximize NPV of cash flows and is

FIN 350 Business Finance Homework 7 Fall 2014 Solutions

FIN 350 Business Finance Homework 7 Fall 2014 Solutions 1. Home Builder Supply, a retailer in the home improvement industry, currently operates seven retail outlets in Georgia and South Carolina. Management

FIN 350 Business Finance Homework 7 Fall 2014 Solutions 1. Home Builder Supply, a retailer in the home improvement industry, currently operates seven retail outlets in Georgia and South Carolina. Management

Capital Budgeting, Part II

Capital Budgeting, Part II Lakehead University Fall 2004 Making Capital Investment Decisions 1. Project Cash Flows 2. Incremental Cash Flows 3. Basic Capital Budgeting 4. Capital Cost Allowance 5. The

Capital Budgeting, Part II Lakehead University Fall 2004 Making Capital Investment Decisions 1. Project Cash Flows 2. Incremental Cash Flows 3. Basic Capital Budgeting 4. Capital Cost Allowance 5. The

Final Examination (Optional) MASTERING DEPRECIATION

MASTERING DEPRECIATION") Final Examination (Optional) MASTERING DEPRECIATION Instructions: Detach the Final Examination Answer Sheet on page 247 before beginning your final examination. Select the correct letter for the answer

Final Examination (Optional) MASTERING DEPRECIATION Instructions: Detach the Final Examination Answer Sheet on page 247 before beginning your final examination. Select the correct letter for the answer

Chapter Review Problems

Chapter Review Problems Unit 19.1 Depreciation for financial accounting 1. Depreciation for financial accounting is identical to depreciation for federal income tax purposes. (T or F) False For Problems

Chapter Review Problems Unit 19.1 Depreciation for financial accounting 1. Depreciation for financial accounting is identical to depreciation for federal income tax purposes. (T or F) False For Problems

Chapter 8. Rate of Return Analysis. Principles of Engineering Economic Analysis, 5th edition

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

ACCTG101 Revision MODULES 10 & 11 LITTLE NOTABLES EXCLUSIVE - VICKY TANG

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

FREDERICK OWUSU PREMPEH

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 5 Advanced Investment Appraisal & Application of option pricing

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 5 Advanced Investment Appraisal & Application of option pricing

Chapter 8: Fundamentals of Capital Budgeting

Chapter 8: Fundamentals of Capital Budgeting - 1 Chapter 8: Fundamentals of Capital Budgeting Note: Read the chapter then look at the following. Fundamental question: How do we determine the cash flows

Chapter 8: Fundamentals of Capital Budgeting - 1 Chapter 8: Fundamentals of Capital Budgeting Note: Read the chapter then look at the following. Fundamental question: How do we determine the cash flows

Exercise Session #3 Suggested Solutions

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Date: 17/10/2017 Exercise Session #3 Suggested Solutions Problem 1. (6.20 Marsha Jones has bought a used Mercedes horse transporter

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Date: 17/10/2017 Exercise Session #3 Suggested Solutions Problem 1. (6.20 Marsha Jones has bought a used Mercedes horse transporter

Performance Pillar. P1 Performance Operations. 24 November 2010 Wednesday Morning Session

Performance Pillar P1 Performance Operations 24 November 2010 Wednesday Morning Session Instructions to candidates You are allowed three hours to answer this question paper. You are allowed 20 minutes

Performance Pillar P1 Performance Operations 24 November 2010 Wednesday Morning Session Instructions to candidates You are allowed three hours to answer this question paper. You are allowed 20 minutes

CAPITAL BUDGETING. Key Terms and Concepts to Know

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

Solutions to this Item Set can be found on our Level 2 Test Bank.

