Homework Solutions - Lecture 2

|

|

|

- Jonah Jacobs

- 5 years ago

- Views:

Transcription

1 Homework Solutions - Lecture 2 1. The value of the S&P 500 index is and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over 4%. a. Calculate the implied equity premium assuming the dividend yield in the most recent year was 4% of the current index value and dividends are expected to grow at a constant rate of 5% annually. How does this implied premium compare to the value we calculated when ignoring repurchases? Div = (.04)(1.05) = Div1 R = g + =.05 + CurrentValue = = 9.20% Implied Risk Premium = = 7.37% All of the values in this problem are the same as the problem we did in class except the dividend yield. Because the current value of the index ( ) does not change, but the forecasted dividends here are higher, the implied premium is higher than the one we calculated in class. Note that Damodaran suggests using the L-T Treasury yield as an estimate of long-term growth. If you replace the 5% long-term growth rate with 1.83%, the implied risk premium equals 4.2%. b. Calculate the implied equity premium assuming the dividend yield in the most recent year was 4% of the current index value, dividends are expected to grow at an annual rate of 10% for the next five years, and at a constant rate of 5% thereafter (Hint: you can use the solver function in excel). How does this implied premium compare to the value we calculated when ignoring repurchases? Here you will need to use the Solver function in excel. Specifically, you should solve for the required return that sets the present value of future dividends equal to the current index value. Div = (.04)(1.10) = = /( R.05) + 5 R = 10.20% Implied Risk Premium = = 8.37% Again, all of the values in this problem are the same as the problem we did in class except the dividend yield. Because the current value of the index ( ) does not change, but the forecasted dividends here are higher, the implied premium is higher than the one we calculated in class. Again, Damodaran might suggest replacing the 5% long-term growth rate with the 1.83% treasury yield. If we make this substitution, the risk-premium equals 5.78%.

2 2. An analyst at your firm comes to you with a valuation of a Greek firm done with Euro cash flows. The analyst has used the 24.69% yield on the Euro-denominated Greek government bond as the riskfree rate in the cost of equity calculation, along with a 4.5% global equity risk premium. What assumptions is this analyst making about country risk? Would it be appropriate for the analyst to add a separate country risk premium to the CAPM equation? The 24.69% yield on the Greek Euro bond includes a real risk-free rate, an expectation of inflation, and a default spread. Including the default spread is one method of estimating country risk. The implicit assumptions are that (1) the country risk premium can be approximated by the default spread on local government bonds, and (2) the sensitivity to country risk is the same across all firms in the Greece, or λ=1. Because the analyst has already implicitly incorporated country risk, an additional country risk term should not be added separately. Yields on 10-Year Government Bonds 30.0% 25.0% 20.0% 15.0% 22.80% estimated default spread 1.89% risk-free rate based on German Euro bond (including estimate of Euro inflation) 24.69% 10.0% 6.24% 7.34% 10.48% 5.0% 0.0% -0.60% 1.75% 2.73% 1.89% 2.81% 1.45% 3.45% 3.69% -5.0% U.S. (Inflation Indexed) U.S. ($U.S.) Brazil C-Bond ($U.S.) Italy (Euro) Germany (Euro) Spain (Euro) Greece (Euro) Portugal (Euro) Japan (Yen) Singapore (SGD) China (Yuan) Mexico (Peso) ( Risk Premium ) Country Spread E( R) = R f + β U S % Euro risk-free rate (excluding 22.80% country default spread) 22.80% country bond default spread for Greek CCC rated bonds %

3 3. In 1995, Time Warner Inc. had a Beta of Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989, which amounted to $10 billion in The market value of equity at Time Warner in 1995 was also $10 billion. The marginal tax rate was 40%. a) Estimate the unlevered Beta for Time Warner as of Using the formula for leveraging a beta that includes tax effects (to account for the extremely high and changing leverage), we get: E 10 β u = β e = 1.61 = D(1 T ) + E 10(1.4) + 10 b) Estimate the Beta for Time Warner in 1996 and 1997 if the debt/equity ratio is reduced by 10% each year (i.e., from 1.00 in 1995 to 0.90 in 1996 and 0.80 in 1997). The debt/equity ratio in 1995 was 10/10 = 1.0. If the debt ratio goes from 1.0 in 1995, to 0.9 in 1996, and 0.8 in 1997, the levered betas for 1996 and 1997 would equal: D(1 T ) β e = β u 1 + = = E ( +.9(1.4)) D(1 T ) β e = β u 1 + = = E ( +.8(1.4))

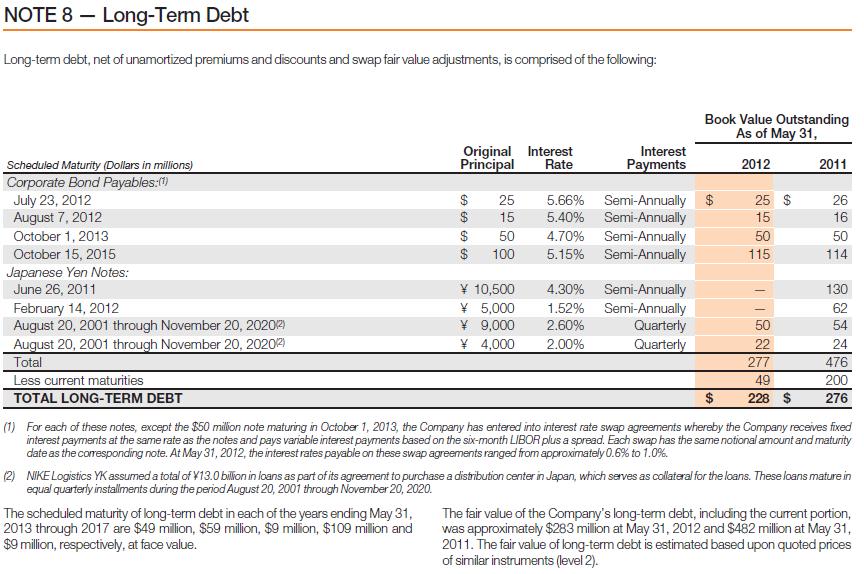

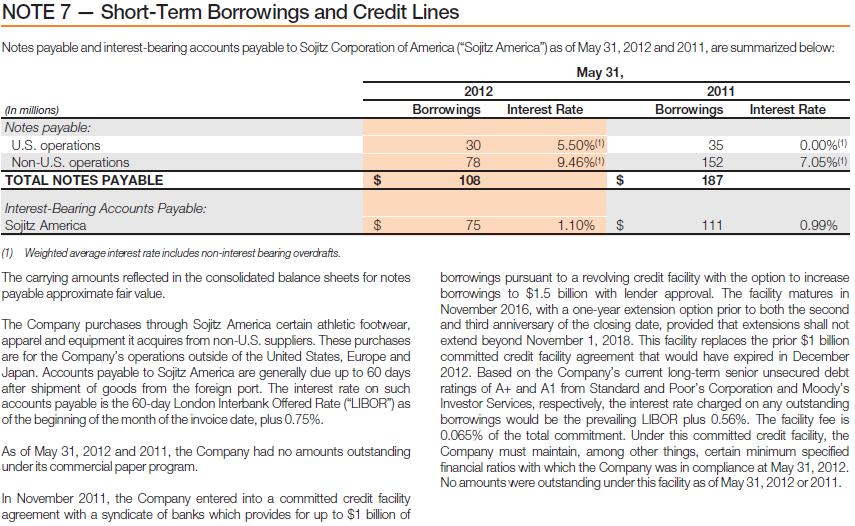

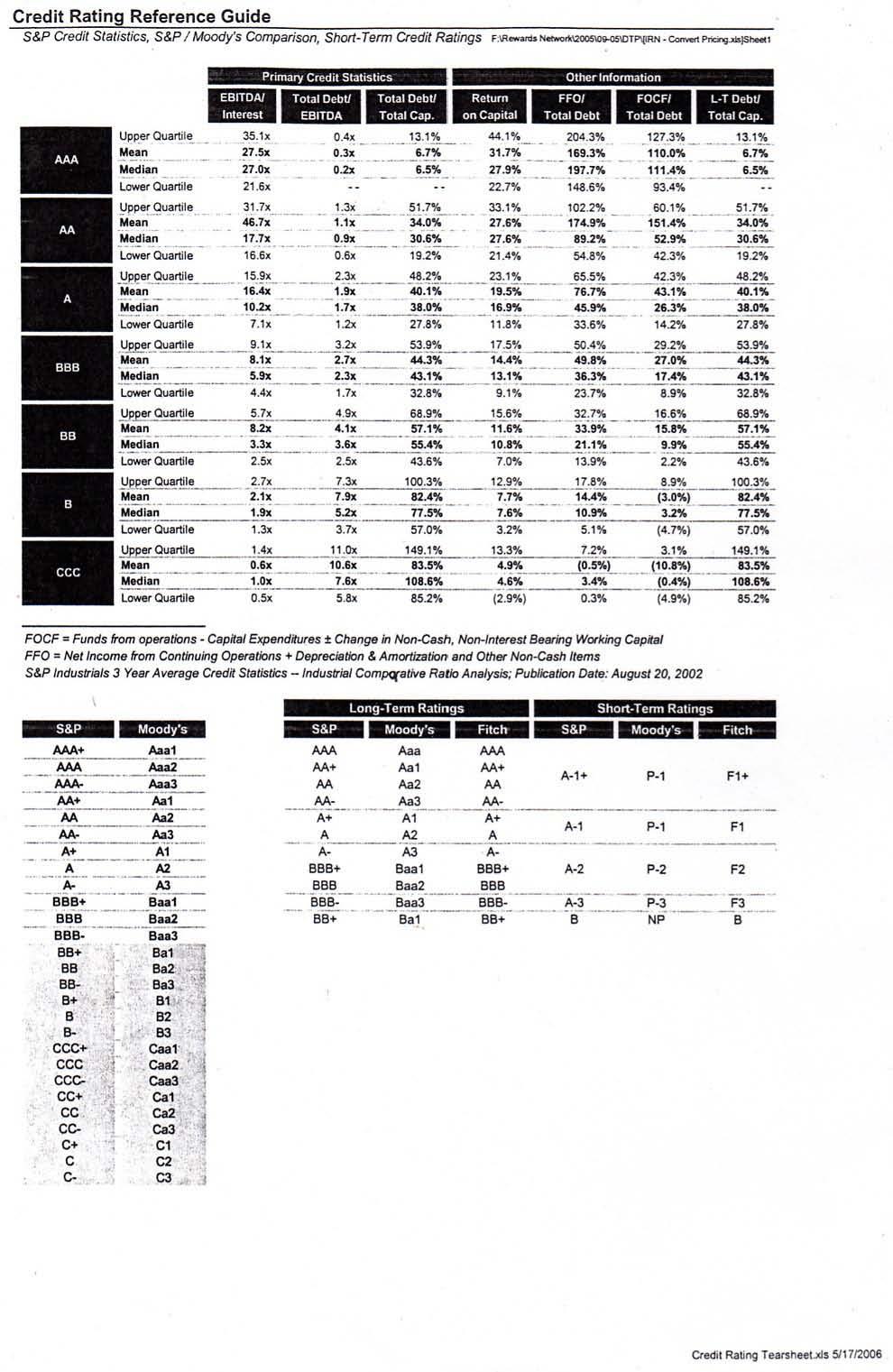

4 4. Cost of Capital for Nike: In this problem, you will calculate the cost of equity and weighted average cost of capital for Nike as of May 31, Be sure to explain any assumptions you make to arrive at your answers. a. Collect monthly return data for both Nike and the S&P 500 Index for the 60-month period ending in May Using this data, estimate the Beta for Nike based on a market model (CAPM) regression. Using this Beta estimate, calculate the cost of equity (K e ) for Nike based on the CAPM model. Note that you must choose an appropriate risk-free rate and market risk premium to use in the CAPM equation. Briefly explain your choice for each of these variables. I will assume that the risk-free rate equals the 10-year Treasury Yield as of 5/31/12, or 1.59%. The market model regression using 60-months of returns for Nike and the S&P gives a Beta estimate of (see the attached graph). I will use a market risk premium of 4.5%. This estimate reflects both the historical equity risk premium relative to U.S. Treasury Bonds and the implied equity premium calculations we discussed in class. Using this information, the cost of equity can be calculated as: K e = 1.59% (4.5%) = 5.68% Note that we might consider using a temporarily high market risk premium to be consistent with the unusually low risk-free rate. Using a market risk premium of 5.5% would give a cost of equity equal to 6.59%. We might also consider normalizing the risk-free rate. Using a risk-free rate of 4%, along with the market risk-premium of 4.5%, gives a cost of equity equal to 8.09%. b. Estimate the market value of debt and the market value of equity for Nike as of May 31, Use the firm's A+ rating and the default spreads provided in the course notes to estimate the firm's cost of debt (K d ). Using these estimates and your answer to (a), calculate the weighted average cost of capital (WACC) for Nike. Assume a marginal tax rate of 24.8%. Based on the default spread table provided in the class notes, the average default spread on A+ rated corporate bonds is 1.041%. Combining this with the risk-free rate from (a) gives a cost of debt equal to 2.63% (1.59% %). In the Notes to the Consolidated Financial Statements, Nike estimates the market value of longterm debt (including current installments) to be $283 million (compared to a book value of $277m). Combining this with the firm's short-term debt valued at $108 million gives a total market value for debt of $391 million. Using methods we will discuss in Lecture 3, I find that the debt value of Nike's operating leases equals $1,929 million (see the attached table). Together, this gives a total adjusted market value of debt equal to $2,320 million. Nike's shares outstanding include 90.0 million class A shares and million class B shares. Treating these shares as identical and multiplying by the stock price as of May 31, 2012 ($108.18) gives a total equity market value of $49,546 million. To this, we must add the after-tax value of employee stock options (which will be discussed in more detail in Lecture 5), or $1,138 million. This gives an adjusted market value of equity equal to $50,684 million.

