Handout for Unit 4 for Applied Corporate Finance

|

|

|

- Lester Davidson

- 5 years ago

- Views:

Transcription

1 Handout for Unit 4 for Applied Corporate Finance

2 Unit 4 Capital Structure

3 Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving at Optimal Capital Structure a. The Cost of Capital Approach b. The Operating Income Approach c. The Adjusted Present Value Approach d. The Sector Approach 6. Does Equity Value Change when we reach Optimal Capital Structure? 7. What happens in a Buyback? 8. Capital Structure Determinants 9. Case Capital Structure Analysis of MRF

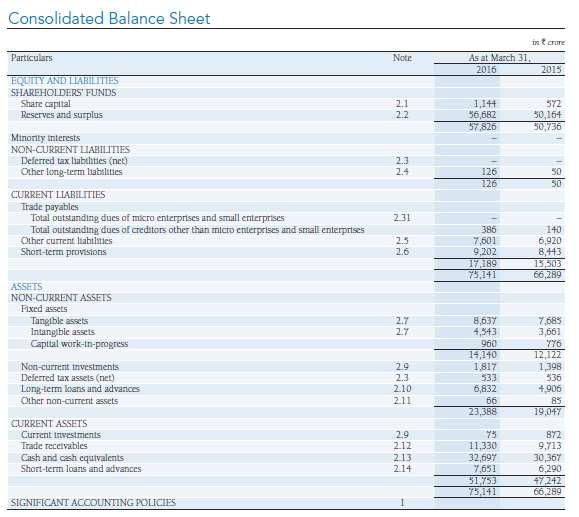

4 Types of Financing A firm can either raise Money using Equity, or using Debt. While Equity is expensive, and is the residual payout, after paying the lenders, debt is cheaper, and is a fixed payout. Equity Residual payout, expensive Debt Fixed payout, Cheaper We can find about the debt and equity levels from the balance sheet of a company. For example, in the image below, we can find out what is the debt and equity level for Apollo Tyres. Debt in the above figure is the long and short term borrowing, while equity values can be found by adding Share Capital and Reserves and Surplus.

5 Financing Choices Financing choices of the firm change based on its maturity, and business. Usually, smaller firms use own capital, while large public firms use debt. Stage of Firm Initial Startup Phase Rapid Expansion High Growth Mature Growth Declining Growth Typical Financing Choice Internal Financing Own Capital Venture Capital, Common Stock Common Stock, Convertibles Debt Repay sources of Funding How to measure the Debt Financing for a firm? We typically use the debt to capital ratio, given by Debt (Debt + Equity) Debt includes all long term and short Term Debt. Equity could be book value or market value, but needs to be used consistently across the spectrum of firms being analysed. How much debt is good? Assume a firm can borrow money at 8%, and its cost of equity is 12%. Should it raise any capital as debt, or have 100% Equity? If the answer to the first question on debt is Yes, then how much should a firm raise as debt? How much is too much? Are there any benefits of using debt? Are there any costs attached to this? Our next discussion is going to try and answer these questions. However, there are some firms who do not have any debt. For example Infosys, Eicher Motors. Take a look at the Infosys Balance Sheet. They have zero debt. This is not necessarily the best capital structure, since Infosys is taking money from Equity holders at nearly 11-13%, and keeping it in cash and bank balances. This is debatable from the shareholders perspective

6

7 Debt Benefits and Costs Borrowing money from lenders sometimes adds some benefits to the firm. The key benefits of borrowing for a firm are Lower Costs Cost of Debt is lesser than cost of Equity. So technically, debt is a cheaper source of funding. This is because debt holders have a priority in getting the payments, so they are happier with smaller returns. Tax Benefits The interest that a firm pays on debt, reduces the pre tax profits. This interest thus is tax deductible, and gives a form of tax shield to the firm. When the firm uses equity, it is not allowed to deduct payments to equity (such as dividends) to arrive at taxable income. Those payments happen after the tax is paid. Therefore, all other things being equal, higher the marginal tax rate in the business, higher the chances of the firm having more debt. Added Discipline Debt requires fixed payments, and inability to make those payments may lead to the closure of the business. Therefore, the firms that take debt, usually seem managements more proactive, and less complacent.

8 On the other hand, the key Costs related to debt are Bankruptcy Costs If a firm is not able to repay its debt, this would result in different forms of costs that could come up. The first point to note is the probability of bankruptcy, which may be different for different industries. In addition, there are direct and indirect costs of bankruptcy. Direct costs are legal costs and filing costs. Indirect costs are the losses arising because the markets perceive the firm to be in trouble. Firms with more volatile earnings and cash flows will face bigger chances of bankruptcy. The probability of bankruptcy should be a function of the predictability (or variability) of earnings. Similarly, for some industries, indirect costs or loss of business or issues arising from chances of bankruptcy could be higher. Examples would be industries which require repeat customer interaction for example auto industry. Another example would be the retail industry, where suppliers may ask for faster payments since the firm is only selling a third party product, nothing of their own is being sold. Firms with more indirect costs arising out of bankruptcy would possibly have lesser room to take a lot of debt. Agency Costs An agency cost comes into picture when the person who is hired to do the work (agency) has different motivations than the person who is hiring (Principal). When a business borrows money, the stockholders use that money in the course of running that business. Stockholders interests are different from lenders interests, because lenders are interested in getting their money back, while stockholders are interested in maximizing their wealth. Firms may pay large dividends or take riskier project such that the bond holder interest is put at stake. Loss of Future Borrowing Capacity When a firm borrows more today, it loses capacity to borrow in the future. This may be considered detrimental, in case a good project comes up later. Therefore, firms that are uncertain about future projects and financing needs would keep lower leverage levels today.