Capital Budgeting Project Analysis Cash Flows 1) investment outlay equipment cost, working capital 2) after tax operating cash flows net income + depreciation 3) terminal year non-operating cash flows

Capital Budgeting Project Analysis Cash Flows 1) investment outlay equipment cost, working capital 2) after tax operating cash flows net income + depreciation 3) terminal year non-operating cash flows

PM013: Project Management Detailed Engineering for Capital Projects

PM013: Project Management Detailed Engineering for Capital Projects PM013 Rev.001 CMCT COURSE OUTLINE Page 1 of 6 Training Description: Large capital-intensive projects require substantial and often risky

PM013: Project Management Detailed Engineering for Capital Projects PM013 Rev.001 CMCT COURSE OUTLINE Page 1 of 6 Training Description: Large capital-intensive projects require substantial and often risky

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MAMANGMENT JUNE 2011 Suggested

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MAMANGMENT JUNE 2011 Suggested

PMP045 Project Management Detailed Engineering for Capital Projects

PMP045 Project Management Detailed Engineering for Capital Projects H.H. Sheik Sultan Tower (0) Floor Corniche Street Abu Dhabi U.A.E www.ictd.ae ictd@ictd.ae Course Introduction: Large capital-intensive

PMP045 Project Management Detailed Engineering for Capital Projects H.H. Sheik Sultan Tower (0) Floor Corniche Street Abu Dhabi U.A.E www.ictd.ae ictd@ictd.ae Course Introduction: Large capital-intensive

5. The beta of a company is a function of a number of factors. Perhaps the three most important are:

Page 423 Summary and Conclusions Earlier chapters on capital budgeting assumed that projects generate riskless cash flows. The appropriate discount rate in that case is the riskless interest rate. Of course,

Page 423 Summary and Conclusions Earlier chapters on capital budgeting assumed that projects generate riskless cash flows. The appropriate discount rate in that case is the riskless interest rate. Of course,

Project Free Cash Flows = NOPAT + Depreciation Gross Investment in Fixed Operating Assets Investment in Operating Working Capital

Project Free Cash Flows = NOPAT + Depreciation Gross Investment in Fixed Operating Assets Investment in Operating Working Capital = EBIT (1 t) + Depreciation Gross Investment in Fixed Operating Assets

Project Free Cash Flows = NOPAT + Depreciation Gross Investment in Fixed Operating Assets Investment in Operating Working Capital = EBIT (1 t) + Depreciation Gross Investment in Fixed Operating Assets

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

University of Alabama Culverhouse College of Business. Intermediate Financial Management

University of Alabama Culverhouse College of Business FI 410 Intermediate Financial Management Dr. Anup Agrawal Test 1 (Practice) Instructions: Answer all questions. Show all work. There is partial credit

University of Alabama Culverhouse College of Business FI 410 Intermediate Financial Management Dr. Anup Agrawal Test 1 (Practice) Instructions: Answer all questions. Show all work. There is partial credit

Hire Purchase and Instalment Sale Transactions

11 Hire Purchase and Instalment Sale Transactions Learning Objectives After studying this chapter, you will be able to: Understand the salient features and nature of Hire purchase transactions. Journalise

11 Hire Purchase and Instalment Sale Transactions Learning Objectives After studying this chapter, you will be able to: Understand the salient features and nature of Hire purchase transactions. Journalise

NPV Method. Payback Period

1. Why the payback method is often considered inferior to discounted cash flow in capital investment appraisal? A. It does not take account of the time value of money B. It does not calculate how long

1. Why the payback method is often considered inferior to discounted cash flow in capital investment appraisal? A. It does not take account of the time value of money B. It does not calculate how long

c) (3 pts.) Based on this Balance Sheet, what is the Current Ratio on 1/1/2010?

(3 pts.) Based on this Balance Sheet, what is the Current Ratio on 1/1/2010?") AAE 320 Spring 2010 Exam #2 Name: 1) (16 pts. total) a) (5 pts.) Use the information given and your knowledge of the relationships among Balance Sheet entries to fill in the five missing cells and then

AAE 320 Spring 2010 Exam #2 Name: 1) (16 pts. total) a) (5 pts.) Use the information given and your knowledge of the relationships among Balance Sheet entries to fill in the five missing cells and then

Capital investment decisions

Chapter 20 Capital investment decisions Business Accounting and Finance 2nd Edition Questions 1. The Tullane Biscuit Company plc is a successful biscuit manufacturer. Since it was established five years

