P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E

|

|

|

- Elvin Townsend

- 6 years ago

- Views:

Transcription

1 1 P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E

2 2 The objective of a manager is to maximize NPV of cash flows and is derived from the firm s objective to maximize firm value. Earnings flows do not translate into spendable resources though they will resemble cash flows in the long run. Furthermore, in determining whether to accept a project or not, we need to look at the extent to which it adds to the value of the firm. In other words, we need to look at incremental cash flows. The devil is in the details of how one defines incremental.

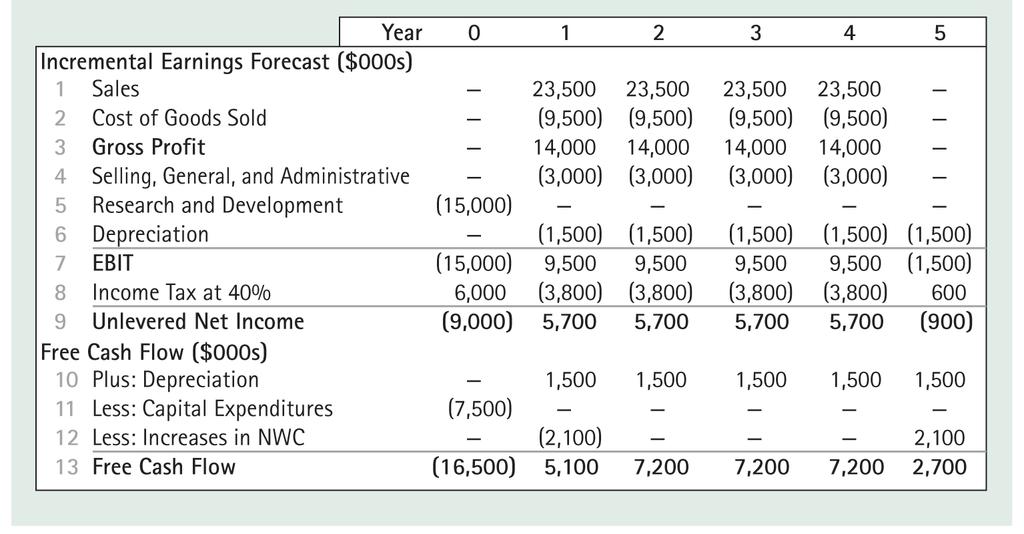

3 3 Consider the development of a wireless networking appliance, called HomeNet by Linksys. The firm forecasts annual sales of 100,000 units for 4 years at a price of $260, with production cost of $110 per unit. Other details are as given below (note assumed treatment of depreciation):

are also not considered.")

4 4 Unlevered Net Income is income from the project if it were financed entirely with equity (sometimes referred to as Net Operating Income). Hence, interest expense is not taken into account in cash flows. On the other hand, tax advantages of debt (interest deductibility) are also not considered. Financing costs are instead generally considered in the cost of capital discount rate. SG&A expenses are estimated to be about $2.8m per year; however, these expenses are fixed and do not vary with the level of production. Is this true in the real world? The project requires investment of $7.5m. in equipment to be depreciated straight line over its estimated life of 5 years. Even though the project life is 4 years, we ll assume that the equipment is not recoverable after 4 years and is depreciated over the entire 5 years. Else, after 4 years, the equipment would have been worth $7.5/5 = $1.5m book value. The project requires initial R&D expenditure of $15m. The tax rate is assumed to be 40% (considering both federal and state taxes).

5 5 Recall that we need incremental cash flows; hence, we need to adjust our figures for externalities. Externalities are indirect effects of the project that may increase or decrease the profits of other business activities of the firm. Here are some examples. If the introduction of the new product would lead to increased sales in other areas of the firm, that would be a positive externality. In HomeNet s case, we have the following negative externality. 25% of HomeNet s sales would come from customers who would otherwise have purchased an existing Linksys router, which sells for $100. Hence, the amount of cannibalization of revenue can be computed as 0.25(100,000)(100) = $2.5m. Net incremental sales are $26m. - $2.5m. or $23.5m. Cost of producing the existing router is $60. Hence total COGS will be lower by 0.25(100,000)(60) = $1.5m. Net incremental COGS is $11m. - $1.5m. = $9.5m. In terms of presentation, it s often better to show cannibalization or other externalities as a separate line item.