5 Ignoring the adjustments for operating lease debt and employee stock options, the weighted average cost of capital (WACC) is calculated as: WACC = 5.68% + (2.63%)(1.248) = 5.65% After incorporating operating lease debt and employee stock options, the weighted average cost of capital (WACC) is calculated as: WACC = 5.68% + (2.63%)(1.248) = 5.52% Again, note that these values would change if we choose to normalize the market risk premium, the risk-free rate, or both.

6 5. Synthetic Debt Ratings: a. The following information was taken from the income statement and balance sheet of a real firm. Use this information to calculate the EBITDA-to-interest ratio, the Debt-to-EBITDA ratio, the Debt-to-Capital ratio, and the Return on Capital. Based on the values you calculate, use the S&P Ratings Guide on the attached page to estimate a synthetic debt rating for this firm. EBIT = $5,839 EBITDA = $7,455 Interest Expense = $530 Total Debt = $9,749 Stockholder s Equity = $18,889 Tax Rate = 36.7% EBITDA Interest Debt EBITDA = 7455 = = = Debt Capital 9749 = = 34.04% (1.367) ROC = = 12.91% Based on these ratios, the firm is roughly similar to other firms in the low A or high BBB ratings categories. b. The firm described above has significant operating leases. The notes to the financial statements show that the firm s operating lease expenses during the period were $823, of which $289 is estimated to be interest expense. In addition, you calculate the debt value of operating leases to be $5,927. Recalculate the ratios above incorporating this new information. Based on these corrected values, use the S&P Ratings Guide to estimate a revised synthetic debt rating for this firm. EBIT = $5, = $6,128 EBITDA = $7, = $8,278 Interest Expense = = $819 Total Debt = 9, ,927 = $15,676 Stockholder s Equity = $18,889 Tax Rate = 36.7% EBITDA Interest Debt EBITDA = 8278 = = = Debt Capital = = 45.35% (1.367) ROC = = 11.22% Based on these revised ratios, the firm appears to fall at the middle or high end of BBB rated firms (or the very low end of A rated firms). Note that I assume the operating lease expense of $823 is a combination of interest expense and depreciation.

7 Question 4 Regression Output: SUMMARY OUTPUT Regression Statistics R Square Observations 60 Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Intercept X Variable y = x R² = % 15.00% 10.00% 5.00% 0.00% % % % -5.00% 0.00% 5.00% 10.00% 15.00% -5.00% % % %

8

0 0 0 0 Operating Lease Commitments (mil) 2012 (or year +1) $408.0 $374.0 $334.0 $330.2 2013 (or year +2) $387.0 $310.0 $264.0 $281.3 2014 (or year +3) $271.0 $253.0 $220.0 $233.")

9 Question 4 Nike Operating Lease Information: Inputs: 5/31/2012 5/31/2011 5/31/2010 5/31/2009 Cost of Debt 2.63% 2.63% 2.63% 2.63% Round Annuity Length? (1=yes, 0=no) Operating Lease Commitments (mil) 2012 (or year +1) $408.0 $374.0 $334.0 $ (or year +2) $387.0 $310.0 $264.0 $ (or year +3) $271.0 $253.0 $220.0 $ (or year +4) $224.0 $198.0 $177.0 $ (or year +5) $186.0 $174.0 $148.0 $168.6 >2016 (after year ) $662.0 $535.0 $466.0 $588.5 Total $2,138.0 $1,844.0 $1,609.0 $1,797.8 Estimation (based on yr 5 pymt): Year 5 payment $186.0 $174.0 $148.0 $168.6 Annuity yrs PV of Lease Pmts $1,929.1 $1,669.8 $1, ,617.0

: Stock Price (S) $108.18 Stock Price (S) $108.18 Strike Price (X) $61.18 Strike Price (X) $61.18 Volatility (σ) 29.50% Volatility (σ) 29.50% Risk-free Rate 1.59% 1.")

10 Question 4 Nike Employee Stock Options Valuation: Employee Options at Nike updated 2012 Black-Scholes Option Pricing Model Inputs: Black-Scholes Option Pricing Model (with dilution) Inputs (with dilution effects): Stock Price (S) $ Stock Price (S) $ Strike Price (X) $61.18 Strike Price (X) $61.18 Volatility (σ) 29.50% Volatility (σ) 29.50% Risk-free Rate 1.59% 1.40% Risk-free Rate 1.59% Time to expiration (T) 6.30 yrs Time to expiration (T) 6.30 yrs Dividend Yield 1.40% Dividend Yield 1.40% # of Options (mil) # of Options (mil) # Shares Outstanding (mil) # Shares Outstanding (mil) Marginal Tax Rate 24.80% Marginal Tax Rate 24.80% Output: Output: Adjusted S (dilution) $ D D D D N(D1) N(D1) N(D2) N(D2) Call Price $50.19 Call Price $46.98 Put Price $6.49 Put Price $6.96 Value of Call Options (mil) $1, Value of Call Options (mil) $1, After-tax Option Value (mil) $1, After-tax Option Value (mil) $1,137.67

11

Homework Solutions - Lecture 2 Part 2

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 011 Wednesday, November 16, 011 INSTRUCTIONS: 1. You have 110 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 011 Wednesday, November 16, 011 INSTRUCTIONS: 1. You have 110 minutes to complete

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Monday, October 10, 2005 Multiple Choice (28 points) Choose the best answer

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Monday, October 10, 2005 Multiple Choice (28 points) Choose the best answer

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

Home Depot: Background and Model Choice. Home Depot: Background and Model Choice

Home Depot: Background and Model Choice Home Depot is the largest home improvement retailer in the world and the second largest retailer of any kind in the U.S. Because Home Depot s leverage ratio is fairly

Home Depot: Background and Model Choice Home Depot is the largest home improvement retailer in the world and the second largest retailer of any kind in the U.S. Because Home Depot s leverage ratio is fairly

Twelve Myths in Valuation

Twelve Myths in Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Why do valuation? " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 1. Valuation is a science

Twelve Myths in Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Why do valuation? " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 1. Valuation is a science

The Dark Side of Valuation

The Dark Side of Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 The Lemming Effect... Aswath Damodaran 2 To make our estimates, we draw our information from.. The firm

The Dark Side of Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 The Lemming Effect... Aswath Damodaran 2 To make our estimates, we draw our information from.. The firm

FINAL EXAM SOLUTIONS

FINAL EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Wednesday, December 14, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

FINAL EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Wednesday, December 14, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

Valuing Equity in Firms in Distress!

Valuing Equity in Firms in Distress! Aswath Damodaran http://www.damodaran.com Aswath Damodaran! 1! The Going Concern Assumption! Traditional valuation techniques are built on the assumption of a going

Valuing Equity in Firms in Distress! Aswath Damodaran http://www.damodaran.com Aswath Damodaran! 1! The Going Concern Assumption! Traditional valuation techniques are built on the assumption of a going

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 Misconceptions about Valuation

Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 Misconceptions about Valuation

Those who are interested in international business may wish to take FIN 430 which is our course on international financial management.

1 For the most part, the basic principles you ll learn in this class apply to both domestic and international businesses. However, two important differences you ll find when doing business internationally

1 For the most part, the basic principles you ll learn in this class apply to both domestic and international businesses. However, two important differences you ll find when doing business internationally

Practitioner s guide to cost of capital & WACC calculation

Practitioner s guide to cost of capital & WACC calculation EY Switzerland valuation best practice February 2018 Table of contents Introduction to cost of capital 1 Cost of equity 2 Cost of debt 3 Other

Practitioner s guide to cost of capital & WACC calculation EY Switzerland valuation best practice February 2018 Table of contents Introduction to cost of capital 1 Cost of equity 2 Cost of debt 3 Other

CHAPTER 19. Valuation and Financial Modeling: A Case Study. Chapter Synopsis

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

Sample Questions and Solutions

Sample Questions and Solutions Public Comparables Question Facts for Company XYZ: Closing stock price is $18.00 1,000 shares outstanding, and 100 outstanding options outstanding with an average exercise

Sample Questions and Solutions Public Comparables Question Facts for Company XYZ: Closing stock price is $18.00 1,000 shares outstanding, and 100 outstanding options outstanding with an average exercise

Understanding Financial Management: A Practical Guide Problems and Answers

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

FINAL EXAM SOLUTIONS

FINAL EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Module 2 Wednesday, December 7, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

FINAL EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Module 2 Wednesday, December 7, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

Valuation. Aswath Damodaran For the valuations in this presentation, go to Seminars/ Presentations. Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Valuation. Aswath Damodaran For the valuations in this presentation, go to Seminars/ Presentations. Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

More Tutorial at Corporate Finance

[Type text] More Tutorial at Corporate Finance Question 1. Hardwood Factories, Inc. Hardwood Factories (HF) expects earnings this year of $6/share, and it plans to pay a $4 dividend to shareholders this

[Type text] More Tutorial at Corporate Finance Question 1. Hardwood Factories, Inc. Hardwood Factories (HF) expects earnings this year of $6/share, and it plans to pay a $4 dividend to shareholders this

Discounted Cashflow Valuation: Equity and Firm Models. Aswath Damodaran 1

Discounted Cashflow Valuation: Equity and Firm Models 1 Summarizing the Inputs In summary, at this stage in the process, we should have an estimate of the the current cash flows on the investment, either

Discounted Cashflow Valuation: Equity and Firm Models 1 Summarizing the Inputs In summary, at this stage in the process, we should have an estimate of the the current cash flows on the investment, either

2013, Study Session #11, Reading # 37 COST OF CAPITAL 1. INTRODUCTION

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

Advanced Corporate Finance. 3. Capital structure

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Aswath Damodaran Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach Value = t=n CF t t=1(1+ r) t where CF t is the cash flow in period t, r is the discount

Discounted Cash Flow Valuation Aswath Damodaran Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach Value = t=n CF t t=1(1+ r) t where CF t is the cash flow in period t, r is the discount

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

Valuation of Warrants

Valuation of Warrants November 9, 2012 Situation Overview ($ in millions) Liberty Media announced that it is spinning off its Starz LLC ( Starz ) business into a new public company through a tax free distribution

Valuation of Warrants November 9, 2012 Situation Overview ($ in millions) Liberty Media announced that it is spinning off its Starz LLC ( Starz ) business into a new public company through a tax free distribution

Problem 4 The expected rate of return on equity after 1998 = (0.055) = 12.3% The dividends from 1993 onwards can be estimated as:

= 12.3% The dividends from 1993 onwards can be estimated as:") Chapter 12: Basics of Valuation Problem 1 a. False. We can use it to value the firm by looking at the dividends that will be paid after the high growth period ends. b. False. There is no built-in conservatism

Chapter 12: Basics of Valuation Problem 1 a. False. We can use it to value the firm by looking at the dividends that will be paid after the high growth period ends. b. False. There is no built-in conservatism

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Homework #4 BUSI 408 Summer II 2013

Homework #4 BUSI 408 Summer II 2013 This assignment is due 19 July 2013 at the beginning of class. Answer each question with numbers rounded to two decimal places. For relevant questions, identify the

Homework #4 BUSI 408 Summer II 2013 This assignment is due 19 July 2013 at the beginning of class. Answer each question with numbers rounded to two decimal places. For relevant questions, identify the

Valuation Inferno: Dante meets

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

CHAPTER 8 ESTIMATING RISK PARAMETERS AND COSTS OF FINANCING

Solutions to Investment Valuation 25 CHAPTER 8 ESTIMATING RISK PARAMETERS AND COSTS OF FINANCING Problem 1 We use the CAPM: The Expected Return on the stock = 0.058 + 0.95(0.0876) = 0.1412 = 14.12%. Since

Solutions to Investment Valuation 25 CHAPTER 8 ESTIMATING RISK PARAMETERS AND COSTS OF FINANCING Problem 1 We use the CAPM: The Expected Return on the stock = 0.058 + 0.95(0.0876) = 0.1412 = 14.12%. Since

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2006 Monday, November 13, 2006 INSTRUCTIONS: 1. You have 75 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2006 Monday, November 13, 2006 INSTRUCTIONS: 1. You have 75 minutes to complete

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

Indé Global knowledge sharing presents

Indé Global knowledge sharing presents Valuing multi-business, multi-national companies Presenter: Purvesh Kapadia About the Presenter Purvesh Kapadia Assistant Manager Financial Reporting and Valuation

Indé Global knowledge sharing presents Valuing multi-business, multi-national companies Presenter: Purvesh Kapadia About the Presenter Purvesh Kapadia Assistant Manager Financial Reporting and Valuation

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

Discount Rates I. The Riskfree Rate. Aswath Damodaran

27 Discount Rates I The Riskfree Rate The Risk Free Rate: Laying the Foundations 28 On a riskfree investment, the actual return is equal to the expected return. Therefore, there is no variance around the

27 Discount Rates I The Riskfree Rate The Risk Free Rate: Laying the Foundations 28 On a riskfree investment, the actual return is equal to the expected return. Therefore, there is no variance around the

Cost of Capital (represents risk)

") Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

CHAPTER 8 CAPITAL STRUCTURE: THE OPTIMAL FINANCIAL MIX. Operating Income Approach

CHAPTER 8 CAPITAL STRUCTURE: THE OPTIMAL FINANCIAL MIX What is the optimal mix of debt and equity for a firm? In the last chapter we looked at the qualitative trade-off between debt and equity, but we

CHAPTER 8 CAPITAL STRUCTURE: THE OPTIMAL FINANCIAL MIX What is the optimal mix of debt and equity for a firm? In the last chapter we looked at the qualitative trade-off between debt and equity, but we

COST OF CAPITAL

COST OF CAPITAL 2017 1 Introduction Cost of Capital (CoC) are the cost of funds used for financing a business CoC depends on the mode of financing used In most cases a combination of debt and equity is

COST OF CAPITAL 2017 1 Introduction Cost of Capital (CoC) are the cost of funds used for financing a business CoC depends on the mode of financing used In most cases a combination of debt and equity is

Final Exam: Corporate Finance

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Thexos Inc. is a company that has operated in two businesses, housewares

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Thexos Inc. is a company that has operated in two businesses, housewares

Optimal Capital Structure Analysis for Energy Companies Listed in Indonesia Stock Exchange

Optimal Capital Structure Analysis for Energy Companies Listed in Indonesia Stock Exchange Nadhila Qamarani* The main goal of managerial finance is to maximize shareholders wealth which is highly affected

Optimal Capital Structure Analysis for Energy Companies Listed in Indonesia Stock Exchange Nadhila Qamarani* The main goal of managerial finance is to maximize shareholders wealth which is highly affected

Applied Corporate Finance. Unit 4

Applied Corporate Finance Unit 4 Capital Structure Types of Financing Financing Behaviours Process of Raising Capital Tradeoff of Debt Optimal Capital Structure Various approaches to arriving at the optimal

Applied Corporate Finance Unit 4 Capital Structure Types of Financing Financing Behaviours Process of Raising Capital Tradeoff of Debt Optimal Capital Structure Various approaches to arriving at the optimal

FINC 3630: Advanced Business Finance Additional Practice Problems

FINC 3630: Advanced Business Finance Additional Practice Problems Accounting For Financial Management 1. Calculate free cash flow for Home Depot for the fiscal year-ended January 28, 2018 (the 2017 fiscal

FINC 3630: Advanced Business Finance Additional Practice Problems Accounting For Financial Management 1. Calculate free cash flow for Home Depot for the fiscal year-ended January 28, 2018 (the 2017 fiscal

IN PRACTICE WEBCAST: ESTIMATING THE COST OF CAPITAL. Aswath Damodaran

IN PRACTICE WEBCAST: ESTIMATING THE COST OF CAPITAL Aswath Damodaran The Cost of Capital 2 Step 1: Decide on currency Currency is a choice. You can estimate the cost of capital for any company, in any

IN PRACTICE WEBCAST: ESTIMATING THE COST OF CAPITAL Aswath Damodaran The Cost of Capital 2 Step 1: Decide on currency Currency is a choice. You can estimate the cost of capital for any company, in any

Final Exam Finance for AEO (Resit)

") Final Exam Finance for AEO (Resit) Course: Finance for AEO SubjectCode: 226P05 Date: 8 juli 2008 Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations

Final Exam Finance for AEO (Resit) Course: Finance for AEO SubjectCode: 226P05 Date: 8 juli 2008 Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations

FINC 3630: Advanced Business Finance Additional Practice Problems

FINC 3630: Advanced Business Finance Additional Practice Problems Accounting For Financial Management 1. Calculate free cash flow for Home Depot for the fiscal year-ended January 27, 2017 (the 2016 fiscal

FINC 3630: Advanced Business Finance Additional Practice Problems Accounting For Financial Management 1. Calculate free cash flow for Home Depot for the fiscal year-ended January 27, 2017 (the 2016 fiscal

Handout for Unit 4 for Applied Corporate Finance

Handout for Unit 4 for Applied Corporate Finance Unit 4 Capital Structure Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving

Handout for Unit 4 for Applied Corporate Finance Unit 4 Capital Structure Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde. Aswath Damodaran! 1!

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde Aswath Damodaran! 1! First Principles! Aswath Damodaran! 2! Three approaches to valuation! Intrinsic

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde Aswath Damodaran! 1! First Principles! Aswath Damodaran! 2! Three approaches to valuation! Intrinsic

Finance Recruiting Interview Preparation

Finance Recruiting Interview Preparation Discounted Cash Flows Session #3 This presentation is for informational purposes only, and is not an offer to buy or sell or a solicitation to buy or sell any securities,

Finance Recruiting Interview Preparation Discounted Cash Flows Session #3 This presentation is for informational purposes only, and is not an offer to buy or sell or a solicitation to buy or sell any securities,

4. E , = + (0.08)(20, 000) 5. D. Course 2 Solutions 51 May a

(20, 000) 5. D. Course 2 Solutions 51 May a") . D According to the semi-strong version of the efficient market theory, prices accurately reflect all publicly available information about a security. Thus, by this theory, actively managed portfolios

. D According to the semi-strong version of the efficient market theory, prices accurately reflect all publicly available information about a security. Thus, by this theory, actively managed portfolios

Homework Solutions - Lecture 1

Homework Solutions - Lecture 1 1. You are analyzing a company with the expected future cash flows shown below. Based on current market prices, the market value of the firm s equity is $1,96.9. The outstanding

Homework Solutions - Lecture 1 1. You are analyzing a company with the expected future cash flows shown below. Based on current market prices, the market value of the firm s equity is $1,96.9. The outstanding

Advanced Corporate Finance. 5. Options (a refresher)

") Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Week 6 Equity Valuation 1

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

12. Cost of Capital. Outline

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

Appendices Appendix 1. STOXX50 Moving Average Monthly Returns, Source: Bloomberg data, November 2016.

Appendices Appendix 1. STOXX50 Moving Average Monthly Returns, 1987-2016 Source: Bloomberg data, November 2016. 6% STOXX50 Moving Average Monthly Returns 4% 2% 0% 01/12/1987 01/12/1992 01/12/1997 01/12/2002

Appendices Appendix 1. STOXX50 Moving Average Monthly Returns, 1987-2016 Source: Bloomberg data, November 2016. 6% STOXX50 Moving Average Monthly Returns 4% 2% 0% 01/12/1987 01/12/1992 01/12/1997 01/12/2002

Real Options. Katharina Lewellen Finance Theory II April 28, 2003

Real Options Katharina Lewellen Finance Theory II April 28, 2003 Real options Managers have many options to adapt and revise decisions in response to unexpected developments. Such flexibility is clearly

Real Options Katharina Lewellen Finance Theory II April 28, 2003 Real options Managers have many options to adapt and revise decisions in response to unexpected developments. Such flexibility is clearly

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

MBA 203 Executive Summary

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

Economic Risk and Decision Analysis for Oil and Gas Industry CE School of Engineering and Technology Asian Institute of Technology

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.98 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.98 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Chapter 12: Estimating the Cost of Capital

Chapter 12: Estimating the Cost of Capital -1 Chapter 12: Estimating the Cost of Capital Fundamental question: Where do we get the numbers to estimate the cost of capital? => How do we implement the CAPM

Chapter 12: Estimating the Cost of Capital -1 Chapter 12: Estimating the Cost of Capital Fundamental question: Where do we get the numbers to estimate the cost of capital? => How do we implement the CAPM

DIVERSIFICATION, CONTROL & LIQUIDITY: THE DISCOUNT TRIFECTA. Aswath Damodaran

DIVERSIFICATION, CONTROL & LIQUIDITY: THE DISCOUNT TRIFECTA Aswath Damodaran www.damodran.com Fundamental Assumptions The Diversified Investor: Investors are rational and attempt to maximize expected returns,

DIVERSIFICATION, CONTROL & LIQUIDITY: THE DISCOUNT TRIFECTA Aswath Damodaran www.damodran.com Fundamental Assumptions The Diversified Investor: Investors are rational and attempt to maximize expected returns,

CHAPTER 9. Problems and Questions

1 CHAPTER 9 Problems and Questions (In the problems below, you can use a risk premium of 5.5% and a tax rate of 40% if either is not specified) 1. BMD is a firm with no debt on its books currently and

1 CHAPTER 9 Problems and Questions (In the problems below, you can use a risk premium of 5.5% and a tax rate of 40% if either is not specified) 1. BMD is a firm with no debt on its books currently and

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Chapter 8: Prospective Analysis: Valuation Implementation

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 1 Introduction to Valuation

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 1 Introduction to Valuation Lecture 1 is an introduction to valuation. This lecture is intended to give you an overview of

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 1 Introduction to Valuation Lecture 1 is an introduction to valuation. This lecture is intended to give you an overview of

Chapter 14 Capital Structure Decisions ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 14 Capital Structure Decisions ANSWERS TO END-OF-CHAPTER QUESTIONS 14-1 a. Capital structure is the manner in which a firm s assets are financed; that is, the righthand side of the balance sheet.

Chapter 14 Capital Structure Decisions ANSWERS TO END-OF-CHAPTER QUESTIONS 14-1 a. Capital structure is the manner in which a firm s assets are financed; that is, the righthand side of the balance sheet.

Capital Structure Applications

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

P2.T5. Market Risk Measurement & Management. Bruce Tuckman, Fixed Income Securities, 3rd Edition

P2.T5. Market Risk Measurement & Management Bruce Tuckman, Fixed Income Securities, 3rd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Tuckman, Chapter 6: Empirical

P2.T5. Market Risk Measurement & Management Bruce Tuckman, Fixed Income Securities, 3rd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Tuckman, Chapter 6: Empirical

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 15. Topics in Chapter. Capital Structure Decisions

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Risk, Return and Capital Budgeting

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

Toward A Bottom-Up Approach in Assessing Sovereign Default Risk

Toward A Bottom-Up Approach in Assessing Sovereign Default Risk Dr. Edward I. Altman Stern School of Business New York University Keynote Lecture Risk Day Conference MacQuarie University Sydney, Australia

Toward A Bottom-Up Approach in Assessing Sovereign Default Risk Dr. Edward I. Altman Stern School of Business New York University Keynote Lecture Risk Day Conference MacQuarie University Sydney, Australia

FUNDAMENTALS OF CORPORATE FINANCE

FUNDAMENTALS OF CORPORATE FINANCE Time Allowed: 2 Hours30 minutes Reading Time:10 Minutes GBAT9123 Sample exam SUPERVISED OPEN BOOK EXAMINATION INSTRUCTIONS 1. This is a supervised open book examination.

FUNDAMENTALS OF CORPORATE FINANCE Time Allowed: 2 Hours30 minutes Reading Time:10 Minutes GBAT9123 Sample exam SUPERVISED OPEN BOOK EXAMINATION INSTRUCTIONS 1. This is a supervised open book examination.

Valuation. Aswath Damodaran. Aswath Damodaran 186

Valuation Aswath Damodaran Aswath Damodaran 186 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

Valuation Aswath Damodaran Aswath Damodaran 186 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

FIN 350 Business Finance Homework 7 Fall 2014 Solutions

FIN 350 Business Finance Homework 7 Fall 2014 Solutions 1. Home Builder Supply, a retailer in the home improvement industry, currently operates seven retail outlets in Georgia and South Carolina. Management

FIN 350 Business Finance Homework 7 Fall 2014 Solutions 1. Home Builder Supply, a retailer in the home improvement industry, currently operates seven retail outlets in Georgia and South Carolina. Management

PE Ratios. Aswath Damodaran. Aswath Damodaran 1

PE Ratios Aswath Damodaran Aswath Damodaran 1 Price Earnings Ratio: Definition PE = Market Price per Share / Earnings per Share There are a number of variants on the basic PE ratio in use. They are based

PE Ratios Aswath Damodaran Aswath Damodaran 1 Price Earnings Ratio: Definition PE = Market Price per Share / Earnings per Share There are a number of variants on the basic PE ratio in use. They are based

Chapter 4: Risk Measurement and Hurdle Rates in Practice. 1. e. If you are doing the analysis in nominal pesos, you would use this rate.

Chapter 4: Risk Measurement and Hurdle Rates in Practice 1. e. If you are doing the analysis in nominal pesos, you would use this rate. 2. A. b. Ceteris paribus, I would expect the publicly traded company

Chapter 4: Risk Measurement and Hurdle Rates in Practice 1. e. If you are doing the analysis in nominal pesos, you would use this rate. 2. A. b. Ceteris paribus, I would expect the publicly traded company

Risk and Return of Short Duration Equity Investments

Risk and Return of Short Duration Equity Investments Georg Cejnek and Otto Randl, WU Vienna, Frontiers of Finance 2014 Conference Warwick, April 25, 2014 Outline Motivation Research Questions Preview of

Risk and Return of Short Duration Equity Investments Georg Cejnek and Otto Randl, WU Vienna, Frontiers of Finance 2014 Conference Warwick, April 25, 2014 Outline Motivation Research Questions Preview of

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

79 Discount Rates: III Relative Risk Measures 80 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

79 Discount Rates: III Relative Risk Measures 80 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

The Dark Side of Valuation Dante meets DCF

The Dark Side of Valuation Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran! 1! DCF Choices: Equity versus Firm Firm Valuation: Value the entire

The Dark Side of Valuation Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran! 1! DCF Choices: Equity versus Firm Firm Valuation: Value the entire

Consolidated Financial Results for the 1st Quarter of the Fiscal Year Ending March 31, 2009

NIHON KOHDEN CORPORATION (6849) August 6, 2008 Consolidated Financial Results for the 1st Quarter of the Fiscal Year Ending March 31, 2009 Stock Exchange Listing: Head Office: Representative: Contact:

NIHON KOHDEN CORPORATION (6849) August 6, 2008 Consolidated Financial Results for the 1st Quarter of the Fiscal Year Ending March 31, 2009 Stock Exchange Listing: Head Office: Representative: Contact:

1. True or false? Briefly explain.

1. True or false? Briefly explain. (a) Your firm has the opportunity to invest $20 million in a project with positive net present value. Even though this investment adds to the value of the firm, under

1. True or false? Briefly explain. (a) Your firm has the opportunity to invest $20 million in a project with positive net present value. Even though this investment adds to the value of the firm, under

15.414: COURSE REVIEW. Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2

: CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2") 15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

Final Exam. 5. (21 points) Short Questions. Parts (i)-(v) are multiple choice: in each case, only one answer is correct.

Short Questions. Parts (i)-(v) are multiple choice: in each case, only one answer is correct.") Final Exam Spring 016 Econ 180-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question 1. (10 points) What is the duration

Final Exam Spring 016 Econ 180-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question 1. (10 points) What is the duration

CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS

CHAPTER 15 B- 1 CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals

CHAPTER 15 B- 1 CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals

Chapter 12. Topics. Cost of Capital. The Cost of Capital

Chapter 12 The Cost of Capital Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC Measuring Capital Structure Required Rates of Return for individual types

Chapter 12 The Cost of Capital Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC Measuring Capital Structure Required Rates of Return for individual types

Financing decisions (2) Class 16 Financial Management,

Class 16 Financial Management,") Financing decisions (2) Class 16 Financial Management, 15.414 Today Capital structure M&M theorem Leverage, risk, and WACC Reading Brealey and Myers, Chapter 17 Key goal Financing decisions Ensure that

Financing decisions (2) Class 16 Financial Management, 15.414 Today Capital structure M&M theorem Leverage, risk, and WACC Reading Brealey and Myers, Chapter 17 Key goal Financing decisions Ensure that

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #5 Olga Bychkova Topics Covered Today Risk and the Cost of Capital (chapter 9 in BMA) Understading Options (chapter 20 in BMA) Valuing Options

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #5 Olga Bychkova Topics Covered Today Risk and the Cost of Capital (chapter 9 in BMA) Understading Options (chapter 20 in BMA) Valuing Options

Valuation: Lecture Note Packet 1 Intrinsic Valuation

Valuation: Lecture Note Packet 1 Intrinsic Valuation Aswath Damodaran Updated: September 2012 Aswath Damodaran 1 The essence of intrinsic value In intrinsic valuation, you value an asset based upon its

Valuation: Lecture Note Packet 1 Intrinsic Valuation Aswath Damodaran Updated: September 2012 Aswath Damodaran 1 The essence of intrinsic value In intrinsic valuation, you value an asset based upon its

CHAPTER 5 Bonds and Their Valuation

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

Lecture 6 Cost of Capital

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Estimating growth in EPS: Deutsche Bank in January 2008

238 Estimating growth in EPS: Deutsche Bank in January 2008 In 2007, Deutsche Bank reported net income of 6.51 billion Euros on a book value of equity of 33.475 billion Euros at the start of the year (end

238 Estimating growth in EPS: Deutsche Bank in January 2008 In 2007, Deutsche Bank reported net income of 6.51 billion Euros on a book value of equity of 33.475 billion Euros at the start of the year (end

Homework Solutions - Lecture 3

Homework Solutions - Lecture 3 1. Operating Lease Adjustments: Future operating lease commitments for Nike, as listed in Nike s most recent 10K, are shown below. Use this information to answer the questions

Homework Solutions - Lecture 3 1. Operating Lease Adjustments: Future operating lease commitments for Nike, as listed in Nike s most recent 10K, are shown below. Use this information to answer the questions

Options Markets: Introduction

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

] = [1 + (1 0.3)(10/70)] =

![] = [1 + (1 0.3)(10/70)] =](/thumbs/93/114475728.jpg "] = [1 + (1 0.3)(10/70)] =") 7.1. Sicily Pharmaceuticals has $10 million in debt and $70 million in equity. Its tax rate is 30%, cost of debt 8%, and beta 1.5. The riskless rate is 5% and the expected return on the market 12%. Sicily

7.1. Sicily Pharmaceuticals has $10 million in debt and $70 million in equity. Its tax rate is 30%, cost of debt 8%, and beta 1.5. The riskless rate is 5% and the expected return on the market 12%. Sicily

Homework Solutions - Lecture 3

Homework Solutions - Lecture 3 1. Operating Lease Adjustments: Future operating lease commitments for Nike, as listed in the 2009 10K, are shown below. Use this information to answer the questions below.

Homework Solutions - Lecture 3 1. Operating Lease Adjustments: Future operating lease commitments for Nike, as listed in the 2009 10K, are shown below. Use this information to answer the questions below.

EXAMINATION II: Fixed Income Analysis and Valuation. Derivatives Analysis and Valuation. Portfolio Management. Questions.

EXAMINATION II: Fixed Income Analysis and Valuation Derivatives Analysis and Valuation Portfolio Management Questions Final Examination March 2010 Question 1: Fixed Income Analysis and Valuation (56 points)

EXAMINATION II: Fixed Income Analysis and Valuation Derivatives Analysis and Valuation Portfolio Management Questions Final Examination March 2010 Question 1: Fixed Income Analysis and Valuation (56 points)

Math 5621 Financial Math II Spring 2016 Final Exam Soluitons April 29 to May 2, 2016

Math 56 Financial Math II Spring 06 Final Exam Soluitons April 9 to May, 06 This is an open book take-home exam. You may consult any books, notes, websites or other printed material that you wish. Having

Math 56 Financial Math II Spring 06 Final Exam Soluitons April 9 to May, 06 This is an open book take-home exam. You may consult any books, notes, websites or other printed material that you wish. Having