Chapter 20 Capital investment decisions Business Accounting and Finance 2nd Edition Questions 1. The Tullane Biscuit Company plc is a successful biscuit manufacturer. Since it was established five years

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

ACC501 Current 11 Solved Finalterm Papers and Important MCQS

ACC501 Current 11 Solved Finalterm Papers and Important MCQS Solved By EXAMINATION Question No: 1 The accounting definition of income is: Income = Current Assets Income = Fixed Assets - -Current Liabilities

ACC501 Current 11 Solved Finalterm Papers and Important MCQS Solved By EXAMINATION Question No: 1 The accounting definition of income is: Income = Current Assets Income = Fixed Assets - -Current Liabilities

Six Ways to Perform Economic Evaluations of Projects

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Risk, Return and Capital Budgeting

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

JEM034 Corporate Finance Winter Semester 2018/2019

JEM034 Corporate Finance Winter Semester 2018/2019 Lecture #4 Olga Bychkova Topics Covered Today Finalize more practical guidance on making investment decisions with NPV rule and capital budgeting (chapter

JEM034 Corporate Finance Winter Semester 2018/2019 Lecture #4 Olga Bychkova Topics Covered Today Finalize more practical guidance on making investment decisions with NPV rule and capital budgeting (chapter

Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

Principles of Engineering Economic Analysis, 5th edition") Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) 0 1 2 3 4 5 ( - ) Time $2,000 $3,000 $4,000 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A)

Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) 0 1 2 3 4 5 ( - ) Time $2,000 $3,000 $4,000 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A)

Chapter 7 Making Capital Investment Decisions: Further Issues

Making Capital Investment Decisions: Further Issues Solutions to Even-Numbered Problems and Cases 7.2 James Bay Geological Engineering Company Discount rate, 8% Project Cash Flows thousands) Year Machine

Making Capital Investment Decisions: Further Issues Solutions to Even-Numbered Problems and Cases 7.2 James Bay Geological Engineering Company Discount rate, 8% Project Cash Flows thousands) Year Machine

Chapter 6 Capital Budgeting

Chapter 6 Capital Budgeting The objectives of this chapter are to enable you to: Understand different methods for analyzing budgeting of corporate cash flows Determine relevant cash flows for a project

Chapter 6 Capital Budgeting The objectives of this chapter are to enable you to: Understand different methods for analyzing budgeting of corporate cash flows Determine relevant cash flows for a project

CHAPTER 5 ACQUISITIONS: PURCHASE AND USE OF BUSINESS ASSETS

CHAPTER 5 ACQUISITIONS: PURCHASE AND USE OF BUSINESS ASSETS Acquisition Costs (p. 173) When a company buys a long-term asset, the asset account (e.g., Equipment, Machinery, or Furniture) is increased.

CHAPTER 5 ACQUISITIONS: PURCHASE AND USE OF BUSINESS ASSETS Acquisition Costs (p. 173) When a company buys a long-term asset, the asset account (e.g., Equipment, Machinery, or Furniture) is increased.

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #3 Olga Bychkova Topics Covered Today Making investment decisions with NPV rule (more practical guidance) and capital budgeting (chapter 6 in

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #3 Olga Bychkova Topics Covered Today Making investment decisions with NPV rule (more practical guidance) and capital budgeting (chapter 6 in

Options in Corporate Finance

FIN 614 Corporate Applications of Option Theory Professor Robert B.H. Hauswald Kogod School of Business, AU Options in Corporate Finance The value of financial and managerial flexibility: everybody values

FIN 614 Corporate Applications of Option Theory Professor Robert B.H. Hauswald Kogod School of Business, AU Options in Corporate Finance The value of financial and managerial flexibility: everybody values

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Sample Questions for Chapters 10 & 11

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Chapter 8. Fundamentals of Capital Budgeting

Chapter 8 Fundamentals of Capital Budgeting Chapter Outline 8.1 Forecasting Earnings 8.2 Determining Free Cash Flow and NPV 8.3 Choosing Among Alternatives 8.4 Further Adjustments to Free Cash Flow 8.5

