COST OF CAPITAL

|

|

|

- Myles McBride

- 5 years ago

- Views:

Transcription

1 COST OF CAPITAL

2 Introduction Cost of Capital (CoC) are the cost of funds used for financing a business CoC depends on the mode of financing used In most cases a combination of debt and equity is used to finance businesses CoC represents a hurdle rate that must be overcome before generating value 2

3 Company Valuation 3

4 Cost of Capital WACC Simulation Cost of Debt Percent Financed w ith Debt 0% 10% 20% 30% 40% 50% 60% 70% Tax rate Credit Default Spread 0,50 0,60 0,70 0,80 1,50 3,00 4,50 8,00 Cost of Equity Before-tax Cost Debt 3,00% 3,10% 3,20% 3,30% 4,00% 5,50% 7,00% 10,50% 2,50% 7,00% 1,0 CoE (unlevered) 9,50% 35,00% Debt/Value Equity/Value Debt/Equity Post-Tax Ratio Ratio Ratio Cost of Debt 0% 100% 0,00 1,95% 10% 90% 0,11 2,02% 20% 80% 0,25 2,08% 30% 70% 0,43 2,15% 40% 60% 0,67 2,60% 50% 50% 1,00 3,58% 60% 40% 1,50 4,55% 70% 30% 2,33 6,83% Input Parameters Risk-free rate Market risk premium Unlevered beta Levered Beta 1,00 1,07 1,16 1,28 1,43 1,65 1,98 2,52 Cost of Equity 9,50% 10,01% 10,64% 11,45% 12,53% 14,05% 16,33% 20,12% WACC 9,50% 9,21% 8,93% 8,66% 8,56% 8,81% 9,26% 10,81% 4

5 Optimal Cost of Capital Structure Cost of Debt Cost of Equity Percent Credit Financed Default Before-tax w ith Debt Spread Cost Debt Input Parameters 0% 0,50 3,00% Risk-free rate 2,50% 10% 0,60 3,10% Market risk premium 7,00% 20% 0,70 3,20% Unlevered beta 1,0 30% 0,80 3,30% 40% 1,50 4,00% CoE (unlevered) 9,50% 50% 3,00 5,50% 60% 4,50 7,00% 70% 8,00 10,50% Tax rate 35,00% Debt/Value Equity/Value Debt/Equity Post-Tax Levered Cost of Ratio Ratio Ratio Cost of Debt Beta Equity WACC 0% 100% 0,00 1,95% 1,00 9,50% 9,50% 10% 90% 0,11 2,02% 1,07 10,01% 9,21% 20% 80% 0,25 2,08% 1,16 10,64% 8,93% 30% 70% 0,43 2,15% 1,28 11,45% 8,66% 40% 60% 0,67 2,60% 1,43 12,53% 8,56% 50% 50% 1,00 3,58% 1,65 14,05% 8,81% 60% 40% 1,50 4,55% 1,98 16,33% 9,26% 70% 30% 2,33 6,83% 2,52 20,12% 10,81% 5

6 Cost of Equity Cost of Debt Cost of Equity Percent Credit Financed Default Before-tax w ith Debt Spread Cost Debt Input Parameters 0% 0,50 3,00% Risk-free rate 2,50% 10% 0,60 3,10% Market risk premium 7,00% 20% 0,70 3,20% Unlevered beta 1,0 30% 0,80 3,30% 40% 1,50 4,00% CoE (unlevered) 9,50% 50% 3,00 5,50% 60% 4,50 7,00% 70% 8,00 10,50% Tax rate 35,00% Debt/Value Equity/Value Debt/Equity Post-Tax Levered Cost of Ratio Ratio Ratio Cost of Debt Beta Equity WACC 0% 100% 0,00 1,95% 1,00 9,50% 9,50% 10% 90% 0,11 2,02% 1,07 10,01% 9,21% 20% 80% 0,25 2,08% 1,16 10,64% 8,93% 30% 70% 0,43 2,15% 1,28 11,45% 8,66% 40% 60% 0,67 2,60% 1,43 12,53% 8,56% 50% 50% 1,00 3,58% 1,65 14,05% 8,81% 60% 40% 1,50 4,55% 1,98 16,33% 9,26% 70% 30% 2,33 6,83% 2,52 20,12% 10,81% Alternative: Multi-Factor Model 6

7 Cost of Equity - Beta Percent Credit Financed Default Before-tax w ith Debt Spread Cost Debt Input Parameters 0% 0,50 3,00% Risk-free rate 2,50% 10% 0,60 3,10% Market risk premium 7,00% 20% 0,70 3,20% Unlevered beta 1,0 30% 0,80 3,30% 40% 1,50 4,00% CoE (unlevered) 9,50% 50% 3,00 5,50% 60% 4,50 7,00% 70% 8,00 10,50% Tax rate Cost of Debt 35,00% Cost of Equity Debt/Value Equity/Value Debt/Equity Post-Tax Levered Cost of Ratio Ratio Ratio Cost of Debt Beta Equity WACC 0% 100% 0,00 1,95% 1,00 9,50% 9,50% 10% 90% 0,11 2,02% 1,07 10,01% 9,21% 20% 80% 0,25 2,08% 1,16 10,64% 8,93% 30% 70% 0,43 2,15% 1,28 11,45% 8,66% 40% 60% 0,67 2,60% 1,43 12,53% 8,56% 50% 50% 1,00 3,58% 1,65 14,05% 8,81% 60% 40% 1,50 4,55% 1,98 16,33% 9,26% 70% 30% 2,33 6,83% 2,52 20,12% 10,81% In the CAPM, the risk that a security contributes to a diversified portfolio is measured by its Beta and the expected excess return of the security (MRP) is proportional to Beta As higher leverage leads to higher volatility (vis-a-vis the market benchmark), Beta will have to be adjusted through unlevering and re-levering it 7

8 Cost of Equity Relevering Beta Changing a Firm s Capital Structure Debt Equity Tax Levered Beta 30,0% 70,0% 35,0% 1,40 20,0% 50,0% 70,0% 80,0% 50,0% 30,0% 35,0% 35,0% 35,0% 1,27 1,81 2,76 Unlevered Beta 1,09 8

9 Cost of Debt Yield-to-maturity approach Debt-rating approach Cost of Debt Cost of Equity Percent Credit Financed Default Before-tax w ith Debt Spread Cost Debt Input Parameters 0% 0,50 3,00% Risk-free rate 2,50% 10% 0,60 3,10% Market risk premium 7,00% 20% 0,70 3,20% Unlevered beta 1,0 30% 0,80 3,30% 40% 1,50 4,00% CoE (unlevered) 9,50% 50% 3,00 5,50% 60% 4,50 7,00% 70% 8,00 10,50% Tax rate 35,00% Interest on debt is tax deductible; therefore, the cost of debt must be adjusted to reflect this deductibility Debt/Value Equity/Value Debt/Equity Post-Tax Levered Cost of Ratio Ratio Ratio Cost of Debt Beta Equity WACC 0% 100% 0,00 1,95% 1,00 9,50% 9,50% 10% 90% 0,11 2,02% 1,07 10,01% 9,21% 20% 80% 0,25 2,08% 1,16 10,64% 8,93% 30% 70% 0,43 2,15% 1,28 11,45% 8,66% 40% 60% 0,67 2,60% 1,43 12,53% 8,56% 50% 50% 1,00 3,58% 1,65 14,05% 8,81% 60% 40% 1,50 4,55% 1,98 16,33% 9,26% 70% 30% 2,33 6,83% 2,52 20,12% 10,81% 9