6 The lab will be housed in an existing facility, which would have been rented out for $200,000/yr. otherwise. Using it for HomeNet will thus entail an opportunity cost of an equal amount. o If you didn t know what the rental value was, what alternative approach could be used for this opportunity cost? Consequently, the SG&A is now $2.8m. + $0.2m. = $3m. per yr. Should there be other opportunity costs, for example, that are associated with SG&A? Opportunity costs usually result in estimated cost allocations and are often a source of contention between Finance and Operating people. In the long run, there are no fixed costs. 6

7 In order to generate the cash flows, the firm needs to lay out $7.5m in capital expenditures at the very outset, as we noted before. Furthermore, the firm needs to keep resources on hand to fund working capital. That is, the firm might need to provide credit to its customers. Of course, part of this can be offset from credit that the firm s suppliers provide. The firm might also need to keep cash on hand to meet unexpected needs. Furthermore, the firm may need to keep inventory on hand; i.e. firm may need to produce goods that will not be sold in the same period. This will involve a cash outflow that will show up as inventory. Remember that COGS only includes the cost of producing goods that are actually sold in the current period and does not reflect costs of goods that are in inventory. These cash requirements are computed by taking the change in Net Working Capital. 7

(23.5) or 15% of $23.5m. = $3.525m. Similarly, assuming that the firm takes about 54.75 days on average to pay its bills, payables each period are also expected to be 15% of COGS that period.")

8 Suppose customers take days to pay on average, then accounts receivable will consist of days worth of sales (assuming that sales are spread evenly over the year). This works out to (54.75/365)(23.5) or 15% of $23.5m. = $3.525m. Similarly, assuming that the firm takes about days on average to pay its bills, payables each period are also expected to be 15% of COGS that period. 8 If we were to assume zero cash requirements and just-in-time inventory practices (a bit unrealistically), we find that Net Working Capital works out to $2.1m. This requires an infusion of $2.1m which is required only at the end of yr. 1, while at the end of the project life, the $2100 would be recovered and then represents a positive cash flow. Our problem assumes that the $ 2.1m can be withdrawn only at the end of year 5, instead of when the project ends in year 4. The numbers in the table reflect this. In general, the yearly change in Net Working Capital (not presented in table) represents the cash flow effect.

9 We also have to adjust Earnings for expenses that do not actually represent cash flows. Depreciation represents such an expense, and hence we add it back. 9 That is, from a cash flow point of view, buying the equipment initially involves a cash outflow of $7.5m., followed by a cash inflow of whatever salvage value the equipment would have at the end. Thus, if the equipment could be sold for $1.5m after 4 years, there would be an inflow of $1.5 less applicable taxes at the end of 4 years. In our example, there is no final inflow. The assumed depreciation expense each period, therefore, has to be undone. In this sense, depreciation is a fake expenditure because it does not really reflect a cash outflow each period. However, there is a real cash flow implication of depreciation. This is because tax laws generally require payment of taxes only on EBIT (defined according to tax accounting rules). Depreciation is an expense that is deductible for tax purposes. Hence, depreciation reduces taxable income and taxes each period. We take this directly taken into account by computing (Unlevered) Net Income, which includes the tax benefit of depreciation and then adding back the entire depreciation amount to income to arrive at cash flow. Which depreciation figures should one use: book or tax? Normal accounting convention includes depreciation in cost and expense categories and not as separate line item. One should be careful when estimating allocation ratios. Full absorption vs. direct costing.

10 10

11 11 Keep in mind that the formulas given above for Unlevered Net Income, Current Assets and Current Liabilities are not complete they only include the most common components.

12 12 To compute HomeNet s NPV, we must discount its free cash flow at the appropriate cost of capital, i.e. the expected return that investors could earn on their best alternative investment with similar risk and maturity. Here we assume that this rate is 12%.

13 13 Any non-cash expenses, such as amortization, should be added back in computing cash flow from Net Income. If there is a salvage value, the tax implications should be taken into account specifically, the payment of capital gains on the sale. If the project is expected to continue for a long time, the manager may forecast cash flows in a more detailed fashion for a shorter period and then assume that cash flows will grow at a forecasted rate from then on. This is because the manager is likely to have little information about the distant future. The tax rate used should be the marginal tax rate relevant for the company as a whole. Thus, if the company is making losses elsewhere, it may not pay taxes on the income from the project under consideration. On the other hand, if the company has income elsewhere, losses on the project in a particular year may result in tax savings. What if you have multiple projects that exceed the tax loss carryforwards? More often than not in multinational companies, projects entail supply chains with income earned in different countries. One should either use an average global tax rate or decompose project income into each country where the income is earned and tax effect each country s income at its tax rate. Sunk costs can also be a source of controversy: Should you consider sunk costs in pricing decisions?