Chapter 8 Fundamentals of Capital Budgeting Chapter Outline 8.1 Forecasting Earnings 8.2 Determining Free Cash Flow and NPV 8.3 Choosing Among Alternatives 8.4 Further Adjustments to Free Cash Flow 8.5

Lecture 7. Strategy and Analysis in Using Net Present Value

Lecture 7 Strategy and Analysis in Using Net Present Value Strategy and Analysis in Using Net Present Value Decision Trees Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis Monte Carlo Simulation

Lecture 7 Strategy and Analysis in Using Net Present Value Strategy and Analysis in Using Net Present Value Decision Trees Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis Monte Carlo Simulation

THE FINANCIAL EVALUTATION OF INVESTMENTS: THE TIME VALUE OF MONEY, THE PRESENT VALUE, NPV, IRR

THE FINANCIAL EVALUTATION OF INVESTMENTS: THE TIME VALUE OF MONEY, THE PRESENT VALUE, NPV, IRR Lesson 9 Castellanza, 15 th November 2017 SUMMARY The investment definition and analysis Financial value of

THE FINANCIAL EVALUTATION OF INVESTMENTS: THE TIME VALUE OF MONEY, THE PRESENT VALUE, NPV, IRR Lesson 9 Castellanza, 15 th November 2017 SUMMARY The investment definition and analysis Financial value of

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8. CA. Anurag Singal

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8 CA. Anurag Singal Internal Rate of Return Miscellaneous Sums Internal Rate of Return (IRR) is the rate at which NPV = 0 XYZ Ltd., an

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8 CA. Anurag Singal Internal Rate of Return Miscellaneous Sums Internal Rate of Return (IRR) is the rate at which NPV = 0 XYZ Ltd., an

Before discussing capital expenditure decision methods, we may understand following three points:

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

ECMB36 LECTURE NOTES DISCOUNTING AND NET PRESENT VALUE

ECMB36 LECTURE NOTES DISCOUNTING AND NET PRESENT VALUE Townley, Chapters 2 & 3 Many private and public decisions can have important consequences that extend overtime. Assume discount rate is given, will

ECMB36 LECTURE NOTES DISCOUNTING AND NET PRESENT VALUE Townley, Chapters 2 & 3 Many private and public decisions can have important consequences that extend overtime. Assume discount rate is given, will

MAXIMISE SHAREHOLDERS WEALTH.

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

Shanghai Jiao Tong University. FI410 Corporate Finance

Shanghai Jiao Tong University FI410 Corporate Finance Instructor: Xiaorong Zhang Email: xrzhang@fudan.edu.cn Home Institution: Office Hours: Fudan University Office: Term: 2 July - 2 August, 2018 Credits:

Shanghai Jiao Tong University FI410 Corporate Finance Instructor: Xiaorong Zhang Email: xrzhang@fudan.edu.cn Home Institution: Office Hours: Fudan University Office: Term: 2 July - 2 August, 2018 Credits:

PM tutor. Advanced Cost Theory. Presented by Dipo Tepede, PMP, SSBB, MBA. Empowering Excellence. Powered by POeT Solvers Limited

PM tutor Empowering Excellence Advanced Cost Theory Presented by Dipo Tepede, PMP, SSBB, MBA This presentation is copyright 2009 by POeT Solvers Limited. All rights reserved. This presentation is protected

PM tutor Empowering Excellence Advanced Cost Theory Presented by Dipo Tepede, PMP, SSBB, MBA This presentation is copyright 2009 by POeT Solvers Limited. All rights reserved. This presentation is protected

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

ENSC 201 Assignment 5, Model Answers

ENSC 201 Assignment 5, Model Answers 5.1 Gerry likes driving small cars, and buys nearly identical ones whenever the old one needs replacing. He typically trades in his old car for a new one costing about

ENSC 201 Assignment 5, Model Answers 5.1 Gerry likes driving small cars, and buys nearly identical ones whenever the old one needs replacing. He typically trades in his old car for a new one costing about

Corporate Finance. Bin Zou. University of Alberta

Corporate Finance Bin Zou bzou@ualberta.ca University of Alberta 2010 Fall Updated: February 22, 2015 Contents Preface I 1 The Corporation 1 1.1 Organizational Types of Firms.................. 1 1.2 Goals

Corporate Finance Bin Zou bzou@ualberta.ca University of Alberta 2010 Fall Updated: February 22, 2015 Contents Preface I 1 The Corporation 1 1.1 Organizational Types of Firms.................. 1 1.2 Goals

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

1 INVESTMENT DECISIONS,

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

Tools and Techniques for Economic/Financial Analysis of Projects

Lecture No 12 /13 PCM Tools and Techniques for Economic/Financial Analysis of Projects Project Evaluation: Alternative Methods Payback Period (PBP) Internal Rate of Return (IRR) Net Present Value (NPV)

Lecture No 12 /13 PCM Tools and Techniques for Economic/Financial Analysis of Projects Project Evaluation: Alternative Methods Payback Period (PBP) Internal Rate of Return (IRR) Net Present Value (NPV)

The NPV profile and IRR PITFALLS OF IRR. Years Cash flow Discount rate 10% NPV 472,27 IRR 11,6% NPV

PITFALLS OF IRR J.C. Neves, ISEG, 2018 23 The NPV profile and IRR Years 0 1 2 3 4 5 Cash flow -10000 2000 2500 1000 4000 5000 Discount rate 10% NPV 472,27 IRR 11,6% 5 000,00 NPV 4 000,00 3 000,00 2 000,00

PITFALLS OF IRR J.C. Neves, ISEG, 2018 23 The NPV profile and IRR Years 0 1 2 3 4 5 Cash flow -10000 2000 2500 1000 4000 5000 Discount rate 10% NPV 472,27 IRR 11,6% 5 000,00 NPV 4 000,00 3 000,00 2 000,00

Chapter 12. b. Cost of Capital Rationing Constraint = NPV of rejected projects = $45 million

Chapter 12 12-1 Project Investment NPV PI A $25 $10 0.40 B $30 $25 0.83 Accept C $40 $20 0.50 Accept D $10 $10 1.00 Accept E $15 $10 0.67 Accept F $60 $20 0.33 G $20 $10 0.50 Accept H $25 $20 0.80 Accept

Chapter 12 12-1 Project Investment NPV PI A $25 $10 0.40 B $30 $25 0.83 Accept C $40 $20 0.50 Accept D $10 $10 1.00 Accept E $15 $10 0.67 Accept F $60 $20 0.33 G $20 $10 0.50 Accept H $25 $20 0.80 Accept

Monitor: Roberto de Almeida Bastos EPGE-FGV, 2nd Semester Questions Investment, strategy, and economic rents

Professor: Victor Filipe Martins-da-Rocha Principles of Corporate Finance Monitor: Roberto de Almeida Bastos EPGE-FGV, 2nd Semester 2009 Questions Investment, strategy, and economic rents Question 1. Suppose

Professor: Victor Filipe Martins-da-Rocha Principles of Corporate Finance Monitor: Roberto de Almeida Bastos EPGE-FGV, 2nd Semester 2009 Questions Investment, strategy, and economic rents Question 1. Suppose

Finance 402: Problem Set 5 Solutions

Finance 402: Problem Set 5 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. The first step is

Finance 402: Problem Set 5 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. The first step is

SOLUTIONS TO ASSIGNMENT PROBLEMS. Problem No.1

W.N.-1: Calculation of depreciation per annum Depreciation p.a. = SOLUTIONS TO ASSIGNMENT PROBLEMS Cost -Scrap Value Life W.N.-2: Calculation of PAT p.a. Problem No.1 80,000 5 10,000 = Rs.14,000 p.a. 2.

W.N.-1: Calculation of depreciation per annum Depreciation p.a. = SOLUTIONS TO ASSIGNMENT PROBLEMS Cost -Scrap Value Life W.N.-2: Calculation of PAT p.a. Problem No.1 80,000 5 10,000 = Rs.14,000 p.a. 2.