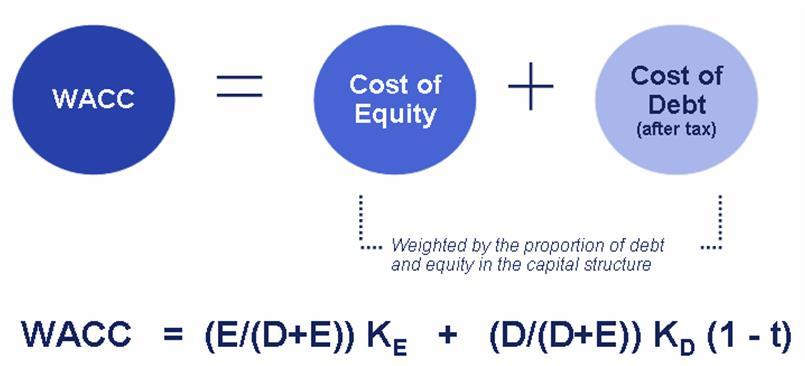

10 Weighting of WACC Components The weighting of Cost of Equity and Cost of Debt in the WACC is to reflect the company s long-term, stable target capital structure Cost of Equity and Cost of Debt are weighted according to their respective market values (and not book values) 10

11 Cost of Capital WACC Simulation Cost of Debt Percent Financed w ith Debt 0% 10% 20% 30% 40% 50% 60% 70% Tax rate Credit Default Spread 0,50 0,60 0,70 0,80 1,50 3,00 4,50 8,00 Cost of Equity Before-tax Cost Debt 3,00% 3,10% 3,20% 3,30% 4,00% 5,50% 7,00% 10,50% 2,50% 7,00% 1,0 CoE (unlevered) 9,50% 35,00% Debt/Value Equity/Value Debt/Equity Post-Tax Ratio Ratio Ratio Cost of Debt 0% 100% 0,00 1,95% 10% 90% 0,11 2,02% 20% 80% 0,25 2,08% 30% 70% 0,43 2,15% 40% 60% 0,67 2,60% 50% 50% 1,00 3,58% 60% 40% 1,50 4,55% 70% 30% 2,33 6,83% Input Parameters Risk-free rate Market risk premium Unlevered beta Levered Beta 1,00 1,07 1,16 1,28 1,43 1,65 1,98 2,52 Cost of Equity 9,50% 10,01% 10,64% 11,45% 12,53% 14,05% 16,33% 20,12% WACC 9,50% 9,21% 8,93% 8,66% 8,56% 8,81% 9,26% 10,81% 11

12 Appendix The Capital Asset Pricing Model 12

13 CAPM How to Measure Risk Financial theory tells us that, on average, higher returns are earned by financial assets that have higher risk. One model used for measuring risk is the Capital Asset Pricing Model (CAPM) In the CAPM, the risk that a security contributes to a diversified portfolio is measured by its beta (or ), and the expected excess return of the security is proportional to beta Excess Return refers to the additional return that the security earns above the riskfree rate The excess return earned by the market portfolio is also known as the market risk premium The risk premium for an individual security may be higher or lower than the market risk premium depending on the security s beta If the beta is greater than one (the beta of the market portfolio is one by definition), then the expected return for the security is higher than the market average, and, if the beta is less than one, the expected return is lower 13

14 CAPM How to Measure Risk (cont d) In the CAPM, the total expected return of a security is given by this equation: Only the excess return varies with beta, and the risk free rate is added to the security s risk premium to get the total expected return The expected return is the return that the investors expect to earn on average given the current price of the security The expected return is what should happen on average over the very long term, but in any given period the realized return may be very different than the expected return The expected return is related to price If the price rises (falls), and our expectations of the future cash flows from the security are unchanged, then our expected return falls (rises) since we are paying more for the same future future cash flows 14

15 CAPM The Beta Beta is a statistical measure which captures the relationship between the returns of a security and the returns of the overall market Beta is calculated as the covariance between the security s excess returns and the excess returns of the market portfolio divided by the market portfolio variance 15

16 CAPM The Beta The graph shows 5-years of monthly excess returns on AT&T stock and the monthly excess market returns The red line is the best fit line showing the relationship between the market s excess returns and AT&T s excess returns The slope of this line is the beta of AT&T The regression relationship between the AT&T return and the market return is far from perfect, but according to the CAPM these errors should average out in a diversified portfolio 16

17 CAPM The Beta (cont d) The graph shows 5-years of monthly excess returns of the Vanguard Balanced Index Fund and the monthly excess market returns Whilst this diverse portfolio of both stocks and bonds has a beta very similar to the one of AT&T scatter plot points in the second graph fall very close to the regression line The diversifiable risk has been eliminated and we are left only with a non-diversifiable exposure to overall market risk 17

18 CAPM Why are average returns expected to be proportional to beta? Assume the average return of a stock was not proportional to its beta If it were possible to find low-beta investment propositions with average returns equal to that of the market, then this would be very desirable portfolio for any risk averse investor Investors would buy these low risk investment propositions (driving up the price of low beta stocks) and avoid the high beta stocks which could increase the market risk of the portfolio (driving down the price of high beta stocks) This arbitrage process would drive down the returns of low beta stocks and drive up the returns of high beta stocks until an equilibrium was reached CAPM suggests that constant trading and instant incorporation of new information keeps markets in exactly this type of an equilibrium: Therefore lowbeta stocks should, on average, earn lower returns than high-beta stocks 18

19 CAPM The Alpha In the CAPM, alpha is a risk-adjusted measure of return It measures the extent to which a security s return exceeds or falls short of the return predicted by the CAPM A positive alpha indicates that, after adjusting for exposure to market risk, a security has outperformed the market portfolio. Alpha can be measured using the following regression: The CAPM suggests that a broadly diversifed portfolio should have an alpha that is close to zero 19

20 CAPM Diversification and Security Market Line 20

21 Contact Christian Schopper Private: Business: 21

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Estimating Beta. The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ): R j = a + b R m

against market returns (R m ): R j = a + b R m") Estimating Beta 122 The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ): R j = a + b R m where a is the intercept and b is the slope of the regression.

Estimating Beta 122 The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ): R j = a + b R m where a is the intercept and b is the slope of the regression.

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

Cost of Capital (represents risk)

") Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

WEIGHTED AVERAGE COST OF CAPITAL

WEIGHTED AVERAGE COST OF CAPITAL Ali Rıza DİNÇ Electricity Tariffs Group Head Energy Market Regulatory Authority Turkey Nature of WACC Weighted average cost of sources used by the regulated company Return

WEIGHTED AVERAGE COST OF CAPITAL Ali Rıza DİNÇ Electricity Tariffs Group Head Energy Market Regulatory Authority Turkey Nature of WACC Weighted average cost of sources used by the regulated company Return

FINANCE 402 Capital Budgeting and Corporate Objectives. Syllabus

FINANCE 402 Capital Budgeting and Corporate Objectives Course Description: Syllabus The objective of this course is to provide a rigorous introduction to the fundamental principles of asset valuation and

FINANCE 402 Capital Budgeting and Corporate Objectives Course Description: Syllabus The objective of this course is to provide a rigorous introduction to the fundamental principles of asset valuation and

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

Corporate Finance - Final Exam QUESTIONS 78 terms by trunganhhung

Corporate Finance - Final Exam QUESTIONS 78 terms by trunganhhung Like this study set? Create a free account to save it. Create a free account Which one of the following best defines the variance of an

Corporate Finance - Final Exam QUESTIONS 78 terms by trunganhhung Like this study set? Create a free account to save it. Create a free account Which one of the following best defines the variance of an

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

2013, Study Session #11, Reading # 37 COST OF CAPITAL 1. INTRODUCTION

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

CHAPTER 14. Capital Structure in a Perfect Market. Chapter Synopsis

CHAPTR 14 Capital Structure in a Perfect Market Chapter Synopsis 14.1 quity Versus Debt Financing A firm s capital structure refers to the debt, equity, and other securities used to finance its fixed assets.

CHAPTR 14 Capital Structure in a Perfect Market Chapter Synopsis 14.1 quity Versus Debt Financing A firm s capital structure refers to the debt, equity, and other securities used to finance its fixed assets.

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Financial Leverage and Capital Structure Policy

Key Concepts and Skills Chapter 17 Understand the effect of financial leverage on cash flows and the cost of equity Understand the Modigliani and Miller Theory of Capital Structure with/without Taxes Understand

Key Concepts and Skills Chapter 17 Understand the effect of financial leverage on cash flows and the cost of equity Understand the Modigliani and Miller Theory of Capital Structure with/without Taxes Understand

Chapter 14: Capital Structure in a Perfect Market

Chapter 14: Capital Structure in a Perfect Market-1 Chapter 14: Capital Structure in a Perfect Market I. Overview 1. Capital structure: Note: usually use leverage ratios like debt/assets to measure the

Chapter 14: Capital Structure in a Perfect Market-1 Chapter 14: Capital Structure in a Perfect Market I. Overview 1. Capital structure: Note: usually use leverage ratios like debt/assets to measure the

The CAPM. (Welch, Chapter 10) Ivo Welch. UCLA Anderson School, Corporate Finance, Winter December 16, 2016

Ivo Welch. UCLA Anderson School, Corporate Finance, Winter December 16, 2016") 1/1 The CAPM (Welch, Chapter 10) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2017 December 16, 2016 Did you bring your calculator? Did you read these notes and the chapter ahead of time?

1/1 The CAPM (Welch, Chapter 10) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2017 December 16, 2016 Did you bring your calculator? Did you read these notes and the chapter ahead of time?

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

79 Discount Rates: III Relative Risk Measures 80 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

79 Discount Rates: III Relative Risk Measures 80 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

Chapter 14: Capital Structure in a Perfect Market

Chapter 14: Capital Structure in a Perfect Market-1 Chapter 14: Capital Structure in a Perfect Market I. Overview 1. Capital structure: mix of debt and equity issued by the firm to fund its assets Note:

Chapter 14: Capital Structure in a Perfect Market-1 Chapter 14: Capital Structure in a Perfect Market I. Overview 1. Capital structure: mix of debt and equity issued by the firm to fund its assets Note:

Homework Solutions - Lecture 2 Part 2

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Final Exam Finance for AEO (Resit)

") Final Exam Finance for AEO (Resit) Course: Finance for AEO SubjectCode: 226P05 Date: 8 juli 2008 Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations

Final Exam Finance for AEO (Resit) Course: Finance for AEO SubjectCode: 226P05 Date: 8 juli 2008 Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Corporate Finance.

Finance 100 Spring 2008 Dana Kiku kiku@wharton.upenn.edu 2335 SH-DH Corporate Finance The objective of this course is to provide a rigorous introduction to the fundamental principles of asset valuation,

Finance 100 Spring 2008 Dana Kiku kiku@wharton.upenn.edu 2335 SH-DH Corporate Finance The objective of this course is to provide a rigorous introduction to the fundamental principles of asset valuation,

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

AFM 371 Winter 2008 Chapter 16 - Capital Structure: Basic Concepts

AFM 371 Winter 2008 Chapter 16 - Capital Structure: Basic Concepts 1 / 24 Outline Background Capital Structure in Perfect Capital Markets Examples Leverage and Shareholder Returns Corporate Taxes 2 / 24

AFM 371 Winter 2008 Chapter 16 - Capital Structure: Basic Concepts 1 / 24 Outline Background Capital Structure in Perfect Capital Markets Examples Leverage and Shareholder Returns Corporate Taxes 2 / 24

The Spiffy Guide to Finance

The Spiffy Guide to Finance Warning: This is neither complete nor comprehensive. I fully expect you to read the textbook and go through your notes and past homeworks. Wai-Hoong Fock - Page 1 - Chapter

The Spiffy Guide to Finance Warning: This is neither complete nor comprehensive. I fully expect you to read the textbook and go through your notes and past homeworks. Wai-Hoong Fock - Page 1 - Chapter

MBA 203 Executive Summary

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 011 Wednesday, November 16, 011 INSTRUCTIONS: 1. You have 110 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 011 Wednesday, November 16, 011 INSTRUCTIONS: 1. You have 110 minutes to complete

Do you live in a mean-variance world?

Do you live in a mean-variance world? 76 Assume that you had to pick between two investments. They have the same expected return of 15% and the same standard deviation of 25%; however, investment A offers

Do you live in a mean-variance world? 76 Assume that you had to pick between two investments. They have the same expected return of 15% and the same standard deviation of 25%; however, investment A offers

CHAPTER 8 ESTIMATING RISK PARAMETERS AND COSTS OF FINANCING

Solutions to Investment Valuation 25 CHAPTER 8 ESTIMATING RISK PARAMETERS AND COSTS OF FINANCING Problem 1 We use the CAPM: The Expected Return on the stock = 0.058 + 0.95(0.0876) = 0.1412 = 14.12%. Since

Solutions to Investment Valuation 25 CHAPTER 8 ESTIMATING RISK PARAMETERS AND COSTS OF FINANCING Problem 1 We use the CAPM: The Expected Return on the stock = 0.058 + 0.95(0.0876) = 0.1412 = 14.12%. Since

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Decomposition (16-3)

") Decomposition (16-3) Decompose shareholders required return on equity into its economic and financial risk premium components. Solution Shareholders required return on equity is the sum of tree components

Decomposition (16-3) Decompose shareholders required return on equity into its economic and financial risk premium components. Solution Shareholders required return on equity is the sum of tree components

Finance 402: Problem Set 6 Solutions

Finance 402: Problem Set 6 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. The CAPM E(r i )

Finance 402: Problem Set 6 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. The CAPM E(r i )

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Define risk, risk aversion, and riskreturn

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010

Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010") Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010 Course Description The purpose of this course is to introduce techniques of financial

Corporate Finance (Honors) Finance 100 Sections 301 and 302 The Wharton School, University of Pennsylvania Fall 2010 Course Description The purpose of this course is to introduce techniques of financial

University of Pennsylvania The Wharton School

University of Pennsylvania The Wharton School FNCE 100 PROBLEM SET #6 Fall Term 2003 A. Craig MacKinlay Capital Structure 1. The XYZ Co. is assessing its current capital structure and its implications

University of Pennsylvania The Wharton School FNCE 100 PROBLEM SET #6 Fall Term 2003 A. Craig MacKinlay Capital Structure 1. The XYZ Co. is assessing its current capital structure and its implications

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

2013/2014. Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities.

Question One: Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities. 2. Diversification will normally reduce the riskiness

Question One: Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities. 2. Diversification will normally reduce the riskiness

Chapter 4: Risk Measurement and Hurdle Rates in Practice. 1. e. If you are doing the analysis in nominal pesos, you would use this rate.

Chapter 4: Risk Measurement and Hurdle Rates in Practice 1. e. If you are doing the analysis in nominal pesos, you would use this rate. 2. A. b. Ceteris paribus, I would expect the publicly traded company

Chapter 4: Risk Measurement and Hurdle Rates in Practice 1. e. If you are doing the analysis in nominal pesos, you would use this rate. 2. A. b. Ceteris paribus, I would expect the publicly traded company

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

Page 515 Summary and Conclusions

Page 515 Summary and Conclusions 1. We began our discussion of the capital structure decision by arguing that the particular capital structure that maximizes the value of the firm is also the one that

Page 515 Summary and Conclusions 1. We began our discussion of the capital structure decision by arguing that the particular capital structure that maximizes the value of the firm is also the one that

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015 Reading Chapters 11 13, not Appendices Chapter 11 Skip 11.2 Mean variance optimization in practice

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015 Reading Chapters 11 13, not Appendices Chapter 11 Skip 11.2 Mean variance optimization in practice

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

CHAPTER 8: INDEX MODELS

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

CHAPTER 27: THE THEORY OF ACTIVE PORTFOLIO MANAGEMENT

CAPTER 7: TE TEORY OF ACTIVE PORTFOLIO ANAGEENT 1. a. Define R r r f Note that e compute the estimates of standard deviation using 4 degrees of freedom (i.e., e divide the sum of the squared deviations

CAPTER 7: TE TEORY OF ACTIVE PORTFOLIO ANAGEENT 1. a. Define R r r f Note that e compute the estimates of standard deviation using 4 degrees of freedom (i.e., e divide the sum of the squared deviations

Chapter 8: Prospective Analysis: Valuation Implementation

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Using Microsoft Corporation to Demonstrate the Optimal Capital Structure Trade-off Theory

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 9 Number 2 Winter 2010 29 Using Microsoft Corporation to Demonstrate the Optimal Capital Structure Trade-off Theory John C. Gardner, Carl B. McGowan Jr.,

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 9 Number 2 Winter 2010 29 Using Microsoft Corporation to Demonstrate the Optimal Capital Structure Trade-off Theory John C. Gardner, Carl B. McGowan Jr.,

Chapter 12: Estimating the Cost of Capital

Chapter 12: Estimating the Cost of Capital -1 Chapter 12: Estimating the Cost of Capital Fundamental question: Where do we get the numbers to estimate the cost of capital? => How do we implement the CAPM

Chapter 12: Estimating the Cost of Capital -1 Chapter 12: Estimating the Cost of Capital Fundamental question: Where do we get the numbers to estimate the cost of capital? => How do we implement the CAPM

Basic Finance Exam #2

Basic Finance Exam #2 Chapter 10: Capital Budget list of planned investment project Sensitivity Analysis analysis of the effects on project profitability of changes in sales, costs and so on Fixed Cost

Basic Finance Exam #2 Chapter 10: Capital Budget list of planned investment project Sensitivity Analysis analysis of the effects on project profitability of changes in sales, costs and so on Fixed Cost

Leverage. Capital Budgeting and Corporate Objectives

Leverage Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Overview Capital Structure does not matter!» Modigliani & Miller propositions

Leverage Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Overview Capital Structure does not matter!» Modigliani & Miller propositions

CORPORATE FINANCE: THE CORE

CORPORATE FINANCE: THE CORE JONATHAN' BERK UNIVERSITY OF CALIFORNIA, BERKHI.EY PETER DEMARZO STANFORD UNIVE RSITY Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City

CORPORATE FINANCE: THE CORE JONATHAN' BERK UNIVERSITY OF CALIFORNIA, BERKHI.EY PETER DEMARZO STANFORD UNIVE RSITY Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Capital Asset Pricing Model

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

From optimisation to asset pricing

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS

CHAPTER 15 B- 1 CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals

CHAPTER 15 B- 1 CHAPTER 15 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

FCF t. V = t=1. Topics in Chapter. Chapter 16. How can capital structure affect value? Basic Definitions. (1 + WACC) t

t") Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2006 Monday, November 13, 2006 INSTRUCTIONS: 1. You have 75 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2006 Monday, November 13, 2006 INSTRUCTIONS: 1. You have 75 minutes to complete

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

FNCE 5205, Global Financial Management H Guy Williams, 2008

CHAPTER 7. ENTERPRISE COST OF CAPITAL The cost of capital is a concept that is central to valuation, investment (and divestment) decisions, measures of economic profit, and performance appraisal. Perhaps

CHAPTER 7. ENTERPRISE COST OF CAPITAL The cost of capital is a concept that is central to valuation, investment (and divestment) decisions, measures of economic profit, and performance appraisal. Perhaps

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

- P P THE RELATION BETWEEN RISK AND RETURN. Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

PRINCIPLES of INVESTMENTS

PRINCIPLES of INVESTMENTS Boston University MICHAItL L D\if.\N Griffith University AN UP BASU Queensland University of Technology ALEX KANT; University of California, San Diego ALAN J. AAARCU5 Boston College

PRINCIPLES of INVESTMENTS Boston University MICHAItL L D\if.\N Griffith University AN UP BASU Queensland University of Technology ALEX KANT; University of California, San Diego ALAN J. AAARCU5 Boston College

80 Solved MCQs of MGT201 Financial Management By

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FIN622 Formulas

The quick ratio is defined as follows: Quick Ratio = (Current Assets Inventory)/ Current Liabilities Receivables Turnover = Annual Credit Sales / Accounts Receivable The collection period also can be written

The quick ratio is defined as follows: Quick Ratio = (Current Assets Inventory)/ Current Liabilities Receivables Turnover = Annual Credit Sales / Accounts Receivable The collection period also can be written

ARCH Models and Financial Applications

Christian Gourieroux ARCH Models and Financial Applications With 26 Figures Springer Contents 1 Introduction 1 1.1 The Development of ARCH Models 1 1.2 Book Content 4 2 Linear and Nonlinear Processes 5

Christian Gourieroux ARCH Models and Financial Applications With 26 Figures Springer Contents 1 Introduction 1 1.1 The Development of ARCH Models 1 1.2 Book Content 4 2 Linear and Nonlinear Processes 5

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

COST OF CAPITAL: REVISITING BASICS & GETTING PERSPECTIVE. Aswath Damodaran

COST OF CAPITAL: REVISITING BASICS & GETTING PERSPECTIVE Aswath Damodaran Cost of Capital: A Financial Balance Sheet Perspective 2 The Swiss Army Knife 3 Every Risk has a place 4 1. Business Risk If you

COST OF CAPITAL: REVISITING BASICS & GETTING PERSPECTIVE Aswath Damodaran Cost of Capital: A Financial Balance Sheet Perspective 2 The Swiss Army Knife 3 Every Risk has a place 4 1. Business Risk If you

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

CHAPTER II LITERATURE REVIEW

CHAPTER II LITERATURE REVIEW II.1. Risk II.1.1. Risk Definition According Brigham and Houston (2004, p170), Risk is refers to the chance that some unfavorable event will occur (a hazard, a peril, exposure

CHAPTER II LITERATURE REVIEW II.1. Risk II.1.1. Risk Definition According Brigham and Houston (2004, p170), Risk is refers to the chance that some unfavorable event will occur (a hazard, a peril, exposure

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

MATH 4512 Fundamentals of Mathematical Finance

MATH 451 Fundamentals of Mathematical Finance Solution to Homework Three Course Instructor: Prof. Y.K. Kwok 1. The market portfolio consists of n uncorrelated assets with weight vector (x 1 x n T. Since

MATH 451 Fundamentals of Mathematical Finance Solution to Homework Three Course Instructor: Prof. Y.K. Kwok 1. The market portfolio consists of n uncorrelated assets with weight vector (x 1 x n T. Since

Financial Strategy First Test

Financial Strategy First Test 1. The difference between the market value of an investment and its cost is the: A) Net present value. B) Internal rate of return. C) Payback period. D) Profitability index.

Financial Strategy First Test 1. The difference between the market value of an investment and its cost is the: A) Net present value. B) Internal rate of return. C) Payback period. D) Profitability index.

HURDLE RATES V: BETAS THE REGRESSION APPROACH. A regression beta is just a staasacal number

HURDLE RATES V: BETAS THE REGRESSION APPROACH A regression beta is just a staasacal number Set Up and Objective 1: What is corporate finance 2: The Objective: Utopia and Let Down 3: The Objective: Reality

HURDLE RATES V: BETAS THE REGRESSION APPROACH A regression beta is just a staasacal number Set Up and Objective 1: What is corporate finance 2: The Objective: Utopia and Let Down 3: The Objective: Reality

IRG Regulatory Accounting. Principles of Implementation and Best Practice for WACC calculation. February 2007

IRG Regulatory Accounting Principles of Implementation and Best Practice for WACC calculation February 2007 Index 1. EXECUTIVE SUMMARY... 3 2. INTRODUCTION... 6 3. THE WEIGHTED AVERAGE COST OF CAPITAL...

IRG Regulatory Accounting Principles of Implementation and Best Practice for WACC calculation February 2007 Index 1. EXECUTIVE SUMMARY... 3 2. INTRODUCTION... 6 3. THE WEIGHTED AVERAGE COST OF CAPITAL...

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Chapter 15. Topics in Chapter. Capital Structure Decisions

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries