Chapter 8. Rate of Return Analysis. Principles of Engineering Economic Analysis, 5th edition

|

|

|

- Daniella Lester

- 6 years ago

- Views:

Transcription

1 Chapter 8 Rate of Return Analysis

2 Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5. Compare the alternatives 6. Perform supplementary analyses 7. Select the preferred investment

3 Internal Rate of Return Analysis Single Alternative

4 Internal Rate of Return determines the interest rate (i * ) that yields a future worth equal to zero over the planning horizon 1 the rate of interest earned on the unrecovered balance of the investment a very popular DCF method n 0 A t (1 i * ) n t t 0 1 can also determine the interest rate that equates the present worth or annual worth to zero

5 Internal Rate of Return Determining the value of i * that satisfies the n-degree polynomial given below can be very challenging, since there can exist n distinct roots for an n-degree polynomial. Descartes rule of signs indicates an n-degree polynomial will have a single positive real root if there is a single sign change in the sequence of cash flows, A 1, A 2,, A n-1, A n ; if there are 2 sign changes, there will be either 2 or 0 positive real roots; if there are 3 sign changes, there will be either 3 or 1 positive real roots; if there are 4 sign changes, there will be 4, 2, or 0 positive real roots; To determine if exactly one real and positive-valued root exists, use Norstrom s criterion if the cumulative cash flow begins with a negative value and changes only once to a positive-valued series, then there exists a unique positive real root. t 0 A t (1 i 0 n * ) n t

6 Example 8.1 SMP Investment Internal Rate of Return Analysis EOY CF 0 -$500, $92, $50,000 FW(i * %) = -$500,000(F P i * %,10) + $50,000 + $92,500(F A i * %,10) = $0

7 Example 8.1 SMP Investment Internal Rate of Return Analysis EOY CF 0 -$500,000 i FW 1-10 $92,500 12% $120, $50,000 15% -$94, FW(i*%) = -$500,000(F P i*%,10) + $50,000 + $92,500(F A i*%,10) = $0 i* %

8 Example 8.1 Excel Solution A B 1 EOY CF 2 0 -$500, $92, $92, $92, $92, $92, $92, $92, $92, $92, $142, IRR = [=IRR(B2:B12)] IRR = %

9 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% SMP Investment Present Worth $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0 -$100,000 -$200,000 MARR

10 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% SMP Investment Future Worth $1,000,000 $500,000 $0 -$500,000 -$1,000,000 -$1,500,000 -$2,000,000 MARR

11 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% SMP Investment Annual Worth $60,000 $40,000 $20,000 $0 -$20,000 -$40,000 -$60,000 MARR

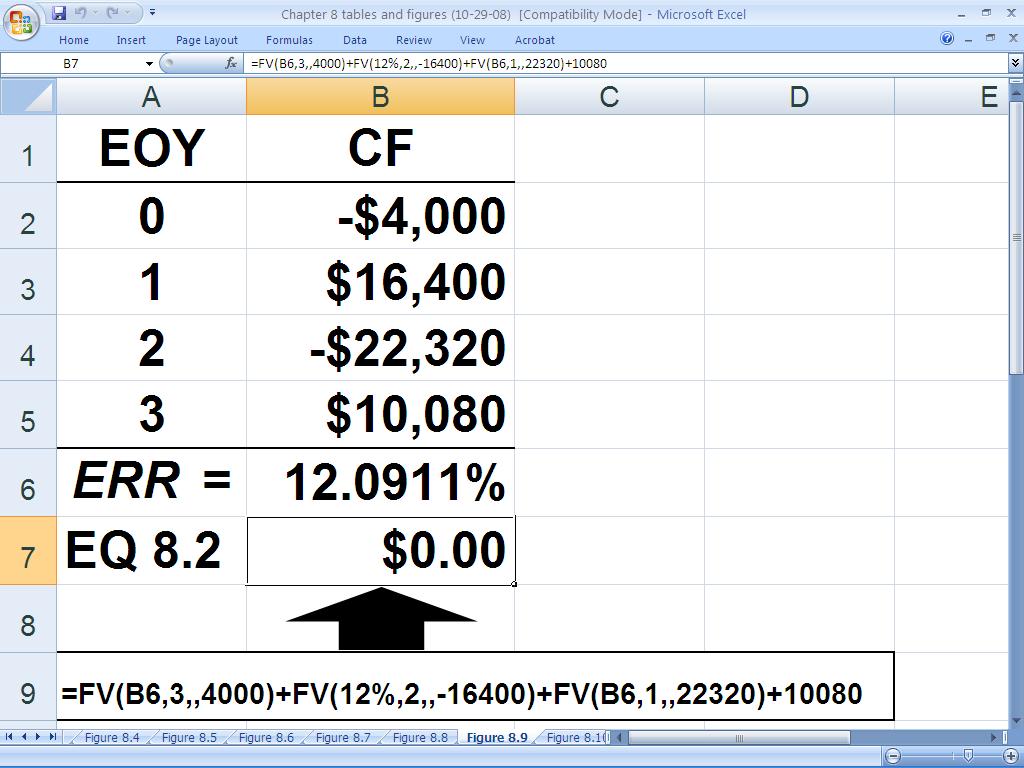

12 Example 8.2 Consider the cash flow profile given below. The FW equals zero using a 20%, 40%, or 50% interest rate. EOY CF 0 -$4,000 1 $16, $22,320 3 $10,080 FW 1 (20%) = -$4000(1.2) 3 + $16,400(1.2) 2 -$22,320(1.2) + $10,080 = 0 FW 2 (40%) = -$4000(1.4) 3 + $16,400(1.4) 2 -$22,320(1.4) + $10,080 = 0 FW 3 (50%) = -$4000(1.5) 3 + $16,400(1.5) 2 -$22,320(1.5) + $10,080 = 0

13 Future Worth $120 $80 $40 $0 10% 20% 30% 40% 50% 60% -$40 MARR

14 IRR Value Obtained from Excel's IRR Worksheet Function 60% 50% 40% 30% 20% 10% 0% 28% 29% 45% 0% 20% 40% 60% 80% 100% =IRR(values,guess) Guess

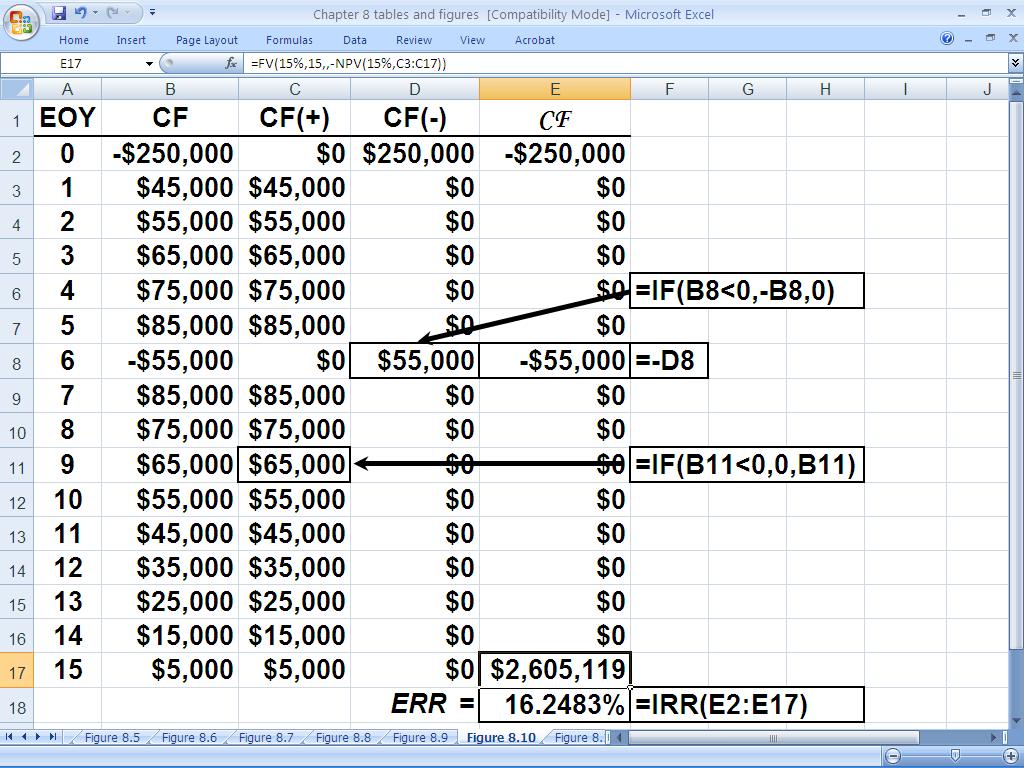

15 Example 8.3 Julian Stewart invested $250,000 in a limited partnership to drill for natural gas. The investment yielded annual returns of $45,000 the 1 st yr, followed by $10,000 increases until the 6 th yr, at which time an additional $150,000 had to be invested for deeper drilling. Following the 2 nd drilling, the annual returns decreased by $10,000 per year, from $85,000 to $5,000. Using Excel, the IRR = 19.12%. Plot future worth as a function of MARR and determine the MARR that maximizes FW.

16

17

18

19

20

21 Notice, the cumulative cash flow series changes from negative to positive and remains positive. Therefore, a unique positive real root exists. (Interestingly, if the interim investment is $200,000, Norstrom s criterion is not met, but a unique positive real root exists. Recall, Norstrom s criterion is a sufficient condition, not a necessary condition.)

22 Internal Rate of Return Analysis Multiple Alternatives

23 Example 8.4 You have available $70,000 to invest and have been presented with 5 equal-lived, mutually exclusive investment alternatives with cash flows as depicted below. Currently, you are earning 18% on your investment of the $70,000. Hence, you will not choose to invest in either of the alternatives if it does not provide a return on investment greater than 18%. Using the internal rate of return method, which (if either) would you choose? What is its rate of return?

24 Data for Example 8.4 Investment Initial Investment $15, $25, $40, $50, $70, Annual Return $3, $5, $9, $11, $14, Salvage Value $15, $25, $40, $50, $70, Internal Rate of Return 25.00% 20.00% 23.13% 22.50% 20.36% With an 18% MARR, which investment would you choose?

25 When the salvage value equals the initial investment and annual returns are a uniform annual series, the internal rate of return equals the quotient of the annual return and the initial investment Box 8.2

26 Solution to Example 8.4 Investment Δ Investment Δ Annual Return Δ Salvage Value Δ IRR 25.00% 12.50% 22.00% 20.00% 15.00% > MARR? Yes No Yes Yes No Defender $ 1 5, $ 1 0, $ 2 5, $ 1 0, $ 2 0, $ 3, $ 1, $ 5, $ 2, $ 3, $ 1 5, $ 1 0, $ 2 5, $ 1 0, $ 2 0,

27 Portfolio Solution to Example 8.4 Do Nothing $70,000(0.18) = $12,600/year Invest in 1 $3,750 + $55,000(0.18) = $13,650 Prefer 1 to Do Nothing Invest in 2 $5,000 + $45,000(0.18) = $13,100 Prefer 1 to 2

28 Portfolio Solution to Example 8.4 Invest in 3 $9,250 + $30,000(0.18) = $14,650 Prefer 3 to 1 Invest in 4 $11,250 + $20,000(0.18) = $14,850 Prefer 4 to 3 Invest in 5 $14,250 Prefer 4 to 5 Choose 4

29 Present Worths with 10-Year Planning Horizon Investment Initial Investment $15, $25, $40, $50, $70, Annual Return $3, $5, $9, $11, $14, Salvage Value $15, $25, $40, $50, $70, Present Worth $4, $2, $9, $10, $7,415.24

30 Present Worths with 10-Year Planning Horizon Investment Initial Investment $15, $25, $40, $50, $70, Annual Return $3, $5, $9, $11, $14, Salvage Value $15, $25, $40, $50, $70, Present Worth $4, $2, $9, $10, $7, PW = $11,250(P A 18%,10) + $50,000(P F 18%,10) - $50,000 =PV(18%,10,-11250,-50000)-50000

31 Principle #6 Continue to invest as long as each additional increment of investment yields a return that is greater than the investor s TVOM Box 8.3

32 The object of management is not necessarily the highest rate of return on capital, but to assure profit with each increment of volume that will at least equal the economic cost of additional capital required. Donald Brown Chief Financial Officer General Motors 1924

33 Example 8.5 Recall the theme park example involving two designs for the new ride, The Scream Machine: A costs $300,000, has $55,000/yr revenue, and has a negligible salvage value at the end of the 10-year planning horizon; B costs $450,000, has $80,000/yr revenue, and has a negligible salvage value. Based on an IRR analysis and a 10% MARR, which is preferred? PW A (12%) = -$300,000 + $55,000(P A 12%,10) = $10, PW A (15%) = -$300,000 + $55,000(P A 15%,10) = -$23, interpolating, IRR A = 12% + 3%($10,762.10)/($10, $23,967.65) = 12.93% IRR A =RATE(10,-55000,300000) IRR A = 12.87% > MARR = 10% (Alt. A is acceptable) PW B-A (12%) = -$150,000 + $25,000(P A 12%,10) = -$ PW B-A (10%) = -$150,000 + $25,000(P A 10%,10) = $37, interpolating, IRR B-A = 10% + 2%($ )/($ $37,951.35) = % IRR B-A =RATE(10,-25000,150000) = 10.56% > MARR = 10% (Alt. B is preferred) IRR B =RATE(10,-80000,450000) = 12.11%

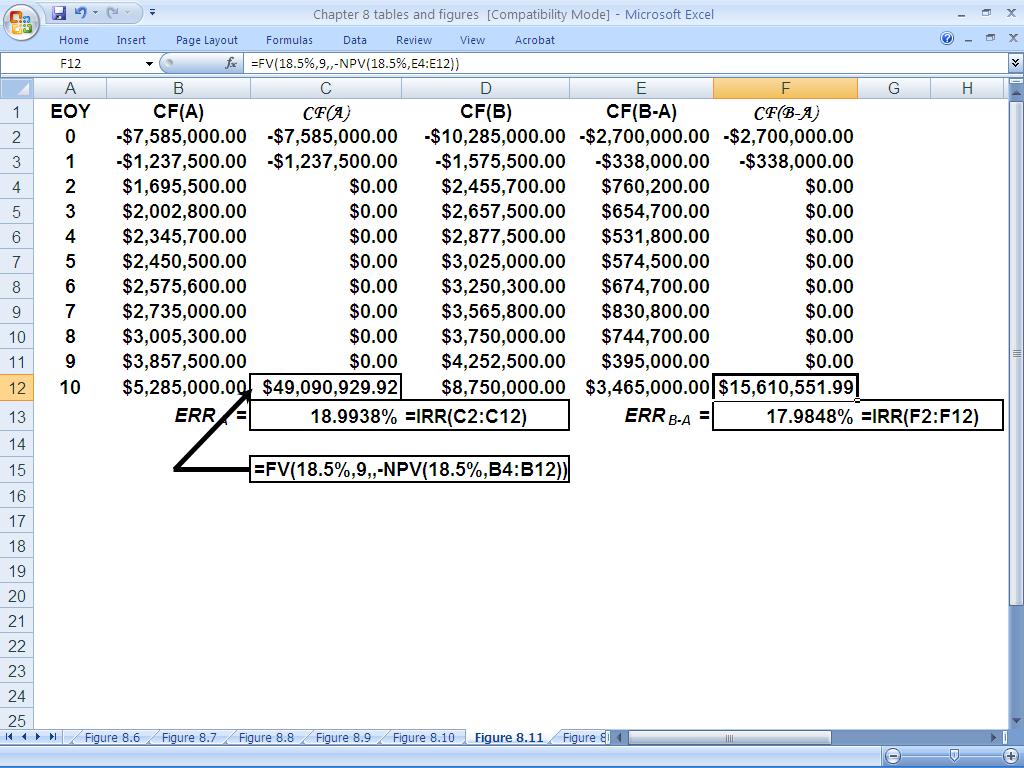

34 Example 8.6 A batch chemical processing company is adding centrifuges. Two alternatives are in consideration. The estimated cash flow profiles are shown below. Using a MARR of 18.5%, which should be chosen? EOY CF(A) CF(B) 0 -$7,585, $10,285, $1,237, $1,575, $1,695, $2,455, $2,002, $2,657, $2,345, $2,877, $2,450, $3,025, $2,575, $3,250, $2,735, $3,565, $3,005, $3,750, $3,857, $4,252, $5,285, $8,750,000.00

35 Recommend Alternative A

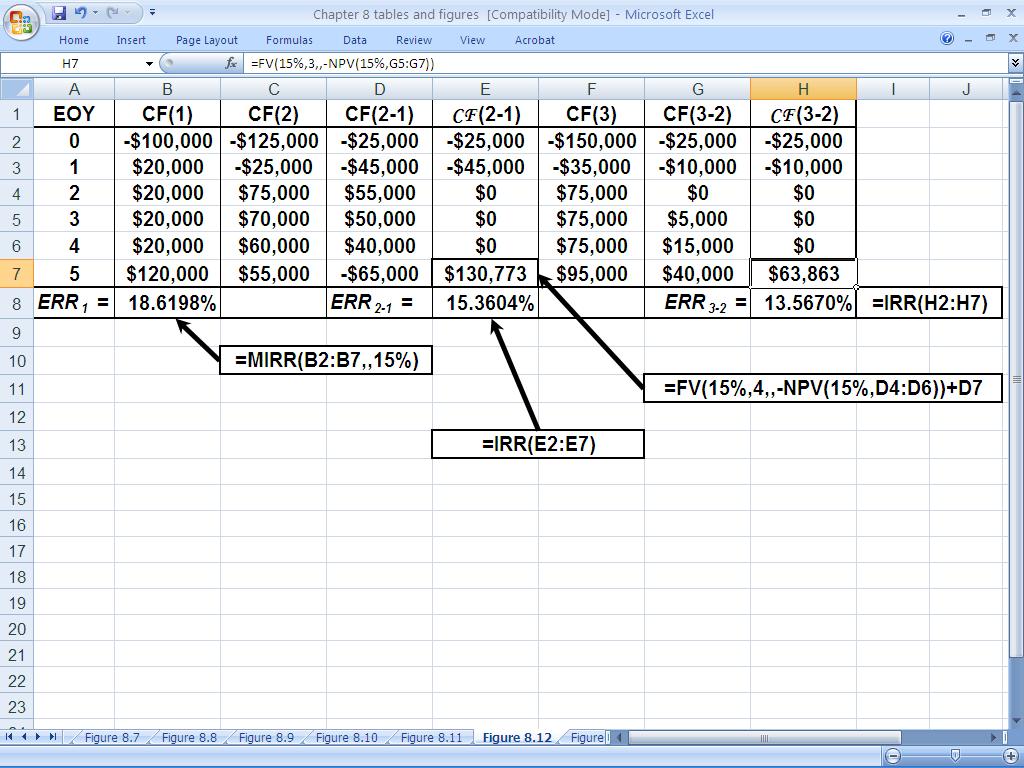

36 Example 8.7 Three mutually exclusive investment alternatives are being considered; the cash flow profiles are shown below. Based on a 15% MARR, which should be chosen? EOY CF(1) CF(2) CF(3) 0 -$100,000 -$125,000 -$150,000 1 $20,000 -$25,000 -$35,000 2 $20,000 $75,000 $75,000 3 $20,000 $70,000 $75,000 4 $20,000 $60,000 $75,000 5 $120,000 $55,000 $95,000

37 Example 8.7 (Continued) EOY CF(1) CF(2) CF(3) CF(2-1) CF(3-2) 0 -$100,000 -$125,000 -$150,000 -$25,000 -$25,000 1 $20,000 -$25,000 -$35,000 -$45,000 -$10,000 2 $20,000 $75,000 $75,000 $55,000 $0 3 $20,000 $70,000 $75,000 $50,000 $5,000 4 $20,000 $60,000 $75,000 $40,000 $15,000 5 $120,000 $55,000 $95,000 -$65,000 $40,000 IRR = 20.00% 19.39% 18.01% 16.41% 13.41% Recommend Alternative 2 PW 1 (15%) =PV(0.15,5,-20000, ) = $16, PW 2 (15%) =NPV(0.15,-25,75,70,60,55)* = $17, PW 3 (15%) =NPV(0.15,-35,75,75,75,95)* = $15,702.99

38 PW (x $10,000) -70% -60% -50% -40% -30% -20% -10% 0% 10% 20% Incremental IRR Comparison of Alternatives $2,000 $1,500 $1,000 MARR $500 $0 -$500 -$1,000 -$1,500 -$2,000 CF(2-1) CF(3-2)

39 -10% -5% 0% 5% 10% 15% 20% 25% PW (x $10,000) Incremental IRR Comparison of Alternatives $8 $7 $6 $5 $4 $3 $2 $1 $0 -$1 -$2 MARR CF(2-1) CF(3-2)

40 External Rate of Return Analysis Single Alternative

41 External Rate of Return Method equates the future worth of positive cash flows using the MARR to the future worth of negative cash flows using the ERR, i not a popular DCF method n n R t (1 r ) n t C t (1 i ' ) n t t 0 t 0 R t is positive-valued cash flow and C t is the absolute value of a negative-valued cash flow; r is the MARR (useful way to avoid the multiple root problem of the IRR)

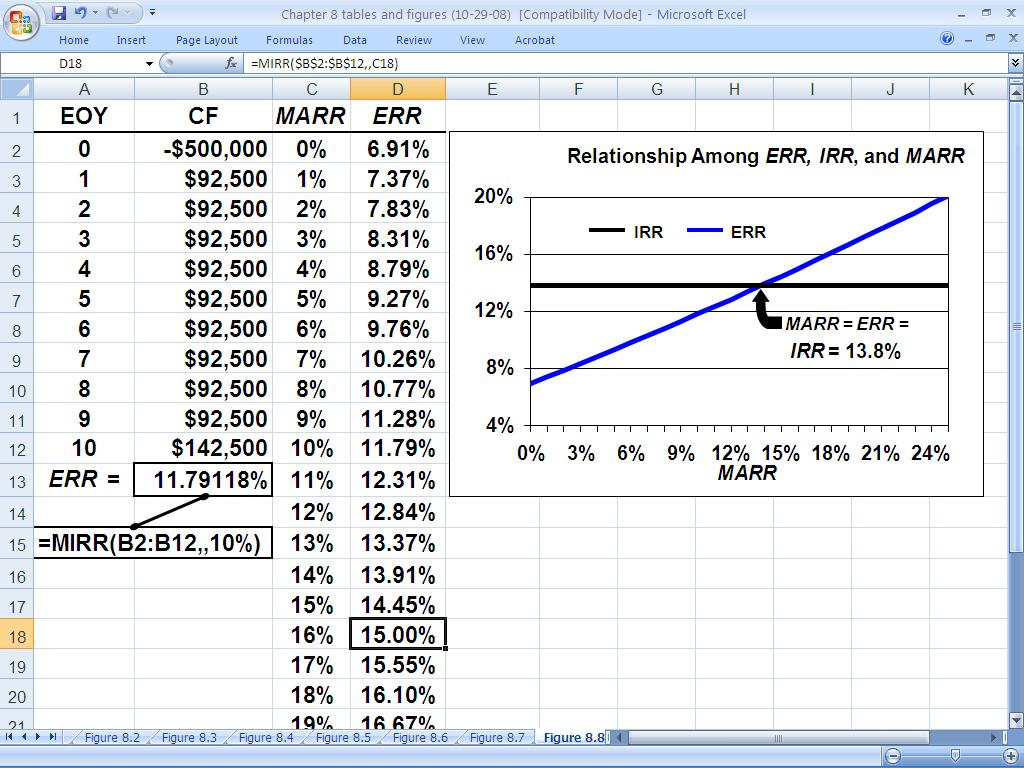

42 Relationships among MARR, IRR, and ERR If IRR < MARR, then IRR < ERR < MARR If IRR > MARR, then IRR > ERR > MARR If IRR = MARR, then IRR = ERR = MARR

43 Example 8.8 SMP Investment External Rate of Return Solution EOY CF 0 -$500, $92, $50,000 $500,000(F P i'%, 10) = $92,500(F A 10%,10) + $50,000

44 Example 8.8 SMP Investment External Rate of Return Solution EOY CF 0 -$500, $92, $50,000 $500,000(F P i'%,10)= $92,500(F A 10%,10) + $50,000 (F P i'%,10) = i' = % i' = % (using Excel)

45 Example 8.8 Excel Solution A B 1 EOY CF 2 0 -$500, $92, $92, $92, $92, $92, $92, $92, $92, $92, $142, ERR = [=MIRR(B2:B12,,10%)] 14 ERR = %

46

47 Example 8.9 Recall the cash flow profile, given below, that produced 3 IRR values: 20%, 40%, or 50%. If MARR = 12%, what is the ERR? For various values of MARR, what are the corresponding values of ERR? EOY CF 0 -$4,000 1 $16, $22,320 3 $10,080 $4000(F P i,3) + $22,320(F P i,1) = $16,400(F P MARR,2) + $10,080

48

49

50

51 ERR Values for Various MARR Values in Example 8.9 MARR ERR MARR ERR 0% % 30% % 2% % 32% % 4% % 34% % 6% % 36% % 8% % 38% % 10% % 40% % 12% % 42% % 14% % 44% % 16% % 46% % 18% % 48% % 20% % 50% % 22% % 52% % 24% % 54% % 26% % 56% % 28% % 58% %

52 Example 8.10 Recall Julian Stewart s $250,000 investment in a limited partnership to drill for natural gas. The investment yielded annual returns of $45,000 the 1 st yr, followed by $10,000 increases until the 6 th yr, at which time an additional $150,000 had to be invested for deeper drilling. Following the 2 nd drilling, the annual returns decreased by $10,000 per year, from $85,000 to $5,000. Since there were multiple negative values in the cash flow profile for the investment (EOY = 0 and EOY = 6), Excel s MIRR worksheet function cannot be used to solve for ERR. When faced with multiple negative-valued cash flows, we construct a new CF profile that contains the negativevalued cash flows, zeroes, and the future worth of the positive-valued cash flows, with the FW based on the MARR.

53

54 External Rate of Return Analysis Multiple Alternatives

55 Example 8.11 Recall the 5 equal-lived, mutually exclusive investment alternatives which guaranteed your original investment back at any time you wished to end the investment. With $70,000 to invest and an 18% MARR, you chose investment 4 using an IRR analysis. Using the external rate of return method, which would you choose? What is its external rate of return? (We use a 10-year planning horizon.)

56 Solution to Example 8.11 Investment Initial Investment $15, $25, $40, $50, $70, Annual Return $3, $5, $9, $11, $14, Salvage Value $15, $25, $40, $50, $70, ERR 21.27% 19.02% 20.47% 20.19% 19.19% Investment Δ Investment $15, $10, $25, $10, $20, Δ Annual Return $3, $1, $5, $2, $3, Δ Salvage Value $15, $10, $25, $10, $20, Δ ERR 21.27% 14.70% 19.97% 19.02% 16.30% > M ARR? Yes No Yes Yes No Defender Choose 4

57 Solution to Example 8.11 Investment Initial Investment $15, $25, $40, $50, $70, Annual Return $3, $5, $9, $11, $14, Salvage Value $15, $25, $40, $50, $70, ERR 21.27% 19.02% 20.47% 20.19% 19.19% =RATE(10,,-50000,FV(18%,10,-11250)+50000) Investment Δ Investment $15, $10, $25, $10, $20, Δ Annual Return $3, $1, $5, $2, $3, Δ Salvage Value $15, $10, $25, $10, $20, Δ ERR 21.27% 14.70% 19.97% 19.02% 16.30% > M ARR? Yes No Yes Yes No Defender Choose 4

58 Example 8.12 Recall the example involving two designs (A & B) for a new ride at a theme park in Florida: A costs $300,000, has $55,000/yr revenue, and has a negligible salvage value at the end of the 10-year planning horizon; B costs $450,000, has $80,000/yr revenue, and has a negligible salvage value. Based on an ERR analysis and a 10% MARR, which is preferred? ERR A (10%) =RATE(10,, ,FV(10%,10,-55000)) = % > MARR = 10% (A is acceptable) ERR B-A (10%) =RATE(10,, ,FV(10%,10,-25000)) = % > MARR = 10% (B is preferred) ERR B (10%) =RATE(10,, ,FV(10%,10,-80000)) = %

59 Example 8.13 Recall the batch chemical processing company that is considering two centrifuges for possible acquisition. The estimated cash flows are given below. With an 18.5% MARR, which should be chosen using an ERR analysis? EOY CF(A) CF(B) 0 -$7,585, $10,285, $1,237, $1,575, $1,695, $2,455, $2,002, $2,657, $2,345, $2,877, $2,450, $3,025, $2,575, $3,250, $2,735, $3,565, $3,005, $3,750, $3,857, $4,252, $5,285, $8,750,000.00

60 Choose Investment A

61 Example 8.14 Recall, the three mutually exclusive investment alternatives having the cash flow profiles shown below. Based on a 15% MARR and ERR analysis, which should be chosen? EOY CF(1) CF(2) CF(3) 0 -$100,000 -$125,000 -$150,000 1 $20,000 -$25,000 -$35,000 2 $20,000 $75,000 $75,000 3 $20,000 $70,000 $75,000 4 $20,000 $60,000 $75,000 5 $120,000 $55,000 $95,000

62 Choose Investment 2

63 Analyzing Alternatives with No Positive Cash Flows

64 Example 8.15 A company must purchase a new incinerator to meet air quality standards. Three alternatives have been identified, with cash flow profiles given below. Based on a 7-year planning horizon and a 12% MARR, which should be purchased? Perform PW, AW, IRR, and ERR analyses. Alt Initial Investment Annual Operating Cost Cost A $250,000 $105,000 $42,000 B $385,000 $78,000 $28,000 C $475,000 $65,000 $18,000 Annual Maintenance

65 Solution to Example 8.15 PW A (12%) = $250,000 + $147,000(P A 12%,7) = $250,000 + $147,000( ) = $920, =PV(12%,7, ) = $920, PW B (12%) = $385,000 + $106,000(P A 12%,7) = $385,000 + $106,000( ) = $868, =PV(12%,7, ) = $868, PW C (12%) = $475,000 + $83,000(P A 12%,7) = $475,000 + $83,000( ) = $853, =PV(12%,7,-83000) = $853, Choose C

66 Solution to Example 8.15 (Continued) EUAC A (12%) = $250,000(A P 12%,7) + $147,000 = $250,000( ) + $147,000 = $201, =PMT(12%,7, ) = $201, EUAC B (12%) = $385,000(A P 12%,7) + $106,000 = $385,000( ) + $106,000 = $190, =PMT(12%,7, ) = $190, EUAC C (12%) = $475,000 + $83,000(P A 12%,7) = $475,000 + $83,000( ) = $187, =PMT(12%,7, ) = $187, Choose C

67 Solution to Example 8.15 (Continued) IRR analysis Incremental solution: B-A ($135,000 incremental investment produces $41,000 incremental reduction in annual costs) IRR B-A (12%) =RATE(7,41000, ) = 23.4% > 12% (B>>A) Incremental solution: C-B ($90,000 incremental investment produces $23,000 incremental reduction in annual costs) IRR C-B (12%) =RATE(7,23000,-90000) = % > 12% (C>>B) Choose C

68 Solution to Example 8.15 (Continued) ERR analysis Incremental solution: B-A ($135,000 incremental investment yields $41,000 reduction in annual costs) $135,000(1+ERR B-A ) 7 = $41,000(F A 12%,7) (1+ERR B-A ) 7 = $41,000( )/$135,000 ERR B-A = % > 12% (B>>A) =RATE(7,, ,FV(12%,7,-41000)) = % > 12% Incremental solution: C-B ($90,000 incremental investment yields $23,000 reduction in annual costs) $90,000(1+ERR C-B ) 7 = $23,000(F A 12%,7) (1+ERR C-B ) 7 = $23,000( )/$90,000 ERR C-B = % > 12% (C>>B) =RATE(7,,-90000,FV(12%,7,-23000)) = % > 12% Choose C

69 Pit Stop #8 Halfway Home! Miles to Go! 1. True or False: For personal investment decision making, rates of return are used more frequently than present worth. 2. True or False: Unless non-monetary considerations dictate otherwise, you should choose the mutually exclusive investment alternative having the greatest rate of return over the planning horizon. 3. True or False: If ERR > MARR, then IRR > ERR > MARR. 4. True or False: If PW > 0, then IRR > MARR. 5. True or False: If ERR > MARR, then MIRR > MARR. 6. True or False: If IRR(A) > IRR(B), then ERR(A) > ERR(B). 7. True or False: If PW(A) > PW(B), then FW(A) > FW(B), AW(A) > AW(B), CW(A) > CW(B), and IRR(A) > IRR(B). 8. True or False: Multiple roots can exist when using IRR and MIRR methods. 9. True or False: Excel s IRR worksheet function signals if multiple roots exist for a cash flow series. 10. True or False: Of all the equivalent DCF methods, the one that is the most difficult to use is the external rate of return method because of its requirement of a reinvestment rate for recovered capital.

70 Pit Stop #8 Halfway Home! Miles to Go! 1. True or False: For personal investment decision making, rates of return are used more frequently than present worth. TRUE 2. True or False: Unless non-monetary considerations dictate otherwise, you should choose the mutually exclusive investment alternative having the greatest rate of return over the planning horizon. FALSE 3. True or False: If ERR > MARR, then IRR > ERR > MARR. TRUE 4. True or False: If PW > 0, then IRR > MARR. TRUE 5. True or False: If ERR > MARR, then MIRR > MARR. FALSE 6. True or False: If IRR(A) > IRR(B), then ERR(A) > ERR(B). FALSE 7. True or False: If PW(A) > PW(B), then FW(A) > FW(B), AW(A) > AW(B), CW(A) > CW(B), and IRR(A) > IRR(B). FALSE 8. True or False: Multiple roots can exist when using IRR and MIRR methods. FALSE 9. True or False: Excel s IRR worksheet function signals if multiple roots exist for a cash flow series. FALSE 10. True or False: Of all the equivalent DCF methods, the one that is the most difficult to use is the external rate of return method because of its requirement of a reinvestment rate for recovered capital. FALSE

Chapter 4. Establishing the Planning Horizon & MARR. Principles of Engineering Economic Analysis, 5th edition

Chapter 4 Establishing the Planning Horizon & MARR Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate

Chapter 4 Establishing the Planning Horizon & MARR Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate

Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

Principles of Engineering Economic Analysis, 5th edition") Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) 0 1 2 3 4 5 ( - ) Time $2,000 $3,000 $4,000 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A)

Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) 0 1 2 3 4 5 ( - ) Time $2,000 $3,000 $4,000 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A)

IE 343 Midterm Exam 2

IE 343 Midterm Exam 2 Nov 16, 2011 Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Exam 2 has three

IE 343 Midterm Exam 2 Nov 16, 2011 Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Exam 2 has three

IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation

Using Excel Financial Functions for Project Evaluation") IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation 1. Objectives and Overview Solutions Guide by Hong Lanqing, Wang Xin and Mei Wenjie The objective of

IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation 1. Objectives and Overview Solutions Guide by Hong Lanqing, Wang Xin and Mei Wenjie The objective of

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1 LEARNING OBJECTIVES Work with mutually exclusive alternatives based upon ROR analysis 1. Why Incremental Analysis? 2. Incremental Cash Flows

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1 LEARNING OBJECTIVES Work with mutually exclusive alternatives based upon ROR analysis 1. Why Incremental Analysis? 2. Incremental Cash Flows

Comparing Mutually Exclusive Alternatives

Comparing Mutually Exclusive Alternatives Comparing Mutually Exclusive Projects Mutually Exclusive Projects Alternative vs. Project Do-Nothing Alternative 2 Some Definitions Revenue Projects Projects whose

Comparing Mutually Exclusive Alternatives Comparing Mutually Exclusive Projects Mutually Exclusive Projects Alternative vs. Project Do-Nothing Alternative 2 Some Definitions Revenue Projects Projects whose

Lesson FA xx Capital Budgeting Part 2C

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

Principles of Engineering Economic Analysis, 5th edition") Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams (EOY) Example 2.1 Cash Flow Profiles for Two Investment Alternatives End of Year (EOY) CF(A) CF(B) CF(B-A) 0 -$100,000 -$100,000 $0 1 $10,000 $50,000

Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams (EOY) Example 2.1 Cash Flow Profiles for Two Investment Alternatives End of Year (EOY) CF(A) CF(B) CF(B-A) 0 -$100,000 -$100,000 $0 1 $10,000 $50,000

CAPITAL BUDGETING TECHNIQUES (CHAPTER 9)

") CAPITAL BUDGETING TECHNIQUES (CHAPTER 9) Capital budgeting refers to the process used to make decisions concerning investments in the long-term assets of the firm. The general idea is that a firm s capital,

CAPITAL BUDGETING TECHNIQUES (CHAPTER 9) Capital budgeting refers to the process used to make decisions concerning investments in the long-term assets of the firm. The general idea is that a firm s capital,

COMPARING ALTERNATIVES

CHAPTER 6 COMPARING FEASIBLE DESIGN Alternatives may be mutually exclusive (i.e., choice if one excludes the choice of any other alternative) because : The alternatives being considered may require different

CHAPTER 6 COMPARING FEASIBLE DESIGN Alternatives may be mutually exclusive (i.e., choice if one excludes the choice of any other alternative) because : The alternatives being considered may require different

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh Quiz 1, 2, 7, 15,19, 20, 22, 26, 36, 40. The objective of chapter 6 is to evaluate correctly capital investment alternatives when

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh Quiz 1, 2, 7, 15,19, 20, 22, 26, 36, 40. The objective of chapter 6 is to evaluate correctly capital investment alternatives when

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

INTERNAL RATE OF RETURN

INTERNAL RATE OF RETURN Introduction You put money in a bank account and expect to get a return 1 percent You can think of investment/business/project in the same way Every investment/business/project

INTERNAL RATE OF RETURN Introduction You put money in a bank account and expect to get a return 1 percent You can think of investment/business/project in the same way Every investment/business/project

Seminar on Financial Management for Engineers. Institute of Engineers Pakistan (IEP)

") Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Chapter 9. Depreciation. Principles of Engineering Economic Analysis, 5th edition

Chapter 9 Depreciation Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5. Compare the

Chapter 9 Depreciation Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5. Compare the

IE463 Chapter 4. Objective: COMPARING INVESTMENT AND COST ALTERNATIVES

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

Multiple Choice: 5 points each

Carefully read each problem before answering. Please write clearly, and show and label all factors used in any problem requiring mathematical calculations. SHOW ALL WORK. Multiple Choice: 5 points each

Carefully read each problem before answering. Please write clearly, and show and label all factors used in any problem requiring mathematical calculations. SHOW ALL WORK. Multiple Choice: 5 points each

Other Analysis Techniques. Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period

Benefit-Cost Ratio Analysis (BCRA) Payback Period") Other Analysis Techniques Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period 1 Techniques for Cash Flow Analysis Present Worth Analysis Annual Cash Flow Analysis Rate of Return

Other Analysis Techniques Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period 1 Techniques for Cash Flow Analysis Present Worth Analysis Annual Cash Flow Analysis Rate of Return

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

Mutually Exclusive Choose at most one From the Set

1 Mutually Exclusive Choose at most one From the Set This lecture addresses an issue that is confusing to many users of the rate of return method. When choosing among mutually exclusive alternatives, never

1 Mutually Exclusive Choose at most one From the Set This lecture addresses an issue that is confusing to many users of the rate of return method. When choosing among mutually exclusive alternatives, never

IE463 Chapter 3. Objective: INVESTMENT APPRAISAL (Applications of Money-Time Relationships)

") IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

2, , , , ,220.21

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

ECLT 5930/SEEM 5740: Engineering Economics Second Term

ECLT 5930/SEEM 5740: Engineering Economics 2015 16 Second Term Master of Science in ECLT & SEEM Instructors: Dr. Anthony Man Cho So Department of Systems Engineering & Engineering Management The Chinese

ECLT 5930/SEEM 5740: Engineering Economics 2015 16 Second Term Master of Science in ECLT & SEEM Instructors: Dr. Anthony Man Cho So Department of Systems Engineering & Engineering Management The Chinese

1.011Project Evaluation: Comparing Costs & Benefits

1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs of the project? Present, Future, and Annual Worth Internal

1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs of the project? Present, Future, and Annual Worth Internal

8: Economic Criteria

8.1 Economic Criteria Capital Budgeting 1 8: Economic Criteria The preceding chapters show how to discount and compound a variety of different types of cash flows. This chapter explains the use of those

8.1 Economic Criteria Capital Budgeting 1 8: Economic Criteria The preceding chapters show how to discount and compound a variety of different types of cash flows. This chapter explains the use of those

IE 343 Section 1 Engineering Economy Exam 2 Review Problems Solutions Instructor: Tian Ni March 30, 2012

IE 343 Section 1 Engineering Economy Exam 2 Review Problems Solutions Instructor: Tian Ni March 30, 2012 1. A firm is considering investing in a machine that has an initial cost of $36,000. For a period

IE 343 Section 1 Engineering Economy Exam 2 Review Problems Solutions Instructor: Tian Ni March 30, 2012 1. A firm is considering investing in a machine that has an initial cost of $36,000. For a period

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives Why ROR measure is so popular? This

Chapter 7 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives Why ROR measure is so popular? This

An Interesting News Item

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 26: Other Analysis Techniques If you work just for money, you'll never make it, but if you love what you're doing and you always

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 26: Other Analysis Techniques If you work just for money, you'll never make it, but if you love what you're doing and you always

Lecture 5 Present-Worth Analysis

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

What Is a Project? How Do We Justify a Project? 1.011Project Evaluation: Comparing Costs & Benefits Carl D. Martland

MIT Civil Engineering 1.11 -- Project Evaluation Spring Term 23 1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs

MIT Civil Engineering 1.11 -- Project Evaluation Spring Term 23 1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs

Engineering Economy. Lecture 8 Evaluating a Single Project IRR continued Payback Period. NE 364 Engineering Economy

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

SOLUTIONS TO SELECTED PROBLEMS. Student: You should work the problem completely before referring to the solution. CHAPTER 1

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

IE 343 Midterm Exam 2

IE 343 Midterm Exam 2 April 6, 2012 Version A Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest

IE 343 Midterm Exam 2 April 6, 2012 Version A Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR. ENG2000: R.I. Hornsey CM_2: 1

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR ENG2000: R.I. Hornsey CM_2: 1 Introduction This chapter introduces a second method for comparing between projects While the result of the process

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR ENG2000: R.I. Hornsey CM_2: 1 Introduction This chapter introduces a second method for comparing between projects While the result of the process

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Comparing Mutually Exclusive Alternatives

Comparing Mutually Exclusive Alternatives Lecture No. 18 Chapter 5 Contemporary Engineering Economics Copyright 2016 Comparing Mutually Exclusive Projects: Basic Terminologies Mutually Exclusive Projects

Comparing Mutually Exclusive Alternatives Lecture No. 18 Chapter 5 Contemporary Engineering Economics Copyright 2016 Comparing Mutually Exclusive Projects: Basic Terminologies Mutually Exclusive Projects

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Engineering Economics

Engineering Economics Lecture 7 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Engineering Economics Lecture 7 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Capital Budgeting Process and Techniques 93. Chapter 7: Capital Budgeting Process and Techniques

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Chapter 11: Capital Budgeting: Decision Criteria

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

i* = IRR i*? IRR more sign changes Passes: unique i* = IRR

Decision Rules Single Alternative Based on Sign Changes of Cash Flow: Simple Investment i* = IRR Accept if i* > MARR Single Project start with zero, one sign change Non-Simple Investment i*? IRR Net Investment

Decision Rules Single Alternative Based on Sign Changes of Cash Flow: Simple Investment i* = IRR Accept if i* > MARR Single Project start with zero, one sign change Non-Simple Investment i*? IRR Net Investment

Net Present Value Q: Suppose we can invest $50 today & receive $60 later today. What is our increase in value? Net Present Value Suppose we can invest

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Sample Questions for Chapters 10 & 11

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Present Worth Analysis

Present Worth Analysis Net Present Worth of initial and future cash flows can be used to select among alternative projects It is important to understand what Net Present Worth means, especially when the

Present Worth Analysis Net Present Worth of initial and future cash flows can be used to select among alternative projects It is important to understand what Net Present Worth means, especially when the

CHAPTER 2 LITERATURE REVIEW

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

An Introduction to Capital Budgeting Methods

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

CAPITAL BUDGETING. Key Terms and Concepts to Know

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

TAX ECONOMIC ANALYSIS 1 Haery Sihombing. Learning Objectives

Ir. /IP Pensyarah Pelawat Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka 1. Terminology and Rates 2. Before and After-Tax Analysis 6 3. Taxes and Depreciation 4. Depreciation Recapture

Ir. /IP Pensyarah Pelawat Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka 1. Terminology and Rates 2. Before and After-Tax Analysis 6 3. Taxes and Depreciation 4. Depreciation Recapture

Software Economics. Metrics of Business Case Analysis Part 1

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

# 6. Comparing Alternatives

IE 5441 1 # 6. Comparing Alternatives One of the main purposes of this course is to discuss how to make decisions in engineering economy. Let us first consider a single period case. Suppose that there

IE 5441 1 # 6. Comparing Alternatives One of the main purposes of this course is to discuss how to make decisions in engineering economy. Let us first consider a single period case. Suppose that there

Session 2, Monday, April 3 rd (11:30-12:30)

") Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

Chapter One. Definition and Basic terms and terminology of engineering economy

Chapter One Definition and Basic terms and terminology of engineering economy 1. Introduction: The need for engineering economy is primarily motivated by the work that engineers do in performing analysis,

Chapter One Definition and Basic terms and terminology of engineering economy 1. Introduction: The need for engineering economy is primarily motivated by the work that engineers do in performing analysis,

1 Week Recap Week 2

1 Week 3 1.1 Recap Week 2 pv, fv, timeline pmt - we don t have to keep it the same every period. Ex.: Suppose you are exactly 30 years old. You believe that you will be able to save for the next 20 years,

1 Week 3 1.1 Recap Week 2 pv, fv, timeline pmt - we don t have to keep it the same every period. Ex.: Suppose you are exactly 30 years old. You believe that you will be able to save for the next 20 years,

INTRODUCTION TO CAPITAL BUDGETING

00_-_ch.qxd //0 : PM Page CHAPTER INTRODUCTION TO CAPITAL BUDGETING Overview. The NPV Rule for Judging Investments and Projects. The IRR Rule for Judging Investments. NPV or IRR, Which to Use?. The Yes

00_-_ch.qxd //0 : PM Page CHAPTER INTRODUCTION TO CAPITAL BUDGETING Overview. The NPV Rule for Judging Investments and Projects. The IRR Rule for Judging Investments. NPV or IRR, Which to Use?. The Yes

Techniques for Cash Flow Analysis

Techniques for Cash Flow Analysis Present Worth Analysis Chapter 5 Annual Cash Flow Analysis Chapter 6 Rate of Return Analysis Chapter 7 Incremental Analysis Other Techniques: Future Worth Analysis Benefit-Cost

Techniques for Cash Flow Analysis Present Worth Analysis Chapter 5 Annual Cash Flow Analysis Chapter 6 Rate of Return Analysis Chapter 7 Incremental Analysis Other Techniques: Future Worth Analysis Benefit-Cost

Session 02. Investment Decisions

Session 02 Investment Decisions Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Session 02 Investment Decisions Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Capital Budgeting Decision Methods

Capital Budgeting Decision Methods Everything is worth what its purchaser will pay for it. Publilius Syrus In April of 2012, before Facebook s initial public offering (IPO), it announced it was acquiring

Capital Budgeting Decision Methods Everything is worth what its purchaser will pay for it. Publilius Syrus In April of 2012, before Facebook s initial public offering (IPO), it announced it was acquiring

Incremental Cash Flow: Example

Note 8. Making Capital Investment Decisions To include or not to include? that is the question. General Milk Company is currently evaluating the NPV of establishing a line of chocolate milk. As part of

Note 8. Making Capital Investment Decisions To include or not to include? that is the question. General Milk Company is currently evaluating the NPV of establishing a line of chocolate milk. As part of

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

Chapter 15 Inflation

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

MGT201 Lecture No. 11

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

Although most Excel users even most advanced business users will have scant occasion

Chapter 5 FINANCIAL CALCULATIONS In This Chapter EasyRefresher : Applying Time Value of Money Concepts Using the Standard Financial Functions Using the Add-In Financial Functions Although most Excel users

Chapter 5 FINANCIAL CALCULATIONS In This Chapter EasyRefresher : Applying Time Value of Money Concepts Using the Standard Financial Functions Using the Add-In Financial Functions Although most Excel users

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Chapter 5. Interest Rates ( ) 6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.

6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.") Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Capital Budgeting Decision Methods

Capital Budgeting Decision Methods 1 Learning Objectives The capital budgeting process. Calculation of payback, NPV, IRR, and MIRR for proposed projects. Capital rationing. Measurement of risk in capital

Capital Budgeting Decision Methods 1 Learning Objectives The capital budgeting process. Calculation of payback, NPV, IRR, and MIRR for proposed projects. Capital rationing. Measurement of risk in capital

CHAPTER 7: ENGINEERING ECONOMICS

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

SOLUTIONS TO ASSIGNMENT PROBLEMS. Problem No.1 10,000 5,000 15,000 20,000. Problem No.2. Problem No.3

MASTER MINDS No. for CA/CWA & MEC/CEC. CAPITAL BUDGETING SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. Calculation of ARR for machine A and B: Machine A Step : Average Profit After Tax 5,, 5,, 5, Total

MASTER MINDS No. for CA/CWA & MEC/CEC. CAPITAL BUDGETING SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. Calculation of ARR for machine A and B: Machine A Step : Average Profit After Tax 5,, 5,, 5, Total

hp calculators HP 12C Platinum Internal Rate of Return Cash flow and IRR calculations Cash flow diagrams The HP12C Platinum cash flow approach

HP 12C Platinum Internal Rate of Return Cash flow and IRR calculations Cash flow diagrams The HP12C Platinum cash flow approach Practice with solving cash flow problems related to IRR How to modify cash

HP 12C Platinum Internal Rate of Return Cash flow and IRR calculations Cash flow diagrams The HP12C Platinum cash flow approach Practice with solving cash flow problems related to IRR How to modify cash

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

Chapter 7 An Economic Appraisal II: NPV, AE, IRR Technique

Chapter 7 An Economic Appraisal II: NPV, AE, IRR Technique Powerpoint Templates Page 1 Net Present Value Technique NPV=The Sum of The Present Values of All Cash Inflows The Sum of The Present Value of

Chapter 7 An Economic Appraisal II: NPV, AE, IRR Technique Powerpoint Templates Page 1 Net Present Value Technique NPV=The Sum of The Present Values of All Cash Inflows The Sum of The Present Value of

AFM 271. Midterm Examination #2. Friday June 17, K. Vetzal. Answer Key

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

10. Estimate the MIRR for the project described in Problem 8. Does it change your decision on accepting this project?

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

SOLUTIONS TO ASSIGNMENT PROBLEMS. Problem No.1

W.N.-1: Calculation of depreciation per annum Depreciation p.a. = SOLUTIONS TO ASSIGNMENT PROBLEMS Cost -Scrap Value Life W.N.-2: Calculation of PAT p.a. Problem No.1 80,000 5 10,000 = Rs.14,000 p.a. 2.

W.N.-1: Calculation of depreciation per annum Depreciation p.a. = SOLUTIONS TO ASSIGNMENT PROBLEMS Cost -Scrap Value Life W.N.-2: Calculation of PAT p.a. Problem No.1 80,000 5 10,000 = Rs.14,000 p.a. 2.

KING FAHAD UNIVERSITY OF PETROLEUM & MINERALS COLLEGE OF ENVIROMENTAL DESGIN CONSTRUCTION ENGINEERING & MANAGEMENT DEPARTMENT

KING FAHAD UNIVERSITY OF PETROLEUM & MINERALS COLLEGE OF ENVIROMENTAL DESGIN CONSTRUCTION ENGINEERING & MANAGEMENT DEPARTMENT Report on: Associated Problems with Life Cycle Costing As partial fulfillment

KING FAHAD UNIVERSITY OF PETROLEUM & MINERALS COLLEGE OF ENVIROMENTAL DESGIN CONSTRUCTION ENGINEERING & MANAGEMENT DEPARTMENT Report on: Associated Problems with Life Cycle Costing As partial fulfillment

Advanced Cost Accounting Acct 647 Prof Albrecht s Notes Capital Budgeting

Advanced Cost Accounting Acct 647 Prof Albrecht s Notes Capital Budgeting Drawing a timeline can help in identifying all the amounts for computations. I ll present two models. The first is without taxes.

Advanced Cost Accounting Acct 647 Prof Albrecht s Notes Capital Budgeting Drawing a timeline can help in identifying all the amounts for computations. I ll present two models. The first is without taxes.

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Lecture Guide. Sample Pages Follow. for Timothy Gallagher s Financial Management 7e Principles and Practice

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

CHAPTER 11. Topics. Cash Flow Estimation and Risk Analysis. Estimating cash flows: Relevant cash flows Working capital treatment

CHAPTER 11 Cash Flow Estimation and Risk Analysis 1 Topics Estimating cash flows: Relevant cash flows Working capital treatment Risk analysis: Sensitivity analysis Scenario analysis Simulation analysis

CHAPTER 11 Cash Flow Estimation and Risk Analysis 1 Topics Estimating cash flows: Relevant cash flows Working capital treatment Risk analysis: Sensitivity analysis Scenario analysis Simulation analysis

Overall ROR: 30,000(0.20) + 70,000(0.14) = 100,000(x) x = 15.8% Prepare a tabulation of cash flow for the alternatives shown below.

+ 70,000(0.14) = 100,000(x) x = 15.8% Prepare a tabulation of cash flow for the alternatives shown below.") Chapter 8, Problem 2. What is the overall rate of return on a $100,000 investment that returns 20% on the first $30,000 and 14% on the remaining $70,000? Chapter 8, Solution 2. Overall ROR: 30,000(0.20)

Chapter 8, Problem 2. What is the overall rate of return on a $100,000 investment that returns 20% on the first $30,000 and 14% on the remaining $70,000? Chapter 8, Solution 2. Overall ROR: 30,000(0.20)

chapter11 In 1970, the Adolph Coors Company was a The Basics of Capital Budgeting: Evaluating Cash Flows

chapter11 The Basics of Capital Budgeting: Evaluating Cash Flows In 1970, the Adolph Coors Company was a small brewer serving a regional market, but because of its quality products and aggressive marketing,

chapter11 The Basics of Capital Budgeting: Evaluating Cash Flows In 1970, the Adolph Coors Company was a small brewer serving a regional market, but because of its quality products and aggressive marketing,

Principles of Financial Feasibility ARCH 738: REAL ESTATE PROJECT MANAGEMENT. Morgan State University

Principles of Financial Feasibility ARCH 738: REAL ESTATE PROJECT MANAGEMENT Morgan State University Jason E. Charalambides, PhD, MASCE, AIA, ENV_SP (This material has been prepared for educational purposes)

Principles of Financial Feasibility ARCH 738: REAL ESTATE PROJECT MANAGEMENT Morgan State University Jason E. Charalambides, PhD, MASCE, AIA, ENV_SP (This material has been prepared for educational purposes)

Methods of Financial Appraisal

Appendix 2 Methods of Financial Appraisal The of money over time There are a number of financial appraisal techniques, ranging from the simple to the sophisticated, that can be of use as an aid to decision-making

Appendix 2 Methods of Financial Appraisal The of money over time There are a number of financial appraisal techniques, ranging from the simple to the sophisticated, that can be of use as an aid to decision-making

IE 343 Midterm Exam. March 7 th Closed book, closed notes.

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still