9 Approaches to Optimal Capital Structure So what is the optimal capital structure? There are 4 approaches which can be used by a firm to arrive at the optimal capital structure. Cost of Capital Approach The D/E ratio that minimizes the cost of capital The Operating Income Approach The D/E ratio that minimizes the cost of capital and maximizes the operating income The adjusted Present Value approach Optimal Debt Ratio maximizes the overall value of the firm The Sector Approach The optimal debt ratio reaches close to sector averages Let us now understand each approach in detail. The Cost of Capital Approach We already know how to calculate the cost of capital for a firm. The idea is to find the level of D/E which minimizes this cost of Capital. But would that not be 100% debt? It is not 100% debt, since the equation is dynamic. Both Cost of Equity and Cost of Debt will change as we get more debt in the firm. Cost of Equity will increase since the levered beta of the firm will increase, and with more debt, the credit rating of the firm would fall, and hence cost of debt will increase too. Let us calculate this for Apollo Tyres. To be able to find this, we need to find the debt equity ratio that minimizes the Cost of Capital. For that we need the following Risk Free Rate Equity Risk Premium Current Debt Equity Ratio of Apollo Tyres Beta for Apollo Tyres

10 Debt Rating Schedule (how ratings change with debt to capital ratio) Assuming that the beta is 1.04, we calculate the unlevered beta, and then use the below table for the rating vs capital structure to arrive at the lowest cost of capital. Government Bond Yield 7% Risk Free Rate 5% ERP 8% Tax Rate 30% Current D/E 0.24 Unlevered Beta 0.90 Debt to Capital is Rating is Spread is Cost Of Debt D/E Levered Beta Cost of Equity Cost Of Capital 0 AAA 0.50% 7.50% % 12.21% 0.1 AA 1.00% 8.00% % 12.05% 0.2 A 1.50% 8.50% % 11.97% 0.3 BBB 2.00% 9.00% % 11.95% 0.4 BB 2.50% 9.50% % 12.00% 0.5 B 3.00% 10.00% % 12.13% 0.6 CCC 3.50% 10.50% % 12.32% 0.7 CC 4.00% 11.00% % 12.59% 0.8 C 5.00% 12.00% % 13.20% 0.9 D 7.00% 14.00% % 14.58% 1 D 7.00% 14.00% Infinite We realize that the cost of capital first goes down as we increase the debt, and then after reaching an optimal level, starts rising again as cost of equity and debt both begin rising with higher debt levels % Cost Of Capital 14.50% 14.00% 13.50% 13.00% 12.50% 12.00% 11.50% 11.00% The result is the given U-shaped cost of capital curve. Thus, the ideal Debt Equity ratio for Apollo tyres is given as 0.43.

11 The Operating Income Approach As a company borrows money, there are chances that the indirect costs of bankruptcy cause the operating income to fall. Rather than looking at a single number for operating income, and assuming the firm value to be constant, we will now evaluate if the firm value itself changes due to changes in operating income (EBIT). We will now look to find the level where the firm value is highest, since at other levels the operating income may drop Let us assume the following levels of drop in EBITDA with the rating changes for the firm Rating is Fall in EBIT AAA 0% AA 0% A 0% BBB 5% BB 8% B 10% CCC 13% CC 15% C 18% D 20% Let us evaluate the changes to the value of the company here. For that, we will firm need the EBIT levels for Apollo Tyres, and then need to arrive at the Free Cash Flow Levels. Current EBIT is Rs million. We will also assume that the firm is in steady state, and hence the depreciation is the same as the capex. We also assume no changes in working capital. Terminal growth rate is assumed to be 4%. We find the below changes to operating income. Debt to Capital is Rating is Spread is Cost Of Debt D/E Levered Beta Cost of Equity Cost Of Capital FCFF Fall in EBIT Value of the Firm 0 AAA 0.50% 7.50% % 12.21% 11, , AA 1.00% 8.00% % 12.05% 11,635 0% 150, A 1.50% 8.50% % 11.97% 11,635 0% 151, BBB 2.00% 9.00% % 11.95% 11,053 5% 144, BB 2.50% 9.50% % 12.00% 10,762 8% 139, B 3.00% 10.00% % 12.13% 10,471 10% 133, CCC 3.50% 10.50% % 12.32% 10,180 13% 127, CC 4.00% 11.00% % 12.59% 9,889 15% 119, C 5.00% 12.00% % 13.20% 9,599 18% 108, D 7.00% 14.00% % 14.58% 9,308 20% 91,466 We realize that the highest firm value is at a debt equity of Post that the income drop results in the firm value dropping, even though the Cost of Capital is lower elsewhere.

12 The Adjusted Present Value Approach In the adjusted present value approach, the value of the firm is the sum of the value of the firm without debt (the unlevered firm) and the effect of debt on firm value. Firm Value = Unlevered Firm Value + (Tax Benefits of Debt - Expected Bankruptcy Cost from the Debt) The optimal debt level is the one that maximizes firm value. To solve this, we need to first find the unlevered value of the firm. This can be found by either valuing the firm using a cost of equity calculated with unlevered beta, or by removing the tax benefits and making the adjustments for bankruptcy costs in the current market value. At every debt level, we need to calculate the value of the tax benefits due to debt. Similarly, we need to calculate the expected bankruptcy cost, and the probability of bankruptcy at every debt level. While it is difficult to find a probability of default for any firm, some studies have established the approximate chances of a firm defaulting given its rating. One such study is known as the Altman study of bonds. The table on the right estimates the default probabilities based on the bond rating of a firm. Altman estimated these probabilities by looking at bonds in each ratings class ten years prior and then examining the proportion of these bonds that defaulted over the ten years. Rating Likelihood of Default AAA 0.07% AA 0.51% A+ 0.60% A 0.66% A- 2.50% BBB 7.54% BB 16.63% B % B 36.80% B % CCC 59.01% CC 70.00% C 85.00% D % Current Enterprise Value of the firm = 109, ,577 7,158 = 117,029 Tax Benefit of current Debt = 14,577 * 30% = 4,373 Probability of Default at current debt levels = 0.51% Assume Cost of Bankruptcy at 25% of current firm value Expected cost of Bankruptcy = 0.51%*25%*117,029 = 149 Unlevered Value of the firm = 117,029 4, = 112,805

13 At every debt level, we need to calculate the value of the tax benefits due to debt. Similarly, we need to calculate the expected bankruptcy cost, and the probability of bankruptcy at every debt level. Debt to Capital is Rating is Default Probability Total Debt Tax Benefit of the Debt Expected Cost of Default Unlevered Firm Value Levered Firm Value 0 AAA 0.07% , , AA 0.51% 11,703 3, , , A 0.66% 23,406 7, , , BBB 7.54% 35,109 10,533 2, , , BB 16.63% 46,812 14,043 4, , , B 36.80% 58,515 17,554 10, , , CCC 59.01% 70,217 21,065 17, , , CC 70.00% 81,920 24,576 20, , , C 85.00% 93,623 28,087 24, , , D % 105,326 31,598 29, , ,146 1 D % 117,029 35,109 29, , ,657 The above table shows us the calculations, and shows that the optimal debt to capital ratio is 0.4. The Sector Approach Here we believe that the optimal debt/equity ratio is one where the sector average is met. Looking at peers such as MRF and Ceat, we see that the average debt / equity ratio should be about 14.2% for Apollo Tyres. Market Cap Debt D/E MRF Tyres 173,510 23, % CEAT 42,700 6, % Sector Average 14.2%

14 Does Equity Value Change when we reach Optimal Capital Structure? Now that we have looked at the variety of methods about finding the optimal capital structure of the firm, our endeavor should be to see if this enhances shareholder value. Let us assume we will follow our first approach of Capital Structure optimization the cost of capital approach. We will repeat our analysis using the market value of equity now, and then check what the firm needs to do. The current capital structure includes debt of Rs 14,577 million, and equity (market value) of Rs 109,610 million. Our analysis shows that optimal debt to equity ratio is 0.43, and hence the new debt should be Rs 37,256 million. Thus the firm needs to borrow an additional Rs 22,679 million, and then buy back shares with this money, or return this as dividend to shareholders. Enterprise Value before the change = INR 117,029 million Cost of Financing at Current Debt Values = 12.51% Cost of Financing at New Debt Values = 12.38% Saving = 0.13% * = 153 million Increase in Value = Increase in Value = Savings Next Year Cost of Capital growth rate % 4% This is equal to Rs 1825 million. The new enhanced enterprise value should thus be = Rs 118,854 million We can divide this increase by number of shares outstanding, to get a sense of increase in per share value. Number of shares outstanding is million, and each shares trades at Rs 215. The increase in share value would be thus Rs 1825 million / = Rs 3.58 per share increase. What happens in a Buyback? Assume that the extra debt is used to buyback shares. The firm has to raise an extra INR 22,679 million, and this can be used for a buyback. Let us assume a buyback at the price of Rs 215. Number of shares that can be bought back = 22,679 / 215 = million.

15 Net shares after the buyback = = million Equity value after buyback = Optimal Enterprise value + Cash Debt Equity value after buyback = Equity value after buyback = Per Share Value = / = Rs Determinants of Capital Structure There are 4 major determinants of the capital structure The Tax Rate Higher the tax rate, higher the debt firms will raise, since the benefit of taxes will be higher The Cash FLows Higher the cash flows, and more stable they are, easier it is for the firm to borrow more The Operating Risk Firms with higher operating leverage (high fixed cost) will see bigger earnings volatility, and hence will have lower borrowing capacity Risk Premiums When risk premiums rise, firms will be able to borrow lesser

16 Case 4 Unit 4 Capital Structure Evaluation The analysis of optimal capital structure needs to happen for another firm. Pick up MRF tyres, and do the analysis of optimal capital structure. (Use the same data for risk free rate, equity premium, change of EBIT with debt and change of rating with debt as given earlier). You will need other data from the internet. 1. Calculate the current firm value, book value of equity, market capitalization, and cost of equity 2. Find the optimal capital structure - Using Cost of Capital Approach 3. Find the optimal capital structure - Using the Operating Income Approach 4. Find the optimal capital structure - Using the Adjusted Present Value Approach 5. Should the company do a buyback? If a company does a buyback using the increased proceeds of debt, what would be the impact on the share price?

Applied Corporate Finance. Unit 4

Applied Corporate Finance Unit 4 Capital Structure Types of Financing Financing Behaviours Process of Raising Capital Tradeoff of Debt Optimal Capital Structure Various approaches to arriving at the optimal

Applied Corporate Finance Unit 4 Capital Structure Types of Financing Financing Behaviours Process of Raising Capital Tradeoff of Debt Optimal Capital Structure Various approaches to arriving at the optimal

Loss of future financing flexibility

Loss of future financing flexibility 22 When a firm borrows up to its capacity, it loses the flexibility of financing future projects with debt. Thus, if the firm is faced with an unexpected investment

Loss of future financing flexibility 22 When a firm borrows up to its capacity, it loses the flexibility of financing future projects with debt. Thus, if the firm is faced with an unexpected investment

Determinants of the Op0mal Debt Ra0o: 1. The marginal tax rate

78 Determinants of the Op0mal Debt Ra0o: 1. The marginal tax rate The primary benefit of debt is a tax benefit. The higher the marginal tax rate, the greater the benefit to borrowing: 78 2. Pre- tax Cash

78 Determinants of the Op0mal Debt Ra0o: 1. The marginal tax rate The primary benefit of debt is a tax benefit. The higher the marginal tax rate, the greater the benefit to borrowing: 78 2. Pre- tax Cash

Optimal Debt Ratio for a young, growth firm: Baidu

Optimal Debt Ratio for a young, growth firm: Baidu The optimal debt ratio for Baidu is between 0 and 10%, close to its current debt ratio of 5.23%, and much lower than the optimal debt ratios computed

Optimal Debt Ratio for a young, growth firm: Baidu The optimal debt ratio for Baidu is between 0 and 10%, close to its current debt ratio of 5.23%, and much lower than the optimal debt ratios computed

Applied Corporate Finance. Unit 5

Applied Corporate Finance Unit 5 Dividend Policy Measures Yield, Payout and Dividend Rate Determinants of Dividend Policy Various schools of though on Dividend Policy Managing Changes in Dividend Policy

Applied Corporate Finance Unit 5 Dividend Policy Measures Yield, Payout and Dividend Rate Determinants of Dividend Policy Various schools of though on Dividend Policy Managing Changes in Dividend Policy

Bond Ratings, Cost of Debt and Debt Ratios. Aswath Damodaran

Bond Ratings, Cost of Debt and Debt Ratios 49 Stated versus Effective Tax Rates You need taxable income for interest to provide a tax savings. Note that the EBIT at Disney is $10,032 million. As long as

Bond Ratings, Cost of Debt and Debt Ratios 49 Stated versus Effective Tax Rates You need taxable income for interest to provide a tax savings. Note that the EBIT at Disney is $10,032 million. As long as

CHAPTER 8 CAPITAL STRUCTURE: THE OPTIMAL FINANCIAL MIX. Operating Income Approach

CHAPTER 8 CAPITAL STRUCTURE: THE OPTIMAL FINANCIAL MIX What is the optimal mix of debt and equity for a firm? In the last chapter we looked at the qualitative trade-off between debt and equity, but we

CHAPTER 8 CAPITAL STRUCTURE: THE OPTIMAL FINANCIAL MIX What is the optimal mix of debt and equity for a firm? In the last chapter we looked at the qualitative trade-off between debt and equity, but we

CHAPTER 9 CAPITAL STRUCTURE - THE FINANCING DETAILS. A Framework for Capital Structure Changes

1 CHAPTER 9 CAPITAL STRUCTURE - THE FINANCING DETAILS In chapter 7, we looked at the wide range of choices available to firms to raise capital. In chapter 8, developed the tools needed to estimate the

1 CHAPTER 9 CAPITAL STRUCTURE - THE FINANCING DETAILS In chapter 7, we looked at the wide range of choices available to firms to raise capital. In chapter 8, developed the tools needed to estimate the

Finding the Right Financing Mix: The Capital Structure Decision

Packet 2: Corporate Finance Spring 2008 The Financing Principle The Dividend Principle Valuation 1 Finding the Right Financing Mix: The Capital Structure Decision Neither a borrower nor a lender be Someone

Packet 2: Corporate Finance Spring 2008 The Financing Principle The Dividend Principle Valuation 1 Finding the Right Financing Mix: The Capital Structure Decision Neither a borrower nor a lender be Someone

Corporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and Valuation

Corporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and Valuation B40.2302 Aswath Damodaran Aswath Damodaran! 1! Capital Structure: The Choices and the Trade off Neither a borrower

Corporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and Valuation B40.2302 Aswath Damodaran Aswath Damodaran! 1! Capital Structure: The Choices and the Trade off Neither a borrower

Capital Structure: The Choices and the Trade off

Corporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and Valuation B40.2302 Aswath Damodaran Aswath Damodaran! 1! Capital Structure: The Choices and the Trade off Neither a borrower

Corporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and Valuation B40.2302 Aswath Damodaran Aswath Damodaran! 1! Capital Structure: The Choices and the Trade off Neither a borrower

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

CHAPTER 9 CAPITAL STRUCTURE: THE FINANCING DETAILS. Immediate or Gradual Change. A Framework for Capital Structure Changes

1 2 CHAPTER 9 CAPITAL STRUCTURE: THE FINANCING DETAILS In Chapter 7, we looked at the wide range of choices available to firms to raise capital. In Chapter 8, we developed the tools needed to estimate

1 2 CHAPTER 9 CAPITAL STRUCTURE: THE FINANCING DETAILS In Chapter 7, we looked at the wide range of choices available to firms to raise capital. In Chapter 8, we developed the tools needed to estimate

PAPER No.: 8 Financial Management MODULE No. : 25 Capital Structure Theories IV: MM Hypothesis with Taxes, Merton Miller Argument

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 25: Capital Structure Theories IV: MM Hypothesis with Taxes and Merton Miller

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 25: Capital Structure Theories IV: MM Hypothesis with Taxes and Merton Miller

IV. Assessing Existing or Past investments

IV. Assessing Existing or Past investments 317 While much of our discussion has been focused on analyzing new investments, the techniques and principles enunciated apply just as strongly to existing investments.

IV. Assessing Existing or Past investments 317 While much of our discussion has been focused on analyzing new investments, the techniques and principles enunciated apply just as strongly to existing investments.

CORPORATE FINANCE FINAL EXAM: FALL 1992

Practice finals CORPORATE FINANCE FINAL EXAM: FALL 1992 1. You have been asked to analyze the capital structure of DASA Inc, and make recommendations on a future course of action. DASA Inc. has 40 million

Practice finals CORPORATE FINANCE FINAL EXAM: FALL 1992 1. You have been asked to analyze the capital structure of DASA Inc, and make recommendations on a future course of action. DASA Inc. has 40 million

Capital Structure I. Corporate Finance and Incentives. Lars Jul Overby. Department of Economics University of Copenhagen.

Capital Structure I Corporate Finance and Incentives Lars Jul Overby Department of Economics University of Copenhagen December 2010 Lars Jul Overby (D of Economics - UoC) Capital Structure I 12/10 1 /

Capital Structure I Corporate Finance and Incentives Lars Jul Overby Department of Economics University of Copenhagen December 2010 Lars Jul Overby (D of Economics - UoC) Capital Structure I 12/10 1 /

Aswath Damodaran 2. Finding the Right Financing Mix: The. Capital Structure Decision. Stern School of Business. Aswath Damodaran

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 2 First Principles Invest in projects that yield a return greater than the minimum

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 2 First Principles Invest in projects that yield a return greater than the minimum

FCF t. V = t=1. Topics in Chapter. Chapter 16. How can capital structure affect value? Basic Definitions. (1 + WACC) t

t") Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Chapter 15. Topics in Chapter. Capital Structure Decisions

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

CHAPTER 17: CAPITAL STRUCTURE: TRADEOFFS AND THEORY

CHAPTER 17: CAPITAL STRUCTURE: TRADEOFFS AND THEORY 17-1 a. Annual tax savings from debt = $ 40 million *.09 *.35 = $1.26 b. PV of Savings assuming savings are permanent = $40 million *.35 = $14.00 c.

CHAPTER 17: CAPITAL STRUCTURE: TRADEOFFS AND THEORY 17-1 a. Annual tax savings from debt = $ 40 million *.09 *.35 = $1.26 b. PV of Savings assuming savings are permanent = $40 million *.35 = $14.00 c.

THE FINANCING DECISION

1 THE FINANCING DECISION You can have too much debt or too little.. Debt Ratios across Companies 2 2 Debt Ratios across Sectors 3 3 The Financial Balance Sheet 4 Assets Liabilities Existing Investments

1 THE FINANCING DECISION You can have too much debt or too little.. Debt Ratios across Companies 2 2 Debt Ratios across Sectors 3 3 The Financial Balance Sheet 4 Assets Liabilities Existing Investments

Chapter 16 Capital Structure

Chapter 16 Capital Structure LEARNING OBJECTIVES 1. Explain why borrowing rates are different based on ability to repay loans. 2. Demonstrate the benefits of borrowing. 3. Calculate the break-even EBIT

Chapter 16 Capital Structure LEARNING OBJECTIVES 1. Explain why borrowing rates are different based on ability to repay loans. 2. Demonstrate the benefits of borrowing. 3. Calculate the break-even EBIT

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 3 20.02.2014 Selecting the Right Investment Projects Capital Budgeting Tools 2 The Capital Budgeting Process Generation

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 3 20.02.2014 Selecting the Right Investment Projects Capital Budgeting Tools 2 The Capital Budgeting Process Generation

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation Operating lease Operating Lease offers Financing AND MAINTENANCE: often the Lessor is the Supplier / Vendor of the Asset i.e.

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation Operating lease Operating Lease offers Financing AND MAINTENANCE: often the Lessor is the Supplier / Vendor of the Asset i.e.

Maximizing the value of the firm is the goal of managing capital structure.

Key Concepts and Skills Understand the effect of financial leverage on cash flows and the cost of equity Understand the impact of taxes and bankruptcy on capital structure choice Understand the basic components

Key Concepts and Skills Understand the effect of financial leverage on cash flows and the cost of equity Understand the impact of taxes and bankruptcy on capital structure choice Understand the basic components

PAPER No. 8: Financial Management MODULE No. 27: Capital Structure in practice

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 27: Capital Structure in Practice COM_P8_M27 TABLE OF CONTENTS 1. Learning outcomes

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 27: Capital Structure in Practice COM_P8_M27 TABLE OF CONTENTS 1. Learning outcomes

Advanced Corporate Finance. 3. Capital structure

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Quiz Bomb. Page 1 of 12

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Homework Solution Ch15

FIN 302 Homework Solution Ch15 Chapter 15: Debt Policy 1. a. True. b. False. As financial leverage increases, the expected rate of return on equity rises by just enough to compensate for its higher risk.

FIN 302 Homework Solution Ch15 Chapter 15: Debt Policy 1. a. True. b. False. As financial leverage increases, the expected rate of return on equity rises by just enough to compensate for its higher risk.

Capital Structure Planning. Why Financial Restructuring?

Giddy/SIM Capital Structure /1 SIM/NYU The Job of the CFO Capital Structure Planning Prof. Ian Giddy New York University Why Financial Restructuring? The Asian Bet The Solution, Part I: Recapitalization

Giddy/SIM Capital Structure /1 SIM/NYU The Job of the CFO Capital Structure Planning Prof. Ian Giddy New York University Why Financial Restructuring? The Asian Bet The Solution, Part I: Recapitalization

Valuing Equity in Firms in Distress!

Valuing Equity in Firms in Distress! Aswath Damodaran http://www.damodaran.com Aswath Damodaran! 1! The Going Concern Assumption! Traditional valuation techniques are built on the assumption of a going

Valuing Equity in Firms in Distress! Aswath Damodaran http://www.damodaran.com Aswath Damodaran! 1! The Going Concern Assumption! Traditional valuation techniques are built on the assumption of a going

Capital Structure Decisions

GSU, Department of Finance, AFM - Capital Structure / page 1 - Corporate Finance Capital Structure Decisions - Relevant textbook pages - none - Relevant eoc-problems - none - Other relevant material -

GSU, Department of Finance, AFM - Capital Structure / page 1 - Corporate Finance Capital Structure Decisions - Relevant textbook pages - none - Relevant eoc-problems - none - Other relevant material -

600 Solved MCQs of MGT201 BY

600 Solved MCQs of MGT201 BY http://vustudents.ning.com Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

600 Solved MCQs of MGT201 BY http://vustudents.ning.com Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION

1 CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION In the last chapter, you were introduced to the notion that the value of an asset is determined by its expected cash flows

1 CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION In the last chapter, you were introduced to the notion that the value of an asset is determined by its expected cash flows

OPTIMAL FINANCING MIX II: THE COST OF CAPITAL APPROACH. It is be8er to have a lower hurdle rate than a higher one.

OPTIMAL FINANCING MIX II: THE COST OF CAPITAL APPROACH It is be8er to have a lower hurdle rate than a higher one. Set Up and Objective 1: What is corporate finance 2: The Objective: Utopia and Let Down

OPTIMAL FINANCING MIX II: THE COST OF CAPITAL APPROACH It is be8er to have a lower hurdle rate than a higher one. Set Up and Objective 1: What is corporate finance 2: The Objective: Utopia and Let Down

Homework Solutions - Lecture 2 Part 2

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Quiz 3: Spring This quiz is worth 10% and you have 30 minutes. and cost of capital at 20%. The long term treasury bond rate is 7%.

Practice Quizzes Quiz 3: Spring 1998 This quiz is worth 10% and you have 30 minutes. 1. You have been provided the information on the after-tax cost of debt and cost of capital that a company will have

Practice Quizzes Quiz 3: Spring 1998 This quiz is worth 10% and you have 30 minutes. 1. You have been provided the information on the after-tax cost of debt and cost of capital that a company will have

Debt. Firm s assets. Common Equity

Debt/Equity Definition The mix of securities that a firm uses to finance its investments is called its capital structure. The two most important such securities are debt and equity Debt Firm s assets Common

Debt/Equity Definition The mix of securities that a firm uses to finance its investments is called its capital structure. The two most important such securities are debt and equity Debt Firm s assets Common

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Optimal Capital Structure Analysis for Energy Companies Listed in Indonesia Stock Exchange

Optimal Capital Structure Analysis for Energy Companies Listed in Indonesia Stock Exchange Nadhila Qamarani* The main goal of managerial finance is to maximize shareholders wealth which is highly affected

Optimal Capital Structure Analysis for Energy Companies Listed in Indonesia Stock Exchange Nadhila Qamarani* The main goal of managerial finance is to maximize shareholders wealth which is highly affected

CHAPTER IV DATA ANALYSIS. Table 4.1 Risk Free Rate and Market Return

CHAPTER IV DATA ANALYSIS 4.1 Research Data Collection There are 13 data from 5 companies from year 2009 until 2011 that are used as sample in this research. Actualy, the total sample from IDX 2009 are

CHAPTER IV DATA ANALYSIS 4.1 Research Data Collection There are 13 data from 5 companies from year 2009 until 2011 that are used as sample in this research. Actualy, the total sample from IDX 2009 are

AFM 371 Practice Problem Set #2 Winter Suggested Solutions

AFM 371 Practice Problem Set #2 Winter 2008 Suggested Solutions 1. Text Problems: 16.2 (a) The debt-equity ratio is the market value of debt divided by the market value of equity. In this case we have

AFM 371 Practice Problem Set #2 Winter 2008 Suggested Solutions 1. Text Problems: 16.2 (a) The debt-equity ratio is the market value of debt divided by the market value of equity. In this case we have

EMP 62 Corporate Finance

Kellogg EMP 62 Corporate Finance Capital Structure 1 Today s Agenda Introduce the effect of debt on firm value in a basic model Consider the effect of taxes on capital structure, firm valuation, and the

Kellogg EMP 62 Corporate Finance Capital Structure 1 Today s Agenda Introduce the effect of debt on firm value in a basic model Consider the effect of taxes on capital structure, firm valuation, and the

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Mandated Dividend Payouts

Mandated Dividend Payouts 207 Assume now that the government decides to mandate a minimum dividend payout for all companies. Given our discussion of FCFE, what types of companies will be hurt the most

Mandated Dividend Payouts 207 Assume now that the government decides to mandate a minimum dividend payout for all companies. Given our discussion of FCFE, what types of companies will be hurt the most

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file Which group of ratios measures a firm's ability to meet short-term obligations? Liquidity ratios Debt ratios Coverage ratios Profitability

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file Which group of ratios measures a firm's ability to meet short-term obligations? Liquidity ratios Debt ratios Coverage ratios Profitability

Final Exam: Corporate Finance

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Regal Inc. is a publicly traded company that operates in the travel

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Regal Inc. is a publicly traded company that operates in the travel

MGT201 Financial Management Solved MCQs

MGT201 Financial Management Solved MCQs Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because they have invested

MGT201 Financial Management Solved MCQs Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because they have invested

CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS

CHAPTER 15 B- 1 CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals

CHAPTER 15 B- 1 CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals

Capital Structure Applications

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Chapter 16 Debt Policy

Chapter 16 Debt Policy Konan Chan Financial Management, Fall 2018 Topic Covered Capital structure decision Leverage effect Capital structure theory MM (no taxes) MM (with taxes) Trade-off Pecking order

Chapter 16 Debt Policy Konan Chan Financial Management, Fall 2018 Topic Covered Capital structure decision Leverage effect Capital structure theory MM (no taxes) MM (with taxes) Trade-off Pecking order

Capital structure I: Basic Concepts

Capital structure I: Basic Concepts What is a capital structure? The big question: How should the firm finance its investments? The methods the firm uses to finance its investments is called its capital

Capital structure I: Basic Concepts What is a capital structure? The big question: How should the firm finance its investments? The methods the firm uses to finance its investments is called its capital

THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613. Business Finance Final Exam

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Learn about bond investing. Investor education

Learn about bond investing Investor education The dual roles bonds can play in your portfolio Bonds can play an important role in a welldiversified investment portfolio, helping to offset the volatility

Learn about bond investing Investor education The dual roles bonds can play in your portfolio Bonds can play an important role in a welldiversified investment portfolio, helping to offset the volatility

Question # 1 of 15 ( Start time: 01:53:35 PM ) Total Marks: 1

Total Marks: 1") MGT 201 - Financial Management (Quiz # 5) 380+ Quizzes solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Date Monday 31st January and Tuesday 1st February 2011 Question # 1 of 15 ( Start time: 01:53:35 PM

MGT 201 - Financial Management (Quiz # 5) 380+ Quizzes solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Date Monday 31st January and Tuesday 1st February 2011 Question # 1 of 15 ( Start time: 01:53:35 PM

Applied Corporate Finance. Unit 2

Applied Corporate Finance Unit 2 Calculating the Hurdle Rate Definition of Risk Risk vs Return Hurdle Rate Choosing a risk return model CAPM Risk Free Rate Equity Risk Premium Beta First Principles Maximize

Applied Corporate Finance Unit 2 Calculating the Hurdle Rate Definition of Risk Risk vs Return Hurdle Rate Choosing a risk return model CAPM Risk Free Rate Equity Risk Premium Beta First Principles Maximize

Final Exam: Corporate Finance

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. GRL Inc. is a publicly traded company that operates in the software

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. GRL Inc. is a publicly traded company that operates in the software

Chapter 14: Capital Structure in a Perfect Market

Chapter 14: Capital Structure in a Perfect Market-1 Chapter 14: Capital Structure in a Perfect Market I. Overview 1. Capital structure: Note: usually use leverage ratios like debt/assets to measure the

Chapter 14: Capital Structure in a Perfect Market-1 Chapter 14: Capital Structure in a Perfect Market I. Overview 1. Capital structure: Note: usually use leverage ratios like debt/assets to measure the

Case 3: BP: Summary of Dividend Policy:

208 Case 3: BP: Summary of Dividend Policy: 1982-1991 Summary of calculations Average Standard Deviation Maximum Minimum Free CF to Equity $571.10 $1,382.29 $3,764.00 ($612.50) Dividends $1,496.30 $448.77

208 Case 3: BP: Summary of Dividend Policy: 1982-1991 Summary of calculations Average Standard Deviation Maximum Minimum Free CF to Equity $571.10 $1,382.29 $3,764.00 ($612.50) Dividends $1,496.30 $448.77

Chapter 18 Interest rates / Transaction Costs Corporate Income Taxes (Cash Flow Effects) Example - Summary for Firm U Summary for Firm L

Example - Summary for Firm U Summary for Firm L") Chapter 18 In Chapter 17, we learned that with a certain set of (unrealistic) assumptions, a firm's value and investors' opportunities are determined by the asset side of the firm's balance sheet (i.e.,

Chapter 18 In Chapter 17, we learned that with a certain set of (unrealistic) assumptions, a firm's value and investors' opportunities are determined by the asset side of the firm's balance sheet (i.e.,

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

A final thought: Side Costs and Benefits

A final thought: Side Costs and Benefits Most projects considered by any business create side costs and benefits for that business. The side costs include the costs created by the use of resources that

A final thought: Side Costs and Benefits Most projects considered by any business create side costs and benefits for that business. The side costs include the costs created by the use of resources that

Chapter 15. Chapter 15 Overview

Chapter 15 Debt Policy: The Capital Structure Decision Chapter 15 Overview Target and Optimal Capital Structure Risk and Different Types of Financing Business Risk Financial Risk Determining the Optimal

Chapter 15 Debt Policy: The Capital Structure Decision Chapter 15 Overview Target and Optimal Capital Structure Risk and Different Types of Financing Business Risk Financial Risk Determining the Optimal

Risk and Term Structure of Interest Rates

Risk and Term Structure of Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Explain factors that can cause interest rates to be different for bonds of different

Risk and Term Structure of Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Explain factors that can cause interest rates to be different for bonds of different

Solved MCQs MGT201. (Group is not responsible for any solved content)

") Solved MCQs 2010 MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

Solved MCQs 2010 MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

Chapter 13 Capital Structure and Distribution Policy

Chapter 13 Capital Structure and Distribution Policy Learning Objectives After reading this chapter, students should be able to: Differentiate among the following capital structure theories: Modigliani

Chapter 13 Capital Structure and Distribution Policy Learning Objectives After reading this chapter, students should be able to: Differentiate among the following capital structure theories: Modigliani

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 3: Capital Structure

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 3: Capital Structure Ibrahim Sameer AVID College Page 1 Chapter 3: Capital Structure Introduction Capital

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 3: Capital Structure Ibrahim Sameer AVID College Page 1 Chapter 3: Capital Structure Introduction Capital

Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions

Analysis Quiz Questions") Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions 1. How much would you be willing to pay for a company that generates exactly $100 in Free Cash Flow into eternity?

Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions 1. How much would you be willing to pay for a company that generates exactly $100 in Free Cash Flow into eternity?

A Primer on Financial Statements

A Primer on Financial Statements Much of the information that is used in valuation and corporate finance comes from financial statements. An understanding of the basic financial statements and some of

A Primer on Financial Statements Much of the information that is used in valuation and corporate finance comes from financial statements. An understanding of the basic financial statements and some of

Problem 4 The expected rate of return on equity after 1998 = (0.055) = 12.3% The dividends from 1993 onwards can be estimated as:

= 12.3% The dividends from 1993 onwards can be estimated as:") Chapter 12: Basics of Valuation Problem 1 a. False. We can use it to value the firm by looking at the dividends that will be paid after the high growth period ends. b. False. There is no built-in conservatism

Chapter 12: Basics of Valuation Problem 1 a. False. We can use it to value the firm by looking at the dividends that will be paid after the high growth period ends. b. False. There is no built-in conservatism

Module 4: Capital Structure and Dividend Policy

Module 4: Capital Structure and Dividend Policy Reading 4.1 Capital structure theory Reading 4.2 Capital structure theory in perfect markets Reading 4.3 Impact of corporate taxes on capital structure Reading

Module 4: Capital Structure and Dividend Policy Reading 4.1 Capital structure theory Reading 4.2 Capital structure theory in perfect markets Reading 4.3 Impact of corporate taxes on capital structure Reading

Advanced Risk Management

Winter 2015/2016 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 4: Risk Management Motives Perfect financial markets Assumptions: no taxes no transaction costs no

Winter 2015/2016 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 4: Risk Management Motives Perfect financial markets Assumptions: no taxes no transaction costs no

Value Enhancement: Back to Basics

Value Enhancement: Back to Basics Aswath Damodaran NACVA Conference Aswath Damodaran 1 Price Enhancement versus Value Enhancement Aswath Damodaran 2 DISCOUNTED CASHFLOW VALUATION Cashflow to Firm EBIT

Value Enhancement: Back to Basics Aswath Damodaran NACVA Conference Aswath Damodaran 1 Price Enhancement versus Value Enhancement Aswath Damodaran 2 DISCOUNTED CASHFLOW VALUATION Cashflow to Firm EBIT

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Clarix Inc. is a publicly traded company that operates in two businesses

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Clarix Inc. is a publicly traded company that operates in two businesses

Applied Corporate Finance Project for. M/s. Godrej Consumer Products Ltd

Applied Corporate Finance Project for M/s. Godrej Consumer Products Ltd (Finance Elective Paper in III Semester) Mini Project Report submitted in partial fulfillment of the requirements for the award of

Applied Corporate Finance Project for M/s. Godrej Consumer Products Ltd (Finance Elective Paper in III Semester) Mini Project Report submitted in partial fulfillment of the requirements for the award of

Page 515 Summary and Conclusions

Page 515 Summary and Conclusions 1. We began our discussion of the capital structure decision by arguing that the particular capital structure that maximizes the value of the firm is also the one that

Page 515 Summary and Conclusions 1. We began our discussion of the capital structure decision by arguing that the particular capital structure that maximizes the value of the firm is also the one that

FUNDAMENTALS OF CREDIT ANALYSIS

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

Chapters 10&11 - Debt Securities

Chapters 10&11 - Debt Securities Bond characteristics Interest rate risk Bond rating Bond pricing Term structure theories Bond price behavior to interest rate changes Duration and immunization Bond investment

Chapters 10&11 - Debt Securities Bond characteristics Interest rate risk Bond rating Bond pricing Term structure theories Bond price behavior to interest rate changes Duration and immunization Bond investment

Valuation Inferno: Dante meets

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

Allison Behuniak, Taylor Jordan, Bettina Lopes, and Thomas Testa. William Wrigley Jr. Company: Capital Structure, Valuation, and Cost of Capital

Allison Behuniak, Taylor Jordan, Bettina Lopes, and Thomas Testa William Wrigley Jr. Company: Capital Structure, Valuation, and Cost of Capital The Situation ² Aurora Borealis was an active-investor hedge

Allison Behuniak, Taylor Jordan, Bettina Lopes, and Thomas Testa William Wrigley Jr. Company: Capital Structure, Valuation, and Cost of Capital The Situation ² Aurora Borealis was an active-investor hedge

MGT Financial Management Mega Quiz file solved by Muhammad Afaaq

MGT 201 - Financial Management Mega Quiz file solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Afaaqtariq233@gmail.com Asslam O Alikum MGT 201 Mega Quiz file solved by Muhammad Afaaq Remember Me in Your

MGT 201 - Financial Management Mega Quiz file solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Afaaqtariq233@gmail.com Asslam O Alikum MGT 201 Mega Quiz file solved by Muhammad Afaaq Remember Me in Your

I m going to cover 6 key points about FCF here:

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

CHAPTER 4 SHOW ME THE MONEY: THE BASICS OF VALUATION

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 2. False. A reduction in leverage will decrease both the risk of the stock and its expected return.

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 2. False. A reduction in leverage will decrease both the risk of the stock and its expected return.

EMBA in Management & Finance. Corporate Finance. Eric Jondeau

EMA in Management & Finance Corporate Finance EMA in Management & Finance Lecture 3: Capital Structure Modigliani and Miller Outline 1 The Capital-Structure Question 2 Financial Leverage and Firm Value

EMA in Management & Finance Corporate Finance EMA in Management & Finance Lecture 3: Capital Structure Modigliani and Miller Outline 1 The Capital-Structure Question 2 Financial Leverage and Firm Value

Twelve Myths in Valuation

Twelve Myths in Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Why do valuation? " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 1. Valuation is a science

Twelve Myths in Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Why do valuation? " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 1. Valuation is a science

Financial Leverage: the extent to which a company is committed to fixed charges related to interest payments. Measured by:

Wk 11 FINS1613 Notes 13.1 Discuss the effect of Financial Leverage Financial Leverage: the extent to which a company is committed to fixed charges related to interest payments. Measured by: The debt to

Wk 11 FINS1613 Notes 13.1 Discuss the effect of Financial Leverage Financial Leverage: the extent to which a company is committed to fixed charges related to interest payments. Measured by: The debt to

Introduction This note gives an introduction to the concept of relative valuation using market comparables. Relative valuation is the predominate meth

Saïd Business School teaching notes APRIL 2009 Note on Valuation and Mechanics of LBOs This Note was prepared by Tim Jenkinson and Ruediger Stucke. Tim Jenkinson is Professor of Finance at the Saïd Business

Saïd Business School teaching notes APRIL 2009 Note on Valuation and Mechanics of LBOs This Note was prepared by Tim Jenkinson and Ruediger Stucke. Tim Jenkinson is Professor of Finance at the Saïd Business

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending Today: I. What s a Repo? II. Financing with Repos III. Shorting with Repos IV. Specialness and Supply

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending Today: I. What s a Repo? II. Financing with Repos III. Shorting with Repos IV. Specialness and Supply

Financial Leverage and Capital Structure Policy

Key Concepts and Skills Chapter 17 Understand the effect of financial leverage on cash flows and the cost of equity Understand the Modigliani and Miller Theory of Capital Structure with/without Taxes Understand

Key Concepts and Skills Chapter 17 Understand the effect of financial leverage on cash flows and the cost of equity Understand the Modigliani and Miller Theory of Capital Structure with/without Taxes Understand

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Valuation: Closing Thoughts

Valuation: Closing Thoughts Spring 2010 Aswath Damodaran Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately) to

Valuation: Closing Thoughts Spring 2010 Aswath Damodaran Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately) to

OPTIMAL CAPITAL STRUCTURE & CAPITAL BUDGETING WITH TAXES

OPTIMAL CAPITAL STRUCTURE & CAPITAL BUDGETING WITH TAXES Topics: Consider Modigliani & Miller s insights into optimal capital structure Without corporate taxes è Financing policy is irrelevant With corporate

OPTIMAL CAPITAL STRUCTURE & CAPITAL BUDGETING WITH TAXES Topics: Consider Modigliani & Miller s insights into optimal capital structure Without corporate taxes è Financing policy is irrelevant With corporate

Corporate Financial Management. Lecture 3: Other explanations of capital structure

Corporate Financial Management Lecture 3: Other explanations of capital structure As we discussed in previous lectures, two extreme results, namely the irrelevance of capital structure and 100 percent

Corporate Financial Management Lecture 3: Other explanations of capital structure As we discussed in previous lectures, two extreme results, namely the irrelevance of capital structure and 100 percent

Fall 1996 Problem 1. Problem 3 Unlevered Beta (using last 5 years) = 0.9/(1+(1-.4)(.2)) = 0.80 Unlevered Beta of Non-cash assets = 0.80/(1-.15) = 0.

= 0.9/(1+(1-.4)(.2)) = 0.80 Unlevered Beta of Non-cash assets = 0.80/(1-.15) = 0.") Spring 1996 Price/BV for AlumCare = 4 P/BV ratio for HealthSoft = 2 If AlumCare's Price is thrice that of HealthSoft, Let MV of Equity for AlumCare = $ 100.00 Then MV of Equity for HealthSoft = $ 33.33

Spring 1996 Price/BV for AlumCare = 4 P/BV ratio for HealthSoft = 2 If AlumCare's Price is thrice that of HealthSoft, Let MV of Equity for AlumCare = $ 100.00 Then MV of Equity for HealthSoft = $ 33.33