Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

|

|

|

- Blaise Price

- 6 years ago

- Views:

Transcription

1 Topics in Corporate Finance Chapter 2: Valuing Real Assets

2 Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods Discounted cash flows (DCF) Internal rate of return (IRR) Payback method

3 Valuing real assets Should we invest? For example, in buying a fridge or an office building First, how can we evaluate these projects? Net Present Value: value today net of investment costs Then, the answer is easy Positive Undertake it!! Negative Don t!

4 Present and Future Value A pound today is worth more than one tomorrow! Why? If the interest is 10% a year Investing 28 million today gives 30,8 million year The future value (in a year) of 28 million is 30.8 million The present value of 30.8 million in a year is 28 million

5 More generally Future Value: Amount to which an investment will grow after earning interest FV = x (1 + r) Present Value: Value today of a future (expected) cash flow. PV = (1 1 + r) Discount Factor: Present value of a 1 future (expected) payment Discount Rate, hurdle rate or (opportunity) cost of capital Interest rate used to compute present values of future cash flows Best available expected return offered in the market on an investment of comparable risk and term to the cash flow being discounted (methods: CAPM, APT, see asset pricing module, next term) t t C t

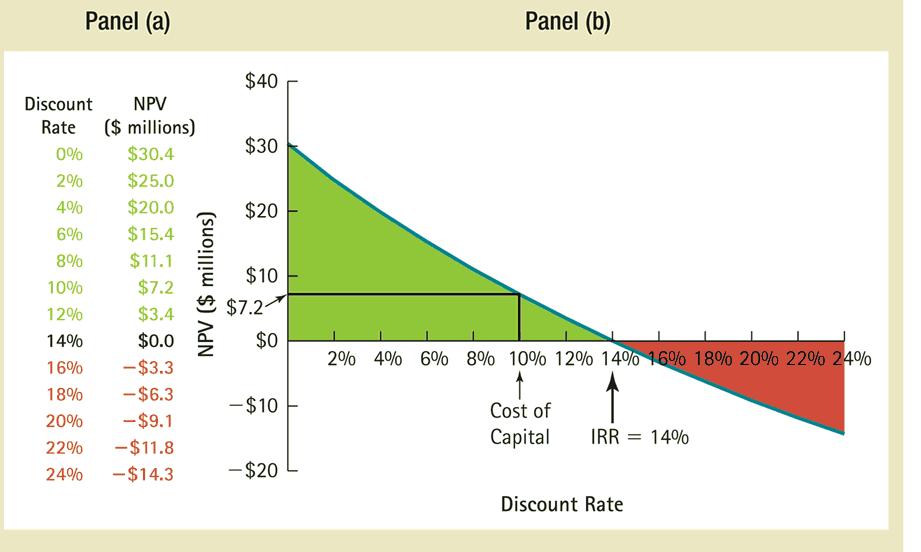

6 Example A fertilizer company can create a new environmentally friendly fertilizer at a large savings over the company s existing fertilizer Step 1: Forecast cash flows The fertilizer will require a new factory that can be built at a cost of 81.6 million Estimated revenues on new fertilizer 28 million after the first year, and lasting four years Step 2: Estimate opportunity cost of capital Project s cost of capital is 10% Step 3: Discount future cash flows See next slide Step 4: Go ahead if PV of payoff exceeds investment

7 Computing NPV Timeline with estimated returns: Cash flows: immediate 81.6 million outflow and an annuity inflow of 28 million per year for 4 years Therefore, given a discount rate r, the NPV is: NPV = r (1 + r ) (1 + r ) (1 + r ) Substituting r=0.1, the NPV is 7.2 million>0, hence invest!!

8

9 More generally Net present value or discounted cash flow : C1 C2 C3 NPV = C r (1 + r ) (1 + r ) Where sometimes we denote C (1 + T r T ) T C1 C2 C3 NPV = C0 + PV where PV = r (1 + r ) (1 + r ) CT (1 + r T ) T Back to the example: If cash flows are certain, should r 2 be higher than r 1? What if the fertilizer cash flows have higher risk (same expected value)? What would the NPV if the fertilizer cash flows last forever?

10 Value of a perpetuity The present value of a perpetuity (constant cash flows Cf and constant r): Proof: PV(perp.) Cf = = (1 + r) t t= 1 Cf r V CF CF CF = ( 1+ r) ( 1+ r) ( 1+ r) 2 3 CF CF (1 + rv ) = CF ( 1+ r) ( 1+ r) subtract the first equation from the second CF rv = CF (or) V= r 2

11 Project Selection 1. If only one from a set of positive NPV projects can be selected, we should select that with the largest NPV 2. When resources are limited, the profitability index (PI) helps selecting among various project combinations and alternatives: PI = PV / -C 0 If resources are unlimited, we should select projects with PI>1 If resources are limited and projects are scalable then PI is useful Example: Two scalable projects and GBP 10,000 Project C0 C1 C2 A PI B

12 Project Selection 1. If only one from a set of positive NPV projects can be selected, we should select that with the largest NPV 2. When resources are limited, the profitability index (PI) helps selecting among various project combinations and alternatives: PI = PV / -C 0 If resources are unlimited, we should select projects with PI>1 If resources are limited and projects are scalable then PI is useful Example: Two scalable projects and GBP 10,000 Project C0 C1 C2 A B PI 9 3

13 But, are there other criteria? Survey Data on CFO Use of Investment Evaluation Techniques NPV, 75% IRR, 76% Payback, 57% Book rate of return, 20% Profitability Index, 12% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% SOURCE: Graham and Harvey, The Theory and Practice of Finance: Evidence from the Field, Journal of Financial Economics 61 (2001), pp

14 Rate of Return Rule Accept investments that offer (internal) rates of return in excess of their opportunity cost of capital Example A project generates in a year but requires an investment of today, and the foregone investment opportunity is 12%. Should we take it? profit 420, ,000 Return = = =.135 or 13.5% investment 370,000

15 More generally The rate of return of a cash flow stream is the interest rate y that makes the NPV of a project equal to 0: 0 C1 C2 C3 = C y (1 + y) (1 + y) CT (1 + y) T Fertilizer example: NPV = (1 + IRR ) (1 + IRR ) (1 + IRR ) (1 + IRR ) 1 = 0 IRR = 14%

16

17 IRR and NPV Computing the IRR is useful if estimate of cost of capital is imprecise IRR rule same criteria as NPV rule if NPV is decreasing wrt discount rate However, the IRR rule has some pitfalls: If NPV increases (e.g. borrowing money), we should therefore ask for an IRR lower than the opportunity cost of capital There might be several IRRs or none Ignores magnitude and cannot select among different projects Even more problematic if we discount rates are not stable over time (with which one do we compare?)

18 Payback The payback period of a project is the number of years it takes before the cumulative forecasted cash flow equals the initial outlay. The payback rule says only accept projects that payback in the desired time frame. This method is flawed, primarily because it ignores later year cash flows and the the present value of future cash flows Therefore it biases decisions towards accepting projects paying early

19 Payback Example Examine the three projects and note the mistake we would make if we insisted on only taking projects with a payback period of 2 years or less. Project C0 C1 C2 C3 A B C Payback Period NPV@ 10% + 2,

20 Reading How CFOs make capital budgeting and capital structure decisions, Journal of Applied Corporate Finance (2002)

21 Appendix

22 Compounding Most interest rates are stated in annual terms. This does not, however, mean that interest is paid only once a year. Many securities pay interest semi-annually (e.g. Corporate Bonds), monthly (some savings accounts), daily, or even continually. If the compounding frequency is not annual, then the stated interest rate is not equal to the actual return you are earning (effective annual yield). If the compounding frequency increases, so does the effective annual yield.

23 An example: What is the future value of 1 in 5 years if r is 6% under: 1) annual compounding FV = 1 ( 1.06 ) 5 = ) Semi-annual compounding (3% every six months) FV ( ) 5 2 = = ) Monthly compounding (0.5% per month) FV ( ) 512 = = 1.349

24 In general, the future and present values of 1 dollar T years from now at a compounding frequency of m times per year are given by: FV m T r $1 = $1 1 + PV = m r 1+ m m T Note: For continuous compounding, these expressions approach: m T r $1 FV = lim $1 1 + = e PV = lim = e m m r 1+ m r T -r T m m T where e = is the base of the natural logarithm

25 Consequently, we can convert r (stated by banks) to the effective annual yield. We can then use the effective annual yield in order to compare interest rates that are paid with differing compounding frequencies. 1 + Effective Annual Yield = 1 + r m m again, for continuous compounding, this rate approaches Effective Annual Yield = e r -1 (Note: For a given r, a higher compounding frequency [i.e. more frequent interest payments] leads to a higher future value of an investment and a lower present value of future cash flows)

26 IMPORTANT: Unless otherwise specified, the interest rate (r) is the annually compounded annual interest rate. I.e. if I tell you the interest rate is 4%, that means that after 1 year, the investor will have 1.04 for every 1 invested.

27 Inflation: We have treated all cash flows as nominal cash flows. Real cash flows are adjusted for inflation and thus comparable across time in terms of their purchasing power. One nominal dollar in 1995 is worth less (in terms of purchasing power) than one nominal dollar in One real, inflation adjusted dollar in 1995 is worth the same (in terms of purchasing power) as a real dollar in Interest rates also appear in real and nominal terms. The quoted interest is always nominal.

28 Always discount nominal cash flows with the nominal rate and real cash flows with the real rate. If you earn a 6% nominal rate (r) on your investment of 100 and 3% of that return is eaten up by inflation (i), then your real return (ρ) is computed as: 100 (1+ρ) = $100 (1 + (1 + i) r) = $ or ρ = 2.91% More Generally: (1+r) = (1+ρ) (1+i)

29 Suppose you receive a nominal cash flow of 50 next year (i = 4%, r = 12%) $50 PV = = Suppose you receive a real cash flow of next year (equivalent to a 50 nominal cash flow) compute the real interest rate: 1+ρ = 1.12/1.04 = $48.08 PV = = Either way is correct. Most of the time calculating everything in nominal terms is easier. That does not mean that we are ignoring inflation, because inflation cancels out from using nominal cash flows and nominal interest rates.

30 Cash Flow Calculations It would be nice if we could get cash flow forecasts directly. Unfortunately, we often get numbers filtered through the Generally Accepted Accounting Principles (GAAP) or some other non-cash based format. Even innocent projections by project managers often are about project specific incomes and expenses which, after running through firm wide tax effects and other distortions, are different from actual cash flows. The specifics are for an accounting class. We will only cover the very basic ideas and adopt a cookie cutter approach.

31 Review: Revenues - Costs = Operating Income (EBITDA) - Non-Cash Expenses (NCE) = EBIT (Operating Profit) - Interest Expenses = Pretax Income - Taxes = Net Income - Dividends = Addition to Retained Earnings Also: EBIT (1-t) = NOPAT Current Assets - Current Liabilities = Working Capital Current Assets are things like inventories, accounts receivables, etc. Current Liabilities are things like Accounts Payable NCE are items like depreciation and ammortization

32 Free Cash Flow Calculations Let Cf t denote the net cash flow at time t. Cf t = Cash Inflow at t - Cash Outflow at t Cf t = NOPAT + Non-Cash Expenses (NCE) - net capital outlays - increase in working capital = EBITDA (1 t) + NCE t - net capital outlays - increase in working capital = NI + NCE + Interest x (1-t) - net capital outlays - increase in working capital

33 IMPORTANT: NEVER include financing cash flows (discounting takes care of the cost of capital) The Statement of Cash Flows does often include financing cash flows (hence, use with caution!) Do not include sunk costs. Often it is easier to estimate incremental cash flows. Include the true opportunity costs of using existing assets. Treat these as cash outflows if the project under consideration eliminates other profitable uses of the assets Do not allocate a share of the general overhead based on an arbitrary measure, such as sales or labor hours, just because the accountants do it. The real costs are relevant.

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Introduction to Discounted Cash Flow

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Net Present Value Q: Suppose we can invest $50 today & receive $60 later today. What is our increase in value? Net Present Value Suppose we can invest

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

Capital Budgeting, Part I

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

Capital Budgeting, Part I Lakehead University Fall 2004 Capital Budgeting Techniques 1. Net Present Value 2. The Payback Rule 3. The Average Accounting Return 4. The Internal Rate of Return 5. The Profitability

ACCTG101 Revision MODULES 10 & 11 LITTLE NOTABLES EXCLUSIVE - VICKY TANG

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

ACCTG101 Revision MODULES 10 & 11 TIME VALUE OF MONEY & CAPITAL INVESTMENT MODULE 10 TIME VALUE OF MONEY Time Value of Money is the concept that cash flows of dollar amounts have different values at different

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Topic 1 (Week 1): Capital Budgeting

: Capital Budgeting") 4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

Lecture 6 Capital Budgeting Decision

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Financial Management I

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Chapter 8 Net Present Value and Other Investment Criteria Good Decision Criteria

Chapter 8 Net Present Value and Other Investment Criteria Good Decision Criteria We need to ask ourselves the following questions when evaluating decision criteria Does the decision rule adjust for the

Chapter 8 Net Present Value and Other Investment Criteria Good Decision Criteria We need to ask ourselves the following questions when evaluating decision criteria Does the decision rule adjust for the

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

HOW TO CALCULATE PRESENT VALUES

HOW TO CALCULATE PRESENT VALUES Chapter 2 Brealey, Myers, and Allen Principles of Corporate Finance 11 th Global Edition Basics of this chapter Cash Flows (and Free Cash Flows) Definition and why is it

HOW TO CALCULATE PRESENT VALUES Chapter 2 Brealey, Myers, and Allen Principles of Corporate Finance 11 th Global Edition Basics of this chapter Cash Flows (and Free Cash Flows) Definition and why is it

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

What is it? Measure of from project. The Investment Rule: Accept projects with NPV and accept highest NPV first

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Analyzing Project Cash Flows. Chapter 12

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

(2) shareholders incur costs to monitor the managers and constrain their actions.

shareholders incur costs to monitor the managers and constrain their actions.") (2) shareholders incur costs to monitor the managers and constrain their actions. Agency problems are mitigated by good systems of corporate governance. Legal and Regulatory Requirements: Australian Securities

(2) shareholders incur costs to monitor the managers and constrain their actions. Agency problems are mitigated by good systems of corporate governance. Legal and Regulatory Requirements: Australian Securities

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Chapter 9 Net Present Value and Other Investment Criteria. Net Present Value (NPV) Net Present Value (NPV) Konan Chan. Financial Management, Fall 2018

Net Present Value (NPV) Konan Chan. Financial Management, Fall 2018") Chapter 9 Net Present Value and Other Investment Criteria Konan Chan Financial Management, Fall 2018 Topics Covered Investment Criteria Net Present Value (NPV) Payback Period Discounted Payback Average

Chapter 9 Net Present Value and Other Investment Criteria Konan Chan Financial Management, Fall 2018 Topics Covered Investment Criteria Net Present Value (NPV) Payback Period Discounted Payback Average

CAPITAL BUDGETING. John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada

CHAPTER 2 CAPITAL BUDGETING John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada LEARNING OUTCOMES After completing this chapter, you will be able to do the following:

CHAPTER 2 CAPITAL BUDGETING John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada LEARNING OUTCOMES After completing this chapter, you will be able to do the following:

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #2 Olga Bychkova Topics Covered Today Review of key finance concepts Valuation of stocks (chapter 4 in BMA) NPV and other investment criteria

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #2 Olga Bychkova Topics Covered Today Review of key finance concepts Valuation of stocks (chapter 4 in BMA) NPV and other investment criteria

J ohn D. S towe, CFA. CFA Institute Charlottesville, Virginia. J acques R. G agn é, CFA

CHAPTER 2 CAPITAL BUDGETING J ohn D. S towe, CFA CFA Institute Charlottesville, Virginia J acques R. G agn é, CFA La Société de l assurance automobile du Québec Quebec City, Canada LEARNING OUTCOMES After

CHAPTER 2 CAPITAL BUDGETING J ohn D. S towe, CFA CFA Institute Charlottesville, Virginia J acques R. G agn é, CFA La Société de l assurance automobile du Québec Quebec City, Canada LEARNING OUTCOMES After

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT. FCA, CFA L3 Candidate

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

Discounting. Capital Budgeting and Corporate Objectives. Professor Ron Kaniel. Simon School of Business University of Rochester.

Discounting Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Topic Overview The Timeline Compounding & Future Value Discounting & Present

Discounting Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Topic Overview The Timeline Compounding & Future Value Discounting & Present

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

1. give a picture of a company's ability to generate cash flow and pay it financial obligations: 2. Balance sheet items expressed as percentage of:

1. give a picture of a company's ability to generate cash flow and pay it financial obligations: a. Management ratios b. Working capital ratios c. Net profit margin ratios d. Solvency Ratios 2. Balance

1. give a picture of a company's ability to generate cash flow and pay it financial obligations: a. Management ratios b. Working capital ratios c. Net profit margin ratios d. Solvency Ratios 2. Balance

Time Value of Money. PV of Multiple Cash Flows. Present Value & Discounting. Future Value & Compounding. PV of Multiple Cash Flows

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting. Konan Chan Financial Management, Time Value of Money

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CHAPTER 2 LITERATURE REVIEW

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

MAXIMISE SHAREHOLDERS WEALTH.

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

Capital Budgeting, Part II

Capital Budgeting, Part II Lakehead University Fall 2004 Making Capital Investment Decisions 1. Project Cash Flows 2. Incremental Cash Flows 3. Basic Capital Budgeting 4. Capital Cost Allowance 5. The

Capital Budgeting, Part II Lakehead University Fall 2004 Making Capital Investment Decisions 1. Project Cash Flows 2. Incremental Cash Flows 3. Basic Capital Budgeting 4. Capital Cost Allowance 5. The

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

Module 4: Free Cash Flow (FCF) Which cash flows do we discount?

Which cash flows do we discount?") 70391 - Finance Module 4: Free Cash Flow (FCF) Which cash flows do we discount? 70391 Finance Fall 2016 Tepper School of Business Carnegie Mellon University c 2016 Chris Telmer. Some content from slides

70391 - Finance Module 4: Free Cash Flow (FCF) Which cash flows do we discount? 70391 Finance Fall 2016 Tepper School of Business Carnegie Mellon University c 2016 Chris Telmer. Some content from slides

MGT201 Current Online Solved 100 Quizzes By

MGT201 Current Online Solved 100 Quizzes By http://vustudents.ning.com Question # 1 Which if the following refers to capital budgeting? Investment in long-term liabilities Investment in fixed assets Investment

MGT201 Current Online Solved 100 Quizzes By http://vustudents.ning.com Question # 1 Which if the following refers to capital budgeting? Investment in long-term liabilities Investment in fixed assets Investment

Chapter 6 Making Capital Investment Decisions

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

The Use of Modern Capital Budgeting Techniques. Howard Lawrence

The Use of Modern Capital Budgeting Techniques. Howard Lawrence No decision places a company in more jeopardy than those decisions involving capital improvements. Often these investments can cost billions

The Use of Modern Capital Budgeting Techniques. Howard Lawrence No decision places a company in more jeopardy than those decisions involving capital improvements. Often these investments can cost billions

Finance 303 Financial Management Review Notes for Final. Chapters 11&12

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

WEEK 7 Investment Appraisal -1

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10. Risk and Refinements In Capital Budgeting

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10 Risk and Refinements In Capital Budgeting INSTRUCTOR S RESOURCES Overview Chapters 8 and 9 developed the major decision-making aspects

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10 Risk and Refinements In Capital Budgeting INSTRUCTOR S RESOURCES Overview Chapters 8 and 9 developed the major decision-making aspects

CHAPTER 2. How to Calculate Present Values

Chapter 02 - How to Calculate Present Values CHAPTER 2 How to Calculate Present Values The values shown in the solutions may be rounded for display purposes. However, the answers were derived using a spreadsheet

Chapter 02 - How to Calculate Present Values CHAPTER 2 How to Calculate Present Values The values shown in the solutions may be rounded for display purposes. However, the answers were derived using a spreadsheet

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

LO 1: Cash Flow. Cash Payback Technique. Equal Annual Cash Flows: Cost of Capital Investment / Net Annual Cash Flow = Cash Payback Period

Cash payback technique LO 1: Cash Flow Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the purchase of

Cash payback technique LO 1: Cash Flow Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the purchase of

Chapter 8. Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 8. Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 8. Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive

Future Value of Multiple Cash Flows

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Financial planning. Kirt C. Butler Department of Finance Broad College of Business Michigan State University February 3, 2015

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Chapter 10: Making Capital Investment Decisions. Faculty of Business Administration Lakehead University Spring 2003 May 21, 2003

Chapter 10: Making Capital Investment Decisions Faculty of Business Administration Lakehead University Spring 2003 May 21, 2003 Outline 10.1 Project Cash Flows: A First Look 10.2 Incremental Cash Flows

Chapter 10: Making Capital Investment Decisions Faculty of Business Administration Lakehead University Spring 2003 May 21, 2003 Outline 10.1 Project Cash Flows: A First Look 10.2 Incremental Cash Flows

FinQuiz Notes

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Monetary Economics Valuation: Cash Flows over Time. Gerald P. Dwyer Fall 2015

Monetary Economics Valuation: Cash Flows over Time Gerald P. Dwyer Fall 2015 WSJ Material to be Studied This lecture, Chapter 6, Valuation, in Cuthbertson and Nitzsche Next topic, Chapter 7, Cost of Capital,

Monetary Economics Valuation: Cash Flows over Time Gerald P. Dwyer Fall 2015 WSJ Material to be Studied This lecture, Chapter 6, Valuation, in Cuthbertson and Nitzsche Next topic, Chapter 7, Cost of Capital,

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 310 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 15 November, 2007 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 310 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 15 November, 2007 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Lecture Guide. Sample Pages Follow. for Timothy Gallagher s Financial Management 7e Principles and Practice

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

The formula for the net present value is: 1. NPV. 2. NPV = CF 0 + CF 1 (1+ r) n + CF 2 (1+ r) n

n + CF 2 (1+ r) n") Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Study Session 11 Corporate Finance

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

You will also see that the same calculations can enable you to calculate mortgage payments.

Financial maths 31 Financial maths 1. Introduction 1.1. Chapter overview What would you rather have, 1 today or 1 next week? Intuitively the answer is 1 today. Even without knowing it you are applying

Financial maths 31 Financial maths 1. Introduction 1.1. Chapter overview What would you rather have, 1 today or 1 next week? Intuitively the answer is 1 today. Even without knowing it you are applying

Copyright 2009, Jack Wheeler.

Unless otherwise noted, the content of this course material is licensed under a Creative Commons Attribution-Noncommercial-Share Alike 3.0 License. http://creativecommons.org/licenses/by-nc-sa/3.0/ Copyright

Unless otherwise noted, the content of this course material is licensed under a Creative Commons Attribution-Noncommercial-Share Alike 3.0 License. http://creativecommons.org/licenses/by-nc-sa/3.0/ Copyright

Analyzing Project Cash Flows. Principles Applied in This Chapter. Learning Objectives. Chapter 12. Principle 3: Cash Flows Are the Source of Value.

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Chapter 4 The Time Value of Money

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

2, , , , ,220.21

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Adv. Finance Weekly Meetings. Meeting 1 Year 15-16

Adv. Finance Weekly Meetings Meeting 1 Year 15-16 1 Weekly Meeting I Finance 2 Agenda Introduction What can you expect from the following meetings Four types of firms Ownership Liability Conflicts of Interest

Adv. Finance Weekly Meetings Meeting 1 Year 15-16 1 Weekly Meeting I Finance 2 Agenda Introduction What can you expect from the following meetings Four types of firms Ownership Liability Conflicts of Interest

FINANCE FOR EVERYONE SPREADSHEETS

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

Chapter 11: Capital Budgeting: Decision Criteria

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

Capital Budgeting Process and Techniques 93. Chapter 7: Capital Budgeting Process and Techniques

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

Session 2, Monday, April 3 rd (11:30-12:30)

") Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Chapter Organization. Net present value (NPV) is the difference between an investment s market value and its cost.

is the difference between an investment s market value and its cost.") Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Tools and Techniques for Economic/Financial Analysis of Projects

Lecture No 12 /13 PCM Tools and Techniques for Economic/Financial Analysis of Projects Project Evaluation: Alternative Methods Payback Period (PBP) Internal Rate of Return (IRR) Net Present Value (NPV)

Lecture No 12 /13 PCM Tools and Techniques for Economic/Financial Analysis of Projects Project Evaluation: Alternative Methods Payback Period (PBP) Internal Rate of Return (IRR) Net Present Value (NPV)

Software Economics. Metrics of Business Case Analysis Part 1

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

Breaking out G&A Costs into fixed and variable components: A simple example

230 Breaking out G&A Costs into fixed and variable components: A simple example Assume that you have a time series of revenues and G&A costs for a company. What percentage of the G&A cost is variable?

230 Breaking out G&A Costs into fixed and variable components: A simple example Assume that you have a time series of revenues and G&A costs for a company. What percentage of the G&A cost is variable?