14 14 It s important to do break-even analysis on the parameters viz., at what level of the parameter will the project no longer be profitable? This can be done on a parameter-by-parameter basis, e.g. for cost of capital, units sold per year, sale price per unit, cost of goods sold per unit, etc. The likelihood of the break-even value not being achieved should then be evaluated to get a feel for the uncertainty and risk involved. Alternatively, the impact on NPV of best and worst case assumptions can be examined. One can also rank the percentage change in NPV for a +/- 10% change in each parameter to determine which are the most sensitive parameters because more effort should be expended to estimate these more accurately.

15 Green bars show the change in NPV under the best-case assumption for each parameter; red bars show the change under the worst-case assumption. Also shown are the break-even levels for each parameter. Under the initial assumptions, HomeNet s NPV is $5.0 million. 15

16 We may also want to change several parameter values simultaneously. For example, if we assume a higher sales price of $275, then it makes sense to assume a lower level of sales, rather than to keep the level of sales constant. The table below shows NPV values for three different combinations of price and sales. This can be done for other combinations of parameters, as well. An even more sophisticated approach is to use Monte Carlo simulation whereby probabilities are estimated for different outcomes of parameters and cash flows to generate a probability distribution of NPV. 16

17 Another way of analyzing the data is to see what combinations of parameters will yield the same NPV. 17 The manager can use this information to decide on the optimal action, taking into account other strategic considerations that may not have been explicitly included in the analysis.

Chapter 8. Fundamentals of Capital Budgeting

Chapter 8 Fundamentals of Capital Budgeting Chapter Outline 8.1 Forecasting Earnings 8.2 Determining Free Cash Flow and NPV 8.3 Choosing Among Alternatives 8.4 Further Adjustments to Free Cash Flow 8.5

Chapter 8 Fundamentals of Capital Budgeting Chapter Outline 8.1 Forecasting Earnings 8.2 Determining Free Cash Flow and NPV 8.3 Choosing Among Alternatives 8.4 Further Adjustments to Free Cash Flow 8.5

Chapter 8: Fundamentals of Capital Budgeting

Chapter 8: Fundamentals of Capital Budgeting - 1 Chapter 8: Fundamentals of Capital Budgeting Note: Read the chapter then look at the following. Fundamental question: How do we determine the cash flows

Chapter 8: Fundamentals of Capital Budgeting - 1 Chapter 8: Fundamentals of Capital Budgeting Note: Read the chapter then look at the following. Fundamental question: How do we determine the cash flows

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Should there be a risk premium for foreign projects?

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Cash Flow and the Time Value of Money

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Chapter 4. Funds-Flow Analysis and Forecasting. Overview of the Lecture. September The Statement of Cash Flows. Pro Forma Financial Statements

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

Key Expense Assumptions

Key Expense Assumptions 204 The operating expenses are assumed to be 60% of the revenues at the parks, and 75% of revenues at the resort properties. Disney will also allocate corporate general and administrative

Key Expense Assumptions 204 The operating expenses are assumed to be 60% of the revenues at the parks, and 75% of revenues at the resort properties. Disney will also allocate corporate general and administrative

Topic 1 (Week 1): Capital Budgeting

: Capital Budgeting") 4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

Measuring Investment Returns

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

Finance 303 Financial Management Review Notes for Final. Chapters 11&12

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

DISCOUNTED CASH-FLOW ANALYSIS

DISCOUNTED CASH-FLOW ANALYSIS Objectives: Study determinants of incremental cash flows Estimate incremental after-tax cash flows from accounting data and use them to estimate NPV Introduce salvage value

DISCOUNTED CASH-FLOW ANALYSIS Objectives: Study determinants of incremental cash flows Estimate incremental after-tax cash flows from accounting data and use them to estimate NPV Introduce salvage value

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT. FCA, CFA L3 Candidate

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

CHAPTER 2 LITERATURE REVIEW

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 9 CONCEPT REVIEW QUESTIONS

CHAPTER 9 CONCEPT REVIEW QUESTIONS 1. Why is it important for the financial analyst to (a) focus on incremental cash flows, (b) ignore financing costs, (c) consider taxes, and (d) adjust for noncash expenses

CHAPTER 9 CONCEPT REVIEW QUESTIONS 1. Why is it important for the financial analyst to (a) focus on incremental cash flows, (b) ignore financing costs, (c) consider taxes, and (d) adjust for noncash expenses

Study Session 11 Corporate Finance

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BOND VALUATION. YTM Of An n-year Zero-Coupon Bond

BOND VALUATION BOND VALUATIONS BOND: A security sold by governments and corporations to raise money from investors today in exchange for promised future payments 1. ZERO COUPON BONDS ZERO COUPON BONDS:

BOND VALUATION BOND VALUATIONS BOND: A security sold by governments and corporations to raise money from investors today in exchange for promised future payments 1. ZERO COUPON BONDS ZERO COUPON BONDS:

*Efficient markets assumed

LECTURE 1 Introduction To Corporate Projects, Investments, and Major Theories Corporate Finance It is about how corporations make financial decisions. It is about money and markets, but also about people.

LECTURE 1 Introduction To Corporate Projects, Investments, and Major Theories Corporate Finance It is about how corporations make financial decisions. It is about money and markets, but also about people.

I m going to cover 6 key points about FCF here:

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

REVIEW FOR SECOND QUIZ. Show me the money

REVIEW FOR SECOND QUIZ Show me the money The skill set for this test Can you compute the cost of capital for a project (rather than a firm)? How do you estimate the cost of equity for a project? What debt

REVIEW FOR SECOND QUIZ Show me the money The skill set for this test Can you compute the cost of capital for a project (rather than a firm)? How do you estimate the cost of equity for a project? What debt

1) Side effects such as erosion should be considered in a capital budgeting decision.

Side effects such as erosion should be considered in a capital budgeting decision.") Questions Chapter 10 1) Side effects such as erosion should be considered in a capital budgeting decision. [B] :A project s cash flows should include all changes in a firm s future cash flows. This includes

Questions Chapter 10 1) Side effects such as erosion should be considered in a capital budgeting decision. [B] :A project s cash flows should include all changes in a firm s future cash flows. This includes

Simple Financial Measures

Handout for Business 189 undergraduate course in Strategic Management Simple Financial Measures Simon Rodan Department of Management Lucas College of Business San José State University One Washington Square

Handout for Business 189 undergraduate course in Strategic Management Simple Financial Measures Simon Rodan Department of Management Lucas College of Business San José State University One Washington Square

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

Chapter 11 Cash Flow Estimation and Risk Analysis ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 11 Cash Flow Estimation and Risk Analysis ANSWERS TO END-OF-CHAPTER QUESTIONS 11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the actual flow of cash,

Chapter 11 Cash Flow Estimation and Risk Analysis ANSWERS TO END-OF-CHAPTER QUESTIONS 11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the actual flow of cash,

Homework #3 Suggested Solutions

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #3 Suggested Solutions Problem 1. (6.6) When appraising mutually exclusive investments in plant and equipment, financial

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #3 Suggested Solutions Problem 1. (6.6) When appraising mutually exclusive investments in plant and equipment, financial

Chapter 12. Evaluating Project Economics and Capital Rationing. 1. Explain and be able to demonstrate how variable costs and fixed costs affect the

Chapter 12 Evaluating Project Economics and Capital Rationing Learning Objectives 1. Explain and be able to demonstrate how variable costs and fixed costs affect the volatility of pretax operating cash

Chapter 12 Evaluating Project Economics and Capital Rationing Learning Objectives 1. Explain and be able to demonstrate how variable costs and fixed costs affect the volatility of pretax operating cash

MAXIMISE SHAREHOLDERS WEALTH.

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Sample Questions for Chapters 10 & 11

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Chapter 3: Accounting and Finance

FIN 301 Class Notes Chapter 3: Accounting and Finance INTRODUCTION Accounting Function: Gathering, processing, and reporting data. End result is a set of four financial statements 1- Balance sheet 2-Income

FIN 301 Class Notes Chapter 3: Accounting and Finance INTRODUCTION Accounting Function: Gathering, processing, and reporting data. End result is a set of four financial statements 1- Balance sheet 2-Income

CAPITAL BUDGETING AND THE INVESTMENT DECISION

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

VENTURE ANALYSIS WORKBOOK

VENTURE ANALYSIS WORKBOOK ANALYSIS SECTION VERSION 1.2 Copyright (1990, 2000) Michael S. Lanham Eugene B. Lieb Customer Decision Support, Inc. P.O. Box 998 Chadds Ford, PA 19317 (610) 793-3520 genelieb@lieb.com

VENTURE ANALYSIS WORKBOOK ANALYSIS SECTION VERSION 1.2 Copyright (1990, 2000) Michael S. Lanham Eugene B. Lieb Customer Decision Support, Inc. P.O. Box 998 Chadds Ford, PA 19317 (610) 793-3520 genelieb@lieb.com

chapter12 Home Depot Inc. grew phenomenally Cash Flow Estimation and Risk Analysis

chapter12 Cash Flow Estimation and Risk Analysis Home Depot Inc. grew phenomenally during the 1990s, and it is still growing rapidly. At the beginning of 1990, it had 118 stores and annual sales of $2.8

chapter12 Cash Flow Estimation and Risk Analysis Home Depot Inc. grew phenomenally during the 1990s, and it is still growing rapidly. At the beginning of 1990, it had 118 stores and annual sales of $2.8

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Project Free Cash Flows = NOPAT + Depreciation Gross Investment in Fixed Operating Assets Investment in Operating Working Capital

Project Free Cash Flows = NOPAT + Depreciation Gross Investment in Fixed Operating Assets Investment in Operating Working Capital = EBIT (1 t) + Depreciation Gross Investment in Fixed Operating Assets

Project Free Cash Flows = NOPAT + Depreciation Gross Investment in Fixed Operating Assets Investment in Operating Working Capital = EBIT (1 t) + Depreciation Gross Investment in Fixed Operating Assets

HPM Module_6_Capital_Budgeting_Exercise

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

Lecture 6 Capital Budgeting Decision

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Handout for Unit 4 for Applied Corporate Finance

Handout for Unit 4 for Applied Corporate Finance Unit 4 Capital Structure Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving

Handout for Unit 4 for Applied Corporate Finance Unit 4 Capital Structure Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving

STATEMENT OF CASH FLOWS

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Calculating Investment Returns. Remick Capital, LLC

Calculating Investment Returns Remick Capital, LLC Calculating Returns Critically Important When you invest or save your money, the end goal is to generate a good return on your funds. What defines good

Calculating Investment Returns Remick Capital, LLC Calculating Returns Critically Important When you invest or save your money, the end goal is to generate a good return on your funds. What defines good

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Would lead us to conclude that...

Would lead us to conclude that... Do not invest in this park. The return on capital of 4.18% is lower than the cost of capital for theme parks of 8.46%; This would suggest that the project should not be

Would lead us to conclude that... Do not invest in this park. The return on capital of 4.18% is lower than the cost of capital for theme parks of 8.46%; This would suggest that the project should not be

EE266 Homework 5 Solutions

EE, Spring 15-1 Professor S. Lall EE Homework 5 Solutions 1. A refined inventory model. In this problem we consider an inventory model that is more refined than the one you ve seen in the lectures. The

EE, Spring 15-1 Professor S. Lall EE Homework 5 Solutions 1. A refined inventory model. In this problem we consider an inventory model that is more refined than the one you ve seen in the lectures. The

Chapter 22 examined how discounted cash flow models could be adapted to value

ch30_p826_840.qxp 12/8/11 2:05 PM Page 826 CHAPTER 30 Valuing Equity in Distressed Firms Chapter 22 examined how discounted cash flow models could be adapted to value firms with negative earnings. Most

ch30_p826_840.qxp 12/8/11 2:05 PM Page 826 CHAPTER 30 Valuing Equity in Distressed Firms Chapter 22 examined how discounted cash flow models could be adapted to value firms with negative earnings. Most

Question: Insurance doesn t have much depreciation or inventory. What accounting methods affect return on book equity for insurance?

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Question 4.1: Accounting Returns

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Question 4.1: Accounting Returns

Institute of Certified Management Accountants of Sri Lanka. Strategic Level May 2012 Examination. Financial Strategy and Policy (FSP / SL 3-403)

") Copyright Reserved Serial No Strategic Level May 2012 Examination Examination Date : 12 th May 2012 Number of Pages : 08 Examination Time: 9.30 a:m. 12.30 p:m. Number of Questions: 05 Instructions to Candidates

Copyright Reserved Serial No Strategic Level May 2012 Examination Examination Date : 12 th May 2012 Number of Pages : 08 Examination Time: 9.30 a:m. 12.30 p:m. Number of Questions: 05 Instructions to Candidates

ch11 Student: 3. An analysis of what happens to the estimate of net present value when only one variable is changed is called analysis.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

A Simple Model. IFS: Integrating Financial Statements (Transcript)

") In this video you will learn to build an integrated financial statement model. This model provides the core or platform from which most thorough financial models are built. This can be used to run through

In this video you will learn to build an integrated financial statement model. This model provides the core or platform from which most thorough financial models are built. This can be used to run through

Real Options and Risk Analysis in Capital Budgeting

Real options Real Options and Risk Analysis in Capital Budgeting Traditional NPV analysis should not be viewed as static. This can lead to decision-making problems in a dynamic environment when not all

Real options Real Options and Risk Analysis in Capital Budgeting Traditional NPV analysis should not be viewed as static. This can lead to decision-making problems in a dynamic environment when not all

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

Before discussing capital expenditure decision methods, we may understand following three points:

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #3 Olga Bychkova Topics Covered Today Making investment decisions with NPV rule (more practical guidance) and capital budgeting (chapter 6 in

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #3 Olga Bychkova Topics Covered Today Making investment decisions with NPV rule (more practical guidance) and capital budgeting (chapter 6 in

CAPITAL BUDGETING. John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada

CHAPTER 2 CAPITAL BUDGETING John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada LEARNING OUTCOMES After completing this chapter, you will be able to do the following:

CHAPTER 2 CAPITAL BUDGETING John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada LEARNING OUTCOMES After completing this chapter, you will be able to do the following:

25557 Corporate finance

25557 Corporate finance Lecture 1 Introduction and major theories: Corporate finance: Is about how corporations make financial decisions Is about money and markets, also about people Is also known as business

25557 Corporate finance Lecture 1 Introduction and major theories: Corporate finance: Is about how corporations make financial decisions Is about money and markets, also about people Is also known as business

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Updated: December 13, 2006 Question

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Updated: December 13, 2006 Question

Essential Learning for CTP Candidates TEXPO Conference 2017 Session #02

TEXPO Conference 2017: Essential Learning for CTP Candidates Session #2 (Monday. 10:30 11:45 am) ETM5-Chapter 8: Financial Accounting and Reporting ETM5-Chapter 9: Financial Planning and Analysis Essentials

TEXPO Conference 2017: Essential Learning for CTP Candidates Session #2 (Monday. 10:30 11:45 am) ETM5-Chapter 8: Financial Accounting and Reporting ETM5-Chapter 9: Financial Planning and Analysis Essentials

Breaking out G&A Costs into fixed and variable components: A simple example

230 Breaking out G&A Costs into fixed and variable components: A simple example Assume that you have a time series of revenues and G&A costs for a company. What percentage of the G&A cost is variable?

230 Breaking out G&A Costs into fixed and variable components: A simple example Assume that you have a time series of revenues and G&A costs for a company. What percentage of the G&A cost is variable?

Benchmarking. Club Fund. We like to think about being in an investment club as a group of people running a little business.

Benchmarking What Is It? Why Do You Want To Do It? We like to think about being in an investment club as a group of people running a little business. Club Fund In fact, we are a group of people managing

Benchmarking What Is It? Why Do You Want To Do It? We like to think about being in an investment club as a group of people running a little business. Club Fund In fact, we are a group of people managing

Financial planning. Kirt C. Butler Department of Finance Broad College of Business Michigan State University February 3, 2015

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

UNIT 5 COST OF CAPITAL

UNIT 5 COST OF CAPITAL UNIT 5 COST OF CAPITAL Cost of Capital Structure 5.0 Introduction 5.1 Unit Objectives 5.2 Concept of Cost of Capital 5.3 Importance of Cost of Capital 5.4 Classification of Cost

UNIT 5 COST OF CAPITAL UNIT 5 COST OF CAPITAL Cost of Capital Structure 5.0 Introduction 5.1 Unit Objectives 5.2 Concept of Cost of Capital 5.3 Importance of Cost of Capital 5.4 Classification of Cost

Real Estate. Refinancing

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Financial Controls in Project Management Activities

Financial Controls in Management Activities Objective Complete hands-on exercises to apply cost control techniques Budgeting Budgeting Process Overview Budgeting Budgeting - aggregating the estimated costs

Financial Controls in Management Activities Objective Complete hands-on exercises to apply cost control techniques Budgeting Budgeting Process Overview Budgeting Budgeting - aggregating the estimated costs

ACCA. Paper F9. Financial Management. December 2014 to June Interim Assessment Answers

ACCA Paper F9 Financial Management December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions and

ACCA Paper F9 Financial Management December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions and

Slides by Yee-Tien (Ted) Fu

Fu") Chapter 14 Multinational Capital Budgeting J. Gaspar: Adapted from Jeff Madura, International Financial Management 14. 1 Slides by Yee-Tien (Ted) Fu Capital Budgeting Capital budgeting involves the allocation

Chapter 14 Multinational Capital Budgeting J. Gaspar: Adapted from Jeff Madura, International Financial Management 14. 1 Slides by Yee-Tien (Ted) Fu Capital Budgeting Capital budgeting involves the allocation

Introduction to Capital Budgeting

Introduction to Capital Budgeting Pamela Peterson, Florida State University O U T L I N E I. Introduction II. The investment problem III. Capital budgeting IV. Classifying investment projects V. Cash flow

Introduction to Capital Budgeting Pamela Peterson, Florida State University O U T L I N E I. Introduction II. The investment problem III. Capital budgeting IV. Classifying investment projects V. Cash flow

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Introduction to Capital

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Consolidated financial statements Financial Year. Publicis Groupe consolidated financial statements financial year ended December 31,

Consolidated financial statements 2017 Financial Year Publicis Groupe consolidated financial statements financial year ended December 31, 2017 1 Consolidated income statement Notes 2017 2016 Revenue 9,690

Consolidated financial statements 2017 Financial Year Publicis Groupe consolidated financial statements financial year ended December 31, 2017 1 Consolidated income statement Notes 2017 2016 Revenue 9,690

A Primer on Financial Statements

A Primer on Financial Statements Much of the information that is used in valuation and corporate finance comes from financial statements. An understanding of the basic financial statements and some of

A Primer on Financial Statements Much of the information that is used in valuation and corporate finance comes from financial statements. An understanding of the basic financial statements and some of

FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE

NET PRESENT VALUE") FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE 1. INTRODUCTION Dear students, welcome to the lecture series on financial management. Today in this lecture, we shall learn the techniques of evaluation

FINANCIAL MANAGEMENT ( PART-2 ) NET PRESENT VALUE 1. INTRODUCTION Dear students, welcome to the lecture series on financial management. Today in this lecture, we shall learn the techniques of evaluation

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Essential Learning for CTP Candidates Carolinas Cash Adventure 2018 Session #CTP-04

Carolinas Cash Adventure - 2018: CTP Track Financial Statements, Analysis & Decisions Session #4 (Mon. 9:15 10:15 am) ETM5-Chapter 8: Financial Accounting and Reporting ETM5-Chapter 9: Financial Planning

Carolinas Cash Adventure - 2018: CTP Track Financial Statements, Analysis & Decisions Session #4 (Mon. 9:15 10:15 am) ETM5-Chapter 8: Financial Accounting and Reporting ETM5-Chapter 9: Financial Planning

Financial Statement Balance Sheet

Financial Statement Balance Sheet Page 1 of 1 Financial Statement Balance Sheet Accounting Title 2014/09/30 2013/12/31 2013/09/30 Balance Sheet Assets Current assets Cash and cash equivalents Total cash

Financial Statement Balance Sheet Page 1 of 1 Financial Statement Balance Sheet Accounting Title 2014/09/30 2013/12/31 2013/09/30 Balance Sheet Assets Current assets Cash and cash equivalents Total cash

3 Leasing Decisions. The Institute of Chartered Accountants of India

3 Leasing Decisions BASIC CONCEPTS AND FORMULAE 1. Introduction Lease can be defined as a right to use an equipment or capital goods on payment of periodical amount. Two principal parties to any lease

3 Leasing Decisions BASIC CONCEPTS AND FORMULAE 1. Introduction Lease can be defined as a right to use an equipment or capital goods on payment of periodical amount. Two principal parties to any lease

accounts receivable: dollar amount due from customers from sales made on open account.

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

CASH FLOW ESTIMATION AND RISK ANALYSIS

C H A P T E 12 R CASH FLOW ESTIMATION AND RISK ANALYSIS AP PHOTO/NYSE, MEL NUDELMAN Home Depot Keeps Growing Home Depot Inc. (HD) has grown phenomenally since 1990, and it shows no signs of slowing down.

C H A P T E 12 R CASH FLOW ESTIMATION AND RISK ANALYSIS AP PHOTO/NYSE, MEL NUDELMAN Home Depot Keeps Growing Home Depot Inc. (HD) has grown phenomenally since 1990, and it shows no signs of slowing down.

11B REPLACEMENT PROJECT ANALYSIS

App11B_SW_Brigham_778312_R2 1/6/03 9:12 PM Page 11B-1 11B REPLACEMENT PROJECT ANALYSIS Replacement Analysis An analysis involving the decision of whether or not to replace an existing asset with a new

App11B_SW_Brigham_778312_R2 1/6/03 9:12 PM Page 11B-1 11B REPLACEMENT PROJECT ANALYSIS Replacement Analysis An analysis involving the decision of whether or not to replace an existing asset with a new

Chapter 9. Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions. Answers to Concepts Review and Critical Thinking Questions

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 9. Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 9. Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or

2, , , , ,220.21

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

Paramount Trading (Jamaica) Limited Financial Statements 31 May 2015

Limited Financial Statements 31 May 2015") Financial Statements Index Page INDEX Independent Auditors' Report to the Members Financial Statements Statement of Comprehensive Income 1 Statement of Financial Position 2 Statement of Cash Flows 3 Statement

Financial Statements Index Page INDEX Independent Auditors' Report to the Members Financial Statements Statement of Comprehensive Income 1 Statement of Financial Position 2 Statement of Cash Flows 3 Statement

Allen & Betty Abbett. Personal Retirement Analysis. Sample Plan - TOTAL Cash-Flow-Based Planning

Mar 29, 2018 Personal Retirement Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

Mar 29, 2018 Personal Retirement Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

INTERMEDIATE MICROECONOMICS LECTURE 9 THE COSTS OF PRODUCTION

9-1 INTERMEDIATE MICROECONOMICS LECTURE 9 THE COSTS OF PRODUCTION The opportunity cost of an asset (or, more generally, of a choice) is the highest valued opportunity that must be passed up to allow current

9-1 INTERMEDIATE MICROECONOMICS LECTURE 9 THE COSTS OF PRODUCTION The opportunity cost of an asset (or, more generally, of a choice) is the highest valued opportunity that must be passed up to allow current

Incremental Cash Flow: Example

Note 8. Making Capital Investment Decisions To include or not to include? that is the question. General Milk Company is currently evaluating the NPV of establishing a line of chocolate milk. As part of

Note 8. Making Capital Investment Decisions To include or not to include? that is the question. General Milk Company is currently evaluating the NPV of establishing a line of chocolate milk. As part of

FIN622 Solved MCQs BY

FIN622 Solved MCQs BY http://vustudents.ning.com Question # 1 of 15 Which of the following investment criteria does not take the time value of money into consideration? Simple payback method (page#34)

FIN622 Solved MCQs BY http://vustudents.ning.com Question # 1 of 15 Which of the following investment criteria does not take the time value of money into consideration? Simple payback method (page#34)

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT. (Profit and loss statement)

") HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

SIMULTRAIN STRATEGIC MANAGEMENT USER GUIDE

SIMULTRAIN STRATEGIC MANAGEMENT USER GUIDE You develop a strategy for a portfolio of projects. Working in a large company, you start planning a five-year portfolio of projects. You need to put the right

SIMULTRAIN STRATEGIC MANAGEMENT USER GUIDE You develop a strategy for a portfolio of projects. Working in a large company, you start planning a five-year portfolio of projects. You need to put the right

2 Cost Concepts in Decision Making

2 Cost Concepts in Decision Making LEARNING OBJECTIVES : After studying this unit you will be able to : Understand the meaning and prerequisites of relevant costs. Learn and apply the opportunity cost

2 Cost Concepts in Decision Making LEARNING OBJECTIVES : After studying this unit you will be able to : Understand the meaning and prerequisites of relevant costs. Learn and apply the opportunity cost

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

Discounted Cash Flow Analysis Deliverable #6 Sales Gross Profit / Margin

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

INTERNATIONAL JOURNAL OF MULTIDISCIPLINARY RESEARCH CENTRE (IJMRC)

") ISSN: 2454-3659 (P), 2454-3861(E) Volume I, Issue 7 December 2015 International Journal of Multidisciplinary Research Centre Research Article / Survey Paper / Case Study A STUDY ON CAPITAL BUDGETING PROCESS

ISSN: 2454-3659 (P), 2454-3861(E) Volume I, Issue 7 December 2015 International Journal of Multidisciplinary Research Centre Research Article / Survey Paper / Case Study A STUDY ON CAPITAL BUDGETING PROCESS

Exercises Corporate Finance

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage